Abstract

Consumer credit has become an important element of the economy despite the negative effects: Over-indebtedness has wide-ranging repercussions affecting consumers and society as a whole. We analysed the debt judgements (N = 4,095) of Finnish district courts from 2014 to 2016, as well as administrative data on debtors. Our focus was on the position of consumers on the credit market and their consumption-related problem debts, namely instant loans, extensive consumer credit, and credit-card as well as distance-selling indebtedness. Regarding the four credit products, first we considered the average amount of outstanding debt and then we looked at the sociodemographic and socioeconomic characteristics of the debtors. The results revealed that the average outstanding debt (€) varied according to the credit product and that the highest average amount originated from extensive consumer credit. Instant loans and distance-selling indebtedness caused debt problems especially among low-income young adults, adverse selection seemingly being one factor behind instant-loan-related debts. Extensive consumer credit and credit-card indebtedness were behind debt judgements against older consumers with a good socioeconomic position and numerous previous loans. This is a moral-hazard situation whereby borrowers may have more information about their total amounts of debt than the lenders. We suggest that, in many cases, debt problems reflect an abundant supply of consumer credit, which seems to foster asymmetric information, the consumer’s position and competence to act in the credit market, as well as various overall risk factors. The findings highlight the need to strengthen consumers’ financial skills and for loan products that meet the needs of low-credit-rated consumers. Moreover, lenders should act responsibly in the current credit market.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Consumer credit is a significant and common factor in household finances that facilitates consumption during different life stages. Martin (2002) refers to this phenomenon as “everyday financialization.” The democratization of finance is one of its outcomes, as it has opened up the credit market to new and seemingly risky borrower groups (Livshits et al., 2016; see also Ertürk et al., 2007). Another outcome is the increasing number of debt problems. Thus, over-indebtedness is acknowledged nowadays as a serious and permanent social problem in Western societies (see, e.g., Hiilamo, 2018; Muttilainen, 2002; Poppe et al., 2016).

It has been reported (Eurofound, 2020) that in 2016, approximately 21 per cent of people in the European Union area (EU28) had difficulties in making ends meet, and 14 per cent were not able to make scheduled payments. Even if these proportions are lower in the Nordic countries, which have similar financial markets and societal structures, the number of debt problems has increased in recent years (Hiilamo, 2018; Hohnen & Hansen, 2021). Nordic comprehensive welfare states still have many tools with which to protect citizens from social risks, even if such an aim is perhaps somewhat less visible than it has been (Kangas & Kvist, 2018). One risk factor that remains, however, is the propensity among numerous Finnish consumers to take high-interest-rate loans and the related debt problems (Aaltonen & Koskinen, 2019). Hiilamo (2018) goes as far as to state that the instant loan has been a structural cause of over-indebtedness in Finland.

Attempts to reduce over-indebtedness by means of regulation have been made in societies in which credit markets are aggressive and safety nets are failing (Cerini, 2017; Hiilamo, 2018; van den Zwan, 2014, see also, e.g., Livada, 2019). Responsible lending requires lenders not to act solely in their own interests, for example, and to assess the creditworthiness of applicants, in other words their repayment capacity. Borrowers must not be offered inappropriate credit products that risk over-indebtedness (Ramsay, 2012). Cerini (2017) emphasizes the need to find a balance between responsible lending and protecting vulnerable consumers who are at risk of over-indebtedness.

According to Hohnen and Hansen (2021), research on debt in the Nordic countries has focused on default debt with the purpose of identifying specific socio-demographic groups at risk, risky loan types, and a lack of financial knowledge. The aim of this article is to expand this stream of research by focusing on debt problems related to unsecured consumer credit. Administrative data provides information on defaulted debtors, whereas information originating from the debt judgements allows the pinpointing of credit products that tend to cause debt problems in a financialized society, namely instant loans (resembling payday loans),Footnote 1 extensive consumer credit,Footnote 2 credit-card debt,Footnote 3 and distance sellingFootnote 4 (online shopping).

Indebtedness is a challenging research area, which requires a wide and multidisciplinary approach. A further challenge is that loan companies rarely give out individual-level information about their clients, in other words about consumers who apply for, take, or do not repay credit. To give a better picture, we focus the discussion in this article on some of the many actors in the credit market, including lenders (i.e., loan companies), loan applicants and borrowers (i.e., consumers), and insolvent borrowers (i.e., debtors who have received a debt judgement concerning a specific credit product). Legislation relating to lending practices and insolvency also has an effect on debt problems.

In the following section, we present a more precise conceptual framework, discuss previous research results, and introduce our two research questions. Our main aim is to highlight the different positions of consumers on the credit market, in other words their chances of obtaining credit, based on their sociodemographic characteristics (including socioeconomic position). The findings indicate that the risk of defaulted debt is higher among certain groups, especially young adults, because their position in the credit market is low from the beginning. We therefore suggest a new perspective for research related to debt problems.

Conceptual Framework

Asymmetric Information in the Credit Market

An increasing number of financial institutions have recently joined traditional banks in offering various credit products, most of which are available to low-income consumers who have previously been outside of the credit market (see, e.g., Majamaa et al., 2019; Montgomerie, 2007; Rantala & Tarkkala, 2010; van der Zwan, 2014). The democratization of credit is one significant outcomes of financialization (Livshits et al., 2016). As a concept, financialization could be described as the expansion and strengthening of financial markets, and it has been used with reference to changes in economic systems since the industrial era, accelerated by technological developments (van der Zwan, 2014). There is currently a supply of and a demand for short-term consumer credit that is facilitated by financial innovations and is not tied to specific products, credit cards, or collateral, nor does it rely on a long-term customer-creditor relationship (Takalo, 2019).

The lender is usually understood as a professional in the credit business and the client as a layperson who might not know enough about the terms of a loan, its repayment, or the consequences of default. A market participant who knows more than others about consumer behaviour, for example, is said to have asymmetric information (Drake & Holmes, 1995; Mishkin, 1991; Takalo, 2019.) Asymmetry between creditors and borrowers in this sense hampers the functioning of the credit market, in particular, due to adverse consumer selection and moral hazard (ibid). De Meza (2002) further suggests that asymmetric information creates a systematic opportunity for low-quality credit firms to free ride in the credit market with the help of firms that manage the risks more effectively.

One example of adverse selection is when high-risk borrowers in particular are willing to take out high-interest loans. The interest rate could serve as a screening tool, in that consumers who are willing to pay a high rate may, in general, be more vulnerable to risk (Stiglitz & Weiss, 1981). This kind of adverse selection also increases the price of the loan for low-risk consumers (Drake & Holmes, 1995). Moral hazard refers to the risk of reckless behaviour among debtors, such as giving a lender false information about their own financial situation. For example, a borrower may not disclose any previous outstanding loans in their loan application (Gathergood et al., 2019). In short, asymmetric information may lead to excessive lending and borrowing, which may have an effect on the stability of the financial sector (De Meza, 2002; Takalo, 2019).

Bowles (2004, p. 104) uses the term loss aversion with reference to people who are more afraid of losses than of equivalent benefits. It may offer some explanation of certain anomalies in everyday economics, such as the use of high-cost credit products. The fear of a payment-default entry or of foreclosure may cause consumers to make poor credit decisions, for example (Rantala, 2012). The process of obtaining unsecured consumer loans is quick and convenient, but one disadvantage is the higher cost for consumers compared to traditional bank loans. There is considerable evidence that low-income consumers with no assets who need to improve their financial situation have fewer options and may be forced to accept high-cost credit (Autio et al., 2009). Bowles (2004, pp. 303–306) refers to these consumers as credit-constrained, because they do not have the same opportunities in credit markets as people with more assets. Young adults, for instance, tend to be financially vulnerable and risky as a consumer group because of their high debt burden in times of growing economic insecurity (Oksanen et al., 2015), and their credit use has shifted from mortgages to unsecured consumer credit (Houle, 2014).

