Abstract

We study the impact of tiered payments originating from client banks on the liquidity consumption (relative intraday liquidity use) of settlement banks. Estimates of a panel data model, employing wholesale payments in euro, show that a higher share of tiered payments reduces liquidity consumption by settlement banks. Metrics on timing, delay, and payment priorities suggest that settlement banks use more leeway in settling tiered payments from client banks compared to in-house payments. Payment timing as a proxy for external delay suggests that tiered payments help smooth liquidity positions. Payment delay within the system does not follow a clear dynamic over time, whereas banks consistently de-prioritize tiered payments. Thereby, settlement banks employ tiered arrangements to manage intraday liquidity more efficiently. To a certain extent, this hints at “free riding” or higher recycling of liquidity from client banks’ payments. However, the results are also consistent with settlement banks’ monitoring role or tiered payments potentially exhibiting different characteristics which may be attributable to contractual arrangements.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Payment systems form the basis for the settlement of debt obligations in an economy. A universal feature of payment systems is the settlement of payments on behalf of clients by direct system participants, called tiering. Instead of directly sending payments to a payment system, some banksFootnote 1 choose to delegate settlement, akin to correspondent banking arrangements. The arrangement of an indirect participant (client bank) processing its payments through a direct participant (settlement bank) forms a tiered arrangement.

The underlying economic reasons that influence banks’ decision on how to access a payment system are manifold. For smaller banks, it might be more cost-efficient to choose tiered settlement arrangements, avoiding costs related to operational setup and liquidity management. In addition, many jurisdictions restrict direct access to a payment system for foreign banks.

The Principles for Financial Market Infrastructures (PFMIs), developed by CPSS-IOSCO (2012), specify high international standards for financial market infrastructures (FMIs) such as payment systems and offer guidance on potential sources of risk and risk mitigation. Principle 19.4 of the PFMIs states that “an FMI should regularly review risks arising from tiered participation”. Such risks include credit, liquidity and operational risk. According to the PFMIs, these risks may be especially large for highly tiered systems. From a regulator’s view, tiering comes at the potential cost of concentration and hence operational bulk risks. A large share of tiered payments may increase exposures of settlement banks to client banks and vice versa. Liability issues may arise for such exposures in the event of a default.

However, tiered participation not only entails risks but can increase the efficiency of payment systems. Costs of payment settlement decrease with tiered participation, as direct participants can profit from economies of scale [see for example Adams et al. (2010); Chapman et al. (2013)]. Tiering generally decreases liquidity consumption, as payments offset each other when concentrated among fewer direct participants. Pooling liquidity leads to lower cost of capital, as higher traffic volumes offset payments within the system or because banks settle payments internally on their own books without drawing on liquidity in their payment system account.Footnote 2 However, little is known about the effect of tiering at the participant level and how tiering factors into banks’ active liquidity management.

From a settlement bank’s perspective, tiered payments feed into the overall liquidity disposition of payments that are settled in a way to minimize liquidity use. Monitoring intraday liquidity is part of the Basel framework to ensure banks are able to meet payment obligations. Banks monitor intraday liquidity metrics in accordance with Basel Committee on Banking Supervision (2019), also factoring in secured and unsecured credit lines and unencumbered assets. Central bank reserves and participation in wholesale payment systems are only one part of banks’ liquidity management, but arguably one of the most important parts.

In this study, we empirically investigate the effect of tiering on the relative intraday liquidity use—referred to as liquidity consumption here—of settlement banks in TARGET2, the Eurosystem’s wholesale payment system.Footnote 3 Liquidity consumption is defined as the maximum amount of liquidity needed in the course of a day to settle the payments of a settlement bank relative to all payments sent by that bank. The measure indicates how efficiently a bank uses liquidity to settle its payments.

Using transaction-level data from TARGET2 spanning 10 years and a total of more than 1200 direct participants, we find that higher shares of tiered payments reduce the liquidity consumption of settlement banks. This finding sheds light on why banks have an incentive to provide settlement services for other banks. The results are robust controlling for pooling effects via bank fixed effects, general payment activity and other factors.Footnote 4 The main driver appears to be that banks have more discretion in settling tiered payments. Payment timing suggests that tiered payments help settlement banks to more effectively manage intraday liquidity, for example by assigning lower priorities to them compared to banks’ own or in-house payments. As a result, settlement banks employ tiered arrangements to more effectively manage intraday liquidity. To some degree, this indicates discriminatory practices, as settlement banks treat their own payments with higher urgency, thus using more liquidity for settling own payments relative to tiered payments.

Settlement banks reducing their cost of liquidity is consistent with their role in monitoring client banks and offering cost-efficient settlement services based on private information relevant to creditworthiness [see for example Chapman et al. (2013)]. From this perspective, settlement banks mitigate risk from tiered arrangements by smoothing their liquidity positions. At the same time, the findings are also consistent with tiered payments exhibiting different characteristics. Tiered payments may arrive later in the day and by nature be less urgent, so settlement banks can use these payments to optimize their liquidity positions.

As acquiring liquidity for payment purposes is usually costly, settlement banks exhibiting lower values of liquidity consumption settle payments in a more cost-efficient manner. Liquidity in the form of central bank reserves can be assumed to be costly as it is acquired from the central bank or the interbank market. There is an opportunity cost to dedicating liquidity for the purposes of settling payments and from pledging collateral. When liquidity is scarce and interest rates are high, the cost of acquiring liquidity is thus expected to be larger. Consistent with this reasoning, liquidity consumption is lower when liquidity is scarce and interest rates are high.

The paper estimates the effect of tiered payments on liquidity consumption and sheds light on whether a predominantly risk-based view of tiering is warranted. The results indicate that tiered payments give banks more leeway in liquidity management. Benefits and risks should be weighed more carefully by system designers and overseers.

2 Tiering in large-value payment systems

Large-Value Payment Systems (LVPSs) typically settle transfers that are high value or high priority. Many LVPSs, such as TARGET2, settle transactions immediately on a gross basis and are also referred to as Real-Time Gross Settlement (RTGS) systems. This stands in contrast to net settlement systems in which net payment positions are settled at a specified time. Hence, RTGS systems require higher amounts of liquidity for settling payments.

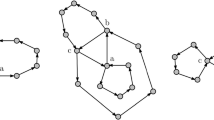

Aside from central banks and government entities, direct access to an LVPS is mostly restricted to banks. Banks can choose to access payment systems directly or through a direct participant (correspondent bank), though there are regulatory restrictions and access criteria that apply.Footnote 5 Access criteria often restrict direct access for foreign banks. Participation in monetary policy operations may require direct access to an LVPS. At the same time, banks with direct access may still settle payments via other banks due to considerations concerning risk management or operational efficiency. Payment transactions include a sender and receiver bank and, for tiered transactions, an originator bank for sent payments or a beneficiary bank for received payments, as illustrated in Fig. 1. The relationship between indirect participants and direct participants is subject to bilateral agreements.

Tiered settlement

The level of tiering differs widely across systems. While there are over 1000 direct participants in TARGET2, there are only around 30 direct participants in the UK’s payment system CHAPS.Footnote 6 As indirect participants, almost 700 credit institutions from the European Economic Area (EEA) and more than 4000 correspondents worldwide can settle payments via TARGET2.Footnote 7 The number is quite similar for CHAPS, with roughly 5000 financial institutions being able to settle payments via CHAPS. The ratio of direct to indirect participants is roughly 1:5 for TARGET2 and 1:160 for CHAPS, meaning CHAPS is a much more highly tiered system than TARGET2.

