Abstract

Increasing the participation of women in top-level corporate boards is high on the agenda of policy-makers. Yet, we know little about director appointment dynamics and the drivers and impediments of women appointments. This study builds on organizational and group-level behavior theories and empirically investigates how ex-ante board structures and gender-specific board dynamics impact the representation of women on corporate boards. We study boards of listed firms in Europe between 2002 and 2019 and find a declining appointment probability for every additional woman, i.e., the share of women already on the board negatively predicts the likelihood of additional women appointments. Further, we find evidence of a replacement effect, i.e., the likelihood of a woman being appointed as director is significantly larger when a woman, compared to when a man, leaves the board. We do not find spillover effects from non-executive to executive boards. These results are robust to econometric model specifications that address potential endogeneity concerns using matching and instrumental variables. Our results confirm that board director appointments are gender specific and suggest that demand-side factors such as explicit and implicit norms drive women appointments up to a certain threshold.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Boards of directors play a central role in the corporate governance of listed firms. Board structures and their determinants therefore receive considerable attention in both public debate and academic research.Footnote 1 One of the most debated trends in the development of corporate boards is the representation of women (Baker et al., 2020). In light of women earning more college degrees than men in many OECD countries for nearly 40 years (OECD, 2020), it is striking that their presence in boardrooms and c-level positions does not reflect this evolution. In 2020, women held only 6.4% of Fortune 500 chairperson roles, and only around one-fourth of all board members in US firms are women (Deloitte, 2021). The picture is similar in Europe. Recent publications report low, although increasing, levels of women in executive and non-executive board roles in the largest listed firms in the European Union. In 2020, 31% of the non-executive and 18% of the executive directors were women. However, only 8% held the role of board chair or CEO (European Institute of Gender Equality, 2021). These observations raise the question of how board director appointment dynamics contribute to these outcomes.

Besides education, work experience, and qualification in certain areas of expertise,Footnote 2 other supply-side factors such as differences in career interruptions (Bertrand et al., 2010) and preferences for competition (Maggian et al., 2020; Niederle & Vesterlund, 2007) have been discussed as drivers of the under-representation of women on corporate boards. At the same time, institutional barriers and demand-side factors—including unconscious and conscious discriminatory and stereotypical biases—contribute to a “glass ceiling” blocking women’s upward mobility (Bertrand et al., 2019; Bjerk, 2008; Field et al., 2020). Women often need stronger leadership competence signals (Finseraas et al., 2016) and have less elite networks (Michelman et al., 2022; Zimmerman, 2019).

In this paper, we focus on demand-side drivers and impediments of gender diversity in the boardroom. We derive hypotheses from organizational and group-level theories and empirically investigate how ex-ante voluntary and mandatory gender composition of the board and the gender of any departing board member influence appointment decisions of executive and non-executive women directors. Explicit and implicit norms can increase the attention on gender and lead to t(w)okenism (Chang et al., 2019; Kanter, 1977, 1987) and an early saturation of board gender diversity. On the other hand, according to homophily theory (Pfeffer & Salancik, 1978), groups tend to pick new members in line with their own profile. With an increasing representation of women (exposure), especially after reaching a certain threshold (critical mass), the degree of the minority’s influence on group decisions and outcomes will grow (Broome et al., 2011; Konrad et al., 2008) and favor women appointments. Finally, the status quo bias (Kahneman et al., 1991) suggests that if appointments are not to disrupt internal dynamics, they could follow a gender-matching heuristic (Tinsley et al., 2017), where women are only appointed to replace departing women. These theoretical considerations suggest that ex-ante board structures and dynamics affect appointments. As directors have different roles, these structures and dynamics could vary between executive and non-executives. Executives are the highest c-level managers while non-executives are responsible for advising, monitoring, appointing, and remunerating executive directors.

Our analyses contribute to research on corporate governance, particularly to work that draws attention to the determinants of board diversity. Previous research draws from institutional, resource-dependency, and group-level theories to explain drivers of board size, independence, multi-directorships, and diversity. While external environmental (Arena et al., 2015; Brammer et al., 2009; Grosvold & Brammer, 2011; Tyrowicz et al., 2020) and internal firm-specific factors, such as firm size, network linkages, strategic orientation, and performance, have been examined (Barrios et al., 2022; Gregorič et al., 2017; Hillman et al., 2007; Markoczy et al., 2020; Withers et al., 2012), the evidence on ex-ante board composition and dynamics driving women appointments is limited.

This study extends single-country studies by Farrell and Hersch (2005) on firms in the 1990s in the United States, Gregory-Smith et al. (2014) during the late 1990s and the 2000s in the UK, and Smith and Parrotta (2018) during the 2000s in Denmark. They find that the likelihood of adding a woman to the board in a given year negatively depends on the number of women already on the board. Further, they show that the probability of appointing a woman is higher when a woman director departs the board. With our European cross-country focus, we observe heterogeneous institutional contexts, different types of board structures, and pay explicit attention to the representation of women via quotas.

Finally, we add to Matsa and Miller (2011) and Bozhinov et al. (2021) and their analyses of diversity spillover effects in the US and Germany by explicitly differentiating between non-executive and executive roles of board members and their appointment dynamics. As non-executive directors are responsible for appointing executive directors, the dynamics we expect inside the board could also spill over from non-executive to executive directors.

Our analyses build on data comprising executive and non-executive director appointments in 3353 listed European firms between 2002 and 2019. We first provide descriptive evidence on board composition for mandatory quota and non-quota implementing countries. Next, we illustrate director appointment dynamics over time, where we observe important differences between non-executive and executive roles. Whereas women have been increasingly appointed to non-executive roles as of 2010, the share of women in executive roles has been rather constant at low levels over time.

We account for country, firm, and board characteristics and find that women are more likely to be appointed to non-executive than executive roles. Second, we find that the appointment likelihood for women declines the more women are already on the board. Thus, we find evidence of early board diversity saturation effects. Third, we show that the likelihood of a woman being appointed is significantly larger when a woman leaves, compared to when a man leaves the board. Combined, these findings could reflect t(w)okenism, where efforts to increase the representation of women on the board are made to reach or maintain a specific threshold below gender balance. Yet, these efforts do not allow an equal opportunity of appointment to all director positions, especially to important executive positions (Chang et al., 2019; Gregory-Smith et al., 2014). Finally, we do not find evidence for spillover effects regarding the impact of gender diversity among non-executive directors on executive women appointments.

These results are robust to addressing potential endogeneity issues of the initial board composition using econometric matching techniques (Imbens, 2004) and a heteroscedasticity-based instrumental variable approach (Lewbel, 2012). The findings are also robust to dynamic model specifications, alternative measures of women director participation and appointments, and different control variables. In additional analyses, we examine potential differences between firms in countries with and without mandatory quotas, countries with different levels of female labor force participation, and firms operating in men- versus women-dominated industries. We find stronger evidence for gender-specific appointment dynamics before reaching gender balance in environments with increased external demand for and decreased supply of women director candidates.

Our findings have important implications for the debate on increasing board diversity and the roles women take on corporate boards. While the data provide evidence that the share of women on European boards has been increasing over time, they also show that new appointments are mostly to non-executive roles and that demand for diversity quickly saturates with higher existing diversity. Moreover, the appointment dynamics show that public pressure and mandated quotas trigger gender-specific appointments without reaching gender balance. We do not find robust evidence in favor of exposure or critical-mass effects. While quotas may be an appropriate instrument to increase diversity, two important aspects need to be considered. First, supply might be a constraining factor if the institutional environment disadvantages women, for example, by limiting the extent to which women can combine family and job responsibilities, with discrimination at earlier career stages, and systemic gender bias. Second, board quotas do not lead to executive position spillovers if these positions are not specifically targeted. Social policy reforms and trainings that address career interruptions and unconscious biases may be more effective than mandatory quotas in increasing the representation of women in corporate leadership roles.

