Abstract

This research documents changes in employment and wages in the Netherlands for different types of workers. We compare 2017 to 2023 using regression-adjusted wages to make sure changes in composition of the workforce do not influence our estimates. The research period has been characterised by high labour demand, negative supply shocks, high levels of inflation and economic lockdowns, all of which have contributed to substantial labour-market dynamics. Our findings suggest that employment has been growing by 2 percent in the period 2017–2023, of which 1.8 percent has been due to additional workers finding employment. Women have experienced the largest increase in employment, while the employment of men on temporary contracts has slightly fallen. Wages have been rising for workers at the bottom of the wage distribution. From the median of the wage distribution onwards real gross hourly wages have been fallen. The most likely explanation for rising wages at the bottom is the stepwise increase in minimum wages enforced by new labour-market legislation.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Labour markets in many OECD countries have been historically tight (OECD, 2023).Footnote 1 Employment seems to be stable at a very high level, with the average number of hours worked per worker rising over the last ten years in all countries. The demand for labour remains high as revealed by a high number of vacancies and expansionary policies in many countries to deal with societal challenges such as climate change. As a result, nominal wages are rising fast, which should increase households’ disposable income levels.

At the same time, several supply and demand shocks have affected output, unemployment and inflation from 2020 onwards (Baqaee & Farhi, 2022). For example, macroeconomic shocks like the COVID-19 pandemic, the war in Ukraine, and rising trade barriers have influenced prices in an unprecedented way (Bernanke & Blanchard, 2024). A striking observation is the significant reduction in wage inequality due to rising wages at the bottom of the wage distribution, occasionally referred to as the unexpected compression of the wage distribution (Aeppli & Wilmers, 2022; Autor et al., 2023; Blanchet et al., 2022).Footnote 2 Also, at the microeconomic level household choices seem to have changed, which has had an impact on labour supply. Lee et al. (2023) document a fall in labour supply in the United States from 2020 onwards, which they refer to as the great resignation. People who lost their jobs in the midst of the COVID-19 pandemic have not returned to the labour market, especially in low-wage jobs (Chetty et al., 2024). In addition, those who are employed seem to have reduced their number of working hours, which is sometimes referred to as quiet quitting.Footnote 3

The small and open Dutch economy is likely to be exposed above average by these shocks. Especially the labour market is likely to be affected, not least because of its unique structure with relatively many workers being employed on temporary contracts. For example, employment protection legislation for workers with temporary contracts is substantially lower than for workers employed in permanent positions (OECD, 2021).Footnote 4 This likely increases wages and working hours during booms when there is a lot of demand, but makes workers vulnerable to lower wages and unemployment during economic downturns when labour demand is low. In addition, the average number of hours worked by Dutch employees is relatively low (1,344 h annually in 2023), with the average female employee working only 1,157 h annually (CBS, 2023). Because of this unique labour-market structure, combined with a period of macroeconomic instability, there have been concerns about trends in disposable income for different types of workers.

This research documents and interprets trends in wages and employment in the Netherlands in the period 2017–2023. We use administrative data available at the remote-access facility of Statistics Netherlands (CBS). These data contain information about employees in the Netherlands. We are unable to include self-employed workers into the analysis because we cannot measure hours worked and income in a consistent way and make a sound comparison with employees.

Our main findings can be summarised as follows. First, we document the changes in employment by distinguishing changes in the number of workers and changes in the number of working hours. We find, contrary to Lee et al. (2023) a rise in both the number of workers in employment (an increase of 1.8 percent in the period 2017–2023) and working hours (an increase of 0,2 percent). During the COVID-19 pandemic employment measured in employed workers dropped by 1.1 percent, while the change in the number of hours worked remained positive over the entire period (measured from year to year). When we split the sample into men and women and workers on a permanent and temporary contract, the results remain similar except for the fact that employment of men on temporary contracts has slightly dropped (by 1.0 percent during 2017–2023). At the same time, the fraction of men with permanent contracts increased by 2.5 percent, likely due to the recent policy incentive to make permanent contracts more attractive (and temporary contracts more expensive to employers). This suggests that labour-market tightness in the Netherlands is not the result of a reduction in labour supply (both measured in the number of workers and number of hours). It also implies that quiet quitting or a great resignation is not a phenomenon influencing the Dutch labour market in this period.