The ratio of direct and indirect participants gives an indication of how broadly banks access a system. In addition, the number of direct participants hints at the number of options potentially available to client banks. However, not all direct participants offer settlement on behalf of client banks. In TARGET2, out of 1209 participants in the sample, 438 do not send any tiered payments, only 266 settle tiered payments making up more than 1 percent of their traffic, and it is only in the case of 128 participants that tiered payments make up more than 5 percent of their traffic. Smaller participants are much less likely to engage in settlement on behalf of client banks. Therefore, we restrict the sample to larger participants in some specifications for robustness. The concept of tiering employed here refers to volumes and values of payments rather than the number of participants. For a detailed overview of tiered arrangements in TARGET2 against the background of the regulation of systemically important payment systems (SIPS), see Glowka et al. (2022).

Tiered payments may be settled internally in the accounts of a settlement bank. These payments do not provide a source of intraday liquidity for the settlement bank or act as a drain on its intraday liquidity as they are not linked to the payment system. However, these internalized payments do have implications for exposures and liquidity positions between settlement and customer banks and thus for potential risks. For banks, outgoing payments settled internally save liquidity compared to payments that are settled via a payment system. Surveys of correspondent banks in the UK have shown that internalized payments make up around one third of interbank payment values [see Adams et al. (2010)]. In the case of TARGET2, it might be assumed the share is lower as the system is less tiered.

Levels of tiered participation depend on institutional design and the system’s pricing policy. Depending on what outcome a regulator desires, legal requirements and rules of access may be designed in a way to encourage direct participation. Policy makers and regulators often emphasize the risks of tiered settlement. As described by Finan et al. (2013), the Bank of England persuaded large indirect participants to become direct participants in the UK’s highly tiered CHAPS system on account of financial stability considerations. CHAPS can be considered as an extreme example, with historically few direct participants. However, even in this setting, Benos et al. (2017) find that the effects of the largest indirect participants becoming direct participants (de-tiering) have a low impact on risk measures.

For other systems, such as the RTGS system Fedwire in the US, information on tiered payments is not available from transaction data. Thus, the analysis of risk relies on information gathered from other sources. Overall, risks for Fedwire from tiered arrangements are believed to be small and manageable through regular reviews and by the mitigation of risks posed by direct participants [see Fedwire Funds Service (2019)].

Tiered participation also reflects the banking system structure and historical developments. For example, the Australian RTGS system previously imposed restrictions on tiered arrangements. These were lifted in 2003, allowing participants whose RTGS payments are less than 0.25 percent of the total value of RTGS payments to settle payments via direct participants. There has been inertia in banks adjusting their access, potentially due to setup costs [see Arculus et al. (2012)].

A variety of factors influence the decision on how to access a payment system. Table 1 summarizes the benefits and risks of tiering from a client bank’s risk perspective. Banks balance cost-effectiveness and exposure to risks. Direct participation may entail operational setup costs and investments in liquidity management. Indirect participation may give rise to credit risk, as exposures accumulate during the day against settlement banks. In addition, payment services to client banks may be bundled together with other services, thus making direct participation less attractive. Typically, smaller domestic banks and foreign banks are more likely to become indirect participants.

Direct participants offer tiered settlement when profits outweigh the cost of providing settlement services. Direct participants may profit from economies of scale and tiering may help recoup some of the investment cost for operational setup. Banking structures also affect the degree of tiering. For example, head institutions of savings banks and credit cooperatives often provide services including payment settlement to member banks. This not only includes settlement in RTGS systems but also payments settled in internal giro systems.

Tiering often leads to uncollateralized credit positions between banks. Rochet and Tirole (1996) study tiered arrangements in the context of interbank monitoring and systemic risk. Kahn and Roberds (2009) discuss the trade-off between widespread access to an LVPS versus the efficiency gains achieved by private monitoring in tiered relationships. Chapman et al. (2013) show that tiered arrangements can arise via two channels. The first is through settlement banks monitoring client banks. Settlement banks leverage private information on creditworthiness by offering different settlement modes. The modes of settlement are similar to system-level differences between deferred net settlement systems and RTGS systems. Tiering represents a balance between deferred settlement, with lower liquidity costs but higher credit risk, and immediate settlement, with high liquidity costs but low or absent credit risk. The second channel is through settlement banks benefiting from economies of scale that reduce overall costs in the system. Given their roles, failures of settlement banks would lead to substantial welfare losses in terms of operational risks and loss of information.

From a central bank perspective, monitoring payment system activity is crucial for risk mitigation. A variety of approaches are available to identify different risks. Berndsen and Heijmans (2020) develop a traffic light approach based on different indicators to identify credit, liquidity and operational risk in TARGET2. Triepels et al. (2018) apply an unsupervised learning method to detect anomalies in RTGS systems. Sabetti and Heijmans (2021) apply a similar approach to Canadian LVPS data and discuss how deep-learning methods could be implemented by operators. Rubio et al. (2020) built on their work to assess deep networks to detect anomalies in the largest systemically important payment system in Ecuador. Aside from anomalies that can relate to different sources of risk, liquidity risk is of particular interest for the smooth functioning of payment systems and financial stability. Heuver and Triepels (2019) apply supervised machine learning in an experimental setting to identify banks encountering liquidity stress.

From a settlement bank’s perspective, liquidity needed to fund payments in RTGS systems needs to be obtained from the central bank or the interbank market at a cost. The central bank may also offer overdraft facilities for banks to fund payments. Additionally, payments received allow banks to recycle liquidity from other participants to fund outgoing payments. McAndrews and Rajan (2000) develop a measure to decompose different sources of payment funding and find incoming payments accounting for 25–40\(\%\) of liquidity sources during the day in Fedwire. With increases in reserves, the funding of payments shifts to banks using available balances (Garratt et al. 2014).

Intraday behavior in RTGS systems is also studied by Bech and Garratt (2003) using a game theory approach. Typically, banks have an incentive to postpone payments when liquidity is costly and they thus delay payments and recycle incoming payments. To account for banks changing behavior during disruption events, rather than assuming a given behavior, Arciero et al. (2009) employ agent-based modeling to simulate payment activity. Liquidity saving mechanisms in RTGS systems can affect banks’ behavior, illustrated by Martin and McAndrews (2008). One example is the use of limits in TARGET2 that allow maximum bilateral or multilateral exposures to be set [see Diehl and Müller (2014)]. More broadly, Alexandrova-Kabadjova et al. (2023) study the determinants of intraday liquidity usage in LVPSs across different countries.

Banks relying heavily on incoming payments as a liquidity source can be labeled free-riders. Diehl (2013) provides an overview of different measures and interpretations in the context of free-riding in TARGET2. Heijmans and Heuver (2014) show that banks react dynamically to stress events and some banks delay payment. They find that timing indicators can help in detecting liquidity problems. Abbink et al. (2017) study the effect of disruptions on banks’ reactions in an experimental setting. The path dependency of disruptions may lead to inefficient coordination outcomes at the system level. Concerning market structure, a homogeneous market could relate to a highly tiered system with few active banks. The study finds that a heterogeneous market structure achieves efficient coordination more easily due to a leadership effect.

