Abstract

Increasing global concern about climate change and the circular economy have successfully established itselves in international and national policies over the last decade, with the aim of reshaping the production and consumer behavior. The circular economy is one of the core pillars of European Union policy and its success depends on the energy efficiency, reducing production costs, and maintaining employment levels by ensuring continuous strong economic independency of the region. While crises are unavoidable and continue to appear, this paper aims to project the impact of any crisis on sustainability transitions using data analysis of the Global Financial crisis from 2008 to 2009 and discuss how the success of the circular economy implementation and environmental policies could be affected. The paper notes that the global financial crisis of 2008–2009 had a short-term positive impact on environmental degradation and that economic interests overshadowed environmental goals. Due to the recent events of the ongoing Russia and Ukraine war, COVID-19 societal and industrial behavior has shifted from sustainable to linear and has taken a step backward in reducing environmental pollution and achieving Sustainable Development Goals. Analysis of already present data and the context of the 2008–2009 global financial crisis, reviewing of COVID-19 impact on the global economy, health sector, and environmental policies allows us to predict the consequences, as it relates to the future of circular economy policy.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Since the Industrial Revolution, humankind itself has become a geological force leading to a human-induced climate change caused by the burning of fossil fuels for energy use and industrial purposes, mass extinction of species due to rapid urbanization and unsustainable agricultural activities, rising sea levels, and global plastic pollution (de Wit et al., 2018). As a result, we are living above ecosystems’ boundaries causing an ecological overshoot (Rockström et al., 2009) and it is happening even faster than countries are able to achieve social thresholds (Fanning et al., 2021). Industrial activities over the past 200 years have led to a global environmental crisis that requires urgent actions ensuring environmental and economic stability for future generations. Increased number of international activities pursuing circular economy and sustainability is taking a place aiming to maintain and significantly reduce the impact to the environment.

The sustainability principles are core position of the European Union’s (EU) circular economy policy incorporated in the Green Deal package (European Commission, 2020). The concept of circular economy (CE) has an ambitious plan to transform production and consumption processes by replacing the linear economy with circular alternatives and reducing the consumption of primary resources, waste and emissions output by closing the loop of economic activities (Haas et al., 2015; Haupt et al., 2017; Korhonen et al., 2018; Peters et al., 2007). The last decade marked a drastic and successful rise of the CE concept at the international and national levels (Besenbacher, 2015; Fitch-Roy et al., 2021), which provided CE the role of modernizing the industrial sector and solving the rising economic and environmental challenges (Calisto Friant et al., 2021). Addressing those challenges, the Green Deal strategy sets a goal to transform the EU into a modern resource-efficient and competitive economy with no net emissions of greenhouse gas by 2050 (European Commission, 2020). The implementation of this goal is complicated because of relationship between economy, ecosystems and earth systems tackling climate change and ensuring economic growth at the same time (Dolge & Blumberga, 2021).

Economic growth with increased production and consumption activities is desirable for its positive social and economic impact to the societies and states (Alam & Kabir, 2013). The economic transformation from unsustainable to more sustainable and circular ones can be difficult because it requires radical and systematic political and economic changes in the context of existing social and ecological structures and processes in society, which have to be overcome in the transition process (Olsson et al., 2014). The economic development and industrial activities in the most developed countries are based on natural resource extraction, which decreases resource efficiency and environment damage (Scheel et al., 2020). The EU’s circular economy and the new Green Deal policy are based on economic growth by boosting sustainable development, green technologies, transport with significant emission reduction (Klemeš et al., 2020). As a result, it could be the key in solving the climate change problem. However, Calisto Friant et al. (2021) finds that the EU chose an optimistic CE approach, which was based on technological growth and innovation, but transformative changes exclude the reduction of overall material consumption. Some studies on economic decoupling also confirm that it is impossible to achieve the reduction of the material footprint, and increase Gross Domestic Product (GDP) per capita at the same time (Albert, 2020; Apeaning, 2021; Haberl et al., 2020), simply because there is a strong correlation between energy consumption and economic growth (Akram, 2013). Thereby some studies confirm environmental problems escalation as economic growth increase (Dolge & Blumberga, 2021; D. Wang et al., 2019). Furthermore, the CE implementation goals described in international and national regulations have fallen short of the expected current levels of implementation in terms of energy recovery, circular economy and environmental improvement. All assumptions and research findings had been confirmed in the UN Emission Gap report (UNEPT, 2019) with a conclusion that countries have never managed to stop the growth of greenhouse gas emissions with an annual increase of 1.5% in the last decade.

While the global coronavirus pandemic favorably contributed to climate change mitigation by leading to an unprecedented 5.4% drop in CO2 emissions, post-pandemic economies are bouncing back to the pre-pandemic levels with rising Green House Gas (GHG) emissions (UNEP, 2021). According to the Circularity Gap report, only 8.6% of the global economy was circular in 2019, up from 9.1% just 2 years ago (de Wit et al., 2020). The report suggests that this could be explained by 3 underlying trends: “high rates of material extraction, ongoing stock build-up caused by urbanization, and low levels of end-of-use processing and cycling” (UNEPT, 2019). A recent publication of Bradshaw et al. (2021) analysis highlights several problems and incapacity of today’s society and government taking urgent action to stop raising environmental issues that are more threatening than currently believed: continuing biodiversity loss, scientifically undeniable sixth mass extinction of species, growing population size, and overconsumption causing social problems, failing implementation of international sustainable goals and climate change, and political impotence to take necessary action to stop the environmental crisis.

The COVID-19 pandemic and the financial crisis that came along with it mark a new stage for the future of the CE and environmental policies and might be seen as a disturbance. As todays situation on global economic instability and the ongoing Russia – Ukraine war caused food and energy shortages, inflation, unwinding asset bubbles in the U.S., supply chain bottlenecks, and debt crises in developing countries (Alden, 2022), it is important to review how sustainability indicators had been impacted by previous financial crisis happened in 2008–2009 to improve our future decisions for meeting upcoming challenges and testing resilience of sustainability. The CE concept was introduced by the EU a few years after the economic impact global financial crisis in 2008–2009 completed and was developed during the economic upswing period. In times of shock and uncertainty, countries’ determination to apply sustainability principles and keep the core of the current direction has to follow meaningful and operational decision-making process, including normative sustainability criteria by keeping the transition above the minimum levels (Derissen et al., 2011). Sustainability resilience analysis could help identify and cover any potential disruptions which could cause disturbances and how sustainability could recover from a disruption through adaptive components (Marchese et al., 2018). Some authors agree that sustainability resilience should include risk management framework to explore potential threats and issues regarding sustainability implementation to minimize their impact by applying controls and mitigation actions (Park et al., 2013; Saunders & Becker, 2015).

The relationship between economic growth and environmental sustainability, political changes and sustainability has been widely studied in the scientific articles, environmental and economic literature, while research on the environmental effects of the financial crisis is scarce (Burns & Tobin, 2016; Pacca et al., 2020) and lacks profound analysis and had been briefly addressed only in few scientific publications. Siddiqi (2000) results from the Asian Financial Crisis in 1998–2000 confirms short-term benefits from the reduction of air and water pollution, but with an economic slowdown its deferments to replace inefficient equipment with more efficient alternatives, has a negative impact on the land environment by increasing the pressure to clear forests for fire-wood, timber, or agricultural land. Another scientific article published by Geels (2013) analyses the impact of a financial-economic crisis on sustainability transitions through renewable energy, green policies, climate policies, urban initiatives, public opinion, and civil society initiatives. Author finds that during the global financial, crisis governments across the globe responded with “green stimulus” packages that boosted the investments in renewable energy, energy efficiency, and green innovations. The global growth was mostly driven by the expansion of solar power (61%), while investments in other renewable energy industries such as wind, biomass, biofuels, geothermal, and marine shrunk. The research concludes that the global financial crisis weakened public and political priorities on climate and sustainability policies and as a result, countries failed to fulfill Copenhagen 2009 objectives with no success of the Kyoto, reduced feed-in tariffs and renewable support, and failed the Emission Trading System. Although, todays technologies to exploit renewable resources are not sufficient to satisfy primary energy demand and has financial and technological disadvantages which requires capital-intensive investments, have high production costs, lower energy production volumes comparing to fossil energy production, and no guarantee for stability of energy production (Cucchiella & D’Adamo, 2012).

Furthermore, Brem et al. (2020) research finds that the financial crisis also affects the business sector’s willingness to take risks and invest in innovations and research mostly for financial reasons. Bank loans are still the most important source of corporate financing and the banking sector’s decision to refrain from investment in innovative firms because of the risk of capital loss had a bigger effect on the business than the raised funding from the government.

