Abstract

This systematic literature review contributes to the increasing interest regarding corporate social responsibility (CSR) in family firms—a research field that has developed considerably in the last few years. It now provides the opportunity to take a holistic view on the relationship dynamics—i.e., drivers, activities, outcomes, and contextual influences—of family firms with CSR, thus enabling a more coherent organization of current research and a sounder understanding of the phenomenon. To conceptualize the research field, we analyzed 122 peer-reviewed articles published in highly ranked journals identifying the main issues examined. The results clearly show a lack of research regarding CSR outcomes in family firms. Although considered increasingly crucial in family firm research, a study investigating family outcomes (e.g., family community status, family emotional well-being), as opposed to firm outcomes, is missing. This literature review outlines the current state of research and contributes to the actual debate on CSR in family firms by discussing how family firms can use CSR activities as strategic management tools. Moreover, our analysis shows a black box indicating how CSR links different antecedents and outcomes. The black box is significant since firms generally need to know where to allocate their scarce resources to generate the best outcomes. We identify nine research questions based on these findings, which we hope will inspire future research.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Family firms are the most common form of business organization in the world economy (La Porta et al., 1999; Rovelli et al., 2022). Although the relative size of the family firm sector differs from nation to nation, in most countries, at least 50% of the business population is made up of family firms, and in some countries, e.g., Brazil, Italy, USA, more than 90% (International Family Enterprise Research Academy, 2003). Many family firms have been operating successfully for generations—some for more than a century (Ahmad et al., 2020; Koiranen, 2002; Lorandini, 2015). As a result, they not only contribute enormously to global economic prosperity, are responsible for a large number of jobs (Soleimanof et al., 2018) and innovation drivers (Calabrò et al., 2019) but also shape the values and behavior of national economies (Memili et al., 2015).

Chua et al., (1999, p. 25) define a family firm as “a business governed and/or managed with the intention to shape and pursue the vision of the business held by a dominant coalition controlled by members of the same family or a small number of families in a manner that is potentially sustainable across generations of the family or families.” Reduced to its very core, a family firm forms a unity between the two subsystems, family and firm (Danes et al., 2008; Frank et al., 2017; Stafford et al., 1999), meaning that with growing overlap of both subsystems, the family and its family members become increasingly linked to the company, and vice versa (Izzo & Ciaburri, 2018; Rousseau et al., 2018).

Since the relationship between family members and the firm cannot be separated as easily as between non-family executives and the firm, the owning family influences the firm’s operations, culture, and social behavior (Chrisman et al., 2005; Daspit et al., 2021). Thus, family firm research states that most owning families have a strong interest in ensuring that their firm not only does well financially but is also perceived as valuable by society since the firm’s reputation is closely linked to that society (Giner & Ruiz, 2020; Handler, 1989; Lumpkin & Brigham, 2011; Yanez-Araque et al., 2021). Therefore, research argues that family firms conduct corporate social responsibility (CSR)—meaning that they “[…] integrate social and environmental concerns in their business operations and in their interaction with their stakeholders on a voluntary basis” (Commission of the European Communities, 2001, p. 6)—not only to build a competitive advantage by building superior stakeholder relationships (Bendell, 2022; Bingham et al., 2011; El-Kassar et al., 2018) but also to enhance the public image of the owning family which is closely related to the image of the firm (Campopiano & De Massis, 2015; Zientara, 2017). Although this also applies to other shareholder primacy relationships, Faller and zu Knyphausen-Aufseß (2018) found that CSR’s perceived value seems higher than average for family ownership.

Block and Wagner (2014a) found in an analysis of the S&P 500 that even large, publicly-listed companies with a high proportion of family ownership are more likely to adopt CSR than those with less family ownership. Even family-owned firms that are not considered responsible players, such as Walmart (Walton family) or Ford (Ford family), try to give something back to society through foundations such as the Walton Family Foundation or the Ford Foundation (Scott, 2009; Sutton, 1987)—admittedly, not necessarily through altruistic motives. The Sackler family—founders of Purdue Pharma and Mundipharma and accused of being responsible for the opioid epidemic in the USA, and cited in 1600 lawsuits—used reputation laundering and donations to museums and universities to try and redeem their name and un-tarnish their reputation (Ballantyne & Loeser, 2021). So, although family firms are not necessarily more socially responsible or even ethical than non-family firms, the research shows that if an owning family is involved in the business, compared to a non-family-owned firm, it will be more inclined to conduct CSR for reputational reasons (García-Sánchez et al., 2021; Palma et al., 2022; Seckin-Halac et al., 2021). Multinational corporation conglomerates such as those of Rupert Murdoch and the Koch brothers have caused irreparable damage to the climate movement and use CSR to attempt to green-wash their policies. Bosch, on the other hand, as a large, 100% family-owned firm, is considered a predominantly socially responsible player, especially in terms of its supplier management (Kumar & Vaz, 2017). In this context, however, it is essential to note that the many good deeds of small and medium-sized family firms making up the majority of the world’s business population stay unnoticed by the general public, as these firms tend not to publicize their good deeds (see, e.g., Déniz & Suárez, 2005; Discua Cruz, 2020; Niehm et al., 2008; Peake et al., 2017; Uhlaner et al., 2004). Given the severe social and environmental problems our world faces, it is crucial to understand what does or will motivate this group of firms to engage in CSR.

From the literature, we note that family firms implementing CSR have significantly more benefits compared to non-family firms (e.g., Antheaume et al., 2013; Niehm et al., 2008; Panwar et al., 2014) and that family firms with a higher overlap of family and firm will conduct more CSR (e.g., Kashmiri & Mahajan, 2010, 2014a; Uhlaner et al., 2004). Following this line of thought, we assume that when the family and firm subsystems overlap, the owning family will transfer family resources (e.g., financial, human, or social capital) to the firm, which they—at least partially—will invest in CSR activities such as involving themselves in environmental concerns; providing improved working conditions; supporting non-profit organizations; being involved in local community projects (Turker, 2009), thereby generating both firm and family outcomes.

Research on CSR in family firms has increased significantly over the last few years, and the related research field is growing (Faller and zu Knyphausen-Aufseß, 2018; Kuttner & Feldbauer-Durstmüller, 2018; Mariani et al., 2021; Preslmayer et al., 2018). Due to the variety of studies, the opportunity has come to synthesize the current state of research so that future research can depart from a common understanding. We therefore intent to provide a holistic view of the research field’s peculiarities offers; i.e., specific drivers (antecedents), activities, results (outcomes) and contextual factors of CSR in family firms. Such a framework would help better contextualize existing research and provide guidance for the further development of the research field. Consequently, we pose the following research questions:

-

(1)

Which antecedents drive a family firm’s corporate social responsibility?

-

(2)

Which outcomes do family firms realize by conducting corporate social responsibility?

-

(3)

Which of the family firm’s corporate social responsibility antecedents and outcomes correspond and are the resources used effectively to achieve the intended outcomes?

To study this phenomenon, we decided to examine, synthesize, and systemize the growing body of research on family firms’ CSR activities identifying the CSR antecedents and outcomes in family firms. Following Tranfield et al. (2003) systematic literature review approach, we analyzed 122 peer-reviewed research articles regarding CSR in family firms, applying our theoretical framework inspired by Stafford et al. (1999) Sustainable Family Business Theory (SFBT). The SFBT draws from the systems theory and a resource-based view assuming that the specific behavior of a family firm system emerges from the interaction of its subsystems (i.e., family and firm) and the associated resource transaction between the two. Therefore, our theoretical model builds on the existing research literature offering a critical analysis of family and firm antecedents and outcomes of CSR and guidance for future research regarding the phenomenon’s essence.

Consequently, we contribute to a better understanding of CSR in family firms. Firstly, our literature analysis reveals a pattern showing that family resources integrated into the firm through family influence increase the firm’s probability of conducting CSR activities. Most researchers have found that family firms can use CSR as a strategic tool to obtain favorable outcomes (e.g., Adomako et al., 2019; Craig & Dibrell, 2006; Lamb et al., 2017; Wu et al., 2014; Zientara, 2017) illustrating that family influence within a firm should not necessarily be seen as a liability but as a strategic asset.