The Role of Gender in Board Appointment Dynamics

Growing empirical literature provides evidence that the composition and structure of boards of directors are relevant for the governance and performance of firms. Studies have focused on explaining the influence of women directors on corporate behavior and outcomes (e.g., Adams & Funk, 2012; Ahern & Dittmar, 2012; Carbonero et al. 2021; Green & Homroy, 2018; Torchia et al. 2011; Wahid, 2019). It is often argued that the appointment of women directors enhances human and social capital in the boardroom because a wider and more diverse talent pool regarding knowledge and experience can be exploited (Adams & Ferreira, 2009; Kim & Starks, 2016; Terjesen et al., 2009). However, studies also hint at challenges related to diversity in the boardroom. Relations-oriented diversity in terms of age, gender, and ethnicity can result in conflict, subgroup formation, or an inter-group bias (Hewstone et al., 2002; Talke et al., 2010; Williams & O’Reilly, 1998) and hence negatively affect firm performance.

Yet, we still know little about the drivers and impediments of attaining diversity in the boardroom. Following the supply logic, directors can and will be appointed from a pool of qualified candidates, regardless of their gender. Even if gender disparity could be explained by factors leading to a smaller pool of qualified women compared to men, the process of director appointment would not be gender specific. In this case, the gender of an appointed director should be independent from the initial board composition or the gender of a departing board member. However, corporate governance research shows that the supply of suitable candidates cannot fully explain the dynamics of the observed appointment bias (Adams & Kirchmaier, 2013). During the last decades, more women entered the lower and middle management levels and thereby increased the pool of qualified candidates for the board. This is in line with the findings by Singh et al. (2008) who show that newly appointed women directors in the UK, although slightly younger than their male counterparts, have at least equal qualifications.

Recent studies, therefore, focus on demand-based factors of appointments. Demand for women directors can either be advanced or inhibited by external environmental and internal firm-specific factors. Institutional and cultural norms can foster unconscious or conscious biases forming a “glass ceiling” as a barrier to women’s career advancement. Different types of discrimination, statistical, taste-based, and implicit, can hinder women’s appointment to leadership positions (Bjerk, 2008; Gabaldon et al., 2016). There exists empirical evidence speaking to this argument. Selection procedures for men and women seem to differ in the sense that women need stronger signals and more often additional skills in terms of education, reputation, competence, and board and career experience than men to be appointed or promoted (Finseraas et al., 2016; Guo et al., 2020; Spence, 1973). Further, research highlights that board directors are traditionally recruited from a limited pool of socially connected candidates. As a result, dense networks of multiple directorships can be observed (Adams & Ferreira, 2009; Fracassi & Tate, 2012). These traditionally male-dominated networks may hinder women to enter top-management positions (McDonald & Westphal, 2013; Michelman et al., 2022; Zimmerman, 2019).

Public opinion, regulatory and reputational pressure, as well as shareholder activism can create positive external demand for diversity in board composition (Brammer et al., 2009; Gormley et al., 2021; Green & Homroy, 2018; Tyrowicz et al., 2020). Especially larger firms that are more in the public eye are often more reactive to diversity demand (Agrawal & Knoeber, 2001; Carter et al., 2003; Hillman et al., 2007). Moreover, social norms for diversity can originate inside organizations and professional groups (Brammer et al., 2007; Mateos de Cabo et al., 2012; Mawdsley et al., 2022), but are typically influenced by external factors such as implicit industry standards or explicit quotas (Arena et al., 2015; Chang et al., 2019). The pressure for gender diversity from different stakeholders through explicit and implicit norms can make gender more salient in appointment processes (Knippen et al., 2019). Since gender is only one dimension of diversity, demand for additional women may evaporate once women have some representation. Farrell and Hersch (2005), Gregory-Smith et al. (2014), and Smith and Parrotta (2018) empirically show that in the 1990 and 2000s, when demand for women leaders was still relatively low, women were more likely to be appointed to a board with lower ex-ante representation. More recently, Bonet et al. (2020) find that in some leadership settings, women have an advantage of being appointed as long as there is no or only one other executive woman. This evidence suggests that external pressure creates demand for diversity that is saturated before reaching gender balance.

Board appointments consistent with these demand-side arguments may result in the addition of a few women only when the ex-ante board representation of women is low. This gender-specific appointment pattern might be stronger when public attention to gender issues and external pressure to appoint women according to a social norm is higher. Based on these considerations, we hypothesize the following.

Hypothesis 1a (Saturation)

The probability of appointing a woman as director decreases with higher ex-ante female representation.

While outside pressure, combined with discriminatory biases, suggests an early saturation effect of the presence of women board members on new appointments, the exposure argument suggests that the appointment of an additional woman is more likely the larger the representation of women currently on the board. Exposure to women directors may lead to men updating their beliefs about the suitability of women leaders and act as signaling to potential women candidates (Carrell et al., 2015; Finseraas et al., 2016; Porter & Serra, 2020). Gangadharan et al. (2016) argue that women who attained leadership positions through quotas face male rejection which is only mitigated by higher exposure to women leaders. More generally, Guiso and Rustichini (2018) find that the participation of women in management is higher in countries with more pronounced emancipation of women.

Beyond pure exposure, critical-mass theory predicts that when a certain threshold is reached, the degree of the minority’s influence grows (Konrad et al., 2008). The concept of critical mass hence implies that relative representation matters for the dynamics of heterogeneous groups (Kanter, 1977, 1987). Once a certain minority reaches a critical mass, members can form coalitions and affect group decisions and outcomes. Previous research found some support for the critical-mass theory on different types of board- and firm-level outcomes (Joecks et al., 2013; Konrad et al., 2008; Torchia et al., 2011). Yet, we know little about its effect on the dynamics of board director appointments. Research suggests that groups show a tendency to select new group members who resemble the existing group, labeling this tendency “homophily” (Pfeffer & Salancik, 1978) or inter-group bias (Hewstone et al., 2002). These patterns create barriers for out-group members and appear to also occur on corporate boards (Gabaldon et al., 2016; McDonald & Westphal, 2013; Westphal & Stern, 2007; Zhu & Westphal, 2014). If women reach a critical mass of board representation, they could influence appointment decisions towards candidates that resemble them, e.g., with respect to gender.

If the above arguments hold, we expect that ex-ante gender diversity should have a positive impact on future diversity and that the growing influence of women when attaining a critical mass additionally favors the appointment of women directors.

Hypothesis 1b (Exposure)

The probability of appointing a woman as director increases with higher ex-ante female representation.

In principle, this suggests that once women achieve higher shares on corporate boards, inter-group biases may also result in an over-representation, i.e., holding more than 50% of board positions. However, it is unclear whether such dynamics would materialize given that once gender parity is achieved, other norms and mechanisms may unfold. Hence, these arguments apply to settings with zero to full gender diversity, where the latter relates to a gender-balanced board with 40–60% women.

The variation of diversity inside the board room affects internal group dynamics and may have consequences beyond saturation and exposure. Empirical evidence finds that individuals are more motivated by threats of loss than by opportunities for gain from change, which is a strong driver of preferences for the status quo (Kahneman et al., 1991). This ’status quo’ bias can also apply to the boardroom setting (Gregory-Smith et al., 2014). Tinsley et al. (2017) find that exits of women directors increase the probability of women re-appointments. They label this phenomenon “gender-matching heuristic.” Such a heuristic implies that boards may aim to maintain a certain share of women, consistent with the respective norm without disrupting existing internal dynamics.

