Abstract

One of the greatest challenges facing the contemporary research and academic world is to review the relationship between sustainable development and performance management system (PMS). More and more companies are embracing a strategic approach that includes sustainability issues into their corporate strategy. However, to date, sustainability and corporate strategy are still not adequately integrated in the organizations. Several criticisms are connected to its effectiveness and its practical implementation. In this context, in view of the numerous critical issues emerged in the literature, the aim of this paper is twofold: (1) to provide a clear view on the main sustainability dimensions considered relevant in the managerial practice, and (2) to identify a suitable approach to align the sustainability dimensions identified in the corporate strategy. To this end, we conducted a semi-structured interview with 70 middle and senior managers of Italian companies, specializing in sustainable development issues. Accordingly, the findings have revealed that to implement sustainable development strategy, organizations need to integrate five sustainability dimensions (environmental, social, economic, cultural and organizational) in the PMS execution. The results led to the identification of a cultural dimension as a key driver to support managers in implementing sustainability at a strategic level. The authors provided a sustainable framework oriented to emphasize the cultural change in the organizations as a first step of the sustainable development process.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

Emphasis upon sustainable development (SD) drivers and its integration at a strategic level has rapidly attracted practitioners’ interest, who urgently looked for practical solutions and tools to address Sustainable development Goals (SDGs) in their organizations (Farias et al., 2019). In this context, Environmental, Social and Governance (ESG) practices represent a structured guide (Clementino & Perkins, 2021; Lokuwaduge & Heenetigala, 2017) oriented to reporting and measuring how much a company is sustainable (Bhattacharyya & Cummings, 2015; Trianni et al., 2019; Wu et al., 2018). Despite the global relevance of the sustainability, as pointed out by the Agenda 2030 pillars, several studies have reported weakness of the emphasis on the sustainability dimensions in the corporate strategy (Morioka & de Carvalho, 2016). Moreover, although the contribution of the ESG reporting is assuming more and more relevance in the managerial practices, to date sustainability remains far from becoming an integral part of the corporate strategy (Hristov & Appolloni, 2021). Thus, to place sustainable strategies in the context of PMS and to implement related strategic tools remains puzzled for managers (Wu et al., 2018). In addition, a clear view of the main sustainability dimensions, and connected value drivers that impact on the practical implementation of the SD process in the organizations, is strongly required (Hristov et al., 2021).

To this end, we have decided to address our attention to the managerial experience and their perceptions of the SD drivers. Accordingly, aiming at filling this gap, the authors addressed the following two research questions:

(Rq1):

What are the main sustainability dimensions considered relevant in the managerial practices?

(Rq2):

How can sustainability dimensions be implemented into the corporate strategy to pursuit SD process?

Accordingly, to answer these research questions, in addition to the literature review, a survey upon 195 managers, and a semi-structured interview with 70 of them, was conducted.

With regard to the first purpose (1), the authors have identified five main sustainability dimensions, and connected value drivers, that the managers perceived positively, which are connected to: (i) the traditional triple bottom line (TBL) dimensions (environmental, social and economic), (ii) a cultural and (iii) an organizational dimension. We found that these dimensions play a crucial role in the management’s choice, whether implementing a sustainable strategy or not. For each dimension, we provided an exhaustive analysis of the key value drivers connected to the performance. Accordingly, we answered our first research question (Rq1) by providing a clear interpretation of the sustainable drivers considered relevant for the managers’ value creation process. This added bricks to the existing knowledge on the sustainability dimensions perceived by managers. Our results give managers a clear view in terms of sustainability value drivers as a key to increase their knowledge, directly supported by the same management experience (Cinquini & Mitchell, 2005) and therefore, strongly correlated to daily matters, which is useful to support managers’ decision process on the implementation of a sustainable strategy or not.

About the second research objective of this paper (2), some specific questions were addressed to the 70 respondents, aiming to analyze and discuss the managerial practices, together with the main challenges and criticisms, to find a way to deliver sustainable solutions to increase sustainability effectiveness at a strategic level.

In this view, we developed a strategic five-dimensional sustainable COESE (Culture, Organizational, Environment, Social and Economic) framework based on a set of sustainable value drivers, intended to support SD process in the organizations. In addition, we found that to integrate sustainability at a strategic level, it is necessary for it to be incorporated in the organizational culture.

Therefore, the paper enriches the existing literature in several directions. First, it provides a clear view on the sustainability dimensions considered relevant in practices, which clearly identify the managers’ perceptions on sustainable value drivers connected to a company’s performance. Thus, we have expanded the existing literature by integrating the managers’ practical contribution. Second, we found that the managers are very interested in the organizational and cultural dimensions, which were not been appropriately addressed in the existing literature from a strategic and accounting point of view. Accordingly, we have added it to the traditional TBL in our model. Third, we provide a structured model that suggests how to integrate sustainability and corporate strategy, which can be used for monitoring and implementing a sustainable-oriented strategy.

