Abstract

Several European countries plan to phase out coal-fired power plants in order to reach their greenhouse gas abatement targets. Additionally, the phase-out will bring about so-called ancillary effects or co-effects. In our study, we focus on the co-effects induced in the countries that export coal to Europe. Furthermore, we examine the ancillary effects imposed on China as a major supplier of technologies (like solar energy technologies) that will replace coal-fired power plants. Using a combination of an input-output model, econometric analysis and employing the concept of the United Nations’ Sustainable Development Goals, we assess impacts of coal phase-out policies on environmental, economic, and societal dimensions. Our results show that despite negative impacts on income and employment in coal-exporting countries, a phase-out of coal-fired power plants is linked with multiple positive effects. In particular, we observe improvements in water management and biodiversity conservation, reduced release of pollutants, and improvements on a societal level. However, even if we consider a reduction in the use of coal in the European steel production sector as an additional challenge, these positive impacts on coal exporting countries remain rather small. The same applies to the effects we observe for China.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

At the 21st Conference of the Parties (COP) of the UNFCCC in Paris, it was agreed that measures should be taken to limit global warming to well below 2 degrees Celsius. In response to the Paris Agreement, the Canadian and the British governments launched at the COP23 in Bonn in 2017 the Powering Past Coal Alliance supporting the phase-out of coal-fired power plants. Currently, the alliance consists of 34 national governments (incl. e.g., France, Germany, Italy, Netherlands and the United Kingdom), 35 sub-national governments (e.g., Australian Capital Territory, New York, Wales and Washington), and 44 businesses or organizations (e.g. Iberdrola, Marks and Spencer, and Unilever) (Powering Past Coal Alliance, 2021). In the European Union (EU28), about 19% (2018) of electricity is produced in coal-fired power plants (Eurostat, 2020c). Coal-fired power plants contribute 22% to the EU’s overall greenhouse gas (GHG) emissions (UNFCCC, 2021). Hence, a phase-out of coal-fired power plants in the EU will lower GHG emissions significantly.

In the year 2018, 650 million tonnes of coal were consumed in the EU. The power sector’s share was 74%. 27% of the coal was imported (Eurostat, 2020d). The countries of origin include industrialized countries such as the USA, emerging economies, e.g. Russia, and developing countries such as Colombia and South Africa (Eurostat, 2020b). A phase-out of coal-fired power plants in Europe will have effects on these coal-exporting countries. Examples of possible impacts include changes in export revenues and employment. Impacts are not restricted to economic aspects, but also include societal and environmental effects which can either hamper or foster sustainable development of the affected countries.

With respect to the overall impact of a phase-out of coal-fired power plants in Europe, an assessment should include information on primary benefits (i.e. benefits from pursuing the policy’s main goal of climate protection), as well as on co-effects (e.g. effects on environmental protection, human health, or gender equality) (Buchholz et al., 2020). In the following, we assess the broad range of impacts of a phase-out of coal-fired power plants in the EU. We examine the influence on reaching the UN Sustainable Development Goals (SDGs) and thereby include economic, social and environmental aspects. By employing the list of the SDGs of the United Nations (United Nations, 2020), the analysis includes an assessment of factors like reduction of poverty, improvement of health and well-being, use and release of water, responsible consumption and production, changes in biodiversity, decent jobs and economic growth. In particular, we focus on the following research questions:

-

How does phasing-out coal-based value chains affect industrialized and developing countries? Which countries will be affected the most by the phasing-out? To which extent will changes in the steel industry (a decline in the production using coal-based technologies) enhance the impacts?

-

To which extent will a change in the use of coal in Europe affect the attainment of SDGs on a global scale?

For economies like those of South Africa, India, Indonesia, Australia and Colombia, coal mining plays a prominent role. But their societies and the environment are also significantly affected by coal mining (see e.g., World Bank, 2020; Spencer et al., 2018). Earnings from mining activities are influencing well-being (Poudyal et al., 2019) and lifestyle (Cardoso, 2015). Examples of the impacts of mining on the environment are natural resource depletion, massive interventions in water regimes and the landscape (see e.g., Sinha et al., 2017; Park et al., 2020; Mudd, 2010). Monteiro et al. (2019) employ the SDG list and review articles with respect to the impacts of mining on the SDGs. The authors conclude that mining affects a broad range of SDGs. Challenges for the coal sector resulting from the transition of the energy system are highlighted in an aggregated way by e.g. Oei and Mendelevitch, (2019); Haftendorn et al., (2012).

In recent decades, several approaches have been developed to assess the impacts of technological, economic and policy changes on SDGs. Barbero-Vignola et al. (2020) and Allen et al. (2016) clustered the approaches into input–output, top-down econometric, computable general equilibrium (CGE), system dynamics, bottom-up optimization/partial equilibrium, bottom-up simulation, multi-agent and hybrid models.

Input-output (IO) models are based on so-called input-output tables. These tables contain information on financial flows between different economic sectors. In contrast to other top-down approaches, the number of sectors is relatively high. By adding information on environmental and social aspects, the IO approach can be applied to analyze the impacts of changes in financial flows on SDGs (Tukker et al., 2013). As Barbero-Vignola et al. (2020) point out, the results of IO analysis are easy to interpret. IO models are mostly used for short term analyses since the assumed fixed input-/output ratios restrict the consideration of dynamics, including the feedback from changes in prices (Miller & Blair, 2009).

Macro-econometric models are based on the assumption that historical relations and dynamics will still prevail in the future. For their calibration, a great amount of historical data is necessary. Upward and downward trends in development, data and time gaps, as well as occurrences of black swans, restrict the identification of a significant number of parameters. Hence, macro-econometric approaches are used rather rarely for SDG assessments (see e.g., Hedenus et al., 2013; Rocchi et al., 2019). Dynamic computable general equilibrium (CGE) models, in contrast, are well-suited. CGE models focus on market equilibria. Hence, special attention is paid to impacts of changes in prices on demand and supply for goods and vice versa. However, Barbero-Vignola et al. (2020) stress the lack of historical validation and the large-scale modelling, as drawbacks for the use of CGE approaches (see e.g., Böhringer & Löschel, 2006; Capros et al., 2013). System dynamics models are usually used to analyze the development of systems by taking into consideration feedback loops (Ford, 1999; Forrester, 1971). They are mainly employed for the analysis of smaller systems. Critics focus on the definition of correct boundaries and feedback loops (Barbero-Vignola et al., 2020). Bottom-up optimization and simulation models focus on technological developments on the sectoral level. Accordingly, they are not suitable for capturing influences on the overall economy level (see e.g., Allen et al., 2016; Vandyck et al., 2018). Multi-agent models stress the importance of interaction between individual actors. They can quickly become quite complex (Wieland & Gutzler, 2014). Regarding the analyses of SDGs, they are currently rarely used. Hybrid and integrated assessment models have been developed to overcome the limitations of the approaches mentioned above, to extend the system boundaries and to combine the strengths of different approaches (see e.g., Rodríguez-Serrano et al., 2017; Mohebali et al., 2019). Still, the calibration of these models can be challenging (see e.g., Capros et al., 2013; Hourcade et al., 2006).

By scanning 80 different modelling approaches, Allen et al. (2016) show that the approaches mainly focus on environmental-economic aspects. They conclude that the “modelling of social variables can … also be considered as an important gap in modelling capabilities” (Allen et al., 2016, p. 9). Barbero-Vignola et al. (2020) support the conclusions drawn by Allen et al. (2016). After assessing their broad set of models, Barbero-Vignola et al. (2020, p. 30) state that: “here is a need to extend the SDG framework through an integrated modelling framework under the umbrella of the SDGs”.

By using the phase-out of coal-fired power plants in the EU as an example, we investigate the research questions outlined above. Since the use of IO models for SDG assessment is widespread and often serves as the core for other, more extensive approaches, we will employ this type of modelling.

The paper is organized as follows: In Section 2, we give an overview of the SDG concept. Section 3 focuses on the current coal demand and supply in Europe. In Section 4, we describe the approach we apply for linking the developments in the coal sector with SDGs. Results are presented and discussed in Section 5. Section 6 concludes.