Financial innovations are cited as a key factor in the increase in household access to credit and to higher aggregate borrowing (Livshits et al., 2016). Bowles (1998) argues that not enough is known about cultural transmission, prevalent traits, social learning, or the conception of homo economicus and that disciplinary boundaries may hinder the formation of a clear picture about human behaviour in economics. He suggests that preferences motivate behaviour, are endogenous, and have certain implications. However, the very fact that an increasing number of financial institutions offer and promote credit use may influence the preferences of consumers in enlarged financialized credit markets. Addictions, weakness of will, and other defective behavioural patterns should also be borne in mind (Bowles, 2004, p. 100).

Financial Literacy in a Financialized Society

According to Martin (2002), everyday financialization has strengthened the impact of financial products and economic motives that affect every aspect of daily life among consumers. From the consumer’s perspective, the increasing availability of financial products requires more personal responsibility and better financial skills (ibid.). One concern is whether consumers have the calculative competence to decide on complex financial instruments or are capable of planning their finances in the long term (Ertürk et al., 2007). Financial literacy, in other words money-related knowledge and skills, implies the ability to process relevant information and to make informed decisions about financial planning, wealth accumulation, debt, and pension provision (Lusardi & Mitchell, 2007, 2014).

In general, younger and older age groups are less financially literate than the middle-aged (Lusardi & Mitchell, 2011) and, on average, find it more difficult to manage their debt responsibilities (Brown et al., 2018). Many retirees have accumulated wealth, such as in the form of an owner-occupied dwelling. It is therefore not surprising that the default risk is low among the over-60 s, whereas it is very high among young adults, as well as people in their mid-30 s (Thomas, 2000). With regard to Finland, Kalmi and Ruuskanen (2016) found that Finns were quite competent financially but that young, female, and older people tended to have problems acquiring financial knowledge and that low-income people struggled with their financial behaviour.

Even if a financially literate consumer is capable of processing information when applying for a loan, some surprises may arise. For example, consumers tend to underestimate how a change in interest rate may affect the duration of a loan (Yard, 2004), and only giving information about minimum required payments does not enhance repayment decisions (Navarro-Martinez et al., 2011). Furthermore, consumers with a low level of financial literacy are more likely to incur high-cost debts and to have problems settling them (Lusardi & Tufano, 2009).

Increased financial vulnerability, especially among young adults, is not solely attributable to a low level of financial literacy. Financialization with its easy access to credit products has brought structural changes in the labour market, for example, with the spread of non-standard employment (Chan, 2013). Precarious work, irregular working hours, and growing job insecurity affect consumers in terms of income, financial management, and progression over the life cycle (Karamessini et al., 2019; Nielsen et al., 2019). In particular, a low socioeconomic position appears to have a link with the emergence of debt problems (see, e.g., Oksanen et al., 2015), even if they occur in all income categories (Betti et al., 2007; Oksanen et al., 2015).

Credit Scoring, Creditworthiness, and Responsible Lending

Lenders must be able to identify customers who repay their loans to safeguard their operations and returns (Stiglitz & Weiss, 1981). Financial institutions collect comprehensive information on consumers and price their credit products according to the borrowers’ default risk based on credit-scoring models (Livshits et al., 2016). Where applicable, assessments of creditworthiness rely on internal and external sources, including databases, but among the lending firms, the main source of information is the applicant (Ferretti & Livada, 2016). This may be problematic in that applicants, intentionally or through negligence, may provide incorrect information (ibid). More detailed credit assessment is necessary when the amount applied for is large because the risk to the creditor increases, as does the borrower’s risk of default. Demographic characteristics such as age, gender, marital status, and number of dependents are utilized in the assessment of creditworthiness, i.e., credit scoring (see, e.g., Abdou & Pointon, 2011; Kočenda & Vojtek, 2011; Leyshon & Thrift, 1999).

Of even more significance is the applicant’s socioeconomic position, assessed in terms of monthly income, educational level, car ownership and housing status, previous loans, and guarantees, all of which affect the credit score and, by association, the ability to repay the loan. For example, tenants, on average, have lower incomes and less wealth than homeowners and therefore fewer credit options (Bridges & Disney, 2004). Two-breadwinner households have more credit opportunities, but what matters is being able to make financial arrangements to balance income and debt (Xiao & Yao, 2020). Even if retirement income is linked to previous income-based contributions, disposable income falls considerably upon retirement (Cupák et al., 2019). This is evident in women’s occupational pensions, in particular (Fasang et al., 2013), but also more generally in women’s income, which is lower than men’s income, on average (Callegari et al., 2020).

Creditworthiness is a prerequisite for adults to function fully in a modern consumer society (DuFault & Schouten, 2020). Subjective creditworthiness is difficult to define, and many consumers assume that they are creditworthy as long as they are granted new credit (Rantala & Tarkkala, 2010). This is problematic, especially in light of the circles of debt that seem to emerge from having easy access to credit, combined with a lack of self-control and over-optimism (Rantala, 2012). Furthermore, consumers might perceive their credit limit as a signal of their future earning potential, which in turn could positively affect the propensity to spend (Soman & Cheema, 2002). However, according to Avery et al. (2004), the situational circumstances of consumers, both economic and personal, are generally not accounted for in models of credit history, even though adverse and temporary economic or personal shocks such as income disruption are major factors influencing payment performance.

Failure to engage in responsible lending stems from information asymmetry between consumers and lenders and the lenders’ exploitation of consumers’ behavioural biases (Cherednychenko & Meindertsma, 2019). Also regulatory failures may lead to irresponsible lending (Cherednychenko & Meindertsma, 2019; Keinänen & Vartiainen, 2016), and problems of asymmetric information seem to be more prevalent in countries with a negative credit registry (Ruuskanen et al., 2021). This negative focus identifies (potential) defaulters rather than consumers with financial potential and is operational in Denmark and Finland, for example (Hohnen & Hansen, 2021). Previous studies (Cerini, 2017; Ramsay, 2012) point out that, alongside evaluating creditworthiness, responsible lending practices should protect customers from over-indebtedness.

The interest-rate cap is one way in which legislature can curb debt problems, but it may be detrimental as it does not promote the careful assessment of creditworthiness (Mishkin, 1991; Takalo, 2019). Takalo also claims (2019) that capping the interest rate is an inefficient way of regulating the short-term consumer credit market on the grounds that it increases credit demand, especially among consumers with a poor credit rating. However, one justification for the regulation is that it protects consumers in terms of ensuring the availability of suitable financial products (ibid.).

Finance companies seem more intent on maximizing the profit a consumer brings than minimizing the risk of defaulting (Thomas, 2000), and customers who pay late generate the most profit as long as lending is profitable (Lander, 2016). Lenders are therefore unlikely to curb their money-lending business unless it is outlawed or becomes unprofitable. The adjustment of the interest-rate cap in Finland in 2013 (HE 78/2012) is a good example. After the reform, most firms offering instant loans, specifically in very small amounts, left the market, and financial institutions other than banks began to offer increasingly higher amounts of consumer credit, i.e., extensive credit (Järvelä et al., 2019). It seems that these firms had to impose a higher interest rate to be able to lend money to high-risk consumers. Exacerbated by these changes, the amount of debt originating from extensive consumer credit and distance selling increased, whereas the number of instant loans decreased (Majamaa et al., 2017).

There are some indications that financial institutions do not adequately evaluate the repayment capacity of Finnish customers (Hiilamo, 2018). First, Nordic countries still have a functioning universalistic welfare system and relatively equal income distribution, which means that larger population groups are creditworthy borrowers compared to other societies (Tranøy et al., 2020). Second, welfare states support the over-indebted in their financial distress. For example, Finns may apply for and be granted social assistance if they have unpaid debts in enforcement (Kela, 2021). Third, even if helping the over-indebted with their problems is expensive for society, it is worthwhile in that it reduces costs related to social welfare and housing, for example (Jungmann & Anderson, 2013). Thus, it seems that financial institutions do not fully carry the costs of bad credit decisions and default, some of which are met by the Finnish welfare state.

