Abstract

It is notoriously difficult to estimate the impact of information frictions on trade. The 1866 transatlantic telegraph connection has been used to estimate these impacts, but I demonstrate this sample violates the assumptions of an arbitrage model in ways that are likely to bias empirical result. I avoid this bias by constructing a novel dataset that meets all relevant assumptions during the 1848 rollout of the telegraph across the U.S., ultimately estimating the magnitude of the distortions on prices, quantities, and efficiency to be roughly half as large as those found in prior literature.

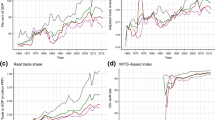

Source The Pre-Civil War data are collected from newspapers as described in the text, and the Post-Civil War data are obtained from Steinwender (2018)

Source The Pre-Civil War data are collected from newspapers as described in the text, and the Post-Civil War data are from Steinwender (2018)

Similar content being viewed by others

Notes

Markups are calculated as the export-weighted averages of \(\left({p}_{t+k}^{LIV}-{p}_{t}^{NYC}-{\tau }_{t}\right)/\left({p}_{t}^{NYC}+{\tau }_{t}\right)\) using data from Steinwender (2018).

The three busiest ports by tonnage cleared in 1848 were New York (931,509), New Orleans (487,690), and Boston (414,400). Source The Foreign Commerce and Navigation of the United States, 1849.

Steinwender’s Table 13 finds a reduction in DWL by 87 percent. Since the telegraph reduced news lags by 8.72 days, the daily impact is 87/8.72 = 10.0 percent.

Foreign Commerce and Navigation of the United States, 1850.

Assuming that all U.S. cotton was grown in the South. Based on author’s own calculations from New-Orleans Price-Current, 01 September 1851.

Based on author’s own calculations from issues of the Shipping and Commercial List [New York] from 03 January 1846 through 27 July 1850.

This mail route went from New York to Wilmington, North Carolina via railroad, then by ship to New Orleans.

The mail was often delayed by inclement weather and human error. The New Orleans Daily Picayune constantly inveighed against the Postmaster General’s “puerile excuses for imperfect mail service” and stated, “a remedy can and will be found for the evil.” Picayune 30 September 1846.

Couriers galloped news from Richmond in July 1847, Louisville in November 1847, St. Louis in February 1848, and Mobile in April 1848.

Picayune 19 July 1848.

Picayune issues dated 25 June 1847, 22 August 1848, and 19 September1848.

Picayune 02 March 1848.

See, for example, the New Orleans Commercial Bulletin issues dated 09 August 1849, 19 May 1848, 08 July 1848, 27 May 1848, or the Picayune issues dated 13 January 1848 and 17 October 1848. For the first six months after the first connection, the telegraph’s performance was so bad that “…one-half of the messages sent are never received at all, and of those that do get to hand, a large portion of them are outstripped by the mail.”.

Cotton receipts are assumed exogenous because of its strongly seasonally deterministic trend in Fig. 3. This deterministic trend occurs for two reasons. First, inflows are price inelastic in the short run because cotton’s production is determined in advance during planting and cannot be adjusted until the next planting season. Second, the need to pay off short-term debt prohibited farmers from storing cotton on their farm for long.

See the appendix for a formal proof.

See the appendix for a formal proof.

See the appendix for a formal proof.

There were also various methods of determining the quality of cotton until the 1850s. I select newspapers in both locations that adhere to the Liverpool classification of cotton grading.

These ledgers are for transactions between New Orleans and Liverpool, so I assume unloading costs in New York are comparable to those in Liverpool.

I use the same method as that in McCusker (1978).

These data are not distinguished by quality, but middling cotton is the most common quality and exports are likely to be highly correlated across qualities.

The fastest news transmission observed was from 1:20 pm the same day which was printed in the afternoon edition of the Picayune on 25 April 1850.

I convert Steinwender’s (2018) demand slope from -0.05 pence/1,000 bales using the following conversion rate:

\(-0.05\frac{{\text{pence}}}{\mathrm{1,000 bales at }400\mathrm{ lbs}}\times \frac{400{\text{lbs}}}{455{\text{lbs}}}\times \frac{1{\text{GBP}}}{240{\text{pence}}}\times \frac{7.5{\text{USD}}}{{\text{GBP}}}\times \frac{100{\text{cents}}}{{\text{USD}}}=-0.137\frac{{\text{cents}}}{1000\mathrm{ bales at }455\mathrm{ lbs}}\).

I also assume that agents account for structural breaks in the time series when forecasting. The structural breaks are defined to occur on 20 Dec 1846, 19 Oct 1847, 12 Jul 1849, and 01 Jan 1850. These are visually apparent in the top panels of Fig. 3.