Depending on banks’ use of liquidity, costs incurred by direct participants are passed on to indirect participants. Adams et al. (2010) simulate the emergence of tiered arrangements in a network structure where banks balance the liquidity costs incurred through direct participation and the service fees they pay as client banks. The service fee consists of direct participants’ liquidity costs and profits. The cost of liquidity is found to influence choices regarding system participation. Liquidity pricing is modeled proportionally to liquidity usage or up to a certain amount as free when banks have to post collateral to the central bank for prudential reasons. In such regimes, banks can draw on liquidity provided against collateral without incurring additional costs.

Arango and Cepeda (2017) study the trade-off between increased liquidity savings and larger credit risk with a higher degree of tiering in the context of the Colombian RTGS. Liquidity savings are found to increase non-monotonically. At the same time, credit risk changes little when smaller participants become indirect members, while substantial increases are found if large participants become tiered. This points to the fact that finding an optimal balance between credit and liquidity risks depends on the banking structure and type of banks. Lasaosa and Tudela (2008) use a simulation approach to study tiering in CHAPS. Results indicate that increasing tiering would lead to significant liquidity savings stemming from pooling. At the same time, concentration risk would increase substantially, while effects on credit risk appear to be small.

Operational disruptions due to technical outages in a payment system can affect the whole system or its individual participants. In the context of tiering, participant disruptions are of interest. Tiering has at least two opposing effects that are hard to quantify [see for example Arculus et al. (2012)]. Since tiering contributes to a higher concentration of settlement banks, the impact of any operational failure of a settlement bank becomes larger. However, a bank transmitting significantly more payments than others may be better at fulfilling its operational duties. Client banks are generally smaller in terms of payment traffic. Therefore, they often lack the funds to invest in state-of-the-art operational systems and to dedicate resources to liquidity management. This aspect is reinforced by the sizable complexity of modern RTGS systems, which offer a large range of options and mechanisms that require specialization among banks’ liquidity managers. Moreover, only a limited share of banks offer tiering and can be considered to be specialized. Therefore, it stands to reason that the probability of a failure of a large settlement bank is lower than the probability of an operational failure of a client bank. However, as comprehensive data on operational outages for direct and indirect participants is not available,Footnote 8 this assumption is difficult to verify. We are inclined to assume that the operational risks are at least not significantly changed by tiering and that it is more likely that tiering leads to higher operational proficiency.

The effect of tiering on operational and credit risks is not considered here. Operational proficiency is difficult to quantify, especially for smaller participants. Glowka et al. (2018) discuss this issue in the context of operational outages. Credit risks can be measured as exposures stemming from payment transactions. However, contractual arrangements between direct and indirect participants, such as pricing and pre-funding of payments as well as potential collateralization, are unobserved. In addition, internal payments that give rise to credit risk are unknown from TARGET2 data. The study focuses on implications for intraday liquidity rather than other risk implications.

3 TARGET2 data

3.1 Overview and sample

TARGET2 is the largest LVPS in Europe and one of the largest RTGS systems in the world. The system is owned and operated by the Eurosystem. In 2022, around 399,000 transactions were settled on average per business day, amounting to a value of 2.2 trillion euro daily.Footnote 9 Annual payments settled in TARGET2 amounted to roughly 40 times the annual GDP of the euro area. Even though TARGET2 relies on a single technical platform, from a legal perspective, individual central banks in the Eurosystem own separate (national) components. In addition, some EU central banks that are not members of the Eurosystem are connected to TARGET2. In the system, domestic and cross-border payments in euro are settled in real time, including interbank and customer payments, monetary policy operations and transactions with ancillary systems and other financial market infrastructures. Underlying business reasons for large-value or urgent transfers are manifold, including for example payments for goods and services, the purchase or sale of securities, loan payments or transactions based in the real economy.

The measures in Sect. 4 are constructed using TARGET2 transaction data from 2010 to the end of 2019. We focus on the transactions of commercial banks as participants of TARGET2. Transaction-level data is filtered for central bank operations, participants’ liquidity transfers between their own accounts and technical transfers in order to focus on business-related payments that affect settlement banks’ liquidity position during the day and to exclude payments that serve the purpose of liquidity management. In addition, we disregard start-of-day balances that banks hold, in part, for fulfilling minimum reserve requirements. The filtering allows us to study payment behavior and intraday liquidity, irrespective of how liquidity used for payments is acquired.

Besides customer and interbank transactions, we include transactions with ancillary systems and other market infrastructures, such as the securities settlement system T2S. For some ancillary systems there are fixed time windows for settlement, such as for the Continuous Linked Settlement (CLS) foreign exchange settlement system. Thus, participants may not be able to time such payments according to their own preferences. Nevertheless, these payments affect participants’ liquidity constraints during the day. The results are robust to excluding payments with fixed time windows. Central banks and ancillary systems themselves are not included as participants as they typically do not engage in active liquidity management and exhibit different characteristics than commercial banks.

The sample spans over 2500 business days with a total of more than 1200 direct participants. Note that the term participant relates to BICs (Bank Identifier Codes), i.e. accounts in TARGET2. Banks may use multiple BICs to settle their payments. Different accounts of the same participant are not grouped together, but results are similar when sub-accounts are consolidated.Footnote 10

Due to changes in the banking system structure, settlement banks drop in and out of the sample. In addition, some banks do not interact with TARGET2 every day, creating an unbalanced panel. We drop observations where direct participants only send or receive payments and when payments sent are below a threshold of 1000 euro. In these cases, active liquidity management on the part of settlement banks is deemed irrelevant and payment activity too low to generate meaningful results. More than 1.7 million daily observations remain in total after the adjustments.

3.2 Tiering concept applied to TARGET2

Credit institutions established in the European Economic Area (EEA) are eligible as direct participants, while credit institutions from outside the EEA may use direct participants as access points to TARGET2 (also referred to as correspondent banking). The data includes transaction details that make it possible to identify payments sent and received on behalf of client banks. While these fields in payment messages are optional, they are typically filled by banks in TARGET2 to enable quick routing of the payments. Arguably, the transaction details provided make it possible to identify most tiered payments.

Banks settling payments on behalf of client banks are referred to as senders and receivers, while the client banks using the service of settlement banks are called originators and beneficiaries (for an illustration, see Fig. 1). In the transaction data, there are multiple message fields, in some instances forming a chain of on-behalf information. Only the first and last BIC in a chain of payment information are used in the analysis to identify the ultimate client banks.

Internalized payments are out of scope here, as no information on internal transactions is available from payment system data. Such information is also not available to system operators and overseers. At the same time, internalized payments would distort the calculation of exposures between settlement and client banks.

Tiering is defined here in a narrow sense as the settlement on behalf of client banks that do not belong to the same banking group, similar to the definition employed by Benos et al. (2017) among others. In a wider sense, tiering can be seen as settlement on behalf of any client bank, irrespective of affiliations. Choosing the narrow definition here reflects the fact that intragroup settlement arrangements differ in economic terms from arrangements with outside banks. Intragroup payments may exhibit other properties due to broader interconnections between banks that entail more than payment operations stretching across other areas of banking. Therefore, extra-group relations provide a less biased measure of tiered settlement arrangements for investigating the effects of indirect settlement on participants’ behavior. Henceforth, we refer to tiering in the narrow sense and intragroup transactions as a separate category.

To distinguish extra-group transfers as tiered settlement, we use data from the SWIFT Bank Directory PlusFootnote 11 to classify payments according to banking group structures. The directory data includes information on individual BICs and their affiliated banking groups, which is mapped to payment transactions. Data from the directory is available from 2012 onward. Earlier data might not reflect banking group structures accurately, as mergers and other changes to the group structures are not accounted for. The further back in time one looks prior to the available data, the greater the inaccuracies, even though group structures typically remain relatively stable. The data includes only two previous years, starting in 2010, to avoid too much distortion. The data should exhibit only a few inaccuracies and is the most reliable information available.

