Abstract

This Study Analyzes the Factors that Explain the Evolution of banks´ Nonperforming loan Ratios Worldwide. We use a Sample of 1,631 Entities from 111 Countries Grouped into the Eight Central Regions in the World, with Information Corresponding to the Period 2007–2021. Applying Panel data Methods and an Extensive set of both Specific and Macroeconomic Variables, the Results show that Nonperforming loan Ratio is Determined by a Series of Specific Factors, Regardless of where or when they Operate. These Results may be Helpful to Minimize the cost of Building Models for the Nonperforming loan Analysis in the world´s most Critical Regions.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The financial system influences economic development through its impact on choices related to saving and investment, risk management, efficient distribution of funds, and facilitation of transactions. The banking sector plays a pivotal role in sustaining the financial system in nations with bank-centric economic structures. Consequently, the banking sector largely dominates the financial market. Technological advancements in the financial industry have opened up opportunities for expanding the range of products and customer bases. The rising demand for loans, and banks’ eagerness to meet these demands by assuming higher risks, elevates the likelihood of loans turning into Non-Performing Loans (NPL) (Erdas & Ezanoglu, 2022).

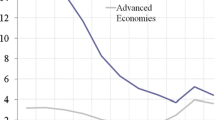

The recent financial crises have been the focus of the attention of professionals and academics due to their essential economic consequences (Tomczak, 2023; Agnello and Sousa, 2012). These crises have arisen mainly due to the increase in NPL in the banking system since, by eliminating the structural profitability of banks, they are forced to limit credit in the system (Park & Shin, 2021). Financial entities that operate in stable, well-regulated markets and with acceptable levels of economic growth do not usually have high NPL rates. On the other hand, those entities with the worst efficiency ratios and reduced levels of competition tend to have the highest NPL (Ferreira, 2022). These regional, temporary, and structural differences that impact the NPL have been present in the recent experience of all world regions. Figure 1 shows the NPL evolution in the world´s eight central regions (Africa, Eastern Europe, Far East and Central Asia, Middle East, North America, Oceania, South and Central America, and Western Europe). Apart from the logical differences between regions, we can observe how the NPL ratio evolves consistently in three stages. The first general increase in NPL after the bursting of the financial bubble of 2008–2009 derived from the strong non-payments produced, especially by the real estate sector. Subsequently, between 2015 and 2018, a relative general decrease in NPL (with some exceptions, such as Africa) was mainly facilitated by a general environment of abnormally low-interest rates that reduced the financial cost of indebted agents and enabled debt repayment. And finally, since the end of 2019, a phase derived from the COVID-19 pandemic, with a different evolution in each region. In this last stage, some areas, such as Western Europe, Africa, or South and Central America, suffered severe rises in NPL. In contrast, other areas, such as Eastern Europe, Oceania, or Far East and Central Asia, either did not suffer NPL increases or had lower ratios.

Impaired loans/gross customer loans by country (%)

NPL stand out as a crucial metric on credit risk, directly impacting the banking system and indicating the likelihood of losses. The magnitude of NPL plays a vital role in maintaining the stability of a country’s banking sector. So, NPL not only reflects credit risk but also influences the performance of banks, potentially leading to financial and economic strain (Khan et al., 2020). Consequently, a surge in NPL could directly endanger the future and consistency of the banking system and indirectly impact the real economy. Therefore, minimizing NPL is a fundamental requirement for enhancing financial markets and fostering economic growth, and conducting a thorough credit risk analysis is imperative to mitigate losses in the loan-providing process (Mahyoub & Said, 2021).

Recognizing the significance of banks in the national economy and acknowledging that lending risk poses a substantial threat to banks, it becomes crucial to examine the NPL factors. A rise in NPL may prompt banks to increase their lending rates to offset the reduction in profits. While this action could decrease the NPL ratios that impede lending conditions for banks, it might adversely impact sectors in need of funds (Erdas & Ezanoglu, 2022). Therefore, it is essential to analyze different factors, such as bank-specific and macroeconomic factors, providing crucial insights for banks, banking regulators, and supervisory bodies. The significance of understanding the determinants of NPL lies in the potential to identify a set of warning indicators, enable timely intervention and minimize the likelihood and associated costs of crises (Msomi, 2022). High NPL ratios have been shown to deteriorate bank balance sheets, reduce credit growth, and delay recovery after financial problems (Aiyar et al., 2015). The increase in NPL indicates relevant risks for the financial system, both for liquidity reasons and from the point of view of profitability (Ghosh, 2015). Therefore, the NPL ratio can be interpreted as a relevant indicator of the probable arrival of a financial crisis (Reinhart & Rogoff, 2010). In any case, the determining factors of the NPL in a country or different countries have been a relevant element in previous financial literature (Nkusu, 2011; Louzis et al., 2012; Castro, 2013; Rachman et al., 2018; Ferreira, 2022; Theong et al., 2022). However, these previous studies have focused only on specific countries or regions, and currently, there is a demand for studies that address this problem from a global perspective (Gjeçi et al., 2023; Chowdhury et al., 2023; Umaternate et al., 2023). To cover this gap in research on NPL, this study aims to analyze the factors that explain the NPL ratio worldwide. We examine a data panel of 1,631 banks corresponding to 111 countries in 8 world regions, which has given rise to 24,915 observations for the period 2007–2021. As possible factors associated with the variation in the NPL ratio, a set of 12 variables selected from previous literature has been used (Chaibi & Ftiti, 2015; Castro, 2013). With this panel data, we have constructed a Generalized Method of Moments (GMM) based on the proposal of Arellano and Bond (1991), eliminating the biases that may arise with the traditional panel data estimators.

The present research adds significant value to the existing literature. Firstly, our study delves into the factors influencing the global NPL ratio, not confining itself to a single country or a limited set of countries. As Kartikasary et al. (2020) note, the anticipated substantial increase in NPL over the next few years could significantly impact liquidity and banks´ profitability, posing challenges to the overall well-being of a country. The stability and prosperity of the economy are closely tied to the success of the banking sector, where NPL directly impacts the efficacy of financial intermediation. In situations where accurate loan risk analysis is not conducted, economic downturns or crises in a country may lead to non-repayment of loans (Erdas & Ezanoglu, 2022). Secondly, our study offers a potential tool to assist regulatory authorities and banks. NPL serves as a metric for the bank system’s performance and profitability and captures the central attention of policymakers and bank management. Reinhart and Rogoff (2010) stress that scrutinizing the factors contributing to NPL holds substantial importance for policymakers. NPL can serve as an early indicator of a banking crisis, significantly impeding economic growth and diminishing economic efficiency. To avert a worrisome increase in NPL, it becomes imperative for banking regulatory authorities to formulate new regulations. However, any policy response from the concerned authority in this context necessitates a thorough understanding of the factors causing NPL in a specific economy. Therefore, the examination of NPL factors holds significance for both regulatory authorities and banks, contributing to enhancing the financial system’s functioning and regulation and preventing financial instability (Ahmed et al., 2021).