Following this introduction, the theoretical background on the main issues addressed in this work is provided (Sect. 2). Then, the paper develops the research methodology (Sect. 3), which is followed by the research findings (Sect. 4). The next sections discuss the results in view of sustainable theoretical development (Sect. 5), and the paper closes with the conclusion (Sect. 6).

2 Theoretical background

2.1 Sustainability dimensions in management accounting research

Interest in management accounting research on the SD issues has rapidly increased in the last 20 years and many scholars started focusing on the concept of corporate sustainability, which is defined as a business approach creating and sustaining the long-term value of a company (Hristov et al., 2021). This approach generally includes to embrace the TBL to recognize the urgent needs for radical changes in current, unsustainable business practices (De Villiers et al., 2016; Maas & Reniers, 2014). Hence, SD intervenes in achieving higher quality performance, when intended as a process designed to meet the present needs without compromising the ability of future generations to meet their own needs (Gond et al., 2012). The main stream of research recognizes the TBL as a key to implement sustainability. The environmental dimension is oriented to include the green value drivers (emissions, consumption, renewable resources and eco-efficiency) in the corporate strategies (Trianni et al., 2019). The social dimension requires the capacity of providing equal distribution among work conditions, human rights and social initiatives (Bellucci et al., 2019; Hristov & Chirico, 2019).

The last key dimension, mostly discussed in the literature, is the economic development associated to sustainability issues. The World Summit has treated relevant aspects of SD in Johannesburg (2002) and Paris (2015), moved attention to the fact that development must be considered a priority with respect to economic growth. This dimension is mainly implemented by the SDG 8, related to the decent work and economic growth.

Nevertheless, part of the recent literature (Hristov et al., 2021; Naciti et al., 2021) argues that many organizations feel SD as a constraint to the financial performance. It seems that the integration process in the managerial practices is not advancing quickly enough mainly due to the cultural barrier in organizations and the absence of trust in the financial benefits that are derived from the SD strategy (Bortolotti et al., 2015). Therefore, sustainability is, firstly, a cultural issue that requires more attention in the implementation of the sustainable strategy.

From the theoretical background outlined is evident that the main sustainability dimensions used to implement SD strategy are related to the TBL approach, extended to an additional cultural dimension. Accordingly, we decided to explore, directly with the managers, what are the main sustainability dimensions which are crucial in generating sustainable value. With regard to our first research question, we can hypothesize that the consideration of these four dimensions is relevant for managers and its integration in the corporate strategy has a positive impact on the overall company’s performance. We will test our hypothesis by the survey and a semi-structured interview, conducted with managers, as will be seen in the results’ Sect. (4).

2.2 Sustainable practices and measures

The integration of sustainability in the corporate strategy is strictly endorsed by the international standards, which underlines how a long-term strategic approach to sustainability is fundamental for the sustainable value creation of the organizations (Hsu & Chen, 2015; McWilliams & Siegel, 2000). Many certifications such as ISO 26000, Global Reporting Initiative (GRI) and the integrated reporting framework of the International Integrated Reporting Council (IIRC), refer to the sustainable practices as a key element to address SD at a business level (Adams & Frost, 2008). In addition, key performance indicators (KPIs) are used in the literature and practices to explain the integration of sustainable dimensions within the corporate strategy (Hristov & Chirico, 2019; Morrow & Rondinelli, 2002). In this context, the Balanced Scorecard (BSC) is one of the most relevant strategic tools used in supporting PMS’s implementation (Kaplan & Norton, 1992). However, during the years many authors have underlined critical issues related to the tool, such as the use of qualitative indicators, the integration, the role of the sustainability and the rigidity in consider multiple stakeholders (Busco & Quattrone, 2014; Chen et al., 2016; Chenhall, 2005; Jensen, 2001; Lipe & Salterio, 2000; Nørreklit, 2000). Moreover, a further impulse toward an evolution comes from the topic of sustainability, with entails the opportunities to create value for both the company and its surrounding actors. Overcoming the limits of the original version of the BSC has been possible by using its multidimensional nature, including social and environmental dimensions. These considerations lead to develop the Sustainability Balanced Scorecard (SBSC) introduced by Figge et al. (2002). What emerges, is the presence of several variations of the SBSC, resulting in as many frameworks suitable for different companies and contexts. At the same time, the drawback is that the SBSC suffers from excessive fragmentation, lacking uniformity. As already occurred with the BSC, even for its latest evolutions several problems have been evidenced. Among these critical issues, an example is the relationship between sustainability and corporate strategy, to which major attention should be given, since a strategy wrongly outlined undermines the success of the tool (Hristov et al., 2019).

3 Research method

3.1 Sample design and data collection

Data were gathered mainly through semi-structured interviews (Dai et al., 2019; Evans et al., 2015). In order to increase the knowledge to the existing literature, and therefore provide a practical implication, we collected data from a final sample of 70 managers who specialized in a sustainable strategy. Therefore, we applied a double process selection: (1) survey questionnaire for the sampling procedure and preliminary data, and (2) interview questionnaire for data selection and analysis. In this context, managers played a relevant role in providing a structured analysis of the practices and measures connected to the use of a sustainable strategy in management and governance.