When the originator and sender (or the receiver and beneficiary) of a payment have the same legal head institution, these payments are labeled as intragroup transfers. Tiering henceforth refers only to payments that are sent or received by settlement banks on behalf of an originator or beneficiary outside the banking group of the acting bank. Own payments are those transactions where no originator or beneficiary is involved in the transaction.Footnote 12 The same payment can fall into different categories on the sending and receiving side. For example, a payment can be labeled as tiered for the sending bank but labeled as an intragroup payment for the receiving bank.

4 Measures

This section describes the indicators employed to measure the impact of tiering. We construct measures related to liquidity consumption, timing and delay to analyze the effects of tiered settlement. The measures are calculated using only the aforementioned subset of TARGET2 transactions.

4.1 Liquidity use and consumption

Importantly, measures of liquidity use do not involve sources of liquidity such as participants’ account balances, liquidity transfers and monetary policy operations. In the setting relevant here, the actual liquidity needed by direct participants to settle payments in the course of a day is of interest.

The payments sent by participant i on business day b are given by:

With individual payment values in time interval t (ranging from 0 to T) given by s.

Respectively, payments received R are given by:

Total payments sent on a given business day in TARGET2 are given by the sum of payments sent by participants i (with i ranging from 1 to N) on day b:

Liquidity needed to settle payments during the day is given by the debit position of participants, which has a positive value here, while received payments factor in negatively.Footnote 13 The debit position D (running balance) of each participant at time interval t is given by the cumulated difference between payments sent (s) and received (r):

As described in Leinonen and Soramäki (1999), the liquidity needed to settle all payments during the day given their order is expressed by LN, which is calculated as the maximum of the running balance for the payment categories included in the study. This yields the daily maximum debit position of each participant. The calculation corresponds to the daily maximum intraday liquidity usage in the Basel Committee on Banking Supervision (2019) framework. The minimum is set at zero.Footnote 14 Consequently, negative debit positions, i.e. arising intraday credit positions, are not considered:

An LN above zero occurs when the value of the payments sent exceeds the value of payments received at any point during the day. A positive LN can also be referred to as maximum exposure, largest net debit position, or liquidity provision to the system for participant i on business day b.

To adjust for the total payment obligations of a bank in relation to its liquidity usage, we divide LN by total payments sent by a bank from Eq. (1). We call liquidity consumption LC which takes values between 0 and 1. A bank’s LC on a given day is stated as:

And on the system level, with \(S^b\) from Eq. (3) as:

As LC can never be larger than the sum of payments sent, the maximum value of 1 means all payments are sent by a participant before any payments are received. The minimum value of 0 means a participant does not draw on liquidity for settling payments, payments received fully funding any payments sent.

Following Denbee et al. (2014), we also use the cost-based measure of relative liquidity need for robustness, which is defined as:

Negative values signify that a bank provides less liquidity to the system relative to its share of payments, and vice versa for positive values.

4.2 Timing

One channel via which banks may manage liquidity is by postponing payments before they enter the system. Internal queue management is one tool that banks employ to shuffle payments and manage liquidity positions more efficiently.

Timing indicators show when payments are settled on average in the system, weighted by the value of payments. This gives us the average settlement time of the payments sent and received by participants during business hours (between 7 am and 6 pm). We follow Massarenti et al. (2012) who apply timing indicators to TARGET2 data, as described by Kaliontzoglou and Müller (2015).Footnote 15 One could assume that there is no reason for significant and consistent differences between payments by indirect participants and direct participants. Reasons why there may be consistent differences are banks’ business models and international payment obligations. For example, relative to European time zones, indirect participants located in the US are late payers and indirect participants located in Asia are early payers. Abstracting from such reasoning, the settlement time and time differences of own payments and tiered payments indicate how settlement banks manage different types of payments and if they delay them.

The average settlement time of payments sent TS of bank i on day b is given by:

The respective average receiving time of payments TR is given by:

The difference between payments sent and received TD indicates whether payments are recycled or whether individual banks, on average, send out payments before incoming payments arrive. The measure can therefore be interpreted as a proxy for the external delay of payments:

TD calculated on a system level would result in a value of zero. However, this does not hold for TD across different payment categories as payments are, for example, tiered on the sending side but not on the receiving side. Timing indicators serve as a proxy for bank behavior, as banks can actively decide on when to send payments of client banks to the system.

Assuming there are no structural reasons for timing differences between direct and indirect participants, differences in TD for non-tiered and tiered payments would result from direct participants treating tiered payments differently in terms of timing, for example via internal queue management. Contractual arrangements between direct and indirect participants are unknown. Therefore, postponing settlement of tiered payments may be in line with contractual provisions.

A negative value of TD indicates that banks send payments later than they receive them, while a positive value shows that banks send payments earlier than they receive them. Abstracting from potential structural differences, a negative value implies that banks recycle liquidity rather than providing it. If it is assumed that all payment instructions arrive at banks independently, meaning without structural differences in the timing of payments sent and received across categories, the difference in timing would measure external delay. Differences in timing would occur if banks rearranged payments and thus delayed payments outside (external to) the system.Footnote 16 The actual transmission and obligation to pay is unobserved, as payments show up in the data only upon entering the system. Assuming that payments do not differ structurally in terms of when direct participants receive payment instructions, payment timing can be regarded as a proxy for how participants manage their payments outside the system. Payment timing across different categories of payments can serve as an approximation for the treatment of payments in internal queues.

4.3 Delay indicator

Through delaying payments, direct participants may hold back liquidity and rely on incoming funds for making payments. Delays occur in two ways. First, as described above, participants can externally delay sending payments for settlement in the payment system. Second, within the system, a vdelay can occur between when payments are sent to the system and when they are actually settled in the system. Delays between when direct participants become aware of payment instructions and when payments are sent to the system are only observed indirectly. By contrast, delays within the system can be observed directly. Delays within the system occur when liquidity is not sufficient for settlement and payments are queued. Banks may also use different liquidity saving mechanisms available in TARGET2. One channel is assigning settlement priorities for processing in the system. Banks choose payment priorities ranging from normal to highly urgent, according to which payments are queued in TARGET2.Footnote 17 In addition, banks can reserve liquidity for highly urgent and urgent payments which is then not available for lower priority payments. Participants may also set bilateral and multilateral limits, thus limiting their net positions vis-à-vis other participants.

Following Kaliontzoglou and Müller (2015), we measure the delay in payments by comparing the introductionFootnote 18 and settlement time in the system relative to the latest possible settlement time. The latest possible settlement time considered here is the close of business. The indicator of delay is stated as:

where \(t_{1,i}\) is the time during the business day when the payment is available to be settled, \(t_{2,i}\) is the actual settlement time of the payment and T is the end of day, i.e. the latest possible settlement time.Footnote 19

5 Results

The results are organized starting with the overall levels of tiering and liquidity consumption. To formally test the effect of tiering on liquidity consumption, we then estimate a panel data model on the settlement bank level. Timing and delay indicators then identify the channels via which tiering reduces liquidity consumption.