Secondly, the literature shows that current research often suffers from a misalignment between empirical research and theory. The prevailing assumption is that family objectives drive family firm CSR activities (Preslmayer et al., 2018), thereby obtaining family and firm outcomes, whereas family firm CSR outcome-related studies only examine firm outcomes, not family and firm outcomes. Although there is much theorizing about family outcomes playing a significant role in family firm management, we could not identify any empirically-related findings.

Thirdly, current research does not identify which family firm antecedents are linked to which family firm outcomes by which CSR activities. Our literature analysis reveals that family firms can benefit greatly from CSR by generating both firm and family outcomes. It is, therefore, crucial for family firms to understand how and where to allocate their resources to achieve optimal results. To clarify CSR’s catalytic role in family firms and to enable family firms to deploy their resources for appropriate CSR activities constructively, we recommend that future research opens this black box and focuses on the particular CSR activities’ mediating effect on family firm antecedents and family firm outcomes.

The remainder of the paper is structured as follows: We discuss our literature review’s theoretical framework and describe the method used to establish the review’s article samples. We ascertain the current research status and identify subsequent lacunae. We then present an agenda for future research regarding CSR in family firms, deriving nine research questions using our SFBT-based theoretical framework. Finally, we discuss our findings and provide theoretical and practical implications based on our results.

Theoretical Framework

The SFBT draws from the systems theory and a resource-based view assuming that the specific behavior of a family firm system emerges from the interaction of its subsystems (i.e., family and firm). This subsystem dynamic differentiates family firms from non-family firms. The family subsystem uses its resources to achieve its family-related goals, which can be subjective (e.g., emotional well-being) and objective (e.g., financial well-being). The firm subsystem also uses its resources, independent of the family, to achieve its business goals (Danes et al., 2008; Stafford et al., 1999). Both subsystems interact, enabling both firm and family to benefit from each other’s resource base.

Although both are independent systems, the subsystems overlap in family firms (Frank et al., 2017). The extent of this overlap between the family and firm systems varies: In family firms where the separation of family and firm is predominant, there is little overlap. Conversely, in family firms where the overlap is high, the extent of the interface of the family and firm subsystems is significant (Bergamaschi & Randerson, 2016). The more the two subsystems overlap, the more likely the owning family will attempt to influence the firm’s management (Astrachan et al., 2020; Chadwick & Dawson, 2018; Chua et al., 1999; Kuttner et al., 2021; Meier & Schier, 2021; Shanker & Astrachan, 1996; Sharma, 2004).

Most research is related to non-family firms (Miller & Le Breton-Miller, 2007). Non-family firms are not driven by trans-generational orientation or socioemotional wealth (SEW), which makes them more flexible since they do not have to consider emotional or generational aspects in their strategies. SEW explains the emotional needs of an owning family, such as identity, the ability to exercise family influence, and the perpetuation of the family dynasty (Gómez-Mejía et al., 2007). Non-family firms are not bound to a particular management pool and can be driven by short-run objectives, maximizing profits quarterly. Also, non-family and publicly-listed firms may have a more ‘democratic’ ownership and are more visible (Blodgett et al., 2011; Cruz et al., 2019; International Family Enterprise Research Academy, 2003; Miller & Le Breton-Miller, 2007).

Most researchers have found that where CSR is concerned, family firms behave differently to non-family firms (Cabeza-García et al., 2017; Cuadrado-Ballesteros et al., 2017; El Ghoul et al., 2016; Fehre & Weber, 2019; Izzo & Ciaburri, 2018) showing that family firms conduct more CSR activities than non-family firms (Faller and zu Knyphausen-Aufseß, 2018). The owning family provides the firm with a particular set of family resources: financial, human, or social capital to pursue its personal goals within the firm (Pütz et al., 2022; Weismeier-Sammer et al., 2013). Familiness describes the family resources integrated within the firm and is “the unique bundle of resources a particular firm has because of the system interaction between the family, its individual members, and the business.” (Habbershon & Williams, 1999, p. 11). Familiness is available regardless of the market situation (Frank et al., 2017) and can enable a family firm to overcome internal and external disruptions (Danes et al., 2008; Stafford et al., 1999).

Family firm research theorizes that family firms with significant levels of familiness combined with the firms’ resources will be able to achieve increased performance levels (Chrisman et al., 2005; Pütz et al., 2022; Weismeier-Sammer et al., 2013). The research literature shows that family firms have higher CSR levels (e.g., Dyer & Whetten, 2006; Liu et al., 2017; Singal, 2014), and we propose that this phenomenon is mainly rooted in the familiness effect where family resources (i.e., financial, human, and social capital) are provided by the owning family (Danes et al., 2008; Weismeier-Sammer et al., 2013) for the benefit of the firm and the family. The increased CSR levels are explained through the image spillover effect. Owning families are often entrenched in their local communities and set great store by their public image. CSR is a valued tool, particularly by family-owned firms (Faller and zu Knyphausen-Aufseß, 2018), that facilitates image enhancement, thereby encouraging client loyalty and embedding the firm’s reputation, consequently leading to increased financial success (Giner & Ruiz, 2020; Handler, 1989; Lumpkin & Brigham, 2011; Yanez-Araque et al., 2021).

Family firms are usually trans-generationally oriented and, therefore, strive to preserve family or firm outcomes so the next generation may benefit (Bammens & Hünermund, 2020; Memili et al., 2020; Pan et al., 2018). By applying the SFBT (Stafford et al., 1999) to our research questions, we created a conceptual framework (see Fig. 1 below) dividing family firm CSR antecedents and outcomes into either the family or the firm subsystem. While family antecedents emerge from the family subsystem, firm antecedents emerge from the firm subsystem. In terms of outcomes, the family subsystem profits from the family outcomes, while the firm subsystem profits from firm outcomes. The more the two subsystems overlap, the greater the interdependencies between family and firm antecedents or outcomes. We also include a loopback from the family firm outcomes to the family firm antecedents since we believe that the outcomes from today can be the antecedents of tomorrow.

Theoretical Model

Following Elkington’s (1998) triple-bottom-line approach that states sustainable development must take place on a different dimension, we classify the applied CSR measures into environmental-, economic-, and societal-related CSR activities and postulate that the family resources provided to the firm should lead to higher levels of CSR. The family subsystem should also benefit through family outcomes. Environmental-related CSR activities are those that aim to reduce or compensate for environmentally harmful behavior, e.g., by fostering ecologically sustainable innovations, adapting green investment strategies, or adopting their behavior according to eco-certification standards (e.g., Bammens & Hünermund, 2020; Dou et al., 2019; Miroshnychenko et al., 2022; Richards et al., 2017). Economic-related CSR activities favor stakeholders who directly relate to the company’s value creation, e.g., employees, customers, or suppliers (e.g., Bennedsen et al., 2019; Dangelico, 2017; Graafland, 2020; Uhlaner et al., 2004; Zheng et al., 2017). Societal-related CSR includes generalized activities such as donations, attention to pressing community issues, or non-profit organization support (e.g., Bhatnagar et al., 2020; Bingham et al., 2011; Uhlaner et al., 2004).

CSR is a firm-level construct. Through these activities, firms maintain or strengthen relationships with different stakeholders, thereby increasing their competitive position (Stock et al., 2022; Wagner, 2010). However, due to the interdependence between family and firm, in the case of family-owned firms, both subsystems benefit from the positive effects CSR generates.

The SFBT also theorizes that a family firm is more resilient to external disruptions due to the buffer that family resources can provide (Stafford et al., 1999). Researchers must also look at moderating contextual factors outside the family firm system to understand the heterogeneous findings better. For example, when CSR is essential for stakeholders (e.g., valued by customers, society, or industry regulations), the family firm may be more incentivized to invest its resources in CSR activities (e.g., Baù et al., 2021; Chen & Liu, 2022; Samara et al., 2018). In CSR research, such factors are often understood as directly affecting CSR activities (Aguinis & Glavas, 2012). Our SFBT-based theoretical model includes contextual factors as exogenous drivers, while family and firm antecedents form endogenous drivers. In a family firm-specific context, we consider that more or fewer resources from the family or firm subsystem are allocated to CSR activities due to the pressure emerging from the context in which the family firm operates.