Consumer Preferences and Four Types of Unsecured Credit Products

Unsecured consumer credit is widely used for various reasons. Revolving credit makes it possible to consume even though liquid assets are allocated to future expenses (Gorbachev & Luengo-Prado, 2019). This kind of behaviour could stem from attitudes towards risk, time discounting, and perceptions of future risk related to credit access (ibid.). Consumers may have saved liquid assets to pay for cash-only spending (Telyukova, 2013), they may lack self-control (Rantala, 2012) and financial literacy (Gathergood et al., 2019), or they may need to make ends meet; thus, they prefer available unsecured credit (Navarro-Martinez et al., 2011).

There were only a few consumer-credit products in Finland before the deregulation of financial markets in the 1980s (e.g., Muttilainen, 2002), including bank loans and instalment purchases of durable goods. Following the advent of everyday financialization, however, credit providers, financial institutions, and banks nowadays offer various credit products to a wide range of consumers. In the case of unsecured credit, the money is lent based on qualifying factors such as the borrower’s credit history, income, work status, and other existing self-reported debts.

Credit-card debt is usually authorized by traditional banks and is used for repeated lending. It is widespread especially among middle-aged and middle-income consumers (Hohnen & Hansen, 2021). Males are more likely to incur such debts, and the amounts are more likely to be higher than among female credit-card holders (Yilmazer & DeVaney, 2005). Easy Internet access has also increased credit-card usage (Basnet & Donou-Adonsou, 2018), as has online shopping, which in Finland seems to be popular among all age categories (OSF, 2019a). However, young adults and those with a low educational level are the most susceptible to online-shopping-related debt problems, whereas a relatively large number of middle-aged men are particularly likely to default on credit-card debt (Majamaa et al., 2019).

Instant loans entered the Finnish credit market in the mid-2000s and became popular especially among young adults (Autio et al., 2009; Kaartinen & Lähteenmaa, 2006). This short-term consumer credit is intended to meet acute but temporary needs for money. Larger amounts of unsecured consumer credit are traditionally granted by a bank, the lenders knowing their customers and their payment history (see Hohnen & Hansen, 2021). Nowadays, a number of lending firms offer larger unsecured loans (over EUR 2000) with a long payback period (Aaltonen & Koskinen, 2019). We refer to this here as extensive consumer credit, which is granted by financial companies, and the interest-rate cap did not apply when the data was gathered.Footnote 5 Many people who take instant loans have a low level of education, live in rented accommodation, and rely on social assistance (Caplan et al., 2017); thus, it is not surprising that young adults who are in the middle of the transition phase to adulthood are particularly likely to default on such a loan (Hörkkä, 2010; Majamaa et al., 2019; Rantala, 2012). In contrast, middle-aged and older consumers are more likely to default on more extensive unsecured consumer credit (Majamaa et al., 2019).

Research Questions

Previous studies point out that consumption-based credit causes debt problems in all income brackets (Oksanen et al., 2015) but that certain sociodemographic groups are more prevalent among debtors when the focus is on the specific credit product (Majamaa et al., 2019). In that credit products tend to vary by the amount of the loan, the interest rate, and the repayment schedule, for example, assessment of creditworthiness differs accordingly. Thus, we believe that defaulted debtors will differ by the amount of the outstanding debt and by the credit product concerned. As pointed out in a previous study, credit-card-related debt problems are more common among middle-aged consumers than among young adults, whereas instant loans and online shopping cause problem indebtedness among young adults in particular (ibid).

In the following empirical analysis, we consolidate understanding gleaned from the literature reviewed above and further expand empirical knowledge about debt problems related to four unsecured forms of consumer credit: instant loans, extensive consumer credit, and both credit-card and online shopping. With reference to the theory of asymmetric information, we assume that the negative consequences of adverse selection are apparent especially with regard to instant loans and that young consumers with a low socioeconomic position in particular will suffer. Furthermore, in line with the concept of moral hazard, overly optimistic consumers in a good socioeconomic position may face more frequent debt problems originating from credit-card use and extensive consumer credit.

The analysis is based on the reformed consumer-protection act of 2013 (HE 78/2012). Because the interest-rate cap concerned only instant loans, i.e., consumer credit of less than EUR 2000, we decided to separate them from extensive consumer credit involving larger amounts. Furthermore, before the reform, the assessment of creditworthiness regarding small amounts was limited to checking whether the applicant had had a default notice, but post-reform it also took into account the applicant’s income and other economic circumstances (Järvelä et al., 2019).

Given that assessment of creditworthiness is more precise the larger the amount of credit, and that the four credit products under study are different, we first assess the association between the consumer’s position on the credit market (i.e., sociodemographic characteristics including socioeconomic position) and the amount of default debt. Our first research question (q1a) is thus: Does the amount of outstanding debt (€) differ depending on the product: (a) instant loan, (b) extensive consumer credit, (c) credit-card use, and (d) online shopping? If so, we further ask (q1b): How does the average amount (€) of outstanding debt related to the credit product vary by the sociodemographic characteristics (including socioeconomic position) of the debtor?

Assessment of creditworthiness is strongly based on the sociodemographic characteristics of consumers (including socioeconomic position) (Abdou & Pointon, 2011), and certain social groups are more credit-constrained than others (Bowles, 2004). Our second research question (q2) therefore concerns whether defaulted debtors (depending on the credit product in question) differ in the type of debt: How do defaulted debtors differ in terms of socioeconomic position when the debt problem originates from a particular credit product? We compare consumers whose debt problems originated from an instant loan, extensive consumer credit, or distance-selling to those with credit-card indebtedness. Credit-card indebtedness is a clear choice of credit product as a base group, because we assume that the information available to the consumer and the creditor is the most symmetric, given the link to the consumer’s bank.

Data, Variables, and Methods

Debt Judgements and Administrative Data

A debt judgement always triggers a payment-default entry, although the debtor may receive the notice from another source, via foreclosure or debt adjustment, for example. The aim is to prevent additional indebtedness and to inform potential lenders of the person’s payment difficulties. As noted, Finland has a negative credit register, meaning that those appearing on it are no longer eligible to buy on hire purchase or to take a bank loan, and access to consumer credit, rental housing, telephone subscriptions, Internet services, and insurance is limited. Consumers therefore do their best to avoid payment-default notices.

The following analysis is based on a random sample of 4,962 debt judgements dating from 1 January 2014 to 30 June 2016. Given that a debt judgement is a public document, non-response bias does not affect the structure of the data. It should be borne in mind, however, that the data generally provides information on one debt per debtor, not comprehensive information on all the debts that a person may have. Even so, debt judgements provide reliable information on credit products and the amount of outstanding debt.

The judgements were coded one by one, and they yielded a wealth of information on the debtor (age, gender, and place of residence), the debt (amount of debt capital and related costs), and the original creditor or claimant [dataset]. We also requested debtor-related administrative data from Statistics Finland, which we were able to merge with the data on debt judgement. The administrative data we used in the analysis reflected the situation of debtors at the end of 2013, the year that was covered most comprehensively.

If the debt capital had been paid off during the legal process, or the debt related to business or post collection, the judgements were excluded from the analysis. Cases in which the register data could not be linked to the debtors were also excluded. We used Stata 16.1 software for the analyses. Its “duplicates drop” command facilitated the removal of extra judgements involving debtors who appeared twice or three times in the data, leaving a total of 4,095 cases to be analysed. Approximately 31 per cent of the judgements concerned more than one debt and/or original creditor, the highest number of debts in one judgement being 53. If the debt judgement covered more than one form of debt capital, we included only the first one in the analyses.

We should point out that the data is a sample of debtors who received a debt judgement in 2014–2016; it is not a sample of the Finnish population. In brief, this means that young people are over-represented and those of at least 55 years of age are under-represented, as are women. In addition, debtors are more likely to be single or divorced than married or widowed, compared to the Finnish population. On average, they also have a lower level of education than the Finnish population aged 20 years or more (see Majamaa et al., 2019).

Variables

The Credit Products Under Scrutiny

We focused on four credit products in this study: defaulted debts originating from instant loans, extensive consumer credit, credit-card use, and distance selling. These four products covered 59 per cent of all debt judgements in the data. Appendix Table 2 shows the distribution of the data (n = 4095), as well as the share of debtors (%) and the average amount of outstanding debt (€) related to four different credit products by the sociodemographic and economic characteristics of the debtors.