The rest of the paper is organized as follows. Section 2 presents a review of the literature. Section 3 describes the data, variables, and methods used. Section 4 presents the results and discussion. Finally, the main conclusions, implications, and suggestions for future lines of research are recorded.

2 Literature Review

In previous literature, the factors identified as significant in explaining the behaviour of the NPL ratio can be classified into specific factors (internal to each entity) and macroeconomic factors (relative to the country or region where the entity operates). Concerning the specific factors that affect NPL, the profitability, efficiency, solvency, size, and diversification of the business stand out. For example, different studies have analyzed the relationship between NPL and profitability in the financial system. Such is the case of Messai et al. (2013), who, applying a panel analysis to a sample of 85 banks in Italy, Greece, and Spain for the period 2004–2008, identified the entity’s profitability as a significant factor and with an inverse relationship concerning the NPL ratio. Ghosh (2015) concluded that the profitability of financial institutions reduced NPL in the U.S. from 1984 to 2013. Rachman et al. (2018) analyzed the case of 36 listed commercial banks in Indonesia from 2008 to 2015. Using a regression panel model, they concluded that profitability and credit growth inverse influence NPL. Similar conclusions were obtained by Kjosevski and Petkovski (2021) for commercial banks in the Baltic countries from 2005 to 2016. Recently, Ciptawan and Melly (2023) have demonstrated the inverse relationship between profitability and NPL using a sample of 46 listed financial institutions in Indonesia.

Regarding the relationship between efficiency and NPL, Espinoza and Prasad (2010) pointed out that the most efficient banks have lower NPL ratios. And this relationship has also been subsequently confirmed in the studies by Louzis et al. (2012), Koju et al. (2018), Partovi and Matousek (2019), Ozili (2019), and Khan et al. (2020). Likewise, the effects of solvency and capital quality have been revealed by Kjosevski et al. (2019) for the Macedonian banking sector in 2003–2014 and by Ersoy (2022) for the Turkish banking sector between 2010 and 2019. Similar results regarding the inverse relationship between solvency and NPL were reported in Keeton’s studies (1999), Salas and Saurina (2002), Klein (2013), and Makri et al. (2014). However, other studies found no significant relationship between solvency and NPL (Louzis et al., 2012; Cheng et al., 2016).

For its part, the direct and positive relationship between the size of the entity (measured as the total volume of assets) and the NPL ratio has been pointed out by Ahmed et al. (2021) for commercial banks in Pakistan and by Koju et al. (2018) for a sample of financial institutions in Nepal. Previously, Salas and Saurina (2002) had pointed out this significant relationship between size and NPL for Spanish commercial banks in 1985–1997 and El-Maude et al. (2017) for listed commercial banks in Nigeria from 2010 to 2014. Ghosh (2015) and Hughes and Moon (2022) using data from U.S. banks from 1984 to 2016.

In general, and concerning the diversification of the banking business, it has been found that financial institutions that have a lower proportion of the traditional banking business (taking deposits and granting credit) are more exposed to financial crises, which seems to demonstrate a clear relationship between the business model of each entity and its risk profile (Ercegovac et al., 2020). Khan et al. (2020) showed the inverse relationship between diversification and NPL ratio for a sample of listed financial institutions in Pakistan. Likewise, Lee et al. (2019) verified that entities with greater diversification are less susceptible to taking more significant risks in their credit business and better control their NPL ratio. On the contrary, Ismail et al. (2017) and Ahmed et al. (2021) demonstrated a positive relationship between diversification and NPL, indicating that when a bank has different sources of income, it does not concentrate on its natural credit business and NPL increases due to selecting the worse quality of its debtors. However, in other previous studies, the relationship between diversification and NPL is not significant (Rachman et al., 2018; Putri et al., 2020).

Other specific factors influence an entity’s risk profile and NPL ratio. Specifically, they are factors such as corporate governance and banking regulation. Some authors point out that robust corporate governance indicators of entities help reduce NPL (Balgova et al., 2017). For their part, Gonzalez-Garcia and Grigoli (2013) showed that in countries where the public sector has direct participation in the capital of financial entities, the financial industry is more likely to give more credit to this sector, generating higher NPL ratios due to worse corporate governance models and more significant conflicts of interest. Similarly, Lee et al. (2022) demonstrated, through a panel of 32 listed financial institutions in Taiwan for the period 2008–2015, that financial institutions with the worst corporate governance (measured as those with a higher level of related party transactions, or with personal profiles of administrators with higher indebtedness).

Among macroeconomic factors, economic growth, interest rates, inflation, unemployment, and exchange rates have been significant (King and Plosser, 1982; Bernanke and Gertler, 1999; Kiyotaki & Moore, 1997). Numerous studies conclude that NPL increases when the economic environment deteriorates (Cifter et al., 2009; Ali and Daly, 2010; Louzis et al., 2012; Castro, 2013). For example, Mitrakos and Simigiannis (2009) analyzed the relationship of certain macroeconomic factors with the likelihood of debt default in Greece. They found that unemployment and income level are highly correlated with the probability of debt default. Espinoza and Prasad (2010) used a sample of 80 Gulf Cooperating Council entities (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates) from 1995 to 2008. Applying a dynamic panel, they concluded that the NPL increases as economic growth decreases and interest rates rise.