Methodology

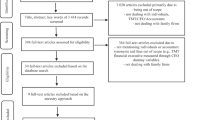

To answer our research questions, we applied the Tranfield et al. (2003) methodology, which uses three phases (i.e., planning, conducting, and reporting) to systematically review and collect significant scientific contributions in a specific research area. We developed a detailed search strategy and search protocol for English articles in peer-reviewed scientific journals. We then carried out the pre-defined search in the following databases: (1) EBSCO Business Source Elite; (2) Elsevier Science Direct; (3) Emerald; (4) Springer Link; (5) Wiley Online Library; and (6) ISI Web of Science. We searched these databases using a combination (AND conjunction) of two keyword groups. Due to the nascent stage of CSR in family firm research (Kuttner et al., 2021) and the wide range of synonyms regarding CSR (Dahlsrud, 2008; Matten & Moon, 2008; Van Marrewijk, 2013), we decided to apply a wide range of keywords. The first group dealt with the identification of CSR-relevant research using: (CSR OR ‘corporate social responsibility’ OR ‘social responsibility’ OR ‘corporate responsibility’ OR ‘corporate social’ OR ‘corporate citizenship’ OR ‘environmental management’ OR ‘sustainab*’ OR ‘social management’ OR ‘ethic’ OR SDG OR ‘sustainable development goals’). The second group concentrated on the relevant literature concerning family firms: (‘family firm*’ OR ‘family business*’ OR ‘family enterprise*’ OR ‘family sme’ OR ‘family own*’ OR ‘family-own*’ OR ‘family control*’ OR ‘family led’ OR ‘family involve*’ OR ‘family influence*’).

By screening all search results that included both a keyword from the CSR and the family firm keyword group in the title or abstract (current analysis covers published research up to June 30th, 2022), we identified 368 studies. We did not consider articles that included one term of both keyword groups but did not deal with both categories explicitly or implicitly, as was the case with studies dealing with CSR (or one of its synonyms) using family firms for the analysis without addressing their particularities. Studies dealing with the ethical values in family firms, but not their impact on CSR activities or related concepts, were also excluded. After this initial screening, we excluded all articles in journals that were not ranked as ‘2 or better’ by the Association of Business Schools’ (2021) Academic Journal Guide. By doing this, 122 articles remained a final sample for further in-depth analysis. Two authors read all papers independently and extracted information regarding author(s), year, title, journal, research method, applied theory, geographic scope, and critical variables using a data-extraction sheet. To better understand the articles within our sample, we also looked up the number of citations per paper using google.scholar.

The 122 articles were then categorized by whether the key variables analyzed were CSR antecedents or outcomes of family firms or both CSR antecedents and outcomes. Articles that examined the effect of family firm-specifics on CSR were classified into ‘antecedents,’ while articles classified into the ‘outcome’ category examined how family firm-specifics affect CSR’s effects. First, we subdivided antecedents and outcomes into a family and a firm’s subcategories, as suggested by the SFBT. The SFBT indicates that integrating family and firm resources helps encounter internal and external disruptions (Danes et al., 2008; Stafford et al., 1999). Consequently, we created a subcategory with contextual factors affecting a firm’s longevity, including stakeholder pressure and community embeddedness. Two authors discussed and iteratively organized all subdivisions during the analysis process. Two subsequent authors were consulted when a disagreement occurred, and all authors discussed categorization extensively until a consensus was found.

Current Research Status

Article Characteristics

The 122 reviewed articles were published in 52 journals, mainly on general management, ethics, gender, and social responsibility. It is noteworthy that the journal with the most significant number of publications is the Journal of Business Ethics, which is responsible for 18.85% of all publications in our review. We identified 15 journals, each publishing at least two articles relevant to our research field. These 15 journals account for 51.64% of all reviewed articles. The remaining 36 journals published one article each, accounting for 29.51% of all reviewed articles. Our citation analysis shows similar results. First, the 122 articles have a general citation count of 15,952. Once again, the Journal of Business Ethics stands out, covering 20.44% of the citations, followed by Entrepreneurship Theory and Practice with 18.81% and Family Business Review with 13.10%. Drawing on the Academic Journal Guide (Association of Business Schools, 2021) to evaluate the journal quality (‘4’ being the highest score and ‘2’ the lowest), 12.30% of the reviewed articles appeared in journals ranked as ‘4’, 57.38% were ranked as ‘3’, and 30.32% ranked as ‘2’ (see Table 1).

The density of publications on CSR in family firms has increased significantly in the last ten years (see Fig. 2). One reason might be that CSR research, in general, became more attractive since the global financial crisis of 2007/2008, when corporate entities’ mismanagement and irresponsible behavior were discovered and made public (Blodgett et al., 2011). This crisis necessitated a major social reassessment and overhaul of business practices in financial and corporate institutions (Crane et al., 2013). Due to their trans-generational orientation (Giner & Ruiz, 2020; Lumpkin & Brigham, 2011), family firms have been discussed as a counter-model to opportunistic, shareholder-value-oriented, non-family firm management (Blodgett et al., 2011), which could explain increased research activities regarding CSR antecedents in family firms. Although it is still a significantly under-researched area, the debate about CSR’s family firm outcomes has become more popular (Kuttner & Feldbauer-Durstmüller, 2018). The relatively lower research output since 2021 could be explained by focusing on the COVID-19 pandemic. Nevertheless, given the significant social and environmental problems our world faces, our research field’s growth will likely continue (see, e.g., Le Breton-Miller & Miller, 2022). Researchers want to examine how family firms differ from non-family firms (Adams et al., 1996; Campopiano & De Massis, 2015; Maung et al., 2020) and what both types of firms can learn from these differences (Craig & Dibrell, 2006; Kashmiri & Mahajan, 2014b; Samara & Arenas, 2017).

Annual Distribution of the 122 Reviewed Published Articles

When looking at reviewed article’s research methods (see Table 2), quantitative research stands out. When analyzing large firms, quantitative research mainly draws from longitudinal databases such as the Thomson Reuters databases (e.g., El Ghoul et al., 2016; Martínez-Ferrero et al., 2017, 2018), KLD data (e.g., Block & Wagner, 2014a, 2014b; Kim et al., 2017; Lamb & Butler, 2018; Liu et al., 2017), annual reports (e.g., Biswas et al., 2019; Sundarasen et al., 2016; Zamir & Saeed, 2020) and S&P 500 firms (e.g., Cui et al., 2018; Kashmiri & Mahajan, 2014b; Wagner, 2010). Quantitative studies examining family-owned small and medium-sized enterprises (SMEs) draw from cross-sectional surveyed data (e.g., Dawson et al., 2020; Peake et al., 2017) as there is little publicly available data on SMEs (Miller & Le Breton-Miller, 2007). Qualitative methods were used for inductive exploration of new research issues and theories, e.g., semi-structured interviews using case study methodology (see Aragón-Amonarriz et al., 2019; Bhatnagar et al., 2020; Marques et al., 2014).

Theories in Use

In sum, we found 96 different applied theories, giving the impression that the research field’s theoretical foundation is fragmented. However, most theories played only a minor role within our sample. When analyzing the applied theories’ underlying assumptions, we noted four theories appearing at least once in 52 papers: The Principal Agency Theory, SEW, Stakeholder Theory, and Institutional Theory (see Table 3). 30 studies combine those by drawing from different assumptions to explain a family firm’s CSR activities.

In CSR-related family firm research, the Principal Agency Theory states that the stronger the control of the owning family (through ownership shares or management), the more successfully the owning family will impose its own goals on the firm (e.g., Block, 2010; López-González et al., 2019; Sahasranamam et al., 2020; Wiklund, 2006). In this regard, twenty-four articles drew on the Principal Agency Theory, focusing on conflicts in the relationship between the principal (mainly the owning family) and the agent (mainly non-family managers), characterized by information asymmetry between the two, where the agent has an information advantage against the principal. The unequal distribution of information among these groups leads to the possibility that the agent may not act in the principal’s best interest and behaves opportunistically for personal gain (Eisenhardt, 1989; Jensen & Meckling, 1976).