For the interpretation of results, the following is implicitly or explicitly assumed:

-

Tiered and non-tiered payments do not differ structurally in terms of when payment obligations arise and when incoming payments are received by other participants. Without active liquidity management, similar arrival and sending times are expected. This assumption holds if the payment categories do not differ structurally due to their underlying business cases, emergence from activity in different time zones or other considerations by banks. Testing the assumption would require banks’ internal data and business logic.

-

Banks actively manage liquidity to limit intraday peaks. They can shuffle payments to some degree in order to limit their overall liquidity position across payments from different client banks as well as intragroup and their own payments.

-

Direct participants have some leeway in when they settle payments. Given internal queuing mechanisms for payment settlement, this assumption holds. However, contractual arrangements may limit leeway.

-

Resulting from the previous points, payment timing in the system differs largely due to liquidity management rather than different average instruction times across tiered and non-tiered payments.

5.1 Tiering and liquidity consumption

The share of tiered payments in total payments lies roughly at between 15 and 25 percent over the observation period (see Fig. 2). The number of tiered payments is higher on the sending side. However, in terms of values, the share of tiered payments is similar on the sending and receiving side. This means the average size of payments on the receiving side is larger for tiered payments. At the same time, indirect participants send higher volumes of payments than they receive, which can either indicate that client banks have a greater number of lower denominated payment obligations or that they break up payment obligations into smaller tranches compared to payments received. Overall, the level of tiering in TARGET2 is relatively low compared to other jurisdictions.Footnote 20

Share of tiered payments on system level. Note The share of tiering is calculated using the number and value of tiered payments divided by all payments included in the sample. Tiered arrangements are identified on the sending and receiving side, meaning the same payment can fall into different categories

Figure 3 shows liquidity consumption based on Eq. (7) calculated separately for tiered and non-tiered payment legs. Directly comparing outcomes in terms of liquidity consumption shows that participants use less liquidity for tiered transactions. However, isolating different categories of payments here does not take into account the overall liquidity position of participants. There might be a bias, as liquidity management may change during the day, depending on a participant’s net overall position. It cannot be ruled out that banks’ own payments are by nature (and not by choice) of higher priority and need to be settled earlier in the day, thereby increasing banks’ liquidity use for their own payments. Settlement banks also have no influence on when they receive payments. Aside from such caution, the consistently lower levels of liquidity consumption for tiered payments indicate that tiered payments leave settlement banks more discretion, enabling them to use less liquidity.

Liquidity consumption on system level. Note Moving averages over 30 calendar days. Liquidity consumption is calculated at the system level versus outgoing and incoming tiered payments only. For the indicator of tiered payments, non-tiered payments on the sending or receiving side respectively are ignored. Intraday balances do not reflect actual liquidity positions, but rather the hypothetical scenario in which only tiered payments would be processed

5.2 Model of liquidity consumption

To derive the effect of tiering on settlement banks’ daily liquidity consumption, we estimate a panel data model using bank and time fixed effects. We prefer fixed effects over random effects, as the latter assume the unobserved bank-level effects are uncorrelated with the independent variables. As the level of tiering and size of settlement banks probably factor into the unobserved effects, fixed effects seem more appropriate here. However, the results are robust to employing random effects.

Liquidity consumption is calculated daily across direct participants. As the independent variable of interest, the share of tiered payments is included. The share of tiering regards the sending side, as settlement banks can manage outgoing payments but not at what time they receive tiered payments. Table 2 reports summary statistics for the variables in the model. The share of tiering lies at 3 percent. This is the average across business days and banks, whereas many banks do not engage in tiering and relatively few large banks settle the majority of tiered payments. The share of tiered payments on a system level in Fig. 2 is therefore much higher.

We use the log of overall payments sent by direct participants as controls to account for size. Direct participants with more payments should be better able to manage liquidity, as they can smooth their liquidity usage by pooling payments [see Adams et al. (2010)]. Accounting for size makes it possible to abstract from such pooling effects. The average priority of the direct participant’s sent payments controls for the urgency of payments.Footnote 21 TARGET2 payments have the classifications normal, urgent or highly urgent. The difference in the average timing of payments sent and received proxies the degree of active liquidity management. In addition, we include the concentration of payments sent and received respectively, calculated as the Gini coefficient of payment values. The concentration of payments determines to some extent how granularly participants can manage liquidity. A higher concentration of payments inhibits participants from shuffling payments, as only a few large payments can be rearranged compared to a situation with smaller payments that can allow for more granular liquidity management. As controls for the cost of liquidity and the overall levels of liquidity, the overnight interbank money market rate and overall liquidityFootnote 22 are included. The money market rate is calculated using an algorithm proposed by Furfine (1999), applied to TARGET2 data following Arciero et al. (2016) and Frutos et al. (2016). We use a modified version of the latter to calculate the euro money market rate.Footnote 23 The algorithm identifies interbank loans by matching payments with plausible repayments the next business day.

We estimate the model with data from 2010 to 2019 using fixed effects for direct participants and time effects on a yearly basis to account for changes over time. Changes over time occur as a result of shifts in banking structures or payment processing. Events such as Brexit may trigger changes in how banks access TARGET2, for example by consolidating liquidity management or client banks using a different direct participant to route payments.Footnote 24

The effect of tiered arrangements may partly be picked up in bank fixed effects. Specifications without fixed effects exhibit higher coefficients and significance levels for tiering and other control variables.Footnote 25 The estimated model is therefore a conservative estimate of the effects of tiered arrangements.

The model for liquidity consumption is stated with the share of tiered payments by settlement bank i on business day b as the independent variable of interest and different control variables in vector \(X'_{ib}\). Bank-level effects are denoted as \(\alpha\) and yearly time effects as \(\pi\).

We estimate the model for the full sample between 2010 and 2019 using fixed effects for direct participants and yearly fixed effects. One issue in the case of TARGET2 is that direct participants with very low payment activity may distort results using relative measures. Small participants may only access TARGET2 for certain types of payments or are simply very small and do not actively engage with the system or play any significant role within the system.

We estimate the model for all direct participants, and for sub-samples of direct participants with at least 0.1 percent (128 direct participants) of overall traffic value and a threshold of 0.5 percent (50 direct participants). Results are presented in Table 3. In terms of significance and magnitude, the effect of tiering is quite stable within different sub-samples. The results for the sub-samples of participants are more meaningful, as larger settlement banks are more relevant in the context of tiered arrangements and of higher interest due to their importance in the payment system. Including only the largest 50 settlement banks seems most useful to investigate differences for those participants that are most critical to the system and most active in offering tiered arrangements.

The share of tiered payments has a negative impact on liquidity consumption in all specifications, meaning a higher share of tiered payments leads to participants using less liquidity relative to their payment obligations. The effect is statistically significant at least on the 10 percent level, and significance increases when only including larger participants. In terms of economic significance, the effect increases as smaller participants are dropped. While the change in one unit of tiering has an effect of roughly 0.05 on liquidity consumption, the effect increases to around 0.21 for large participants. The effect of tiering does not constitute a mere pooling effect, given the control variables and estimation using fixed effects.

With regard to liquidity risk, the findings suggest that settlement banks’ liquidity risk decreases as the share of tiering increases. This result holds controlling for other factors relevant to liquidity management and to settlement banks’ business models. Therefore, tiering allows settlement banks to save on liquidity input beyond mere pooling effects.

The size of direct participants measured by log value sent leads to increases in liquidity consumption. Larger participants thus appear to provide more liquidity relative to payments to the system, but the effect is not significant when smaller direct participants are dropped. This is counter-intuitive to the hypothesized direction. The fixed effects specification of the model may partly capture the effect of the size of participants, as larger participants take advantage of pooling effects, which could explain this result.

