Abstract

This paper identifies a contemporaneous substitutional relationship between retail deposits and wholesale funds, while the lagged relationship between the two is rather weak-a finding consistent with our “stable capitalization hypothesis.” We find that this substitution effect is much more pronounced for banks facing retail deposit inflows compared to those facing outflows, suggesting that influxes of deposits allow banks to cut wholesale funding more aggressively to maintain their capital structures. This substitution effect is also negatively associated with wholesale funding maturity and riskiness. Furthermore, we show that the substitutional relationship is weaker during funding shocks such as the 2007-2009 financial crisis and that the substitution itself does not help banks maintain their lending, which supports the argument for a lender of last resort. Finally, we demonstrate that liquidity regulation curbs this substitution, which overall helps banks improve financial stability.

Similar content being viewed by others

Data Availability

This research is based on publicly available data, including FR Y-9C reports, Summary of Deposits, and Quarterly Banking Profile from the FDIC. Researchers can access these data sources on the websites of institutions such as the Federal Reserve and FDIC.

Notes

Wholesale funding sources primarily consist of short-term funds or deposits provided by foreign institutions, nonfinancial firms, non-depository financial institutions and state or local municipalities.

We leave the discussion of sample period in detail to Section 4.

We leave the detailed theoretical discussion in the hypothesis development section.

In this analysis, we utilize a more comprehensive liquidity ratio that incorporates Treasury and agency debt: broader liquidity ratio. Variable construction details are shown in Table A1.

Although our bank-level panel regression analysis partially mitigates the omitted variable bias concern that exists in the time-series analysis at the aggregate level, there are still endogeneity concerns that need to be addressed. On one hand, although we control for lending growth in our model specifications, loan demand or lending opportunities may still affect the growth of retail deposits and wholesale funds simultaneously because they jointly shape the bank lending process. On the other hand, characteristics of the suppliers of wholesale funding (i.e., wholesale funding investors) may confound this substitution effect between the two funding sources because they may or may not be informationally sensitive to curbing their funding supplies to banks (Perignon et al. 2018).

In terms of transparency, we rely on the public status of BHCs in the sample as prior literature indicates that public banks are more transparent than private ones. We leave the discussion of this in detail to Section 5.10.2.

Wholesale funds are heterogeneous as they vary by riskiness and maturity. In this paper, we categorize them into time deposits of $100,000 or more, foreign deposits, subordinated notes and debentures, Federal funds purchased and securities sold under agreements to repurchase, and other borrowed money.

A counterargument to this logic is that the effective maturities of retail deposits are similar to CDs given depositor behavior; however, CDs are relatively less liquid than short-term funding sources such as Federal funds so our expectation holds.

The data can be retrieved from the FDIC’s website: https://www.fdic.gov/bank/analytical/qbp/.

FR Y-9C report data source: https://www.chicagofed.org/applications/bhc/bhc-home.

Table A1 provides detailed descriptions of the aggregate time-series variables, bank-level characteristics and other relevant micro variables that are used in this study.

According to Acharya and Mora (2015), wholesale funds are the sum of large time deposits, deposits held by foreign institutions, subordinated debt and debentures, gross Federal funds purchased, repos and other borrowed money. Choi and Choi (2021) define wholesale funds as the sum of wholesale deposits, Federal funds and repos, and other borrowed money. Lin (2020) defines wholesale funds as the sum of brokered deposits, foreign institutions’ deposits, other borrowed money and Federal funds purchased.

Branch offices and their corresponding parent BHCs are linked based on the variable, “rssdhcr”, in the Summary of Deposits database.

We also plot the figures by quarter. The unreported results show that in the years after 2012, we notice a mechanical relationship between the growth rates of retail deposits and wholesale funds. In the second quarter of each year, the median and average growth rates of wholesale funds increase to levels higher than those of retail deposits while, at the same time, the growth rates of retail deposits sharply decrease.

We also employ a broader definition of wholesale funds that includes brokered deposits and these results are found in Table A2. Nonetheless, the results indicate that our bank-level findings remain unchanged.

