Abstract

Our experiment explores the impact of asymmetric incentives on collaboration within a context where participants can coordinate and potentially engage in deceptive practices to secure financial gains. We contrast two scenarios: one in which cooperation results in an equal distribution of gains, and another where the distribution is unequal. Our investigation focuses on the dynamics of collaborative behavior over time and digs into individual strategies employed by participants. We find that corruptive collaboration persists when its gains are unequally divided. Over time, participants acquire experience in collaborative tactics, often utilizing their reports to covert signals. Notably, participants coordinate around compromise distributions that yield smaller payments, suggesting that this context may actually reduce the perceived cost of dishonesty.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Profitable cheating frequently involves the collaboration of two parties. Consider bribery as an example: one party must initiate the proposal, while the other must accept it. Although economic literature has extensively explored both dishonesty and cooperation as distinct areas of study, there is a recent surge in research focused on examining dishonesty within cooperative contexts (for a review see Weisel and Shalvi 2022 and Leib et al. 2021). When subjects are required to cooperate with another person, dishonesty becomes more prevalent compared to situations where they act independently (Weisel and Shalvi 2015). The prospect of collaboration exerts a detrimental influence on honesty. This phenomenon of dishonest collaboration is observable in various experimental designs, encompassing situations where players make decisions jointly (Muehlheusser et al. 2015), sequentially (Weisel and Shalvi 2015), or simultaneously (Kocher et al. 2018). Over time, collaborative involvement in dishonest activities tends to increase, with the deceit of one partner showing a positive correlation with the deception of the other (Leib et al. 2021). In such collaborative settings, reciprocity and altruism emerge as two additional factors influencing (dis)honest behavior.

In this paper, we examine whether settings in which collaborative dishonesty yields unequal payoffs can effectively mitigate dishonest behavior. In contrast to existing literature, which explores scenarios where subjects evenly divide ill-gotten gains, our study delves into the dynamics of collaborative dishonesty concerning how the (unequal) allocation of cheating-derived rewards between collaborating parties impacts this behavior. Unequal incentives can represent a way to reduce dishonest collaboration, the collaboration that leads to negative consequences. Following the ancient saying “divide et impera” (divide and conquer) policymakers can use the payoff distribution to create a conflict of interest between the partners to reduce their dishonest collaboration.

Focusing on collaborations that involve deceptive reporting, such as collusion to manipulate environmental data (e.g., pollution levels) or the presentation of false information (e.g., inflating performance, expenses, or sales), and the subsequent negative consequences (e.g., false environmental data leading to inadequate response measures and diminished public health, or financial misreporting resulting in losses for the government, akin to cases involving price regulations or subsidies), policymakers and managers may consider implementing a strategy of uneven incentives linked to reporting. By altering how the profits associated with each specific report are distributed between the two parties involved, this approach can incentivize honesty. This shift encourages individuals to view honesty as a natural and cost-effective choice when deciding how to split the gains, thereby reducing the overall cost of dishonesty.

We experimentally investigate the effect of such a strategy by comparing a situation in which two subjects can collaborate on reporting (dishonestly or not) and receive the same payoff, to one where there is inequality in the payoff distribution. The two potential collusion partners are ‘divided’ by the asymmetry in the profit distributions. Such changes are implemented to promote honesty. When there is uncertainty about who will attain the greatest profit, reaching an agreement becomes less likely, given subjects’ aversion to unequal distributions that are perceived as unfair (Thaler 1988). In both treatments, partners are motivated to coordinate on a single report since, otherwise, neither would attain a positive payoff. Nevertheless, in one case, the report seeks to maximize profits for both partners, whereas in the other, each partner’s optimal outcome diverges. In this latter scenario, the partners engaged in collusion grapple with not only the ethical dilemma of choosing between honesty and deceit but also the complexity of opting for a first-best or second-best solution, potentially leading to no gains for either party.

We expect that with unequal payoffs, cheating will be reduced. Experimental findings on dishonesty showed that subjects face an intrinsic cost of lying: not all subjects engage in cheating, even in various studies where lies remained undetected and unpunished (Abeler et al. 2019). In addition, subjects prefer fair allocation of resources, and they are willing to forgo money to demonstrate their refusal to accept unfair distributions that disadvantage them (Thaler 1988). Thus, our hypothesis is that subjects will cheat less when this act produces an unequal profit distribution. However, while a “divide et impera” strategy might seem promising to reduce corrupt collaborations, its effectiveness is not assured, as the involved factors can interact in unpredictable ways, and individuals can change their behavior over time.