The Institutional Theory was referred to in eighteen articles and focused on how firms must adapt to a different environment to gain legitimacy while conducting their business (Campopiano & De Massis, 2015; Du et al., 2016; Zamir & Saeed, 2020). Since firms ostensibly adapt their behavior to the rules of the institutional norms and routines of broader society, the Institutional Theory is used to explain social behavior in different contexts (e.g., Du et al., 2016; Ge & Micelotta, 2019; Singal, 2014). Family firm-related CSR research uses this theory mainly to examine how specific antecedents affect CSR under different contextual factors (e.g., Agostino & Ruberto, 2021; Du et al., 2016; Kim et al., 2017). For example, the location of a company’s industry influences how family ownership or management affects CSR (Chen & Cheng, 2020). The same applies to cultural contexts (Samara et al., 2018).

SEW was applied in twenty-one articles and used as a theoretical concept. The first article in our sample using SEW was published in 2014, and this concept has gained popularity ever since (Swab et al., 2020). SEW focuses on the family’s affective and non-financial goals, such as strengthening the family image and maintaining control over the own firm (Gómez-Mejía et al., 2007; Labelle et al., 2018; Marques et al., 2014; Yu et al., 2015). Therefore, the most dominant argument among studies influenced by SEW is that the owning family wants to protect its family image and therefore engages in CSR to improve that image and look good to stakeholders (e.g., Dick et al., 2021; Labelle et al., 2018; Ma et al., 2022; Madden et al., 2020; Nadeem et al., 2020).

The Stakeholder Theory was used in thirteen articles and is one of the fundamental and dominant theories of general CSR research (Freeman & Dmytriyev, 2017; Freeman et al., 2010). This theory explains why family firms are stakeholder-focused and, therefore, conduct more CSR than non-family firms (Bingham et al., 2011; Delmas & Gergaud, 2014) and is attributed to the presence of an owning family. Reasons for this include, for example, inter-generational thinking and higher awareness of stakeholder pressure compared to non-family firms (Cruz et al., 2014; Delmas & Gergaud, 2014). Additionally, CSR-related family firm research assumes that owner families use their firms to pursue financial and non-financial family goals and are more inclined to engage in CSR towards their stakeholders to achieve these goals (Bingham et al., 2011; Cruz et al., 2014).

There is a contemporary trend proposing a combination of the four prevailing theories (e.g., García-Sánchez et al., 2021; López-González et al., 2019; Sahasranamam et al., 2020; Seckin-Halac et al., 2021), although, notably, approximately 30% of the articles used no theories at all. However, more recent studies tend towards being theory-driven, indicating that the understanding of family firms has advanced.

Content Findings

Family Firm Antecedents

In total, 96 of all articles in our sample (78.69%) dealt exclusively with the antecedent angle of CSR in family firms, while 16 (14.95%) dealt with both antecedents and outcomes simultaneously showing the predominance of antecedent-related focus of the field of CSR in family firms.

When the first articles addressing family antecedents (see Adams et al., 1996; Graafland et al., 2003; Gallo, 2004; Uhlaner et al., 2004) were published, it was implicitly theorized that family resources (i.e., family social capital toward stakeholders) are antecedents of CSR activities (Uhlaner et al., 2004). Subsequent publications applied different exercises to identify family antecedents of CSR, with family ownership being the most prominent measure (see Table 4).

The research reveals that most studies use family ownership (e.g., Bammens & Hünermund, 2020; Kim et al., 2020; Rees & Rodionova, 2015; Terlaak et al., 2018) followed by family management (e.g., Block, 2010; Cui et al., 2018; Oh et al., 2019) or a combination of both (e.g., Craig & Dibrell, 2006; Dangelico, 2017; Kim & Lee, 2018) for examining the effect of family antecedents on CSR in family firms. Although there is a moderate tendency towards a positive effect, no apparent effect on CSR activities can be found; this could be because these measures alone are insufficient to influence firm decisions, as the owning family cannot adequately influence internal decision-making processes by their mere presence (Terlaak et al., 2018; Yu et al., 2021). As suspected, the operational measures do not sufficiently reflect the overlap between family and company (Chua et al., 1999).

Although SEW covers the influence of the owning family much better than research using family ownership and management, it similarly shows heterogeneous results regarding CSR (e.g., Arena & Michelon, 2018; Dayan et al., 2019; Kariyapperuma & Collins, 2021; Zientara, 2017). Even though the probability that SEW emerges increases with the overlapping of the subsystems family and firm (Berrone et al., 2010), it does not have a resource-increasing character per se, which can be directed to conduct more CSR. Therefore, CSR only partially supports SEW-related goals, which also explains the heterogeneous results of the other studies (e.g., Cruz et al., 2014; Dick et al., 2021; Zientara, 2017). For example, SEW causes family firms to engage in CSR with external stakeholders more often than non-family firms in order to generate a positive image spillover effect for the owning family, but less to engage in CSR with internal stakeholders, as the owning family is afraid of losing control over their own company by making concessions to, e.g., employees (Cruz et al., 2014).

In line with our theoretical assumption, research using the family generation measure (e.g., Dawson et al., 2020; Delmas & Gergaud, 2014; Uhlaner et al., 2004) and family value measures (e.g., Aragón-Amonarriz et al., 2019; Marques et al., 2014; Sánchez-Medina & Díaz-Pichardo, 2017), which are better at capturing the overlap between family and firm, show predominantly positive effects on CSR. These studies argue that as the control of the owning family gets stronger on day-to-day operations, so does the opportunity to influence internal business decisions (Sharma & Sharma, 2011; Uhlaner et al., 2012). Probably the most significant overlap between family and firm is shown when the firm has the same name as the owning family and leads to an overall positive effect on CSR (e.g., Kashmiri & Mahajan, 2010, 2014a; Uhlaner et al., 2004). Thus, more sophisticated degrees of family influence, such as family generation, family values, and the family firm name, tend to be associated with a strong interrelation of family and firm subsystem.

Since a family firm consists not only of a family subsystem but also of a firm subsystem, research studies examined the influence of general firm antecedents on CSR activities in our sample (see Table 5). These studies answer how firm antecedents interact with family antecedents regarding CSR. They focus mainly on (internal) non-financial antecedents predominantly showing the effect on CSR and examine the effect of governance (e.g., Campopiano et al., 2014; El-Kassar et al., 2018; Terlaak et al., 2018) and non-family management (e.g., Martínez-Ferrero et al., 2017; Oh et al., 2019; Samara et al., 2018) on family firms’ CSR activities. With only two studies examining the effect of financial antecedents, it is apparent that further research is still needed.

Family Firm Outcomes

Ten studies within our sample (8.20%) examined the outcome side of CSR exclusively, while 16 (13.11%) dealt with both antecedents and outcomes simultaneously, showing the predominance of antecedent-related focus of CSR in family firms. Remarkably, most outcome-related studies found that family firms generate better results from CSR activities than non-family firms (see Table 6), indicating that family firms, in general, are better at utilizing CSR (e.g., Antheaume et al., 2013; Niehm et al., 2008; O’Boyle et al., 2010; Panwar et al., 2014).

Most studies show how family firms improve their financial outcomes through, among others, the cost of capital (Wu et al., 2014) or return on new products (Kashmiri & Mahajan, 2014a), but mainly focus on the firm’s general performance (e.g., Adomako et al., 2019; Choi et al., 2019; Kashmiri & Mahajan, 2014b). Family firms can also improve their internal non-financial outcomes (Ahmad et al., 2020), such as longevity (Antheaume et al., 2013; Samara & Arenas, 2017) or innovation performance (Biscotti et al., 2018; Craig & Dibrell, 2006; Wagner, 2010) and in external non-financial areas such as firm reputation (Samara & Arenas, 2017; Zientara, 2017), credibility (Hsueh, 2018; Panwar et al., 2014), or customer orientation (Ahmad et al., 2020).

