Abstract

A local projection is a statistical framework that accounts for the relationship between an exogenous variable and an endogenous variable, measured at different time points. Local projections are often applied in impulse response analyses and direct forecasting. While local projections are becoming increasingly popular because of their robustness to misspecification and their flexibility, they are less statistically efficient than standard methods, such as vector autoregression. In this study, we seek to improve the statistical efficiency of local projections by developing a fully Bayesian approach that can be used to estimate local projections using roughness penalty priors. By incorporating such prior-induced smoothness, we can use information contained in successive observations to enhance the statistical efficiency of an inference. We apply the proposed approach to an analysis of monetary policy in the United States, showing that the roughness penalty priors successfully estimate the impulse response functions and improve the predictive accuracy of local projections.

Similar content being viewed by others

Notes

See, e.g., Geweke (2005) for a general introduction to Bayesian analysis.

Bayesian inference using the Jeffreys prior for \(\varvec{\Sigma }\) almost always fails for the synthetic and real data used in the subsequent section.

All programs were written in Matlab 2016a (64 bit) and executed on an Ubuntu Desktop 16.04 LTS (64 bit), running on Intel Xeon E5-2607 v3 processors (2.6 GHz).

When the degree of the B-spline bases is increased to 5, the weight set becomes {1/120, 13/60, 33/60, 13/60, 1/120}. The added weights are too small to affect the estimate \(\left( 1/120\approx 0.0083\right) \).

The time series of monetary policy shocks is from Yuriy Gorodnichenko’s website (https://eml.berkeley.edu//~ygorodni/index.htm).

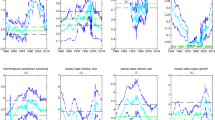

In the “Online Appendix”, Figs. A.1, A.2, and A.3 display credible intervals for all the specifications.

Both the DIC and WAIC are asymptotically related to the AIC. Thus, one might consider evaluating the statistical significance of the difference in the values of the criteria of two models by applying a rule of thumb that is originally proposed to Bayes factor. As Burnham and Anderson (2004) describe, the AIC can be interpreted as an approximation of the log marginal likelihood of a model under a “savvy” prior that is a function of sample size and the number of model parameters. According to Jeffreys’s (1961) rule of thumb, the statistical significance of the difference between two models is “weak” if the difference in the AIC/DIC/WAIC is 0-2, “positive” if 2–6, “strong” if 6–10, or “very strong” if >10 (see also Raftery 1995). When this rule of thumb is directly applied to Table 3, one might be able to interpret the results as follows: the statistical significance of the differences related to the prior choice is “very strong,” and the significance of the differences attributable to the use of B-splines is “weak” or “positive” when the Normal prior is used while it is “very strong” when the N-RP prior is used.

We minimize the information criteria using the limited-memory Broyden-Fletcher-Goldfarb-Shanno algorithm with bounds (Byrd et al. 1995), using a Matlab routine minConf_TMP.m written by Mark Schmidt. (https://www.cs.ubc.ca/~schmidtm/Software/minConf.html).

We also considered Jeffreys prior for \(\sigma _{\left( h_{i}\right) }^{2}\) and obtained almost the same result for the half-t prior (thus, it is not reported).

As T increases (e.g., \(T=500\)), the relative performance of the FGLS approach with unrestricted covariance becomes comparable with that with diagonal covariance (not reported).

References

Aikman, D., Bush, O., & Taylor, A. M. (2016). Monetary versus macroprudential policies: Causal impacts of interest rates and credit controls in the era of the UK radcliffe report. NBER working paper 22380.

Alvarez, I., Niemi, J., & Simpson, M. (2014). Bayesian inference for a covariance matrix. In 26th Annual conference on applied statistics in agriculture.

Auerbach, A. J., & Gorodnichenko, Y. (2013). Fiscal multipliers in recession and expansion. In A. Alesina & F. Giavazzi (Eds.), Fiscal policy after the financial crisis (pp. 63–98). Chicago: University of Chicago Press.

