Abstract

This paper applies the meta-frontier Data Envelopment Analysis and the main concepts of convergence from the economic growth literature (β-convergence and σ-convergence) to analyze integration and convergence both in efficiency and in technology gap of European Union (EU) insurance markets. We evaluate 10 EU life insurance markets over the 17-year-period 1998–2014. Results show convergence in cost/revenue efficiency among major EU life insurance markets during the sample period. These findings indicate that the least efficient countries in 1998 have shown a higher improvement in cost/revenue efficiency than the most efficient countries in the same year as well as that the dispersion of the mean efficiency scores among EU life insurance markets decreased over the sample period. We also find convergence in cost/revenue technology gap among these markets, suggesting that they become more technologically homogeneous during the sample period. However, results show that the global financial crisis has led to a slowdown in the progress of integration and convergence in efficiency and technology gap of EU life insurance markets in terms of cost efficiency but not in terms of revenue efficiency.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Important steps have been taken over the recent decades to foster integration in European Union (EU) financial services markets in order to build EU single markets in providing banking, insurance and other financial services (see e.g. Swiss Re, 1996; ECB, 2011, 2020). Financial integration is expected to favor competition and efficiency on financial markets, which results in price reductions in financial services leading to direct gains for consumers but also for firms since the sharing of best management practices among financial institutions is one of the forms of financial integration (see e.g. Berger, 2003; Cummins & Rubio-Misas, 2006; Casu et al., 2016). It is therefore of utmost interest to investigate whether financial integration has taken place in the EU especially when a current debate exists on further EU financial integration.

To provide evidence of this topic, researchers have analyzed convergence in efficiency across EU financial markets based on the idea that the definition of financial integration is closely related to the law of one price, which states that if financial services have identical risks and returns, they should be priced identically regardless of where they are traded (see e.g. Weill, 2009; Casu & Girardone, 2010). Most papers on convergence in efficiency across EU financial services markets have performed the efficiency analysis on a common frontier technology, assuming that the EU offers a homogeneous production environment for financial services, with exceptions in banking such as Casu et al. (2016). However, EU countries show heterogeneity in terms of economic environment as well as other legal, cultural and institutional factors, which may need to be taken into account in estimating efficiency. In addition, most analyses on convergence in efficiency across EU financial services markets have focused on the banking industry (see e.g. Weill, 2009; Casu & Girardone, 2010; Matousek et al., 2015; Casu et al., 2016; Tziogkidis et al., 2020) and only Giantsios and Noulas (2020a, 2020b) have analyzed convergence in efficiency of European insurance markets although they did not consider that European countries are heterogeneous.Footnote 1

This paper comes to solve this lack of literature by addressing the extant heterogeneity among EU countries and analyzing integration and convergence both in efficiency and in technology gap of 10 EU life insurance markets over the period 1998–2014, a period including the global financial crisis that may have influenced the progress of integration. We gauge cost and revenue efficiencies of firms operating in 10 EU national life insurance markets for the period from 1998 to 2014 by applying the meta-frontier data envelopment analysis (DEA) approach (see O’Donnell et al., 2008). The meta-frontier framework implies a common frontier which envelops the frontiers of all countries. Thus, efficiencies measured relative to the meta-frontier can be decomposed into two components: a component that measures the distance of the firm to the country-specific frontier; and a component that measures the distance between the country’s frontier and the meta-frontier, named meta-technology efficiency ratio. The meta-frontier framework involves accounting for the presence of heterogeneity in production possibility sets among groups.Footnote 2

After asserting the suitability of the meta-frontier DEA approach to estimate efficiency in our data set, we conduct a comprehensive analysis of whether a process of integration has taken place in EU life insurance markets during the sample period. In doing so, we focus on two key components that the meta-frontier DEA framework provides: meta-frontier efficiency scores and meta-technology efficiency ratios. The first component is used to evaluate whether EU life insurance markets converge in efficiency during the sample period. The second one allows analysing whether EU life insurance markets have become more technologically homogeneous during the sample period. That is, since we observe technological heterogeneity across the analysed EU life markets and address this heterogeneity by using the meta-frontier DEA framework, we argue that a suitable analysis of whether a process of integration has taken place over the sample period should evaluate not only convergence in efficiency across EU life insurance markets, but also convergence in technology gap across them. Then, the analysis of convergence in technology gap across EU life insurance markets constitutes an innovative application of the meta-frontier DEA framework to evaluate integration of EU life insurance markets.

The analysis of convergence (both in efficiency and in technology gap) of EU life insurance markets is conducted in a second stage by using two major concepts of convergence from the economic growth literature (see Barro & Sala-i-Martin, 1995): the β-convergence (which captures the catch-up effect) and the σ-convergence (which captures the speed of convergence). Therefore, this study aims to answer the following main questions: (1) Do EU life insurance national markets converge in cost and revenue efficiency during the sample period? (2) Do EU life insurance markets become more technologically homogeneous over the sample period? (3) Has the global financial crisis led to a slowdown in the progress of integration of EU life insurance markets?

To sum up, this paper belongs to the growing literature on DEA applications in the insurance industry by using the meta-frontier DEA approach in analysing integration and convergence in efficiency and technology gap of EU life insurance markets.Two are the main contributions of this article to literature: (1) The first to apply the meta-frontier DEA cost/revenue efficiency scores (meta-technology DEA cost/ revenue efficiency ratios) to evaluate convergence in efficiency (technology gap) of financial services marketsFootnote 3; and (2) the first to analyze integration and convergence in technology gap of EU insurance markets. As previously stated, most analyses on convergence in efficiency in EU financial services markets use efficiency scores resulting from a common or pooled frontier (see e.g., Weill, 2009; Casu & Girardone, 2010) and to the best of our knowledge only Casu et al. (2016) use a parametric (our analysis is a non-parametric approach) meta-frontier Divisia index to estimate convergence in productivity (our analysis focuses on the cost and revenue efficiency analyses and studies not only convergence in efficiency but also convergence in technology gap).

The remainder of the paper is organized as follows. Section 2 presents theoretical background and formulates hypotheses. Section 3 describes the sample and defines outputs, inputs, prices and estimation methodology. The results are presented in Sects. 4 and 5 concludes.

2 Theoretical background and hypotheses formulation

As we exposed above, over the recent decades, important steps have been taken to promote integration in European insurance markets. The first step started with deregulation policies such as the 1994 Third Generation Insurance Directives. The main objective of these Directives (Directives 1992/49/EC and 1992/96/EC for non-life and life insurance, respectively) was to increase competition in European insurance markets both within and across national boundaries by removing entry barriers. They basically implied the establishment of a single EU license such that an insurer could operate in the EU by obtaining a license from only one national EU regulator rather than being licensed in each member nation. They also introduced the home country supervision principle, which means that the insurer is supervised only by the nation that issued its licence. The Directives also abolished several important areas of insurance supervision, deregulating pricing, contracting, and other insurance operations, and focusing regulation on solvency control. This set of regulatory rules was expected to transform the EU life insurance industry into a more competitive and efficient market, increasing consumer choice and reducing prices (see Swiss Re, 1996; Cummins & Rubio-Misas, 2006). Another step taken towards an integrated European life insurance market was the introduction of the Euro in 1999. The creation of the single currency removed the exchange risk for insurers in cross-border acquisitions and in the supply of cross border services. Afterwards, the EU issued new Directives for life and non-life insurers (Directives 2002/83/EC and 2002/13/EC) to implement standardized solvency requirements. Later, Solvency II Directive (Directive 2009/138/EC) was approved. These supervisory Directives as well as other technical Directives issued by the EU during the sample period aimed to reinforce, directly or indirectly, the single market in insurance and promote integration.