Unsurprisingly, the average difference in the timing of payments leads to increases in liquidity consumption and is significant at the 1 percent level in all specifications. Participants sending payments earlier than they receive them, on average, use more liquidity. As expected, a higher concentration of outgoing payments increases liquidity usage, while the opposite is true for the concentration of incoming payments. Highly concentrated sent payments give direct participants less leeway for liquidity management, as few large payments affect intraday balances. For incoming payments, the same reasoning applies, as receiving banks have less leeway in adjusting liquidity management when payments arrive in larger bulks. The coefficients are not significant for larger participants. Larger participants here refer to those settling higher payment values. Even when large participants’ payments are highly concentrated, there might still be leeway to rearrange payments. In contrast, a higher concentration for participants with few payments makes granular liquidity management difficult. A higher average priority increases liquidity consumption, although the effects are not significant for larger participants. While higher average priorities lead to payments being settled in a timelier manner and thus act as a drain on liquidity, larger participants may predominately use internal queuing mechanisms rather than priorities within the system.

It is expected that overall liquidity will have a positive impact, while the price of liquidity, as measured by the overnight money market rate, will have a negative impact. When money market rates are high, liquidity becomes more expensive for banks, prompting them to exercise greater caution in managing their liquidity. High levels of overall liquidity arguably loosen the liquidity constraints on banks and provide less incentive for active liquidity management. The effects are substantial and significant in all specifications for the money market rate. The effect of overall liquidity is positive and significant in most specifications. The R-squared is lower for specifications including smaller direct participants. A likely explanation is the heterogeneity of direct participants in those specifications. Direct participants with little payment activity and probably little liquidity management likely lead to the lower levels of explained variance.

For robustness, we estimate the model with an alternative outcome variable, the cost-based measure of liquidity need cLN:

Results in Table 4 show a similar picture. The effect of tiering is slightly less consistent and the significance of some control variables changes. The effect of payment concentration becomes less significant and changes direction for payments sent. Meanwhile, the effect of timing differences stays highly significant. The effect of liquidity cost mostly remains negative and that of overall liquidity is positive. However, for the cost-based liquidity need they are not statistically significant. Liquidity conditions and cost may be picked up to some degree by the yearly fixed effects. Notably, the explained variance is lower for the cost-based measure compared to liquidity consumption.

5.3 Timing

As one route of explanation for the results on liquidity consumption, timing differences are observed for tiered and non-tiered payments. Payment timing serves as a proxy for external delay, as banks queue payments internally before sending them to the system. The timing indicators from Eq. (11) are calculated for larger participants (0.1 percent threshold) and all other participants. For simplicity, these are called large and small participants, respectively. Types of payments are all payments sent and received, payments on banks’ own behalf, intragroup payments and tiered payments. Figure 4a shows timing differences are positive for large participants for their own payments (on average payments are sent before payments are received), but not for tiered payments. In terms of value-weighted timing, large participants receive tiered payments before they send them out, suggesting that banks may structurally delay tiered payments.

For non-tiered payments, the opposite is the case. Non-tiered payments are on average sent earlier than incoming payments arrive. Intragroup payments do not show a clear pattern over time. In earlier years, the timing differences of intragroup payments were in fact positive and only turned negative in recent years. At the same time, time differences for tiered payments are in lower negative territory for the full time period. Banks’ own payments hover above zero for most of the period before turning more positive in recent years, creating a wedge with intragroup payments. Given that results are value-weighted, figures for large participants are almost identical to the overall system level.

Comparing results with those of smaller participants, Fig. 4b paints a very mixed picture. Dynamics change over time and time differences for tiered payments move from negative to positive values. The volatile observations may be attributed to changes in group structures and payment routing. The dynamic likely also reflects that smaller banks settle payments on behalf of client banks less frequently and engage less actively in liquidity management.

Reasons for the observed differences between tiered and non-tiered payments could be that participants wait for incoming liquidity before sending payments on behalf of their client banks. This could be done by giving tiered payments a lower priority in internal or system queues. At the same time, client banks receiving payments earlier than sending their instructions to direct participants would also explain the observed differences. Importantly, the observed difference in the treatment of tiered payments may result from settlement banks limiting exposures to their client banks. Chapman et al. (2013) argue that settlement banks monitor client banks and offer settlement modes based on credit risk. Thus, settlement banks may limit exposures to their client banks by de-prioritizing client payments.

Importantly, timing differences can serve as a proxy for the internal payment queuing of direct participants. This assumes for different categories of payments that there is no difference between the sending and the receiving side in terms of when direct participants become aware of them. Whether this assumption is realistic or not is difficult to validate, as bank internal data is not available.

Timing differences. Note Moving averages over 30 calendar days. Results for large participants depicted on the left-hand side are almost identical to the overall system level. Large participants are those with at least 0.1 percent of overall sent payments over the observation period, accounting for 91 percent of traffic

Delay indicator for different payment types. Note Moving averages over 30 calendar days

5.4 Delay

Delay indicators from Eq. (12) depicted in Fig. 5 measure delays at the system level, i.e. when payments have been submitted to TARGET2 by direct participants. Indicators show uneven development over time. While tiered payments tended to exhibit higher levels of delay in earlier years, in recent years the levels have fallen below the delays in banks’ own payments. One reason could be that the expansion of monetary policy and the asset purchases of the Eurosystem have decreased active liquidity management incentives at the system level, as liquidity has become abundant.

As delays occur mainly due to a lack of liquidity within the system, ample liquidity probably contributed to fewer delays. In conjunction with timing differences, some banks may have shifted liquidity management outside the system, while system internal delays were further minimized. Over time, participants may have become more efficient in limiting delays at the system level. For recent years, we find no evidence of significant differences across tiered and non-tiered payments, meaning tiered payments are not delayed once sent to the system for settlement.

Interestingly, delays in TARGET2 have been accompanied by an overall decrease in the use of priorities over time (Fig. 6). We categorize priorities from normal (1) to highly urgent (3).Footnote 26 Value-weighted priorities are consistently lower for intragroup and tiered payments, while banks’ own payments receive higher priority.. The decrease in the use of prioritisation in TARGET2 suggests that such liquidity savings mechanisms have become less important over time. One possible explanation is that banks’ increasingly relied on internal mechanisms, while another explanation could be that they have dialed back liquidity savings arrangements due to ample available liquidity.

Value-weighted priorities for different payment types. Note Moving averages over 30 calendar days. Priority categories constructed with range from 1 (normal) to 3 (highly urgent)

6 Discussion

Liquidity needs for settling payments are lower when tiering is more prevalent and may lead to an operationally more stable system. At the same time, the heterogeneity of participants at a system level should be taken into account. Policies on tiering at a system level should consider cases of individual participants and their behavior, with special attention given to large and interconnected participants. The introduction of RTGS systems around the world has led to instant rather than delayed settlement at the cost of higher liquidity needs. Tiering reintroduces netting at a participant level, thus delaying settlement while reducing liquidity needs. Similar to RTGS systems introducing liquidity saving mechanisms, this offers benefits but also comes with risks. Higher degrees of tiering can thus be seen as tipping the scale in favor of liquidity savings.