In line with this idea, we argue that the gender of the departing director plays a role in the new appointment of women.

Hypothesis 2 (Replacement)

The probability of appointing a woman as director is higher in the case of the departure of a woman compared to no departure or the departure of a man.

We expect the replacement effect to be higher with increased demand through external pressure and with a lower supply of women director candidates through their participation in the workforce.

Even though most diversity reforms address non-executive and executive board roles combined, women tend to be appointed to non-executive positions, which are typically less influential (European Women on Boards, 2021) and receive lower financial compensations (Rebérioux & Roudaut, 2019). This suggests that explicit norms such as legally mandated gender quotas may have unintended consequences, where women are less likely to be appointed into major board roles (Hwang et al., 2018; Knippen et al., 2019). For example, Foss et al. (2022) show that while generally, a higher share of women in management positions is related to greater innovativeness of firms, this link is weaker in the presence of legally mandated gender quotas. Such patterns suggest that women are primarily appointed as “tokens” to signal compliance with implicit or explicit norms, e.g., when mandatory quotas are in effect or a firm is particularly distant from diversity norms. Tokens act as representatives of their category, but have limited influence on corporate decisions (Kanter, 1977). Recently, the twokenism norm has replaced tokenism in many firms and industries, where having exactly two women on the board is very common in US firms (Chang et al., 2019). Gregory-Smith et al. (2014) find that in the UK, non-executive appointments are gender specific while executive appointments are not. These observations stress the importance of distinguishing between appointment dynamics for executive and non-executive roles.

We hypothesize that if appointments occur to conform to norms without influencing major decision-making processes, women could be predominantly appointed to non-executive positions. Again, this pattern is likely stronger in settings where the norm is more explicit.

Hypothesis 3 (Role-Specificity)

Gender-specific appointment dynamics are more prevalent for non-executive than executive directors.

Finally, we take into account that non-executive directors are typically responsible for appointing executive directors (Bozhinov et al., 2021; Matsa & Miller, 2011). The empirical evidence on whether “women help women” is mixed. While Derks et al. (2016) argue that because of the queen-bee effect women tend not to support or even undermine women subordinates, others suggest that female leaders help other women advance in the firm, leading to gender-diverse spillovers on lower hierarchical levels (Cohen et al., 1998; Kleinbaum et al., 2013; Kunze & Miller, 2017). These women and their direct environment are less likely to view other women through the lens of traditional gender stereotypes (Clark et al., 2021; Stainback et al., 2011) and they enforce female-friendly policies and organizational cultures (Gagliarducci & Paserman, 2015; Tate & Yang, 2015). Matsa and Miller (2011) and Bozhinov et al. (2021) find compelling evidence for spillover effects from the non-executive to the executive board in line with the latter argument.

Following this reasoning, we hypothesize that a growing influence of non-executive women in appointment decisions through higher representation, especially after reaching a critical mass, will have a positive impact on executive women’s appointments.

Hypothesis 4 (Spillover)

The probability of appointing a woman as executive director increases with higher ex-ante representation of non-executive women directors.

Institutional Framework, Data, and Method

Institutional Framework

Existing studies on gender diversity frequently rely on national data. Due to an increasingly international market for top managers, we base our empirical investigation on a sample of Western European firms. This approach allows us to exploit cross-firm and cross-country variation and consider institutional and legal differences between countries when examining appointment dynamics of executive and non-executive roles.

In Europe, an essential distinction can be made between monistic one-tiered (Anglo-Saxon) structures and dualistic two-tiered boards traditionally predominant in continental Europe. Some European countries allow both ‘one-tier’ and ‘two-tier’ board structures. The majority of French and Spanish firms, for instance, have voluntarily implemented one-tier board structures. Countries such as Austria or Germany have mandatory two-tier board structures (Gelter & Siems, 2021; OECD, 2012). While two-tiered boards prescribe a strict separation of executive and non-executive directors, one-tiered systems combine executive and non-executive directors on a unitary board, sometimes including a dual CEO–Chairman. Recently, several European countries have implemented voluntary and mandatory quotas for women directors. Depending on the board structure, these apply either to all board directors or only non-executive directors. We account for the countries’ varying institutional and legal settings and distinguish between director roles.

Empirical literature argues that board roles and their responsibilities are similar in both two-tiered and one-tiered boards and that structures and processes in Europe converge due to governance codes (Davies & Hopt, 2013; Fauver & Fuerst, 2006). The main tasks of members of dualistic executive boards and executive directors on one-tiered boards include day-to-day operations of a company. Members of dualistic supervisory boards and non-executive directors on one-tiered boards are responsible for advising, monitoring, and decisions about the remuneration and appointment of executive directors. While executive directors perform their tasks as a full-time job, non-executive directors often have multiple mandates, multi-directorships. The type and intensity of cooperation between executive and non-executive directors in the boardroom depend on the respective structure of the board. Due to the strict separation of management and control, non-executive directors on two-tiered boards are typically more independent but information asymmetries between executive and non-executive directors are more pronounced compared to one-tiered boards (Adams & Ferreira, 2007).

Generally, in dualistic systems, the shareholder representatives elect the members of the supervisory board at the annual general meeting, while the latter appoints the members of the executive board. Nomination committees are supposed to ensure the participation of supervisory boards in the appointment and removal process of executive directors by identifying and recommending potential candidates (European Commission, 2005). In monistic systems, the shareholders appoint all directors at the annual general meeting. The CEO of a company takes an outstanding position in the boardroom (particularly in the case of CEO–chairman duality) and may influence executive appointments (Shivdasani & Yermack, 1999).

As a consequence, in a multi-country setting, it is important to classify individual board members according to the role they take. We therefore carefully categorize directors by differentiating between non-executive and executives according to their role and position descriptions as listed in the ORBIS database. We draw this distinction by applying a role-based categorization which takes into account that board structures differ between European countries. Members of the two-tier supervisory board and one-tier directors with non-executive roles are considered non-executive directors. In our analyses, we call them supervisory directors. We categorize members of the two-tier executive board and one-tier directors with executive roles as executive directors.

Data and Sample

Our empirical analysis is based on combined data from several sources. We obtain detailed information on board members and firm ownership from the ORBIS database provided by Bureau van Dijk. Financial information stems from Worldscope provided by Refinitiv. Our main sample includes 27,486 firm-year observations from 3353 listed firms observed during the period 2002 to 2019 in 17 European countries. In line with previous studies, we exclude utilities and financial firms with two-digit SIC codes 49 and 60–69 (Adams et al., 2018). We follow Kim and Starks (2016) and restrict our attention to firm-year observations, where the director appointment and departure dates are available for a particular firm.Footnote 3 In order to correctly capture board composition, we include only firm-year observations where data for at least two directors are available.Footnote 4

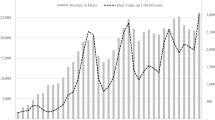

Figure 1 shows the development of women director representation in the different countries included in our main sample. The figure illustrates that, on average, the share of women on the board of directors has been increasing in the past two decades both in countries with (Norway, Italy, France, Belgium, Germany, Austria, and Portugal) and without mandatory quotas (Switzerland, Denmark, Spain, Finland, UK, Greece, Ireland, Luxembourg, Netherlands, and Sweden).

Share of Women on Boards (country averages). This figure reports the average time trend of the share women in each country’s board of directors. “Other” countries have low number of observations and include Portugal and Greece. Between 2002 and 2019, seven countries implemented mandatory quotas for a minimal share of the underrepresented gender on corporate boards. These include Norway, Italy, France, Belgium, Germany, Austria, and Portugal

Definition of Variables

Our main variable of interest is an indicator for the appointment of at least one non-executive or executive woman in a given year. In additional analyses, we replace this main dependent flow variable with the number of appointed women and the difference (delta) between the share of women in a given year and the year before.