2 Sustainability as a guiding goal

2.1 Preliminary remarks

Reaching the goals of the Paris Agreement will require restructuring many emission-intensive sectors, such as heavy industry, transportation, and energy. At the same time, the reduction of emissions must be sustainable, meaning that the three dimensions of sustainability, namely (i) environmental, (ii) social and (iii) economic aspects have to be taken into account. The United Nations (2020) formulated seventeen sustainability goals to guide global change (Table 1).

In order to make the goals more concrete and tangible, 169 targets were defined. Within these targets, however, a further distinction can be made. There are 81 process targets, aimed at facilitating the goals’ achievement. Furthermore, there are 88 outcome targets, indicating desirable results (UNDP, 2017). Each target is assigned to a specific SDG. The differentiation between outcome and process targets is done by a number or letter (i.e., the first outcome target of SDG is described with 1.1, the first process target with 1.a).

Although the formulation of the associated targets makes the SDGs less abstract, indicators must be defined for sufficient measurability of target achievement, which can provide information on the developments concerning the respective targets and with it concerning the SDGs. In total, more than 200 indicators were defined to help describe national progress on the SDGs and their targets. However, the challenge of measuring these signs of progress is not unencumbered by disputes. Therefore, the following Sect. 2.2 takes a closer look at the problems involved and possible solutions.

2.2 Relevance and challenges of SDG measurement concepts

In general, the concept of SDGs is designed as an all-encompassing vision that links the aspects of economy, society, and environment. As these aspects in turn represent broad concepts with many interlinkages and connections, dependencies and interactions, this complexity is also passed on to the discussion of SDGs. Created as a supranational guideline, the interests of many different stakeholders are combined within the SDG concept. Economic prosperity, societal welfare and sustainable development interact, create synergies, and generate conflicts across the political agenda (see e.g., Fukuda‐Parr, 2019; Lafortune et al., 2020; Guzel et al., 2021). The high relevance of the SDGs stems from all of these characteristics, but especially from the fact that the SDGs represent a general consensus agreed upon by all parties in the UN (Fukuda‐Parr and McNeill, 2019; United Nations, 2020).

Under the main objective that all interests are met in a sustainable way, goals, targets, and indicators that follow this consensus can be developed. However, this advantage in the SDG’s conception is also its inherent weakness. The assessment of the goals and targets, and finally, the degree of success in meeting the guidelines based on the given indicators follows the viewpoint of the analyst. This is because of different priorities resulting from the choice of different technocratic methodologies (in particular, if they influence the scope of what is measured, especially when goals are societal in nature (Fukuda‐Parr and McNeill, 2019)).

Nevertheless, while the SDGs symbolize an important global consent on sustainability, the concept also struggles with several difficulties arising from the system’s complexity. Concerning SDG measurement methods (see e.g., Bidarbakhtnia, 2019), Fukuda‐Parr and McNeill (2019) and Unterhalter (2019) argue that conventional measuring approaches experience difficulties and reach an impasse when dealing with the SDGs, as some goals and concepts are difficult to measure comprehensively in numbers (e.g. education). In addition, the achievement of individual goals, which is used to measure the overall level of success, can be evaluated positively or negatively depending on the measurement system. This can be explained by the methodological approaches, which have different measurement bases and objectives. This creates a kind of tunnel vision, which depends on the investigator’s perspective. For example, the OECD focuses more on the economy, meaning that high-income countries generally perform better because of the mostly economically oriented indicators. When using other systems, they may actually not perform as well (Lafortune et al., 2020).

Fukuda‐Parr and McNeill (2019) further state that the meaningfulness of the goals alone does not make the indicator set flawless. The reason for this is that the indicators may deviate from the actual goal, as they may be difficult to measure or there is limited data available to measure them. In the pursuit of meeting key performance indicator targets, misaligned incentives can occur that distract from the actual goal. Further challenges in working with SDGs measurement systems are that the indicators suggested are often consisting of multiple sub-indicators, making transparent differentiation difficult. Often, data sources are mixed and there exists no consent about the data sources in all countries, as some of the values for indicators are not available. Data may be not recorded and thus cannot be obtained and used for measuring and making comparisons, data quality may be lacking and a coherent system of metrics or definitions for all countries is missing. This leads to am incomparability of results across countries. The possibility of incomparability has to be taken into account in any framework. Accordantly, its consideration is an important requirement of any methodology established for evaluating the achievement of SDG targets and indicators (compare European Comission, 2020).

El‐Maghrabi et al. (2018) list another set of important points to consider. Furthermore, they explain that consistency in the methodology for measuring the SDGs is elementary and that targets are often interdependent, leading to positive or negative correlations. At the same time, repeated use of an indicator to measure different goals can in turn result in the correlation of goals. This becomes especially apparent with goals 6 to 12. The concept of path-dependency helps to identify and explain diverging results in country-specific SDG achievement.

Breuer et al. (2019) present a comprehensive overview of the challenges in the methodological assessment of SDGs. They conclude that replicability, rigour in the assessment, and an informed decision by policymakers concerning the ranking are indispensable. Another reason for the challenges of working with SDGs can be explained by considering them as “wicked problems”: As they lack clear formulation, available information is misleading, and stakeholders have conflicting values (see e.g., Eden and Wagstaff, 2020; McCall and Burge, 2016; Crowley and Head, 2017; Peters and Tarpey, 2019). Furthermore, the goals themselves cannot be classified as true or false, they are just good or bad. In addition, as this classification is based on normative rather than empirical criteria, this poses a challenge to policymakers, because they are accountable for the success or failure of the “wicked problems”.

The degree of the goals’ complexity, together with their partly nebulous quality in terms of their definition, hampers consistent assessment. Nevertheless, there exist possibilities to deal with the SDGs and assessment methods. The recognition of the methodology constraints and the role of the indicators allow for more comprehensive analyses. The reason for this is not only that there is a variety of proposed indicator concepts that can be applied, but, also, the fact that the need for these indicators is confirmed at supranational level is itself a powerful factor (see e.g., Fukuda‐Parr (2019) and Eden and Wagstaff (2020)).

For Europe, as an aggregate of predominantly highly developed countries, the coal phase-out is an important step towards a sustainable energy future. Related measures may strive for the attainment of specific SDGs, but simultaneously induce indirect impacts on other SDGs Non-EU countries are also impacted by the European coal phase-out, (mainly the countries exporting coal to Europe). IO analysis is able to trace the effects of a coal phase-out through the whole value chain and further allows to give a comprehensive view of the impacts of coal consumption of nations. With the help of IO analysis, reductions in European coal dependency (consumption) can be traced back along the way to its origin. Effects identified by executing the IO analysis can be measured via indicators pointing to the SDGs. These effects may not only be one-directional but may affect different economic, societal, and political sectors on multiple levels (see e.g., Bjelle et al., 2020; El-Maghrabi et al., 2018).

3 Coal demand and supply in Europe

3.1 Preliminary remarks

The EU represents an important sales market for coal. Its overall consumption of coal was roughly 650 million tonnes in 2018 (Eurostat, 2020d). With a share of 63%, steam coal dominates the coal imports. Coking coal has a share of 27% in coal imports and ranks second (Eurostat, 2020a). Steam coal is mainly used for the generation of heat and electricity, while the use in coke ovens for steel production is negligible. On the other hand, coking coal is primarily used for steel production and the share of its use in coking ovens is relatively steady (see Fig. 1). Domestic production of coking coal only plays a minor role and its share steadily decreased over the past 40 years. While coal already plays only a minor role in the electricity sector in many member states (e.g., Belgium, France, Sweden), some countries (e.g., Czech Republic, Germany, Poland, The Netherlands) still rely heavily on coal-fueled power plants (Eurostat, 2020a). The coal consumption of Germany accounts for 233 million tonnes. About 78% of the coal is used for electricity production and about 12% for steel production. For Poland’s power plants, each year about 102 million tonnes of coal is needed which corresponds to 75% of the national coal demand. The Czech Republic ranks third in Europe with respect to the demand for coal. Like in Germany and Poland, coal is mainly used for electricity generation. In 2019, the share of lignite and hard coal in gross electricity generation in the EU-28 states was about 22% and emissions from coal-fired power plants (hard coal and lignite combined) accounted for 31% of EU ETS emissions (Agora and Sandbag, 2020).

