Abstract

The 2008 global financial crisis highlighted the significant impact bank bailouts, state-owned enterprise recapitalizations, and other so-called contingent liability realizations can have on public finances. In this paper, we construct a novel dataset of contingent liability realizations in advanced and emerging market economies for the period 1990–2014. We find that when they materialize, contingent liabilities are a major source of fiscal distress. The average gross government payout related to a contingent liability realization is 6% of GDP, but gross payouts can be as high as 40% of GDP for major financial sector bailouts. Contingent liability realizations from different sources are correlated among each other and tend to occur during periods of weak growth and economic crisis, accentuating pressure on public finances during already difficult times. We find that they accounted for as much as one-third of the debt increases after the financial crisis. Indicative evidence suggests that countries with stronger governance indicators and, in particular, more comprehensive coverage of fiscal accounts, suffer more moderate contingent liability realizations. Improved oversight and transparency thus seems to go some way in reducing public financial risks.

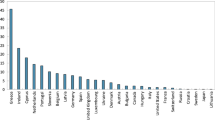

Source: Authors’ calculations based on dataset

Source: Authors’ calculations based on dataset

Source: Authors’ calculations based on dataset

Source: Authors’ calculations based on dataset

Source: Authors’ calculations based on dataset

Source: Authors’ calculations based on dataset

Source: Authors’ calculations based on Eurostat. GDP data from IMF World Economic Outlook

Source: Authors’ calculations based on Eurostat. GDP data from IMF World Economic Outlook

Source: Authors’ calculations based on dataset. Debt data from IMF World Economic Outlook. The regression line shows the fit of a binary regression of debt increases during the time of a CL realization on the identified gross fiscal impact of the CL realization

Source: Authors’ calculations based on dataset

Source: Authors’ calculations based on dataset and data from World Bank Worldwide Governance Indicators (WGI) Database, Transparency International (TI), International Budget Partnership (IBP) Open Budget Survey, and IMF Coverage of Fiscal Reporting (COFR) Database. Data on GDP per capita in US Dollars come from the World Economic Outlook (WEO) database of the IMF

Similar content being viewed by others

Notes

The dataset is available in Excel format on the journal Web site.

The direct impact is to be distinguished from indirect impact, where the former identifies direct government outlays or debt increases related to the shock, usually impacting the current deficit and debt, and the latter identifies the total change in public debt over time due to the shock and its impact on other macroeconomic variables.

The assumption of a debt liability of one entity by another entity, usually by mutual agreement (IMF 2003).

Indeed, Jaramillo et al. (2016) show using our dataset that CLs are a major driver of debt spikes that are unexplained by changes in nominal growth and overall deficit.

The literature often quantifies the fiscal impact using the term “fiscal cost,” while actually referring to gross government payouts (impact on government liabilities). When referring to our baseline gross measure we use the term gross payouts.

See Appendix A for a full list of countries.

The universe of CL materializations would likely include numerous small-scale episodes that are not documented. We exclude episodes with an impact below 0.2% of GDP for two reasons. First, data availability decreases the smaller the impact. By setting an explicit floor we limit the scope of the dataset but reduce measurement error. Second, since our goal is to capture “macrorelevant” CL realizations we need to define a cutoff for macrocriticality. The precise 0.2% of GDP cutoff is somewhat arbitrary but does not impact the overall picture. Nine episodes would be excluded if the threshold were increased to 0.3.

The database lists the exact sources used for each entry in the column “Sources.”

When no payout figure is available, we leave the column blank in the database. For natural disasters, besides reporting the government payout if available, we report an economic damage estimate for each episode in the additional information column, but this is not to be confused with the payout.

While many episodes entail payouts over several years, to present the data concisely in the stylized facts below, we report total payouts per episode unless otherwise specified.

We do not look at contingent asset realizations such as bandwidth auctions, nor at contingent “windfalls” in the form of debt write-offs, or unexpected revenue flows due to natural resource discovery. Thus, the distribution is truncated at 0 by construction.

One might be surprised by the relatively low number of PPP episodes. This is because individual PPP failures tend to create relatively small payouts, usually below our cutoff at 0.2% of GDP. Additionally, the number of PPPs has only recently started to increase significantly globally. We might thus expect more and larger CL payouts related to PPPs in the future. As indicated above, many costly legal CL realizations resulted from court decisions mandating compensation payments for domestic and foreign currency deposits frozen in Eastern Europe economies during the collapse of the Soviet Union.