The Sociodemographic and Economic Characteristics of the Debtors

We determined the age of the debtor according to the year the judgement was received, classified in six age groups as follows: 18–24, 25–29, 30–39, 40–49, 50–59, and 60 years and over. The last group covered 25 years (60–84), given the very low proportion of debtors among them (9.1%). The oldest debtor was aged 84. The second variable was gender. Marital status was divided into four categories: single, married, divorced, and widowed. The number of children under the age of 18 was categorized in three groups: none, one child, and at least two children. The first category also included debtors whose children lived with another parent or had moved out of the parental home.

We measured the socioeconomic position of the defaulted debtor using five variables. Educational level classified debtors in three categories based on their highest qualification: those with no qualification beyond compulsory school were categorized on the basic level; those with a matriculation or a vocational-school diploma, or a special vocational qualification, were placed on the secondary level; and those with at least a degree from a university of applied sciences (previously called a college degree) were placed on the tertiary level. Disposable monetary income includes items and benefits in kind connected to the job relationship (OSF, 2019b). Accordingly, we divided the debtors into five equal monthly income quintiles, each accounting for 20 per cent of them. We recoded labour-market position in five categories: employed, unemployed, student, retired, and other (including conscripts and other individuals outside the workforce). The amount-of-previously-taken-loans variable does not include instant and short-term loans or larger consumer credit under the Consumer Protection Act, in other words the credit products under scrutiny. We divided the debtors into three groups according to the amount of previously taken loans in Euros: no loans, up to EUR 15 000, and more than EUR 15 000. This variable reflects the consumer’s position in the credit market to some extent: Individuals with a good position are able to obtain reasonably large bank loans. The homeowner variable was dichotomous: yes or no. A right-of-occupancy apartment lies somewhere between rental and owner-occupied property. We decided to include this in the “Yes” category (homeowners), given that a right-of-occupancy payment generally amounts to 15 per cent of the purchase price of the apartment. The “No” category included debtors who were living in some type of rented accommodation.

Methods

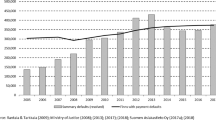

First, we report our results descriptively (Appendix Table 2). We cross-tabulated (%) the debtors’ background variables within all defaulted debts and within four types of defaulted debt: instant loans, extensive consumer credit, and credit-card and distance-selling debt. After this, we calculated the average debt capital (€) in all the defaulted debt, and in the four credit products, by the eight characteristics of debtors. We used Dunn’s post hoc test to determine whether the average amount of outstanding debt differed in the four credit products (Fig. 1).

Average amounts (€) of outstanding debt related to instant loans, extensive consumer credit, credit-card indebtedness, and distance selling: Dunn’s post hoc test between the credit products (a, b, and c)

Second, we carried out the Kruskal–Wallis H test, which identifies statistically significant differences in the means of outstanding debt. It is the nonparametric alternative to the one-way Anova if the dependent variable is not approximately normally distributed for each category of the independent variable. Initially we used the test to find out whether the amount of outstanding debt differed among debtors in all defaulted debts (Appendix Table 2). Next, we focused on debtors in receipt of a debt judgement because of an instant loan, extensive consumer credit, credit-card debt, or distance-selling debt (Appendix Table 3). Given that the Kruskal–Wallis H test only shows that at least some categories are different, we then conducted Dunn’s post hoc test to determine more closely which of the categories differed from each other statistically significantly. Figures 2 and 3 show how the amount of outstanding debt (€) originating from instant loans differs by the debtors’ characteristics.

Average amounts of instant-loan-related debt (€) by age group, gender, marital status, and number of children under the age of 18: Dunn’s post hoc test (n = 1,255) (*** p < 0.001; ** p < 0.01; * p < 0.05; + p < 0.10)

Average amounts of instant-loan indebtedness (€) by educational level, disposable income, labour-market position, home ownership, and amount of previously taken debt: Dunn’s post hoc test (n = 1,225) (*** p < 0.001; ** p < 0.01; * p < 0.05; + p < 0.10)

Third, we subjected our data to multinomial logistic regression analysis, in which the response variable has more than two categories, and then we compared group X and the base group. We made three comparisons between defaulting debtors by the different credit products: (1) instant loan, (2) extensive consumer credit, and (3) distance-selling debt, the base group consisting of those whose judgement originated from credit-card debt. The first category in each explanatory variable is the reference group with the relative risk ratio (RRR) of one (1). We included only four credit products in the analyses (n = 2,420).

We fitted each main effect into the model (Model 1) one at a time to find out the extent to which debtor characteristics were associated with debt problems attributable to the different credit products. To control for all the characteristics of the debtors under consideration (Table 1), we fitted all the main effects into Model 2.

We should point out that when the RRR is interpreted, comparisons are always made with the base group. As Table 1 shows (Model 1), for example, the relative risk ratio for women who had debt problems because of an instant loan compared to those whose problem debts related to credit-card use (base category) is 1.42 times as high as the same ratio for men. In other words, instant-loan indebtedness is more likely among women than among men when those whose default relates to an instant loan are compared to those in default because of credit-card debt. The significance levels of the p-values in Table 1, Fig. 2, and Fig. 3 are shown with asterisks: + p < 0.1; * p < 0.05; ** p < 0.01; *** p < 0.001.

We should also reiterate that a consumer’s total debt problem usually includes a number of different debts, as well as different credit products, such as unpaid consumer credit and overdue invoices, unpaid rent, mortgages, and taxes (Poppe et al., 2016). Even if our dataset does not allow scrutiny of the total structure of a consumer’s debt, we can focus on those whose indebtedness relates to a particular product. The consumer’s choice to take (and to default on) an instant loan, for example, does not rule out the possibility of also taking (and defaulting on) credit-card indebtedness. In short, our analysis highlights which consumer groups are at the highest risk of default related to a specific credit product during a certain time phase, thereby enabling us to discuss in greater depth the position of consumers in the credit market, consumer creditworthiness and the factors that increase the risk of default.

Results

Overview: The Average Amount (€) of Outstanding Debt Varies by the Four Credit Products

Almost one-third of the defaulted debts are related to an instant loan (30.6%). Default related to distance selling was also quite common (15.4%), whereas debt-capital-related credit-card default (7.6%) and extensive consumer credit (5.4%) were less prevalent (Appendix Table 2). Outstanding debt was highest in cases of extensive consumer credit, accounting for more than five times the amount of debt from instant loans (EUR 3330 vs. EUR 700), and lowest concerning judgements related to distance selling, at around EUR 260. The average debt capital related to credit-card indebtedness was EUR 2290. As depicted in Fig. 1, Dunn’s post hoc test revealed that the average amounts of outstanding debt were statistically significant between all four credit products (q1a).

We ran the Kruskal–Wallis H test to see if the debtors’ sociodemographic characteristics (including socioeconomic position) differed by the amount of defaulted debt (€) in the four credit products, in other words instant loans, extensive consumer credit, credit-card debt, and distance selling (q1b). The results revealed statistically significant differences only in debt capital originating from instant loans. The differences were statistically significant for all the examined variables except gender (Appendix Table 3); therefore, we focus only on problems originating from instant loans. Appendix Table 2 shows all average outstanding debts (€) by the debtors’ background variables.

The Better the Socioeconomic Position of an Instant-Loan Debtor, the Higher the Average Amount of Debt

In further addressing our first research question (q1b), we ran Dunn’s post hoc test, comparing the average amounts of instant-loan debt (€) by the debtors’ sociodemographic characteristics (including socioeconomic position). The referent category (ref.) of each variable is in darker blue, and the asterisks show the statistical significance between the referent and the other groups. The notation “n.s.” below the bar means that the difference between the means in question is not statistically significant (see Figs. 2 and 3).