Figure 2, Chart (a) shows that on average, 0.05 female supervisory directors were appointed in the year 2002. This number increased to 0.35 in the year 2019. We also observe that the number of women appointments to executive positions slightly increases over time in Chart (b), but remains at a substantially lower level. Similar findings appear for the total share of women directors: Chart (c) shows that the fraction of female supervisory directors increased from 5 percent in the year 2002 to more than 25 percent in 2019. The fraction of female executive directors increased from 5 to 11 percent in the same period (Chart (d)). In our sample, the representation of women on supervisory boards increases at an accelerating rate, from a 0.5 percentage point increase per year in 2003 to 1.5 percentage points by 2019 (Chart (e)). In contrast, Chart (f) depicts a constant increase in the representation of women on executive boards. Each year, the share of women increases by roughly 0.4 percentage points.

Appointments and share of women directors (over time)

We follow Farrell and Hersch (2005) and use the lagged share of women directors as the main predictor variable. Furthermore, we generate two indicator variables for men and women director exits in the given year. Exits include all reasons for director departure. We calculate lagged board size and test the influence of and robustness to the inclusion of other 1 year lagged board-level variables in additional specifications, such as the share of independent, foreign, and multi-directors. Multi-directors represent those directors that hold at least one additional board position in an external company. Further, we account for average director age and tenure, as well as a binary variable indicating whether the CEO or chairperson is a woman.

Table 1 presents descriptive statistics of our main variables reflecting the dynamics of executive and non-executive director appointments. All non-executive directors are included in the supervisory board observations of our sample, all executive directors are included in the executive board observations. As we have less data on executive directors for the key variables, the executive board sample only counts 20,672 instead of 27,486 firm-year observations. Table 7 in the Appendix provides the variable definitions and their respective data origins.

In all specifications, we include firm age and the logarithm of total assets to control for maturity and firm size. The average age of the firms in our sample is 16.8 years with a maximum of 54 years. This low number is partly due to changes in legal structure resulting in updated firm identifiers. Our sample’s median values for firm size amount to 201 million euros in total assets and 1050 employees. Approximately one-third of our sample’s firms are considered small and medium enterprises (SMEs), which have fewer than 250 employees and fewer than 50 million euros in annual turnover or 43 million euros in total assets (European Union, 2003). Further, Tobin’s Q captures the expected influence of market-based firm performance on the likelihood of new women appointments. Tobin’s Q amounts to an average of 2.6 per year over the entire period 2002 to 2019. Additionally, a dummy variable based on ownership data provided by Bureau van Dijk controls for potential ownership concentration. In line with the literature, this block indicator takes the value of 1 if one or more shareholders with a fraction of at least 25 percent of the capital stock are identified (Czarnitzki & Kraft, 2009). GDP per capita, total employment rate, and women’s participation in the labor force are included to control for country-specific time-variant labor market factors.

Empirical Methodology

We examine the specific factors that predict women director appointments according to our hypotheses in a multivariate regression framework. The probabilities (P) of appointing a woman as supervisory and executive director are estimated from linear probability models for firm i = 1,..., N at time period t = 1,..., T:

The set of Predictors includes the lagged share of female (non-)executive directors. To account for a possible non-linear relationship between the previous year’s proportion of women directors and the likelihood of a current female director appointment, we add the squared term of this share. Following empirical evidence for a critical-mass effect and social norms (twokenism) for a specific number of a minority group’s representation, we replace the lagged share of female (non-)executive directors with the lagged number of female (non-)executive directors in additional specifications. For executive appointments, we follow Matsa and Miller (2011) by taking into account both the lagged share of female non-executive and executive directors. Further, we include dummy variables indicating female and male (non-)executive exits from the board. The exit and appointment variables are from the same year, as they are often decided at the shareholders’ meeting in the first half of the fiscal year, based on the previous year’s annual report. \(\textbf{X}_{it}\) is the vector of lagged board-, firm-, and country-specific controls. Finally, we include year fixed effects (\(\lambda _t\)) to capture aggregate time trends and fluctuations and firm-fixed effects to absorb the time-invariant unobserved heterogeneity \(c_i\) between firms. This heterogeneity could represent differences in firm culture, strategic orientation, or location. We draw statistical inferences based on firm-clustered standard errors robust to heteroscedasticity and autocorrelation.

Due to the binary nature of our dependent variable, women appointment, the linear probability model can only approximate probabilities. However, the coefficients of interest can still give reasonable estimates of average partial effects (Wooldridge, 2010). We estimate the linear probability models with OLS. For robustness, we report the results of logit and poisson model estimations in the Appendix.

Empirical Analysis

The first set of results describes the dynamics and predictors of supervisory director appointments and we subsequently discuss the results for appointments as executive directors. We start with presenting correlations before we account for the potential endogeneity of key variables in the model.

Analysis of Supervisory Director Appointments

Table 2 reports the main results for the probability of appointing women to the supervisory board. The coefficients estimate average partial effects on the linear approximation of these probabilities. All specifications include firm- and country-specific time-variant control variables and year- and firm-fixed effects. The average marginal effect from Specification (1) reports that, on average, the probability of appointing a female supervisory director decreases by 0.7 percentage points if the previous year’s share of female supervisory directors increases by 1 percentage point, ceteris paribus. This average marginal effect takes into account the significant first- and second-order term of the share of women variable. The demand for women directors is increasingly saturated up to a certain point.

We visualize the non-linear relationship between share women on the board and the probability of appointing at least one woman in Fig. 3. The figure shows the margins of Specification (1), i.e., the predicted appointment probabilities of women from the linear approximation at different thresholds of lagged share women, holding all other predictors constant at their mean. Margins decline steeply with increasing female representation up to 50% in line with the saturation hypothesis. Once, gender balance is reached, the relationship becomes flat at very low appointment probabilities. Less than 5% of our sample’s observations are at this end of the share distribution, which makes interpreting the range beyond gender balance difficult. Attaining a critical mass of 30% does not lead to a higher appointment likelihood for women. This finding is in line with our saturation Hypothesis 1a and contradicts the exposure and critical mass Hypothesis 1b.

Relationship between share women and women’s appointment probability to the supervisory board (margins)

Further, in Specification (1) we see that the appointment probability of women increases by 27.4 percentage points when a woman leaves the supervisory board in the same year, compared to only 8.6 percentage points when a man leaves the board. The probability increase of appointing at least one woman is three times higher when a woman compared to when a man leaves the board. A t-test confirms their statistically significant difference at a 1% level in line with our replacement Hypothesis 2. This result suggests that firms follow a gender-matching heuristic, in line with the status quo bias (Gregory-Smith et al., 2014; Tinsley et al., 2017). The declining probability of women appointments with higher initial shares, i.e., the saturation effect, combined with the higher replacement likelihood when a woman leaves, show that supervisory director appointments are gender specific. Firms take into account gender as a characteristic to appoint new directors and may pursue the (unstated) goal to not move backwards in their level of gender diversity as a response to outside pressure.

The size of the board also plays a role. Inside a firm, periods with larger boards are characterized by a lower probability of appointing a female supervisory director. Firm size measured by total assets and firm performance, measured by Tobin’s Q, is not significantly related to the likelihood of new female supervisory directors when controlling for firm-fixed effects. Finally, a country’s higher women labor force participation is associated with a higher appointment probability.