Ali and Dali (2010) conducted a comparative study of the U.S. and Australia from 1995 to 2009. They determined that the main factors affecting NPL were gross domestic product (GDP), interest rates, industrial production, and total indebtedness. However, they warned that there are differences in the effect of the same variables on both economies, pointing out that the U.S. economy is much more sensitive to macroeconomic shocks than the Australian economy. For their part, Nkusu (2011) and Louzis et al. (2012) demonstrated that volatility in macroeconomic variables can generate unemployment, inflation, or changes in interest rates, impacting the behaviour of financial institutions and their NPL ratio. Subsequently, Castro (2013) used a sample of financial institutions from Spain, Portugal, Italy, Ireland, and Greece for the period 1997–2011, concluding that the main factors affecting NPL are GDP growth, the index housing prices, unemployment, interest rates, the exchange rate, and credit growth. Staehr and Uusküla (2017) used a panel of data from European Union entities between 1997 and 2017, confirming that the key macroeconomic factors in reducing the NPL ratio are GDP growth, inflation, and indebtedness. Other factors, such as the current account balance and house price levels, were determinants for some regions within the European Union, especially in Central and Eastern Europe. Ozili (2019) analyzed the effect of economic development on NPL using a sample of 134 countries from 2003 to 2014. Their conclusions indicate that economic development, measured by the presence of foreign financial institutions and the quality of financial intermediation, is related to NPL because low levels of supervision by regulators lead to lower-quality profiles of credit.

Likewise, Syed and Aidyngul (2022) carried out an analysis for the period 1995–2019 based on the Generalized Method. Using a sample of developed and developing countries, they determined that the main macroeconomic factors affecting NPL are economic growth, inflation, and interest rates. Chowdhury et al. (2023) analyzed the specific and macroeconomic factors affecting NPL in Bangladesh from 2007 to 2018. They concluded that credit growth, leverage, and interest margin reduce the NPL ratio. In contrast, inflation and GDP growth are the macroeconomic factors with influence. More regional research on the NPL ratio in the financial system has been developed by Zeng (2012) on the banking system in China, Koju et al. (2018) on the financial system of Nepal, Kjosevski et al. (2019) on the case of Macedonia, Staehr and Uusküla (2020) for banks in the European Union, Petkovski et al. (2021) for Poland, Rathnayake (2021) in Sri Lanka, Žunić et al. (2021) for Bosnia Herzegovina, Lemma-Lalisho (2022) for Ethiopia, and Umaternate et al. (2023) for Indonesia. However, there is no relevant literature on global analyses that model the behaviour of NPL in the financial system, except for specific cases such as that of Beck et al. (2015), which analyzes the macroeconomic factors that determine NPL in a sample of 75 countries over ten years. Their findings suggest that GDP growth, share prices, the exchange rate, and the interest rate on loans are the factors that significantly affect the NPL ratio. Also, the study by Boumparis et al. (2019), with a panel of 72 countries in 1998–2016, delved into the relationship between sovereign risk and NPL of financial institutions. Ari et al. (2021) analyzed the dynamics of the NPL throughout 92 banking crises since 1990, identifying that the critical factors for the appearance of problems are high public and private debt ratios, fixed exchange rates, and low profitability. Likewise, Gjeci et al. (2023;) analyzed how the NPL ratio affects credit growth for a sample of banks from 42 countries from 2000 to 2017.

Recently, there have been investigations into the effects of fiscal consolidation on NPL in heavily indebted countries, particularly in the aftermath of the global financial crisis and the subsequent sovereign debt crisis. To address the NPL time persistence issue, researchers utilized a dynamic panel data estimator, which provides an unbiased estimation. The results indicate that fiscal consolidation measures tend to raise NPL levels. This is because such measures limit the capacity of households and businesses to service their loans (Rahman et al., 2023). In addition, recent studies such as the one by Barra and Ruggiero (2023) delve into the influence of factors unique to individual banks on the NPL ratio within Italy from 1994 to 2015. The findings from the analysis indicate that the critical determinants of NPL are regulatory credit policies, capital reserves, the amount of credit extended, and the level of intermediation costs. Kartal et al. (2023) analyze the synchronized movement between NPL and economic growth in Turkey. This investigation utilizes quarterly data from the first quarter of 2005 to the fourth quarter of 2019 and employs the wavelet coherence method. The results demonstrate that there is a noteworthy susceptibility of NPL and economic growth during the specified period at various time intervals. Second, in the long run, economic growth in Turkey significantly influences NPL. Third, economic growth is a short-term factor causing NPL in Turkey, particularly between 2007 and 2010. In their study, Hassan et al. (2023) focus on Islamic banking within the context of Bangladesh. Their findings emphasize the need for future research to carefully consider this sector. This includes investigating areas such as green banking, the integration of Islamic microfinance with Islamic banking, the efficiency of Islamic banking, governance concerns, and risk management within the Islamic banking framework.

3 Data, Variables and Methods

3.1 Data

This study uses an unbalanced data panel made up of 1,631 banks corresponding to 111 countries in 8 world regions (Africa, Eastern Europe, Far East and Central Asia, Middle East, North America, Oceania, South and Central America, and Western Europe), which has given rise to 24,915 observations for the period 2007–2021. Bank-specific drivers are taken from the Orbis Bank Focus by Moody’s database. For its part, the macroeconomic data have been extracted from the World Development Indicators by the World Bank database and the Bank for International Settlements public databases. Table 1 reports the banks´ distribution in the sample among the world´s regions, and Fig. 2 illustrates the allocation of countries to each of the areas considered.

Sample countries’ regional distribution

3.2 Variables

As possible factors associated with the variation in the NPL ratio, a set of 12 variables selected from previous literature has been used (Chaibi & Ftiti, 2015; Berger and DeYoung, 1997; Hasan & Wall, 2004; Nkusu, 2011; Louzis et al., 2012; Castro, 2013). These independent variables include, on the one hand, specific aspects of the entities (provisions for insolvencies, efficiency ratio, leverage, the relative weight of the non-lending business, size, and profitability) and, on the other hand, macroeconomic factors of the countries (inflation, GDP per capita, GDP growth, unemployment, interest rate, and exchange rate). Table 2 offers a detailed definition of all the variables used in the research.

3.3 Empirical Strategy

Given that the panel data are unbalanced, as each variable is observed during a different period, it is necessary to consider the persistence over time of the NPL structure. To do this, our model introduces the lagged dependent variable (NPLi,t−1), as shown in Eq. (1).

where α is a constant term; i = 1,. . ., N and t = 1,. . ., T denote the cross-section and time dimension of the panel, respectively; Xit is the vector of explanatory variables; β is the vector of coefficients; vi are the unobserved country-specific effects, and εit is the error term.