Barnichon, R., & Matthes, C. (2019). Functional approximations of impulse responses. Journal of Monetary Economics, 99(1), 41–55.

Barnichon, R., & Brownlees, C. (2019). Impulse response estimation by smooth local projections. Review of Economics and Statistics, 101(3), 522–230.

Byrd, R. H., Peihuang, L., Nocedal, J., & Zhu, C. (1995). A limited memory algorithm for bound constrained optimization. SIAM Journal on Scientific Computing, 16, 1190–1208.

Coibion, O., Gorodnichenko, Y., Kueng, L., & Silvia, J. (2017). Innocent bystanders? Monetary policy and inequality. Journal of Monetary Economics, 88, 70–89.

De Boor, C. (1978). A practical guide to splines (Vol. 27). New York: Springer.

Eilers, P. H. C., & Marx, B. D. (1996). Flexible smoothing with B-splines and penalties. Statistical Science, 11, 89–121.

El-Shagi, M. (2019). A simple estimator for smooth local projections. Applied Economics Letters, 26, 830–834.

Geweke, J. (2005). Contemporary Bayesian econometrics and statistics (Vol. 537). New York: Wiley.

Guo, W. (2002). Functional mixed effects models. Biometrics, 58, 121–128.

Huang, A., & Wand, M. P. (2013). Simple marginally noninformative prior distributions for covariance matrices. Bayesian Analysis, 8, 439–452.

Hurvich, C. M., Simonoff, J. S., & Tsai, C.-L. (1998). Smoothing parameter selection in nonparametric regression using an improved akaike information criterion. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 60, 271–293.

Jordà, Ò. (2005). Estimation and inference of impulse responses local projections. American Economic Review, 95, 161–182.

Lang, S., & Brezger, A. (2004). Bayesian P-splines. Journal of Computational and Graphical Statistics, 13, 183–212.

Miranda-Agrippino, S., & Ricco, G. (2017). The transmission of monetary policy shocks. Staff working paper 657, Bank of England.

Morris, J. S., & Carroll, R. J. (2006). Wavelet-based functional mixed models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 68, 179–199.

Ramey, V. A. (2016). Macroeconomic shocks and their propagation, Chap. 2. In J. B. Taylor & H. Uhlig (Eds.), Handbook of macroeconomics (Vol. 2A, pp. 71–162). Amsterdam: Elsevier.

Ramey, V. A., & Zubuairy, S. (2018). Government spending multipliers in good times and in bad: Evidence from U.S. historical data. Journal of Political Economy, 126(2), 850–901.

Riera-Crichton, D., Vegh, C. A., & Vuletin, G. (2015). Procyclical and countercyclical fiscal multipliers: Evidence from OECD countries. Journal of International Money and Finance, 52, 15–31.

Romer, C. D., & Romer, D. H. (2004). A new measure of monetary shocks: Derivation and implications. American Economic Review, 94, 1055–1084.

Rue, H. (2001). Fast sampling of Gaussian Markov random fields. Journal of the Royal Statistical Society, Series B, 63, 325–338.

Rue, H., & Held, L. (2005). Gaussian Markov random fields: Theory and applications. Boca Raton: CRC Press.

Spiegelhalter, D. J., Best, N. G., Carlin, B. P., & Van Der Linde, A. (2002). Bayesian measures of model complexity and fit. Journal of the Royal Statistical Society, Series B, 64, 583–639.

Stock, J. H., & Watson, M. W. (2007). Why has US inflation become harder to forecast? Journal of Money, Credit and Banking, 39, 3–33.

Watanabe, S. (2010). Asymptotic equivalence of Bayes cross validation and widely applicable information criterion in singular learning theory. Journal of Machine Learning Research, 11, 3571–3594.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Tanaka, M. Bayesian Inference of Local Projections with Roughness Penalty Priors. Comput Econ 55, 629–651 (2020). https://doi.org/10.1007/s10614-019-09905-y

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10614-019-09905-y