These insights are robust to including the dependence indicator in Specification (2), which does not significantly affect the appointment probability. The dependence indicator equals one if ownership is concentrated, i.e., if at least one shareholder holds 25% or a higher fraction of the shares. With our firm-fixed effects, we already control for time-invariant firm heterogeneity. Ownership concentration does change over time, but often not substantially. Specification (3) includes additional board characteristics. Due to missing values, the sample size is restricted to 9247 observations. Even for this subsample, we find the same patterns. The previously found saturation effect is more pronounced in this subsample and when controlling for additional board-level characteristics. Having a woman as chair of the supervisory board increases the appointment probability by 19.6 percentage points, on average. This effect is in line with the prevalent empirical evidence of women leaders helping other women, leading to spillovers to lower hierarchical levels. Moreover, the share of directors that serve on other boards, multi-directors, is positively associated with women’s appointment probability.

In Specification (4), we replace the share women with an integer indicating the number of women directors. Our results remain unchanged. With each additional woman already on the board, the probability of appointing a new female supervisory director decreases by 5.9 percentage points, on average. We visualize the effects of the number of women on the appointment probability in Fig. 4, where we additionally consider an interaction between the number of women on the supervisory board and our director exit indicators. We report the corresponding specifications in Appendix Table 8. In Fig. 4b, we show that the replacement effect outweighs the average saturation effect if the board has two or fewer female supervisory directors. The likelihood of appointing a new female supervisory director increases with each additional woman on the board if one woman leaves and no more than two women are already on the board. Whether someone or no one leaves the board, the appointment probability does not increase if the number of women already on the board reaches a critical mass. We find no significant positive effect on the appointment probability of women when there are at least three women already on the board in Fig. 4. These findings are in line with twokenism, where adding two women to the board conceptually signals compliance with current norms.

Relationship between number of women and women’s appointment probability to the supervisory board (margins)

Heterogeneity in Supervisory Director Appointments

To better understand possible country and industry heterogeneity in our main findings, we perform several additional analyses. We investigate three dimensions: industries’ average board gender diversity, countries’ level of female labor force participation, and countries’ mandatory quota legislation. Firms operating in industries with relatively high shares of women directors are likely characterized by different appointment procedures than firms in industries with comparatively low board gender diversity. We define an industry to be diverse if it has an above-median share (i.e., more than 12% in our sample) of women in board positions. In a more diverse industry, there is likely both higher supply and higher demand for female directors. To disentangle supply and demand heterogeneity, we include two additional dimensions. We argue that high female labor force participation increases the supply of suitable women director candidates. Mandatory quotas reflect increased public attention to gender diversity, external pressure to achieve it, and salience of social diversity norms and increase the demand for women directors up to a certain threshold. Therefore, we expect saturation and replacement effects to be more pronounced in environments with increased external demand for and decreased supply of women candidates.

Table 3 presents the results. We find no substantial differences between “female- and male-dominated” industries in Specifications (1) and (2). The saturation effect is slightly higher in industries with higher share of women on the boards of directors. The replacement effect, i.e., the difference in appointment probability between when a woman, compared to when a man leaves the board, is similar. In countries with low female labor force participation, we see stronger saturation and replacement effects. Thus, our previous results are stronger in settings with lower supply of women candidates.

Consistent with our expectations, we find that in quota country observations with increased demand for women directors, the saturation effect is stronger (Specification (6)). It should be noted, however, that the average probability for appointing at least one woman is overall higher in the presence of binding quotas. The re-appointment effect is also stronger in quota observations for both women and men leaving the supervisory board. The difference between the two coefficients remains similar in both subsamples. Combined, our cross-sectional results show that gender-specific appointments are more pronounced in environments with increased external demand for and decreased supply of women candidates.

Robustness Tests and Sensitivity Analyses of Supervisory Director Appointments

The inferences we draw from our main analysis rely on the assumption of exogenous predictors. Yet, our variables of interest, in particular, the dummy for departing directors and the share of women on the board could be considered endogenous. In order to address this concern, we tackle potential endogeneity issues arising from confounding observable and unobservables factors influencing the predictors of interest as well as the appointment probability.

First, we rerun our main analysis on subsamples including at least one director appointment in each firm-year observation in Specification (1) of Table 4 and at least one director departure (Specification (2)). A director appointment is not necessarily a reaction to a departure and therefore, the two subsamples and their dynamics might differ. In these specifications, we aim to reduce unobserved time-variant heterogeneity between firms resulting in particular appointment patterns. The share women coefficients are larger than in our main specification because the average appointment probabilities are higher in both subsamples. The average probability for appointing at least one woman in our main sample is 14%, while the appointment and exit subsample probabilities are 34% and 21%, respectively. In Specifications (1) and (2), we find that a 1 percentage point increase in the share women on the supervisory board results in a 1.3 and 1.2 percentage points decrease (average marginal effects) in the appointment probability for women. In both specifications, women’s appointment probability is significantly larger when women rather than men exit the board. In Specification (2), men’s exit is the baseline category and we compare women’s exit coefficient with 0. The saturation and replacement effects are prominent in both subsamples. There is no evidence for an exposure or critical-mass effect.

In Specification (3) of Table 4, we estimate a dynamic model and include lagged values of women appointments to the supervisory board as auto-regressive terms to control for persistence in the dependent variable (Matsa & Miller, 2011). These auto-regressive terms show that the appointment of a woman in previous years is associated to a lower appointment probability in the subsequent year. The lagged appointments pick up some of the previously captured saturation dynamics, but our results remain robust to those from the main specification in Table 2. The appointment probability is almost three times bigger when a woman leaves compared to when a male board member leaves.

Next, we follow Nekhili et al. (2020) and employ a matching technique to account for observable differences between firms with varying initial representations of women on their boards. The goal of this approach is to achieve better comparability between firms with and without women on the board. Since a relatively large share of firms has no or only one woman, we distinguish between firms with (group 1) and without any women (group 0) on the board in the first half of our sample period when external pressure was still considerably lower. That is, we only compare firms that have had at least one female director before the year 2010 to those firms without a female director, but that are otherwise very similar. The idea of the 2010 cut-off is that there was an increased external demand for women directors throughout Europe afterward.

We use Mahalanobis distance-based nearest-neighbor matching to find the most similar firms in both groups (Imbens, 2004). Distance matching allows finding the closest neighbor(s) of a particular observation within a radius in terms of the applied characteristics (industry, country, firm age and size, Tobin’s Q, and board size) to all other observations in the sample. Each observation from group 0 obtains a weight after the matching. The weights balance the distribution of the characteristics of group 0 according to the distribution of those in group 1, i.e., a t test of differences in means is insignificant for all included measures. The weight of a group 1 observation is always equal to one, while the sum of the weights of its counterfactuals also adds up to 1 (Doherr, 2021). The weights are then used for the subsequent estimation of Specification (4) in Table 4. Previous conclusions regarding the negative link between the ex-ante share of women and the likelihood of a woman being appointed to the supervisory board hold. However, the saturation effects disappears after 30% of women representation, instead of 50% as in our main specification in Table 2. This result by itself points to critical-mass effects, but is not robust to alternative specifications. The replacement effect is still present and statistically significant.

Finally, we address remaining endogeneity concerns by generating instrumental variables for our main predictors. We follow the approach proposed by Lewbel (2012) who develop a method of a two-stage least squares regression without the need for an external instrumental variable. Finding appropriate instrumental variables which satisfy all formal requirements is often difficult in settings like ours. In Lewbel’s method, identification is achieved by including regressors from within the data that are uncorrelated with the product of heteroscedastic errors.Footnote 5 One pre-condition is that the first-stage errors are indeed heteroscedastic. In our case, this is fulfilled for all our endogenous variables, i.e., the shares and exit dummies. We do not over-identify our model and have as many generated exogenous instruments as endogenous predictors. We perform a test for the presence of weak instruments proposed by Stock and Yogo (2005) and find the Kleibergen–Paap Wald F-statistic of 56.9 above the rule-of-thumb critical values. Therefore, we can reject concerns for weak instruments. The results from this heteroscedasticity-based instrumental variable approach (Specification (5) of Table 4) are in line with our main and alternative specifications. We observe a negative significant effect of the share of women on the appointment probability of at least one female supervisory director and a statistically significantly higher appointment probability if a woman leaves, compared to when a man leaves the board.