Beginning in 2017, the FR Y-9C report increased the cutoff amount from $100,000 to $250,000 on time deposits. Because of this inconsistency in the financial report, we choose to shorten the sample period to end in 2016. However, the actual deposit amounts between $100,000 and $250,000 are likely not significant. In order to verify, we conduct an additional analysis using the cutoff of $100,000 for the data before 2017 and $250,000 for the data after 2016. The corresponding items for these two cutoffs are BHCB2604 (total time deposits of $100,000 or more) and BHCBJ474 (time deposits of more than $250,000). By combining these two cutoffs in two separate periods in the sample, we can create a comprehensive sample that extends to the first quarter of 2020 right before the start of the global outbreak of COVID-19. Hence, we conduct a corresponding analysis for our bank-level baseline regressions as a robustness check. Nevertheless, our results remain unchanged and are displayed in Table A8.

As the substitution effect could be directional for both retail deposits and wholesale funds, we also use a seemingly unrelated regression model to test the dynamics in these directions. The untabulated results show that our main finding here continues to hold.

We interpret and display the results of Table 5 according to the order in Hypothesis 2.

However, subordinated notes and debentures are relatively easy to issue compared to other types of wholesale funding, which may influence this result.

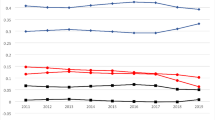

These subfigures plot the wholesale funds ratios of large and small banks from 2002 to 2016. Figure 4a and b display the mean and median ratios, respectively, of banks using a $10 billion threshold to classify bank size. Figure 4c and d display the mean and median ratios, respectively, of banks using a $50 billion threshold to classify bank size. Moreover, Fig. 4e through h plot the retail deposits ratios for large and small banks, which exhibit opposite patterns compared to the corresponding figures with wholesale funds ratios.

For details regarding U.S. stress tests, see this link: https://www.fdic.gov/regulations/laws/rules/5000-5360.html#:~:text=Under%20the%20Stress%20Test%20Rule%2C%20each%20covered%20bank%20is%20required,all%20categories%20of%20financial%20data.

An anonymous reviewer expressed concerns that we gave more weight to smaller banks in early years when creating a constant sample. Thus, as a robustness check, the reviewer suggested that we adopt the strictest reporting size threshold adjusted by inflation, which is a reasonable alternative approach. To that end, we use the threshold of $3 billion that was effective in 2018 and adjust this backwards by inflation throughout our sample for periods prior to 2018 using the series “inflation, consumer prices for the United States” obtained from the Federal Reserve Bank of St. Louis. We then reconduct most of the bank-level baseline regressions that are found in Tables 3 through 6. Using this threshold considerably reduces the sample observations to fewer than 10,000. Nonetheless, the modified regression results remain unchanged by adopting this alternative approach except in Panel B of Table 4, where we investigate the asymmetry of the substitutional relationship between retail deposits and wholesale funds by using subsamples of only negative or positive retail deposits growth. We attribute this inconsistency to small samples as this approach further significantly decreases observations. All results from this alternative approach are displayed in Tables A4 through A7, accordingly.

To make this figure more intuitive, we take the absolute values of these coefficients over the sample period when we draw the figure.

Due to valid economic reasons, banks might not want to maintain current levels of lending during a financial crisis. However, our results show that banks with stronger active management of wholesale funds for retail deposits were not better suppliers of loans during this funding shock.

On the other hand, all else being equal, a bank’s access to wholesale funding markets is a crucial component of its business and without such access a bank would be considered very risky. In theory, banks should seek to strike a balance between retail deposits and wholesale funds without overrelying on the latter.

These interaction terms are broader liquidity ratio and high liquidity dummy which identifies banks with broader liquidity ratios higher than the median.

While this approach mitigates this confounding effect, it is impossible to consider all of the factors that may affect a bank’s decision to lend as the lending decision is influenced by many factors including the availability of retail funds and economic conditions. These factors may, in turn, affect a bank’s reliance on wholesale funding and thus the substitution effect.