In addition, we have considered that constructing the dynamic model econometric biases may arise with the traditional panel data estimators (grouped OLS, fixed effects, and random effects). To eliminate these biases, we use the GMM proposal by Arellano and Bond (1991), which uses a difference to avoid the correlation between the unobserved effect at the individual level (vi) and the variable NPLi,t−1. These considerations appear in Eqs. (2) and (3).

Due to the construction of Eq. (3), the new error term (εi,t − εi,t−1) is correlated with the lagged dependent variable NPLit−1. In this case, assuming that a serially uncorrelated error term and an explanatory variable are weakly exogenous, the moment conditions expressed in (4) and (5) are proposed.

Even with the previous, Blundell and Bond (1998) show that their lagged levels are weak instruments for the difference regression equation for persistent explanatory variables. Arellano and Bover (1995) and Blundell and Bond (1998) provide a solution to avoid the possible biases above by using an estimator that combines regression on differences with regression on levels through the additional moment conditions (6) and (7).

In some cases, the approach taken by Arellano and Bover (1995) and Blundell and Bond (1998) may cause estimation bias. Roodman (2009) points out that the difference and the GMM system can lead to a risk of instrument proliferation. To avoid this potential problem, it is suggested to modify Eq. (4) as it appears in (8).

Consequently, we employ the extended set of moment conditions, Equations (4 to 7), to generate consistent and efficient parameter estimates. On the other hand, the consistency of the GMM estimator also depends on the fact that the error terms do not show serial correlation and that the instruments are valid. To verify these assumptions, we use the Sargan and Roodman tests.

4 Results

4.1 Descriptive Statistics

Table 3 shows the main descriptive statistics of the variables used in the research. Regarding the dependent variable, the region with the highest NPL ratio is Eastern Europe, with a mean value of 10.2%. Africa, for its part, has maintained an NPL ratio that is also high, with an average of 7.62% in the observed series. On the other hand, North America and Oceania are the regions that have historically had the lowest levels of default, maintaining an average value of 1.55% and 1.04%, respectively.

About the specific independent variables of each entity, LLP indicates the cost that the entities have had to bear concerning the total number of loans to customers. Higher levels of NPL are expected to be related to higher risk costs. In this case, Eastern Europe and Africa have the highest mean LLP levels (0.015 and 0.013, respectively), although lower than South and Central America (0.022). For its part, OEI shows the relationship between operating costs and operating income, that is, the entity’s efficiency ratio. Western Europe has the worst efficiency data, having an average data in the observed series of 0.658, far from the region with the best data, the Middle East, with an average of 0.490. In turn, LEV relates the total liabilities to the entity´s total assets. The regions with the highest leverage levels are Western Europe and Far East and Central Asia, with mean values above 0.91. The rest of the areas are all in the interval 0.87–0.90. Likewise, NII is a measure of business diversification since it shows the proportion of income other than an interest in the entity´s total income. In this case, the Middle East, Western Europe and South and Central America are the regions with the most diversified businesses (38.28%, 37.88%, and 36.13%, respectively), and Oceania and North America are the most dependent on credit (23.06% and 26.05% respectively).

The size of the entities, measured through the LNA variable, is calculated as the natural logarithm of the total assets. In this case, the largest entities correspond to the Oceania and Western Europe regions (mean LNA data of 16.99 and 16.81, respectively) and the smallest to North America (16.04). For its part, ROE is an indicator of business profitability since it relates the net profit to the total net worth of the entity. In this case, Africa and South and Central America present the highest ROE rates (around 14%). Still, it is true that with high levels of variation in the historical series, as reflected in the standard deviation (11.77% and 10.88%, respectively). The region with the lowest ROE is Western Europe (4.40%), which also presents a low standard deviation (2.53%).

Regarding macroeconomic variables, it is observed that Africa is the region with the highest average NFI (above 8%), and Western Europe is the region with the lowest NFI (1.58%). Also, the highest annual variation rates of GDP appear for the Far East and Central Asia (3.55%) and Africa (3.15%), while Western Europe is the region with the lowest growth GDP rate (1.16%). On the other hand, all areas present unemployment rates above 5% and below 8%, except Africa (11.18%) and the Far East and Central Asia (3.87%). Finally, regarding interest rates (INT), once again, Africa stands out with the highest average (9.76%), followed by South and Central America (7.70%). These values contrast with the estimates for North America and Western Europe (0.79% and 0.83%, respectively). And for exchange rates (EXC), the weakest currencies are found in Africa, the Far East and Central Asia (0.072 and 0.076), while Western Europe and the Middle East have stronger currencies against the dollar (1.104 and 1.033).

4.2 Results Analysis

Tables 4 and 5 present the estimates of the GMM coefficient and the Roodman coefficient for each region considered in the study. The results on the validity of the estimates according to the Sargan test and the serial correlation that appear in Table 4 indicate the validity of the GMM coefficient for all regions, except South and Central America, whose p values in the Sargan test are close to 1. This implies that, for this region, the model presents the problem of overfitting (Roodman, 2009), which can give rise to biased parameter estimates (Windmeijer, 2005). Due to this, and to verify the robustness of our results, we adopt the solution proposed by Roodman (2009) to reduce the dimensionality of the matrix of variables. Table 5 presents Roodman’s estimates and confirms the problem of overfitting in the GMM estimates, as Sargan’s p-value decreases for all regions. Therefore, in our analysis, we retained Roodman’s estimates. However, to verify the robustness of the GMM estimates, we calculate the OLS estimates. The results show that the coefficient of the lagged variable is statistically significant for all regions. As a result, we understand that random effects are controlled for and that NPL is likely to increase when they increase in the previous year.

Tables 4 and 5 also show that regions are sensitive to bank-specific determinants, albeit in different ways. The LLP ratio is significantly positive relative to banks’ NPL in Africa, Eastern Europe, the Middle East, North America, and Western Europe but negligible in the Far East and Central Asia, Oceania, and South and Central America. These results indicate that banks allocate higher provisions in regions where LLP is significant when loans are potentially impaired. The variable that indicates cost efficiency (OEI) is significantly positive about the NPL in Africa, Eastern Europe, Middle East, Oceania, and Western Europe. In these regions, the higher (worse) the efficiency ratio, the higher the NPL ratio. In other words, those entities with higher costs over total income tend to have worse credit quality.