As Fig. 2 shows, members of the youngest age group (18–24) had, on average, significantly lower levels of debt capital originating from instant loans (EUR 360) than those in the other age groups. The amount of defaulted debt among young adults was above half of that in the older age groups: Among debtors over the age of 60, for example, the average amount was EUR 960. There were no gender differences in average amounts of outstanding debt (€), and the value of defaulted instant loans was approximately EUR 700 among women and men (Fig. 2). Furthermore, singles, who also tend to be under the age of 30, had lower average debt capital than those in the other marital-status groups. However, the difference was not statistically significant when we compared singles to widows. Figure 2 further shows that debtors with at least two children under the age of 18 have higher average debt capital from instant loans than those without children.

Debtors with higher educational and income levels, on average, had higher liabilities than their less-highly-educated and lower-income counterparts (Fig. 3). The amount of debt capital involved was lower among students, the unemployed, and “others,” whereas the average amount of instant loans among pensioners was EUR 680. The difference in debt capital among the retired (Fig. 3) and among people aged 60 years and over (EUR 681 vs. EUR 956) is somewhat surprising, but it is explained by the particularly high average amount of instant loans (EUR 1,100) among the oldest debtors still of working age (40.2%). (This result is not shown.)

As Fig. 3 further shows, the average amounts of debt capital were higher among homeowners than among non-owners: Defaulted debt originating from instant loans was, on average, EUR 799 and EUR 641, respectively. The amount of outstanding debt involved was also higher, on average, among debtors with previous loans of over EUR 15 000 than among those with no previously incurred debt (EUR 617 vs. EUR 864). If higher education and income levels, employment, homeownership, and larger amounts of previously incurred debt are considered a sign of good standing in the credit market, our results are consistent with previous findings (see, e.g., Bridges & Disney, 2004; Xiao & Yao, 2020).

Debtors’ Socio-demographic Characteristics Vary Depending on the Credit Product

Our second research question concerns the socioeconomic position of defaulted debtors and how they differ from each other in the four credit products. We used multinomial logistic regression to compare debtors in default by the different products. Table 1 shows the relative risk ratios (RRR) for debtors in receipt of a debt judgement originating from an instant loan, extensive consumer credit, and distance-selling debt, the referent group being credit-card indebtedness. Model 1 shows each variable introduced one at a time, and Model 2 presents the estimates adjusted for all variables.

When we compared debtors from three different credit products to consumers with unpaid credit-card debt, almost all the variables we included in Model 1 (gender, age, marital status, number of children under the age of 18, educational level, disposable income, labour-market position, amount of previously taken debt, and home ownership) were associated with the different credit products (Table 1, Model 1). The only exceptions were the number of children under the age of 18, educational level, amount of previously taken debt, and homeowner status, which were not statistically significant with regard to defaulted debts originating from extensive consumer credit compared to credit-card indebtedness.

Instant Loans Versus Credit-Card Indebtedness

As the results in Table 1 (Model 2) show, women seem to be more likely (than men) to have a debt problem because of an instant loan relative to credit-card debt (RRR = 1.583**). It was less surprising, however, that the under-25 s, in particular, are more likely (than their older counterparts) to have an instant-loan-related debt problem relative to credit-card debt. The relative risk ratio of marital status indicates that the married are less likely than singles to have defaulted debts originating from instant loans if the reference group is credit-card debtors. Furthermore, debtors with a low monthly income as well as those with no previously taken debt are more likely to have a debt problem related to instant loans than to credit-card debt. However, we could not find differences relating to educational level, labour-market position, or homeowner status.

Extensive Consumer Credit Versus Credit-Card Indebtedness

As Table 1 (Model 2) shows, debt problems among women, compared to men, are more likely to be attributable to extensive consumer credit than to credit-card debt (RRR = 1.990***). Moreover, older debtors are more at risk of incurring debt attributable to extensive consumer credit than to credit-card use. According to our findings, the relative risk ratio is 0.4999(*) among the unemployed (ref. employed) when the debt originates from extensive consumer credit compared to credit-card use. We found no differences based on educational level, disposable income, amount of previously taken debt, or homeowner status, however.

Distance-Selling Versus Credit-Card Indebtedness

Once again, it seems that women are more likely than men to have a debt problem because of this credit product: The relative risk ratio in distance-selling as opposed to credit-card debt is 2.52 (***). Moreover, debts among the over-30 s compared with the under-25 s are less likely to be attributable to distance selling when the reference group comprises those with a credit-card debt. Furthermore, the higher the number of children under the age of 18 in the household, the more likely it is that debt originates from distance selling than from credit-card use. It is also more likely that indebtedness among those on a low income and without previously taken debt is attributable to distance selling than to credit-card use (Table 1). We found no other differences among the variables measuring the socioeconomic position of the defaulted debtor.

Summary and Discussion

There is little available information about the customers of lending companies, but our results shed some light on consumers who have problem debts, meaning unpaid debts arising from various unsecured consumer loans. The data used in this study comprised approximately 4000 debt judgements issued in 2014–2016 and administrative data on the debtors [dataset]. Our aim was to expand empirical knowledge of debt problems related to four types of unsecured consumer credit: instant loans, extensive consumer credit, credit-card use, and online shopping. Even if the results are mixed, there are some uniform features, and young adults are highlighted. Next, we discuss the significance of our main findings.

We found that the average debt capital originating from instant loans was highest among the retired and significantly lower among young adults (who tended to belong to the lowest income group). Our findings also showed that debtors in a lower socioeconomic position had less outstanding debt (€) on average, at least in terms of instant loans. Assessment of creditworthiness has focused more closely on the consumer’s income and other economic circumstances since the reform of 2013 (HE 78/2012); thus, these results imply that finance companies evaluate the socioeconomic position of potential lenders in some way.

Given that young adults have particularly weak financial skills (Kalmi & Ruuskanen, 2016; Lusardi & Mitchell, 2011), and they also have limited opportunities to be active in the credit market (Bowles, 2004), it was not surprising that the number of debt judgements originating from instant loans and distance selling was higher among the under-25 s than in the other age groups. Our results also revealed that the middle-aged and the retired were more likely than young adults to have outstanding debts related to extensive consumer credit, as well as credit-card debt, but many of them also had problem debts originating from instant loans. These findings indicate that, because of their wealth (Bridges & Disney, 2004), middle-aged and retired people are in a better position than young people to obtain larger amounts of different types of credit.

One interesting finding relates to gender, which was strongly associated with unpaid debt attributable to the credit products under investigation. Women were at a higher risk of incurring problem debts related to instant loans, distance selling, and extensive consumer credit relative to credit-card debt. One reason for this result could be the average lower income of women, which affects their position in the credit market (Callegari et al., 2020) and increases their risk to default on these credit products. This claim needs further research, however.

Young adults in particular were likely to default because of instant loans before the 2013 reform (Hörkkä, 2010; Rantala, 2012). According to our results, this tendency is still present in that the risk of default was highest among young adults with a low socioeconomic position. Another credit product used among high-risk consumers is distance selling, which is very popular in Finland (OSF, 2019a), and because the amounts of outstanding debt are very small on average, we believe that those who have problem debts related to distance-selling generally have difficulties in making ends meet. Addictions, weakness of will and other defective behavioural patterns (Bowles, 2004; Cherednychenko & Meindertsma, 2019) such as compulsive shopping may also be behind the outstanding debt.

Our results further reveal that those who run into debt problems because of instant loans or distance selling are less likely than those whose debt judgement originated from credit-card use to have taken a loan previously. The trend nowadays, especially among some young people, is to use little or no credit to invest in future projects such as education and housing and to use more for everyday consumption and making ends meet (see also Houle, 2014). They may not understand the various consequences and possible sanctions if they do not comply with credit terms. A small number of debts related to unpaid instant loans and online shopping resulted in a payment-default notice. Combined with a bad credit history, this makes it difficult for many young adults to obtain a loan or to conclude a contract, and risks ruining their prospects.