Development of import and consumption of coal (EU 28). Source: (Eurostat, 2020a)

Figure 1 shows the development of coal consumption in Europe and of the share of coal imports in the recent years. It can be observed that the share of coal imports in the generation of heat and electricity has been decreased slowly during the past 30 years. At the same time, inland production dropped sharply making Europe more and more dependent on coal imports.

3.2 Demand for coal

3.2.1 Electricity sector

Due to their ambitious GHG emission reduction targets, many member states within the EU are striving to phase-out coal-fired power plants (European Comission, 2019). Table 2 lists exit plans of individual states. Furthermore, it displays their coal consumption in the power sector and sets this consumption in relation to imports.

Based on the information presented in Table 2, countries can be classified in groups concerning their share of imported coal and the share of the power sector in total coal consumption across all domestic sectors of the national economy (IEA, 2019). In the first group, the power sector accounts for the largest share of coal use among economic sectors but has low dependence on coal imports: e.g., Germany and Poland. Their power sectors rely strongly on the use of domestic coal resources. Their planned phase-out horizon is the longest among those of the listed European countries. In the second group, countries are heavily dependent on coal imports, but the coal use of their power sector is comparatively low: e.g., Austria, France, and Sweden. The phase-out takes place in near future. In the third group, countries are dependent on coal imports and have a significant share of the power sector in total coal uses in all economic sectors (for classification of coal types see Annex Fig. 10). These countries form the majority among the states listed in Table 2. Portugal and Denmark are the outermost representatives of this group with the strongest import dependence. Ireland follows them with a lower share of the power sector in total coal consumption. Coal phase-out policies in this group of countries will have a significant impact on reducing coal import flows to Europe in the next decade.

3.2.2 Steel industry

As mentioned above, coking coal is mainly used in the production of steel (IEA, 2020a). With its high demand for coal, the steel industry belongs to the CO2 intensive industries and is a major contributor to the EU ETS emissions. As a sector with high relevance for CO2 emissions, the steel industry is in the focus of GHG reduction efforts (see e.g., BMWi, 2020; IEA, 2020a). These efforts aim to reduce the use of coking coal or increase the capture and storage of CO2 emissions. Both measures are resulting in similar reductions of CO2 emission but differ with respect to their effects on the demand for coal. In its study on the steel industry Material Economics (2019) presented two scenarios which could serve as examples for future pathways of steel production in the EU (Fig. 2).

Futures for steel production. Remarks: Primary steel with CCS/U means that coking coal is used Source (Material Economics, 2019)

In the “New Processes Pathway” scenario, the conventional coal-based production route (“unabated primary steel production”) will more and more be replaced by a new production route which is based on hydrogen (“hydrogen—direct reduction H-DRI”) and by an increase in the use of the secondary steel route (“recirculated steel with electric arc furnaces (EAF)”). In the second scenario, it is assumed that carbon capture and storage (CCS) and/or carbon capture and utilization (CCU) will be implemented as CO2 reduction measure, which implies that coal will still be used for steel production.

CO2 reduction is only one of the challenges the steel industry in Europe is faced with. Another challenge arises from increasing competition in the international steel market. In particular, overcapacities and cost gaps between steel produced in Europe and China threaten the European steel industry. Hence, there are doubts whether European steel production can be kept on the current level in the future (see e.g., Vögele et al., 2020).

3.3 Coal supply

Figures 3 and 4 illustrate Europe's imports of steam, anthracite, and coking coal by country of origin. It can be observed that coal imports of individual European countries originate mainly from outside Europe. Colombia and Russia are the most important exporters of steam coal and anthracite in this context, followed by the USA and South Africa. In contrast, the United States and Australia are the largest exporters of coking coal to Europe. Consequently, European coal imports stem from both developed and developing countries.

Europe’s imports of anthracite and other bituminous coals. Source (Eurostat, 2020b)

Coking coal imports to Europe

4 Methodology

In order to assess the extent to which changes in European coal demand affect other countries in terms of their SDGs, we employ several different indicators. A significant share of these indicators relates to developments at the national level and can hardly be linked to individual industries or actors. At the same time, at the local level, the activities of individual companies can have significant impacts on the environment, and local economic and societal factors. An appropriate assessment of the impact of a European coal phase-out on sustainability goals in coal-exporting countries must take this multi-level character into account. Hence, we employ a multi-level approach to look at the impacts both aggregate at the national level and in detail at the local level.

Our approach consists of three “levels” representing different scales:

-

Level 1: In a first step, we focus on developments on the sectoral level. Accordantly, we are looking at impacts resulting from changes in activities of industries by using average data on activities and their consequences for selected economic sectors.

-

Level 2: In addition to indicators being strongly related to a specific sector, we assume that these impacts are related to economic activities in general. This level investigates the impacts on all economic sectors involved in the value chain of coal production.

-

Level 3: In principle, on-site production can cause impacts that differ from the average of the corresponding sector. To account for such effects, we extend the analysis by looking more closely at the local impacts of coal-producing sites.

The impacts at Level 1 are assessed by using an input–output approach. With this approach, it is possible to take direct and indirect links between countries and between sectors into consideration (see e.g., Miller & Blair, 2009). Besides information on production values and employment, the approach can be used to assess e.g., impacts on water consumption and emissions (see e.g., Tukker et al., 2013). By using information on overall economic activities, we draw conclusions on SDGs at Level 2. Information on impacts at Level 3 is derived from literature reviews focusing on specific coal mining sites. In the following, we take a closer look at the approaches we will use for the assessment of the level-specific impacts.

4.1 Assessment of impacts on sectoral level (Level 1)

We employ a standard IO approach and assume linear-limitational production functions (Miller & Blair, 2009). The production of one unit of good i always requires a fixed amount of goods (inputs) from \(1\) to n. Therefore, goods are used both as intermediate inputs for the production in industrial sectors and as commodities satisfying the so-called final demand. Final demand consists of the demand of private households, the demand of the government, exports as well as demand for investment goods.

with Xi: output of industry I ; \(a_{ij}\): intermediate input coefficient describing how much intermediates from industry i are needed to produce a unit of output of industry j.; ; Yi: output of sector i used as final demand

Using matrix notation, the equation reads:

with X: vector of outputs Xi, i =1 to n; A: matrix with intermediate input coefficients; Y:final demand vector

By activating the equation towards X, we get Eq. (3).

Hence, with a given vector Y, it is possible to calculate related direct and indirect production effects.

Regarding social and environmental effects as well as additional economic factors, we assume that they are directly linked to economic activities of the industrial sectors and final demand in a fixed ratio. Hence, increased production of a good or services goes hand in hand with an increase in the related stress factors.

A well-established database being used for environmental oriented IO analysis is EXIOBASE (Tukker et al., 2013). EXIOBASE was introduced in 2012 as a database for analyzing emissions and resources extraction as well as economic impacts related to economic activities. It is a so-called Multi-Regional Environmentally Extended Input–Output Table. The newest version of EXIOBASE contains information on 44 countries, 5 Rest of World regions, 200 products, 163 industries, 3 employment skill levels per gender, 417 emission categories and 662 material and resources categories (Stadler et al., 2018). A second source that is widely in use, is the World Input–Output Database (WIOD) (Timmer et al., 2015). The first version of WIOD was published in 2012. The newest was released in 2016. Besides information on economic flows between 56 industries located in 43 countries, the new database includes satellite accounts with 16 socio-economic indicators (Timmer et al., 2015). Unfortunately, the most recent version was published without satellite accounts containing e.g., environmental data. Hence, for environmental analysis, the release from 2013 has to be used which provides information on 8 kinds of emissions and 25 other environmental indicators (incl. e.g., uses of materials and resources). The two databases differ with respect to the number of countries, classification of sectors and selection of additional indicators. In EXIOBASE, for example, “Anthracite”, “Coking coal”, “Other bituminous coal” and “Sub-bituminous coal” are listed as sectors dealing with extraction of coal, whereas in WIOD, all mining activities belong to the sector “Mining”. Since the databases complement each other to some extent, we decided to use both for our analysis. However, even if we use both databases, we will neither be able to address all SDGs nor to calculate all indicators which are usually used for the assessment of SDGs on national levels (Table 3). In the following, we show how these gaps can be closed by extending the approach.