The research literature determines two main reasons family firms generate augmented outcomes through CSR. The signaling effect associated with family firm status prompts external non-financial outcomes (e.g., Martínez-Ferrero et al., 2018; Maung et al., 2020; Sekerci et al., 2022), and the familiness dynamic, which allows family firms to translate CSR into positive financial and internal non-financial outcomes (e.g., Craig & Dibrell, 2006; Pan et al., 2018; Wagner, 2010). The signaling effect means external stakeholders are less likely to perceive the family firm’s CSR activities as opportunistic green-washing, particularly in the case of SMEs where the owning family is evident (e.g., Ahmad et al., 2020; Dangelico, 2017; O’Boyle et al., 2010) but also with large, publicly listed family firms (e.g., Biscotti et al., 2018; Kashmiri & Mahajan, 2014a; Wu et al., 2014).

The familiness stream of literature is not concerned with whether family firms engage in more or less CSR than non-family firms but with the extent to which family firms can better translate CSR activities into positive outcomes (e.g., Wagner, 2010). Family firms have the advantage of asserting more influence on the operational management and increasing control over the firm’s subsystem (Doluca et al., 2018; Niehm et al., 2008). Both streams utilize the transgenerational aspect particular to family firms that ensures their strategies and aims have long-term focus leads them to use CSR to maximize positive outcomes for the owning family and the firm (e.g., Campopiano & De Massis, 2015; Niehm et al., 2008; Zientara, 2017).

We did not find research providing practical information on whether CSR-improved stakeholder relations affect family outcomes, even though the importance of family outcomes was referred to in the reviewed literature (e.g., Campopiano & De Massis, 2015; Niehm et al., 2008; Zientara, 2017). Déniz and Suárez (2005) note how owning families are personally affected by the relationships with stakeholders since they are inseparable from it. Furthermore, the findings of Aragón-Amonarriz et al. (2019) conclude that the owning family derives honors from socially responsible behavior and, therefore, could act as a basis for family outcome-related CSR research.

Contextual Factors

A fundamental assumption of studies analyzing family firms is that owning families are more sensitive to external contextual factors than other non-family owners, thus leading to a greater tendency to implement the requirements of external stakeholders (Ge & Micelotta, 2019). The owning family assigns greater importance to the firm’s image, as the family identifies with the firm (e.g., Amidjaya & Widagdo, 2020; Discua Cruz, 2020; Labelle et al., 2018; Zientara, 2017). If the firm carries the family name, the family and the firm’s reputation become inseparable, and maintaining or acquiring a good reputation is paramount (e.g., Abeysekera & Fernando, 2020; Bammens & Hünermund, 2020; Kashmiri & Mahajan, 2010; Pan et al., 2018; Uhlaner et al., 2004). Following this argumentation, an owning family will be more willing to provide resources to the family firm system for CSR activities intended for brand enhancement and expected from the firm by external stakeholders.

The research literature analysis revealed that contextual factors could be divided into general stakeholder pressure and community embeddedness. While public stakeholder pressure can be abstract communication from an anonymous group (e.g., industry) resulting in a generic response (e.g., via CSR reports) (e.g., Campopiano & De Massis, 2015), family firms with community embeddedness are more involved and use CSR to respond to the needs or requirements of the community (e.g., Niehm et al., 2008; Peake et al., 2017). Table 7 shows we found 26 studies covering general stakeholder pressure and ten explicitly covering the impact of family community embeddedness on a family firm’s CSR activities (e.g., Fitzgerald et al., 2010; Laguir et al., 2016; Peake et al., 2017).

It is noteworthy that the relevance of public stakeholder pressure (e.g., industry norms, national culture) is more pronounced in studies analyzing large firms (e.g., Blodgett et al., 2011; Cruz et al., 2014; Cuadrado-Ballesteros et al., 2015). Studies on SMEs tend towards community embeddedness (e.g., Dekker & Hasso, 2016; Kallmuenzer et al., 2018; Peake et al., 2017). The community embeddedness perspective shifts the focus away from general stakeholder groups and examines the owning family’s interpersonal ties within the local community. The latter research argues that family-owned SMEs use CSR as a strategic tool to influence external stakeholders’ perception (i.e., local community) positively to closer relationships between them (Lamb et al., 2017; Uhlaner et al., 2012). Interestingly, all studies unanimously agree that family firms react with more CSR towards pressure from contextual factors.

Although most studies show the positive effect of external pressure on a firm to conduct CSR activities, this is country and region-dependent (Ertuna et al., 2019; Ge & Micelotta, 2019; Labelle et al., 2018; Zamir & Saeed, 2020). The first studies with US American datasets were conducted between 2003 and 2013. The economic relevance of Asia has recently increased, engendering an increase in CSR-related family firm studies and applying Asian datasets since 2009 (see Table 8). While studies using US American data mainly recorded positive effects of family antecedents on CSR (e.g., Cordeiro et al., 2020; Lamb & Butler, 2018; McGuire et al., 2012; Panwar et al., 2014), Asian studies have frequently shown the contrary (Biswas et al., 2019; El Ghoul et al., 2016; Huang et al., 2009; Muttakin & Khan, 2014).

The reason Western cultures incorporate CSR more than their Asian counterparts can be attributed to the difference in cultural and political aims and values. Western countries tend to be highly stakeholder-oriented, and the values are based on “liberal democratic rights, justice, and societal structures” (Amann et al., 2012, p. 331), leading to more significant institutional pressure for firms to comply accordingly (Campopiano & De Massis, 2015; Dekker & Hasso, 2016). Asian countries have a more shareholder-oriented culture. Therefore, there is less social pressure to become CSR-compliant (El Ghoul et al., 2016), and the owning families tend to focus more on their personal financial well-being, subsequently regarding CSR as relatively inconsequential (e.g., Biswas et al., 2019; Du, 2015; Du et al., 2016; Muttakin & Khan, 2014). Family firms form the backbone of the Asian economy, with family ownership being the most dominant ownership form of companies in the Asia Pacific region (El Ghoul et al., 2016). Of the largest 500 largest global family firms ranked by revenue, over 20% are Asia-based, with combined revenue of almost $2 trillion (Global Family Business Index, 2021). Although it is not required by law for Asian companies to be CSR compliant, there is a trend towards encouraging more CSR from companies to entice foreign investment. Foreign investors from Western countries and companies are encouraged by their external stakeholders to provide ethically and ecologically sourced products, and therefore the investors and companies will require CSR from the Asian company they are importing from or collaborating with (Cordeiro et al., 2018; Du et al., 2018; Muttakin & Khan, 2014).

In India, for example, many local family firms are voluntarily socially responsible (Bhatnagar et al., 2020; Sahasranamam et al., 2020). They aim at better working conditions for employees, for example, and are involved in improving the local community; e.g., the Godrej Group preferred to protect mangroves on its land in Mumbai, despite the insatiable demand for housing development. Jardine Matheson, a Fortune 500 and Hong Kong-based multinational conglomerate controlled by the Keswick family has pledged its commitment to biodiversity and is implementing sustainability strategies in its many operating companies. The company has a proactive approach and collaborates with public stakeholders on climate issues, ecological sustainability, and forest protection aiming to mitigate any adverse impact from its operations and products (Jardine Matheson, 2021).

From the research literature, we conclude that it is not only essential to understand the effects of different organizational settings (i.e., family and firm subsystem) on CSR (Dahlsrud, 2008) but also the effects of external contextual and cultural factors that influence the internal processes of a family firm when considering CSR as a driver.

Corporate Social Responsibility Activities

We examined which CSR activities were used in our study samples and how their antecedents and outcomes differed. According to Elkington’s (1998) triple-bottom-line approach, we classified the applied CSR measures into environmental-, economic-, and societal-related CSR activities (see Table 9).

Twenty-nine articles were allocated to environmental-related CSR (23.77%), 21 to economic-related CSR (17.21%), and thirteen articles to societal-related CSR (10.66%). Furthermore, we found that in 59 articles (48.36%), the majority of research is based on CSR measures that do not differentiate between different activities but average different activities in one measure (e.g., Gallo, 2004; Hsueh, 2018; Iyer & Lulseged, 2013; McGuire et al., 2012). Looking at different family and firm subsystem antecedents and outcomes through the lens of individual CSR activities gives us a balanced perspective. None of the CSR activities focus on specific antecedents or outcomes, and there are no significant differences in the effects between the activities. We conclude that the related CSR activities have not yet been sufficiently differentiated in family firm research, and the disproportionately large number of articles that do not distinguish between different CSR activities supports this view.