For its part, leverage (LEV) has a significantly positive relationship concerning NPL in Africa, Far East and Central Asia, North America, Oceania, and South and Central America, indicating that higher levels of LEV cause higher NPL ratios. On the other hand, the diversification variable (NII) has no significant relationship with NPL. Likewise, the coefficient that measures the size of the entities (LNA) yields an essential positive relationship in all regions, which implies that the larger the entity´s size, the higher levels of NPL, regardless of the area where it is located. Finally, profitability (ROE) maintains a negative and significant relationship in all areas, which indicates that the higher the ROE, the lower its NPL ratio in any part of the world.

Regarding macroeconomic factors, INF is negative and significant in the NPL ratio in Africa, Eastern Europe, South and Central America, and Western Europe, meaning higher inflation levels mean higher levels of NPL. Also, GDP is significantly negative in Africa, the Middle East, North America, and Western Europe, indicating that higher economic growth (and, therefore, a higher level of financing for economic agents) implies lower NPL ratios in these regions. For its part, UNE has a significant and positive effect in all areas of the world. So, the higher the level of unemployment, the higher the NPL ratio of the system, regardless of the area where the bank is located. The interest rates (INT) have also turned out to be a significant variable with a positive effect on NPL in all the regions analyzed, indicating that higher interest rates lead to higher NPL ratios. This relationship makes sense since higher interest rates imply more significant difficulties for economic agents to pay the debt. Finally, the exchange rate of the dollar (EXC), which measures the strength (or weakness) of the national currencies of the regions analyzed, is also significant concerning the NPL rate in all banking entities.

5 Discussion

From our analysis, it can be deduced that specific and macroeconomic factors are significant in explaining the NPL ratio regardless of the region where the financial entity operates. Among the specific factors, size (LNA) and profitability (ROE) explain the NPL significantly for all regions of the world, presenting a positive relationship between LNA and a negative for ROE. Although there is no relevant literature on a worldwide analysis of the NPL, there are earlier analyzes of a regional nature that partially obtain results along the same lines as those of the present study. Thus, previous authors have already demonstrated the positive relationship between size and NPL, such as Ahmed et al. (2021) on a sample of entities from Pakistan, Koju et al. (2018) for financial institutions in Nepal, Salas and Saurina (2002) for the case of Spain, and Ghosh (2015) for U.S. banks. Regarding ROE, previous studies endorse our conclusions on the negative relationship between profitability and NPL, although with a regional scope. Thus, Messai and Jouini (2013) demonstrated the inverse relationship between profitability and NPL in countries such as Italy, Spain, or Greece, and Ciptawan and Melly (2023) for Indonesia. Previously, Kjosevski and Petkovski (2021) also concluded that profitability is among the specific factors determining Baltic banks´ NPL ratio. In contrast, Kumar and Kishore (2019) studied the factors influencing NPL in the UAE banking system and found no significant relationship between NPL and bank profitability.

Regarding business diversification (NII), in line with our results, previous studies have not shown a significant relationship between diversification and NPL (Rachman et al., 2018; Putri et al., 2020). Instead, Ismail et al. (2017) confirmed that the relationship between diversification and NPL is positive in Indonesian entities. And in the same line, Ahmed et al. (2021) also support this positive relationship. On the other hand, our results on the OEI variable indicate a significant and positive relationship between efficiency and NPL in Africa, Eastern Europe, Middle East, Oceania, and Western Europe. Along the same lines, Espinoza and Prasad (2010), Berger and DeYoung (1997), Podpiera and Weill (2008), Louzis et al. (2012), Koju et al. (2018), Ozili (2019), and Khan et al. (2020) demonstrated the correlation between low-efficiency ratios and high NPL ratios in their regional studies on financial institutions.

For its part, macroeconomic factors, unemployment (UNE), interest rates (INT), and exchange rates (EXC) are, in any case, factors that significantly explain NPL (UNE and INT present a positive relationship, and EXC has a positive relationship in all regions except the Far East and Central Asia, Oceania, and South and Central America). In this sense, we have identified several authors with conclusions similar to our study (Nkusu, 2011; Louzis et al., 2012; Castro, 2013). In contrast, Staehr and Uusküla (2020) found a negative relationship between UNE and NPL in some countries of the European Union. Also, regarding the significantly positive relationship between INT and NPL, several previous studies have results similar to those obtained in the present investigation. However, they are based only on regional studies (Espinoza & Prasad, 2010; Beck et al., 2015; Ali and Dali, 2010; Castro, 2013; Syed & Aidyngul, 2022; Chen et al., 2022). Additionally, Louzis et al. (2012) pointed out a more significant correlation when the loans are denominated with variable interest rates since the debtor is also assuming a more significant risk since there is no cap on the rate he can pay. For this reason, the authors suggest analyzing the two variables with a dynamic model that provides variable correlations over time. Castro (2013) and Beck et al. (2015) pointed out the importance of the strength of domestic currencies against the dollar to maintain relatively contained NPL ratios, which aligns with the results obtained in this study. Despite this, the impact of the real exchange rate on NPL in previous research is uncertain.

At a global level, certain variables that refer to national levels of economic development have also been relevant to explain NPL. For example, the bank size (LNA) presents a positive and significant relationship concerning NLP, indicating that in those economies where the entities reach a larger size, the level of NPL is higher. However, although other previous studies have already confirmed this relationship (Ahmed et al., 2021), these results are different from those obtained by Barra and Ruggiero (2023), who highlight that the default rate is not significantly affected by the level of competition or the banks` size. Perhaps because larger banks often manage more complex loan portfolios, with significant exposures to corporate loans and large-scale projects, risk management could be affected by a lack of adequate attention to specific portfolio segments, thus increasing the risk of default. On the other hand, high UNE levels appear in our models associated with greater NLP. Other studies have also confirmed these findings (Louzis et al., 2012), but controversy remains about this effect in more current research (Uusküla, 2020). In this sense, our results seem to recognize that a high UNE affects the financial health of companies and families, which in turn can affect their ability to meet credit obligations.