The dataset spans 80 countries and 25 years, so a total of 2000 country–years. In 172 country–years a CL shock with identified payout over 0.2% of GDP occurred, which leads to an ex-post probability of 172/2000, or 8.6%.

The unweighted average is 47%. There is a strong positive relationship between the size of gross payouts and the ratio of net to gross payouts.

We exclude episodes in which the government made a small net fiscal gain from the analysis. The biggest gain was in Denmark with 0.6% of GDP.

See Appendix C for robustness checks—controlling for lagged oil price changes and fiscal aggregates, using a linear probability model instead of a logit specification, using the gross payouts rather than the occurrence of CLs as the dependent variable. We also use the 4-year moving average of growth rather than lagged growth as an explanatory variable and include natural disaster CLs in the regressions.

\( E\left( {\text{CL}} \right) = {\text{pr}}\left( {{\text{CL}}\;{\text{realization}}} \right) * {\text{payout}}({\text{CL}}|{\text{realization}}) \).

Assuming for simplicity that the government payouts (e.g., outlays and debt assumptions) related to CL realizations are debt creating.

The coverage of fiscal reporting (COFR) database provided by the Fiscal Affairs Department of the IMF presents data on the quality and transparency of fiscal reporting for 186 countries covering 2003–2013.

References

Acharya, V., Drechsler, I., & Schnabl, P. (2014). A pyrrhic victory? Bank bailouts and sovereign credit risk. The Journal of Finance, 69, 2689–2739.

Cebotari, A. (2008). Contingent liabilities: Issues and practice. IMF Working Paper 08/245. Washington: International Monetary Fund.

Cebotari, A., Davis, J., Lusinyan, L., Mati, A., Mauro, P., Petrie, M., & Velloso, R. (2009). Fiscal risks: Sources, disclosure and management. IMF Departmental Paper 9/01. Washington: International Monetary Fund.

Christofzik D., & Kessing, S. (2014). Does fiscal oversight matter? CESifo Working Paper No. 5023.

Cordes, T., Guerguil, M., Jaramillo, L., Moreno-Badia, M., & Ylaoutinen, S. (2014). Subnational fiscal crises, chapter 6. In C. Cottarelli (Eds.), Designing a european fiscal union: Lessons from the experience of fiscal federations. London: Routledge.

Crivelli, E., & Staal, K. (2013). Size, spillovers and soft budget constraints. International Tax and Public Finance, 20, 338–356.

Emergency Events Database (EM-DAT). (2015). International Disaster Database. Centre for Research on the Epidemiology of Disasters (CRED). Brussels: Université Catholique de Louvain. Available at http://www.emdat.be/database.

European Commission (Eurostat). (2015). Eurostat Supplementary Table for the Financial Crisis. Background Note (Brussels). Available at http://ec.europa.eu/eurostat/documents/1015035/2022710/Background-note-fin-crisis-OCT-2015-final.pdf.

Flanagan, M. (2008). Resolving a large contingent fiscal liability: Eastern european experiences. IMF Working Paper 08/159 Washington: International Monetary Fund.

Freeman, P., Keen, M., & Mani, M. (2003). Dealing with increased risk of natural disasters: Challenges and options. IMF Working Paper 03/197. Washington: International Monetary Fund.

Honohan, P., & Klingebiel, D. (2000). Controlling the fiscal costs of banking crises. World Bank Policy Research Working Paper 2441. Washington: World Bank.

International Monetary Fund (IMF). (2003). External debt statistics: Guide for compilers and users. Washington: Inter-Agency Task Force on Finance Statistics. http://www.imf.org/external/pubs/ft/eds/Eng/Guide/index.htm.

International Monetary Fund (IMF). (2012). Fiscal transparency, accountability and risk. IMF Policy Paper (Washington). Available at http://www.imf.org/external/np/pp/eng/2012/080712.pdf.

International Monetary Fund (IMF). (2014). Government finance statistics manual. Washington. https://www.imf.org/external/Pubs/FT/GFS/Manual/2014/gfsfinal.pdf.

International Monetary Fund (IMF). (2016). Analyzing and managing fiscal risks—Best practices. IMF Board Paper (Washington). Available at https://www.imf.org/external/np/pp/eng/2016/050416.pdf.

Jaramillo, L., Mulas-Granados, C., & Kimani E. (2016). The blind side of public debt spikes. IMF Working Paper 16/202 Washington: International Monetary Fund.

Kharas, H., & Mishra, D. (2000). Hidden deficits and contingent liabilities. Part 1 of the study “Opportunities and Risks in Central European Finances”, co-sponsored by the European Commission and the World Bank. Washington: World Bank.