For the analysis at Level 1, we need to mention the limitations of the IO table-based method. Even if EXIOBASE and WIOD provide information on a great number of sectors and countries, the aggregation level is still high. In particular, we have to work with averaged data for economic sectors, which makes it difficult to assess technology-specific impacts. An important limitation arises from missing detailed information for some countries. This limitation is overcome by clustering them into regions while reducing the degree of disaggregation. Further problems arise due to data inconsistencies ranging from changes in classifications to changes in the underlying accounting concepts over time. However, a complementing multi-level approach can help to alleviate related limitations of the IO approach.

4.2 Assessment of impacts on the value chain on an aggregated level (Level 2)

In the year 2016, the Bertelsmann Stiftung and the Sustainable Development Solutions Network (SDSN) introduced a concept of SDG scores assessing the achievement of SDGs. The scores indicate the percentage of achievement of a specific SDG in a selected country. A value of 100 means that the country has fully reached the SDG. A value lower than 100 indicates that there is still something to do (Sachs et al., 2019). In the following, we use the SDG score approach for closing data gaps.

In a first step, we test if gross domestic product (GDP) can be used as explaining variable for SDG scores. Since economic activities are directly and indirectly responsible for every change in the sustainability indicators, we assume as hypothesis that SDG scores and GDP should be correlated. Hence, changes in GDP (caused e.g., by lower coal exports) impact the sustainability indicators. Equation (5) reflects this link.

with \(X^{i} = \ln \left( {\frac{GDP}{{capita}}} \right);\)sdj: SDG Score Index; \(\alpha_{ij}\), \(\beta_{j}\): parameters of the regression function (see Table 4).

\(\alpha_{ij}\) and \(\beta_{j}\) are calculated based on the database of Bertelsmann Stiftung and the Sustainable Development Solutions Network (Sachs et al., 2019) which contains information on SDG performances of 193 countries. For our assessment, we use the scoring indexes of 2019. According to Eq. (6), changes in the scoring of SDG j can be calculated by:

Concerning the correlations of GDP/capita and SDG scores, according to our calculations, the scores of SDG 1, SDG 3, SDG 4, SDG 6, SDG 7, SDG 9 and SDG 12 seem to be highly correlated with the level of GDP/capita \(\left( {\frac{GDP}{{capita}}} \right)\) (see Table 4). In all of these cases, causality is given. This means that there are arguments which support the correlation between the factors.

Our conclusions that SDG 1, SDG 3, SDG 4, SDG 6, SDG 7, SDG 9 and SDG 12 are linked, are in line with the results of Pradhan et al. (2017) and El-Maghrabi et al. (2018). In contrast to our approach, the authors of these studies took a closer look on the time-series of SDGs. By comparing pairs of indicator time‐series they analyzed which changes in SDG are positively or negatively correlated. Examples of coherent goals identified by Pradhan et al. (2017) are presented in Fig. 5.

Coherences between SDG. Source (Pradhan et al., 2017)

For Level 2, we made some simplifying assumptions concerning the correlation between the GDP and SDG scores, which will influence the explanatory power of the results. The assumption on causality of the relationship between GDP and SDG, significantly influences the interpretation of the results. It should be taken into account that the correlations are estimated for a broad set of countries when looking at each individual country case. This limitation is alleviated by combining this method with the results of Levels 1 and 2.

4.3 Assessment of impacts on the value chain on local level (Level 3)

The Level 1 and Level 2-assessments are based on calculations using aggregated numbers on a sectoral or national level. In principle, the effects on site-specific levels can differ from sectoral figures. In addition, site-specific assessments can provide information on SDGs which is ignored by using IO approaches. Since, in particular for the mining sites, a broad range of publications exist, we decided to conduct a literature review rather than collecting primary data.

Yet, there are limitations in this literature review due to the different time periods covered in the chosen publications. This is due to the problem of data availability, as analyses have not been carried out and published for every country in the same level of aggregation or within the same time scale. This should be considered when interpreting the results of the literature review.

4.4 Calibration and scenario specification

4.4.1 Current state of reaching SDGs

Australia

The main challenges for Australia are to improve SDG1 “Zero Hunger”, SDG 7 “Affordable and Clean Energy”, SDG 12 “Responsible Consumption and Production” and SDG 13 “Climate Action” (Sachs et al., 2019). While clear progress has been made in the areas of SDG 1 and 7 in recent years, it is particularly striking that SDG 13 has hardly improved at all. While Australia can keep up with international comparisons and ranks 37th, Allen et al. (2019) show that Australia would need to make significant efforts to avoid failing to meet its 2030 emission reduction target.

Canada

With a total score of 78.2, Canada ranks 21st. SDG 13 and SDG 14, but also SDG 17 “Partnerships for the Goals” are rated the weakest (see Annex Table 9). A study by McArthur and Rasmussen (2017) found that Canada may be missing its Sustainable Development Goals and identified a declining trend for many SDGs, such as SDG 5 “Gender Equality”. However, the new Global SDG Trends report shows a positive trend for most of the goals rated as “significant challenges”.

China

For China, the assessment of the SDGs gives a mixed picture: “Education”, “Decent Work and Economic Growth” are the topics where China shows its strengths. China does less well on the SDGs “Reduce Inequality”, “Climate Action” and “Peace, Justice and Strong Institutions”. In 2020, almost all SDGs show either a trend of improvement or hardly any stagnation. However, it is striking that SDG 15 “Life on Land” and SDG 17 “Partnerships for the Goals” show a negative trend. A comparison of the ranking between 2019 and 2020 indicates strong fluctuations. While China ranked 39th in 2019, only four points behind the USA (Sachs et al., 2019), it is in 48th place in 2020.

Colombia

In 2020, Colombia ranked 67th out of 166 countries with a score of 70.4. In particular, regarding the targets “Reduced Inequality” and “Peace, Justice and Strong Institutions”, other countries perform better than Colombia. A strong negative trend shows “Quality of Education”. In past years, the access to electricity and to clean fuels and technology for cooking have been improved, whereas the share of the population who feel safe walking alone at night in the city or area has dropped. In the business sector more and more companies include SDGs in their corporate strategy planning. SDG 5 “Gender Equality”, SDG 12 “Responsible Consumption and Production”, SDG 8 “Decent Work and Economic Growth” and SDG 16 “Peace, Justice and Strong Institutions” have received special attention so far. All in all, the SDG-performance is moderately improving.

Indonesia

According to a 2019 voluntary national review (Republic of Indonesia, 2019), Indonesia attached particular importance to 6 SDGs, among them “Quality Education”, “Decent Work and Economic Growth”, “Climate Action”, “Peace, Justice and Strong Institutions”, and “Partnerships for the Goals”. These are seen as enablers to achieve the goal of “Reduced Inequalities”. Indonesia still faces major challenges in achieving SDGs. SDGs 2, 3, 6, 9, 10, 11, 15 and 17 are rated “major challenges remain”.

Russia

An examination of Russia's SDG rating structure shows that the goals “Good Health and Well-Being” and “Peace Justice and Strong Institutions” score particularly poorly. Overall, Russia places 57th with a score of 71.9.

South Africa

South Africa ranks 110th with a score of 63.4. In the course of the development of a “National Development Plan”, a constantly high level of unemployment, low quality of education, poorly distributed regional infrastructures, resource-intensive growth, an inadequate health system, an inefficient public service, as well as corruption and a lack of social cohesion were identified as the greatest challenges. This is clearly reflected in the SDG rankings, with weak scores for goals as “No Poverty”, “Good Health and Well-Being”, “Clean water Sanitation”, “Decent Work and Economic Growth” and “Climate Action”.

USA

An analysis of the SDGs in the United States allows us to draw two conclusions: Firstly, the successful implementation of the SDG targets seems to be geographically clustered, with the region around New England performing best and the central South-East performing worst. Secondly, there are structural inequalities in social, economic and environmental aspects. A 2018 study of the SDGs (Sachs et al., 2018) identifies a considerable need for action to achieve set targets for SDG 1 “No Poverty”, SDG 5 “Gender Equality”, SDG 10 “Reduced Inequalities”, SDG 13 “Climate Action” and SDG 15 “Life on Land”. Among industrialized countries, the United States perform relatively weakly. They are in 31st place and achieve a score of 76.4 (Sachs et al., 2019).