Information on settlement banks’ internal procedures and contractual arrangements with client banks is available only implicitly. The analysis is limited to information from systems data focusing on payments once they enter TARGET2, which is only one part of banks’ overall liquidity position. Other systems, bilateral relationships and exposures may play a significant role in banks’ liquidity disposal. These limitations of the study point to the need to shift the focus of policy to individual participants and their interconnections, rather than focusing solely on systems as a whole. Importantly, agreements between direct and indirect participants cannot be observed. Taking a more holistic view of participants is highly beneficial. Gathering more data on participants and their internal procedures for settlement could shed more light on questions of potential free-riding, postponement of payments and exposures.

In terms of operational proficiency, tiering may have benefits that are not directly observable in the system. The results on a participant level in this study have highlighted differences between large and small participants and areas where closer investigation from a regulatory perspective would be useful. Tiering may pose additional risks, such as banks’ giving preference to own payments over tiered ones. This could put indirect participants at a disadvantage if direct participants face financial stress or experience outages. At the same time, tiering should not only be regarded as a source of risk.

Intraday positions are not necessarily risky on a system level, as banks supplying liquidity to other participants, by sending payments on a net basis for at least a limited time, exhibit high intraday exposures. However, effective liquidity management and its monitoring is aligned with risk considerations at a bank level.

Direct participants managing tiered payments in a way that allows them to save on liquidity could be beneficial for indirect participants, as the cost of liquidity is lower compared to a situation in which more participants join the system as direct participants. The more efficiently direct participants manage liquidity needs, the lower the fees paid by indirect participants should be.

The study has implications for the changing dynamics in payment systems and future infrastructures. When moving to instant payment in retail payments or a retail variant of a central bank digital currency (CBDC), there is a different trade-off compared to wholesale payments. As liquidity needs for payment funding are high in RTGS systems, immediate settlement comes at the cost of higher liquidity needs. In contrast, instant payments require low amounts of liquidity and immediate settlement and thus does not come with the same trade-off. Tiering can be seen as netting at a participant level and a tool for participants to save liquidity in wholesale systems, whereas in retail systems these benefits are likely to be small.

The implications of CBDC in the wholesale context depend on technology rather than representing a new concept. Funds transferred via TARGET2 are already a digital form of central bank money. If access and business logic remain unchanged alongside a new underlying technology, the results pointing to benefits of tiered settlement still hold.. The effect hinges not least on the form of providing wholesale CBDC. Providing separate tokens to circulate on platforms external to the RTGS will in general increase the liquidity needs whereas any interoperability solution that keeps central bank money in the RTGS will not have any impact. The impact could be partly mitigated by incorporating liquidity saving mechanisms into wholesale CBDC platforms. Another aspect is the degree of tiering. The use of new technologies such as DLT could induce a broader access to central bank money beyond banks and FMIs. This will certainly increase liquidity needs. If access remains restricted to banks and FMIs the indirect participation of non-bank corporates could be interpreted as an increase of the level of tiering since they will have to use accounts with banks or FMIs. Given the setup costs for system participation and active liquidity management, a tiered structure is likely preferable for a substantial share of non-bank corporations.

7 Conclusion

This paper investigates the impact of tiered settlement on liquidity consumption using TARGET2 transaction data. Our results show that tiering has beneficial effects on liquidity consumption and therefore reduces the liquidity risk of settlement banks, as they are able to meet payment obligations drawing on less liquidity. Tiered payments enable settlement banks to smooth their liquidity positions in the course of a day beyond a mere pooling effect, which is a direct result of aggregating payments at a participant level. The results are robust to including several controls and bank fixed effects. Lower liquidity needs due to tiering are therefore unlikely to occur because of pooling effects or heterogeneous liquidity management across banks. Timing and priorities of payments appear as channels via which tiered payments are incorporated into settlement banks’ active liquidity management. Payment timing as a proxy for external delay suggests tiered payments are treated with less urgency than settlement banks’ own or in-house payments. Payment priorities also point in this direction, as they are consistently lower for tiered payments. Results on payment delay within the system show no clear dynamic over time. This is in line with findings from the literature that the use of liquidity saving mechanisms in payment systems can be low, as banks use in-house tools to manage payment queues before entering the system.

While in line with contractual arrangements, some degree of “free-riding” or higher recycling of liquidity from client banks’ could pose risks for indirect participants, as their payments are treated with less urgency. However, the results are also consistent with settlement banks’ monitoring of indirect participants and differing terms of settlement for their clients. While seemingly less likely, sent and received tiered payments could inherently exhibit different characteristics due to geographical and other factors. If that was the case, tiered payments would be a way to reduce liquidity needs without introducing new risks.

As system overseers and operators typically have no access to bank internal contracts and data, our analysis relies on inference and system internal dynamics. Policy makers need to balance efficiency gains and potentially emerging risks. Future research could build on findings here and in the literature to derive welfare effects of tiered settlement. Arguably, internal processes of banks would need to be better understood to holistically evaluate the risks posed by tiered arrangements.

Notes

With regard to terminology, we use the term credit institution interchangeably with the term bank throughout the paper. Direct participants in a payment system are referred to as settlement banks, while indirect participants are referred to as client banks. For brevity, we at times refer to settlement banks as banks and direct participants as participants.

Pooling here does not refer to strategically timing payments but rather to liquidity savings due to offsetting when payments are concentrated among fewer participants.

TARGET2 refers to the second generation Trans-European Automated Real-time Gross Settlement Express Transfer System operated by the Eurosystem.

Pooling effects stem from banks settling more payments overall, which reduces their relative liquidity consumption compared to a situation in which multiple banks settle their own payments.

For an overview of RTGS system features and institutional design see CPSS (2005).

See ecb.europa.eu/paym/target/target2 and bankofengland.co.uk/payment-and-settlement/chaps for information and recent numbers.

In TARGET2, there are so-called indirect participants and addressable BICs (Bank Identifier Codes). In both cases, banks use a direct participant to connect to TARGET2, but only supervised credit institutions established within the EEA can become indirect participants. In the context of this study, the difference is not relevant, and we refer broadly to indirect participants.

This stems from the fact that banks typically use one or few main accounts for payments.

See swift.com/SWIFTRef for further information on the dataset.

In addition, cases where the originator or the beneficiary coincide with the sender or receiver are treated as own payments.

This is contrary to typical account statements.

Zero is the supposed start-of-day balance of the participant and serves as the starting point for calculation.

However, for tiered payments, no information is available to observe when client banks send instructions to direct participants. Therefore, the lag between becoming aware of payment instructions from client banks and sending them to the system is unknown.

It could be the case that tiered payments are sent to settlement banks later in the day. Note that on a system level, the timing of all payments sent and received is equal if all participants are observed. This is not the case for different categories of payments, such as tiered payments. The sending leg and receiving leg of payments may fall into different categories.

Given some payment types such as CLS payments have higher priorities but exhibit lower levels of tiering, this could influence results to some degree.

Participants can specify the date and time when a payment should be executed. The first attempt for settlement by the system will be made at that point in time. In those cases, we use the time for payment execution rather than when the instruction for later settlement reached the system.

Cut-off times differ for different types of payment. For simplicity, we assume the latest cut-off for all payments to be the end of the day.

For our subset of the data, tiering levels are higher compared to values on the overall system level. For details on yearly levels of tiering in TARGET2, see the respective Annual Reports on TARGET2.

Generally, priority setting is either an internal queue-management process within banks or observable when banks assign priorities for settlement using the functionality within the payment system, the concept employed here.