Second, we estimate wage equations and document the results in terms of real wage development at each decile of the wage distribution. Changes in wages are measured from January 2017 to June 2023 (the most recent month of data available at this time). We use the consumer price index to calculate real wages. Our findings suggest that for both men and women who work on temporary contracts there has been real wage growth up to the 40th percentile of the wage distribution. A likely explanation is the rise of the minimum wage in this period, which went up by over 20 percent.Footnote 5 For workers on permanent contracts the wage level is substantially lower at all points in the wage distribution. Only male workers at the lowest decile have experienced real wage growth. What is striking is that the higher the wage in 2017 the higher has been the real wage loss in the period 2017–2023. This suggest a compression of the wage distribution, which is consistent with the U.S. finding, where an unexpected compression has taken place after the economic lockdowns during the COVID-19 pandemic (e.g., Autor et al., 2023). The reason for this compression in the Netherlands is not entirely driven by market forces of labour demand and labour supply, but also by rising minimum wages enforced by new regulation.

The remainder of the paper is organised as follows: Sect. 2 presents the most salient aspects of our data and describes the methodology for analysing wage and employment trends. In Sect. 3 a detailed decomposition of changes in employment is presented in terms of changes in working hours and changes in the number of workers throughout the period 2017–2023. Section 4 documents wage developments for men and women working on temporary and permanent contracts at deciles of the wage distribution. Section 5 concludes.

2 Data and Strategy

We make use of administrative data available through remote access facilities of Statistics Netherlands (CBS). These data contain detailed information about all Dutch citizens, including employment status, sector of employment, wages and a range of individual characteristics such as age, gender and educational level. We compose a database with monthly information on employment, sector of employment, gross monthly income, number of working hours (according to a person’s contract), the type of contract of all employees and individual characteristics (age, gender and level of education).

We make a distinction between two types of contracts: permanent contracts and temporary contracts. Permanent contracts refer to employment agreements with an indeterminate period of time with no end date, whereas temporary contracts refer to those workers who are employed on fixed-term contracts (among other temp-workers and workers who are on call). In the Dutch context this is an important distinction. The main reason is that the Flexibility and Security Act, introduced in 1999, is an important driver of the growth of temporary contracts in the Netherlands (Bolhaar et al., 2018). The Act raised employment protection for permanent workers, while at the same time it created more opportunities for flexible employment to grow. With the Employment and Security Act of 2015 the Dutch government tried to decrease gaps in job security, costs and risks between various employment relationships and new labour-market legislation implemented in 2020 (the Balanced Labour Market Act) reduces the attractiveness of temporary contracts further.Footnote 6 Self-employed workers are excluded from the analysis because it is impossible to determine working hours and the part of their revenues which should be considered as labour compensation.

In June 2023, 7.9 million people are employed in the Netherlands for at least 40 h a month. This marks an increase of nearly one million persons compared to June 2017. Not only has the workforce expanded, individuals have also extended their working hours. The average number of hours worked each month has increased from 136.9 to 138.3 h.

By making use of gross monthly income and working hours we compute gross hourly wages. We analyse the development of hourly wages in the period from January 2017 until June 2023. For each month in the data, we determine the total number of hours worked and an individual’s total wage. We limit the sample to individuals who have worked between 40 and 200 h within one month. The reason is that we want to exclude very small parttime jobs of youngsters who are still in school and have a job on the side, and people who report unusually high working hours which are above what is agreed upon in collective agreements and are most likely mismeasured in the data.Footnote 7 On a monthly basis, we compute the gross hourly wage of each employee by dividing the total gross income by the number of hours worked. The analysis distinguishes men and women (next to temporary and permanent contracts). Biesenbeek and Volkerink (2023) have shown the importance of analysing the outcomes of men and women separately when explaining wage and employment dynamics in the Dutch labour market. They find in an empirical analysis of wage differentials between workers a gap of on average 10 percent between temporary and permanent contracts (adjusted for observables in their models). The estimated coefficients suggest that the wage gap is largest for men who are employed as temporary employees.