4.4.2 Scenario specification.

The development of the future demand for coal is subject to a high degree of uncertainty and cannot be reasonably forecasted. Hence, we decided to analyze six different scenarios (see Table 5): In scenarios A1 and A2, we assume that until 2040, only Austria, France, Sweden, United Kingdom and Italy will phase out coal-fired power plants. In the scenarios B1 and B2, we extend the list of countries phasing out coal-fired power plants to include Portugal, the Netherlands, Denmark, Ireland, Spain, Poland and Germany. In the scenarios C1 and C2, we assume that all European countries, as well as the United Kingdom, will shut down their coal-fired power plants until 2040. With regard to the demand for coal in steel production, we follow Material Economics (2019) and distinguish between a future with a high share of CCS and a future where hydrogen-based technologies increasingly replace conventional steel production. Accordantly, the scenarios A1, B1 and C1 reflect the development of the demand for coal in the case of employing CCS technologies in the steel sector. For A2, B2 and C2, we assume that BOF/BF production is partly replaced by hydrogen-based technologies.

The scenarios are specified by using data provided in the energy balances for European countries on the use of coal for the year 2018 (Eurostat, 2020a) in combination with information on coal im- and exports of individual countries and prices for coal published by the German Coal Importers Association (Verein der Kohlenimporteure, 2019). For the scenarios, changes in financial flows are calculated by assuming that the demand for coal used for power plants in the selected “phasing out coal-fired power plants”-countries will drop to zero. The changes in physical flows are linked with data on coal prices. Based on information the German Coal Importers Association (Verein der Kohlenimporteure, 2019) provided we assume a price of 75.6 Euro/t for steam coal and for coking coal 148.3 Euro/t. By combining prices and changes in physical flows, we get information on changes in the corresponding financial flows.

As compensation for phasing out coal-fired power plants, we follow ENTSO-E (2018) and assume a phase-out of coal-fired will greatly go hand in hand with an increase in the installed PV. We pay special attention to PV also because PV modules are imported to a large extent (mainly from China), in contrast to e.g., wind turbine components and other renewable technologies. Expenditures for importing PV modules are calculated by using the information of ENTSO-E on changes in installed capacity of PV per changes in installed capacity of coal-fired power plants (ENTSO-E, 2018), in combination with the assumed scenario-specific developments in the coal power plant sector and cost assumptions on prices for PV modules. Regarding the assumption on the prices for PV modules, we follow IEA (2020b) and assume a price of 490 $/kW peak for imported PV modules for the year 2040.

Regarding changes in expenditure for coal used in the steel sector, we assume that in all European countries (and the United Kingdom) the steel production changes equally (corresponding to the scenario-specific assumptions on the use of steel technologies). The resulting financial flows are presented in Table 5.

5 Results and discussion

5.1 Level 1

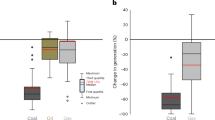

A decline in European coal demand reduces salary payments to employees in coal exporting countries. According to the assumption that more PV modules will be imported from China, we calculate a small positive impact on employment in China. The calculations show very little change in land use and the share of female employees in total employment. In coal exporting countries less grey water will be released. The share of renewable energy will increase. Compared to other impact indicators, “material efficiency” will be affected to a greater extent: Since, in particular, extraction of coal is correlated with overburden from mining, reduction of coal extraction goes hand in hand with lower needs for so-called “used materials”. The reductions in the amount of “used materials” will be higher than the changes in GDP. Hence, reduction in coal extraction will result in improvements in material efficiency (Fig. 6).

Results Level 1

5.2 Level 2

The calculations conducted by using GDP as an explanatory variable for SDG-scales show that in general a decrease in GDP results in lower scores for SDGs 1, 3, 4, 6, 7 as well as SDG 9. In addition, there is an increase in the scores for SDG 12.

Depending on the scenario, on average the scores of SDG1 of the coal exporting countries will be lowered between 0 and 0.02%. SDG 3 will be affected similarly, whereas the scores of SDGs 4 and 6 will drop at a maximum of 0.01%. With a decrease of up to 0.015%, SDG 7 is slightly more affected. SDG 9 will be impacted even more strongly: According to our calculations, a decrease of up to 0.05% can be expected.

The positive impact on SDG 12 will be a little bit smaller than the impact on SDG 9 but still higher than the negative impacts on most of the other SDGs. Since for the scenarios A1 and A2 we assumed only small changes in financial flows, SDG scores will be affected less than e.g., in scenarios B2 and C2.

In terms of SDGs 1, 3, 4, 6, 7, and 9, among the countries considered, Russia will be impacted the hardest, followed by Indonesia and South Africa. With respect to the positive effects (SDG 12), Australia will rank first, Russia second and Canada third (Fig. 7). All in all, the impacts on coal exporting countries are very small.

Results Level 2 (Changes of SDG scores in comparison to data for 2018)

The coal-exporting countries considered do not only differ in terms of their export share to Europe, but also in terms of other factors such as GDP per capita, the general wage level in the coal sector or mining efficiency (measured in coal extraction per employee). The country-specific effects of a European coal phase-out, therefore, not only diverge with regard to the scenarios, but heterogeneous patterns can also be observed within the respective countries. Yet, an analysis of the relationship between GDP and developments regarding specific SDGs shows that groups can be formed. Consequently, the following analysis of the impacts of a European coal phase-out refers to clusters of countries rather than to individual country.

5.3 Clustering on Level 1 and Level 2

The changes in SDG scores are determined by the scenario's context and differ in both direction and magnitude for each country. Quantitatively, these changes are presented in Figs. 6 and 7. In this chapter, we analyse them using the k-mean clustering method to reveal similarities between the countries in the scope. The results of the clustering are visualised in Fig. 8. The colour scale shows the Euclidean distances between the vectors of the SDG scores characterising each country (for the analyses on Levels 1 and 2).

Cluster analysis. Note: Colors represent the Euclidean distances between the vectors of the SDG scores for each country at the corresponding Levels 1 and 2, countries in brackets signal for strong divergence of the country within the cluster.

The identified clusters allow us to draw generalised conclusions for the group of countries showing similarity in SDG weights changes. Let us consider Cluster 1 at Level 1 of the analysis for all scenarios defined in Table 6. It consists of the two countries China and Russia. Both countries show divergent patterns in their response to a decrease in coal demand compared to other countries analysed at Level 1. They are also very different from each other in terms of changes in SDG target metrics, with similarities only in SDG 7 showing the decline in the share of renewable energy and energy efficiency. Thus, Cluster 1 depicts two countries that must be considered separately from the other countries in the scope. Cluster 2 includes countries that show more similarity in response of SDG outcome and process targets. Australia stands out in this cluster for scenarios A1 and A2, showing less exposure to reductions of coal imports from the selected European countries. This can be explained by the relatively small share of imports of coking coal and anthracite from Australia. The same argument is valid for Australia at Level 2 that analyzes the impact on economic activities. Cluster 1 for scenarios A1 and A2 includes China and Australia: Both countries show a very divergent response to a reduction in European coal imports. In Australia, SDG 12 “Responsible Consumption and Production” is showing improvement in contrast to a subtle decline of this metric in China. SDG 6 “Clean Water and Sanitation” similarly reveals two opposing trends for this pair of countries. Countries in Cluster 2 for scenarios A1 and A2 experience changes in SDG targets of the same direction: strongly positive improvements in SDG 12, negative in SDG 6 and 9. Mixed direction changes appear in SDG 1 and 7. Inside this cluster, Indonesia, Colombia and South Africa reveal more similarities in percentage changes: For SDG 1, changes in these three countries range between − 4.1 and − 5.7%. For Canada and the United States, changes are positive, namely − 3.4 and 2.4%, respectively. This is an illustration that each cluster can be divided into sub-clusters for a more detailed analysis of specific SDGs. Clusters are helpful to facilitate the process and generalize the conclusions at the desired level of aggregation.