This variable, high DMP dummy, is coded as 1 if the bank-level HHI is above the median bank HHI in the total sample and as 0 otherwise.

We utilize a dummy variable because public banks are subject to more rigorous regulations and are relatively more transparent than private ones in financial disclosure.

Public companies typically have better financial disclosure quality and are more transparent than private ones.

Overall, our study is not without limitations as the dynamics between retail deposit and wholesale fund flows are quite complex and not truly exogenous. The factors driving shifts in retail deposits influence the wholesale funding markets and vice versa. Furthermore, changes in banks’ lending opportunities due to market conditions further complicate the relationship.

References

Acharya VV, Mora N (2015) A crisis of banks as liquidity providers. J Financ 70(1):1–43

Allen F, Babus A, Carletti E (2012) Asset commonality, debt maturity and systemic risk. J Financ Econ 104(3):519–534

Bai G, Elyasiani E (2013) Bank stability and managerial compensation. J Bank Financ 37(3):799–813

Banerjee RN, Mio H (2018) The impact of liquidity regulation on banks. J Financ Intermediation 35:30–44

Berger A, Bouwman C (2013) How does capital affect bank performance during financial crises? J Financ Econ 109(1):146–176

Berger A, El Ghoul S, Guedhami O, Roman R (2017) Internationalization and bank risk. Manage Sci 63(7):2283–2301

Bernanke BS (2007) The financial accelerator and the credit channel. Board of Governors of the Federal Reserve System (U.S.)

Bernanke BS, Gertler M, Gilchrist S (1999) The financial accelerator in a quantitative business cycle framework. Handbook of Macroeconomics 1:1341–1393

Bonner C, van Lelyveld I, Zymek R (2015) Banks’ liquidity buffers and the role of liquidity regulation. J Financ Serv Res 48(3):215–234

Bordo MD (1990) The lender of last resort: Alternative views and historical experience. FRB Richmond Econ Rev 76(1):18–29

Bruno B, Onali E, Schaeck K (2018) Market reaction to bank liquidity regulation. J Financ Quant Anal 53(2):899–935

Buchak G, Hu J, Wei SJ (2021) FinTech as a financial liberator. (No. w29448). National Bureau of Economic Research

Buser S, Chen A, Kane E (1981) Federal deposit insurance, regulatory policy, and optimal bank capital. J Financ 36(1):51–60

Caballero RJ, Hoshi T, Kashyap AK (2008) Zombie lending and depressed restructuring in Japan. Am Econ Rev 98(5):1943–77

Chen Q, Goldstein I, Huang Z, Vashishtha R (2022) Bank transparency and deposit flows. J Financ Econ 146(2):475–501

Choi DB, Choi HS (2021) The effect of monetary policy on bank wholesale funding. Manage Sci 67(1):388–416

Chu Y, Deng S, Xia C (2020) Bank geographic diversification and systemic risk. Rev Financ Stud 33(10):4811–4838

Demirguç-Kunt A, Huizinga H (2010) Bank activity and funding strategies: The impact on risk and returns. J Financ Econ 3(98):626–650

Diamond D (1991) Debt maturity structure and liquidity risk. Q J Econ 106(3):709–737

Diamond D, Dybvig P (1983) Bank runs, deposit insurance, and liquidity. J Pol Econ 91(3):401–419

Diamond D, Rajan R (2000) A theory of bank capital. J Financ 55(6):2431–2465

Drechsler I, Drechsel T, Marques-Ibanez D, Schnabl P (2016) Who borrows from the lender of last resort? J Financ 71(5):1933–1974

Drechsler I, Saviv A, Schnabl P (2017) The deposit channel of monetary policy. Q J Econ 132(4):1819–1876

Eichengreen B, Portes R (1987) The anatomy of financial crises. (No. w2126). National Bureau of Economic Research

Fang Y, Hasan I, Marton K (2014) Institutional development and bank stability: Evidence from transition countries. J Bank Financ 39:160–176