Consumer credit is widely used for consumption purposes in everyday-life contexts (Aaltonen & Koskinen, 2019). According to our results, high-cost credit in particular causes problems. Our findings also indicate that asymmetric information among consumers and lenders may lead to failure in the lending process. However, the effects of information asymmetry manifest differently depending on whether the focus is on the actors in the credit market, namely consumers (loan applicants) and loan companies, or those affected by the negative outcomes of erroneous credit decisions, namely defaulted consumers.

According to the theory of asymmetric information, low-risk consumers are the ones who “pay the price” of high interest rates due to information asymmetry and adverse selection, given that the interest rates are high for high-risk consumers in any case (Drake & Holmes, 1995). If lending companies had enough information about their customers and their default risk, they could target negative credit decisions on high-risk loan applicants (e.g., young adults) and positive decisions with low interest rates on low-risk applicants. However, as our results revealed, many older consumers with a good socioeconomic position defaulted. If a new loan (such as extensive consumer credit or an instant loan) is taken out to remedy financial difficulties and repay previously taken loans, debt easily defaults in the long term. Thus, loss aversion may incur the moral hazard problem, manifested as a debt spiral. Indeed, the threat of a negative credit register may provoke Finnish debtors into avoiding a payment-default entry as long as possible (Rantala, 2012). Defaulted middle-aged and retired consumers would survive with less damage if they had acknowledged their inability to pay previously taken debts at an earlier stage.

As the Finnish government regulated instant-loan contracts for less than EUR 2,000 and many small firms offering instant loans left the credit market (Järvelä et al., 2019), we believe that the interest-rate cap in 2013 was advantageous for young adults. Many young people defaulted on small instant loans before the regulation came into force (see Hörkkä, 2010; Rantala, 2012), but then the rate of default began to decline (Asiakastieto, 2021; Majamaa et al., 2017) and an increasing number applied for social assistance (Kela, 2018). In addition to the interest-rate cap, there could be more price transparency related to short-term consumer credit (Takalo, 2019) that would help consumers to understand what a high interest rate means in practice, for example.

One intriguing question concerns what would happen if these unsecured credit products were not available to high-risk consumers. Would they resort to the informal loan market or pawn shops, for example (Dobbie & Skiba, 2013)? We believe that if high-risk consumers do not have access to the most problematic unsecured credit, they will have to rely on support from the welfare state or their friends and relatives, as many young adults seem to do. However, one possibility is that illegal and hidden black-market activities would flourish, which could have even more severe consequences for over-indebted consumers than default. There is very little information about this phenomenon in Finland, but at least according to Rantala (2012), typical debtors who are active in the black market, or what she refers to as the “criminal loan market,” seem to be criminals rather than “ordinary consumers.” It is possible that high-risk consumers would reduce their overall consumption if their access to such forms of credit was blocked, which would negatively affect their welfare in the short term. In the end, however, defaulted debt threatens not only financial, but also physical and emotional welfare (Hiilamo, 2018).

Conclusion

This article focused on debt judgements originating from four different credit products. Even if our data gives a good picture of problem debts among Finnish consumers, we should point out that the overall situation remains unclear. In general, the market position of consumers varies, which affects their access to credit. Credit-constrained consumers may need to take on more expensive unsecured loans from a finance company instead of the bank, where they are known but are considered risky clients. A low level of financial literacy may lead to the taking on of high-cost credit and further to insolvency. Regulation should protect young consumers in the current loan market, in particular, even if there are also some negative consequences. For example, many providers of instant loans disappeared from the Finnish credit market after 2013, but there is still a demand for them. We therefore highlight the need to develop more sustainable loan products to meet the requirements of high-risk, low-income consumers. In terms of social responsibility, small and low-interest credit products should be more easily available to applicants with a realistic repayment plan, for example.

Because lenders are seen as professionals in financialized credit markets, and clients as laypeople, we suggest that financial institutions should focus more strongly on the assessment of customer creditworthiness even in the case of loans involving small sums. As long as high-risk borrowers have an incentive to apply for credit to ease their financial situation or to buy goods, or because of behavioural bias, the risk of default is high: If realized it will harm the borrower in particular, but also the lender (see, e.g., Hiilamo, 2018). Lenders may not have the same information as borrowers, but as professionals, they know the odds of defaulting, and which sociodemographic groups are most at risk (see Hörkkä, 2010). Indeed, they could use this information more actively in their credit decisions.

The number of consumers with debt problems continues to grow, and it is not clear why. We suggest that at least some lending firms fall short in terms of responsible practices and the effective assessment of creditworthiness and that consumers have inadequate financial skills (see also Lusardi & Mitchell, 2011; Xiao & Yao, 2020). Consumer responsibility in terms of applying for, using, and repaying credit is a prerequisite in current credit markets to avoid the harmful consequences of default on the individual as well as on the societal level. Other events that are known to cause financial difficulties and debt problems include the transition to adult life, as well as sudden life changes in families such as going through a relationship break up (Autio et al., 2009; Nielsen et al., 2019; Oksanen et al., 2016;), but lending companies do not appear to take these risks into account in their credit-scoring models (Avery et al., 2004). We therefore pose the following question. Should potential lenders in the current financialized society consider some of the most common life transitions in their assessments of consumer creditworthiness?

Over-lending may result if consumers apply for and receive loans that far exceed their ability to repay or creditors grant new credit despite a history of previous (unpaid) loans. Indeed, customer selection in loan companies needs some fine-tuning. Asymmetric information systematically allows some firms to free ride with lending firms that manage their risks more effectively (De Meza, 2002), but a positive credit register prevents at least some such activity. Finland currently has a negative credit register in which only payment-default entries are listed. In practice, this means that consumers have relatively free access to new credit as long as their credit reference is good. A positive credit register will be introduced in 2024. In yielding information about customer loans, excluding distance-selling purchases and other overdue invoices, this will probably flag repayment problems at an earlier stage and thus promote responsible lending (Kontkanen & Lång, 2018), but the lack of such information will make it difficult to recognize some debt problems in the future, too.

Lending companies provide very little information about their customers, their credit-scoring systems, or their clients who run into debt problems attributable to the credit. This complicates regulation given that legislators have to make decisions based on incomplete information, and regulation can be used only up to a certain limit. In addition, as a new product, e-commerce is difficult to regulate. Thus, consumers in current credit markets need to accept responsibility for their borrowing and to act accordingly.

Debt problems are strongly associated with well-known risk factors such as a low level of financial literacy, a low socioeconomic position, and life transitions (see, e.g., Lusardi & Mitchell, 2011; Nielsen et al., 2019; Oksanen et al., 2015, 2016). According to the findings reported in this article, debtors stand out in terms of sociodemographic characteristics (including their socioeconomic position) by credit product and the amount of debt. Thus, we conclude that current debt problems reflect (1) an abundant supply of consumer credit, which seems to foster asymmetric information, (2) the consumer’s position in the credit market (i.e., income level, access to different products), (3) the consumer’s competence to act in the credit market (i.e., the use of unsecured consumer credit), and (4) various overall risk factors (i.e., gender, age, and employment). Moreover, these factors are partly overlapping. Overall, there is a need to build a more comprehensive picture of the various types of debt that lead to severe problems. It would be particularly useful to conduct population-level analyses of indebtedness across different credit products, as well as of attitudes towards lending.

Data Availability

Dataset is not publicly available to preserve individuals’ privacy under the European General Data Protection Regulation.

Change history

13 October 2022

Missing Open Access funding information has been added in the Funding Note.

Notes

Instant loans typically amount to less than EUR 1,000. Given that the repayment time is very short, usually a few weeks or months, the annual interest rate for this type of unsecured consumer credit used to be well over 100 per cent, but after the legislative reform of June 2013 (HE 78/2012), an interest-rate cap (benchmark interest rate + 50%) was set on unsecured consumer loans of less than EUR 2,000.

Extensive consumer credit refers to instant loans of over EUR 2,000, normally at an interest rate of less than 50 per cent.

Credit-card indebtedness refers to unpaid instalments, the interest rate tending to be approximately 10 per cent.

Debts related to distance selling are incurred mainly from online shopping and credit accounts attached to commodities related to ecommerce.