Calculated as the sum of current account holdings and use of the deposit facility, minus use of the marginal lending facility.

For a discussion on the measurement of money market rates, see Müller and Paulick (2020).

The model is robust to employing time fixed effects on a monthly basis. However, including monthly fixed effects leads to multicollinearity with the prevailing money market rate and overall liquidity. We therefore prefer the yearly fixed effects to allow for the interpretation of the effects of the money market rate and liquidity conditions.

Results are available upon request.

We deviate from the values in the original data, which start at 2 (normal), with 4 being urgent and a maximum of 7 being highly urgent.

References

Abbink K, Bosman R, Heijmans R, van Winden F (2017) Disruptions in large-value payment systems: an experimental approach. Int J Centr Bank 13(4):63–95

Adams M, Galbiati M, Giansante S (2010) Liquidity costs and tiering in large-value payment systems. Bank of England working papers 399, Bank of England

Alexandrova-Kabadjova B, Badev A, Bastos SB, Benos E, Cepeda-Lopéz F, Chapman J, Diehl M, Duca-Radu I, Garratt R, Heijmans R, Kosse A, Martin A, Nellen T, Nilsson T, Paulick J, Pustelnikov A, Rivadeneyra F, do Coutto Bastos MR, Testi S (2023) Intraday liquidity around the world. BIS Working Papers 1089, Bank for International Settlements

Arango CA, Cepeda FH (2017) Non-monotonic tradeoffs of tiering in a large value payment system. J Financ Market Infrastr 6(1):45–78

Arciero L, Biancotti C, D’Aurizio L, Impenna C (2009) Exploring agent-based methods for the analysis of payment systems: a crisis model for StarLogo TNG. J Artific Soc Soc Simul 12(1):686

Arciero L, Heijmans R, Heuver R, Massarenti M, Picillo C, Vacirca F (2016) How to measure the unsecured money market: the Eurosystem’s implementation and validation using TARGET2 data. Int J Centr Bank 12(1):247–280

Arculus R, Hancock J, Moran G (2012) The impact of payment system design on tiering incentives. RBA Research Discussion Papers 2012-06, Reserve Bank of Australia

Arjani N, Heijmans R (2020) Is there anybody out there? Detecting operational outages from Large Value Transfer System transaction data. J Financ Market Infrastr 8(4):23–41

Basel Committee on Banking Supervision (2019) Supervisory review process, Liquidity monitoring metrics. Technical Report SRP50, Bank for International Settlements

Bech M, Garratt R (2003) The intraday liquidity management game. J Econ Theory 109:198–219

Benos E, Ferrara G, Gurrola Perez P (2017) The impact of de-tiering in the United Kingdom’s large-value payment system. J Financ Market Infrastr 6(2/3):31–62

Berndsen R, Heijmans R (2020) Near-real-time monitoring in real-time gross settlement systems: a traffic light approach. J Risk 22(3):39–64

Chapman J, Chiu J, Molico M (2013) A model of tiered settlement networks. J Money Credit Bank 45(2–3):327–347

CPSS (2005) New developments in large-value payment systems. CPMI Papers 67, Bank for International Settlements, Committee on Payment and Settlement Systems

CPSS-IOSCO (2012) Principles for Financial Market Infrastructures (PFMI). CPMI papers 101, Bank for International Settlements, Committee on Payment and Settlement Systems and International Organization of Securities Commissions

Denbee E, Garratt R, Zimmerman P (2014) Variations in liquidity provision in real-time payment systems. Bank of England Working Papers 513, Bank of England

Diehl M (2013) Measuring free riding in large-value payment systems: the case of TARGET2. J Financ Market Infrastr 1(3):31–53

Diehl M, Müller A (2014) Analysis of the use and impact of limits. J Financ Market Infrastr 3(1):33–60

Fedwire Funds Service (2019) Disclosure. 23 December, Fedwire

Finan K, Lasaosa A, Sunderland J (2013) Tiering in CHAPS. Bank Engl Quarter Bullet 53(4):371–378

Frutos JC, Garcia-de Andoain C, Heider F, Papsdorf P (2016) Stressed interbank markets: evidence from the European financial and sovereign debt crisis. Working Paper Series 1925, European Central Bank

Furfine CH (1999) The microstructure of the federal funds market. Financ Mark Instit Instr 8:24–44

Garratt R, Martin A, McAndrews JJ (2014) Turnover in fedwire funds has dropped considerably since the crisis, but It’s Okay. Liberty street economics, Federal Reserve Bank of New York

Glowka M, Müller A, Friz LP, Testi S, Valentini M, Vespucci S (2022) TARGET2 analytical tools for regulatory compliance. ECB Occasional Paper 300, European Central Bank

Glowka M, Paulick J, Schultze I (2018) The absence of evidence and the evidence of absence: an algorithmic approach for identifying operational outages in TARGET2. J Financ Market Infrastr 6(2/3):63–91

Heijmans R, Heuver R (2014) Is this bank ill? The diagnosis of doctor TARGET2. J Financ Market Infrastr 2(3):3–36

Heuver R, Triepels R (2019) Liquidity stress detection in the European banking sector. DNB Working Papers 642, De Nederlandsche Bank

Kahn CM, Roberds W (2009) Payments settlement: tiering in private and public systems. J Money Credit Bank 41(5):855–884

Kaliontzoglou A, Müller A (2015) Implementation aspects of indicators related to payments timing. In: Diehl M, Alexandrova-Kabadjova B, Heuver R, Martínez-Jaramillo S (eds) Anal Econ Financ Market Infrastr. IGI-Global, pp 169–190

Klee E (2010) Operational outages and aggregate uncertainty in the federal funds market. J Bank Financ 34:2386–2402

Lasaosa A, Tudela M (2008) Risks and efficiency gains of a tiered structure in large-value payments: a simulation approach. Bank of England working papers 337, Bank of England

Leinonen H, Soramäki K (1999) Optimizing liquidity usage and settlement speed in payment systems. Research Discussion Papers 16/1999, Bank of Finland

Martin A, McAndrews J (2008) Liquidity-saving mechanisms. J Monetar Econ 55(3):554–567

Massarenti M, Petriconi S, Lindner J (2012) Intraday patterns and timing of TARGET2 interbank payments. J Financ Market Infrastr 1(2):3–24

McAndrews JJ, Rajan S (2000) The timing and funding of Fedwire funds transfers. Econ Policy Rev July:17–32

Müller A, Paulick J (2020) The devil is in the details, but so is salvation - Different approaches in money market measurement. Discussion Paper 66/2020, Deutsche Bundesbank

Rochet J, Tirole J (1996) Interbank lending and systemic risk. J Money Credit Bank 28(4):733–62

Rubio J, Barucca P, Gage G, Arroyoa J, Morales-Resendiz R (2020) Classifying payment patterns with artificial neural networks: an autoencoder approach. Latin Am J Centr Bank 1:1–4

Sabetti L, Heijmans R (2021) Shallow or deep? Detecting anomalous flows in the Canadian Automated Clearing and Settlement System using an autoencoder. Latin Am J Centr Bank 2(2)

Triepels R, Daniels H, Heijmans R (2018) Detection and explanation of anomalous payment behaviour in real-time gross settlement systems. In: Hammoudi S, Śmiałek M, Camp O, Filipe J (eds) Enterprise information systems, vol 321. Springer, pp 145–161

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors have no conflicting and competing interests to declare that are relevant to this article.

Additional information

Responsible Editor Julia Wörz.

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.