In order to select the sample to interview, thanks to the AIDAFootnote 1 database and personal contacts, a web-based questionnaire survey was emailed to 195 managers in order to identify some basic information, experience with sustainability issues and the availability for interview. More specifically, the criteria for this selection were only companies with more than a hundred employees, because they were expected to have a more sophisticated PMS to manage the sustainable integration process (Lisi, 2015), and the availability of a web page or an email address. We received a total of 120 responses (61%). At this point in our research, in order to guarantee the quality of the selection, we identified those managers to be included in our final sample based on their experience (more than 5 years managing sustainable issues) and their position in the company (middle and top manager). We netted 86 managers and contacted them by email in order to verify their availability to have an interview (online), which resulted in 70 managers who confirmed their availability (Fig. 1).

Sample selection

The Figures below highlight the descriptive statistics of the sample. A large proportion of the sample is male, 40 + years old, who are middle managers with more than 5 years’ experience Fig. 2.

Frequency distribution by gender and experience

In addition, the sample presents managers actually working in manufacturing industry (51%), services (16%), information technology (13%), agriculture (13%) and transportation (7%) Fig. 3.

Frequency distribution by industry

3.2 Interviews and variables analyzed

After the first screening, we focused on the final sample of 70 managers (Fig. 4 and Fig. 5). Each interview lasted 62 min on average, from 51 to 73 min (54 managers by Teams and Skype, 16 by phone interview) and all data were analyzed by associating the responses in new conceptual dimensions Fig. 6. In particular, the questionnaire is composed of three different sections covering 14 questions (see “Appendix”). In developing the questionnaire structure, we were guided by our research questions (Brinkmann & Kvale, 2008; Ferreira & Otley, 2009; Hristov et al., 2021). The first section focused on the sustainability dimensions, the second to the key value drivers connected to the dimensions provided, the last section on the practices and measures, critical issues and main challenges, connected to the implementation of an efficient sustainable model Fig. 7. Through a specific set of questions, for each of the sections, addressed to the managers, we obtained the information that was aimed to support the answer to our first research question. To this end, qualitative data were analyzed by categorizing the responses into major conceptual areas, identifying the main sustainability dimensions, considered relevant by managers for adopt sustainable strategies, and connected key value drivers (Rq1). Finally, coherently to our second research question (Rq2), we investigated the practices and measures to integrate sustainability and strategy, and the main sustainable way and critical issues related to the integration process (Sect. 3 of the questionnaire attached).

Frequency distribution by position and education

Age frequency distribution of interviewees. Note: From the Figures above, we can note that the sample is representative of the Italian managers’ population, as documented by the Eurostat report (2019), which suggests that more than 50% of the Italian managers are aged between 45 and 55 years, with a master’s degree. Moreover, we have registered that a total of 39% of the sample is female, indicating a growth from the data provided by Eurostat, which shows an average of around 30%

3.3 Validity and rigor of the analysis conducted

To evaluate interviews, we adopted quantitative and qualitative approaches (Anderson & Widener, 2006; Ferreira & Merchant, 1992). With regard the first group, we used descriptive statistics supported by charts and tables, as shown below (Sect. 4.1). In the same way, considering the qualitative approach, interview process was prepared based on the Ferreira and Otley (2009) framework, which supports our research process. All the raw data were transcribed after the interviews, which were interpreted and translated into the defined conceptual areas. Moreover, qualitative data were further processed by categorizing the responses into major conceptual groups. In a following step, we asked the sample of interviewees to check the transcribed track and to verify the possible mistakes. Therefore, we improved the validity of the process (Bortolotti et al., 2015). Finally, to improve the internal validity of the data collection, we triangulated all information obtained by the interviews and the secondary data generated by the literature (Eisenhardt & Graebner, 2007).

4 Research findings

We divided our research findings into two parts. The first aims to explore the sustainability dimensions implemented in the organizations (Rq1). The second part, presented in Sect. 5, aims to identify a sustainable way useful to support the future avenue for integration process between the five sustainability dimensions and the PMS (Rq2).

According to our first purpose, after the interviews, we read and analyzed the managers’ answers by including similar information and keywords in a specific cluster/dimension. Once the clusters were generated, we contacted the managers again (first round) to discuss the interpretation of the qualitative data in order to incorporate the changes required (Hristov et al., 2021). After this process, we identified five main dimensions (the traditional three dimensions of the TBL, a cultural and an organizational dimension), which represented the drivers of the SD in integrating sustainability at the strategic level, as explained below.