Comparing the magnitudes of the effects estimated at Level 1 and Level 2 for certain SDGs, it is apparent that there exist differences. First, the size of the impacts is higher for Level 1 estimates than for Level 2 estimates. This is due to the level of aggregation of the data used for the assessments. Sectoral data used for the IO analyses make it possible to work with explicit data of the mining sector, while the Level 2 analyses are based on aggregated data at the national level. Therefore, the sector-specific characteristics are lost in the Level 2 analyses.

A more concrete picture of the impacts on financials flows on SDGs gives the analyses at Level 3: The impact of the coal mining sector on average household income is ambiguous. On the one hand, the development of new deposits can lead to the creation of new local jobs. On the other hand, jobs in this field are regularly characterized by low occupational safety and low wage levels for low experienced positions. However, mean monthly earnings of all employees in the mining sector are usually high, in comparison with other economic sectors, as illustrated in Fig. 9.

Mean nominal monthly earnings of employees in the mining sector. Source: (International labour organisation, 2020)

From the government’s point of view, a decline in coal demand leads to lower tax revenues, royalties or dividends. However, the effects can also have a direct impact on individual population groups. The collapse of income or personal social security systems can be the result.

Regarding SDG 2 we have to distinguish between open-cast and sub-surface mining. Particularly in open-cast mines, mining is associated with restrictions on agriculture, hunting and fishing, as well as the loss of land that can be used for e.g. agriculture or forestry (EnBW, 2019; Siqueira-Gay et al., 2020; Vattenfall, 2017). In Colombia, roughly half of the coal production takes place in open-cast mines, while Indonesia produces the main share of its coal via open-cast mining (Sasaoka et al., 2015). However, also in South Africa about half of the mined coal is extracted by open-cast mining (DMRE, 2020). Generally, mining is associated with large water withdrawals and acid mine drainage, which makes it difficult to recirculate to the natural water systems (see e.g., González-Martínez et al., 2019; Ochieng et al., 2010; Spiegel and Brown, 2017; Moeng, 2019). Furthermore, chemical pollution can often be found in the regions around mining sites, which degrades soil quality (Liu et al., 2020; Munnik et al., 2010). However, the severity of the environmental impact can be partially reduced with the help of extensive regulation. Ali et al. (2017), for example, studied water pollution in the coal regions of Australia and showed that water quality in the affected regions was above the guidelines for freshwater (exceptions were traces of aluminium, iron, manganese, nickel and zinc).

In general, the decommissioning of coal mining areas can create additional capacity for agricultural use. Accordingly, a reduction in coal production can have a positive impact on SDG 2.

In addition to the negative impacts on the environment already mentioned, which can have an effect on health, the direct health risks associated with coal mining must also be taken into account when considering SDG 3. Besides harmful environmental air pollution, occupational diseases and accidents also pose a risk to the health of those affected. Many studies stress the negative impacts of mining on the environment, health and society (see e.g., Cardoso, 2015; Geng and Saleh 2015; Shi et al. 2013). In particular, Hendryx et al. (2008) review several published studies and present evidence for negative health impacts of open-cast mining. Usually, poor working conditions in the mines are stressed as an additional factor, which fosters resistance against the mines. According to a study of Vattenfall, mining activities impacted living conditions in a negative way. Beside deterioration with respect to water use, the access to drinkable water were listed as challenges for reaching SDG 3 (EnBW, 2019; Vattenfall, 2017).

So far, women workers are underrepresented in the mining sector. A large number of studies addresses gender equity issues in the mining sector (see e.g., Eftimi et al., 2009; Johansson and Ringblom, 2017; Kaggwa, 2020; Reeson et al., 2012). According to Botha (2016), cases of sexual abuse and harassment are still prevalent in this sector. Mayes and Pini (2014) also show that women are underrepresented in the mining sector. Additionally, Sharma (2010) argues that women experience significant social and economic disadvantages in Australian mining communities. As a tendency, it can be assumed that a decline in the mining sector will mitigate some of the problems mentioned. Accordingly, it is reasonable to conclude that a decline in coal extraction will have a positive effect on SDG 5.

As already mentioned above, a very critical issue for mining is the use of water and acid water drainage. Cerrejon (2017), DSDG (2020) and Vattenfall (2017) highlighted that the water sources in the mining areas have been significantly impacted by the withdrawal of water and the release of hazardous chemicals and materials. However, the severity of associated water pollution can be partially minimized through effective regulation and appropriate engineering measures (see, e.g., Ali et al., 2017). Nevertheless, in principle, lower reductions in coal extractions might reduce negative impacts on the SDG “Clean Water and Sanitation”.

Since coal is a comparatively cheap and flexible energy carrier, in principle, coal mining could help to extend the access to affordable energy. In addition, it can be argued that by providing mining operations with the necessary infrastructures and energy supply, it can help to bring access of electricity to the surrounding population in rural areas (see e.g., Toledano, 2012). In turn, the use of coal for energy production is associated with high greenhouse gas emissions. The relationship of coal mining to SDG 7 “Affordable and Clean Energy” is, therefore, to be assessed as ambiguous and ambivalent.

Regarding SDG 8 it has to be highlighted that for most coal exporting countries the coal mining industry has been a sector with high relevance for the overall economy. In Colombia for example, about 130.000 people are employed in the mining sector (Agencia Nacional del Mineria, 2017) with nearly 45.000 directly in the mining of coal. Usually, the compensation of the employees is above average. However, many authors stress that the mining industry is linked with low health and safety standards in combination with hostility to labour unions by mining companies (BetterCoal, Cerrejon, 2019; Hermanus, 2007; Peetz & Murray, 2011; Cardoso Diaz, 2016; Vattenfall, 2017). Furthermore, in light of the so-called “resource curse,” the role of resource extraction as a sustainable growth strategy has been regularly questioned see e.g., Deller & Schreiber (2012), Humphreys et al., (2007). Based on these opposing arguments, no clear direction of impacts can be identified with respect to SDG 8.

For the transportation of the mined coal, as well as the delivery of materials and machinery, sufficient infrastructure in the sense of roads, waterways, railways and communications network is required (see e.g. Johnson (2017)). Coal mining requires products from other industries, and the value-added generated in mining stimulates demand for other goods. In developing countries in particular, this can support the entire industrialization process. Consequently, a decline in coal extraction could be accompanied by a decline in investment in new infrastructure. At the same time, measures that have already been implemented will remain in place. A reduction in coal extraction could therefore have a negative impact on SDG 9.

Using Colombia as an example, Cardoso Diaz (2016) emphasizes that in terms of resettlement and opportunities for agriculture, hunting, and fishing, the indigenous population in particular has been discriminated against. Other studies also highlight potential problems that arise when resident populations are relocated (see e.g., Owen and Kemp (2015), Scambary (2013), Terminski (2012) and Owen et al. (2019)). Hajkowicz et al. (2011) find larger inequalities in income in large mining areas. Other studies also make reference to the relationship between the mining sector and inequality (see e.g., Mancini and Sala (2018), Petkova et al. (2009), Reeson et al. (2012) and Loayza and Rigolini (2016)). Yet, for Australian mining regions, Reeson et al. (2012) show that the GINI index follows a Kuznets-type curve, with increasing inequality at the onset of mining activities and decreasing inequality as mining progresses. In developing countries, these impacts may be more relevant than in developed countries.

Few studies explicitly consider the connection between mining and sustainable development of cities and communities (see e.g., Yu et al., 2008). As of 2019, 55% of the world's population lives in urban areas. In principle, both cities, e.g. in the form of royalties and taxes, and small companies can benefit from mining activities (see e.g., Badri & Boudreau-Trudel, 2020). However, despite high royalties and taxes from mining, the municipals in the coal regions are still often poor and have problems to ensure minimum living standards for the majority of their population (BetterCoal, Cerrejon, 2019). The proximity of coal mines to cities and towns affects average levels of particulate matter (PM 2.5, PM 10) in the air, which has a negative impact on human health within 23 km of open-pit mines in northern Columbia, where 92% of coal is produced (Arregocés et al., 2018). In contrast, in a bibliometric analysis of Chinese mining cities, Jiao et al. (2020) show that mining and the transition towards sustainable cities do not necessarily contradict each other. It can be concluded that the relationship between mining and the sustainable development of cities is highly situational and thus cannot be unambiguously assessed.