Another group of research papers (Anger & Barker, 2015; Jalles, 2020; Monteiro et al., 2018; Sadorsky, 2020) focus on the air pollution reduction analysis in the periods during and after the financial crisis. Castellanos and Boersma (2012) research paper confirms the reduction of NO2 emissions by 15–30% in the industrial regions in Europe during the global economic recession period in 2009. It also confirmed the increase in NO2 emissions during the economic recovery period with more intensive production activities.

Today, Europe recognizes environmental pollution and climate change as existential threats and an opportunity to address these issues and transition to a circular society, especially despite the ongoing Russia–Ukraine war, where introduced economic sanctions focus on energy embargo from Russia and detecting the first signs of upcoming global economic crisis. Environmental challenges, growing financial and energy crisis require consolidated actions from the EU institutions to be able effective maintain growing risk failing the circular economy objectives. Debates on the energy mix to achieve the global security of energy supply is growing and creates the perfect opportunity to encourage the transition to sustainability and CE-based economy transformation. Following Geels (2013) approach, financial-economic crisis can be seen as a shock and creates a pressure for governments to take actions and initiate changes. As a result, the sustainability transition may enter the new phase moving from pre-development (with a focus only on research and development activities) to a take-off phase (green innovations deployment and installation). It can be achieved only in countries with strong commitment to sustainable solutions and innovations. On the other hand, Dagar and Malik (2023) find that macroeconomic factors and growing oil prices can cause a lower production, have an impact to export deduction and eruptions in supply chain. It is only confirming the importance of understanding how future financial crises might affect tomorrow’s sustainability transitions and what side effects might be expected to find the perfect balance between economic recovery and commitment to a sustainable transition.

This paper assessing changes in GHG emissions, energy intensity, Gross Domestic Product (GDP), Foreign Direct Investments (FDI), and Research and Development (R&D) changes through the 2009–2021 period after the global financial crisis occurred and during the economic recovery period until these days providing the insights on, what we might expect in future, when a financial or any other crisis occur. The success of the EU’s Green Deal depends on how the EU’s CE policy will be able to cope and move forward to a circularity transition in the context of the economic and environmental crisis caused by COVID-19. Low carbon economy can help to generate wider socioeconomic benefits due to energy dependency reduction by replacing fossil fuels with domestic resources (Moutinho et al., 2018).

To achieve the goal, this study uses the modified Logarithmic mean Divisia index (LMDI) decomposition method with Kaya identity equations to understand factors with the biggest impact to GHG emissions. As biggest economies are more likely have a bigger contribution to GHG emissions, the five biggest European Union economies were chosen for further analysis. LMDI decomposition analysis can help to identify structure effects as changes in each sector and how they drive an environmental impact (Roux & Plank, 2022). The LMDI decomposition method is widely used in recent publications where separate sectors or country—wide impact to GHG emission deduction have been investigated. (Alajmi, 2021; Dolge & Blumberga, 2021; González et al., 2022; Luo et al., 2023; Shao et al., 2016). An combination of LMDI decomposition method and Kaya identity equation was used by Dolge and Blumberga (2021) where analysis of three Baltic states—Latvia, Lithuania and Estonia were conducted to identify key drivers of GHG emissions and how it can be mitigated in the long time period until 2030 by taking into account three possible scenarios: existing measures scenario, additional measures scenario, and business as usual scenario. The study found that energy intensity reduction shows positive effects on lowering GHG emissions. As a result, energy efficiency policies play a key role to speed up positive impact to the climate. Furthermore, the study finds the need to strengthen 3 Baltic states role to be more ambitious and take more drastical decisions on the existing national climate policies with the specific focus on the transport, industry, services, agriculture and household sectors.

We contribute to previous research in various ways. First, the analysis takes 12 years’ period with a specific focus on 2009, 2012, 2019 and 2021 years’ data allowing to evaluate an impact of the global financial crisis in 2009, economic recovery and growth periods in 2012 and 2019, respectively, and the beginning of COVID-19 resulted changes in emissions and financial crisis period in 2021. Second, the LMDI decomposition method allows to measure different factors and their impact on emissions related to energy, foreign direct investments, including research &development. The comparative analysis between five countries is performed to evaluate their performance and efficiency.

The study includes literature review analysis in Sect. 3.1, which presents any scientific publications published on financial crisis and sustainability or environment. Section 3.2 to track the progress toward sustainability and climate mitigation goals on the period 2009–2021 using emission intensity, energy intensity, GDP, FDI, R&D, and population growth analysis. Section 3.3 gives an overview of current events in the context of the CE and taken actions by the EU aiming to maintain upcoming financial and energy security challenges. Therefore, this study presents a novel and practical assessment tool for policy makers in a decisions’ management process giving more assurance on the transitioning to the circular economy effectiveness by highlighting the most critical and significant energy consumption and carbon reduction patterns.

2 Material and methods

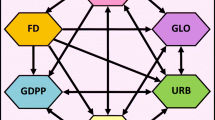

The applied methodology is divided into separate groups: (1) completed literature review to establish research problems and narrows down the research question; (2) 4 selected countries (Germany, France, Italy, and Spain) data analysis was completed using Logarithmic Mean Divisia index (LMDI) decomposition method with Kaya identity equations; (3) overview of taken actions to mitigate COVID-19, financial crisis, and the Russia–Ukraine war caused issues implementing Green Deal objectives. The applied conceptual framework of this study is presented in Fig. 1.

Methodology framework (designed by authors)

2.1 Literature review

In this paper, the search and review of existing literature and publications (scientific articles, case studies, non-governmental organization information from reports view) on the global 2008 financial crisis and its impact on the environment, impacts of COVID-19 on the global economy in the context of CE will help map and assess the research area and justify the research question. Scientific literature was collected from “Elsevier’s Scopus”, “Elsevier’s ScienceDirect” databases, and Google Scholar using keywords “global AND financial AND crisis AND air AND pollution”, “global AND financial AND crisis AND sustainability”, “global AND financial AND crisis AND environment”, “COVID-19 AND circular AND economy” to investigate the relationship between selected variables and provide the review how economic crisis impacts changes in the sustainability pattern. This was used to develop the theoretical framework from which the financial crisis impact on the CE study emerges and the following a conceptual framework that then becomes the basis of the current COVID-19 situation review. The current review explores and compares the impact of the Global Financial crisis in 2008 and COVID-19 on the sustainability and CE policies, including wide range of perspectives from different sources (Snyder, 2019).

The final section of this research includes an overview of the current years COVID-19, financial crisis and energy crisis analysis where implications how it could impact the future development of the circular economy is discussed.

2.2 Kaya LMDI decomposition method

Authors applied and modified Long-Mean Divisia Index (LMDI) decomposition method discussed by Ang (2004) by adding foreign direct investment (FDI) and research & development (R&D) index. Foreign direct investment indicator was selected to investigate how investments to sustainable projects had changed overtime and their correlation level with GHG emissions. LMDI method allows to assess GHG emissions changes taking into account energy intensity (E), economic growth (GDP), foreign direct investment (FDI), expenses on Research and Development (R&D), and population (P) growth variables in certain period. Decomposition analysis was completed by using the Kaya identity equation which is expressed as follow:

Data for Kaya identity decomposition was collected using Eurostat database and summarized in Table 1.

The applied period for data collection was 2008–2020. The decomposition analysis helps to identify fundamental drivers to change GHG emissions based on historical data. A comprehensive assessment of each component’s relative weight on GHG emissions helps to determine the impact of applied policy measures. Jiang et al. (2021) used decomposition analysis method for principal carbon emissions contributors completed on six contributors: China, the US, India, Russia, Japan, and Germany confirms that consumption volumes and international input structures are main factors increasing carbon emissions. Domestic input structure changes helped significantly reduce carbon emissions.

Each identity indicator is had been applied using Kaya identity equation as follows:

The LMDI for a five-factor case had been applied according to defined Kaya identity indicators: emission intensity, (EMI), energy intensity (ENI), GDP growth, FDI growth, and population growth (POP), where the following relationship between variables is presented in the formula:

Selected countries for analysis are Germany, France, Italy, and Spain as biggest economies in Europe. The chosen time interval of the study covers 13-year period from 2009 to 2021. The time interval is justified, because 2009 marks a peak of the global financial crisis and year 2021 is the beginning of the current financial crisis. The analysis period was divided in 3 stages where change analysis had been conducted: (1) comparative analysis between financial crisis 2009 and economic recovery period in 2012; (2) change during economic growth period between 2019 and 2012, and; (3) change analysis between COVID-19 and economic crisis period in 2021 with economic growth period in 2019.