4.1 SD’ dimensions considered relevant in the managerial practices

According to our first purpose, we have concentrated on the key value drivers of the SD strategy addressed in the organizations. More specifically, we asked managers to focus on the main sustainability dimensions retained useful in achieving SD value at a business level (question 3 of the questionnaire). It is proper to specify that, in this step of our research, managers were told to be free in answering, thus without considering a number of options available (Brinkmann & Kvale, 2008). Accordingly, they were totally free to add further dimensions considered relevant in practice for the SD efficiency. In this context, we found two additional dimensions to the TBL, retained crucial for the integration between sustainability and corporate strategy. In addition, we asked managers to provide three key value drivers for each dimension discussed, considered mostly relevant in the managerial practice. In view of the data provided, the authors sorted out the outputs and they provided the five mostly frequent drivers for each dimension selected (Table 1).

Therefore, we arranged all questionnaires returned, then extracted, classified and counted the keywords singularly for each question, later we presented the main output in statistical charts and tables useful to show the opinions of interviewees. Firstly, as described in Fig. 6, managers have strongly confirmed the relevant role of the TBL in implementing sustainability strategies. In particular, a large part of them (67 of the total sample) suggested to integrate Environmental dimension in the corporate strategy as a key dimension in the SD process. Moreover, this dimension seems to be very relevant in the Manufacturing, Agriculture and Transportation industries (100% of the managers), where consumption, emissions, renewable sources, waste reduction and eco-efficiency are considered key concepts strictly correlated to the core business. We attempt to explain this through the consolidated, and partly mechanized, practices characterizing these sectors. It is likely, for example, that manufacturing sector managers perceive their focus to be mostly on environmental dynamics, which are apparently the most relevant for the final economic results they are especially interested in. The second dimension mostly frequent is the Economic dimension, with 61 answers. This dimension is mainly considered by the managers who works in Agriculture (100%) and Information Technology (89%) industry. The main drivers of the Economic dimension, as described in Table 1, are connected to the following categories: increase the sustainable profitability associated to the sustainability initiatives, to guarantee quality and to enhance product technology, and monitoring cost and sustainable revenues. This dimension assumes relevant role in decision-making process, supporting managers to link sustainability to the financial dimension.

Frequency distribution of the sample by sustainability dimension and industry

In addition, according to the results, we found that the social dimension of sustainability is considered relevant in the company’s strategy by 51 organizations. This probably suggests a low consideration of the social practices in the organizations, mainly due to the difficulty in measuring social value created (oriented to a more holistic approach in terms of networking and sustainable practices). More attention to this dimension is attributed by the managers who works in Information Technology and Transportation industries (with 100% of the managers). In this context, the main practices were oriented to the following key drivers: image and reputation, networking, stronger customer loyalty, social initiatives in collaboration with universities and public institutions and environment and work conditions.

As showed in Fig. 6, a total of 50 managers have discussed the relevant role covered by a cultural dimension, aiming to generate personal behavior of the company’s actors oriented to full understanding the importance of including sustainable practice in the strategy. All of the managers in the Information Technology industry (9) highlighted that the integration process is supported by a sustainability culture, for companies and individuals. In particular, one of the senior managers argued that “cultural change can be considered in the same time, a driver to support the implementation process of sustainability in a company, and a performance outcome, that reinforce the organizational integration and support corporate strategies in redefining and developing sustainable goals”. That strategically involving sustainability in the culture of the company can be achieved by implementing strategic goals oriented to co-working space, leadership and soft skills, learning and growth, cultural integration and strategic alignment, as shown by Table 1.

Finally, another very interesting issue was emerged by the interviews. Most of the managers have suggested that in practice exists a structural gap between strategy oriented to sustainability and its practical implementation. They focused on the lack of adequate assets, information system and digital transformation to support the implementation process. In particular, a total of 36 managers (51%) clearly identified this crucial aspect, often nonadequately addressed. As shown by Fig. 6, this dimension is uniformly distributed by all sector examined. For example, one of the managers, worked in a Manufacturing company, stated that “if exist a cultural orientation to sustainable development, but the organizational structure is not ready to implement this change, probably the development of the TBL will be inefficient”. The implementation of a SD strategy requires an organizational dimension, aimed to provide the practical conditions oriented to address sustainability issues in the company (Fry & Slocum, 2008; Hubbard, 2009).

In Table 1, we can observe the most frequent key value drivers for each the SD dimensions emerged in the managerial practices. They integration in the strategy can be considered crucial for achieving the sustainable integration.

4.2 Critical issues that hinder the SD success

In order to find potential solutions to support the integration process of sustainability in the corporate strategy, we asked managers to discuss the major criticisms perceived in their experience, in implementing sustainability goals. Several issues were emerged which we categorized in four main dimensions, as shown in Fig. 7.

Critical issues connected to the sustainable integration

Firstly, what clearly emerged (argued by all 70 managers interviewed) is that the missing emphasis of a cultural change contributes to limit the integration process in a company between sustainability and strategy. This can be considered a relevant critical issue in achieving SD. The guidelines along which it is developed is sustainability, the latter being included in the overall strategy, must be understood by the different departments and units. As a consequence, it is necessary to implement strategic goals related to the preparation of the organization to the cultural change, to increase the integration and to invest in learning and growth. In addition, very important is the actions and processes aimed to concrete network of relationships that can lead to different opportunities. The organizational alignment with corporate strategies oriented to SD practices play a crucial role in the integration process. Therefore, in view of the issues emerged, the cultural dimension can be seen as a key driver to overcome the critical issues connected to the lack of efficacy of the integration process. Before starting to implement sustainable strategies, a cultural change in the organization is strongly required.