Analysis of Executive Director Appointments

The descriptive evidence in Fig. 2 suggests differences in appointment dynamics between supervisory and executive boards. Therefore, we analyze the appointments of female directors to executive positions. We rerun previous models with non-executive and executive predictors on women appointment probabilities to the executive board. The estimation results in Table 5 show similar but weaker negative relationships between the lagged share of executive women directors and the probability of appointing at least one new female executive director. In Specification (1) of Table 5, we find that a 1 percentage point increase in the share women on the executive board results in an, on average, 0.5 percentage points decrease in the appointment probability for women. Again, this average marginal effect takes into account the significant first- and second-order terms of the share of women variable. The first-order term is significantly negative and the second-order term is significantly positive, but smaller.

We illustrate the non-linear dynamics from Specification (1) in Fig. 5. The demand for women directors is increasingly saturated for low shares of women and becomes flat above 40% of women on the executive board. The negative relationship between female executive representation and appointment is statistically significant at low shares of female executives. Once gender balance is reached, the dynamics point to an exposure effect. However, the appointment probability does not yet increase after attaining a critical mass of 30%. Note that a share of 30% of women corresponds to the 90th percentile in our sample.

Relationship between share women and women’s appointment probability to the executive board (margins)

Testing the conjecture of possible spillover effects, we further investigate the influence of ex-ante gender diversity among the non-executive directors who are generally involved in hiring the executives of a firm. For this purpose, we include the share of women in the supervisory board as an additional predictor in all specifications. We find no consistent empirical indications of a positive or negative relationship between the presence of female supervisory directors and the promotion of women as executive directors. The share of women on the supervisory board does not seem to influence the executive women director appointment probability, contradicting our spillover Hypothesis 4.

With regard to possible replacement effects, we see in Specification (1) that the increase in appointment probabilities for the cases when a man or woman leaves the executive board is smaller than for non-executive appointments. However, the increase for when a woman leaves the executive board is still approximately three times higher than when a man leaves the board. Therefore, we also confirm our replacement hypothesis for executive appointments. Interestingly, we find a positive relationship between board size and the probability of appointing a woman to the executive board.

Our results hold when additionally controlling for a firm-year-specific dependence indicator in Specification (2) and become stronger when controlling for further board-specific indicators in Specification (3) of Table 5. In Specification (3), we find that the share women in the supervisory board negatively affects the appointment probability for executive women. This result is not robust to alternative specifications but points to saturation, spillover, and queen-bee effects. However, we do not find evidence that chairwomen or women CEOs influence the appointment of women executive directors.

In Specification (4), we replace the share women with a categorical variable of the number of women. Our results remain unchanged. With each additional woman already on the executive board, the probability of appointing a new female executive director decreases by 4.7 percentage points. We visualize the levels of the number of women and their effect on the appointment probability in Fig. 6, where we additionally consider an interaction between the number of women on the executive board and our director exit indicators. We report the corresponding specifications in Appendix Table 10. In both subfigures, we see that the saturation effect for executive appointments disappears when a director, male or female, leaves the executive board. Finally, we observe a positive exposure effect on women’s appointment probability when the executive board has more than three women in the previous year and no man exits in Fig. 6a and no woman exits in Fig. 6b.

Relationship between number of women and women’s appointment probability to the executive board (margins)

Next, we rerun our main analysis on cross-sectional subsamples in Appendix Table 11 and perform robustness checks in Table 6. We include at least one director appointment in each firm-year observation in Specification (1) of Table 6 and at least one director exit in Specification (2). The effects we observe in Specification (1) are stronger than in our main specification. A 1 percentage point increase in the share of executive women leads to an, on average, decrease of 1.4 percentage points in the probability of appointing at least one female executive director. Again, the average appointment probabilities are higher in both subsamples. The average probability for appointing at least one woman in our main sample is 4%, while the appointment and exit subsample probabilities are 19% and 9%, respectively. We do not observe a significant replacement effect in either specification.

In Specification (3), we estimate a dynamic model and include lagged values of the dependent variable as auto-regressive terms to control for persistence in the dependent variable (Matsa & Miller, 2011). The auto-regressive terms show that the appointment of a woman in the previous years is associated to a lower appointment probability in the subsequent year. The lagged appointments pick up some of our main specification’s saturation and replacement dynamics.Footnote 6

Finally, when accounting for endogeneity in Specification (4) of Table 6, we find that the results regarding the ex-ante share of executive women are not robust. In the IV model, neither the share women in the executive nor in the supervisory board is statistically significant. These results indicate that the saturation effect from Hypothesis 1a is not as evident in the executive board as compared to the supervisory board. The replacement effect persists in our IV model and we partly validate Hypothesis 2. Finally, we confirm our third hypothesis, where supervisory director appointments are more gender specific than executive appointments. Taken together, our results suggest that demand-side factors, such as public pressure and biases, play a role in board director appointments. However, the findings also suggest that such factors can lead to t(w)okenism and that representation is often bounded to the minimum level which the explicit or implicit norm prescribes.

Conclusion and Discussion

The presence of women in top corporate boards, and hence their role in corporate decision-making, is receiving considerable attention in the public and policy debate. Yet, factors explaining the decision whether to promote women or men director candidates to the board are still understudied from both a theoretical and an empirical perspective. The question is of particular interest to policy-makers as well as companies since promoting diversity has become a political objective and attracts much attention and controversy.

The present study aims to provide novel empirical evidence on the dynamics of appointments to corporate boards. Building on a new dataset of director appointments in European listed firms in the period 2002 to 2019, our empirical findings shed light on the influence of internal board characteristics and dynamics on the appointment of new board members. We distinguish in our analyses between executive and non-executive roles arguing that there are different appointment dynamics depending on the board position to be filled. In addition, it allows us to test whether there are spillover effects from non-executive to executive directors as often argued by proponents of quotas.

We build on organizational behavior literature and research on minority and majority influence on group decision-making. Our hypotheses establish a link between ex-ante board structure and dynamics and the appointment of women to board positions. In our first hypothesis, we contrast saturation and exposure effects. Pressure to comply with explicit or implicit norms in combination with discriminatory biases can lead to a saturation of demand for diversity, whereas, according to homophily theory and updated beliefs, increased exposure to women above a critical mass increase the demand for diversity.

Our findings indeed support the former theory. The results show that the probability of a woman being appointed to a non-executive director position declines with the share of women already on the board. The appointment probability is highest when no women are present and strongly declines with each additional woman present on the board. Moreover, an appointment is significantly more likely when a woman, compared to when a man, leaves the board. Thus, gender appears to play a significant role in the appointment dynamics of non-executive directors. These patterns are more pronounced in environments—industries and countries—with increased external demand (e.g., in the presence of quotas) and a lower supply of women from the labor force.

For the appointment of executive directors, we find similar but weaker results regarding the relationship between existing diversity and new appointments. The executive appointment probability is highest when no executive women are present and declines with each additional woman until a critical mass of 30% is reached. This saturation effect is not robust to our heteroscedastic instrumental variable approach and disappears when another director leaves the board. The replacement dynamics persist in most specifications. Diversity norms seem to play a role in appointments to executive positions, however, these appointments are less gender specific and less prone to tokenism.