To study changes in the wage distribution at the macroeconomic level, we compare gross hourly wages over time by taking into account compositional differences in the sample and we make use of the consumer price index (CPI) to convert nominal wages into real wages. Schneck (2021) analyses the wage distribution in the Netherlands between 2001 and 2016. She also makes use of administrative data and observes that wage dispersion increases evenly across the wage distribution. This means that—in contrast to other countries—it is not influenced by increases in the upper wage percentiles. Wage inequality among female workers seems to be somewhat lower than for men but has increased at a similar rate in the period 2001–2016. Including part-time female workers decreases wage inequality for all female employees, which is in line with Biesenbeek and Volkerink (2023). Ter Weel (2003) analyses trends in wage inequality between 1986 and 1998 using survey data. He obtains estimates suggesting a small rise in wage dispersion in the 1990s and changes in the composition of labour supply. We therefore adjust for differences in age, gender, educational level, sector, working hours and contract type in the analysis.Footnote 8

The results of the regression analysis are shown in the Appendix (Table 5) for January 2017, June 2017 and June 2023. We estimate separate models for men and women and workers on temporary and permanent contracts. The results of estimating the wage equations (corrected for inflation, so real wages) lead to the following conclusions. Over time wages rise, which can be obtained by studying the constant term. Table 5 shows the coefficients by age and level of education. In general, wages rise with age, which is a reflection of working experience that is positively rewarded by employers. Relative to employees between 40 and 50 years old, the coefficients for male workers and female workers with flexible contracts become smaller over time. This suggests that the premium for working experience becomes lower between 2017 and 2023. A similar pattern is observed when three levels of education are distinguished.Footnote 9 Relative to those with medium levels of education, the wage penalty for low-educated male workers drops and the wage premium for high-educated workers falls between 2017 and 2023. This seems to be consistent with the estimates obtained in the United States in the same period (e.g., Autor et al., 2023). The assertion that older employees have more working experience and earn higher incomes does not seem to apply to female workers with permanent contracts. All coefficients for workers aged 50 or above are negative, indicating that female workers in these age groups typically earn less on average compared to female workers aged 40–50 with similar levels of education. A possible explanation for this observation is the increased labour-force participation among younger women in terms of working hours and their increased level of education in the past decades. Older women may have gained lower levels of working experience because it was relatively uncommon for women to work long hours when they were younger. Consequently, women in this age group obtained a negative working experience premium.Footnote 10

3 Employment

Figure 1 shows changes in total working hours in the Netherlands. We distinguish between the extensive and intensive margin by reporting changes in the number of employees and changes in the number of working hours in the period 2017–2023.

Annual changes in employment in number of employees and hours worked, 2017–2023

The overall annual growth of employment has been 2.0 percent in the period 2017–2023, which is shown by the bar in the final column of Fg. 1. A breakdown into persons and hours reveals that 90 percent of annual employment growth is due to more persons being employed as employees.Footnote 11 Annual changes in employment are reported by the first six bars in the figure. With the exception of the change in 2019–2020 the number of persons in employment has risen faster than the number of hours worked. The number of hours worked has also increased throughout all years (with the exception of 2018–2019 and 2021–2022), but much less in comparison to the number of persons in employment as employees. When considering two subperiods and excluding the COVID-19 period (2019–2020), annual employment growth has been a little bit faster in the pre-pandemic period than afterwards.

Lee et al. (2022) present a similar analysis for the United States in which they also distinguish between the pre- and post-COVID-19 period. They obtain an increase in both the extensive (5.1 percent) and intensive (1.6 percent) margin in the period 2013–2019 and a decrease in both margins in the period 2019–2022 of 5.8 and 6.2 percent. Our breakdown suggests that employment growth continues to develop after the pandemic with an obtained growth of 2.3 and 0.1 percent on the extensive and intensive margin. In the period of lockdowns we observe an increase in the number of working hours. This is likely due to the measures taken during COVID-19 pandemic. During this period many jobs have been saved by substantial government interventions, whereas in the United States funds have been distributed to households directly to foster consumer liquidity and not aiming directly at saving jobs. In addition, new labour-market regulation has been implemented in the Netherlands in this period of time, which creates an incentive for employers to transform temporary contracts into permanent contracts. Another possible explanation is that primarily workers with smaller jobs lost their jobs during the pandemic. This may have led to an increase in the average number of hours worked, without workers directly increasing their hours.

