Abstract

This paper presents results from an econometric analysis of Russian bank defaults during the period 1997–2003, focusing on the extent to which publicly available information from quarterly bank balance sheets is useful in predicting future defaults. Binary choice models are estimated to construct the probability of default model. In the first part of the paper we analyse bank survival over the financial crisis of 1998. We find that preliminary expert clustering or automatic clustering improves the predictive power of the models and incorporation of macrovariables into the models is useful. Heuristic criteria are suggested to help compare model performance from the perspectives of investors or banks supervision authorities. In the second part of the paper we use the probability of default models developed in the first part in rolling windows to analyse the Russian banking system trends after the crisis 1998.

Similar content being viewed by others

Notes

Violation of CBR standards, first of all the capital adequacy ratio (H1).

Models for other clusters are found in Peresetsky et al. (2004), and are also available by email request.

Coefficients of the separate logit models are presented at the Appendix 5.

Again, data kindly provided by the Mobile Information Agency.

Again as in Sect. 3.1, using a two-year lag between bank data and observed status provides the best results.

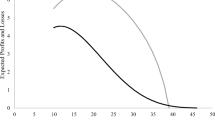

In the case where the investor has incentive to invest all his/her money in “reliable” banks, the optimal behavior is simply to invest all money S into one, the most “reliable” bank.

The Russian Deposit Insurance Agency adopted this methodology in 2007 for the purpose of estimating the adequacy of the Deposit Insurance Fund for possible losses in each following year.

References

Aldrich JH, Nelson FD (1985) Linear probability, logit and profit models, Quantitative Applications in the Social Sciences Series no. 45. SAGE Publications, Beverly Hills

Altman EI (1968) Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. J Finance 23(4):589–609

Altman EI, Rijken HA (2004) How rating agencies achieve rating stability. J Bank Finance 28(11):2679–2714

Altman EI, Marco G, Varetto F (1994) Corporate distress diagnosis:Comparisons using linear discriminant analysis and neural networks (the Italian experience). J Bank Finance 18(3):505–529

Amato JD, Furfine CH (2003) Are credit ratings procyclical? BIS Working Papers No. 129. http://www.bis.org/publ/work.htm

Basel Committee on Banking Supervision (2004) International convergence of capital measurement and capital standards. Bank for International Settlements, June 2004. http://www.bis.org/publ/bcbs107.htm

Bobyshev AA (2001) Russian banks: typical strategies and financial intermediation. NES Best student papers series, BSP/01/047E. http://www.nes.ru/en/programs/econ/rescen/preprints/2001/bobyshev

Borio C (2003) Towards a macroprudential framework for financial supervision and regulation? BIS Working Papers No. 128. http://www.bis.org/publ/work.htm

Borodovsky M, Peresetsky A (1994) Deriving non-homogeneous DNA Markov chain models by cluster analysis algorithm minimizing multiple alignment entropy. Comput Chem 18(3):259–268

Bovenzi JF, Marino JA, McFadden FE (1983) Commercial bank failure prediction models, Federal Reserve Bank of Atlanta. Econ Rev 68:14–26

Cole RA, Gunther JW (1995) Separating the likelihood and timing of bank failure. J Bank Finance 19(6):1073–1089

Cole RA, Gunther JW (1998) Predicting bank failures: a comparison of on- and off-site monitoring systems. J Fin Serv Res 13(2):103–117

Demirguc-Kunt A, Detragiache E (1998) The determinants of banking crises in developed and developing countries. IMF Staff Pap 45(1):81–109

Engelman B, Porath D (2003) Empirical comparison of different methods for default probability estimation. Quanteam Research Paper. http://www.quanteam.de/publications.html

Espahbodi H, Espahbodi P (2003) Binary choice models and corporate takeover. J Bank Finance 27(4):549–574

Estrella A, Park S, Peristiani S (2000) Capital ratios as predictors of bank failure. FRBNY Econ Policy Rev 6(2):33–52

Godlewski C (2004) Are bank ratings coherent with bank default probabilities in emerging market economies? SSRN. http://ssrn.com/abstract=588162

Gunther JW, Moore RR (2003) Early warning models in real time. J Bank Finance 27(10):1979–2001

Jagtiani J, Kolari J, Lemieux C, Shin H (2003) Early warning models for bank supervision: simper could be better, Federal Reserve Bank of Chicago. Econ Perspect 27(3):49–60