3 Results

3.1 Lessons learned from the global financial crisis in 2008

While the concept of the CE itself presents considerable benefits by reducing waste, minimizing dependence on raw materials and imports, long-term economic growth and stability, the results of countries acts in the face of a crisis confirm different approaches. Any environmental, societal, financial or economic disaster are weakening economies and marginalizing efforts to build sustainability and the CE principles-based economy (Elhoseny et al., 2022). Anger and Barker (2015) agree that the effects of the financial crisis on the environment are usually linked to the reduction of emissions, which can be associated with lower economic activity and not by energy production structural changes. As a result, the economic crisis causes a switch of production to lower cost, more pollution intensive activities by using coal instead of gas for electricity production. The EU’s coal demand was steadily declining for a decade with a lowest point in 2020, as a result of COVID-19 pandemic and low gas prices in the market. Consequently, aims to improve economic recovery, rise of gas prices, weak hydropower, and the urgent need to replace Russian suppliers, limited the EU’s alternative resources for the energy production. It was confirmed by coal use trends in 2022 with an annual 1.2% growth to 8,025Mt global consumption mostly for electricity generation in all regions. EU countries increased coal power generation, restarted closed plants together with the acceleration of renewables and extension of lifetimes of nuclear plants (IEA, 2022a).

In addition, Geels (2013) research on the financial-economic crisis impact to sustainability finds a disproportion of investments to renewable and fossil fuel energy in 2011 during the economic recovery period when biggest economy countries’ invested $237 billion in renewable energy while about $302 billion had been invested in new fossil fuel generating capacity such as coal and gas. The author declares that European environmental and climate policy instruments (green stimulus, feed-in tariffs, European emissions trading) are not sufficient enough and appear to be weakening during the financial crisis of 2008–2009. Jalles (2020) finds that the economic crisis led to a statistically significant decrease in CO2 emissions, while methane and fluorinated gas emissions responded positively during the economic crisis and with a negative effect in the presence of strong economic conditions. Moreover, the financial crisis led to a positive response of consumption-related emissions and suggests that the economic crisis encourages the consumption of goods with lower environmental quality.

Among the existing evidence, Sadorsky (2020) finds that after the last financial crisis in 2008–2009, the change in CO2 emissions in the post-financial crisis period was lower than the change in CO2 emissions during pre-financial crisis. While developed countries (Japan, Canada, France, Germany, United Kingdom, Italy, and the U.S.) experienced a negative changes in CO2 emissions in the post-financial crisis period, some countries (Argentina, Australia, Brazil, India, Indonesia, Saudi Arabia, Turkey, China, and India) experienced an increase in CO2 emissions during the post-financial crisis period. However, the short-term positive effects of the crisis, consisting of lower air, and water pollution intensities have been negated in the long run by investments in the economy that aimed to achieve quick returns and recovery by compensating for losses rather than focusing on long term environmental and financial stability (Elliott, 2011; Jiang & Guan, 2017; Liu & Song, 2020; Peters et al., 2007). The analysis results of Jiang and Guan (2017) show that after the end of the financial crisis CO2 emissions from production processes skyrocketed from 206 Mt in 2008 to 1,711 Mt in 2011. Total CO2 emissions increased by 9.3% in 2011 compared with 2009 (IEA, 2018). The degree of annual emissions growth was even higher than before the crisis. China became the world leader in CO2 emissions in 2006 and since then, annual CO2 emissions have continued to rise. Even during the Global Financial crisis in 2008–-2009, China’s total CO2 emissions increased by 5.2% from 7,375 Mt to 7,759 Mt (Global Carbon Atlas, 2019; Pacca et al., 2020). Pacca et al. (2020) examined the impact of 419 financial crises on air pollutant emissions CO2, SO2, NOx, and PM2.5 in 150 countries from 1970 to 2014. The results of his analysis confirmed the decrease in global emissions of CO2, SO2, and NOx in the short-term and showed that the positive effects were only observed in high income countries, while they had no impact in low income countries. While countries focus on increasing their income in the short-term and ensuring the continuous growth of average standards of living (Ehrlich et al., 2012), the need to maintain the unavoidable environmental problems has taken second place and receives little attention (Bradshaw et al., 2021).

Environmental regulations are particularly vulnerable and their potential benefits are difficult to quantify (Jordan et al., 2013). The 2008 global financial crisis showed that governments have been focusing on ensuring financial sector stability to prevent major disruptions by bailing out financial institutions on a massive scale and injecting large amounts of capital (Meier et al., 2021). For example, European governments spent €600 billion on supporting the financial sector, equivalent to 4.6% of European GDP (Benczur et al., 2017), while environmental problems had to take a step back on the list of priorities and the density of EU environmental legislation proposals decreased dramatically during the crisis with only 2 environmental legislation proposals in 2009, 4 proposals in 2010 and 6 proposals in 2011. The significant increase in environmental legislation proposals were found in 2012 with 13 proposals focusing on climate change (Burns et al., 2020). Russel and Benson (2014) find that there has been a shift away from green stimulus measures during periods of economic recession in the UK. These findings suggest that environmental improvement does not become a long-term policy during the economic crisis and in the wider perspective, economic interests overcome SD and CE. Furthermore, Lamperti et al. (2019) predict that climate change through extreme weather events could increase the possibility of financial crises occurring with reduced productivity and industries operation abilities more than twice over.

3.2 LMDI decomposition results for Germany, France, Italy and Spain

Completed literature review confirms the impact of the economic crisis on environmental policies and emission changes. The following analysis of LMDI decomposition was completed on Germany, France, Italy and Spain countries being among the biggest economies in the European Union comparing GDP per capita with other EU’s countries (Eurostat, 2021). As a result, these countries contain enough resources and tools to maintain dual control relationship between climate change mitigation measures and economic growth stimulation. In order to investigate these countries capabilities to mitigate GHG emission deduction, a more in-depth analysis is conducted to observe changes of Kaya identity factors and to analyze different factors effect on GHG emissions. Analysis was conducted comparing 4 periods in the timeline with the following rationale: 2009 during the peak of the global financial crisis, 2012 was a year when economy started recovering, 2019 year selected being as year before the COVID-19 pandemic started, and 2021 year when the first signs of an upcoming economic crisis started to show.

Summary of used data for Kaya identity indicators with calculated change between periods is presented in Table 2.

Initial analysis of 6 indicators shows GHG emissions reduction in all countries comparing 4 selected periods, except in Germany where GHG emissions increased by 18.2 in comparison with 2009 and 2012 data. As discussed previously, authors (Anger & Barker, 2015; Monteiro et al., 2018; Sadorsky, 2020) analyzing energy consumption changes finds the direct correlation between economic activity, measured by GDP changes, and FDI. However, completed more detail year by year analysis finds an increase in GHG emissions during the economy recovery period in some countries (see Fig. 2). Furthermore, it shows a significant increase in GHG emissions in 2021 in all 4 countries. It can be associated with the end of COVID-19 lockdown restrictions when countries started coming back to their normal economic activities by accelerating economic activities along with energy intensity. R&D are one of key factors determining economic success through the increase in economic productivity and greater technological potential (Dima et al., 2018). However, some studies find that a high investment volume in the R&D does not mean a respective increase in the productivity and economic growth (Celli et al., 2021; Gordon, 2018). One of the explanation, it becomes more resource intensive and costly to find and develop ideas that could have a major impact (Bloom et al., 2020).

GHG emission changes in Germany, France, Italy and Spain during the period of 2009–2021 (Eurostat, 2021)

Our analysis cannot fully confirm energy consumption levels association with economic indicators such as GDP and FDI. Only Germany increased energy consumption by 73.0 Mt eq during the period of 2012–2019 with GDP growth of 728.0 million euro, and FDI increase by 529.0 million euro. France, Italy, and Spain was showing energy intensity decrease while GDP, FDI, and investments to R&D were growing. However, comparative data analysis of periods 2019 and 2021 finds that decrease in energy intensity and slowdown in GDP growth in all 4 countries of this analysis. Additionally, countries investments in R&D was also declining in last few years showing a growing concentration to fast economic recovery instead of focusing on long-term investments in innovations.

Summarized results of completed analysis of the LMDI decomposition results for Germany, France, Italy, and Spain is presented in Table 3.