Our setting resembles common real-life situations. For instance, consider a scenario where a household collaborates with a construction company to qualify for a governmental renovation bonus. To secure the incentive, both parties must jointly declare the same scope of completed renovation work. If the incentive is intended to encompass renovations already completed or in progress, both parties have a shared motivation to present the highest level of work accomplished. However, if the incentive also extends to potential future renovation projects, the household might be motivated to accurately report current progress while retaining the opportunity for an additional incentive based on projected future renovations. This scenario introduces a decision point for the household, as it faces the choice between providing an accurate account of the actual renovation progress or strategically embellishing the reported work to maximize both immediate and future incentives.

Our findings revealed that while an unequal payoff distribution did not completely eradicate dishonest collaboration, it introduced fluctuations in stability, particularly during the initial phases. Remarkably, participants often sought a middle ground to sustain dishonesty while leveraging the asymmetric payoffs. Additionally, our study highlighted the use of reported numbers as signals for potential compromise distributions, adding an additional layer to the spectrum of dishonest behavior. The awakening of inequality aversion did not significantly alter the dynamics of dishonest collaboration, especially in a repeated setting. Subjects incurred lying costs to cooperate, even when the gain distribution was unequal. Interestingly, in the presence of unequal gains from cooperation, subjects did not merely mask their reluctance behind honesty; instead, they increasingly used their reports as signals for potential compromise distributions. Furthermore, collaboration within the scenario of unequal payoff distribution tended to expand as the number of remaining rounds decreased, indicating the presence of learning effects and emphasizing participants’ considerations for future interactions. In essence, our study reveals that when both parties have the potential to benefit from cheating, the inclination toward dishonest collaboration remains resilient, even in the face of asymmetric payoffs between the parties.

Our results contribute to the literature on collaborative dishonesty, which is crucial due to the observed tendency for individuals in groups to engage in higher levels of cheating compared to when they act individually (as in Conrads et al. 2013; Weisel and Shalvi 2015; Korbel 2017; Kocher et al. 2018; but not in Conrads et al. 2017). In the meta-study of Leib et al. (2021), they find that people lie noticeably in collaboration with partner(s), especially if their partners lie when the gains from lying are high and in later stages of interaction. Our paper explores the effect of introducing asymmetry in the payoff distribution on dishonest cooperation, building on existing evidence that unequal payoff distributions influence dishonest behavior (Gino and Pierce 2009) and that distributive preferences change when cheating is a source of inequality (Klimm 2019). Our study also contributes to the literature on coordination games, since it represents, to the best of our knowledge, the first to investigate dishonest cooperation when this leads to an unequal split of profits between the partners.

2 Experiment

In our Baseline treatment, subjects played the “dyadic die-rolling paradigm” (Weisel and Shalvi 2015). In the paradigm, Player A rolls the die and reports the outcome; Player B is informed about player A’s report, rolls the die, and reports the outcome. If Player A and B report the same number (i.e., a double), each participant earns points equal to the number reported multiplied by 20 (for instance, 120 points for a double six); zero otherwise. At the beginning of the experiment, we randomly paired subjects and assigned them the roles of Player A or B. Roles and pairs remain fixed during the entire 20 periods of the experiment. Die rolls are private and misreporting is possible. We inform each subject about their report, the counterpart’s report, and the payoff associated with the previous periods. We pay participants for one of the 20 periods, randomly selected at the end of the experiment. In Unequal Profits, we use an asymmetric payoff scheme, which aims to create a conflict between the economic interests of Player A and Player B. Table 1 summarizes payoffs for each combination of reports. Parametrization was made such that the maximum possible payoff and payment improvements were equal to the baseline. Players still have the incentive to report a double, but Player A prefers lower numbers, while Player B prefers high numbers. Contrary to the situation in Baseline, there is no reporting strategy for which the gains are split equally. This was made to exacerbate the conflict between the two players by not giving the possibility to share equally not even lower gains. This modification can dilute collaborative dishonesty by increasing the difficulty of coordination, decreasing the stakes, and awakening social concerns at the expense of profit maximization. It is also possible that the charm of cheating together goes beyond these difficulties.

