Abstract

Over the past half century, Western Europe has been part of varying currency regimes. Yet, whether under Bretton Woods, the European Monetary System, or the Euro, exchange-rate fluctuations have had an influence on these countries’ trade flows with the United States at the national and the industry level. This study looks at the case of Spain, examining the role of real exchange-rate fluctuations on trade with the United States for 74 industries. We find that the trade balances of only 40 industries are cointegrated with their macroeconomic determinants, but that 26 of these respond positively in the long run to a real depreciation. While industry characteristics do not seem to explain which industries are more likely to do this, we find that a relatively large share of industries in the Machinery sector see their trade balances improve after a depreciation.

Similar content being viewed by others

Notes

More precisely the lagged error-correction term is formed using \( {\text{ECM}}_{t - 1} = \ln \left( {\frac{{X_{i,t - 1} }}{{M_{i,t - 1} }}} \right) - \frac{{\hat{\theta }_{2} }}{{\hat{\theta }_{1} }}\ln Y_{t - 1}^{\text{US}} - \frac{{\hat{\theta }_{3} }}{{\hat{\theta }_{1} }}\ln Y_{t - 1}^{\text{Spain}} - \frac{{\hat{\theta }_{4} }}{{\hat{\theta }_{1} }}\ln {\text{REX}}_{t - 1} \) formula.

References

Andersen PS (1993) The 45°-rule revisited. Appl Econ 25(10):1279–1284

Bahmani-Oskooee M, Alse J (1994) Short-run versus long-run effects of devaluation: error-correction modeling and cointegration. East Econ J 20(4):453–464

Bahmani-Oskooee M, Hegerty SW (2009) The effects of exchange-rate volatility on commodity trade between the US and Mexico. South Econ J 75:1019–1044

Bahmani-Oskooee M, Hegerty SW (2010) The J- and S-curves: a survey of the recent literature. J Econ Stud 37(6):580–596

Bahmani-Oskooee M, Kara O (2005) Income and price elasticities of trade: some new estimates. Int Trade J 19(2):165–178

Bahmani-Oskooee M, Niroomand F (1998) Long-run price elasticities and the Marshall-Lerner condition revisited. Econ Lett 61(1):101–109

Bahmani-Oskooee M, Ratha A (2004) The J-curve: a literature review. Appl Econ 36(13):1377–1398

Bahmani-Oskooee M, Tanku A (2008) The black market exchange rate vs. the official rate in testing PPP: which rate fosters the adjustment process. Econ Lett 99:40–43

Bahmani-Oskooee M, Harvey H, Hegerty SW (2011) Empirical tests of the Marshall Lerner condition: a literature review. J Econ Stud (forthcoming)

De Vita G, Kyaw KS (2008) Determinants of capital flows to developing countries: a structural VAR analysis. J Econ Stud 35:304–322

Halicioglu F (2007) The J-curve dynamics of Turkish bilateral trade: a cointegration approach. J Econ Stud 34:103–119

Himarios D (1989) Do devaluations improve the trade balance? The evidence revisited. Econ Enq 27:143–168

Langwasser K (2009) Global current account adjustment: trade implications for the Euro area countries. Int Econ Econ Policy 6:115–133

Miles MA (1979) The effects of devaluation on the trade balance and the balance of payments: some new results. J Polit Econ 87(3):600–620

Mohammadi H, Cak M, Cak D (2008) Wagner’s hypothesis: new evidence from Turkey using the bounds testing approach. J Econ Stud 35:94–106

Narayan PK (2005) The saving and investment nexus for China: evidence from cointegration tests. Appl Econ 37:1979–1990

Narayan PK, Narayan S, Prasad BC, Prasad A (2007) Export-led growth hypothesis: evidence from Papua New Guinea and Fiji. J Econ Stud 34:341–351

Payne JE (2003) Post stabilization estimates of money demand in Croatia: error correction model using the bounds testing approach. Appl Econ 35(16):1723–1727

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Econ 16(3):289–326

Tang TC (2007) Money demand function for Southeast Asian countries: an empirical view from expenditure components. J Econ Stud 34:476–496

Warner D, Kreinin ME (1983) Determinants of international trade flows. Rev Econ Stat 65:96–104

Wong KN, Tang TC (2008) The effects of exchange rate variability on Malaysia’s disaggregated electrical exports. J Econ Stud 35:154–169

Acknowledgments

Valuable comments of two anonymous referees are greatly appreciated.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

1.1 Data definitions and sources

All data are annual (1962–2009) and are collected from the following sources:

-

(a)

The World Bank.

-

(b)

The International Financial Statistics of the IMF.

1.1.1 Variables

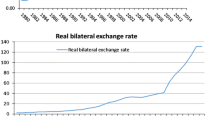

\( \left( \frac{X}{M} \right) \) = For each industry, this is the ratio of Spain’s exports to the United States over its imports from the United States. The data for 74 industries come from source a; Y Spain = Spanish real GDP. The data come from source b; Y US = US real GDP, source b; REX = Real bilateral exchange rate between the Spanish peseta and the dollar, defined as \( \left( {\frac{{{\text{CPI}}_{\text{US}} \times {\text{NEX}}}}{{{\text{CPI}}_{\text{Spain}} }}} \right), \) where CPI is the Consumer Price Index. NEX is the nominal bilateral exchange rate defined as number of pesetas per dollar. Thus, an increase in REX reflects a real depreciation of Spain’s currency. Beginning in 1999, the Euro/dollar nominal rate is converted to pesetas at the rate of 166.386 pesetas per Euro. All these variables come from source b.

Rights and permissions

About this article

Cite this article

Bahmani-Oskooee, M., Harvey, H. & Hegerty, S.W. Regime changes and the impact of currency depreciations: the case of Spanish–US industry trade. Empirica 40, 21–37 (2013). https://doi.org/10.1007/s10663-011-9176-1

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10663-011-9176-1