As it is noted in Table 2, the GHG emissions decreased in all countries during the analysis period, except in Germany, when during the economic recovery period, GHG increased by 18.2 million tons of CO2. Germany’s energy structure consists of 44.6% renewables which includes wind onshore, solar, biomass as the biggest share of all renewables. Lignite, natural gas and hard coal takes another 45% share of energy sources (BDEW, 2022). France is highly dependable on nuclear power which is the main energy source of domestic energy production (77%), bioenergy and waste are second source with 13% share. France imports all coal and oil needs and has the lowest need for fossil fuel among G20 countries thanks to the significant share of nuclear power (IEA, 2021). The major energy source in Italy is fossil fuels mostly from natural gas (43%) and oil (32%). Energy production is not well developed in Italy and takes nearly 20% of total energy production. However, Italy is strongly committed to increase energy production from renewables share by 2026 with 59-billion-euro injection into the energy sector (International Trade Administration, 2022). Renewables are leading energy source in Spain with dominating wind, hydro, and solar sources, followed by nuclear power and natural gas (IEA, 2022b).

Following LMDI analysis results from Table 3, the decrease in absolute GHG emissions was caused mainly by constantly decrease in energy only in Germany from 0.13 in 2009 until 0.09 in 2021. Other countries show consistent increase in energy intensity through the whole periods of the analysis, except small deduction in Italy and Spain during the economic recovery period in 2012, when energy intensity decreased by 0.01 and 0.09 points, respectively. It indicates that countries have been taking efficiency improvement project to reduce energy consumption. The significant growth of the energy intensity in Italy and Spain was found during the following periods in 2019 and 2021 when economic recovery was one of the main goals for economies. As a result, it can be confirmed that countries were able to keep the same growth of economic activities and managed to reduce GHG emissions at the same time.

The end of the global financial crisis marks the growth of economic activity, where GDP, FDI, and R&D growth had been significant, as observed in 2012, 2019, and 2021. Countries were able attract significant amount of FDI and the investments in the R&D activities against GDP were consistent. The R&D growth was in line with countries’ GDP growth. However, economic recession confirms the negative impact on R&D investments. It shows that countries shifted their focus from sustainable innovations and researches to other subjects which gives more concerns to them and give a reason for potential debates if the investment to R&D can be efficient comparing to expectation on their contribution to economy recovery. This issue was discussed by few researches (Bloom et al., 2020; Celli et al., 2021; Gordon, 2018) noting that investments are costly, do not give the same financial benefit or boost to the economy as it was expected in the beginning. In this particular case, countries were focusing on increased health costs and energy independency assurance after the COVID-19 pandemic and Russia’s invasion to Ukraine when multiple number of sanctions were imposed by the EU.

3.3 Environment versus economy in the post-pandemic world

The global economy causes a tight dependence of world countries’ economies to each other and on the intensity of a financial crisis. The relationship between economic growth and environmental sustainability has been widely studied in the publications of the past decade (Cumming & von Cramon-Taubadel, 2018; Kurniawan et al., 2021; Samimi et al., 2011; Sethi et al., 2020). So far, the economic growth has been dissociated from SD and CE to improve human well-being (Arrow et al., 2012; Cumming & von Cramon-Taubadel, 2018; Lawn & Clarke, 2010) causing new socio-economic problems and environmental degradation, while an integrated approach could light the transition to a sustainable and circular society. Jackson and Victor (2011) argue that “the financial-economic crisis and environmental problems as symptoms of deeper cultural problems in modern capitalist societies” with obsession on productivity growth and environmental pollution as undesirable outputs (Yue et al., 2019), extraction and consumption of natural resources (Ahmad et al., 2020), and higher consumer consumption. Geels (2013) concludes that today’s modern society with financial, socio-economic and environmental problems are facing a “triple crisis” that signals the possibility of improving circularity and sustainable transition, if society will recognize deeper structural and cultural roots that are causing global warming. Calisto Friant et al. (2021) states that Europe, in a line with CE, focuses on growth and competitiveness rather than human well-being and ecosystem health and does not address the core socio-ecological challenges of the twenty-first century.

The EU has a fundamental and unique climate policy framework since 2000 with ambitious GHG emission targets set for 2020, 2030, and 2050. The ultimate goal is to become the first climate-neutral continent in the world by 2050 (European Commission, 2020). The global pandemic shifted national policies from environmental to public health course and the impact to the countries’ economies and environment is not incontrovertible while the demand for critical analysis of CE in the context of financial crisis is growing. It was clear that the COVID-19 crisis had affected climate-related investment negatively across all sectors. Around 40% large firms and SME’s decided not invest on climate-related measures (European Investment Bank, 2021). Additionally, Russia’s invasion of Ukraine caused an energy crisis in Europe requiring significant measures to take mitigating market volatility. Current financial crisis gives scientists unique opportunity to analyze crisis impact to EU’s the sustainable development and CE policies. The CE concept was introduced in 2015 after the global financial crisis happened and the economy was in a full recovery speed. As a result, the CE policy was having favorable conditions for stable growth without any eruptions from the external environment. Now EU countries are maintaining the consequences caused by the COVID-19 situation, reacting and shifting energy policy to reduce EU’s energy sector dependency on imports from the Russia and alongside keeping the same path for CE’s objectives implementation.

A summary of literature review results presents the impact of the COVID-19 on the environment and the economy (see Fig. 3).

COVID-19 positive and negative impact on the environment and economic (prepared by authors (Baldasano, 2020; Ellen MacArthur Foundation, 2020; European Environment Agency, 2020; European Investment Bank, 2021; Gama et al., 2021; Ibn-Mohammed et al., 2021; Menut et al., 2020; Reinsdorf et al., 2020; Samimi et al., 2011; Sharif et al., 2020; Smith et al., 2021; J. Wang et al., 2021; Yu et al., 2020; Yue et al., 2019; Zheng et al., 2020)

It is difficult to compare the impact of the global financial crisis and the crisis caused the COVID-19, because of their impact on social and economic activities, but some similarities can be found. National lockdown caused by COVID-19 improve air quality and have a positive impact on the environment (Baldasano, 2020; Filonchyk et al., 2020; Gama et al., 2021; Menut et al., 2020; Shi & Brasseur, 2020; J. Wang et al., 2021) by reducing energy demand, use of fossil fuels and CO2 emissions as it happened during the global financial crisis of 2008–2009. It is estimated that globally CO2 emissions might fall by 8% or 2.6 GtCO2 in 2020 and would be the largest reduction ever and the lowest level since 2010 (IEA, 2020). Across the European Union, annual CO2 emissions fell by 10% relative to 2019. Lower electricity demand drove a more than 20% decline in coal-fired power generation and increased the share of renewables in electricity generation to 39%. However, the prediction of the growing energy consumption and demand in the long run might be caused by market recovery and higher consumption (Global Energy Perspective 2022; IEA, 2020) as it was found during the economic recovery period in 2010. Travel restrictions allowed not only improve air quality, but also helped reduce noise pollution in the cities (Smith et al., 2021). Scientists are divided into different groups questioning is there going to be continuous waves of COVID-19 virus. Events of past months confirmed that the awareness about ongoing virus needed to be stepped aside when the Russia–Ukraine war had begun and new environmental treats arose due to intensive military actions and combats happening putting world into a new and unpredictable environmental crisis to defeat.