Future Directions of Research

Figure 3 recapitulates the scope and robustness of the findings in our data sample. In terms of scope, the literature shows that most CSR-related family firm research focuses on CSR antecedents, and only a few studies are concerned with outcomes. On the antecedent side, research mainly focuses on the direct effect of family antecedents on CSR or the interaction with firm antecedents and its effect on CSR. However, such research examining the interaction of family and firm antecedents on CSR is in the minority. The research clearly shows a lack of analysis on CSR outcomes in family firms, and in terms of firm outcomes, family firms achieve more through CSR than non-family firms. Although there is increasing emphasis on family firm research, the study of family outcomes (e.g., family community status, family emotional well-being) is lacking. Moreover, the catalytic role of CSR activities has not yet been studied in detail, where the fundamental question of which antecedents and outcomes are linked by which CSR activities remain unanswered.

Model of Antecedents and Outcomes of CSR in Family Firms

In terms of robustness, it is evident that the more substantial the interrelation between family and firm (see, e.g., family generation, family values, and the family firm name), the higher the probability that a family firm will conduct CSR. Although the research field is mainly antecedent-oriented, the literature shows that the effect of family on firm antecedents remains unexplored. On the outcome side, CSR predominantly has robust effects on firm outcomes. Considering that an empirical examination of family outcomes is missing, it is unclear how CSR and firm outcomes affect family outcomes. Furthermore, the research literature cannot provide robust findings on how contextual factors affect the outcome side of CSR in family firms.

To gain further insight, we propose nine research questions for future exploration to open the ‘black boxes’ and consequently lead to clarifying significant aspects concerning family firm CSR activities (see Table 10).

Family firm research traditionally focuses on examining family antecedents and only marginally includes firm antecedents in their models. Family and firm antecedents’ effects on CSR are mainly examined independently. Research shows that family involvement (identification and commitment) and family values have a positive effect on CSR activities but do not examine the extent to which family and firm antecedents interact with each other (e.g., Marques et al., 2014; Peake et al., 2017; Sharma & Sharma, 2011; Uhlaner et al., 2012).

Following our SFBT-based theoretical framework, we know that the higher the influence of the owning family within its firm, the greater the interaction between family and firm, and the more resources can be transferred between both (Stafford et al., 1999). When family resources are transferred to the firm subsystem, familiness is generated, providing the family firm with a more extensive resource base, ultimately leading to a competitive advantage in the long term (Frank et al., 2017; Habbershon & Williams, 1999; Weismeier-Sammer et al., 2013). These theoretical assumptions are implicitly applied, explaining that owning families involved within the firm introduces responsible behavior, which stakeholders will eventually repay (e.g., Aragón-Amonarriz et al., 2019; Fitzgerald et al., 2010; Fritz et al., 2021). According to research, the family’s social capital is a crucial driver of a family firm’s CSR activities and competitiveness (e.g., Niehm et al., 2008; Peake et al., 2017; Uhlaner et al., 2004).

Unexamined is the permeability of the two subsystem boundaries and how those affect the effectiveness of the resource transaction. Utilizing the system’s theoretical perspective, we theorize that the subsystem’s boundary permeability can differ (Frank et al., 2017). Depending on how strong the subsystem boundaries are, the impact of family antecedents (i.e., family resources) can be more or less effective on firm antecedents (i.e., firm resources). If the subsystem permeability is low, resources can easily be transferred from one subsystem to another, while such a transaction will be more difficult when the permeability of the subsystem’s boundaries is high (Danes et al., 2008; Hernes & Bakken, 2003). However, this permeability can change, e.g., if the non-family management wants to preserve power within the firm subsystem and tries to hamper the integration of family resources, meaning that the potentially positive effect of family resources (i.e., familiness) would not be achieved.

Thus, although we found that future family firm research should focus on the outcome angle of CSR, we believe that the antecedent’s research angle should also be developed. In this regard, we also propose to examine which factors could hamper the transfer of family and firm subsystem resources between the subsystems and whether this could affect the family firm’s CSR activities.

-

Research Question 1a: Which firm antecedents (i.e., firm resources) affect the association between family antecedents (i.e., family resources) and CSR activities?

-

Research Question 1b: Which conflicts can arise during the resource transaction between family and firm subsystem, and how does this affect CSR activities?

Family firm research mainly concentrates on examining CSR’s antecedent angle. Previous findings dealt with the financial and non-financial firm outcomes while only theorizing about family outcomes without empirically studying them. However, more and more studies have recently scrutinized CSR outcomes in family firms (e.g., Hsueh, 2018; Lin et al., 2020; Sekerci et al., 2022). The empirical scrutiny on CSR family outcomes is logical, considering CSR is a firm-level construct.

It is, however, an assumption of the SFBT-based theoretical framework that while family and firm share their resources to some extent, the family and the firm pursue their specific goals separately (Danes et al., 2008; Stafford et al., 1999). Thus, Campopiano and De Massis (2015) state that owning families can profit from the image-enhancing effect of CSR themselves through an increased family image. Furthermore, Aragón-Amonarriz et al. (2019) conclude that family honorableness is one of the outcomes of a family firm’s CSR activities, indicating that CSR generates family outcomes. However, which family outcomes can be generated through CSR has not yet been examined. Consequently, we recommend exploratory (i.e., qualitative) work in this area to determine which family outcomes an owning family may achieve through CSR.

The literature indicates that if CSR activities do not bring positive results for the owning family, they will probably cease to provide resources for CSR implementation (Palma et al., 2022). Taking a closer look at the implicit assumptions made by the reviewed studies on family outcomes (e.g., family harmony, family well-being), we find indications that a family firm’s CSR could also have an impact on the owning family itself (e.g., Campopiano & De Massis, 2015; Niehm et al., 2008; Zientara, 2017). The family and the firm are overlapping subsystems that mutually affect each other, so the question remains which family outcomes (e.g., family harmony, family well-being) may be achieved. Following Jaskiewicz and Dyer (2017), we ask to what extent these family outcomes act in subsequent phases as family antecedents.

-

Research Question 2: Which family outcomes (i.e., family resources) can an owning family generate through the CSR activities of its firm, and how do those affect the family firm’s CSR activities in subsequent periods?

Although family outcomes were not explicitly examined, the research literature implicitly indicates that CSR-related family outcomes are generated through the use of firm outcomes (e.g., Aragón-Amonarriz et al., 2019; Campopiano & De Massis, 2015; Déniz and Suárez, 2005; Niehm et al., 2008; Zientara, 2017). It is a fundamental assumption of our SFBT-based theoretical framework that resources can be exchanged between family and firm as soon as the overlap of both subsystems is significant enough (Danes et al., 2008; Stafford et al., 1999), meaning the family firm has a unique resource base since it can draw from the owning family’s resources. Since the resource transaction between the two subsystems can also be performed from firm to family, this implies that the owning family can also benefit from the firm’s financial and non-financial outcomes of CSR.

However, as in the case of the antecedents, it is also necessary to consider where outcomes are concerned, that a subsystem’s boundary permeability can hinder the resource transfer effectiveness. For example, some studies examine the extent to which majority shareholders withdraw resources from a company at the expense of minority shareholders (Welford, 2007). This so-called ‘tunneling’ disadvantages minority shareholders, who, due to their limited influence, cannot protect themselves against majority shareholders (Dal Maso et al., 2020; Sahasranamam et al., 2020). Therefore, the potential for the transfer of firm resources (primarily financial or social capital) could lead to the firm subsystem decreasing its permeability to hamper resource flow to the family subsystem.

Although we propose putting greater emphasis on firm outcomes, we also propose that outcomes-related CSR research should include how family outcomes are affected by CSR. For example, it could be examined whether an increase in the firm’s performance through CSR also leads to an increase in the family’s well-being. Another suggestion would be to examine whether a firm image, improved through CSR, leads to more social capital for the owning family. In this regard, we also propose examining the extent to which conflicts occur between family and firm and to what extent this process influences the generation of family outcomes.

-

Research Question 3a: Which firm outcomes (i.e., firm resources) affect the association between CSR activities and family outcomes (i.e., family resources)?

-

Research Question 3b: Which conflicts can arise during the resource transaction between family and firm subsystem, and how does this affect the family firm’s CSR outcomes?