Not all types of employees have experienced similar changes in employment in the Netherlands. We distinguish between women and men and those who work on temporary and permanent contracts. Table 1 shows the changes at both the extensive and intensive margin. The top panel shows the changes in employment for women. The number of hours worked by female employees on temporary contracts (130.6 million hours by 1.2 million workers in June 2017) has grown by 2.1 percent in the period 2017–2023. Most of the annual change is due to an increase in the number of female employees (1.8 percent) and only 0.3 percent is the result of more hours per job. The number of hours worked by female employees on permanent contracts is almost twice as large in June 2017 (258 million hours by 2.1 million workers). The increase is also larger (3.6 percent), again mostly due to an increase in the number of workers (2.8 percent) and not so much by an increase in the number of hours worked in each job (0.9 percent). The average number of hours worked by female employees on permanent contracts has increased faster than the same number for employees on temporary contracts. This increases the gap in hours which was already around seven hours in 2017.

The bottom panel displays the same numbers for male employees. The number of male workers on temporary contracts is 0.1 million larger than the number of female workers. The difference in the total number of hours worked is larger because on average male workers work more hours during one month (137.4 vs. 113.4 in June 2017). The change in temporary work among male employees is negative. There are two main reasons. First, during the COVID-19 pandemic there has been a large outflow of male workers, which has not recovered fully by June 2023. The outflow has been larger for males than for females (20.8 vs. 13.9 percent in terms of total hours worked). Second, the number of male workers on permanent contracts has risen substantially during the COVID-19 pandemic. The level of employment of male employees on permanent contracts is already larger in June 2017 and also the growth during the pandemic has been larger compared to female workers.

A number of periods and events stand out in Table 1. First, during the pandemic employment decreases significantly. Especially among individuals with a temporary contract an unprecedented drop in employment is observed. Second, a significant shift occurred from temporary to permanent contracts, contributing to a rise in the number of permanent contracts. This shift can be partially attributed to the introduction of new labour-market legislation in January 2020, but a causal link is impossible to find due to different events occurring at the same time. Nevertheless, the legislation makes it more attractive for employers to offer employees a permanent contract by increasing the tax premium employers have to pay when employing workers on temporary contracts. The shift from flexible to permanent contracts is also a sign of a relatively tight labour market. In such a tight labour market employers seem to be hoarding labour by trying to retain their workforce during the pandemic.Footnote 12 Finally, we observe that in the period 2020–2023 the growth of total hours worked is larger among those on temporary contracts compared to the period 2017–2019 (we leave out the year 2020 in this comparison). This suggests a rebound in temporary work, which results in a positive growth rate for female employment and a recovery for male employment. Among workers on permanent contracts, the growth in the period 2017–2019 has been larger than in the post-COVID-19 period.

4 Wages

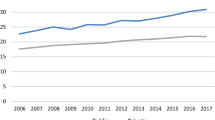

Figure 2 shows in four panels the real wages and percentage changes in real wages for different groups of workers from 2017 to 2023. The data reveal an overall negative trend in real wage growth for the majority of employees, shown by the dark line (and measured on the right axis). This is mainly caused by the high level of inflation during the past few years. At the median, male workers with permanent contracts and female workers have experienced an average decrease of around 3 to 4 percent in their real hourly wages. For male workers with temporary contracts, this decline was only 0.5 percent.

Real hourly wage development for men and women with different types of contracts as a function of income percentiles

Not all types of employees have experienced similar changes in their hourly wages. Tables 2 and 3 report wages in 2017 adjusted to 2023 prices and compares those wages to nominal wages in 2023 for similar workers (that is, using the regression-adjusted wages following Table 5). The comparison thus uses similar workers in both years. We distinguish between temporary and permanent workers and compute the wage growth required to face stable real wages in each third column. The estimated wages suggest that at the lower end of the income distribution there have been increases observed in real hourly wages between 2017 and 2023. This is the case for male employees with a permanent contract up to the 10th percentile and male and female employees with a temporary contract up to the 40th percentile. On the other hand, employees at the top of the income distribution have experienced the largest declines in their real hourly wages. Some employees have seen their hourly wage decrease by up to nine percent in the period 2017–2023. Overall, the results suggest that wage developments have been worse the higher the hourly wage and that it is more unfavourable for employees with permanent contracts compared to those with flexible contracts.