With regard to the SDG “Responsible Consumption and Production”, it must be pointed out that mining is associated with enormous water withdrawals, with the impairment of water bodies through water discharges and/or runoff, as well as with significant impacts on the landscape and with the generation of mining waste. Regarding environmental effects, increasing dust and particulate air emissions, as well as water pollutions resulting from coal-mining operations are reported. As the use of coal is also associated with high CO2 emissions, activities aimed at promoting coal as an energy source counteract measures to combat climate change. This directly contradicts this SDG’s target to reduce the release of harmful chemicals to air, water and soil (see sub goal 12.4). Additionally, SDG 12 also deals with phasing out fossil fuel subsidies. By examining 191 countries, Coady et al. (2019) show that fossil fuel subsidies remain large and estimate the global subsidies for 2017 to $5.2 trillion. They identify China, USA, Russia and the European Union to be the largest subsidizers. Although opposing factors were presented here, a phase-out of coal production seems to tend to be associated with a positive effect on SDG 12.

Both the conversion of coal into electricity and its use as a material for steel production are associated with immense emissions. Accordingly, the phase-out of coal production is classified as positive for SDG 13 “Take Urgent Action to Combat Climate Change and its Impacts”.

No clear impacts of coal mining on SDG 14 “Conserve and Sustainable use of Oceans, Seas and Marine Resources for Sustainable Development” could be identified. Thus, the authors assume a effect negligible.

As previously argued, mining can be associated with the loss of agricultural and forestry land (EnBW, 2019; Siqueira-Gay et al., 2020; Vattenfall, 2017). In addition, there is a significant impact on local water resources due to water withdrawals, acid mine drainage, and environmental pollution from other chemical substances (see e.g., González-Martínez et al. (2019), Ochieng et al. (2010), Liu et al. (2020) and Munnik (2010)). Among others, several studies identify these factors as significant drivers for the loss of biodiversity associated with mining (see e.g., Swer and Singh (2003), Vattenfall (2017), EnBW (2019) and Cerrejon (2017)). Focusing on steam biodiversity Giam et al. (2018) identify negative implications of mining on freshwater biota in the US. They stress, that even after post-mining reclamation, biodiversity impacts remained and that effective environmental policy is needed in order to prevent such effects. It can be assumed that a reduction of coal production will have a positive effect on SDG 15; on the one hand, the progress of land loss will be reduced, and, on the other hand, mining areas can be reclaimed. However, the negative impact of mining and the effectiveness of renaturation in terms of increasing biodiversity is strongly dependent on the design of environmental policy.

In Colombia, involuntary resettlements, health problems resulting from air pollutions and inferences in water bodies (i.e. changes in groundwater level, lower access to drinking water), and inappropriate working conditions have resulted in many complains and conflicts (see e.g., Anwaltskollektiv José Alvear Restrepo (CAJAR) (2019) and Niebank & Utlu (2017)). Similar issues can be found in other countries with mining activities, such as China, the United States, Indonesia, Canada, or Australia (see e.g. Yang et al. (2017), Askland (2018), Terminski (2012), Downing (2002) and Muir and Booth (2012)). Currently, the International Trade Union Confederation lists Colombia as one of the 10 worst countries in the world for working people. Yet, Indonesia and China also received a rating of “No guarantee of rights” (ITUC, 2020). A link between corruption and mining has been discussed in several studies, e.g. for Colombia (Vattenfall, 2017), China (Dong et al., 2019), or Indonesia (Hamidi, 2015). Colombia's mining regions belong to the most corrupted regions within the country. In recent years, measures have been introduced aiming to lower corruption. However, the corruption in Colombia is still on a high level (OECD, 2019; Transparency International, 2019) (Transparency International rank: 99 out of 180).

As mentioned above, we assumed that a phase-out of coal-fired power plants will be linked to increasing imports of PV modules from China. Taking the number of employees in the PV industry into consideration, we expect that increases in the PV exports will result in higher revenues and thus in an increase in income. Hence, in principle, the phase-out of coal-fired power plants in Europe will support China in reaching SDG 1. According to Nkuissi et al. (2020) the production PV module is linked with the use of a lot of toxic chemicals including cadmium telluride, copper indium selenide, cadmium gallium (di)selenide, copper indium gallium (di)selenide, hexafluoroethane, lead, and polyvinyl fluoride. Some of the by-products of production can endanger human health (Mulvaney, 2014). Hence, negative impacts on reaching SDG 3 as well as on SDG 12 (“Responsible Consumption and Production”) can be expected. The incident in Hongxiao Village (ICTA, 2020) showed that the production of PV modules can result in polluted wastewater. Of course, this incident can be seen as an exception. However, it can not be precluded that such incidents will never be repeated. Hence, we have to include the possibility that PV module production will affect SDG 6 (Qi & Zhang, 2017). On the other hand the production of PV modules and the aim of the industry to reduce the cost of production, the PV industry helps to reach SDG 7 (“Affordable and Clean Energy”). Since the production of PV modules is directly and indirectly linked to economic activities, it can be assumed that increasing demand can in principle contribute to the achievement of SDG 8 and SDG 9. Regarding reaching SDG 13 (“Climate Action”) it has to mentioned that even if the production of this technology is indirectly linked with emissions, as a (partial) substitute for coal-fired power plants it contributes to the reduction of GHG emissions.

In China, there have been some protests against PV module producers. ICTA (ICTA, 2020) listed as examples the antipollution protests against JinkoSolar Company in 2011 and Apollo Precision (Fujian) Ltd. in 2015 with more than a thousand protestors. Until now, the protests have been focused on specific companies and have only been relevant on a local level for a relatively short period.

The Chinese module manufacturer GCL System Integration announced that in the next four years they will build a 60 GW solar module factory in eastern China. Hence, it can be expected that the PV industry in China will continue to grow. Assuming that the share of PV-modules imported by Europe from China will still be high (see e.g., Fraunhofer ISE, 2020), the PV exports from China to Germany will account for between 1 and 3 GW. In comparison with the production of PV modules in China, the exports to Germany are very small. Hence, it is unlikely that the demand of Europe for PV modules affects the PV industry in China (and indirectly SDGs) significantly. Table 7 summarizes our conclusions on site-specific SDG effects.

5.4 Overall assessment

As mentioned above, the assessment at Level 1 focuses on showing how the well-established IO Database can be used for the analysis of changes in the demand for coal. We demonstrate that with a standard approach, it is only possible to assess a small number of selected indicators. Using GDP as explanatory variable (Level 2), the assessment of SDG can be extended. However, the employed approach only enables us to assess scores for SDG on an aggregated level. More detailed information provides the analysis at Level 3 which focuses on a review of site-/company-specific surveys.

Table 8 shows the results of the assessment on the different levels focusing on coal-exporting countries. Regarding SDG 1 all assessments point in the same direction. SDG 2 seems to be less clearly assessable. With respect to SDG 3, there is a discrepancy between the results of the assessment at Level 1 and Level 2. Level 1 indicates an improvement in reaching SDG 3, whereas the calculations for Level 2 indicate that the situation could rather worsen.

The assessment at Level 1 and Level 3 do not provide information on SDG 4, whereas the calculation for Level 2 presume very small negative impact on reaching this target. Very small impacts on SDG 5 are indicated by the assessment at Level 1 and Level 3. Regarding SDG 6, only small impacts are calculated at Level 1 and Level 2. The assessment at Level 3, however, shows that on company-/site-specific level there could be significant (positive) effects with respect to water withdraws and uses. By focusing on company-/site-specific effects, the assessment of SDG 7 indicates another direction than the calculations at Level 1 and Level 2 which emphasize aspects on a national level like overall energy efficiency.

According to the IO-analysis conducted for Level 1, labour productivity will decrease slightly. Hence, we get a negative but low impact on reaching SDG 8. No information on SDG 8 is available from the Level 2 analysis. The assessment at Level 3 does not provide an answer in which direction the achievement of SDG 8 will be impacted either.