The experiment took place at the experimental laboratory of Copenhagen University. It lasted 90 min, and we paid participants, on average, 162 DKK (including a show-up fee of 50 DKK and a fixed amount of 46 DKK). We recruited participants through ORSEE (Greiner 2004) and we programmed the software using z-Tree (Fischbacher 2007). At the beginning of the experiment, we randomly allocated participants to cubicles, and we asked them to read a set of instructions (see the Online Appendix). Participants had to correctly answer specific control questions that test their understanding of the rules of the gameFootnote 1. Our final dataset comprises of 1920 decisions from 96 subjects (52.7% female; mean age 26 years old), 50 are assigned to the Baseline condition and 46 to the Unequal Profits condition.

3 Results

Looking at individual behavior, in Baseline, we have strong evidence of dishonesty for Player A (average report 5.06, st. dev. 1.44, p < 0.001) and Player B (average report 4.49, st. dev. 1.69, p < 0.001). Both report distributions are skewed towards higher numbers, for which both players have higher profits. In contrast, we do not observe a strong asymmetry in the distribution of reports in Unequal Profits for Player B (average report 3.55, st. dev. 1.66, p = 0.5) and Player A (average report 3.07, st. dev. 1.57, p < 0.001)Footnote 2, as high reports here give the maximum profits to B but the minimum to A.

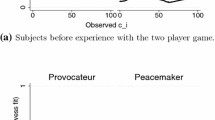

Figure 1 depicts the distribution of reports for Player A (vertical), Player B (horizontal), and joint distribution (core) in our two conditions, Baseline (panel a) and Unequal Profits (panel b). Looking at the joint behavior, we observe similar levels of dishonesty. The difference in the percentage of doubles reported in Baseline compared to Unequal Profits is not different statistically (56% vs. 50%, p = 0.575Footnote 3). While in Baseline the distribution of individual reports of players A and B is concentrated on “six-six”, in Unequal Profits individual distributions are concentrated on the diagonal. In both treatments, a double is reported more often than predicted (16,67% of the times). Even if reaching an agreement on the number to report is harder in Unequal Profits than in Baseline, the number of times it happens is not dissimilar between treatments and higher than expected. The unequal distribution of gains does not prevent dishonest collaboration to happen, instead, we can think it makes it stronger: subjects do cheat even for a smaller profit.

The expected profit in the two treatments is the same, corresponding to 11,67 points for each playerFootnote 4. In the Baseline, both players earn on average 60 points, way more than expected. With Unequal Profits, players anyway earn similar amounts higher than expected but lower than Baseline (Player A 36 and Player B 34). This indicates that, even if the unequal Profit cannot stop dishonesty, at least it reduces the illicit profits.

Distribution of reports in Baseline and in Unequal Profits. Distribution of reports for Player A (vertical), Player B (horizontal) and joint distribution (core) in the Baseline (on the left) and in Conflict of Interest (on the right)

Figure 2 shows the reports of Player A (green triangle) and Player B (red cross), which range from 1 to 6 on the vertical axes, in each of the 20 periods they played together on the horizontal axes. Each subgraph represents the behavior of a pair of players. Subgraphs are ordered by the number of doubles reported in the 20 periods (indicated in the title), from the lowest to the highest. The left panel reports the pairs belonging to the Baseline treatment and the right one reports the ones belonging to the Unequal Profits treatment (right). In Baseline, we observe many cases of dishonest collaboration at the maximum level (where the player’s reports match almost always) and many cases where player A is dishonest (always reports the most profitable report), but player B does not collaborate. In Unequal Profits, the modal pattern is a dishonest collaboration at a medium level. It often takes a while (some periods with different reports) to start dishonest collaboration. We observe fewer cases where Player B unconditionally matches the number reported by A (4% vs. 28%, p = 0.029) and fewer (no) Player As who always report the amount that maximizes their payoffs (0 vs. 32%, p = 0.003), and there is also no Player As who always report the numbers that would minimize the differences in payoffs. Given the higher difficulty in coordinating, Player B in Unequal Profits must be more proactive in suggesting a possible compromise and, therefore, has a more important role in establishing collaborative dishonesty. The role of Player B in the practice is now more complex, s/he has not only to choose to lie or tell the truth but can use the report strategically, as a signal for the number to compromise and to refuse unfair offers. For player B reporting more than 3 consecutive times a number that is not a match is twice more frequent in Unequal Profits than in Baseline (30% vs. 16%). Overall, while in Baseline dishonesty is concentrated in some pairs that coordinate all the time, in Unequal Profits is spread among many pairs. Overall, the pairs’ behavior indicates that subjects more often act dishonestly to give signals for future collaboration instead of hiding behind honesty to kindly decline unfair offers.