The estimated wages over time indicate a compression of the wage distribution, similar to findings in the United States where wage compression is largely explained by market forces influencing labour supply and demand. In the Netherlands, a significant factor likely driving this wage compression is the increase of minimum wages enforced by new labour-market legislation. Minimum wages have been rising stepwise since 2017. In January 2017, the minimum hourly wage for employees aged 21 and older working 36 h a week was €9.95. By January 2023, this minimum hourly wage has risen to €12.40, an increase of almost 25 percent.Footnote 13 Converted to a 32-h workweek, this is equal to a monthly income of €1,380 in 2017 and €1,719 in 2023. In Tables 2 and 3 it can be seen that 2017 adjusted wages for men in temporary contracts up to the 25th percentile and for women in temporary contracts up to the 35th percentile are below the minimum wage of €1,719 in 2023. This means that these employees have faced an increase in their minimum wages between 2017 and 2023, which explains the negative required wage growth in the third column. However, employees earning slightly more than the minimum wage are also more than compensated for inflation. This is the case for male and female workers on temporary contracts up to the 40th percentile, which is consistent with Teulings (2003) who shows that minimum wage increases have an upward effect on wage above the threshold as well.

Temporary workers in the Netherlands at the bottom of the wage distribution earn wages below the adult minimum wage when we convert hourly wages to monthly wages based on a 32-h workweek. The reason for this observation is that these workers are either young (the monthly minimum wage for youngsters between 15 and 18 years old varies between 600 and 1.000 euros) or that there is some degree of measurement error in the number of hours worked, which is likely to be relatively large for workers with fewer and flexible hours worked (Abowd & Card, 1989). We obtain information about average hours worked, which is likely to be relatively unstable over time for workers on flexible work arrangements (Bolhaar et al., 2018).

The above conclusions are further supported by the four panels in Fig. 3. Figure 3 shows the real gross wage development since January 2017 at the 10th, 50th and 90th percentile of the wage distribution. The vertical axis shows the wage increases, where a level of 1 means that the real wage growth is equal to 0. Figures below (above) one suggest real wage decreases (increases). The results are again presented for the four types of employees. It can be observed from the panels that the 10th percentile of both male and female workers who work on temporary contracts (left figures) have experienced a positive wage growth throughout all periods, with the highest growth among women in 2023 with a rate of 26 percent between 2017 and 2023. The hourly wage of employees at the 50th percentile remained stable from 2017 to 2021, followed by a significant decrease from 2022 onwards. Wage growth for workers at the 90th percentile of the real gross wage distribution with temporary contracts remained negative throughout the entire period under investigation. Both male and female workers with permanent contracts (right figures) experienced a constant real hourly wage until 2021 across the entire wage distribution. Starting from 2022 onwards, men at the 10th percentile maintained a steady real gross hourly wage, while those at the 50th and 90th percentiles faced a decline of approximately four to eight percent. Women encountered a decline at all three percentiles.

Real gross wage development since January 2017

5 Conclusion

This research has documented employment and wage trends in the Netherlands during a period of economic turbulence. Labour markets in all OECD-countries have been historically tight and employment is at historically high levels in most countries due to very high levels of aggregate demand. At the same time, negative supply shocks—such as COVID-19 and the war in Ukraine—have hit economies leading to very high peaks of inflation.

Our results suggest that employment in the Netherlands has risen in the period 2017–2023. This rise is mostly due to more workers being employed and not so much because employees have worked more hours. This finding is observed for both men and women and workers on temporary and permanent contracts. At the same time, the number of employees on permanent contracts increases, which is likely to be due to labour-market tightness and new legislation which increases the cost of employing workers on temporary contracts. Women still work fewer hours compared to men and the gap does seem to be closing slowly. From an international point of view, there have been concerns about the great resignation during the COVID-19 pandemic and quiet quitting which refers to the phenomenon of workers adjusting their hours downward. We do not obtain such findings for employees in the Netherlands. In contrast, both working hours and the number of employed workers have gone up.