In addition, another critical issue strongly highlighted by the managers (61 of them), as introduced in the previous subsection (4.1), is a lack of an adequate sustainable structure that could support TBL implementation. Fundamental is to invest in an organizational structure equipped with tangible and intangible assets suitable for support strategy implementation. In addition to the cultural dimension, we found that an organizational dimension is fundamental as a bridge between the cultural change and the traditional TBL. The organization needs to be adequately prepared to allow an effective benefit of the cultural change investments.

Managers have argued (suggested by a total of 32) that an expected competitive advantage is strongly associated to the inclusion of the Corporate Social Responsibility (CSR) practices in the strategy, pointed out that the social drivers need to be included in the PMS’s implementation to achieve high performance. In fact, this dimension represents one of the most critical perspectives of SD due to the limited approaches available in practice and the strategic system used to manage and measure its effective contribution to performance. More work is due by researchers to identify and analyze the role of the social KPIs in the PMS.

Finally, a criticism was emerged with regard to the fact that managers are still too focused on the short-term financial results and this represents an important critical issue that hinders the integration process (discussed by 30 managers). Again, cultural change covers relevant role in contributing to achieving an integrated view of the company’s system in terms of SD approach.

5 Theoretical development

According to the results discussed in the previous sections, we used all data provided and the critical issues highlighted to build a strategic five-dimensional sustainable model, based on three levels, aimed to overcome the gap existing between literature and practical implementation of the strategy SD oriented. More specifically, in a second step (after the discussion of the sustainability dimensions with managers), we built the model and contacted managers (second round) to discuss its potentiality in overcoming the existing gap. We improved the model according to the changes required by the managers and we provided here the final version. By analyzing the results and the critical issues, we conclude that the SD strategies based on the TBL approach, are inadequate if, in an early step of the PMS implementation, company’s members culture change is not completely generated and a sustainable organizational structure is not developed.

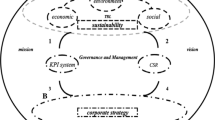

Accordingly, as shown in Fig. 8, in our illustration outcome, we can identify five main dimensions of the SD process divided into three broad levels, developed in different bottom-up moments: first (cultural dimension is implemented), two (organizational dimension is developed), three (TBL implementation, once the organization is ready to generate sustainable value). By following the performance tree introduced by Lebas and Euske (2002), this model is portrayed as a sustainable “house” to illustrate how an organization goes through the process of creating sustainable performance.

Sustainable development performance house framework (COESE)

Firstly, in the Level I, the cultural change needs to be incorporated in the strategy at an early stage, during the planning and formulation of the strategy. This level can be considered as the “foundation”, the most hidden part of the value creation process, on which the achievement of results depends (Lebas & Euske, 2002). In this early stage, a strategy cultural change oriented needs to be formulated, aiming to “shed light” on the relevance of SD issues.

Secondly, once the cultural change is completed and company’s members are aware on the relevance of adopting a sustainable behavior, in the Level II, the model shows an organizational dimension, “the walls of the house”, aimed to sustain the TBL strategy. In fact, this dimension provides a bridge from cultural change to TBL, in order to prepare the organization and its main authors, to efficiently incorporate culture change and to be able to implement the key value drivers of the sustainability.

Lastly, in the Level III, once the cultural change is computed, and the organization is able to support this change, the TBL pillars can be implemented. The consequences of the interaction with the sustainability take time to materialize.

Therefore, this approach allows to encapsulate sustainability dimensions and translate the value drivers generated in strategic goals leading towards a concept of sustainable value creation (Cardoni et al., 2018; Lewandowski, 2017).

According to the model developed above, we identified the actions to realize in order to translate strategy into practice with regard the environmental impact (renewable sources, waste reduction emissions, consumption and eco-efficiency), social performance (networking, work condition, image and reputation, loyalty, collaboration with public institutions) economic dimension (profitability, revenues, quality, product technology and cost), organizational structure (innovation, sustainable assets, information system, recruiting, internal skills) and cultural change (co-working, leadership and soft skills, learning and growth, sustainable training programs, strategic alignment).

6 Conclusion and final considerations

This paper provides insights and a contribution to the discussion about the way to integrate sustainability and corporate strategy. In the following subsections, the authors discussed the implications of the paper, the missing concept and future paths of research.

6.1 Theoretical and practical implications

Moved to our first research question (RQ1), thanks to the interviews, we found that two additional dimensions, to integrate to the traditional TBL, are considered relevant for practice in implementing sustainable strategies. The findings of this paper emphasized the positions of cultural changes and organizational structures in the view of the effectiveness of the SD process in the organizations. The implementation of a cultural dimension, as a first step of the SD orientation, is essential to create a strong foundation in the organization of the relevance associated to the sustainability practices into all levels of business.