According to our SFBT-based theoretical framework, family and firm resources are used to overcome internal and external disruptions. Research has found that family firms are more sensitive to external contextual factors (Uhlaner et al., 2004) and more adaptive to them due to their unique set of resources. Research concerning CSR antecedents shows that stakeholder pressure and community embeddedness increase the likelihood that family firms will engage in CSR (Ge & Micelotta, 2019). The greater the pressure from contextual factors to engage in CSR, the more likely family firms are to mobilize their family resources for the firm (e.g., Berrone et al., 2010; Maggioni & Santangelo, 2017; Zamir & Saeed, 2020).

Research shows that this pressure varies significantly from region to region (Ertuna et al., 2019; Labelle et al., 2018). While it tends to be high in the USA and Europe, it tends to be low in Asian countries (Welford, 2007). However, the economic relevance of the Asian continent has increased, and the economic relationships between Asian countries and the Western world have become more relevant. Muttakin and Khan (2014) found that many Asian firms now use CSR to signal to foreign investors that they have more governance structures than other regional competitors (Cordeiro et al., 2018). Therefore, Asian family firms can use their family resources to enhance CSR and use it as a strategic tool to signal trustworthiness to Western investors (Du et al., 2018).

Contextual factors could affect the relationship between CSR activities and their outcomes. For example, different countries and communities may have different expectations of the owning family regarding CSR. Family firms could respond more effectively towards those expectations when expanding since they have a more significant resource base because of family resources. Therefore, we encourage future research to look for and examine contextual factors affecting the outcomes of CSR in family firms.

-

Research Question 4: Which contextual factors affect the relationship between CSR activities and outcomes (i.e., family and firm outcomes) of family firms?

A crucial connection not yet addressed by current research involves CSR antecedents and defining which antecedents lead to which outcomes, also which CSR activities link those antecedents and outcomes. Whether the firm antecedents lead to firm outcomes or there are crossover connections due to the overlap of family and firm, so that, for example, firm antecedents generate family outcomes remains to be established. The effectiveness between family and firm antecedents is also an angle that should be considered.

Therefore, it is necessary to consider which, how, and why CSR activities link antecedents and outcomes. Labelle et al. (2018) theorize that economic and non-economic goals drive a family firm’s CSR activities. They argue that the higher the proportion of family ownership, the more likely the firm’s business activities align with achieving economic goals. Since they attribute a non-economic effect to CSR, they argue and deduce that more CSR is conducted in firms with lesser family ownership, and fewer CSR activities are conducted in firms with increased family ownership. Interestingly, Terlaak et al. (2018) theorize and empirically find the opposite by arguing that family firms place a higher emphasis on non-economic goals when family ownership within the firm increases.

Thus, since many family firms have scarce resources and must use them efficiently to survive (Ward, 1997), it is vital to understand which CSR activities will help them achieve the best results. Following Stafford et al. (1999) SFBT, a division of family and firm could help clarify these issues. Case studies could be used to identify relationships or disagreements between antecedents and outcomes. Their results could be checked quantitatively afterward using panel surveys to analyze the long-term effect of the measures. In future research, this black box must be opened to prove which CSR activities help achieve which goals and whether family resources can help achieve those.

-

Research Question 5a: Which CSR activities (e.g., environmental, economic, or societal-related) are linked to which antecedents (i.e., family and firm antecedents) and outcomes (i.e., family and firm outcomes)?

-

Research Question 5b: How and why do CSR activities link antecedents and outcomes of family firms?

A central goal of family firms is to ensure that the firm can continue to provide a basis for the family’s existence and even for later generations. While a handful of family firms achieve this goal, others do not (Koiranen, 2002). Among the outcome-related studies, Antheaume et al. (2013) found that CSR is a factor that positively influences the longevity of family firms, indicating that CSR helps family firms succeed over generations. In line with our SFBT-based theoretical framework, we found that substantial family influence leads to a greater propensity of CSR in family firms, which we trace back to family resources integrated within the family firm’s resource base. Those help the family firm to respond more effectively to internal and external disruptions and thus also to generate better outcomes out of CSR.

In this context, Pan et al. (2018) is particularly noteworthy since they find that CSR positively affects the family firm’s post-succession performance. They theorize that to take over successfully, successors of the owning family need to win the support of internal and external stakeholders, which they can do by conducting CSR (Bammens & Hünermund, 2020; Pan et al., 2018). Signaling good intentions to their stakeholders through CSR will increase the motivation of the firm’s stakeholders to interact (Bingham et al., 2011), helping to facilitate the social network transfer from the predecessor to the successor (Aragón-Amonarriz et al., 2019; Pan et al., 2018; Schell et al., 2020). Thus, CSR is a strategic instrument that increases the firm’s legitimacy (Chiu & Sharfman, 2011), consequently increasing the probability of a successful generational handover (Pan et al., 2018).

Accordingly, CSR could help a family firm preserve its resource base during the handover of the firm, thus contributing to the longevity of the firm as this is one of the most crucial issues of family firm research. Research empirically proving this assumption would create a business case for CSR in family firms. Therefore, this assumption must be addressed in future research.

-

Research Question 6: How and why do CSR activities increase the longevity of family firms?

Synthesis

Discussion

This systematic literature review has revealed that CSR is still a relatively young phenomenon in family firm research but is becoming increasingly relevant. This review was guided by three research questions focusing on a family firm’s CSR antecedents and outcomes and their interaction. Using Stafford et al.’s (1999) SFBT to build our theoretical framework, we examined the CSR antecedents and outcomes of a family firm not only from a firm but also from a family’s perspective. We contribute to the literature by summarizing and integrating our findings in an over-arching framework, emphasizing family and firm antecedents, outcomes, and contextual factors. Thus, we uncover the current research focus on family firms’ CSR antecedents and outcomes (see Fig. 3) and show which research questions need to be addressed in the future (see Table 10). Our framework helps researchers to organize the existing research (e.g., Mariani et al., 2021) for a better understanding of this phenomenon and to address future problems and questions. In this regard, our review contributes to the further development of the research field.

Our review of the research literature shows that although CSR is a firm-level construct, CSR decision-making is not exclusively tied to the firm but also to the family subsystem and the family resources it provides (Dimov, 2017; Jang & Danes, 2013). The research literature provides evidence that increased CSR is implemented when the owning family strongly influences the family firm. Consequently, the use of family resources (i.e., familiness) to conduct CSR activities is more pronounced in smaller firms as it is more likely that an owning family will exert its influence in smaller firms than in larger ones (Danes & Brewton, 2012). From an SFBT point of view, this is the case since the owning family directs more family firm resources towards CSR activities from which it benefits doubly—firstly by the firm outcomes and secondly by the family outcomes. Thus, while not necessarily being more ethical than other firm owners, owning families are inclined to use resources provided by the family subsystem to conduct CSR on the firm level.

Also, according to SFBT, as family influence increases, family firms engage in CSR to cultivate their relationships with their stakeholders (Fitzgerald et al., 2010; Stafford et al., 1999), and thereby generate positive firm outcomes and longevity for the family firm by leveraging resources (Kuttner & Feldbauer-Durstmüller, 2018). As in the case of the antecedents-related studies, we consequently also examined the outcomes-related studies from a family and firm perspective. Concerning studies examining the firm outcomes of CSR in family firms, we found that the research focuses strongly on non-financial outcomes, whereas financial outcomes have rarely been researched. Regarding firm outcomes, we recommend that future research assign a higher priority to CSR’s financial firm outcomes. Family outcomes relating to the needs and goals of the owning family (Gómez-Mejía et al., 2007; Jaskiewicz & Dyer, 2017; Jaskiewicz et al., 2017) have not yet been analyzed at all, which is surprising, as the subsystems family and firm form a unit, and accordingly the outcomes should have a reciprocal influence (Stafford et al., 1999). Further research could pinpoint which family-related goals (Chrisman et al., 2010; Kotlar & De Massis, 2013) family firms can achieve through CSR.