Our second set of results concerns wage changes. We use regression-adjusted wages to compute real gross hourly wage developments. This means that we maintain a constant composition of the workforce to be able to make a sound comparison over time. The development of these estimated wages suggests that there have been real gross hourly wage gains at the bottom of the wage distribution. At the top of the wage distribution, real gross hourly wages have fallen up to nine percent. The most likely explanation for wage growth at the bottom of the wage distribution is the stepwise increase of minimum wages enforced by new labour-market regulation in the Netherlands. This finding is consistent with wage developments in the United States but unlikely to be due to demand and supply forces. In the United States there has been wage compression, due to lower levels of labour supply at the bottom of the wage distribution. Together with a rise in demand for low-wage workers, real gross hourly wages have increased. In the Netherlands we obtain real gross hourly wage gains up to the level of the new minimum wage level and slightly above this threshold.

Our analysis has a number of limitations. First, we have been able to document changes in employment and wages for employees but not for all workers. The share of self-employed workers has risen substantially, mainly due to attractive fiscal regulations. It is impossible to measure working hours and the share of revenue which is labour income for this group of workers. Second, our data are limited to mid-2023 while the period of negative supply shocks together with high labour demand is continuing. This merits further analyses of wage and employment trends in the next couple of years. Finally, negative supply shocks have led to very high levels of inflation but high aggregate demand also contributes to inflation. The extent to which negative supply shocks (which make societies worse off) and high aggregate demand (which merits wage rises to balance labour demand and supply) seem to lead to balanced employment and wage growth is still in debate (e.g., Bernanke & Blanchard, 2024). Evidence is suggesting that inflation seems to be driven by wage growth in the last quarters, whereas supply shocks were drivers of inflation in 2021 and 2022.

6 Notification

This research received no specific grant from a funding agency in the public, commercial or not-for-profit sector. There is no conflict of interest to disclose. We comply with the ethical and integrity codes for carrying out scientific research and reporting about it, as specified by the Dutch Research Council: https://www.nwo.nl/sites/nwo/files/documents/Nederlandse%2Bgedragscode%2Bwetenschappelijke%2Bintegriteit_2018_NL.pdf.

Notes

The Employment Outlook (OECD, 2023) shows that labour markets remain tight even as the recovery after the COVID-19 pandemic has stalled. Average unemployment levels in most countries are at a low not seen since the early 1970s. Also nominal wages seem to be catching up with high and persistent inflation, which means that real income of workers are rising in almost all OECD countries.

In the United States this observed reversal of the trend in wage inequality is due to a shrinking gap between low-wage and median-wage workers. In contrast, the gap between top and median workers has persisted (Aeppli & Wilmers, 20,220; Autor et al., 2023). Spending recovered to baseline levels because of substantial income support measures, unemployment benefits, and other programs that led to an increase in disposable income at the bottom of the distribution (Blanchet et al., 2022).

Faberman et al. (2022) calculate that the willingness to work extra hours seems to have disappeared in the United States from 2022 onwards.

The OECD observes that employment protection between different types of contracts is unbalanced. Labour-market legislation to encourage the use of permanent contracts is in place but the effectiveness is still unclear. If effective, it should make economic growth and the labour market more inclusive and resilient (OECD, 2021).

For fulltime working adults (21 years and older) the monthly minimum wage has increased from 1,615 euro in January 2019 to 1,995 euro from the 1st of July 2023 onwards.

In the sample for analysis we do observe young workers (i.e., younger than 18 years old) who work more than 40 h a week. We include those workers in the analysis because they influence changes in the wage distribution at the bottom of the market.

We distinguish 21 different sectors using the Dutch Industry Classification (SBI 2008). We identify three educational levels: low, intermediate and high. Individuals without any basic qualification are classified under the low educational level. Those who completed secondary vocational education (MBO) are considered intermediate and individuals with higher vocational education (HBO) or university (WO) degrees are classified as highly educated.

The educational level is unknown for some employees, particularly older workers and labour migrants. For this reason, a dummy variable for employees with an unknown educational level is included in the regression.

Kahn (2016) investigates the wage premium for permanent jobs relative to temporary jobs in thirteen European countries in the period 1995–2001. He also finds that for women, the permanent job wage premium is lower for older workers and those with longer job tenure.