Nevertheless, despite the regulatory efforts of the European Union to attain a fully integrated European insurance market, many differences among countries in terms of legal system, language and institutional and cultural characteristics continue to exist. In addition, EU countries retain the right to tax differently. Consequently, EU countries do not seem to offer a homogeneous production environment for life insurance products. Considering overall the aforementioned reasoning, we first argue that life insurers located in different countries face different production possibility sets due to differences in the production environment, which also results in country differences in efficiency. Then, one may think that EU life insurers do not operate under a single frontier technology and that estimating efficiency of EU life insurers by the meta-frontier DEA approach would be appropriate. Evaluation results of decision-making units ignoring technical heterogeneity could be biased.

Under the meta-frontier DEA approach, efficiency is measured by a country frontier defined as the boundaries of restricted production possibility sets and by a meta-frontier defined as the boundaries of unrestricted production possibility sets (see O’Donnell et al., 2008). Since the use of the meta-frontier approach is justified if there is heterogeneity in the production environment, we first ascertain whether the DEA meta-frontier methodology is appropriate in our data set. In doing so, we test, by applying the Kruskal–Wallis test (see e.g. Rahman et al., 2019 for a similar procedure), whether there are statistically significant differences in the efficiency relative to the meta-frontier among the analysed EU countries. Results from this test (see Table 2), which are further discussed in Sect. 4, confirm the existence of heterogeneity among production possibility sets and the suitability of the meta-frontier DEA framework for our dataset. Therefore, we develop test procedures to evaluate integration in EU life insurance markets on the base of the meta-frontier DEA framework.

Theoretically, the aim of EU insurance integration should be similar to the convergence towards the law of one price, which states that all firms should charge the same prices for similar products independently of the country where they are traded. To reach the objective of the law of one price, convergence in cost efficiency of European insurers is required because differences in insurance costs prevent insurance prices from converging (see e.g. Weill, 2009; Casu & Girardone, 2010). In addition, we argue that if insurance prices converge, we could also expect convergence in revenue efficiency. Consequently, our analysis of integration of EU life insurance markets focuses not only on cost efficiency but also on revenue efficiency. Therefore, it provides a comprehensive picture of insurers’ performance, since, according to traditional microeconomic theory, firms are profit maximizers by minimizing costs and maximizing revenues (see Cummins & Weiss, 2013).

In order to test convergence in efficiency of EU life insurance markets we borrow two major concepts of convergence from the growth literature: the β-convergence and the σ-convergence proposed by Barro and Sala-i-Martin (1995) and the specification for panel data (see Canova & Marcet, 1995; Parikh & Shibata, 2004; Weill, 2009). In this context, β-convergence means that countries with initial lower levels of insurance efficiency have faster growth rates than countries with higher initial levels of insurance efficiency. Then, β-convergence captures the catch-up effect. And σ-convergence appears if each country’s level of insurance efficiency is converging to the average level of the group of countries. Therefore, it captures the speed of convergence. These arguments lead to the following hypotheses:

H1

We will observe β-convergence in cost and revenue efficiency (measured relative to the meta-frontier) in European life insurance markets.

H2

We will observe σ-convergence in cost and revenue efficiency (measured relative to the meta-frontier) in European life insurance markets.

The fact that the meta-frontier approach is appropriate for our analysis indicates that EU life insurers do not operate under a single frontier technology and that the technologies of the different EU countries in producing life insurance products are heterogeneous. Therefore, we argue that, if a process of EU life insurance integration has taken place during the sample period, we may expect that EU life insurance markets have become more homogeneous. As we stated above, the meta-frontier framework allows the efficiency measured relative to the meta-frontier to be divided into a component that measures efficiency relative to the own-country frontier and a component that measures the meta-technology cost/revenue efficiency ratio or technology gap, which is the reciprocal of the distance between the country frontier and the meta-frontier.

If European life insurance markets have become more homogeneous over our sample period, we expect a decrease in the distances between the country frontiers and the meta-frontier and consequently we expect an increase in meta-technology cost/revenue efficiency ratios as well as a decrease in the spread of these ratios. Considering the concepts of β-convergence and σ-convergence in this context, β-convergence would imply that countries with lower initial levels of meta-technology cost/revenue efficiency ratios (i.e., technologies that depart further from the technology of the meta-frontier) have shown faster technology growth than countries with higher initial levels of meta-technology cost/revenue efficiency ratios. And σ-convergence appears if each country’s level of meta-technology cost/revenue efficiency ratio is converging to the average level of the group of countries. Accordingly, we hypothesize:

H3

We will observe β-convergence in the meta-technology cost/revenue efficiency ratios in European life insurance markets.

H4

We will observe σ-convergence in the meta-technology cost/revenue efficiency ratios in European life insurance markets.

Nevertheless, despite the important steps taken to promote EU insurance integration, the global financial crisis has had a severe impact on the European economy and may have had a negative impact on integration. The global financial crisis has exerted a heterogeneous and asymmetric impact across European countries (Hristov et al., 2012). For instance, countries with a great dependence on external funds and especially on short-term debt markets were strongly affected by the global financial crisis (Milesi-Ferretti & Tille, 2011). So the global financial crisis appears, in fact, to have contributed to a leveraging of the existing differences and fragmentation between countries in Europe (Degl’Innocenty et al., 2017; Matousek et al., 2015). Consequently, the adverse developments and events associated with the global financial crisis may have impacted on insurers’ efficiency and harmed the process of integration as some countries were more vulnerable than others. We argue that the most vulnerable EU life insurance markets for the financial crisis were probably the ones that presented lower levels of efficiency and this fact may have negatively affected the process of integration in terms of β-convergence both in efficiency and technology gap. In addition, since the global financial crisis has impacted EU countries in a heterogeneous and asymmetric way, the process of integration in terms of σ-convergence, both in efficiency and technology gap, may also have been negatively affected. For these reasons, we also state the following general hypothesis:

H5

The financial crisis has led to a slowdown in the progress of integration of European life insurance markets.

3 Data and methodology

3.1 Data sources

The sample comprises an unbalanced panel of life insurers from 10 EU countries spanning the period from 1998 to 2014. This period is particularly appropriate for the analysis conducted in this paper in view of the events that have taken place during this long period of time. It covers not only the post-deregulation years as a consequence of policies such as the Third Generation Directives, but also the introduction of the Euro as well as steps to standardize solvency requirements and harmonize insurance regulation among countries since Solvency II Directive (2009/138/EC) was approved in December 2009. The fact that it encompass a seventeen-year sample period is especially suitable because the integration of financial services markets tends to be a slow-moving process (ECB, 2017). We selected the countries based upon the length of time they have been in the EU and also on considerations of data availability.Footnote 4 Annual financial statements were obtained from the Orbis Insurance Focus dataset provided by Bureau van Dijk to construct the relevant variables of interest.Footnote 5 For each insurer, we use reports prepared under International Financial Reporting Standards/International Accounting Standards (IFRS/IAS) where they exist, otherwise we use reports prepared under local generally accepted accounting principles. Consolidated data are used for groups of insurers and unconsolidated data for unaffiliated single insurance companies. Unaffiliated insurers are associated to the country where they are domiciled. Group of insurers are linked to the country where the group is domiciled, although subsidiaries domiciled in different countries from the group may belong to a group. All monetary variables are expressed in millions of euros and deflated by the country-specific consumer price index (CPI) to the base year 2000. Country-specific CPIs are obtained from the International Labor Organization (ILO). The final sample is a result of a series of screening tests. Non-viable firms such as firms with non-positive incurred benefits, invested assets, equity capital, total debt, net premiums or operating expenses were eliminated. The final sample includes a total of 8594 year-firm observations.