Gatev E, Strahan PE (2006) Banks’ advantage in hedging liquidity risk: Theory and evidence from the commercial paper market. J Financ 61(2):867–892

Goldsmith-Pinkham P, Yorulmazer T (2010) Liquidity, bank runs, and bailouts: spillover effects during the Northern Rock episode. J Financ Servic Res 37(2):83–98

Goodhart C, Schoenmaker D (1995) Should the functions of monetary policy and banking supervision be separated? Oxford Economic Papers, pp 539–560

Hoerova M, Mendicino C, Nikolov K, Schepens G, Van den Huevel S (2018) Benefits and costs of liquidity regulation

Houston J, Lin C, Lin P, Ma Y (2010) Creditor rights, information sharing, and bank risk taking. J Financ Econ 96(3):485–512

Huang R, Ratnovski L (2011) The dark side of bank wholesale funding. J Financ Intermed 20(2):248–263

Iyer R, Peydro JL, da Rocha-Lopes S, Schoar A (2014) Interbank liquidity crunch and the firm credit crunch: Evidence from the 2007–2009 crisis. Rev Financ Stud 27(1):347–372

Kiyotaki N, Moore J (1997) Credit cycles. J Pol Econ 105(2):211–248

Kladakis G, Chen L, Bellos SK (2020) Wholesale funding, liquidity creation and deposit shortage. Working paper

Levine R, Lin C, Tai M, Xie W (2021) How did depositors respond to COVID-19? Rev Financ Stud 34(11):5438–5473

Li Y (forthcoming) Reciprocal lending relationships in shadow banking. J Financ Econ

Li W, Ma Y, Zhao Y (2019) The passthrough of treasury supply to bank deposit funding. Columbia Business School Research Paper, USC Marshall School of Business Research Paper

Lin L (2020) Bank deposits and the stock market. Rev Financ Stud 33(6):2622–2658

Martin C, Puri M, Ufier A (2018) Deposit inflows and outflows in failing banks: The role of deposit insurance. (No. w24589). National Bureau of Economic Research

Miron JA (1986) Financial panics, the seasonality of the nominal interest rate, and the founding of the Fed. Am Econ Rev 76(1):125–140

Myers S, Majluf N (1984) Corporate financing and investment decisions when firms have information that investors do not have. J Financ Econ 13(2):187–221

Perignon C, Thesmar D, Vuillemey G (2018) Wholesale funding dry-ups. J Financ 73(2):575–617

Roberts D, Sarkar A, Shachar O (2018) Bank liquidity creation, systemic risk, and basel liquidity regulations. FRB of New York Staff Report, pp 852

Shin HS (2009) Reflections on Northern Rock: The bank run that heralded the global financial crisis. J Econ Perspect 23(1):101–19

Tripathy N, Wu D, Zheng Y (2021) Dividends and financial health: Evidence from US bank holding companies. J Corp Fin 66:101808

Xiao K (2020) Monetary transmission through shadow banks. Rev Financ Stud 33(6):2379–2420

Zheng Y (2020) Does bank opacity affect lending? J Bank Financ 119:105900

Acknowledgements

We are thankful to Haluk Unal (the editor) and two anonymous reviewers for their constructive comments. We are also grateful for helpful comments from Anna Agapova (discussant), Kevin Caskey, James Forest, Shuguang Liu, Yen Nguyen (discussant), Daniel Shen, Chih-Yang Tsai, Alex Ufier, Yuan Wen, as well as seminar and conference participants at the Eastern Finance Association Annual Meeting, Financial Management Association Annual Meeting, and SUNY New Paltz. All remaining errors are our own.

Funding

The authors did not receive financial support from any organization for the submitted work.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflicts of interest

The authors have no relevant financial or non-financial interests to disclose.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Zheng, Y., Peabody, S.D. Bank Funding Dynamics Between Retail Deposits and Wholesale Funds: Implications for Regulations. J Financ Serv Res (2024). https://doi.org/10.1007/s10693-024-00423-z

Received:

Revised:

Accepted:

Published:

DOI: https://doi.org/10.1007/s10693-024-00423-z