Thus, we have confirmed the hypothesis of the research stream which suggested to add a cultural dimension to the TBL in implementing SD strategy (Hristov et al., 2021; Linnenluecke Griffiths, 2010), and we added an incremental contribution to the existing research, clearly identifying the value drivers of this crucial dimension, and the way to integrate it in the PMS’ implementation. Moreover, we also found that an organizational dimension is positively perceived by managers as a key driver to support their implementation process. These key concerns allowed to guide the definition of the strategic value drivers in the following related perspectives. This implies an important step helping to drive and support future studies and managerial practices to integrate the environmental, social, economic, cultural and organizational dimensions in the corporate governance.

Considering the second research question (RQ2), we provided a five-dimensional model aimed to support researchers and managers in analyzing and implement sustainable strategies. We found that a systematic integration of the sustainability key value drivers, in an early stage of the PMS, positively impacts on the company’s performance. Therefore, the connection described allows a strategic alignment of the cultural, organizational and TBL, promoting SD at the theoretical and practical levels. The framework provided can be considered of interest to practitioners dealing with SD issues at a strategic level, oriented to support decision-making process. A digitalized model can be a software solution providing managers with a tool to support their managerial activities.

In this process, to implement this idea in practice, relevant role is covered by the sustainable KPIs, which need to be addressed by the future studies. More effort is required to identify the relationship between sustainable KPIs and the company’s performance, in view of the dimensions analyzed. The KPI system needs to be structured according to the value drivers generated for each dimension.

Managers and researchers still cannot conclude clearly which KPIs are positively connected to the performance of the company. Further investigation aimed to explore the effectiveness of the indicators on the overall performance of the company is required. Thus, more attention should be paid by future studies and managerial practices on the use, selection, and monitoring of the sustainable indicators.

Accordingly, our paper contributes to expand the existing knowledge on the topic, by providing an additional step on the work done to date by the previous studies on the research filed, and therefore the opportunity to further improve the results achieved here.

6.2 Missing concepts and future directions

Findings pointed out further validation that some relevant issues of integrating sustainability are missing still in the companies’ mission and vision. In particular, on the one hand, a scarce comprehension of sustainability objectives, and on the other hand an unbalanced ratio between objectives that are short-term oriented and the long-term ones. Improving sustainability performance requires not only the right proportion of quantitative and qualitative indicators, but also balancing them over time, allowing the company to constantly grow in a given direction. In addition, we found that the commitment of the management in this phase is crucial to achieve the success of the tool. Manager have to involve all members of the company in the implementation, evaluation and refining process.

Moreover, the effectiveness of the integration between sustainability and strategy lacks a comprehensive analysis in terms of empirical research focusing on the positive impact on the performance. This could be considered one of the scientific challenges to the SD connected research, as the measuring of value created from the sustainable strategy is crucial in the decision to integrate dimensions discussed in this paper. In addition, to improve the evidence provided here, and promote the development of the managerial practices, future research could apply the integrated model in different companies, sectors and countries using a multiple case study approach.

Our analysis indicates that, in the recent years, an increasing interest in the integration between sustainability and PMS is demonstrated, destined to grow further and considerably in the near future.

Notes

Online database containing financial, personal and commercial information on over 500,000 joint-stock and financial companies in Italy.

References

Adams, C. A., & Frost, G. R. (2008). Integrating sustainability reporting into management practices. Account Forum, 32, 288–302. https://doi.org/10.1016/j.accfor.2008.05.002

Anderson, S. W., & Widener, S. K. (2006). Doing quantitative field research in management accounting. Handbooks of Management Accounting Research, 1, 319–341.

Bellucci, M., Nitti, C., Chimirri, C., & Bagnoli, L. (2019). Rendicontare l’impatto sociale. Metodologie, Indicatori e Tre Casi Di Sperimentazione in Toscana, Management Control, 3, 166–187. https://doi.org/10.3280/MACO2019-003009

Bhattacharyya, A., & Cummings, L. (2015). Measuring corporate environmental performance-stakeholder engagement evaluation. Business Strategy and Environment, 24, 309–325. https://doi.org/10.1002/bse.1819

Bortolotti, T., Boscari, S., & Danese, P. (2015). Successful lean implementation: Organizational culture and soft lean practices. International Journal of Production Economics, 160, 182–201. https://doi.org/10.1016/j.ijpe.2014.10.013

Brinkmann, S., & Kvale, S. (2008). Ethics in qualitative psychological research. The Sage Handbook of Qualitative Research in Psychology, 24(2), 263–279.