3.2 Outputs, inputs, and prices

In line with most studies of efficiency in insurance, we use a modified version of the value-added approach to measure insurance outputs and inputs (e.g. Altuntas et al., 2021; Cummins & Weiss, 2013; Eling & Jia, 2019). Most of the existing studies recognize that risk-pooling and risk bearing services, real financial services related to insured losses and intermediation services are the three main services in creating value for insurers (Cummins & Weiss, 2013). A satisfactory proxy for the amount of risk pooling/bearing and real insurance services provided by life insurers is given by the value of real incurred benefits plus addition to reserves (see e.g. Cummins et al., 1999a, 1999b; Cummins & Weiss, 2013; Rubio-Misas, 2022). The output variable which proxies for the intermediation function is the real value of invested assets, the value of assets under management (see e.g. Cummins & Weiss, 2013; Eling & Jia, 2018). Life insurers provide savings and retirement vehicles, so they provide the intermediation function to a higher degree than non-life insurers. The price of the insurance output (\(p_{IB}\)) is defined as \(p_{IB} = (P - IB)/IB \) where \(P\) expresses the premiums; and \(IB\) denotes the value of real incurred benefits plus addition to reserves. For the price of the invested assets output, we utilize the ratio of net investment income to invested assets.

According to the valued-added approach, insurers use three primary inputs: labour, material and business services, and capital (see Cummins & Weiss, 2013). Due to data availability (the number of employees or hours worked per firm and year as well as appropriate indicators to be used as a price of the material and business service input were not available), we combine labor input and materials and business services input to make another input category constructed from the operating expenses category. This combination is commonly used in other international insurance efficiency studies (see e.g. Fenn et al., 2008). Operating expenses includes claims handling expenses, commission expenses, management expenses as well as expenses from investment management. We follow previous research (e.g. Cummins Rubio-Misas & Zi, 2004; Cummins et al., 1999a, 1999b; Rubio-Misas, 2022) and measure the quantity of the operating expenses input by dividing operating expenses by the wage rate used as a price of this input. The other two inputs used in this study, which are standard in research on insurer efficiency, are debt capital and equity capital. Debt capital is calculated as the sum of net loss reserves, net unearned premium reserves, other technical reserves, and total other liabilities (borrowed money). Equity capital is defined as the policyholders’ surplus.

As a proxy for the price of the operating expenses input we use an index based on the wages and salaries of the industry and services for each year and country of the sample period provided by Eurostat. We use the 10-year Treasury Bill rates for each year and country of the sample period provided by the OECD Economic Outlook database as a proxy for the price of debt capital. The price of equity capital is calculated by using the 20-year rolling average of the yearly rates of total return of the country specific MSCI stock market indices (see e.g. Eling & Schaper, 2017).

3.3 Methodology

3.3.1 Efficiency methodology: the DEA meta-frontier and group (country) frontiers

We measure cost and revenue efficiency for each firm in the sample relative to “best practice” cost and revenue frontiers, respectively, consisting of the most efficient firms in the industry. Firms on the frontiers have efficiency scores of one and firms not on the frontiers have efficiency scores between zero and one. For estimating efficient frontiers, we use data envelopment analysis (DEA) which is a non-parametric frontier approach (see e.g. Cooper et al., 2011). In calculating efficiency using DEA, it is necessary to adopt an orientation. In this paper, we utilize input-oriented DEA to estimate cost efficiency and output-oriented DEA to estimate revenue efficiency (see e.g. Cummins et al., 2010; Altuntas et al., 2021; Rubio-Misas, 2022). The choice of input versus output orientation for our efficiency analysis is based on the microeconomic theory of the firm. In microeconomic theory, the objective of the firm is to maximize profits by minimizing costs and maximizing revenues. Cost minimization involves choosing the optimal quantities of inputs to produce a given output vector (i.e., minimizing costs conditional on outputs), and revenue maximization involves choosing the optimal quantities of outputs conditional on the input vector (i.e., maximizing revenues conditional on inputs). This paper adopts the meta-frontier approach suggested by O’Donnell et al. (2008) for estimation of meta-frontier and group-frontier (country-frontier) efficiencies.Footnote 6 The construction of separate country frontiers makes sense when hypothesizing the presence of heterogeneity in production possibility sets among countries. That is, when the evaluation process is performed in a non-unified environment (see e.g., Cheng et al., 2020; Liu et al., 2020a, 2020b; Yu & Chen, 2020).

Suppose producers use input vector \( x = \left( {x_{1} ,x_{2} , \ldots x_{L} } \right)^{\prime } \in R_{ + }^{L}\) to produce output vector \(y = \left( {y_{1} ,y, \ldots y_{M} } \right)^{{\prime }} \in R_{ + }^{M}\) where L is the number of inputs and M is the number of outputs. The meta-technology set contains all input–output combinations that are technologically feasible and is represented as:

The universe of producers can be divided into K groups (in our case K countries). Then the country-specific technology can be represented by:

We assume that T and \(T^{k}\) are convex and satisfies some common properties of production technologies. The input set associated with the meta-technology set is defined as:

and the input set associated to the country k technology, \(V^{k} \left( y \right)\), is defined similarly. These input sets are assumed to satisfying the standard regularity conditions in Färe and Primont (1995). We refer to the boundary of these input sets as the input meta-frontier and the input country-specific frontier, respectively. The input-oriented meta-distance function associated with the input meta-frontier is given by:

and de input-oriented country k specific distance function, \(D_{I}^{k} \left( {x,y} \right)\), is defined similarly. The distance function gives the smallest amount by which a producer can radially contract its input vector, given an output vector. \(D_{I} \left( {x,y} \right)\) is interpreted intuitively as the distance of a given firm's input–output vector \(\left( {x,y} \right)\) from the meta-frontier. The operating points of fully efficient firms, \(D_{I} \left( {x,y} \right) = 1\), lie on the meta-frontier, indicating that they operate with the minimum amount of inputs needed to produce their quantity of output. Inefficient firms, with \(D_{I} \left( {x,y} \right) > 1,\) indicate that they could reduce their input consumption while producing the same quantity of output if they operated on the meta-frontier. Similar interpretation applies for \(D_{I}^{k} \left( {x,y} \right)\) which is analyzed with respect to the country-specific frontier.

The input distance function is the reciprocal of the minimum equi-proportional contraction of the input vector x, given outputs y, i.e., input-oriented meta-frontier technical efficiency \(TE_{I} \left( {x,y} \right) = 1/D_{I} \left( {x,y} \right)\), and input-oriented country-specific technical efficiency \(TE_{I}^{k} \left( {x,y} \right) = 1/D_{I}^{k} \left( {x,y} \right)\).

By explicitly modeling the economic objective of cost minimization, we can estimate the cost efficiency of each firm with respect to the meta-frontier as well as with respect to the country-specific frontier. When the economic objective is to minimize the costs of producing a given output vector, then economic cost efficiency is measured by the ratio of minimum possible cost to actual observed cost. If producers face input prices \(w = \left( {w_{1} ,w_{2} , \ldots w_{L} } \right)^{{\prime }} \in R_{ + + }^{L}\), the minimum cost meta-frontier is defined using the distance function approach as:

If country-specific producers face input prices \(w^{k} = \left( {w_{1}^{k} ,w_{2}^{k} , \ldots w_{L}^{k} } \right)^{{\prime }} \in R_{ + + }^{L}\), the minimum cost country-specific frontier is defined using the distance function approach as:

The optimal input vector \(x^{*}\) minimizes the costs of producing y given the input prices w, and the optimal input vector \(x^{*k}\) minimizes the costs of producing y given the input prices \(w^{k}\). Then metafrontier cost efficiency and country-specific cost efficiency are simply defined, respectively, as:

A measure of how close the country k cost frontier is to the cost meta-frontier can also be obtained by calculating the ratio of the meta-frontier cost efficiency to the country cost efficiency. We named this ratio the meta-technology cost efficiency ratio (henceforth MCER) which has a value between zero and one. As much closer country k cost frontier is to the meta-frontier the meta-technology cost efficiency ratio would be closer to one. MCER means that given the output vector, the minimum costs that could be attained by a firm from the k country is a (1-MCER)% more than the costs which is feasible under the cost meta-frontier.