The pandemic, the slowdown in China, raising inflation, and energy crisis causing an increase in cost-of-living prices, and ongoing war are raising future global economic stability questions. In October 2022, the International Monetary Fund (2022) published The World Economic Outlook with the prediction of the global economy slow growth by 2.7% in 2023—0.5% lower than the 3.2% growth in 2022. The significant economic slowdown has shown in the largest economies: a GDP contraction in US and EU, prolonged COVID-19 outbreak and lockdown in China, growing real estate crisis. Lessons learned from the 2008–2009 financial crisis allowed the financial sector and governments to react rapidly to minimize the economic results according to the financial market’s reaction to the spread of COVID-19 (Brada et al., 2021; Sharif et al., 2020) and raising inflation. Aggressive policy actions from central banks such as constantly increasing interest rates kept the global financial systems from failing into crisis during the COVID-19 pandemic (World Bank, 2021) with an assurance of a timely return of inflation to the 2% medium-term target. There is no doubt that public health during a pandemic is the top priority, but the necessity for economic recovery with stimulus packages raise questions about necessity of focusing more on resilient and low carbon CE instead of rapid economic recovery and growth (Ibn-Mohammed et al., 2021). The vast majority of the government policies implemented during the pandemic are more “rescue” than “recovery” and pay little attention to sustainability, climate change, and resilience. Only a few members of the EU (Spain, Germany, France), United Kingdom, and Canada COVID-19 stimulus “green” packages support more promising sustainable transition (Ellen MacArthur Foundation, 2020; Vivid Economics, 2020). Also, European Investment Bank (2021) report confirms that only 30% of the EU’s long-term budget and COVID-19 recovery fund known as NextGenerationEU which totals about 547 billion Euro will be spent on climate objectives. This confirms the common tendency between world economies—according to the Green Stimulus Index report (Vivid Economics, 2020) 17 major economies announced economic stimulus packages in total worth 11.8 trillion U.S. dollars. Roughly 3.5 trillion U.S. dollars (30%) in the announced stimulus will focus on long-term recovery in environmentally intensive sectors for climate change, biodiversity and local pollution, while the rest of the stimulus package (8.3 trillion U.S. dollars) focuses on non-environmentally relevant sectors. Emerging economies such as China, India, Mexico, and Brazil along with Russia depend on environmental intensive sectors such as high carbon industries, energy sectors and unsustainable agriculture practices. The most notable examples of the COVID-19 response measures are likely to support the current trajectory of manufacturing, energy industries and agriculture sectors with significant deregulation, tax cuts, or subsidies and are likely to worsen environmental outcomes. This implies that economic interests again overcome environmental interests and in the long term period, will not have a positive impact on the environment. As a result, by the end of the pandemic, we might have an even bigger climate crisis than we are having now and this will lead to a bigger economic and social exclusion between different social groups and countries with developed and emerging economies.

The pandemic only sharpened the global circularity problem and shattered the core sustaining pillars by increasing the demand of medical supplies (Yu et al., 2020), use of single use plastic (Nielsen et al., 2019), and increased amount of hazardous waste (Zheng et al., 2020) in 2020. In some cases, the amount of medical waste increased by 350–370% (Klemeš et al., 2020). Furthermore, COVID-19 has further enhanced the need to reflect on social behavior and individual lifestyles and how it impacts the environment and pollution. The consumer exaggerated reaction to the pandemic and announced lockdown. In the situation of panic buying, consumers’ decisions are influenced by their peers’ choices (seeing long queues of hoarders in front of the supermarket, unmeasured high demand of certain products, news on the internet and television) by giving less attention to pro-environmental purchasing choices (Zheng et al., 2020), changes the perception and created uncertainty about future supply based on their observations (Tsao et al., 2019). Changed consumer behavior and a higher need for single-use plastic could put the world into a new environment crisis after COVID-19.

Sustainable supply chains could be a solution to solving the consumption caused environmental crisis and could help to avoid raw materials delays, increased logistic costs, stoppage of production, import and export-related problems that occurred during the pandemic and sharpened global supply and demand issues (Chakraborty & Maity, 2020; Golroudbary et al., 2019; Hossain et al., 2022). Changes in the supply chain to make it more sustainable and flexible could be implemented by taking responsibility and optimizing the sustainable transition through a supply chain organization framework and infrastructure (Dwivedi et al., 2021; Sassanelli et al., 2020). The ability to flexibly allocate resources gives a better position to business companies and governance to deal with any environmental or international trade issues and design more sustainable offerings to consumers (Gelhard & von Delft, 2015). One of the benefits of the sustainable supply chain are the flexibility at the process level through logistic sub-systems and controls which helps to minimize various costs of green/remanufactured products, including energy, labor, material, and logistic costs (Bag & Rahman, 2023).

It is obvious that countries are economically affected by the pandemic and government, society, and business sectors might be focused on rapid economic recovery and not environment protection or further CE implementation. The recovery from the pandemic provides a unique opportunity for economic transformation to carbon neutral and smart green technologies. Yet, uncertainties and financial strains could keep World economies from embarking on the necessary transformation. Countries and cities will have to evaluate the current situation and make strategic decisions for the future CE development.

4 Discussion

This paper highlights the importance of raising environmental issues while countries mostly focus on solving urbanization, resource extraction, economic growth, increasing production and consumption problems. In this context, CE was proposed as an instrument, which could resolve climate change problems while ensuring stable economic growth. Since the introduction of the CE concept in the EU policies, CE have had favorable conditions: stable global economic growth, high local governments, society and interest group involvement. The pandemic is the first serious test of the continuous stability of the CE and pro-environmental policies. While ongoing Russia–Ukraine war could test how far we are willing to go and invest to maintain the current sustainability and CE direction achieving the energy freedom from Russia’s natural resources and ensuring economic stability in the region (Pereira et al., 2022). Data analysis on the global financial crisis of 2008–2009 and economic recovery period helped understand and more effectively moderate the near future of the CE policies during and after any occurring crisis. Results confirms that economic recovery period correlates with a rise of energy intensity, while increase on FDI and R&D helped to manage and reduce GHG emissions effectively. However, to this day, countries’ economies rely on natural resource and the future financial crisis impact on the environment remains significant. Countries’ economies transition to renewable resources could not only reduce impact to the climate, but also reduce emissions differences during and after financial crises.

While the COVID-19 impact confirms the improvement of the environment, it has also sharpened circularity pillars: suspensions on plastic ban policy, increased use of single-use plastic, hazardous and medical waste raise more serious concerns about our future. The economic stimulus packages distributed with the 70% of 11.8 trillion U.S. dollars to non-environmentally relevant sectors confirms that countries are more concerned about rapid economic recovery than the growing global environmental crises. The EU confirms that societal resilience, dependency on a resilient environmental support system, reliance on single-use plastic, and low oil price resulting from lockdowns have negative consequences (European Environment Agency, 2021).

The Russia – Ukraine war could be a turning point to change the public policy, justify and support more the transition to the clean-energy since shocks and crises can drive political processes. This shock could be used as a window to accelerate renewable energy technologies to lose the dependency of fossil fuels by orientating global investments toward sustainability. However, taken actions demonstrates otherwise, the world keeps struggling to strike the balance between the energy sustainability and energy security resulting global coal demand increase by 1% (IEA, 2022c). Furthermore, the EU Parliament had to take political compromise and included gas and nuclear energy in the sustainable finance taxonomy pack. Since January 2023, the Complimentary Delegated Act announced nuclear energy and fossil gas as low-carbon alternatives contributing to climate change objectives and decarbonization of the Union’s economy (European Comission 2022). This decision goes against the EU sustainable development approach, including the Paris agreement and the European Green Deal.

The financial crisis impact on the environment has analyzed only by few studies and requires a broader and deeper analysis focusing on countries’ environmental policies changes, consumer behavior changes in the crisis situation, and how they re-share pro-environmental decisions. Future research on systematic data collection of implied innovations, technologies along with social-economic and environmental indicators are needed to help scientists simulate the possible future economic crisis scenarios, political decisions impact on the economic growth and how it impacts environment.

5 Conclusion

COVID-19 and the Russia–Ukraine war have highlighted the fragility of the sustainability principles and countries high fragility on the energy security. Data analysis from the previous global financial crisis of 2008–2009 helps to modular the possible impact to the environment and countries actions seeking rapid economic recovery. Results from previous studies confirm, that short-term economic recovery policies are unlikely to be sustainable in the long-run. Completed literature review and data analysis results confirm that the financial crisis had a positive impact on GHG emissions reduction in 2009, which can be explained by lower economic activities. Furthermore, countries were able to manage and reduce GHG emissions consistently through the whole period of the analysis with strong commitment funding R&D activities and being able to attract growing amount of FDI. The European Economic Recovery Plan and its strong focus on renewable energy helped increase the renewable energy share in the gross final energy consumption. Furthermore, the EU is strongly committed mitigating energy crisis by adopting REPowerEU Plan, European Gas Demand Reduction Plan, diversifying energy supply sources by importing liquefied natural gas and increasing deliveries of pipeline gas, and putting more investments in the energy infrastructure. However, at the moment the most significant EU focus is energy market stabilization, leaving social, economy and CE principles implementation in the back.