Players’ behavior by pair – Baseline and Unequal Profits. Distribution of the number reported (1 to 6, vertical axes) over the periods (1 to 20, horizontal axes) from Player A of each of the Pairs in Baseline (left) and Unequal Profits (right). Pairs in each condition are ordered by the total number of doubles reported, from lower to higher, indicated as the subgraph title.

Finally, results indicate that time plays an important role in shaping collaborative dishonesty in the presence of unequal payoffs: the percentage of doubles reported is lower in Unequal Profits than in Baseline during the first ten periods (56% vs. 44%, p < 0.01), but there is no difference in the last ten (56% vs. 56%, p = 0.87)Footnote 5. “Divide et impera” can be a successful strategy to reduce collaborative dishonesty in one-shot situations, but with time and experience, subjects find out how to deceive the problem. Also, as the number of future interactions diminishes, more unequal distributions can be accepted as reputation counts less. Figure 3 shows the percentage of doubles in each period and the linear approximation in our two conditions.

Frequency of doubles over the periods, distribution, and linear fit. Distribution of doubles over time in the two treatments (white diamonds for Baseline, black triangles for Unequal Profits) and linear fit (dashed black line for Baseline, solid grey line for Unequal Profits)

While dishonest collaboration in Baseline is almost constant, in Conflict of Interest it is lower in the first periods, but it increases, and over time it reaches Baseline’s level. The correlation of the percentage of doubles with the period is 0.14 (p = 0.001) in Baseline and 0.51 in Conflict (p < 0.001). Using a regression (Random Effect Logit with standard errors clustered for pairs) of a dummy indicating a double over the period (from 1 to 20), we find that the likelihood of observing a double increases over time in Conflict (b = 0.047, p = 0.032) but not in Baseline (b = 0.016, p = 0.358). Note that the observed time trend exists even if subjects know that they will be paid only for one randomly chosen decision.

Regression analysis confirms our findings. The reporting of a double increases over time in Unequal Profits (b = 0.03, p = 0.023). Table 2 reports the regression results from Random Effect Individual Probit of an indicator of when players report a double for Players B in two specifications. As independent variables a dummy indicating whether there was a double in the previous period, the difference between the report of Player B (Player A) in the previous period.

4 Conclusion

In this paper, we delve into the question of whether an unequal payoff distribution could mitigate dishonesty within cooperative settings, exploring the applicability of the ancient adage “divide et impera.” Extending the paradigm of Weisel and Shalvi (2015), our study investigates how participants’ behaviors evolve within an environment featuring unequal payoffs. Our findings reveal that while an unequal payoff distribution does not eliminate dishonest collaboration, it introduces fluctuations in stability, particularly during the initial phases. Notably, subjects often seek a middle ground to sustain dishonesty while capitalizing on asymmetric payoffs. Additionally, our study highlights the use of reported numbers as signals for possible compromise distributions, adding an extra layer of complexity to dishonest behavior.

Interestingly, awakening inequality aversion does not significantly decrease dishonest collaboration, especially in a repeated setting. Subjects incur lying costs to cooperate even if the gain split is unequal. Interestingly, in the presence of unequal gains from cooperation, subjects do not merely conceal their reluctance behind honesty; instead, they increasingly use their reports as signals for potential compromise distributions. Furthermore, cooperation within the unequal payoff distribution scenario tends to grow as the number of remaining rounds diminishes, indicating the presence of learning effects and underscoring participants’ considerations for future interactions. In essence, our study reveals that when both parties stand to gain from cheating, the inclination toward dishonest collaboration remains resistant to asymmetric payoffs between the parties.

As a controlled lab experiment, our findings reflect the dynamics within that setting, and generalizing them to real-world scenarios requires caution. The unequal payoff structure we used, designed to evoke concerns related to inequality aversion, may influence behavior differently than other methods. Furthermore, while our study provides insights into the internal dynamics of decision-making, the extent to which our results can be generalized beyond the lab setting requires validation through field studies. Yet, this research serves as a starting point for understanding complex decision-making processes and exploring intervention efficacy. Our work initiates a dialogue about the interplay of unequal payoff distributions, dark cooperative behavior, and policy mechanisms, paving the way for future research to refine interventions and enhance our understanding of honest decision-making.