We illustrate this analysis in Fig. 1 for an economy where each firm uses two inputs (X1 and X2) with input prices (W1 and W2) to produce a single output (Y). The convex production frontier (a–a′) is the isoquant obtained from country a’s data, the convex frontier (b–b′) is the isoquant obtained from country b’s data, and so on. Thus (a–a′), (b–b′), and (c–c′) are all country-specific frontiers. The isoquant represents the best production technology for the respective country, i.e., firms operating on the isoquant are on the production frontier and are fully technical efficient. The convex frontier, (M–M′), which envelops all those country-specific frontiers is called meta-frontier. In Fig. 1, the meta-frontier (M–M′) is a convex combination of country-specific frontiers (a–a′) and (c–c′), and the frontier (b–b′) is not a part of the meta-frontier (so (b–b′) is not tangent to (M–M′)).

Meta-frontier cost efficiency and meta-technology cost efficiency ratio. Efficiencies for firm operating at point A belonging to country b: Country-specific cost efficiency = OB/OA. Meta-frontier cost efficiency = OC/OA. Meta-technology cost efficiency ratio = OC/OB = (OC/OA)/(OB/OA)

Denote W1–W2 and W′1–W′2 as the price lines tangent (i.e., the isocost lines) to production frontiers M–M′ and b–b′, respectively. Then the country-specific cost efficiency for a firm operating at point A belonging to country b is obtained by the ratio of OB/OA, and the meta-frontier cost efficiency for the same firm is obtained by the ratio of OC/OA. Since OC/OA is less than OB/OA in Fig. 1, the ratio of the meta-frontier cost efficiency to the country-specific cost efficiency, OC/OB, is also less than one. This ratio (OC/OB) is a measure of how close the country b cost frontier is to the cost meta-frontier for the firm operating at point A. We call this ratio the meta-technology cost efficiency ratio (MCER) and it seems clear that, given that the meta-frontier envelops the country-specific frontier, it has to be less than or equal to one. The closer a country-specific frontier is to the meta-frontier, the closer is MCER to one.

In addition to studying cost efficiency, we analyze revenue efficiency. Revenue maximization involves choosing the optimal amounts and combinations of outputs conditional on the input vector. Hence revenue efficiency provides complementary information to the analysis of cost efficiency because the only way to tell whether policies taken in the EU for integration have met with ultimate success is to measure its effects on revenue or profit efficiency (Cummins & Weiss, 2013). The analysis with respect to revenue efficiency is directly analogous to the cost efficiency case and thus is not presented in detail. The primary differences are that it adopts an output-oriented approach to maximize revenues and that the optimal operating points would be determined by the tangency of iso-output-price lines and production possibilities curves (see e.g. Lovell, 1993). Revenue efficiency is defined as the ratio of the revenues of a given firm to the revenues of a fully efficient firm with the same input vector and output prices. We measure revenue efficiency of a given firm with respect to the meta-frontier as well as its revenue efficiency with respect to the country-specific frontier. The firm’s meta-technology revenue efficiency ratio (MRER) is obtained as the ratio of the meta-frontier revenue efficiency to the country revenue efficiency.

3.3.2 Models for cost/revenue efficiency and MCER/MRER convergence

To investigate the convergence of meta-frontier cost/revenue efficiency as well as the convergence of MCERs/MRERs in life insurance markets across the EU countries and over the sample period, we utilize the two well-known concepts of convergence, β-convergence and σ-convergence proposed by Barro and Sala-I-Martin (1995).

To perform the β-convergence test, we employ in a second stage the following model, which is similar to the specification for panel data from Canova and Marcet (1995) and Weill (2009)Footnote 7:

where \(V_{i,t} \) is the mean metafrontier cost/revenue efficiency of the life insurance industry of country i at year t; \(V_{i,t - 1}\) is the mean metafrontier cost/revenue efficiency of the life insurance industry of country i at year t-1; \(\Delta V_{i,t} = ln\left( {V_{i,t} } \right) - ln\left( {V_{i,t - 1} } \right)\); \(D_{i}\) country dummies; \(\alpha ,\) \(\beta , \gamma , \delta\) are parameters to be estimated; \(\varepsilon_{i,t}\) is the error term;;\( i = 1, 2, \ldots I\) and \(t = 1, 2, \ldots T\).Footnote 8 The equation is estimated with and without the lagged dependent variable \(\Delta V_{i,t - 1}\).The parameter \(\beta\) captures the catch-up effect and a negative value of \(\beta \) implies convergence.

To estimate the cross sectional dispersion or σ-convergence we use the following model used in Parikh and Shibata (2004) and Weill (2009):

where \( W_{i,t} = \ln \left( {V_{i,t} } \right) - ln\left( {\overline{{V_{t} }} } \right)\);\( W_{i,t - 1} = \ln \left( {V_{i,t - 1} } \right) - ln\left( {\overline{{V_{t - 1} }} } \right)\);\( \Delta W_{i,t} = W_{i,t} - W_{i,t - 1} \);\( V_{i,t}\),\( V_{i,t - 1}\),\( D_{i}\) are defined as before; \(\overline{{V_{t} }} \) and \(\overline{{V_{t - 1} }}\) are the mean metafrontier cost/revenue efficiencies of the EU life insurance industries used in this study at year t and t-1, respectively; \(\alpha ,\) \(\sigma ,\) \(\rho ,\) \(\delta\) are parameters to be estimated; \(\varepsilon_{i,t}\) is the error term;\( i = 1, 2, \ldots I\) and \(t = 1, 2, \ldots T.\) The equation is also estimated with and without the lagged dependent variable \(\Delta W_{i,t - 1}\). The negative value of the coefficient \(\sigma\) captures the rate of convergence of \(V_{i,t}\) toward the EU average cost/revenue efficiency. The larger the absolute value of \(\sigma\), the faster the rate of convergence. We also evaluate the two convergence equations for meta-technology cost/revenue efficiency ratios.

4 Results and discussion

This section presents and discusses our empirical results. As we stated above, bearing in mind that we consider a period of financial crisis, we also aim to provide evidence regarding the influence of the financial crisis on the integration and convergence in efficiency and technology gap of European life insurance markets.

4.1 Efficiency results

Summary statistics on outputs, inputs, prices and several firm characteristics are shown in Table 1. The table presents averages for the whole sample period (1998–2014) as well as averages for the pre-crisis (1998–2007) and the post-crisis (2008–2014) period. The last column reports differences in mean values between the post- and pre-crisis period. Figures indicate that on average the mean quantities of outputs and inputs are higher in the post-crisis than in the pre-crisis period. These differences are in line with the insurer size (measured as total assets) that was on average higher in the post-crisis than in the pre-crisis period. The increase of the EU life insurer size may be basically due to the consolidation activity that took place over the sample period in EU life insurance markets (see e.g. Swiss Re, 2015).

In order to provide support to the use of the meta-frontier framework in our dataset, Table 2 shows the Kruskal–Wallis test results that were performed to ascertain whether the differences among the country efficiency scores were statistically significant relative to the meta-frontier. The null hypothesis tested is that the mean rank is the same in all countries, which, as expected, is rejected at a 1% level of significance for both the meta-frontier cost efficiency and the meta-frontier revenue efficiency. Consequently, these results support the presence of heterogeneity in production possibility sets among countries.

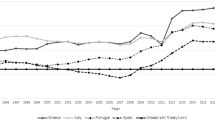

The average cost efficiency results for the whole sample period as well as for the pre-crisis and the post-crisis period in life insurance for the countries in our sample are plotted in Fig. 2. The results are shown for cost efficiencies measured relative to meta-frontier (Panel A) as well as meta-technology cost efficiency ratios (Panel B).Footnote 9 The average meta-frontier cost efficiency scores for the 10 EU life insurance markets over the whole sample period is 0.588, indicating a 41.2% potential reduction in cost on average. As a whole, considering all the observations on the 10 EU countries, the results indicate no differences on average in meta-frontier cost efficiency between the pre- and the post-crisis periods. However, the analysis by country shows that on average the meta-frontier cost efficiency is lower in 3 out of 10 countries in the post- than in the pre-crisis period.