Busco, C., & Quattrone, P. (2014). Exploring how the balanced scorecard engages and unfolds: Articulating the visual power of accounting inscriptions. Contemporary Accounting Research, 32(3), 1236–1262. https://doi.org/10.1111/1911-3846.12105

Cardoni, A., Zanin, F., Bartolacci, F., & Tompson, G. H. J. (2018). Strategic planning for value creation in business networks. Conceptual Framework and Theoretical Proposals, Management Control, 1, 17–44. https://doi.org/10.3280/MACO2018-00100

Chen, Y., Jermias, J., & Panggabean, T. (2016). The role of visual attention in the managerial judgment of balanced-scorecard performance evaluation: Insights from using an eye-tracking device. Journal of Accounting Research, 54(1), 113–146. https://doi.org/10.1111/1475-679x.12102

Chenhall, R. H. (2005). Integrative strategic performance measurement systems, strategic alignment of manufacturing, learning and strategic outcomes: An exploratory study. Accounting, Organizations and Society, 30(5), 395–422. https://doi.org/10.1016/j.aos.2004.08.001

Cinquini, L., & Mitchell, F. (2005). Success in management accounting: Lessons from the activity-based costing/management experience. Journal of Accounting & Organizational Change, 1, 63–78.

Clementino, E., & Perkins, R. (2021). How do companies respond to environmental, social and governance (ESG) ratings? Evidence from Italy. Journal of Business Ethics, 171(2), 379–397.

Dai, N. T., Free, C., & Gendron, Y. (2019). Interview-based research in accounting 2000–2014: Informal norms, translation and vibrancy. Management Accounting Research, 42, 26–38. https://doi.org/10.1016/j.mar.2018.06.002

De Villiers, C., Rouse, P., & Kerr, J. (2016). A new conceptual model of influences driving sustainability based on case evidence of the integration of corporate sustainability management control and reporting. Journal of Cleaner Production, 136, 78–85. https://doi.org/10.1016/j.jclepro.2016.01.107

Eisenhardt, K. M., & Graebner, M. E. (2007). Theory building from cases: Opportunities and challenges. Academy of Management Journal, 50(1), 25–32. https://doi.org/10.5465/amj.2007.24160888

Evans, J. H., Feng, M., Hoffman, V. B., Moser, D. V., & van der Stede, W. A. (2015). Points to consider when self-assessing your empirical accounting research. Contemporary Accounting Research, 32(3), 1162–1192. https://doi.org/10.1111/1911-3846.12133

Farias, L. M. S., Santos, L. C., Gohr, C. F., Oliveira, L. C., & Amorim, M. H. (2019). Criteria and practices for lean and green performance assessment: Systematic review and conceptual framework. Journal of Cleaner Production, 218, 746–762. https://doi.org/10.1016/j.jclepro.2019.02.042

Ferreira, L. D., & Merchant, K. A. (1992). Field research in management accounting and control: a review and evaluation. Accounting, Auditing & Accountability Journal, 5(4), 65–79.

Ferreira, A., & Otley, D. (2009). The design and use of performance management systems: An extended framework for analysis. Management Accounting Research, 20(4), 263–282. https://doi.org/10.1016/j.mar.2009.07.003

Figge, F., Hahn, T., Schaltegger, S., & Wagner, M. (2002). The sustainability balanced scorecard-linking sustainability management to business strategy. Business Strategy and the Environment, 11(5), 269–284. https://doi.org/10.1002/bse.339

Fry, L. W., & Slocum, J. W. (2008). Maximizing the triple bottom line through spiritual leadership. Organizational Dynamics, 37(1), 86.

Gond, J.-P., Grubnic, S., Herzig, C., & Moon, J. (2012). Configuring management control systems: Theorizing the integration of strategy and sustainability. Management Accounting Research, 23(3), 205–223. https://doi.org/10.1016/j.mar.2012.06.003

Hristov, I., Chirico, A., & Ranalli, F. (2021). Corporate strategies oriented towards sustainable governance: Advantages, managerial practices and main challenges. Journal of Management and Governance, 26(2022), 75–97.

Hristov, I., & Appolloni, A. (2021). Stakeholders’ engagement in the business strategy as a key driver to increase companies’ performance: Evidence from managerial and stakeholders’ practices. Business Strategy and the Environment, 30(8), 1–16.

Hristov, I., & Chirico, A. (2019). The role of sustainability key performance indicators (KPIs) in implementing sustainable strategies. Sustainability, 11(20), 5742.

Hristov, I., Chirico, A., & Appolloni, A. (2019). Sustainability value creation, survival, and growth of the company: A critical perspective in the sustainability balanced scorecard (SBSC). Sustainability, 11(7), 2119. https://doi.org/10.3390/su11072119

Hsu, F. J., & Chen, Y. (2015). Is a firm’s financial risk associated with corporate social responsibility? Management Decision, 53, 2175–2199. https://doi.org/10.1108/MD-02-2015-0047

Hubbard, G. (2009). Measuring organizational performance: Beyond the triple bottom line. Business Strategy and the Environment, 18, 177–191. https://doi.org/10.1002/bse.564

Jensen, M. (2001). Value maximisation, stakeholder theory, and the corporate objective function. European Financial Management, 7(3), 297–317. https://doi.org/10.1111/1468-036x.00158

Kaplan, R. S., & Norton, D. P. (1992). The balanced scorecard: measures that drive performance. Harvard Business Review, 70(1), 71–79.