In 2013, the interest-rate cap (50%) on consumer credit of less than EUR 2,000 was adjusted in Finland. Six years later, in September 2019, a cap of 20% was specified for all consumer credit.

References

Aaltonen, M., & Koskinen, K. (2019). New methods needed to rein in consumer credit. Bank of Finland Bulletin 2/2019. https://www.bofbulletin.fi/en/2019/2/new-methods-needed-to-rein-in-consumer-credit/. Accessed 27 June 2022.

Abdou, H. A., & Pointon, J. (2011). Credit scoring, statistical techniques and evaluation criteria: A review of the literature. Intelligent Systems in Accounting Finance & Management, 18(2–3), 59–88.

Asiakastieto. (2021). Nuorten maksuhäiriöt ovat vähentyneet vuodesta 2013 lähtien. https://www.asiakastieto.fi/web/fi/asiakastieto-media/uutiset/nuorten-maksuhairiot-ovat-vahentyneet-vuodesta-2013-lahtien.html. Accessed 27 June 2022.

Autio, M., Wilska, T.-A., Kaartinen, R., & Lähteenmaa, J. (2009). The use of small instant loans among young adults – A gateway to a consumer insolvency? International Journal of Consumer Studies, 33, 407–415.

Avery, R. B., Calem, P. S., & Canner, G. B. (2004). Consumer credit scoring: Do situational circumstances matter? Journal of Banking & Finance, 28, 835–856.

Basnet, H. C., & Donou-Adonsou, F. (2018). Marriage between credit cards and the Internet: Buying is just a click away! Review of Financial Economics, 36(3), 252–266.

Betti, G., Dourmashkin, N., Rossi, M., & Yin, Y. P. (2007). Consumer over-indebtedness in the EU: Measurement and characteristics. Journal of Economic Studies, 34(2), 136–156.

Bowles, S. (1998). Endogenous preferences: The cultural consequences of markets and other economic institutions. Journal of Economic Literature, 36(1), 75–111.

Bowles, S. (2004). Microeconomics. Behavior, institutions, and evolution. Princeton University Press.

Bridges, S., & Disney, R. (2004). Use of credit and arrears on debt among low income families in the United Kingdom. Fiscal Studies, 25, 1–25.

Brown, S., Veld, C., & Veld-Merkoulova, Y. (2018). Credit cards: Transactional convenience or debt-trap? International Review of Finance, 20(2), 295–322.

Callegari, J., Liedgren, P., & Kullberg, C. (2020). Gendered debt – A scoping study review of research on debt acquisition and management in single and couple households. European Journal of Social Work, 23(5), 742–754.

Caplan, M., Kindle, P.A., & Nielsen, R.B. (2017). Do we know what we think we know about payday loan borrowers? Evidence from the Survey of Consumer Finances. The Journal of Sociology & Social Welfare, 44(4), 3.

Cerini, D. (2017). Consumer over-indebtedness, credit contracts and responsible lending. Global Jurist, 17(3), 1–14.

Chan, S. (2013). ‘I am King’: Financialisation and the paradox of precarious work. The Economic and Labour Relations Review, 24(3), 362–379.

Cherednychenko, O. O., & Meindertsma, J. M. (2019). Irresponsible lending in the post-crisis era: Is the EU consumer credit directive fit for its purpose? Journal of Consumer Policy, 42, 483–519.

Cupák, A., Kolev, G. I., & Brokešová, Z. (2019). Financial literacy and voluntary savings for retirement: Novel causal evidence. The European Journal of Finance, 25(16), 1606–1625.

De Meza, D. (2002). Overlending. The Economic Journal, 112(477), F17–F31.

Dobbie, W., & Skiba, P. M. (2013). Information asymmetries in consumer credit markets: Evidence from payday lending. American Economic Journal: Applied Economics, 5(4), 256–282.

Drake, L., & Holmes, M. (1995). Adverse selection and the market for consumer credit. Applied Financial Economics, 5, 161–167.

DuFault, B. L., & Schouten, J. W. (2020). Self-quantification and the datapreneurial consumer identity. Consumption Markets & Culture, 23(3), 290–316.

Ertürk, I., Froud, J., Johal, S., Leaver, A., & Williams, K. (2007). The democratization of finance? Promises, outcomes and conditions. Review of International Political Economy, 14(4), 553–575.

Eurofound. (2020). Addressing household over-indebtedness. Publications Office of the European Union, Luxembourg. https://doi.org/10.2806/25005. Accessed 27 June 2022.

Fasang, A. E., Aisenbrey, S., & Schömann, K. (2013). Women’s retirement income in Germany and Britain. European Sociological Review, 29(5), 968–980.

Ferretti, F., & Livada, C. (2016). The over-indebtedness of European consumers under EU policy and law. In F. Ferretti (Ed.), Comparative perspectives of consumer over-indebtedness: A view from the UK, Germany, Greece, and Italy (pp. 11–37). Eleven International Publishing.

Gathergood, J., Guttman-Kenney, B., & Hunt, S. (2019). How do payday loans affect borrowers? Evidence from the U.K. market. The Review of Financial Studies, 32(2), 496–523.

Gorbachev, O., & Luengo-Prado, M. (2019). The credit card debt puzzle: The role of preferences, credit access risk, and financial literacy. The Review of Economics and Statistics, 101(2), 294–309.

HE. (78/2012). Hallituksen esitys eduskunnalle laeiksi kuluttajansuojalain 7 luvun, eräiden luotonantajien rekisteröinnistä annetun lain sekä korkolain 2 §:n muuttamisesta. https://www.eduskunta.fi/FI/vaski/HallituksenEsitys/Documents/he_78+2012.pdf. Accessed 27 June 2022.

Hiilamo, H. (2018). Household debt and economic crises: Causes, consequences and remedies. Edward Elgar Publishing.

Hohnen, P., & Hansen, A. R. (2021). Credit consumption and financial risk among Danish households— A register-based study of the distribution of bank and credit card deb. Journal of Consumer Policy, 44, 311–328.

Houle, J. N. (2014). A generation indebted: Young adult debt across three cohorts. Social Problems, 61(3), 1–18.

Hörkkä, A. (2010). The determinants of default in consumer credit market. [Master Thesis]. http://epub.lib.aalto.fi/fi/ethesis/pdf/12299/hse_ethesis_12299.pdf. Accessed 27 June 2022.

Jungmann, N., & Anderson, M. (2013). Debt management pays off! A research on the cost and benefits of debt management in the Netherlands*. European Review of Private Law, 21(3), 815–822.

Järvelä, K., Raijas, A., & Saastamoinen, M. (2019). Pikavippiongelmien laatu ja laajuus. Kilpailu- ja kuluttajavirasto, selvityksiä 3/2019. https://www.kkv.fi/globalas-sets/kkv-suomi/julkaisut/selvitykset/2019/kkv-selvityksia-3-2019-pikavippiongelmien-laatu-ja-laajuus.pdf. Accessed 27 June 2022.

Kaartinen, R., & Lähteenmaa, J. (2006). Miten ja mihin nuoret käyttävät pikavippejä ja muita kulutusluottoja? KTM Rahoitetut tutkimukset No. 10. Kauppa- ja teollisuusministeriö.

Kalmi, P., & Ruuskanen, O.-P. (2016). Suomalaiset pärjäävät taloudellisessa tietämyksessä ja käyttäytymisessä hyvin suhteessa muihin maihin. Kansantaloudellinen Aikakauskirja, 112, 6–21.

Kangas, O., & Kvist, J. (2018). Nordic welfare states. In B. Greve (Ed.), Routledge handbook of the welfare state (pp. 124–136). Routledge.

Karamessini, M., Symeonaki, M., Stamatopoulou, G., & Parsanoglou, D. (2019). Factors explaining youth unemployment and early job insecurity in Europe. In B. Hvinden, T. Sirovátka, & J. O’Reilly (Eds.), Youth unemployment and early job insecurity in Europe: Concepts, consequences and policy approaches? (pp. 45–69). Edward Elgar.