Cost efficiency scores of European Life Insurers, 1998–2014. Note: This figure plots the average values for the whole, 1998–2007 (pre-crisis) and 2008–2014 (post-crisis) period for every of the 10 countries of the sample as well as across the 10 EU countries. Differences in mean values between the 2008–2014 and 1998–2007 period were calculated. *** and * represent countries where these differences are statistical significance at 1% and 10% level, respectively

The MCERs allow us to evaluate the closeness of country cost frontiers to the cost meta-frontier. The average MCER for the 10 EU life insurance industries over the sample period is 0.918, which is relatively closer to 1, indicating that in general the country-specific cost frontiers are close to the European life cost meta-frontier. Sweden is the country that shows on average the biggest technology gap (0.666) while the UK (0.977), Germany (0.967), and Spain (0.911) show lower technology gaps between country-specific life cost frontier and the European life cost meta-frontier. We also observe that considering all the observations across the 10 EU countries there are not differences on average in MCERs between the pre- and the post-crisis period. However, the analysis by country show that in 5 (2) countries MCERs are on average lower (higher) in the post- than in the pre-crisis period.

The average revenue efficiency results in life insurance for all 10 EU countries of our sample are plotted in Fig. 3. Panel A shows meta-frontier revenue efficiency scores, and Panel B MRERs. We present results for the whole sample period, the pre- and post-crisis period. The average meta-frontier revenue efficiency scores for the 10 EU life insurance industries over the sample period is 0.166 indicating a 83.4% potential increase in revenues on average. This figure is considerably low relative to cost efficiency (0.588), indicating that on average EU life insurers are more cost efficient than revenue efficient. The average meta-frontier revenue efficiency scores across the 10 EU countries for the pre- and the post-crisis period were 0.149 and 0.187, respectively. This difference is statistically significant and suggests that for the 10 EU countries as a whole meta-frontier revenue efficiency was on average higher in the post-crisis period than in the pre-crisis period. This finding is generally supported in the analysis by country—7 out of 10 countries show an increase in meta-frontier revenue efficiency in the post-crisis period compared to the pre-crisis period.

Revenue efficiency Scores of European Life Insurers, 1998–2014. Note: This figure plots the average values for the whole, 1998–2007 (pre-crisis) and 2008–2014 (post-crisis) period for every of the 10 countries of the sample as well as across the 10 EU countries. Differences in mean values between the 2008–2014 and 1998–2007 period were calculated. ***, ** and * represent countries where these differences are statistical significance at 1%, 5% and 10% level, respectively

The average overall MRERs for the life insurance markets over the sample period is 0.553, indicating than in general the life country revenue frontiers are more distant from the life EU revenue meta-frontier than are the life country cost frontiers from the EU life cost meta-frontier. Austria is the country that shows on average the biggest technology gap (0.109) while Germany (0.830) and the UK (0.647) show lower technology gaps between the country-specific revenue frontier and the European revenue meta-frontier. We also observe an increase in MRERs on average in the post-crisis period compared to the pre-crisis period. This finding is also generally supported in the analysis of MRERs by country since 7 out of 10 life insurance markets show higher MRERs in the 2008–2014 period than in the pre-crisis period.

4.2 Convergence tests

In a second stage, we evaluate β-convergence and σ-convergence for the meta-frontier cost efficiency scores as well as for the meta-frontier revenue efficiency scores by estimating Eqs. (9) and (10).Footnote 10 We estimate these two equations with and without the lagged dependent variable. Additionally we tested whether our results are affected for the period since the financial crisis started. In doing so, we conducted analyses where we also include in the regressions an interaction term of a crisis dummy variable (1 for the years of the period 2008–2014) with the main explanatory variable (the coefficients of these interaction terms are called βcrisis and σcrisis, respectively). Models 2 (1) present the results where the interaction term is (is not) included.

The results of the β and the σ-convergence tests for the meta-frontier cost efficiency scores in EU life insurance are displayed in panel A of Table 3, while the results of the same tests for the meta-frontier revenue efficiency scores in EU life insurance markets are displayed in panel A of Table 4. Focusing first on Models 1, the results provide evidence for β-convergence in meta-frontier efficiency both in costs and revenues. The coefficient β is negative and significant in all tests. These results support hypothesis H1 and confirm that the least cost/revenue efficient countries in 1998 have shown a higher improvement in efficiency than the most efficient countries in 1998. Thus, these results provide evidence of efficiency catch-up among the 10 EU insurance markets over the period 1998–2014. Our results of the β-convergence test for revenue efficiency scores are in line with the ones obtained by Giantsios and Noulas (2020a) on European life insurers although they are not directly comparable, since they use the stochastic frontier analysis, do not take into account the presence of heterogeneity in production possibility sets among countries and refer to a different country sample and period of analysis.

The results from all the estimations of the σ-convergence in the meta-frontier efficiency scores (both in cost and in revenues) support hypothesis H2 and suggest that the dispersion of the mean efficiency scores among EU countries decreased during the sample period as the σ coefficient is always negative and statistically significant. The absolute value of the σ is larger in the meta-frontier cost efficiency analysis than in the meta-frontier revenue efficiency analysis, suggesting faster growth rate of convergence to the average in cost efficiency than in revenue efficiency in the EU life insurance markets during the sample period 1998–2014. This finding may be indicating that, in general, the competition in input prices in the EU life insurance markets during the sample period was higher than the competition in output prices.

Our findings on convergence in cost efficiency of EU life insurance markets are in some way in line with previous results on banking that usually show convergence in cost efficiency of EU banking markets (see e.g. Mamatzakis et al., 2008; Weill, 2009; Casu & Girardone, 2010).Footnote 11 Nevertheless, our particular results on the speed at which EU life insurance markets converged may not be directly comparable with the ones on the speed at which EU banking markets converged because they were estimated under different circumstances. Previous studies on banking remark that results on the speed at which EU banking markets converged in cost efficiency differ depending on factors such as the choice of a frontier efficiency technique (see e.g. Weill, 2009), the choice of a specification of inputs and outputs (see e.g. Weill, 2009) or the econometric model to calculate σ-convergence (see e.g. Casu & Girardone, 2010).

Focusing now on Models 2, results on convergence for the meta-frontier cost efficiency scores (see panel A Table 3) show that the coefficients β and σ are negative and significant but the coefficients of the respective interaction terms (βcrisis and σcrisis) are positive and significant. Since the coefficients of βcrisis and σcrisis are lower (in absolute value) than the respective coefficients β and σ, these results provide evidence of β-convergence and σ-convergence in meta-frontier cost efficiency scores over 1998–2007 as well as over 2008–2014, but suggest faster growth rate of convergence in meta-frontier cost efficiency during the pre-crisis period than over the period 2008–2014. These results support hypothesis H5. Related with this result, we can highlight previous finding in EU banking analyses. This way, Matousek et al. (2015) found that the global financial crisis had a negative impact on the banking integration process in 15 EU countries. Degl’Innocenty et al. (2017) found a consistent decline of bank productivity growth for 28 EU countries during the global financial crisis, but a strong convergence pattern mainly driven by the catch up process of some Eastern countries and the drop in performance of Western countries. Casu et al. (2016) found that bank productivity has slowed since the onset of the financial crisis.

The results on convergence for the meta-frontier revenue efficiency scores when the interaction term is included in the analysis (see panel A Table 4 Models 2) differ from the results with respect to the meta-frontier cost efficiency scores. In the revenue analysis, results show that the coefficient β is negative and significant but the coefficient βcrisis is not significant, indicating that the β-convergence results for the meta-frontier revenue efficiency scores were not affected for the post-financial crisis period. In addition, in the revenue analysis the coefficient σ appears negative and significant but the coefficient σcrisis was also negative and significant (although at 10% and 5% level, respectively, for the models without and with lagged dependent variable).