Figure 4 in the Appendix shows the same figure for all employees (regardless of the number of hours they work). The results are qualitatively similar, but show a total employment rise of 1.8 percent. Across years there are larger fluctuations in changes of number of workers and hours. The post-COVID-19 effect is slightly larger when taking all employees into account, but the pre-COVID-19 effect is somewhat smaller.

The IMF (2024) reports an increasing level of labour-market tightness in the Netherlands from 2014 onwards.

In 2023 the minimum hourly wage is applicable to employees aged 21 years and older.

References

Abowd, J. M., & Card, D. (1989). On the covariance structure of earnings and hours changes. Econometrica, 57(2), 411–445.

Aeppli, C., & Wilmers, N. (2022). Rapid wage growth at the bottom has offset rising US inequality. Proceedings of the National Academy of Sciences. https://doi.org/10.1073/pnas.2204305119

Autor, D., Dube, A. & McGrew, A. (2023). The unexpected compression: Competition at work in the low wage labor market. NBER Working Paper No. 31010.

Baqaee, D., & Fahri, E. (2022). Supply and demand in disaggregated Keynesian economies with an application to the COVID-19 crisis. American Economic Review, 112(5), 1397–1436.

Bernanke, B. & Blanchard, O. (2024). An analysis of postpandemic inflation in 11 economies. Peterson Institute for International Economics Working Paper No. 24–11.

Biesenbeek, C., & Volkerink, M. (2023). The price of flexible jobs: Wage differentials between permanent and flexible jobs in the Netherlands. De Economist, 171(4), 367–401.

Blanchet, T. Saez, E., & Zucman, G. (2022). Real-time inequality. NBER Working Paper No. 30229.

Bolhaar, J., de Graaf-Zijl, M., & Scheer, B. (2018). Three perspectives on the Dutch growth of flexible employment. De Economist, 166(4), 403–432.

CBS. (2023). National accounts 2023. Statistics Netherlands: Den Haag.

Chetty, R., Friedman, J.N., Stepner, M. & Opportunity Insights Team. (2024). The economic impacts of COVID-19: Evidence from a new public database built using private sector data. Quarterly Journal of Economics, 139(2), 829–889.

Faberman, R.J., Mueller, A.I. & Şahin, A. (2022). Has the willingness to work fallen during the covid pandemic? NBER Working Paper No. 29784.

IMF (2024). Kingdom of the Netherlands—the Netherlands. IMF Country Report No. 24/86.

Kahn, L. M. (2016). The structure of the permanent job wage premium: Evidence from Europe. Industrial Relations, 55(1), 149–178.

Lee, D., Park, J. & Shin, Y. (2023). Where are the workers? From great resignation to quiet quitting. NBER Working Paper No. 30833.

OECD. (2021). Economic policy reforms 2021. Going for growth: Shaping a vibrant recovery. Paris: OECD.

OECD. (2023). Employment outlook 2023. OECD.

Schneck, C. (2021). Trends in wage inequality in the Netherlands. De Economist, 169(2), 253–289.

Ter Weel, B. (2003). The structure of wages in the Netherlands, 1986–98. Labour, 17(3), 361–382.

Ter Weel, B. (2018). The rise of temporary work in Europe. De Economist, 166(4), 397–401.

Teulings, C. N. (2003). The contribution of minimum wages to increasing wage inequality. Economic Journal, 113(490), 801–833.

Van der Wiel, K. M. (2010). Better protected, better paid: Evidence on how employment protection affects wages. Labour Economics, 17(1), 16–26.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix 1

Appendix 1

Changes in employment in number of employees and hours worked, 2017–2023

Percentage effects for age groups and educational levels on hourly wages; men with permanent contracts

Percentage effects for age groups and educational levels on hourly wages; men with flexible contracts

Percentage effects for age groups and educational levels on hourly wages; women with permanent contracts

Percentage effects for age groups and educational levels on hourly wages; women with flexible contracts

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Klinker, I., ter Weel, B. Wages and Employment in the Netherlands, 2017–2023. De Economist 172, 233–256 (2024). https://doi.org/10.1007/s10645-024-09438-2

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10645-024-09438-2