As stated before, each of the analyses and methodological approaches has limitations, e.g., concerning timeframes or data availability. Still, the combination of investigating the matter on three different levels allows drawing a set of comprehensive conclusions for almost all SDGs. With the combination of methods, the complexity rises. This complexity has to be accounted for when interpreting the effects and might be a reason for diverging directions of the estimated effects on particular SDGs. Nevertheless, controversial results would generally benefit from replications of the modelling exercise with more recent data or data of a consistent time frame. The approach presented here incorporates both availability and feasibility and is thus unique. The alternating directions of the effects are furthermore not a key issue, as the SDGs as concept are comprised of several indicators correlated to multiple other factors that are not accounted for in the model. As such, the SDG concept is challenging because of its nature as a “wicked problem” (compare Sect. 2.2).

To generate insights about the directions of the effects of the multi-level approach, future analyses could improve the degree of integration between the levels introduced.

As mentioned above, each method has its own shortcomings. The IO analysis shows limitations on the number of indicators that be used for SDG assessment. The Level 2 approach focuses on national data. Hence, it neglects impacts on a sectoral level. The literature review is based on data which is published. Some data are restricted, whereas other data are case-specific. This limits the possibility of drawing of generalized conclusions.

Hence, further research is needed to find an appropriate measure of economic activity that can be used to assess convergence towards the SDG targets and establish a causal direction. Such measures could have a multiplying positive effect if they are implemented as multilevel approach to analyze broad impacts of regional environmental policies on a global scale.

6 Conclusions

Coal-fired power plants have been a main pillar of the European electricity supply system for decades. Concerns about climate change, decreasing cost of non-fossil-fuel technologies as well as declining relevance of domestic mining spur the process of phasing out coal-fired power plants. The steel industry as a sector which also employs coal will be affected by climate policy, too. There are different ways for the steel sector to respond to stricter environmental regulations. An increase in the use of EAF as well as the use of carbon-free technologies, for example, will result in lower demand for coking coal. Hence, coal exporting countries might not only suffer from lower demand for coal resulting from phasing out coal-fired power plants but also from changes in the steel industry.

There are concerns that sustainable development in coal exporting countries could be hampered by reduced export opportunities. Using the three-level approach, we show that changes in coal demand in Europe are associated with both negative and positive impacts on achieving the SDGs in coal-exporting countries.

Our analysis was organized as follows: Firstly, we implemented an IO model by using WIOD and EXIOBASE as a source and assessed the effects of changes in coal demand on SDGs. The analysis shows that WIOD and EXIOBASE are very restricted with respect to the assessment of SDGs. By using these databases, it is possible to identify changes in financial flows on income, employment, different kinds of emissions, material use and land use The assessment of impacts by using GDP as explanatory variable for changes in SDG-scores indicates negative implications on reaching SDGs 1, 3, 4, 6, 7 and 9 as well as positive impacts on SDG 12. Since the IO as well as the econometric approach only provide information on the sectoral or national level, we took a closer look on site-/company-specific effects. In doing so we observe positive impacts of reductions of mining activities on the water management and release of pollutions as well as effects on societal level (e.g., lower need for resettlements).

Since the EU is only one of many partners of coal exporting countries, the phase-out of coal-fired power and changes in the use of steel technologies will not have significant impacts on mining industries. Therefore, the ancillary effects of the reduction of coal use in Europe on reaching SDGs in coal exporting countries will be negligible. This holds all the more true as the coal sector is also just one of the sectors influencing sustainable development in coal exporting countries.

Since phasing out of coal-fired power will result in a higher demand for other power plant technologies, we analyze to which extend China will benefit from ancillary effects. Considering China's huge production of PV modules, we conclude that China's SDGs will not be affected significantly by Europe’s increase in demand for PV.

References

Agencia Nacional del Mineria (2017). Coal, the mining godfather of Colombia. https://www.anm.gov.co/?q=carbon_el_padrino_minero_de_colombia_boletin_prensa (accessed 22/04/2020).

Agora, Sandbag (2020). The European Power Sector in 2019, Berlin.

Ali, A., Strezov, V., Davies, P., & Wright, I. (2017). Environmental impact of coal mining and coal seam gas production on surface water quality in the Sydney basin, Australia. Environmental Monitoring and Assessment, 189, 1–16.

Allen, C., Metternicht, G., & Wiedmann, T. (2016). National pathways to the sustainable development goals (SDGs): A comparative review of scenario modelling tools. Environmental Science & Policy, 66, 199–207.

Allen, C., Metternicht, G., Wiedmann, T., & Pedercini, M. (2019). Greater gains for Australia by tackling all SDGs but the last steps will be the most challenging. Nature Sustainability, 2, 1041–1050.

Anwaltskollektiv José Alvear Restrepo (CAJAR) (2019). Menschenrechtsverletzungen durch den Kohleabbau in El Cerrejón. Misereor, Bogota. https://www.misereor.de/fileadmin/publikationen/publikation-menschenrechtsverletzungen-durch-den-kohleabbau-in-el-cerrejon.pdf. Accessed 08 Jan 2022

Arregocés, H. A., Rojano, R., Angulo, L., & Restrepo, G. (2018). Intake fraction of PM10 from coal mine emissions in the North of Colombia. Journal of Environmental and Public Health, 2018, 8532463.

Askland, H. H. (2018). A dying village: Mining and the experiential condition of displacement. The Extractive Industries and Society, 5, 230–236.

Badri, A., Boudreau-Trudel, B. (2020). Sustainable development in the mining industry: Towards the development of tools for evaluating socioeconomic impact in the Canadian context. Environment, Development and Sustainability, 23(5), 1–27.

Barbero-Vignola, G., Acs, S., Borchardt, S., Sala, S., Giuntoli, J., Smits, P., & Marelli, L. (2020). Modelling for sustainable development goals (SDGs): Overview of JRC models. Publications Office of the European Union.

BetterCoal, Cerrejon (2019). Bettercoal Assessment Public Report: Cerrejón Coal Company, London.

Bidarbakhtnia, A. (2019). Measuring sustainable development goals (SDGs): An inclusive approach. Global Policy, 11, 56–67.

Bjelle, E. L., Többen, J., Stadler, K., Kastner, T., Theurl, M. C., Erb, K.-H., Olsen, K.-S., Wiebe, K. S., & Wood, R. (2020). Adding country resolution to EXIOBASE: Impacts on land use embodied in trade. J Econ Struct, 9, 14–14.

BMWi (2020). For a strong steel industry in Germany and Europe. Federal ministry for economic affairs and energy (BMWi), Berlin.

Bobylev, S., & Solovyeva, S. (2017). Sustainable development goals for the future of Russia. Studies on Russian Economic Development, 28, 259–265.

Böhringer, C., & Löschel, A. (2006). Computable general equilibrium models for sustainability impact assessment: Status quo and prospects. Ecological Economics, 60, 49–64.

Botha, D. (2016). Women in mining still exploited and sexually harassed. SA Journal of Human Resource Management, 14, 1–12.

Breuer, A., Janetschek, H., & Malerba, D. (2019). Translating sustainable development goal (SDG) interdependencies into policy advice. Sustainability, 11, 2092.

Buchholz, W., Markandya, A., Rübbelke, D., & Vögele, S. (2020). Ancillary benefits of climate policy: New theoretical developments and empirical findings. Springer.

Capros, P., Van Regemorter, D., Paroussos, L., Karkatsoulis, P., Perry, M., Abrell, J., Ciscar, J.-C., Pycroft, J., Saveyn, B. (2013). GEM-E3 Model documentation. Joint Research Centre - Institute for Prospective Technological Studies, Seville.

Cardoso, A. (2015). Behind the life cycle of coal: Socio-environmental liabilities of coal mining in Cesar, Colombia. Ecological Economics, 120, 71–82.

Cardoso Diaz, A. (2016). Socio-environmental liabilities of coal mining in Colombia: A political ecology approach to the global coal chain. Universitat Autonoma de Barcelona.

Cerrejon (2017). Sustainability report. https://www.cerrejon.com/index.php/sustainability-reports/?lang=en, (accessed 15/11/2020): Cerrejon.

Coady, D., Parry, I., Le, N.-P., Shang, B. (2019). Global fossil fuel subsidies remain large: An update based on country-level estimates. International Monetary Fund Washington, DC.