The INT variable has also been significant in our global models, indicating that higher interest rates in the economy are associated with higher levels of NLP. Arguably, this finding recognizes that, in unfavourable financial conditions, borrowers may face more significant challenges in meeting their credit obligations. Finally, the global results obtained for EXC postulate that the strength of national currencies is a factor with an evident influence on NPL. In this sense, Klein (2013) also identified a positive relationship (the more a currency depreciates, the lower the default rate), which the author explained as a consequence of the boost in foreign trade due to a depreciation of the local currency, particularly for those countries that base their growth on exports. On the contrary, when economic agents (households and companies) borrow in foreign currency, the local currency´s weakness implies difficulties in meeting the payment of their debts, thus increasing default ratios (Espinoza & Prasad, 2010).

Finally, other variables associated with the economic development of the countries have not been significant in our models. For example, the variable that measures economic growth (DGP) has not shown special significance concerning NPL at a global level, although it was in some regional environments. These results only partially coincide with those obtained by Kartal et al. (2023), Staehr and Uusküla (2017), Espinoza and Prasad (2010), Castro (2013) and Syed and Aidyngul (2022), who concluded that NPL increase as economic growth declines. It is likely that, from certain levels of economic development, GDP can have a dampening effect on late payment. Still, this circumstance is not verified in a global environment, where other factors weigh more in explaining the problem under study. Likewise, the inflation rate (INF) has not been significant in our global models either. These results differ from those obtained by Syed and Aidyngul (2022) who analyzed 22 countries from 1995 to 2019. Perhaps the larger sample used in our study and a more current period is the cause of these differences given that inflation levels show high heterogeneity worldwide.

6 Conclusion

This study adds to the empirical literature related to the determinants of the NPL ratio in banking entities, carrying out a global analysis of the factors that explain said metric. For this, a sample of 1,631 banks from 111 countries has been used, grouped into the eight main regions of the world, which has given rise to a total of 24,915 observations for the period 2007–2022. Applying panel data methods and a set of 12 explanatory variables, both specific and macroeconomic, the results present essential contributions to understanding the factors that explain the evolution of NPL globally.

Among the main findings of this analysis, it is shown that NPL is determined by a series of factors, regardless of the place or moment in which they operate. These factors refer to the bank size, profitability, unemployment, interest, and exchange rates. Identifying these factors is relevant since it allows us to understand which variables significantly influence NPL in the financial system at a global level and to know its financial health in detail. Therefore, it is essential to carefully monitor and evaluate the NPL in such a way as to guarantee financial stability and sustainable economic growth. It is also necessary to have effective regulatory policies and adequate management strategies to mitigate credit risk and ensure the financial system´s stability.

The results of this analysis may have significant implications for managers of financial institutions, regulators, analysts, and academics. From a theoretical perspective, our findings help to understand the evolution of NPL better and the specific and macroeconomic factors that influence its formation. From an applied point of view, our conclusions encourage bank managers to minimize the cost of building models to analyse NPL by facilitating the understanding of the elements that condition its evolution in the world´s most critical regions. For this reason, managers of financial institutions must control, for example, the size and growth of the balance sheet since if a financial institution expands too quickly, it could increase exposure to credit risk, incur losses, and also have to deal with a situation of capital scarcity to support high levels of growth. In periods of growth, it is critical to adequately manage credit risk to ensure that said growth is consistently profitable and with contained NPL ratios. Only in this way the balance between growth, profitability, and NPL will suppose sustainable models in the long term. The study has also revealed the importance of three macroeconomic factors that affect NPL in banks: unemployment, interest rates, and exchange rates. Regulators and economists can use this evidence to design policies that promote employment and strengthen the national currency of each region since both are crucial elements in explaining the evolution of NPL. In addition, monetary policies, supported by the intervention of interest rates, can stimulate investment and consumption, creating employment and reducing the generation of delinquent balances in the financial system.

This study has considered bank-specific variables that refer mainly to the economic and financial aspects of the entities. Therefore, new variables could be included for future research to explain the NPL evolution. These variables could consist of intangible factors such as gender diversity in entities’ management or administrators’ profiles and training. It could also include other elements related to the level of awareness and compliance with environmental policies and sustainability criteria. A second limitation is caused by the panel data method used, which depends on specific distributional assumptions, as do many statistical methods. Future research can also expand these methodological aspects with different non-parametric techniques, such as artificial neural networks, which do not require the prior theoretical assumptions.

Data Availability

The datasets used and/or analysed during the current study are available from the corresponding author on reasonable request.

References

Agnello, L., & Sousa, R. M. (2012). How do banking crises impact on income inequality? Applied Economics Letters, 19(15), 1425–1429.

Ahmed, S., Majeed, M. E., Thalassinos, E., & Thalassinos, Y. (2021). The impact of bank specific and macro-economic factors on non-performing loans in the banking sector: Evidence from an emerging economy. Journal of Risk and Financial Management, 14(5), 217.

Aiyar, M. S., Bergthaler, M. W., Garrido, J. M., Ilyina, M. A., Jobst, A., Kang, M. K. H.,… and, & Moretti, M. M. (2015). A strategy for resolving Europe’s problem loans. International Monetary Fund: Washington.

Ali, A., & Daly, K. (2010). Macroeconomic determinants of credit risk: Recent evidence from a cross country study. International Review of Financial Analysis, 19(3), 165–171.

Arellano, M., & Bond, S. (1991). Some tests of specification for Panel Data: Monte Carlo Evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297.

Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68(1), 29–51.

Ari, A., Chen, S., & Ratnovski, L. (2021). The dynamics of non-performing loans during banking crises: A new database with post-COVID-19 implications. Journal of Banking & Finance, 133, 106140.

Balgova, M., Plekhanov, A., & Skrzypinska, M. (2017). Reducing non-performing loans: Stylized facts and economic impact. In American Economic Association 2018 Annual Meeting Independent Researcher: London.

Barra, C., & Ruggiero, N. (2023). Bank-specific factors and credit risk: Evidence from Italian banks in different local markets. Journal of Financial Regulation and Compliance, 31(3), 316–350.

Beck, R., Jakubik, P., & Piloiu, A. (2015). Key determinants of non-performing loans: New evidence from a global sample. Open Economies Review, 26(3), 525–550.

Berger, A. N. and R DeYoung (1997). Problem loans and cost efficiency in commercial banks. Journal of Banking & Finance, 21(6), 849–870.

Bernanke, B. S., Gertler, M., & Gilchrist, S. (1999). The financial accelerator in a quantitative business cycle framework. Handbook of Macroeconomics, 1, 1341–1393.

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143.