Keinänen, A., & Vartiainen, N. (2016). Pikaluottojen valvonta – miten lainsäädännön valvonta toteutuu käytännössä? Edilex 2016/23. https://www.edilex.fi/artikkelit/16796.pdf. Accessed 27 June 2022.

Kela - Social Insurance Institution of Finland. (2018). Perustoimeentulotukea maksetaan muita useammin nuorille aikuisille. https://sosiaalivakuutus.fi/perustoimeentulotukea-maksetaan-muita-useammin-nuorille-aikuisille/. Accessed 27 June 2022.

Kela - Social Insurance Institution of Finland. (2021). Tulot, jotka eivät vaikuta perustoimeentulotukeen. Retrieved from https://www.kela.fi/toimeentulotuki-tulot-jotka-eivat-vaikuta. Accessed 27 June 2022.

Kočenda, E., & Vojtek, M. (2011). Default predictors in retail credit scoring: Evidence from Czech banking data. Emerging Markets Finance and Trade, 47(6), 80–98.

Kontkanen, E., & Lång, J. (2018). Selvitys positiivisia luottotietoja koskevan järjestelmän edellytyksistä. Helsinki: Ministry of Justice. http://julkaisut.valtioneuvosto.fi/handle/10024/161002. Accessed 27 June 2022.

Lander, D. A. (2016). Consumer Credit Regulation. In J. J. Xiao (Ed.), Handbook of Consumer Finance research (2nd ed., pp. 301–313). Springer Publishing.

Leyshon, A., & Thrift, N. (1999). The capitalization of almost everything: The future of finance and capitalism. Culture and Society, 24(7–8), 97–115.

Livada, C. K. (2019). Assessment of consumers’ creditworthiness. ERA Forum, 20, 225–236.

Livshits, I., Mac Gee, J. C., & Tertilt, M. (2016). The democratization of credit and the rise in consumer bankruptcies. The Review of Economic Studies, 83(4), 1673–1710.

Lusardi, A., & Mitchell, O.S. (2007). Financial literacy and retirement preparedness. Evidence and implications for financial education. Business Economics, 42(1), 35–44.

Lusardi, A., & Mitchell, O. S. (2011). Financial literacy around the world: An overview. Journal of Pension Economics and Finance, 10(4), 497–508.

Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5–44.

Lusardi, A., & Tufano. P. (2009). Debt literacy, financial experiences, and over indebtedness. National Bureau of Economic Research Working Paper 14808. https://www.nber.org/papers/w14808. Accessed 27 June 2022.

Majamaa, K., Lehtinen, A.-R., & Rantala, K. (2019). Debt judgments as a reflection of consumption-related debt problems. Journal of Consumer Policy, 42, 223–244.

Majamaa, K., Sarasoja, L., & Rantala, K. (2017). Viime vuosien muutokset vakavissa velkaongelmissa. Analyysi velkomustuomioista. Yhteiskuntapolitiikka, 82(6), 676–686.

Martin, R. (2002). Financialization of daily life. Temple University Press.

Mishkin, F.S., (1991). Asymmetric information and financial crisis: A historical perspective. A National Bureau of Economic Research Project Report. University of Chicago Press, 69–108.

Montgomerie, J. (2007). Financialization and consumption: An alternative account of rising consumer debt levels in Anglo-America. CRESC Working Paper Series. https://www.escholar.manchester.ac.uk/api/datastream?publicationPid=uk-ac-man-scw:181191&datastreamId=FULL-TEXT.PDF. Accessed 27 June 2022.

Muttilainen, V. (2002). Luottoyhteiskunta: Kotitalouksien velkaongelmat ja niiden hallinnan muodonmuutos luottojen säännöstelystä velkojen järjestelyyn 1980- ja 1990-luvun Suomessa. (English summary). Publication no. 189. National Research Institute of Legal Policy. Hakapaino Oy.

Navarro-Martinez, D. et al. (2011). Minimum required payment and supplemental information disclosure effects on consumer debt repayment decisions. Journal of Marketing Research, 48, SPL, S60–S77.

Nielsen, M. L., Dyreborg, J., & Lipscomb, H. J. (2019). Precarious work among young Danish employees - A permanent or transitory condition? Journal of Youth Studies, 22(1), 7–28.

Oksanen, A., Aaltonen, M., & Rantala, K. (2015). Social determinants of debt problems in a Nordic welfare state: A Finnish register-based study. Journal of Consumer Policy, 38, 229–246.

Oksanen, A., Aaltonen, M., & Rantala, K. (2016). Debt problems and life transitions: A register-based panel study of Finnish young people. Journal of Youth Studies, 19(9), 1183–1203.

OSF – Official Statistics of Finland. (2019a). Use of information and communication technologies by the population [online publication]. http://www.stat.fi/til/sutivi/2019a/sutivi_2019a_2019a-11-07_kat_003_fi.html. Accessed 27 June 2022.

OSF – Official Statistics of Finland. (2019b). Concepts and definitions – Disposable money income. http://www.tilastokeskus.fi/til/tjkt/kas_en.html?/til/tjkt/kas_en.html. Accessed 27 June 2022.

Poppe, C., Lavik, R., & Borgeraas, E. (2016). The dangers of borrowing in the age of financialization. Acta Sociologica, 59(1), 19–33.

Ramsay, I. (2012). Consumer credit regulation after the fall: International dimensions. Journal of European Consumer and Market Law, 1, 24–34.

Rantala, K. (2012). Vippikierteen muotokuva. Helsinki: Oikeuspoliittisen tutkimuslaitoksen verkkokatsauksia 24/2012. https://helda.helsinki.fi/handle/10138/15257. Accessed 27 June 2022.

Rantala, K., & Tarkkala, H. (2010). Luotosta luottoon. Velkaongelmien dynamiikka ja uudet riskiryhmät yhteiskunnan markkinalogiikan peilinä. Yhteiskuntapolitiikka, 75(1), 19–33.

Ruuskanen, O.-P., Godenhielm, M., Vaahtoniemi, S., & Kalmi, P. (2021). Positiivisen luottotietorekisterin vaikutukset luotonantoon ja ylivelkaantumiseen. Valtioneuvoston selvitys 2021:2. http://urn.fi/URN:NBN:fi-fe2021041610748. Accessed 27 June 2022.

Soman, D., & Cheema, A. (2002). The effect of credit on spending decisions: The role of the credit limit and credibility. Marketing Science, 21(1), 32–53.

Stiglitz, J. E., & Weiss, A. (1981). Credit rationing in markets with imperfect information. The American Economic Review, 71(3), 393–410.

Takalo, T. (2019). Regulation of short-term consumer credits. Journal of Banking Regulation, 20, 348–354.

Telyukova, I. (2013). Household need for liquidity and the credit card debt puzzle. The Review of Economic Studies, 80(3), 1148–1177.

Thomas, L. C. (2000). A survey of credit and behavioural scoring: Forecasting financial risk of lending to consumers. International Journal of Forecasting, 16, 149–172.

Tranøy, B. S., Stamsø, M. A., & Hjertaker, I. (2020). Equality as a driver of inequality? Universalistic welfare, generalised creditworthiness and financialised housing markets. West European Politics, 43(2), 390–411.

van der Zwan, N. (2014). State of the art. Making sense of financialization. Socio-Economic Review, 12, 99–129.

Xiao, J. J., & Yao, R. (2020). Debt types and burdens by family structures. International Journal of Bank Marketing, 38(4), 867–888.

Yard, S. (2004). Consumer loans with fixed monthly payments Information problems and solutions based on some Swedish experiences. The International Journal of Bank Marketing, 22(1), 65–80.

Yilmazer, T., & DeVaney, S. A. (2005). Household debt over the life cycle. Financial Services Review, 14, 285–304.

Funding

Open Access funding provided by University of Helsinki including Helsinki University Central Hospital.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of Interest

The authors declare no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Majamaa, K., Lehtinen, AR. An Analysis of Finnish Debtors Who Defaulted in 2014–2016 Because of Unsecured Credit Products. J Consum Policy 45, 595–617 (2022). https://doi.org/10.1007/s10603-022-09525-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10603-022-09525-4