Global lockdown had a positive impact on air quality—reduced CO2 emissions and noise pollution. Still, COVID-19 along with Russia—Ukraine was have caused an even bigger financial and energy crisis than the one that happened in 2008–-2009. The European Union (27) GDP contracted by -6.1% and it is 1.4 times lower than in 2009. The European Union must focus on effective synergy between two strategic goals and its implementation—ensure rapid economy recovery in the context of the ongoing CE policy defined in the Green Deal documentation. The EU is strongly committed transitioning energy production to more renewable sources and reducing energy dependency from Russia, but other aspects of sustainability and CE policies remain uncertain. Evidence shows that the vast majority of government policies implemented during the pandemic focus on pandemic control measures rather than sustainability and resilience. Only 3 European Union countries: Spain, Germany, and France proposed COVID-19 stimulus “green” packages to support a sustainable transition. Major emerging economies (China, India, Russia, Mexico, and Brazil) economic stimulus packages focus on rapid economic recovery and quick returns on non-environmentally relevant sectors. These countries are likely to support the current trajectory of manufacturing, energy industries and agriculture sectors and they are likely to worsen environmental outcomes. China, India and Russia are leaders on global CO2 emissions and their impact on climate change in the next few years is going to be significant. Ongoing Russia–Ukraine war has a significant effect on climate change and removed achieved emissions reductions during the pandemic. However, it significantly shifted the political narrative and gave positive signs of transitioning from a linear to a circular economy and focusing on solutions to increase renewable energy-related projects implementation.

Following the conducted analysis and completed literature review authors believes that successful continuity of the circular economy framework and resilience should be based on the combination of data analysis, forecast of future scenarios and risk management framework. It would help to stay consistent and focus on the current circular economy governance, key objectives and minimize negative impact of any potential crisis.

This paper highlights the ongoing confrontation between the economy and the environment. So far, countries’ actions on sustainable transitions are insufficient and require drastic decisions and economic changes focusing not only on the short-term solutions. This paper is the first step in analyzing the financial crisis impact on sustainability and circular economy implementation. Further scientific and statistical analyzes are needed.

Data availability

All data generated and analyzed during the current study are included in this published article and also can be available in the EUROSTAT database.

References

Ahmad, M., Jiang, P., Majeed, A., Umar, M., Khan, Z., & Muhammad, S. (2020). The dynamic impact of natural resources, technological innovations and economic growth on ecological footprint: An advanced panel data estimation. Resources Policy. https://doi.org/10.1016/j.resourpol.2020.101817

Akram, N. (2013). Is climate change hindering economic growth of Asian economies. Asia-Pacific Development Journal, 19(2), 1–18. https://doi.org/10.18356/e7cfd1ec-en

Alajmi, R. G. (2021). Factors that impact greenhouse gas emissions in Saudi Arabia: Decomposition analysis using LMDI. Energy Policy, 156, 112454. https://doi.org/10.1016/j.enpol.2021.112454

Alam, M. S., & Kabir, M. N. (2013). Economic Growth And Environmental Sustainability: Empirical Evidence from East and South-East Asia. International Journal of Economics and Finance. https://doi.org/10.5539/ijef.v5n2p86

Albert, M. J. (2020). The dangers of decoupling: earth system crisis and the ‘Fourth Industrial Revolution.’ Global Policy. https://doi.org/10.1111/1758-5899.12791

Alden, E. (2022). Why This Global Economic Crisis Is Different. https://foreignpolicy.com/2022/06/14/inflation-stock-market-economic-crisis-trade-wto-ukraine-energy-food-shortages-fed-central-banks/. Accessed 7 August 2022

Ang, B. (2004). Decomposition analysis for policymaking in energy. Energy Policy, 32(9), 1131–1139. https://doi.org/10.1016/S0301-4215(03)00076-4

Anger, A., & Barker, T. (2015). The effects of the financial system and financial crises on global growth and the environment. In P. Arestis & M. Sawyer (Eds.), Finance and the macroeconomics of environmental policies (1st ed., pp. 153–193). Palgrave Macmillan.

Apeaning, R. W. (2021). Technological constraints to energy-related carbon emissions and economic growth decoupling: A retrospective and prospective analysis. Journal of Cleaner Production. https://doi.org/10.1016/j.jclepro.2020.125706

Arrow, K. J., Dasgupta, P., Goulder, L. H., Mumford, K. J., & Oleson, K. (2012). Sustainability and the measurement of wealth. Development Economics, 17(3), 317–353. https://doi.org/10.2307/26265518

Bag, S., & Rahman, M. S. (2023). The role of capabilities in shaping sustainable supply chain flexibility and enhancing circular economy-target performance: An empirical study. Supply Chain Management, 28(1), 162–178. https://doi.org/10.1108/SCM-05-2021-0246

Baldasano, J. M. (2020). COVID-19 lockdown effects on air quality by NO2 in the cities of Barcelona and Madrid (Spain). Science of the Total Environment. https://doi.org/10.1016/j.scitotenv.2020.140353

BDEW. (2022). Jahresbericht: Die Energieversorgung 2022. https://www.bdew.de/service/publikationen/jahresbericht-energieversorgung-2022/

Benczur, P., Cannas, G., Cariboni, J., Di Girolamo, F., Maccaferri, S., & Petracco Giudici, M. (2017). Evaluating the effectiveness of the new EU bank regulatory framework: A farewell to bail-out? Journal of Financial Stability. https://doi.org/10.1016/j.jfs.2016.03.001

Besenbacher, F. (2015). Delivering the circular economy—a toolkit for policymakers. https://www.ellenmacarthurfoundation.org/assets/downloads/government/EllenMacArthurFoundation_Policymakers-Toolkit.pdf. Accessed 13 February 2021

Bloom, N., Jones, C. I., Van Reenen, J., & Webb, M. (2020). Are ideas getting harder to find? American Economic Review, 110(4), 1104–1144. https://doi.org/10.1257/aer.20180338

Brada, J. C., Gajewski, P., & Kutan, A. M. (2021). Economic resiliency and recovery, lessons from the financial crisis for the COVID-19 pandemic: A regional perspective from Central and Eastern Europe. International Review of Financial Analysis. https://doi.org/10.1016/j.irfa.2021.101658

Bradshaw, C. J. A., Ehrlich, P. R., Beattie, A., Ceballos, G., Crist, E., Diamond, J., et al. (2021). Underestimating the challenges of avoiding a ghastly future. Frontiers in Conservation Science. https://doi.org/10.3389/fcosc.2020.615419

Brem, A., Nylund, P., & Viardot, E. (2020). The impact of the 2008 financial crisis on innovation: A dominant design perspective. Journal of Business Research. https://doi.org/10.1016/j.jbusres.2020.01.048

Burns, C., Eckersley, P., & Tobin, P. (2020). EU environmental policy in times of crisis. Journal of European Public Policy, 27(1), 1–19. https://doi.org/10.1080/13501763.2018.1561741

Burns, C., & Tobin, P. (2016). The Impact of the Economic Crisis on European Union Environmental Policy. JCMS: Journal of Common Market Studies. https://doi.org/10.1111/jcms.12396

Calisto Friant, M., Vermeulen, W. J. V., & Salomone, R. (2021). Analysing European Union circular economy policies: words versus actions. Sustainable Production and Consumption. https://doi.org/10.1016/j.spc.2020.11.001

Castellanos, P., & Boersma, K. F. (2012). Reductions in nitrogen oxides over Europe driven by environmental policy and economic recession. Scientific Reports. https://doi.org/10.1038/srep00265

Celli, V., Cerqua, A., & Pellegrini, G. (2021). Does R&D expenditure boost economic growth in lagging regions? Social Indicators Research. https://doi.org/10.1007/s11205-021-02786-5

Chakraborty, I., & Maity, P. (2020). COVID-19 outbreak: Migration, effects on society, global environment and prevention. Science of the Total Environment, 728, 138882. https://doi.org/10.1016/j.scitotenv.2020.138882

European Comission. Complimentary Delegated Act (2022). The European Union. https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32022R1214&from=EN

European Commission. (2020). Communication from the Commission. The European Green Deal. COM(2019) 640 final. https://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1596443911913&uri=CELEX:52019DC0640#document2. Accessed 11 January 2021

Cucchiella, F., & D’Adamo, I. (2012). Estimation of the energetic and environmental impacts of a roof-mounted building-integrated photovoltaic systems. Renewable and Sustainable Energy Reviews, 16(7), 5245–5259. https://doi.org/10.1016/j.rser.2012.04.034

Cumming, G. S., & von Cramon-Taubadel, S. (2018). Linking economic growth pathways and environmental sustainability by understanding development as alternate social–ecological regimes. Proceedings of the National Academy of Sciences. https://doi.org/10.1073/pnas.1807026115

Dagar, V., & Malik, S. (2023). Nexus between macroeconomic uncertainty, oil prices, and exports: evidence from quantile-on-quantile regression approach. Environmental Science and Pollution Research. https://doi.org/10.1007/s11356-023-25574-9