Lebas, M., & Euske, K. (2002). A conceptual and operational delineation of performance. Business Performance Measurement: Theory and Practice, 65–79. https://doi.org/10.1017/cbo9780511753695.006

Lewandowski, S. (2017). Corporate carbon and financial performance: The role of emission reductions. Business Strategy & Environment, 1211, 1196–1211. https://doi.org/10.1002/bse.1978

Linnenluecke, M. K., & Griffiths, A. (2010). Corporate sustainability and organizational culture. Journal of World Business, 45(4), 357–366.

Lipe, M. G., & Salterio, S. E. (2000). The balanced scorecard: Judgmental effects of common and unique performance measures. The Accounting Review, 75(3), 283–298. https://doi.org/10.2308/accr.2000.75.3.283

Lisi, I. E. (2015). Translating environmental motivations into performance: The role of environmental performance measurement systems. Management Accounting Research, 29, 27–44.

Lokuwaduge, C. S. D. S., & Heenetigala, K. (2017). Integrating environmental, social and governance (ESG) disclosure for a sustainable development: An Australian study. Business Strategy and the Environment, 26(4), 438–450.

Maas, S., & Reniers, G. (2014). Development of a CSR model for practice: Connecting five inherent areas of sustainable business. Journal of Cleaner Production, 64, 104–114.

McWilliams, A., & Siegel, D. (2000). Corporate social responsibility and financial performance: Correlation or misspecification? Strategic Management Journal, 21(5), 603–609.

Morioka, S. N., & de Carvalho, M. M. (2016). A systematic literature review towards a conceptual framework for integrating sustainability performance into business. Journal of Cleaner Production, 136, 134–146. https://doi.org/10.1016/j.jclepro.2016.01.104

Morrow, D., & Rondinelli, D. (2002). Adopting corporate environmental management systems: Motivations and results of ISO 14001 and EMAS certification. European Management Journal, 20(2), 159–171.

Naciti, V., Cesaroni, F., & Pulejo, L. (2021). Corporate governance and sustainability: A review of the existing literature. Journal of Management and Governance, 26(2022), 55–74.

Nørreklit, H. (2000). The balance on the balanced scorecard a critical analysis of some of its assumptions. Management Accounting Research, 11(1), 65–88. https://doi.org/10.1006/mare.1999.0121

Trianni, A., Cagno, E., Neri, A., & Howard, M. (2019). Measuring industrial sustainability performance: Empirical evidence from Italian and German manufacturing small and medium enterprises. Journal of Cleaner Production, 229, 1355–1376. https://doi.org/10.1016/j.jclepro.2019.05.076

Wu, L., Subramanian, N., Gunasekaran, A., Abdulrahman, M. D. A., Pawar, K. S., & Doran, D. (2018). A two-dimensional, two-level framework for achieving corporate sustainable development: Assessing the return on sustainability initiatives. Business Strategy and the Environment, 27(8), 1117–1130.

Acknowledgements

The authors would like to thank all managers for their cooperation, thoughtful support, collaboration, and valuable comments and also the University of Rome Tor Vergata, Department of Management and Law, for project funding.

Funding

Open access funding provided by Università degli Studi di Roma Tor Vergata within the CRUI-CARE Agreement.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

This article has been corrected: Funding note has been updated.

Appendix: Questionnaire used

Appendix: Questionnaire used

Section 1–sustainability dimensions |

1. What do you think of the role of sustainability in the PMS? |

2. Are managers interested in implementing strategy oriented to sustainable development (SD)? |

3. Based on your personal experience, what are the main sustainability dimensions which need to be integrated in the corporate strategy to achieve SD? |

4. What are your perception on the relevance of these dimensions in implementing corporate strategy? |

5. Can you discuss the sustainability dimensions mostly used in practice? |

Section 2–key value drivers |

6. According to the dimensions emerged by Sect. 1 of this questionnaire, please provide a maximum three key drivers for each of them |

7. What do you think about the role of cultural change in the value creation process? |

8. How this dimension impacts on the company’s performance? |

Section 3 –critical issues and challenges related to the sustainable integration |

9. Can you talk about the critical issues connected to this integration process between sustainability and corporate strategy? |

10. How can the criticalities linked to the integration process, be overcome? |

11. What do you think about the integration achieved in your company? |

12. What are the management tools used to integrate sustainability at a strategic level? |

13. How sustainability strategies impacted on your performance? |

14. How can a sustainable PMS framework be implemented? |

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visithttp://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Hristov, I., Chirico, A. The cultural dimension as a key value driver of the sustainable development at a strategic level: an integrated five-dimensional approach. Environ Dev Sustain 25, 7011–7028 (2023). https://doi.org/10.1007/s10668-022-02345-z

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10668-022-02345-z