While our literature review has shown that family influence increases the likelihood of CSR activities within family firms, consequently increasing the probability of achieving improved firm outcomes, we could not answer how CSR links both categories. Thus, the question concerning the catalytic role of CSR remains a black box. Since family firms need to know which antecedents can help them achieve their goals (i.e., family and firm outcomes) through CSR activities, this question needs to be answered. Family firms must invest the optimum set of family and firm resources into CSR activities, knowing that those investments will give them the strategic advantage they need; this is especially important for family-owned SMEs, which have considerably fewer resources available than their larger competitors.

In general, Jaskiewicz et al. (2017) called for a more robust integration of family science into this research area to better integrate the family as an organizational actor into management research. Family science uses knowledge coming “from various disciplines such as psychology, sociology, and education” (Jaskiewicz et al., 2017, p. 309) and, therefore, could provide new theoretical and empirical insights for the explanation of CSR’s family outcomes. Since it can be assumed that family firms do not conduct CSR purely out of altruism but also to achieve specific outcomes (Zientara, 2017), this area of research offers many opportunities for future family firm-related studies. Furthermore, a holistic theoretical framework such as Stafford et al.’s (1999) SFBT that considers the unity of family and firm as well as a permanent exchange of resources could be beneficial. This theory assumes that the resources are transferred between the family and the firm subsystem depending on the extent of the subsystems’ overlap (Danes et al., 2008; Fitzgerald et al., 2010). By identifying the underlying reasons for the interaction between family and firm, it might be possible to better explain a family firm’s CSR behavior.

Practical Implications

The literature shows that family firms do indeed engage in more CSR. However, as the Waltons, Fords, Murdochs, and Sacklers of this world show, they do not necessarily do so because they are more ethical than non-family firms but rather because they achieve positive results for the family and the firm by doing so. Therefore, we must bear in mind that family firms are run according to business principles and consequently conduct CSR for the benefit of the family and the firm, and not necessarily for the benefit of society. If the lobby against unethical practices; child labor; slave labor; pollution; animal cruelty, for example, did not exist, would the chemical company continue to pollute the rivers, or the sweatshop stop using child labor? These are rhetorical questions but show CSR’s potential for improving the state of the world, on the one hand, and its limitations simultaneously.

Although we know that family firms use CSR activities, not for altruistic reasons but to benefit personally through family and firm outcomes, we should not forget the positive aspects of those activities for society. Given the severe social and environmental problems the world faces, it is crucial to motivate owning families to spend more resources on CSR activities helping to avoid or overcome those problems and compensate for any damages incurred while conducting their business. Thus, lobbies and regulating authorities, be they local or governmental, should consider how to encourage companies—family-owned or not—to behave with CSR and pursue ways and means to not only enhance their business, reputations, and profits but to behave in an ethical, sustainable manner at the same time.

Since the analysis of the research literature shows that family firms are more sensitive to contextual factors than non-family firms, more regulations for CSR activities can generate positive effects for society as a whole and for the family firm itself. In particular, CSR activities directly related to business (i.e., economic-related CSR) can benefit the firm. Whether a family firm or non-family firm and regardless of the positive effect of family influence and the motivation behind conducting the CSR activities, our study shows and research literature agrees that conducting CSR is a wise and far-sighted move for a company and a functional strategic tool a company can use to engender long-term profitability.

Limitations

Following Tranfield et al.’s (2003) systematic literature review approach has helped us to expand the field of research, even if also accompanied by certain limitations. When using a selection of databases, there is the possibility that not all relevant papers have been considered. However, this limitation is counterbalanced partly by the detailed database description, making the analysis more comprehensible. Despite our systematic approach to searching and analyzing relevant publications, subjectivity cannot be entirely excluded. Nonetheless, this subjectivity has also helped us to identify lacuna and proffer essential questions, which we hope will open up future research on CSR in family firms. Also, we limited our literature search specifically to family firms. It is possible that there is research in the field of family science that further explores the effects between family and firm, as well as CSR activities, and that this review has not considered. Additionally, our chosen theoretical framework may impact the analysis and evaluation of the articles consulted. Accordingly, we clarified our basis of interpretation by explaining the theory and the underlying mechanism in detail.

Quantitative empirical approaches dominate research activities on CSR in family firms. To develop family firm-specific explanatory approaches for the influence of the family on firm antecedents and the function of translation from drivers to outcomes and the emerging dynamics, we encourage subsequent research to draw more on qualitative empirical research in the form of case studies and experiments for example (De Massis & Kotlar, 2014; Lude & Prügl, 2021). In particular, as research in family-owned SMEs is still under-represented (Miller & Le Breton-Miller, 2007), this approach should be conducted within family-owned SMEs. Research in the field of large companies cannot be transferred one-to-one to SMEs (Faller and zu Knyphausen-Aufseß, 2018; Uhlaner et al., 2012), as the involvement and integration of the family are different (Miller & Le Breton-Miller, 2007), leading to a different use of resources as well as goals (Block & Wagner, 2014b; Niehm et al., 2008). Qualitative empirical research could help fathom the underlying motivations of family firms concerning CSR outcomes. We also propose that such research focus more on the role of the owning family and its members. Research considering this could break down the current barriers of the research field and develop it further.

Conclusion

We postulate that research on CSR outcomes is necessary to evaluate the effectiveness of family and firm antecedents. It can also provide further insight into the unity of the family and the firm, especially its use of resources to achieve specific goals. These results lead to a better understanding of the heterogeneity of family firms. Likewise, in future research, these approaches can be applied to non-family firms since, here, managers have a connection to the firms and can help determine the firm’s success through their use of resources such as social and human capital, which in turn enhances their reputation. With this literature review, we want to motivate researchers to continue looking at CSR from different perspectives.

References

Abeysekera, A. P., & Fernando, C. S. (2020). Corporate social responsibility versus corporate shareholder responsibility: A family firm perspective. Journal of Corporate Finance, 61, 101370.

Adams, J. S., Taschian, A., & Shore, T. H. (1996). Ethics in family and non-family owned firms: An exploratory study. Family Business Review, 9(2), 157–170.

Adomako, S., Amankwah-Amoah, J., Danso, A., Konadu, R., & Owusu-Agyei, S. (2019). Environmental sustainability orientation and performance of family and nonfamily firms. Business Strategy and the Environment, 28(6), 1250–1259.

Agostino, M., & Ruberto, S. (2021). Environment-friendly practices: Family versus non-family firms. Journal of Cleaner Production, 329, 129689.

Aguinis, H., & Glavas, A. (2012). What we know and don’t know about corporate social responsibility: A review and research agenda. Journal of Management, 38(4), 932–968.

Ahmad, S., Siddiqui, K. A., & AboAlsamh, H. M. (2020). Family SMEs’ survival: The role of owner family and corporate social responsibility. Journal of Small Business and Enterprise Development, 27(2), 281–297.

Amann, B., Jaussaud, J., & Martinez, I. (2012). Corporate social responsibility in Japan: Family and non-family business differences and determinants. Asian Business & Management, 11(3), 329–345.

Amidjaya, P. G., & Widagdo, A. K. (2020). Sustainability reporting in Indonesian listed banks: Do corporate governance, ownership structure and digital banking matter? Journal of Applied Accounting Research, 21(2), 231–247.

Antheaume, N., Robic, P., & Barbelivien, D. (2013). French family business and longevity: Have they been conducting sustainable development policies before it became a fashion? Business History, 55(6), 942–962.

Aragón-Amonarriz, C., Arredondo, A. M., & Iturrioz-Landart, C. (2019). How can responsible family ownership be sustained across generations? A family social capital approach. Journal of Business Ethics, 159(1), 161–185.

Arena, C., & Michelon, G. (2018). A matter of control or identity? Family firms’ environmental reporting decisions along the corporate life cycle. Business Strategy and the Environment, 27(8), 1596–1608.

Association of Business Schools. (2021). Academic journal guide. Chartered Association of Business Schools.

Astrachan, J. H., Astrachan, C. B., Campopiano, G., & Baù, M. (2020). Values, spirituality and religion: Family business and the roots of sustainable ethical behavior. Journal of Business Ethics, 163(4), 637–645.

Ballantyne, J. C., & Loeser, J. D. (2021). Empire of pain: The secret history of the Sackler dynasty. Anesthesiology, 135(6), 1166–1167.