Laeven, L., & Valencia, F. (2013). Systemic banking crises database. IMF Economic Review, 61, 225–270.

Landier, A., & Ueda, K. (2009). The economics of bank restructuring: Understanding the options. IMF Staff Position Note 09/12. Washington: International Monetary Fund.

Lucas, D. (2014). Evaluating the cost of government credit support: the OECD context. Economic Policy, 29(79), 553–597.

Polackova, H. (1998). Government contingent liabilities: A hidden risk to fiscal stability. Policy Research Working Paper 1989. Washington: World Bank.

Polackova-Brixi, H., & Schick, A. (2002). Government at risk: Contingent liabilities and fiscal risks. Washington: Co-publication of the World Bank and Oxford University Press.

Acknowledgements

We thank Jason Harris, participants of the IMF Fiscal Affairs Department seminar, and the two anonymous referees for very useful comments and suggestions. Younghun Kim provided excellent research assistance.

Author information

Authors and Affiliations

Corresponding author

Additional information

The views expressed in this article represent those of the authors and not necessarily those of the institutions to which they are affiliated. The study was done while Elva Bova and Marta Ruiz-Arranz were at the IMF.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Appendices

Appendix A: List of countries

Algeria, Angola, Argentina, Australia, Austria, Azerbaijan, Belarus, Belgium, Bosnia-Herzegovina, Brazil, Bulgaria, Canada, Chile, China, Colombia, Croatia, Cyprus, Czech Republic, Denmark, Dominican Republic, Ecuador, Egypt, Estonia, Finland, France, Germany, Greece, Hong Kong SAR, Hungary, Iceland, India, Indonesia, Iran, Ireland, Israel, Italy, Japan, Jordan, Kazakhstan, Korea, Kuwait, Latvia, Lithuania, Luxembourg, Macedonia, Malaysia, Malta, Mexico, Moldova, Morocco, the Netherlands, New Zealand, Norway, Oman, Pakistan, Peru, the Philippines, Poland, Portugal, Qatar, Romania, Russia, Saudi Arabia, Serbia, Singapore, Slovak Republic, Slovenia, South Africa, Spain, Sri Lanka, Sweden, Switzerland, Thailand, Turkey, Ukraine, United Arab Emirates, the UK, the USA, Uruguay, and Venezuela.

Appendix B: Data sources

CL realizations

A detailed list of all sources used is given in the database for each individual entry. Here we summarize the main data sources used in a consistent way for all CL realization.

-

IMF Staff Reports for all types of CL realizations and the whole period 1990–2014

-

Laeven and Valencia (2013), Eurostat (2015), Honohan and Klingebiel (2000) on financial sector CLs.

-

Cordes et al. (2014) on subnational government CLs.

-

Flanagan (2008) for legal CLs in Eastern Europe.

-

International Disasters Database (2015) on economic damage generated by natural disasters.

-

Cebotari et al. (2009) for information on various important episodes of CL realizations and associated fiscal costs.

-

Other country-specific sources are listed in the database whenever used.

GDP growth, output gap, inflation, exchange rate, debt, deficit, oil price:

-

All from IMF WEO database.

Systemic banking crises

-

Laeven and Valencia (2013)

Governance and transparency indicators

-

World Bank Worldwide Governance Indicators (WGI) Database

-

Transparency International (TI), Corruption Index

-

International Budget Partnership (IBP), Open Budget Survey

-

IMF Coverage of Fiscal Reporting (COFR) Database

Appendix C: Additional figures and regression tables

See Figs. 12 and 13 and Tables 9, 10, 11, 12, 13, and 14.

Source: Authors’ calculations based on dataset

Gross payouts for CL by year and type (in billions of USD).

Source: Authors’ calculations based on dataset and data from World Bank Worldwide Governance Indicators (WGI) Database, Transparency International (TI), International Budget Partnership (IBP) Open Budget Survey, and IMF Coverage of Fiscal Reporting (COFR) Database

The impact of governance and fiscal transparency on the expected annual gross payout for CL realizations—bivariate regressions. Notes: The figure shows the change in the average annual gross payout for CL realizations in percent of GDP in response to a 1 standard deviation increase in indicators of governance and fiscal transparency.

Rights and permissions

About this article

Cite this article

Bova, E., Ruiz-Arranz, M., Toscani, F.G. et al. The impact of contingent liability realizations on public finances. Int Tax Public Finance 26, 381–417 (2019). https://doi.org/10.1007/s10797-018-9496-1

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10797-018-9496-1