The results for the β-convergence and the σ-convergence for the meta-technology cost efficiency ratios and meta-technology revenue efficiency ratios in the EU life insurance industry are presented in panel B of Table 3 and panel B of Table 4, respectively. Recall that with the analysis of convergence in meta-technology cost/revenue efficiency ratios we want to test whether technologies of the EU life insurance markets converge. Focusing first on Models 1, our results provide evidence for β-convergence in MCERs as well as in MRERs in the life insurance segment over the period 1998–2014. These results suggest that countries having the biggest technology gap in 1998 with respect to the cost/revenue meta-frontier have shown a higher improvement in their technology than the countries having the lowest technology gap in the same year. Our results also provide evidence of σ-convergence in MCERs as well as in MRERs. These results confirm that both the dispersion of both the mean MCERs and the mean MRERs among EU countries decreased during the sample period. Therefore, these findings support hypotheses H3 and H4 and provide evidence that European life insurance markets have become more homogeneous over our sample period, indicating that a process of integration of EU life insurance markets has taken place.

Additionally we present in panel B (Table 3 Models 2) and panel B (Table 4 Models 2) results where the analysis includes the interaction term of the crisis dummy with the main explanatory variable. Results from this analysis with respect to the MCERs are similar to the obtained with respect to the meta-frontier cost efficiency scores in the sense that β and σ are negative and significant but the coefficients of the respective interaction terms (βcrisis and σcrisis) are positive (although lower in absolute value than the respective coefficient β and σ) and significant. These results indicate faster growth rate of convergence in MCERs during the pre-crisis period than over 2008–2014. However, since the results for the MRERs show that βcrisis is not statistically significant and σcrisis is significant only in one (at 10% level) of the two models, they do not seem to indicate that differences in β-convergence and the σ-convergence exist for the MRERs between the two periods considered (1998–2007 and 2008–2014) for the 10 analyzed EU life insurance markets.Footnote 12

Consequently, our findings show that the global financial crisis has led to a slowing down in the progress of integration and convergence in efficiency and technology gap of EU life insurance markets in terms of cost efficiency. However, in terms of revenue efficiency, the global financial crisis does not appear to have had a negative effect in the progress of integration in those markets. These results may be indicating that the global financial crisis has harmed the competition in input prices of EU life insurance markets but not the competition in output prices. These findings provide additional information to previous results by Cummins et al. (2017) who showed a lower level of competition, on average, in European life insurance markets in the 2008–2011 period (post-crisis period) than in the 1999–2007 period (pre-crisis period).

4.3 Analysis of the Eurozone countries

As we stated before, the introduction of the Euro in 1999 was a step taken towards an integrated European life insurance market. Since not all the countries of our sample belong to the Eurozone, we performed the whole analysis focusing exclusively on the Eurozone countries of our sample (Austria, Belgium, France, Germany, Italy, Netherlands and Spain). We want to know if a different behaviour exists among these countries compared to the countries not belonging to the Eurozone. The results are presented in Tables 5 and 6 for the cost and revenue analysis, respectively.

The main results of the existence of β convergence and σ convergence in meta-frontier efficiency scores (both in costs and in revenues) as well as in meta-technology efficiency (both in costs and in revenues) ratios over the period 1998–2014 keep up when we focus the analysis on the Eurozone countries. In addition, results with respect to the coefficients βcrisis and σcrisis prevail (in terms of sign and significance) except in the analysis of convergence of meta-frontier cost efficiency scores where the σcrisis coefficient was not significant. This finding seems to indicate a weaker negative effect of the global financial crisis on the integration of the Eurozone life insurance markets of our sample compared to the countries not belonging to the Eurozone. That is, since we do not find differences in σ convergence in meta-frontier cost efficiency for the Eurozone countries between the two periods considered, but we do find differences for the 10 analyzed EU countries, results seem to indicate that the countries of our sample not belonging to the Eurozone are the most responsible countries for the lower rate of convergence in cost efficiency to the average level of groups of countries during the period 2008–2014.Footnote 13

5 Summary and conclusions

This paper applies the meta-frontier DEA approach to evaluate integration and convergence both in efficiency and in technology gap of EU life insurance markets. Convergence is analysed by using two major concepts of convergence from the economic growth literature: the β-convergence and the σ-convergence. The analysis is carried out on 10 EU life insurance markets over the period 1998–2014 including a total of 8594 year-firm observations. Three are the main analysed issues: whether convergence in (cost and revenue) efficiency of EU life insurance markets have taken place over the sample period; whether EU life insurance markets have become more technologically homogeneous over this period; and if the global financial crisis has affected the integration and convergence in efficiency as well as in technology gap of the analysed markets. The DEA meta-frontier framework provides us with two key components for these analyses: meta-frontier efficiency scores and meta-technology efficiency ratios. The first (second) component is used to evaluate convergence in efficiency (technology gap) of major EU life insurance markets.

As expected, results show convergence in efficiency (both in costs and revenues) among EU life insurance markets over the sample period as well as that EU life insurance markets have become more technologically homogeneous, providing evidence of integration in EU life insurance markets over the period 1998–2014. That is, using the β-convergence concept, we find evidence of efficiency catch-up (the least efficient countries in 1998 have shown a higher improvement in efficiency than the most efficient countries in 1998) among the 10 EU life insurance markets over the sample period. Results, using the σ-convergence concept, also show that the dispersion of the mean efficiency scores among EU life insurance markets decreased during the sample period. In addition, results also show β-convergence and σ-convergence in meta-technology cost/revenue efficiency ratios of the 10 EU life insurance markets, providing evidence that technological discrepancy among the life insurance markets of major EU countries decreased over the sample period.

Nevertheless, we also find that, for the analysis of the 10 EU life insurance markets, the global financial crisis has affected the rates of β-convergence and σ-convergence negatively both in meta-frontier cost efficiency as well as in meta-technology cost efficiency ratio. These negative effects prevail in the analysis of the Eurozone countries of our sample except for σ-convergence in meta-frontier cost efficiency, which was not affected, indicating that the countries of our sample not belonging to the Eurozone were the most responsible countries for the slow rate of convergence in cost efficiency during the post-crisis period. However, in terms of revenue efficiency, results, in general, indicate that the global financial crisis has not influenced the integration of EU life insurance markets negatively. The fact that the global financial crisis has influenced negatively the integration of EU life insurance markets in terms of cost efficiency, but not in terms of revenue efficiency suggests that the crisis harmed competition in input prices but not competition in output prices.

The results of our analysis are relevant in the light of the recent initiatives to increase integration of EU financial markets. In addition, the analysis presented here should stimulate future research on integration and convergence in efficiency and technology gap in the EU non-life insurance market according to the special characteristics of this insurance segment and taking into account the extant heterogeneity among EU countries. One may think that it is more complex to create a fully integrated EU market for non-life insurance than for life insurance and, consequently, one may expect the divergences between the possible sub-technologies representing the country frontiers and the technology of the EU meta-frontier to be bigger in the non-life insurance segment. Reasons for these expectations are that the non-life insurance segment has more lines and more complicated businesses than the life insurance segment. In addition, another reason is that consumers of non-life insurance products, compared to life insurance products, usually prefer buying their insurance policies locally, making integration difficult.

Notes

Literature on efficiency in the insurance industry is growing (see Cummins & Weiss, 2013; Kaffash et al., 2020), including several papers analyzing the effects of deregulation on efficiency and productivity in European national markets (e.g. Cummins & Rubio-Misas, 2006 for Spain; Mahlberg & Url, 2010 for Germany). However, there are relatively few studies on efficiency and productivity of European insurance markets in a cross-country setting (see e.g. Diacon et al., 2002; Fenn et al., 2008; Berry-Stölze et al., 2011; Vencappa et al., 2013; Eling & Schaper, 2017; Eling & Jia, 2018).

Charnes et al. (1981) already made an application of frontier models for efficiency comparison among groups, which was reintroduced by Battese and Rao (2002) as the meta-frontier approach and later improved by Battese et al. (2004) and O’Donnnell et al. (2008). There are many fields in which the meta-frontier approach has been applied. This way, recent applications of the DEA-meta-frontier approach cover fields, such as analyzing efficiency of commercial banks (e.g. Liu et al., 2020a, 2020b); evaluating aquaculture farm efficiency (e.g. Rahman et al., 2019); measuring total-factor energy efficiency across provinces (e.g. Cheng et al., 2020); evaluating the technology gaps in tourist hotels (see e.g. Yu & Chen, 2020); or measuring the energy conservation and emission reduction technology levels of cities (see e.g. Sun & Li, 2021).