Derissen, S., Quaas, M. F., & Baumgärtner, S. (2011). The relationship between resilience and sustainability of ecological-economic systems. Ecological Economics, 70(6), 1121–1128. https://doi.org/10.1016/j.ecolecon.2011.01.003

Dima, A., Begu, L., Vasilescu, M., & Maassen, M. (2018). The relationship between the knowledge economy and global competitiveness in the European Union. Sustainability, 10(6), 1706. https://doi.org/10.3390/su10061706

Dolge, K., & Blumberga, D. (2021). Economic growth in contrast to GHG emission reduction measures in Green Deal context. Ecological Indicators, 130, 108153. https://doi.org/10.1016/j.ecolind.2021.108153

Dwivedi, A., Agrawal, D., Jha, A., Gastaldi, M., Paul, S. K., & D’Adamo, I. (2021). Addressing the challenges to sustainable initiatives in value chain flexibility: Implications for sustainable development goals. Global Journal of Flexible Systems Management, 22(s2), 179–197. https://doi.org/10.1007/s40171-021-00288-4

Vivid Economics. (2020). Green Stimulus Index. An assessment of the orientation of COVID-19 stimulus in relation to climate change, biodiversity and other environmental impacts. https://www.vivideconomics.com/wp-content/uploads/2020/07/GreenStimulusIndex14July.pdf. Accessed 5 March 2021

Ehrlich, P. R., Kareiva, P. M., & Daily, G. C. (2012). Securing natural capital and expanding equity to rescale civilization. Nature. https://doi.org/10.1038/nature11157

Elhoseny, M., Metawa, N., & El-hasnony, I. M. (2022). A new metaheuristic optimization model for financial crisis prediction: Towards sustainable development. Sustainable Computing: Informatics and Systems, 35, 100778. https://doi.org/10.1016/j.suscom.2022.100778

Ellen MacArthur Foundation. (2020). The circular economy: a transformative Covid-19 recovery strategy How policymakers can pave the way to a low carbon, prosperous future. https://www.ellenmacarthurfoundation.org/assets/downloads/The-circular-economy-a-transformative-Covid19-recovery-strategy.pdf. Accessed 4 March 2021

Elliott, L. (2011). Shades of green in East Asia: The impact of financial crises on the environment. Contemporary Politics, 17(2), 167–183. https://doi.org/10.1080/13569775.2011.565985

European Environment Agency. (2020). Air Quality in Europe—2020 report. https://www.eea.europa.eu/publications/air-quality-in-europe-2020-report. Accessed 23 December 2020

European Environment Agency. (2021). COVID-19 measures have mixed impacts on the environment. https://www.eea.europa.eu/highlights/impact-of-covid-19-lockdown. Accessed 6 April 2021

European Investment Bank. (2021). European Investment Bank Investment Report: Building a smart and green Europe in the COVID-19 era.

Eurostat. (2021). Air emissions accounts totals bridging to emission inventory totals. https://ec.europa.eu/eurostat/databrowser/view/ENV_AC_AIBRID_R2__custom_746941/default/table?lang=en. Accessed 28 March 2021

Fanning, A. L., O’Neill, D. W., Hickel, J., & Roux, N. (2021). The social shortfall and ecological overshoot of nations. Nature Sustainability, 5(1), 26–36. https://doi.org/10.1038/s41893-021-00799-z

Filonchyk, M., Hurynovich, V., & Yan, H. (2020). Impact of Covid-19 lockdown on air quality in the Poland, Eastern Europe. Environmental Research. https://doi.org/10.1016/j.envres.2020.110454

Fitch-Roy, O., Benson, D., & Monciardini, D. (2021). All around the world: Assessing optimality in comparative circular economy policy packages. Journal of Cleaner Production. https://doi.org/10.1016/j.jclepro.2020.125493

Gama, C., Relvas, H., Lopes, M., & Monteiro, A. (2021). The impact of COVID-19 on air quality levels in Portugal: A way to assess traffic contribution. Environmental Research. https://doi.org/10.1016/j.envres.2020.110515

Geels, F. W. (2013). The impact of the financial–economic crisis on sustainability transitions: Financial investment, governance and public discourse. Environmental Innovation and Societal Transitions. https://doi.org/10.1016/j.eist.2012.11.004

Gelhard, C., & von Delft, S. (2015). The role of strategic and value chain flexibility in achieving sustainability performance: an empirical analysis using conventional and consistent PLS. In Proceedings of the 2nd International Symposium on Partial Least Squares Path Modeling: The conference for PLS Users. University of Twente. https://doi.org/10.3990/2.350

Global Carbon Atlas. (2019). Global CO2 emissions. http://www.globalcarbonatlas.org/en/CO2-emissions. Accessed 15 February 2021

Golroudbary, S. R., Zahraee, S. M., Awan, U., & Kraslawski, A. (2019). Sustainable operations management in logistics using simulations and modelling: A framework for decision making in delivery management. Procedia Manufacturing, 30, 627–634. https://doi.org/10.1016/j.promfg.2019.02.088

González, P. F., Presno, M. J., & Landajo, M. (2022). Tracking the change in Spanish greenhouse gas emissions through an LMDI decomposition model: A global and sectoral approach. Journal of Environmental Sciences. https://doi.org/10.1016/j.jes.2022.08.027

Gordon, R. J. (2018). Why has economic growth slowed when innovation appears to be accelerating? NBER Working Paper Series. Cambridge. https://www.nber.org/system/files/working_papers/w24554/w24554.pdf

Haas, W., Krausmann, F., Wiedenhofer, D., & Heinz, M. (2015). How circular is the global economy?: An assessment of material flows, waste production, and recycling in the European Union and the World in 2005. Journal of Industrial Ecology. https://doi.org/10.1111/jiec.12244

Haberl, H., Wiedenhofer, D., Virág, D., Kalt, G., Plank, B., Brockway, P., et al. (2020). A systematic review of the evidence on decoupling of GDP, resource use and GHG emissions, part II: synthesizing the insights. Environmental Research Letters. https://doi.org/10.1088/1748-9326/ab842a

Haupt, M., Vadenbo, C., & Hellweg, S. (2017). Do we have the right performance indicators for the circular economy?: Insight into the Swiss Waste Management System. Journal of Industrial Ecology. https://doi.org/10.1111/jiec.12506

Hossain, M. K., Thakur, V., & Mangla, S. K. (2022). Modeling the emergency health-care supply chains: Responding to the COVID-19 pandemic. Journal of Business and Industrial Marketing, 37(8), 1623–1639. https://doi.org/10.1108/JBIM-07-2020-0315

Ibn-Mohammed, T., Mustapha, K. B., Godsell, J., Adamu, Z., Babatunde, K. A., Akintade, D. D., et al. (2021). A critical analysis of the impacts of COVID-19 on the global economy and ecosystems and opportunities for circular economy strategies. Resources, Conservation and Recycling. https://doi.org/10.1016/j.resconrec.2020.105169

IEA. (2018). Data and Statistics. CO2 emissions. https://www.iea.org/data-and-statistics/?country=WORLD&fuel=CO2 emissions&indicator=TotCO2. Accessed 15 February 2021

IEA. (2020). Global Energy Review 2020. https://www.iea.org/reports/global-energy-review-2020/global-energy-and-co2-emissions-in-2020#abstract. Accessed 4 March 2021

IEA. (2021). France 2021: Energy Policy Review. https://iea.blob.core.windows.net/assets/7b3b4b9d-6db3-4dcf-a0a5-a9993d7dd1d6/France2021.pdf

IEA. (2022c). Coal Market Update—July 2022c. https://www.iea.org/reports/coal-market-update-july-2022c/demand. Accessed 1 January 2023

IEA. (2022b). Spain Electricity Security Policy. https://www.iea.org/articles/spain-electricity-security-policy

IEA. (2022a). Coal 2022a. Analysis and forecast to 2025. https://iea.blob.core.windows.net/assets/91982b4e-26dc-41d5-88b1-4c47ea436882/Coal2022a.pdf

International Trade Administration. (2022). Italy—Country Commercial Guide. https://www.trade.gov/country-commercial-guides/italy-natural-gas-renewable-energy

International Monetary Fund. (2022). World Economic Outlook: Countering the Cost-of-Living Crisis. www.imfbookstore.org

Jackson, T., & Victor, P. (2011). Productivity and work in the ‘green economy.’ Environmental Innovation and Societal Transitions. https://doi.org/10.1016/j.eist.2011.04.005