Boumparis, P., Milas, C., & Panagiotidis, T. (2019). Non-performing loans and sovereign credit ratings. International Review of Financial Analysis, 64, 301–314.

Castro, V. (2013). Macroeconomic determinants of the credit risk in the banking system: The case of the GIPSI. Economic Modelling, 31, 672–683.

Chaibi, H., & Ftiti, Z. (2015). Credit risk determinants: Evidence from a cross-country study. Research in International Business and Finance, 33, 1–16.

Chen, Q., Katagiri, M., & Surti, J. (2022). Monetary surprises and bank equity valuation with prolonged low interest rates. Finance Research Letters, 47, 102608.

Cheng, M. C., Lee, C. C., Pham, Q. N. T., & Chen, H. Y. (2016). Factors affect NPL in Taiwan banking industry. Journal of Accounting, 6(1), 65–87.

Chowdhury, M. A. I., Uddin, M. S., Ullah, H., Ahmmed, M., & Shadek, M. J. (2023). What causes non-performing loans? Evidence from the Islamic Banking Sector of Bangladesh. International Journal of Accounting & Finance Review, 14(1), 11–21.

Cifter, A., Yilmazer, S., & Cifter, E. (2009). Analysis of sectoral credit default cycle dependency with wavelet networks: Evidence from Turkey. Economic Modelling, 26(6), 1382–1388.

Ciptawan, C., & Melly, M. (2023). The influence of Loan to Deposit ratio, effective tax rate and non-performing loan toward return on asset in banking companies listed on the Indonesia Stock Exchange. In Proceeding International Conference on Entrepreneurship, 2, 357–365.

Cucinelli, D. (2015). The impact of non-performing loans on bank lending behavior: Evidence from the Italian banking sector. Eurasian Journal of Business and Economics, 8(16), 59–71.

El-Maude, J. G., Abdul-Rahman, A., & Ibrahim, M. (2017). Determinants of non-performing loans in Nigeria’s deposit money banks. Archives of Business Research, 5(1), 74–88.

Ercegovac, R., Pecaric, M., & Klinac, I. (2020). What determines the price to book ratio in the European Banking Sector. Finance a Uver: Czech Journal of Economics & Finance, 70(3), 262–280.

Erdas, M. L., & Ezanoglu, Z. (2022). How do bank-specific factors impact non-performing loans: Evidence from G20 countries. Journal of Central Banking Theory and Practice, 11(2), 97–122.

Ersoy, E. (2022). The determinants of the non-performing loans: The case of Turkish banking sector. International Journal of Insurance and Finance, 1(2), 1–11.

Espinoza, M. R. A., & Prasad, A. (2010). Nonperforming loans in the GCC banking system and their macroeconomic effects. International Monetary Fund: Washington.

Ferreira, C. (2022). Determinants of non-performing loans: A panel data approach. International Advances in Economic Research, 28, 133–153.

Ghosh, A. (2015). Banking-industry specific and regional economic determinants of non-performing loans: Evidence from US states. Journal of Financial Stability, 20, 93–104.

Gjeçi, A., Marinč, M., & Rant, V. (2023). Non-performing loans and bank lending behaviour. Risk Management, 25(1), 7.

Gonzalez-Garcia, M. J., & Grigoli, F. (2013). State-owned banks and fiscal discipline. International Monetary Fund: Washington.

Hasan, I., & Wall, L. D. (2004). Determinants of the loan loss allowance: Some cross-country comparisons. Financial Review, 39(1), 129–152.

Hassan, M. K., İslam, M. T., Ahmed, Z., & Sarker, J. I. (2023). Islamic banking in Bangladesh: A literature review and future research agenda. International Journal of Islamic and Middle Eastern Finance and Management, 16(5), 1030–1054.

Hughes, J. P., & Moon, C. G. (2022). How bad is a bad loan? Distinguishing inherent credit risk from inefficient lending (does the capital market price this difference?). Journal of Economics and Business, 120, 106058.

Ismail, N., Azlan, N. D. A., Husin, M. M., Ishak, I., & Hashim, S. L. M. (2017). Bank efficiencies and Non-performing Loan of Commercial banks in Malaysia. Journal of Humanities Language Culture and Business, 1(5), 34–40.

Kartal, M. T., Kirikkaleli, D., & Ayhan, F. (2023). Nexus between non-performing loans and economic growth in emerging countries: Evidence from Turkey with wavelet coherence approach. International Journal of Finance & Economics, 28(2), 1250–1260.

Kartikasary, M., Marsintauli, F., Serlawati, E., & Laurens, S. (2020). Factors affecting the non-performing loans in Indonesia. Accounting, 6(2), 97–106.

Keeton, W. R. (1999). Does faster loan growth lead to higher loan losses? Economic Review-Federal Reserve Bank of Kansas City, 84(2), 57.

Khan, M. A., Siddique, A., & Sarwar, Z. (2020). Determinants of non-performing loans in the banking sector in developing state. Asian Journal of Accounting Research, 5(1), 135–145.

King, R. G., & Plosser, C. I. (1982). The behavior of money, credit, and prices in a real business cycle (no. w0853). National Bureau of Economic Research. Cambridge.

Kiyotaki, N., & Moore, J. (1997). Credit cycles. Journal of Political Economy, 105(2), 211–248.

Kjosevski, J., & Petkovski, M. (2021). Macroeconomic and bank-specific determinants of non-performing loans: The case of baltic states. Empirica, 48(4), 1009–1028.

Kjosevski, J., Petkovski, M., & Naumovska, E. (2019). Bank-specific and macroeconomic determinants of non-performing loans in the Republic of Macedonia: Comparative analysis of enterprise and household NPLs. Economic Research-Ekonomska Istraživanja, 32(1), 1185–1203.

Klein, N. (2013). Non-performing loans in CESEE: Determinants and impact on macroeconomic performance. International Monetary Fund.

Koju, L., Koju, R., & Wang, S. (2018). Macroeconomic and bank-specific determinants of non-performing loans: Evidence from Nepalese banking system. Journal of Central Banking Theory and Practice, 7(3), 111–138.

Kumar, V., & Kishore, P. (2019). Macroeconomic and bank specific determinants of non-performing loans in UAE conventional bank. Journal of Banking and Finance Management, 2(1), 1–12.