The dynamics of the saturation effect change with the share of women, due to the non-linear relationship between the share of women already on the board and their appointment probability. After attaining gender balance on the supervisory board or a critical mass on the executive board, the saturation effect diminishes and a further increase in the share of women no longer results in lower appointment likelihood for women. The benefits of increased gender diversity might counteract discrimination and external pressure from social norms and result in a flat relationship between gender diversity and women’s appointment probability.

Finally, we do not observe spillover effects between roles such that women non-executive directors support more appointments of women as executive directors. The existence of such spillovers has been used to support quotas for non-executive positions based on the assumption that a critical mass of women in any type of board role would support the addition of more women in top corporate jobs (Gagliarducci & Paserman, 2015; Tate & Yang, 2015). The absence of such effects in European listed companies suggests that other considerations may play a stronger role in the appointment to executive roles or that the influence of women in supervisory roles is rather limited.

A reason for weaker gender-specific effects on executive women appointments may be the still very low representation of women in such jobs and hence the lack of sufficient variation in our dependent variable. Women executive appointments, and especially women CEO appointments, are still extremely rare. The share of women among all executive directors accounts for only eight percent during our sample period. Future research may therefore investigate the question of cross-role spillovers once the number of women directors is higher. Then, a separate investigation of internal and external CEO appointments might add valuable insights (Agrawal et al., 2006; Tsoulouhas et al., 2007).

We acknowledge that our empirical investigation is based on listed firms only. It might be interesting to explore whether the findings are transferable to unlisted European firms, since our results may be specific to listed companies that are more in the spotlight of public attention. Second, future research efforts could be undertaken to systematically disentangle possible reasons for director turnover and thus, corresponding succession events. Directors who leave on friendly terms might have a say in their replacement and increase the likelihood of being replaced by candidates from their own network. Finally, with information on individual characteristics like education, professional experience, and family situation, future research could investigate supply effects and determine to what extent eligible candidates differ.

Our findings have implications for both business practice and policy-makers. While a number of voluntary recommendations for board diversity have been formulated in national and European corporate governance codices, the empirical findings clearly suggest that solely relying on labor market mechanisms does not close the gender gap on corporate boards. Further, a mandatory quota does not result in self-reinforcing dynamics with more women appointments once the quota is reached. On the contrary, the appointment probability of women declines strongly with an increasing share of women below gender balance. Quotas increase the attention on gender and seem to increase token appointments.

Our analyses show that women appointments to non-executive positions have intensified, while the fraction of women as executive directors remains until now on a very low level. Even though both type of directors have important roles and responsibilities inside a firm, non-executives have less strategic influence and often have full-time responsibilities at other firms. With more detailed data available for European companies, a systematic analysis of committee memberships among male and female non-executive directors would provide further insights into the role newly appointed directors assume and their corresponding influence on corporate decisions. As a consequence, regulations that address diversity could distinguish between different functions and roles on corporate boards. Policy-makers should consider further aspects to foster gender equality and overcome discrimination, particularly in the fields of education, family, and social policy.

Notes

A prominent gender gap still exists throughout the entire career path in the STEM fields. Data from a subset of OECD countries have indicated that not only are young women less likely to graduate in engineering and computer science, moreover among graduates with science degrees, 71% of men but only 43% of women work as professionals in physics, mathematics, and engineering (Flabbi & Tejada, 2012). In other fields, women are well-represented at early career stages and in business schools, however, very few climb the ladder to the top (Maggian et al., 2020).

Note that we check the sensitivity of our findings to relaxing this rule and find that our main results are robust to a left censored data sample, i.e., where directors with missing appointment dates are included in the sample.

Our results and the inferences we draw from them are robust to different sample specifications, such as including only observations with three directors or more, as required by law.

See Baum and Lewbel (2019) for a more detailed discussion of the method.

We do not perform nearest-neighbor matching based on whether the firm had early women presence in the executive board, because the number of these firms in the pre-2010 period is too small rendering the matching infeasible.

References

Adams, R. B., & Ferreira, D. (2007). A theory of friendly boards. The Journal of Finance, 62(1), 217–250.

Adams, R. B., & Ferreira, D. (2009). Women in the boardroom and their impact on governance and performance. Journal of Financial Economics, 94(2), 291–309.

Adams, R. B., & Funk, P. (2012). Beyond the glass ceiling: Does gender matter? Management Science, 58(2), 219–235. https://doi.org/10.1287/mnsc.1110.1452

Adams, R. B., & Kirchmaier, T. (2013). From female labor force participation to boardroom gender diversity. FMG.

Adams, R. B., Akyol, A. C., & Verwijmeren, P. (2018). Director skill sets. Journal of Financial Economics, 130(3), 641–662.

Agrawal, A., & Knoeber, C. R. (2001). Do some outside directors play a political role? Journal of Law and Economics, 44(1), 179–198.

Agrawal, A., Knoeber, C. R., & Tsoulouhas, T. (2006). Are outsiders handicapped in ceo successions? Journal of Corporate Finance, 12, 619–644.

Ahern, K. R., & Dittmar, A. K. (2012). The changing of the boards: The impact on firm valuation of mandated female board representation. The Quarterly Journal of Economics, 127(1), 137–197.

Arena, C., Cirillo, A., Mussolino, D., Pulcinelli, I., Saggese, S., & Sarto, F. (2015). Women on board: Evidence from a masculine industry. Corporate Governance: The International Journal of Business in Society, 15(3), 339–356.

Baker, H. K., Pandey, N., Kumar, S., & Haldar, A. (2020). A bibliometric analysis of board diversity: Current status, development, and future research directions. Journal of Business Research, 108, 232–246.

Barrios, J. M., Bianchi, P. A., Isidro, H., & Nanda, D. (2022). Boards of a feather: Homophily in foreign director appointments around the world. Journal of Accounting Research, 60, 1293.

Baum, C. F., & Lewbel, A. (2019). Advice on using heteroskedasticity-based identification. The Stata Journal, 19(4), 757–767.

Bertrand, M., Goldin, C., & Katz, L. F. (2010). Dynamics of the gender gap for young professionals in the financial and corporate sectors. American Economic Journal: Applied Economics, 2(3), 228–255.

Bertrand, M., Black, S. E., Jensen, S., & Lleras-Muney, A. (2019). Breaking the glass ceiling? The effect of board quotas on female labour market outcomes in norway. The Review of Economic Studies, 86(1), 191–239.

Bjerk, D. (2008). Glass ceilings or sticky floors? statistical discrimination in a dynamic model of hiring and promotion. The Economic Journal, 118(530), 961–982.

Bonet, R., Cappelli, P., & Hamori, M. (2020). Gender differences in speed of advancement: An empirical examination of top executives in the fortune 100 firms. Strategic Management Journal, 41(4), 708–737.

Bozhinov, V., Joecks, J., & Scharfenkamp, K. (2021). Gender spillovers from supervisory boards to management boards. Managerial and Decision Economics, 42(5), 1317–1331.

Brammer, S., Millington, A., & Pavelin, S. (2007). Gender and ethnic diversity among uk corporate boards. Corporate Governance: An International Review, 15(2), 393–403.

Brammer, S., Millington, A., & Pavelin, S. (2009). Corporate reputation and women on the board. British Journal of Management, 20(1), 17–29.

Broome, L. L., Conley, J. M., & Krawiec, K. D. (2011). Does critical mass matter? views from the board room. Seattle University Law Review, 34, 1049–1080.

Carbonero, F., Devicienti, F., Manello, A., & Vannoni, D. (2021). Women on board and firm risk attitudes. evidence from exports. Journal of Economic Behavior & Organization, 192, 159–175.

Carrell, S., Hoekstra, M., & West, J. (2015). The impact of intergroup contact on racial attitudes and revealed preferences. National Bureau of Economic Research.