Jalles, J. T. (2020). The impact of financial crises on the environment in developing countries. Annals of Finance, 16(2), 281–306. https://doi.org/10.1007/s10436-019-00356-x

Jiang, M., An, H., Gao, X., Jia, N., Liu, S., & Zheng, H. (2021). Structural decomposition analysis of global carbon emissions: The contributions of domestic and international input changes. Journal of Environmental Management, 294, 112942. https://doi.org/10.1016/j.jenvman.2021.112942

Jiang, X., & Guan, D. (2017). The global CO2 emissions growth after international crisis and the role of international trade. Energy Policy. https://doi.org/10.1016/j.enpol.2017.07.058

Jordan, A., Bauer, M. W., & Green-Pedersen, C. (2013). Policy dismantling. Journal of European Public Policy. https://doi.org/10.1080/13501763.2013.771092

Klemeš, J. J., Van Fan, Y., Tan, R. R., & Jiang, P. (2020). Minimising the present and future plastic waste, energy and environmental footprints related to COVID-19. Renewable and Sustainable Energy Reviews. https://doi.org/10.1016/j.rser.2020.109883

Korhonen, J., Nuur, C., Feldmann, A., & Birkie, S. E. (2018). Circular economy as an essentially contested concept. Journal of Cleaner Production. https://doi.org/10.1016/j.jclepro.2017.12.111

Kurniawan, R., Sugiawan, Y., & Managi, S. (2021). Economic growth—environment nexus: An analysis based on natural capital component of inclusive wealth. Ecological Indicators. https://doi.org/10.1016/j.ecolind.2020.106982

Lamperti, F., Bosetti, V., Roventini, A., & Tavoni, M. (2019). The public costs of climate-induced financial instability. Nature Climate Change. https://doi.org/10.1038/s41558-019-0607-5

Lawn, P., & Clarke, M. (2010). The end of economic growth? A contracting threshold hypothesis. Ecological Economics. https://doi.org/10.1016/j.ecolecon.2010.06.007

Liu, H., & Song, Y. (2020). Financial development and carbon emissions in China since the recent world financial crisis: Evidence from a spatial-temporal analysis and a spatial Durbin model. Science of the Total Environment. https://doi.org/10.1016/j.scitotenv.2020.136771

Luo, X., Liu, C., & Zhao, H. (2023). Driving factors and emission reduction scenarios analysis of CO2 emissions in Guangdong-Hong Kong-Macao Greater Bay Area and surrounding cities based on LMDI and system dynamics. Science of the Total Environment, 870, 161966. https://doi.org/10.1016/j.scitotenv.2023.161966

Marchese, D., Reynolds, E., Bates, M. E., Morgan, H., Clark, S. S., & Linkov, I. (2018). Resilience and sustainability: Similarities and differences in environmental management applications. Science of the Total Environment, 613–614, 1275–1283. https://doi.org/10.1016/j.scitotenv.2017.09.086

Meier, S., Rodriguez Gonzalez, M., & Kunze, F. (2021). The global financial crisis, the EMU sovereign debt crisis and international financial regulation: Lessons from a systematic literature review. International Review of Law and Economics. https://doi.org/10.1016/j.irle.2020.105945

Menut, L., Bessagnet, B., Siour, G., Mailler, S., Pennel, R., & Cholakian, A. (2020). Impact of lockdown measures to combat Covid-19 on air quality over western Europe. Science of the Total Environment. https://doi.org/10.1016/j.scitotenv.2020.140426

Monteiro, A., Russo, M., Gama, C., Lopes, M., & Borrego, C. (2018). How economic crisis influence air quality over Portugal (Lisbon and Porto)? Atmospheric Pollution Research. https://doi.org/10.1016/j.apr.2017.11.009

Moutinho, V., Madaleno, M., Inglesi-Lotz, R., & Dogan, E. (2018). Factors affecting CO2 emissions in top countries on renewable energies: A LMDI decomposition application. Renewable and Sustainable Energy Reviews, 90, 605–622. https://doi.org/10.1016/j.rser.2018.02.009

Nielsen, T. D., Holmberg, K., & Stripple, J. (2019). Need a bag? A review of public policies on plastic carrier bags – Where, how and to what effect? Waste Management, 87. https://doi.org/10.1016/j.wasman.2019.02.025

Olsson, P., Galaz, V., & Boonstra, W. J. (2014). Sustainability transformations: A resilience perspective. Ecology and Society. https://doi.org/10.5751/ES-06799-190401

Pacca, L., Antonarakis, A., Schröder, P., & Antoniades, A. (2020). The effect of financial crises on air pollutant emissions: An assessment of the short vs. medium-term effects. Science of the Total Environment. https://doi.org/10.1016/j.scitotenv.2019.133614

Park, J., Seager, T. P., Rao, P. S. C., Convertino, M., & Linkov, I. (2013). Integrating risk and resilience approaches to catastrophe management in engineering systems. Risk Analysis, 33(3), 356–367. https://doi.org/10.1111/j.1539-6924.2012.01885.x

Pereira, P., Zhao, W., Symochko, L., Inacio, M., Bogunovic, I., & Barcelo, D. (2022). The Russian-Ukrainian armed conflict will push back the sustainable development goals. Geography and Sustainability, 3(3), 277–287. https://doi.org/10.1016/j.geosus.2022.09.003

Global Energy Perspective 2022. (2022). https://www.mckinsey.com/~/media/McKinsey/Industries/Oil and Gas/Our Insights/Global Energy Perspective 2022/Global-Energy-Perspective-2022-Executive-Summary.pdf

Peters, G. P., Weber, C. L., Guan, D., & Hubacek, K. (2007). China’s growing CO2 emissions: A race between increasing consumption and efficiency gains. Environmental Science and Technology, 41(17), 5939–5944. https://doi.org/10.1021/es070108f

Reinsdorf, M., Tebrake, J., O’Hanlon, N., & Graf, B. (2020). CPI Weights and COVID-19 Household Expenditure Patterns.

Rockström, J., Steffen, W., Noone, K., Persson, Å., Chapin, F. S., Lambin, E. F., et al. (2009). A safe operation space for humanity. Nature, 461(10), 472–475.

Roux, N., & Plank, B. (2022). The misinterpretation of structure effects of the LMDI and an alternative index decomposition. MethodsX, 9, 101698. https://doi.org/10.1016/j.mex.2022.101698

Russel, D., & Benson, D. (2014). Green budgeting in an age of austerity: a transatlantic comparative perspective. Environmental Politics. https://doi.org/10.1080/09644016.2013.775727

Sadorsky, P. (2020). Energy Related CO2 Emissions before and after the Financial Crisis. Sustainability. https://doi.org/10.3390/su12093867

Samimi, A. J., Ghaderi, S., & Ahmadpour, M. (2011). Environmental sustainability and economic growth: Evidence from some developing countries Marginal Intra-Industry Trade and Employment Reallocation: The Case Study of Iran’s Manufacturing Industries View project Global Climate Risk and Economic Growth: Evidence from selected countries View project. Article in Advances in Environmental Biology. https://www.researchgate.net/publication/289666603

Sassanelli, C., Urbinati, A., Rosa, P., Chiaroni, D., & Terzi, S. (2020). Addressing circular economy through design for X approaches: A systematic literature review. Computers in Industry, 120, 103245. https://doi.org/10.1016/j.compind.2020.103245

Saunders, W. S. A., & Becker, J. S. (2015). A discussion of resilience and sustainability: Land use planning recovery from the Canterbury earthquake sequence, New Zealand. International Journal of Disaster Risk Reduction, 14, 73–81. https://doi.org/10.1016/j.ijdrr.2015.01.013

Scheel, C., Aguiñaga, E., & Bello, B. (2020). Decoupling economic development from the consumption of finite resources using circular economy. A model for developing countries. Sustainability (switzerland). https://doi.org/10.3390/su12041291

Sethi, P., Chakrabarti, D., & Bhattacharjee, S. (2020). Globalization, financial development and economic growth: Perils on the environmental sustainability of an emerging economy. Journal of Policy Modeling. https://doi.org/10.1016/j.jpolmod.2020.01.007

Shao, S., Yang, L., Gan, C., Cao, J., Geng, Y., & Guan, D. (2016). Using an extended LMDI model to explore techno-economic drivers of energy-related industrial CO2 emission changes: A case study for Shanghai (China). Renewable and Sustainable Energy Reviews, 55, 516–536. https://doi.org/10.1016/j.rser.2015.10.081