Lee, Y. Y., Yahya, M. H. D. H., Habibullah, M. S., & Ashhari, Z. M. (2019). Non-performing loans in European Union: Country governance dimensions. Journal of Financial Economic Policy, 12(2), 209–226.

Lee, J. M., Chen, K. H., Chang, I. C., & Chen, C. C. (2022). Determinants of non-performing loans, firm’s corporate governance and macroeconomic factors. International Journal of Finance & Economics, 27(1), 88–98.

Lemma-Lalisho, D. (2022). Determinant of non-performing loan in Development Bank of Ethiopia. Revista De Investigaciones Universidad Del Quindío, 34(1), 52–69.

Louzis, D. P., Vouldis, A. T., & Metaxas, V. L. (2012). Macroeconomic and bank-specific determinants of non-performing loans in Greece: A comparative study of mortgage, business and consumer loan portfolios. Journal of Banking & Finance, 36(4), 1012–1027.

Mahyoub, M., & Said, R. M. (2021). Factors influencing non-performing loans: Empirical evidence from commercial banks in Malaysia. Research Journal of Business and Management, 8(3), 160–166.

Makri, V., Tsagkanos, A., & Bellas, A. (2014). Determinants of non-performing loans: The case of Eurozone. Panoeconomicus, 61(2), 193–206.

Messai, A. S., & Jouini, F. (2013). Micro and macro determinants of non-performing loans. International Journal of Economics and Financial Issues, 3(4), 852–860.

Mitrakos, T., & Simigiannis, G. T. (2009). The determinants of Greek household indebtedness and financial stress. Bank of Greece Economic Bulletin, 32.

Msomi, T. S. (2022). Factors affecting non-performing loans in commercial banks of selected west African countries. Banks and Bank Systems, 17(1), 1.

Nkusu, M. M. (2011). Nonperforming loans and macrofinancial vulnerabilities in advanced economies. International Monetary Fund.

Ozili, P. K. (2019). Non-performing loans and financial development: New evidence. The Journal of Risk Finance, 20(1), 59–81.

Park, C. Y., & Shin, K. (2021). COVID-19, nonperforming loans, and cross-border bank lending. Journal of Banking & Finance, 133, 106233.

Partovi, E., & Matousek, R. (2019). Bank efficiency and non-performing loans: Evidence from Turkey. Research in International Business and Finance, 48, 287–309.

Petkovski, M., Kjosevski, J., & Jovanovski, K. (2021). Macro and Bank Specific Determinants of Non-performing Loans in Polish Commercial banks. Argumenta Oeconomica, 2(47), 1–20.

Podpiera, J., & Weill, L. (2008). Bad luck or bad management? Emerging banking market experience. Journal of Financial Stability, 4(2), 135–148.

Putri, U. L., Rinofah, R., & Mujino, M. (2020). Pengaruh Profitabilitas, Capital Adequacy ratio Dan Diversifikasi Pendapatan Terhadap Risiko Bank. Jurnal Fokus Manajemen Bisnis, 10(1), 30–40.

Rachman, R. A., Kadarusman, Y. B., Anggriono, K., & Setiadi, R. (2018). Bank-specific factors affecting non-performing loans in developing countries: Case study of Indonesia. The Journal of Asian Finance Economics and Business, 5(2), 35–42.

Rahman, H. U., Arian, A., & Sands, J. (2023). Does fiscal consolidation affect non-performing loans? Global evidence from heavily indebted countries (HICs). Journal of Risk and Financial Management, 16(9), 417.

Rathnayake, R. M. S. S., & Dissanayake, D. M. R. U. (2021). Determinants of non-performing loans: Evidence from Sri Lanka. South Asian Journal of Finance, 2(1), 14–27.

Reinhart, C. M., & Rogoff, K. S. (2010). Growth in a time of debt. American Economic Review, 100(2), 573–578.

Roodman, D. (2009). How to do xtabond2. A introduction to difference and system GMM in Stata. The Stata Journal, 9(1), 86–136.

Salas, V., & Saurina, J. (2002). Credit risk in two institutional regimes: Spanish commercial and savings banks. Journal of Financial Services Research, 22(3), 203–224.

Staehr, K. and L Uusküla (2017). Forecasting models for non-performing loans in the EU countries (no. wp2017-10). Bank of Estonia.

Staehr, K. and L Uusküla (2020). Macroeconomic and macro-financial factors as leading indicators of non-performing loans: Evidence from the EU countries. Journal of Economic Studies, 48(3), 720–740.

Syed, A. A., & Aidyngul, Y. (2022). Macro economical and bank-specific vulnerabilities of nonperforming loans: A comparative analysis of developed and developing countries. Journal of Public Affairs, 22(2), e2414.

Theong, M. J., Lau, W. Y., & Osman, A. F. (2022). Comparative study of determinants of the Malaysian household nonperforming loans: Evidence from Nardl. Singapore Economic Review. https://doi.org/10.1142/S0217590822500242.

Tomczak, K. (2023). Transmission of the 2007–2008 financial crisis in advanced countries of the European Union. Bulletin of Economic Research, 75(1), 40–64.

Umaternate, F. F., & Mongid, A. (2023). Modelling non-performing loans (NPL) for small banks in Indonesia: Are macroeconomic Matter? International Journal of Economics Business and Management Research, 7(1), 57–68.

Windmeijer, F. (2005). A finite sample correction for the variance of linear efficient two-step GMM estimators. Journal of Econometrics, 126(1), 25–51.

Zeng, S. (2012). Bank non-performing loans (NPLS): A dynamic model and analysis in China. Modern Economy, 3(1), 16795.

Žunić, A., & K Kozarić and EZ Dželihodžić. (2021). Non-performing loan determinants and impact of covid-19: Case of Bosnia and Herzegovina. Journal of Central Banking Theory and Practice, 10(3), 5–22.

Acknowledgements

Not applicable.

Funding

Funding for open access publishing: Universidad Málaga/CBUA

Author information

Authors and Affiliations

Contributions

All the authors contributed an equal effort to complete the manuscript.

Corresponding author

Ethics declarations

Competing Interests

The authors declare that they have no competing interests.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Salas, M., Lamothe, P., Delgado, E. et al. Determinants of Nonperforming Loans: A Global Data Analysis. Comput Econ (2024). https://doi.org/10.1007/s10614-023-10543-8

Accepted:

Published:

DOI: https://doi.org/10.1007/s10614-023-10543-8