See Kaffash and Marra (2017) for DEA applications in financial services.

These 10 EU countries are Austria, Belgium, Denmark, France, Germany, Italy, the Netherlands, Spain, Sweden, and the UK. We first considered the countries that were in the EU during all the years of the period of analysis. That is, the EU-15, therefore, we excluded countries which joined the EU in 2004, 2007 and 2013. Furthermore, we excluded Finland, Greece, Ireland, Luxembourg, and Portugal due to the lack of homogeneous data to construct the relevant variables, the limited number of firms per year in some countries and because in some years and countries we did not have any firms after considering the screening tests. The UK is included in the study because it was part of the EU until 2020.

Orbis Insurance Focus dataset provided by Bureau van Dijk was formerly known as ISIS database.

The two-stage approach of DEA has been widely used in empirical applications and is supported by theoretical works such as Banker and Natarajan (2008) and Banker et al. (2019). Banker and Natarajan (2008) establish DEA as a stochastic frontier estimation method that does not impose a strong parametric structure. They show that the two-stage approach of DEA utilized in many DEA applications where DEA efficiency estimates are regressed on firm characteristics and other covariates yields consistent estimates. They also show that this approach is statistically consistent in a composed error framework, i.e. that DEA, like stochastic frontier analysis (SFA), incorporates one and two-side random errors. Furthermore, Banker et al. (2019) explain that DEA, in a first stage followed by ordinary least squares (OLS), in the second stage (which is the utilized approach in the present paper), is the most appropriate method of choice when the production function is contextualized in the Aigner et al. (1977) and Meeusen and Broeck (1977) composed error tradition.

The panel data nature of our data set raises the need to control for the unobserved heterogeneity problem normally present in the presence of countries with potentially different characteristics. We approach this issue by applying OLS controlling for the unobserved country fixed effect through country dummy variables.

We do not present own-country efficiency scores, both in the cost and revenue analyses, to save space.

We are not aware of any papers analyzing convergence in revenue efficiency across EU banking markets. For this reason, our results comparison only focuses on cost efficiency.

Since the number of firms is different from one year to another, we conducted the whole convergence analysis considering the subset of insurers included in all the 17 years of the sample period. Results (available upon request) of the complete panel analysis support the same conclusions as the full sample analysis, with the exceptions of the coefficient of σcrisis variable which was not significant in the analysis of convergence of MCERs as well as in the analysis of convergence of meta-frontier revenue efficiency scores.

As a robustness test of these findings, we performed the whole analysis of convergence on all the countries of our sample where we additionally included interaction terms of a Eurozone dummy variable (1 for the Eurozone countries of our sample) with the main explanatory variables (the coefficients of these interaction terms are called βEurozone and σEurozone, respectively) in all regressions. With these interaction terms we tested if, in general, the results differ between the Eurozone and non-Eurozone countries of our sample. We also included interaction terms of the Eurozone dummy variable with the βcrisis and σcrisis variables (the coefficients of these interaction terms are called βcrisisEurozone and σcrisisEurozone, respectively) in Models 2. With these interaction terms we tested if the financial crisis affected the results of the Eurozone countries differently from the non-Eurozone countries. Results (available upon request) in the cost analysis show that: the coefficient of the βEurozone and σEurozone terms are not statistically significant in the analysis of convergence in efficiency; the coefficients of βcrisis and σcrisis are positive and significant in all regressions; the coefficient of the βcrisisEurozone variable is negative and significant in 3 out of 4 regressions and the coefficient of the σcrisisEurozone variable is negative and significant in all regressions. These results reinforce the findings that, in terms of costs, the financial crisis has led to a higher slowdown in the progress of integration of EU life insurance markets in the non-Eurozone countries of our sample than in the Eurozone countries. However, results in the revenue analysis, show that the coefficients of the βcrisis, σcrisis, βcrisisEurozone and σcrisisEurozone variables are not significant, indicating that the global financial crisis has not influenced the integration of EU life insurance markets negatively in terms of revenue efficiency, in both the Eurozone and non-Eurozone countries of our sample.

References

Aigner, D. J., Lovell, C. A. K., & Schmidt, P. (1977). Formulation and estimation of stochastic frontier production function models. Journal of Econometrics, 6, 21–37.

Al-Amri, K., Cummins, J. D., & Weiss, M. A. (2021). Economies of scope, organizational form, and insolvency risk: Evidence from the Takaful industry. Journal of International Financial Markets Institutions and Money, 70, 101259.

Altuntas, M., Berry-Stölzle, T. R., & Cummins, J. D. (2021). Enterprise risk management and economies of scale and scope: Evidence from the German insurance industry. Annals of Operations Research, 299, 811–845.

Banker, R. D., & Natarajan, R. (2008). Evaluating contextual variables affecting productivity using Data Envelopment Analysis. Operations Research, 56(1), 48–58.

Banker, R. D. R., & Natarajan and D. Zhang,. (2019). Two-stage estimation of the impact of contextual variables in stochastic frontier production model using Data Envelopment Analysis: Second stage OLS versus bootstrap approaches. European Journal of Operational Research, 278(2), 368–384.

Barro, R. J., & Sala-i-Martin, X. (1995). Economic growth. McGraw Hill.

Barros, C. P., & Wanke, P. (2017). Technology gaps and capacity issues in African insurance companies: selected countries evidence. Journal of International Development, 29(1), 117–133.

Battese, G. E., & Rao, D. S. P. (2002). Technology gap, efficiency, and stochastic meta-frontier function. International Journal of Business Economics, 1, 87–93.

Battese, G. E., Rao, D. S. P., & O’Donnell, C. J. (2004). A meta-frontier production function for estimation of technical efficiencies and technology gaps for firms operating under different technologies. Journal of Productivity Analysis, 21, 91–103.

Berger, A. N. (2003). The efficiency effects of a single market for financial services in Europe. European Journal of Operational Research, 150, 466–481.

Berry-Stölzle, T., Weiss, M. A., & Wende, S. (2011). Market structure, efficiency and performance in the European Insurance Industry. Working paper, University of Georgia, Athens, GA.

Canova, F. & Marcet, A. (1995). The poor stay poor: Non convergence across countries and regions. In Presentation at the CEPR workshop on empirical macroeconomics, Brussels.

Casu, B., & Girardone, C. (2010). Integration and efficiency convergence in EU banking markets. Omega, 38, 260–267.

Casu, B., Ferrari, A., Girardone, C., & Wilson, J. O. S. (2016). Integration, productivity and technological spillovers: Evidence for Eurozone banking industries. European Journal of Operational Research, 255, 971–983.

Charnes, A., Cooper, W. W., & Rhodes, E. (1981). Evaluating program and managerial efficiency: An application of data envelopment analysis to program follow through. Management Science, 27(6), 668–697.

Cheng, Z., Liu, J., Li, L., & Gu, X. (2020). Research on meta-frontier total-factor energy efficiency and its spatial convergence in Chinese provinces. Energy Economics, 86, 104702.

Cooper, W. W., Seiford, L. M., & Zhu, J. (2011). Handbook of data envelopment analysis. Springer.

Cummins, J. D., & Rubio-Misas, M. (2006). Deregulation, consolidation and efficiency: Evidence from the Spanish insurance industry. Journal of Money, Credit and Banking, 38(2), 323–355.

Cummins, J. D., Rubio-Misas, M., & Vencappa, D. (2017). Competition, efficiency and soundness in European life insurance markets. Journal of Financial Stability, 28, 66–78.

Cummins, J. D., Rubio-Misas, M., & Zi, H. (2004). The Effect of organizational structure on efficiency: Evidence from the Spanish insurance industry. Journal of Banking and Finance, 28(12), 3113–3150.