Our findings carry policy significance, especially in contexts where governments strive to incentivize certain behaviors, such as addressing environmental challenges or climate change. In these contexts, there might be a risk of unintended consequences, including the potential for collusive behaviors that exploit these incentives for personal gain. The insights garnered from our study underscore the intricate nature of dishonest collaboration and highlight the limitations of relying solely on unequal payoff distributions to curb such behavior. While instruments like unequal payoff distributions can play a role, they must be complemented with measures that foster transparency, accountability, and adherence to ethical norms.

Notes

Participants also performed the Bomb Risk Elicitation Task (BRET, Crosetto and Filippin 2013) and the Personality Traits questionnaire (Ashton and Lee 2009) to be used as controls as dishonesty has been found to correlate with both risk preferences (Becker 1968) and personality (Moshagen et al. 2018; Hilbig et al. 2018).

P-values from one-sample t tests.

Where not else stated, from now on, p-values refer to Two-sample Wilcoxon rank-sum (Mann-Whitney) tests for averages within each pair.

Calculated as 1/6*(1/6*20*1/6*40 + 1/6*60 + 1/6*80 + 1/6*100 + 1/6 + 120).

The result is robust to using other cut points, like 5 or 15.

References

Abeler J, Nosenzo D, Raymond C (2019) Preferences for truth-telling. Econometrica 87(4):1115–1153

Ashton MC, Lee K (2009) The HEXACO-60: a short measure of the major dimensions of personality. J Personal Assess 91(4):340–345

Becker GS (1968) Crime and punishment: an economic approach. J Polit Econ 76(2):169–217

Crosetto P, Filippin A (2013) The “bomb” risk elicitation task. J Risk Uncertainty 47:31–65

Conrads J, Irlenbusch B, Rilke RM, Walkowitz G (2013) Lying and team incentives. J Econ Psychol 34:1–7

Conrads J, Ellenberger M, Irlenbusch B, Ohms EN, Rilke RM, Walkowitz G (2017) Team goal incentives and individual lying behavior. WHU-Otto Beisheim School of Management. 2017, No. WP 17/02

Fischbacher U (2007) z-Tree: Zurich toolbox for ready-made economic experiments. Exp Econ 10(2):171–178

Gino F, Pierce L (2009) The abundance effect: unethical behavior in the presence of wealth. Organ Behav Hum Decis Process 109(2):142–155

Greiner B (2004) An online recruitment system for economic experiments. MPRA Paper No. 13513

Hilbig BE, Kieslich PJ, Henninger F, Thielmann I, Zettler I, Back M (2018) Lead us (not) into temptation: testing the motivational mechanisms linking honesty–humility to cooperation. Eur J Pers 32(2):116–127

Klimm F (2019) Suspicious success–Cheating, inequality acceptance, and political preferences. Eur Econ Rev 117:36–55

Kocher MG, Schudy S, Spantig L (2018) I lie? We lie! Why? Experimental evidence on a dishonesty shift in groups. Manage Sci 64(9):3995–4008

Korbel V (2017) Do we lie in groups? An experimental evidence. Appl Econ Lett 24(15):1107–1111

Leib M, Köbis N, Soraperra I, Weisel O, Shalvi S (2021) Collaborative dishonesty: a meta-analytic review. Psychol Bull 147(12):1241

Moshagen M, Hilbig BE, Zettler I (2018) The dark core of personality. Psychol Rev 125(5):656

Muehlheusser G, Roider A, Wallmeier N (2015) Gender differences in honesty: groups versus individuals. Econ Lett 128:25–29

Thaler RH (1988) Anomalies: the ultimatum game. J Economic Perspect 2(4):195–206

Weisel O, Shalvi S (2015) The collaborative roots of corruption. Proc Natl Acad Sci 112(34):10651–10656

Weisel O, Shalvi S (2022) Moral currencies: explaining corrupt collaboration. Curr Opin Psychol 44:270–274

Acknowledgements

The views expressed are purely those of the authors and may not in any circumstances be regarded as stating an official position of the European Commission. The activities of CEBI are financed by the Danish National Research Foundation, Grant DNRF134. We are grateful to the many colleagues and student assistants who have helped us in planning and running this experiment.

Funding

Open access funding provided by Università degli Studi di Genova within the CRUI-CARE Agreement.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

None.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Braut, B., Valle, N.D. & Piovesan, M. Collaborative Dishonesty with Unequal Profits - an Experimental Investigation. Group Decis Negot 33, 147–157 (2024). https://doi.org/10.1007/s10726-023-09857-7

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10726-023-09857-7