Carter, D. A., Simkins, B. J., & Simpson, W. G. (2003). Corporate governance, board diversity, and firm value. Financial Review, 38(1), 33–53.

Chang, E. H., Milkman, K. L., Chugh, D., & Akinola, M. (2019). Diversity thresholds: How social norms, visibility, and scrutiny relate to group composition. Academy of Management Journal, 62(1), 144–171.

Clark, A. E., D’Ambrosio, C., & Zhu, R. (2021). Job quality and workplace gender diversity in Europe. Journal of Economic Behavior & Organization, 183, 420–432.

Cohen, L. E., Broschak, J. P., & Haveman, H. A. (1998). And then there were more? The effect of organizational sex composition on the hiring and promotion of managers. American Sociological Review, 1998, 711–727.

Czarnitzki, D., & Kraft, K. (2009). Capital control, debt financing and innovative activity. Journal of Economic Behavior and Organization, 71(2), 372–383.

Davies, P. L., & Hopt, K. J. (2013). Corporate boards in europe—accountability and convergence. The American Journal of Comparative Law, 61(2), 301–375.

Deloitte (2021). Missing pieces report: The board diversity census of women and minorities on fortune 500 boards. 6 edition. Retrieved from file:///C:/Users/mhopf/AppData/Local/Temp/missing-pieces- fortune- 500-board-diversity-study-6th-edition.pdf

Derks, B., van Laar, C., & Ellemers, N. (2016). The queen bee phenomenon: Why women leaders distance themselves from junior women. The Leadership Quarterly, 27(3), 456–469.

Deutsch, Y. (2005). The impact of board composition on firms’ critical decisions: A meta-analytic review. Journal of Management, 31(3), 424–444.

Doherr, T. (2021). Ultimatch: Stata module to implement nearest neighbor, radius, coarsened exact, percentile rank and mahalanobis distance matching. Boston College Department of Economics.

European Commission. (2005). Commission recommendation on the role of non-executive or supervisory directors of listed companies and on the committees of the (Supervisory) board. European Commission.

European Institute of Gender Equality. (2021). Gender equality index 2020—Digitalisation and the future of work. European Institute of Gender Equality.

European Women On Boards (2021). European Women on Boards Gender Diversity Index 2020. Retrieved from https://europeanwomenonboards.eu/wp-content/uploads/2021/01/ Gender-Equality-Index-Final-report-2020-210120.pdf

European Union (2003). EU recommendation 2003/361. Retrieved 03.01.2023, from https://eur-lex.europa.eu/legalcontent/ EN/TXT/?uri=CELEX:32003H0361

Farrell, K. A., & Hersch, P. L. (2005). Additions to corporate boards: The effect of gender. Journal of Corporate Finance, 11(1–2), 85–106.

Fauver, L., & Fuerst, M. E. (2006). Does good corporate governance include employee representation? Evidence from german corporate boards. Journal of Financial Economics, 82(3), 673–710.

Field, L. C., Souther, M. E., & Yore, A. S. (2020). At the table but can’t break through the glass ceiling: Board leadership positions elude diverse directors. Journal of Financial Economics, 137, 178.

Finseraas, H., Johnsen, Å. A., Kotsadam, A., & Torsvik, G. (2016). Exposure to female colleagues breaks the glass ceiling–evidence from a combined vignette and field experiment. European Economic Review, 90, 363–374.

Flabbi, L., & Tejada, M. (2012). Gender gaps in education and labor market outcomes in the United States: The impact of employers‘ prejudice. IDB Publications.

Foss, N., Lee, P. M., Murtinu, S., & Scalera, V. G. (2022). The xx factor: Female managers and innovation in a cross-country setting. The Leadership Quarterly, 33(3), 101537.

Fracassi, C., & Tate, G. (2012). External networking and internal firm governance. Journal of Finance, 67(1), 153–194.

Gabaldon, P., de Anca, C., Mateos de Cabo, R., & Gimeno, R. (2016). Searching for women on boards: An analysis from the supply and demand perspective. Corporate Governance: An International Review, 24(3), 371–385.

Gagliarducci, S., & Paserman, M. D. (2015). The effect of female leadership on establishment and employee outcomes: Evidence from linked employer-employee data. Research in Labor Economics, 41, 341–372.

Gangadharan, L., Jain, T., Maitra, P., & Vecci, J. (2016). Social identity and governance: The behavioral response to female leaders. European Economic Review, 90, 302–325.

Gelter, M., & Siems, M. (2021). Letting companies choose between board models: An empirical analysis of country variations (p. 573). ECGI Working Paper.

Gormley, T. A., Gupta, V. K., Matsa, D. A., Mortal, S., & Yang, L. (2021). The big three and board gender diversity: The effectiveness of shareholder voice. European Corporate Governance Institute—Finance Working Paper, 714, 2020.

Green, C. P., & Homroy, S. (2018). Female directors, board committees and firm performance. European Economic Review, 102, 19–38.

Gregorič, A., Oxelheim, L., Randøy, T., & Thomsen, S. (2017). Resistance to change in the corporate elite: Female directors’ appointments onto nordic boards. Journal of Business Ethics, 141(2), 267–287.

Gregory-Smith, I., Main, B. G. M., & O’Reilly, C. A., III. (2014). Appointments, pay and performance in uk boardrooms by gender. The Economic Journal, 124(574), F109–F128.

Grosvold, J., & Brammer, S. (2011). National institutional systems as antecedents of female board representation: An empirical study. Corporate Governance: An International Review, 19(2), 116–135. https://doi.org/10.1111/j.1467-8683.2010.00830.x

Guiso, L., & Rustichini, A. (2018). What drives women out of management? the joint role of testosterone and culture. European Economic Review, 109, 221–237.

Guo, X., Gupta, V. K., Mortal, S., & Nanda, V. K. (2020). Gender and executive job mobility: Evidence from mergers and acquisitions. SSRN Working Paper.

Hermalin, B. E., & Weisbach, M. S. (1988). The determinants of board composition. The RAND Journal of Economics, 19(4), 589–606.

Hewstone, M., Rubin, M., & Willis, H. (2002). Intergroup bias. Annual Review of Psychology, 53(1), 575–604.

Hillman, A. J., Shropshire, C., & Cannella, A. A. (2007). Organizational predictors of women on corporate boards. Academy of Management Journal, 50(4), 941–952.

Hwang, S., Shivdasani, A., & Simintzi, E. (2018). Mandating women on boards: Evidence from the united states. Kenan Institute of Private Enterprise Research Paper

Imbens, G. (2004). Nonparametric estimation of average treatment effects under exogeneity: A review. The Review of Economics and Statistics, 86, 4–29.

Joecks, J., Pull, K., & Vetter, K. (2013). Gender diversity in the boardroom and firm performance: What exactly constitutes a “critical mass?’’. Journal of Business Ethics, 118(1), 61–72.

Kahneman, D., Knetsch, J. L., & Thaler, R. H. (1991). The endowment effect, loss aversion, and status quo bias. The Journal of Economic Perspectives, 5(1), 193–206.

Kanter, R. M. (1977). Some effects of proportions on group life: Skewed sex ratios and responses to token women. American Journal of Sociology, 82(5), 965–990.

Kanter, R. M. (1987). Men and women of the corporation revisited: Interview with rosabeth moss kanter. Human Resource Management, 26(2), 257–263.

Kim, D., & Starks, L. T. (2016). Gender diversity on corporate boards: Do women contribute unique skills? American Economic Review, 106(5), 267–271.

Kleinbaum, A. M., Stuart, T. E., & Tushman, M. L. (2013). Discretion within constraint: Homophily and structure in a formal organization. Organization Science, 24(5), 1316–1336.