Cummins, J. D., Tennyson, S., & Weiss, M. A. (1999a). Consolidation and efficiency in the US life insurance industry. Journal of Banking and Finance, 23, 325–357.

Cummins, J. D., & Weiss, M. A. (2013). Analyzing firm performance in the insurance industry using frontier efficiency and productivity methods. In G. Dionne (Ed.), Handbook of insurance (pp. 795–861). Springer.

Cummins, J. D., Weiss, M. A., Xie, X., & Zi, H. (2010). Economies of scope in financial services: A DEA efficiency analysis of the US insurance industry. Journal of Banking and Finance, 34(7), 1525–1539.

Cummins, J. D., Weiss, M. A., & Zi, H. (1999b). Organizational form and efficiency: The coexistence of stock and mutual property-liability insurers. Management Science, 45(9), 1254–1269.

Degl’Innocenty, M., Kourtzidis, S. T., Sevic, Z., & Tzeremes, N. G. (2017). Bank productivity growth and convergence in the European Union during the financial crisis. Journal of Banking and Finance, 75, 184–199.

Diacon, S. R., Starkey, K., & O’Brien, C. (2002). Size and Efficiency in European long-term insurance companies: An international comparison. The Geneva Papers on Risk and Insurance- Issues and Practice, 27(3), 444–466.

ECB. (2011). Financial integration in Europe. European Central Bank.

ECB. (2017). Financial integration in Europe. European Central Bank.

ECB. (2020). Financial integration and structure in the Euro area. European Central Bank.

Eling, M., & Jia, R. (2018). Business failure, efficiency and volatility: Evidence from the European insurance industry. International Review of Financial Analysis, 59, 58–76.

Eling, M., & Jia, R. (2019). Efficiency and profitability in the global insurance industry. Pacific-Basin Finance Journal, 57, 101190.

Eling, M., & Schaper, P. (2017). Under pressure: How the business environment affects productivity and efficiency of European life insurance companies. European Journal of Operational Research, 258, 1082–1094.

Färe, R., & Primont, D. (1995). Multi-output production and Duality: Theory and applications. Kluwer.

Fenn, P., Vencappa, D., Diacon, S., Klumpes, P., & O’Brien, C. (2008). Market structure and the efficiency of European insurance companies: A stochastic frontier analysis. Journal of Banking and Finance, 32, 86–100.

Giantsios, D. G., & Noulas, A. G. (2020a). Efficiency and convergence in European life insurance industry. Multinational Finance Journal, 24(1/2), 65–91.

Giantsios, D. G., & Noulas, A. G. (2020b). Cost efficiency and convergence in European nonlife insurance industry. Journal of Applied Finance and Banking, 10(6), 117–133.

Hristov, N., Hülsewig, O., & Wollmershäuser, T. (2012). Loan supply shocks during the financial crisis: Evidence for the Euro area. Journal of International Money and Finance, 31(3), 569–592.

Kaffash, S., Arizi, R., Huang, Y., & Zhu, J. (2020). A survey of data envelopment analysis applications in the insurance industry 1993–2018. European Journal of Operational Research, 284(3), 801–813.

Kaffash, S., & Marra, M. (2017). Data envelopment analysis in financial services: A citation network analysis of banks, insurance companies and money markets funds. Annals of Operations Research, 253, 307–344.

Liu, X., Sun, J., Yang, F., & Wu, J. (2020a). How ownership structure affects bank deposits and loan efficiencies: An empirical analysis of Chinese commercial banks. Annals of Operations Research, 290, 983–1008.

Liu, X., Yang, F., & Wu, J. (2020b). DEA considering technological heterogeneity and intermediate output target setting: The performance analysis of Chinese commercial banks. Annals of Operations Research, 291, 605–626.

Lovell, C. A. K. (1993). Production frontiers and productive efficiency. In H. O. Fried, C. A. K. Lovell, & S. S. Schmidt (Eds.), The measurement of productive efficiency. Oxford University Press.

Mahlberg, B., & Url, T. (2010). Single market effects on productivity in the German insurance industry. Journal of Banking and Finance, 34(7), 1540–1548.

Mamatzakis, E., Staikouras, C., & Koutsomanoli-Filippaki, A. (2008). Bank efficiency in the New European Union Member States: Is there convergence? International Review of Financial Analysis, 17, 1156–1172.

Matousek, R., Rughoo, A., Sarantis, N., & Assaf, A. G. (2015). Bank performance and convergence during the financial crisis: Evidence from the ‘Old’ European Union and Eurozone. Journal of Banking and Finance, 52, 208–216.

Meeusen, W., & Broeck, J. (1977). Efficiency estimation from Cobb-Douglas production functions with composed error. International Economic Review, 18(2), 435–444.

Milesi-Ferretti, G. M., & Tille, G. (2011). The great retrenchment: International capital flows during the global financial crisis. Economic Policy, 26(66), 285–342.

O’Donnell, C. J., Prasada Rao, D. S., & Battese, G. E. (2008). Metafrontier framework for the study of firm-level efficiencies and technology ratios. Empirical Economics, 34, 231–255.

Parikh, A., & Shibata, M. (2004). Does trade liberalization accelerate convergence in per capita incomes in developing countries? Journal of Asian Economics, 15, 33–48.

Rahman, M. T., Nielsen, R., Khan, M. A., & Asmild, M. (2019). Efficiency and production environmental heterogeneity in aquaculture: A meta-frontier DEA approach. Aquaculture, 509, 140–148.

Reyna, A. M., Fuentes, H. J., & Nuñez, J. A. (2021). Response to Mexican life and non-life insurers to the low interest rate environment. The Geneva Papers. https://doi.org/10.1057/s41288-021-00208-8

Rubio-Misas, M. (2022). Bancassurance and the coexistence of multiple insurance distribution channels. International Journal of Bank Marketing. https://doi.org/10.1108/IJBM-04-2021-0129

Sun, J., & Li, G. (2021). Optimizing emission reduction task sharing: Technology and performance perspectives. Annals of Operations Research. https://doi.org/10.1007/s10479-021-04273-z

Swiss Re. (1996). Deregulation and liberalization of market access: The European insurance industry on the threshold of a new era in competition, Sigma No. 7/1996 (Zurich, Switzerland).

Swiss Re. (2015). M&A in insurance: Start of a new wave? Sigma No 3/2015 (Zurich, Switzerland).

Tziogkidis, P., Philippas, D., & Tsionas, M. G. (2020). Multidirectional conditional convergence in European banking. Journal of Economic Behavior and Organization, 173, 88–106.

Vencappa, D., Fenn, P., & Diacon, S. (2013). Productivity growth in the European insurance industry: Evidence from life and non-life companies. International Journal of the Economics and Business, 20(2), 281–305.

Wanke, P., & Barros, C. P. (2016). Efficiency drivers in Brazilian insurance: A two-stage DEA metafrontier data mining approach. Economic Modelling, 53(C), 8–22.

Weill, L. (2009). Convergence in banking efficiency across European countries. Journal of International Financial Markets, Institutions and Money, 19, 818–833.

Yu, M.-M., & Chen, L.-H. (2020). A meta-frontier network data envelopment analysis approach for the measurement of technological bias with network production structure. Annals of Operations Research, 287, 495–514.

Funding

Universidad de Málaga/CBUA.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The authors gratefully acknowledge financial support from the Spanish Ministry of Economics and Competitiveness (Project ECO2014-52345-P), the Spanish Ministry of Science, Innovation and Universities (Project RTI2018-097620-B-100) and Universidad de Málaga Campus de Excelencia Internacional Andalucía Tech. They thank Universidad de Málaga/CBUA for funding open access charge.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Cummins, J.D., Rubio-Misas, M. Integration and convergence in efficiency and technology gap of European life insurance markets. Ann Oper Res 315, 93–119 (2022). https://doi.org/10.1007/s10479-022-04672-w

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10479-022-04672-w