Kolari J, Glennon D, Shin H, Caputo M (2002) Predicting large US commercial bank failures. J Econ Bus 54(4):361–387

Komulainen T, Lukkarila J (2003) What drives financial crises in emerging markets? Emerg Mark Rev 4(3):248–272

Korobow L, Stuhr DP (1983) The relevance of peer groups in early warning analysis, Federal Reserve Bank of Atlanta. Econ Rev 68:27–34

Lawrence CL, Smith LD, Rhoades M (1992) An analysis of default risk in mobile home credit. J Bank Finance 16(2):299–312

Lennox C (1999) Identifying failing companies: a reevaluation of the logit, probit and DA approaches. J Econ Bus 51(4):347–364

Löffler G (2004) An anatomy of rating through the cycle. J Bank Finance 28(3):695–720

Marchesini R, Perdue G, Bryan V (2004) Applying bankruptcy prediction models to distressed high-yield bond issues. J Fixed Income 13(4):50–56

Martin D (1977) Early warning of bank failure: a logit regression approach. J Bank Finance 1(3):249–276

Mathe C, Peresetsky A, Dehais P, van Montagu M, Rouze P (1999) Classification of Arabidopsis thaliana gene sequences: clustering of coding sequences into two groups according to codon usage improves gene prediction. J Mol Biol 285(5):1977–1991

Ohlson JA (1980) Financial ratios and the probabilistic prediction of bankruptcy. J Account Res 18(1):109–131

Peresetsky A, Кarminsky A, Golovan S (2004) Probability of default models of Russian banks. Bank of Finland, BOFIT Discussion Papers No 21/2004

Sahajwala R, van den Bergh P (2000). Supervisory risk assessment and early warning systems. Basel committee on banking supervision. Working paper 4. http://www.bis.org/publ/bcbs_wp4.htm

Scott AJ, Wild CJ (1986) Fitting logistic models under case-control or choice-based sampling. J R Stat Soc Ser B 48(2):170–182

Segoviano MA, Lowe P (2002) Internal ratings, the business cycle and capital requirements: some evidence from an emerging market economy. BIS Working Papers, 117. http://www.bis.org/publ/work.htm

Stone M, Rasp J (1991) Tradeoffs in the choice between logit and OLS for accounting choice studies. Account Rev 66(1):170–187

van Soest AHO, Peresetsky AA, Karminsky AM (2003) An analysis of ratings of Russian banks. Tilburg University CentER Discussion Paper Series 2003/85

Wescott SH (1984) Accounting numbers and socioeconomic variables as predictors of municipal general obligation bond ratings. J Account Res 22(1):412–423

Westgaards S, van der Wijst N (2001) Default probabilities in a corporate bank portfolio: a logistic model approach. Eur J Oper Res 135:338–349

Wiginton JC (1980) A note on the comparison of logit and discriminant models of consumer credit behaviour. J Fin Quant Anal 15(3):757–770

Acknowledgments

We are deeply grateful to the participants of the BOFIT seminar and participants of the econometrics seminar in the Center for Economic Research of the Tilburg University for insightful discussions. We also thank Tilburg University Professors Bertrand Melenberg and Arthur van Soest for many helpful comments. We are grateful for BOFIT researchers Iikka Korhonen and Tuomas Komulainen for reading the draft of the paper and their suggestions for improvement. Credit also to Andrei Petrov at the Mobile Information Agency for providing Russian bank data. We thank the students of the New Economic School involved in the bank research project. Special thanks to Greg Moore, his help makes the paper readable. A. Peresetsky worked on this paper as a visiting researcher at the Bank of Finland’s Institute for Economies in Transition (BOFIT) and would like to express his gratitude to BOFIT for the excellent, friendly research environment. Naturally, we are responsible for any erors or omissions.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix 1

Appendix 2

Distribution of Russian bank defaults, 1991–2002. (The August 1998 crisis is indicated with a black bar)

Appendix 3

Appendix 4

Rights and permissions

About this article

Cite this article

Peresetsky, A.A., Karminsky, A.A. & Golovan, S.V. Probability of default models of Russian banks. Econ Change Restruct 44, 297–334 (2011). https://doi.org/10.1007/s10644-011-9103-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10644-011-9103-2