The AR(1) regressions with a deterministic seasonal are \({y}_{t}=\mu +\rho {y}_{t-1}+{\beta }_{1}harvestda{y}_{t}+{\beta }_{2}harvestda{y}_{t}^{2}+{u}_{t},\) where \(harvestday\) counts the day of the year and resets to zero every 15th of September when the season begins.

One exception to this is that two shipping speeds exist in the Post-Civil War setting (steam and sail), while only one (sail) is predominant in the Pre-Civil War setting. I follow Steinwender (2018) in using the shipping speed of steamships in the Post-Civil War setting.

Indeed, storage failed to approach stockout during this period, so storage figures were 78 percent higher when the telegraph was connected than they were exactly one year later. The minimum storage figures for the years 1866–1869 were 151,992, 27,000, 10,000, and 2,100, respectively. The vastly higher storage in 1866 suggests that there was unusually high levels of storage.

The first telegraphic connections are defined as 19 Jul 1848 in the Pre-Civil War period and 30 Jul 1866 in the Post-Civil War period.

Without the restriction that \({x}_{t}^{NY}>0\), (6) predicts that price differentials decline instead of staying stable.

For the Pre-Civil War period, I identify major shocks as periods where the one month moving average of price differentials exceeds 15 percent of New Orleans prices. I then assign the duration of the shock to continue until price differentials return to zero. Data-based criteria are difficult to establish during the Post-Civil War period given how large and asymmetrical the price differentials are throughout. The first shock corresponds to the Panic of 1847, the second is due to the start of the French Revolution of 1848, and the third is due to rampant speculation induced by a contemporaneous miscalculation in the existing stock of cotton. Motivated by the correspondence between shocks and the historical narrative in the Pre-Civil War period, I rely on annual market narratives to identify shocks. The first shock occurred due to speculation over the cotton shortage following the Civil War, while the second is the Panic of 1866.

The ARIMA specification was chosen using the Akaike Information Criterion (AIC) and Bayesian Information Criterion (BIC) on New Orleans prices in the pre-telegraph period.

The weighted average is calculated as 8.16 = (7 \(\times\) 0.27 + 10 \(\times\) 0.17)/(0.27 + 0.17).

The weighted average is calculated as 2.13 = (1 \(\times\) 0.13 + 3 \(\times\) 0.17)/(0.13 + 0.17).

The weighted average of 2.43 = (0.12 \(\times\) 1 + 0.14 \(\times\) 2 + 0.15 \(\times\) 4)/(0.12 + 0.14 + 0.15).

For the Pre-Civil War period, this calculation is the impact of the telegraph divided by average trade costs divided by average number of days that the telegraph reduced news lags, -0.18/1.12/5.72 = -0.028. For the Post-Civil War period, I use Steinwender’s results from column 3 of Table 3 and row 1 of Table 1 and divide by average trade costs to get −0.87/0.933/8.72 = −0.107.

The quadratic nature of this variance makes it sensitive to outliers. As a result, I drop all observations more than 6 standard deviations from the mean.

The coefficient on receipts is also of the opposite sign, but it is close to zero and statistically insignificant.

These results come from column 3 of Table 8 in Steinwender (2018). The exact calculation is that the telegraph increases exports by 0.47 thousand bales when the pre-telegraph average is 0.46. Since the telegraph reduced news lags by 8.72 days, the daily impact is measured as. 47/.46/8.72*100 = 11.7.

The quadratic nature of this variance makes it sensitive to outliers. As a result, I drop all observations with an export variance more than 6 standard deviations from the mean.

F-stat p-val = 0.11.

See Steinwender (2018) for a formal proof.

Steinwender (2018) Table 13 reports a reduction in DWL by 87 percent. Since the telegraph reduced news lags by 8.72 days, the daily impact is 87/8.72 = 10.0 percent. I find a percent decline in DWL of 26/4.57 = 5.7 percent per day.

References

Aker, J. C. (2010). Information from markets near and far: Mobile phones and agricultural markets in Niger. American Economic Journal: Applied Economics, 2(3), 46–59.

Allen, T. (2014). Information frictions in trade. Econometrica, 82(6), 2041–2083.

Anderson, J. E., & van Wincoop, E. (2004). Trade costs. Journal of Economic Literature, 42(3), 691–751.

Boyle, J. E. (1934). The New Orleans cotton exchange. The Country Life Press.

Brown, J. R., & Goolsbee, A. (2002). Does the internet make markets more competitive? Evidence from the life insurance industry. Journal of Political Economy, 110(3), 481–507.

Campanella, R. (2002). Time and Place in New Orleans. Pelican Publishing.

Coleman, A. (2009). Storage, slow transport, and the law of one price: Theory with evidence from nineteenth-century US corn markets. The Review of Economics and Statistics, 91(2), 332–350.

Donnell, E. J. (1872). Chronological and statistical history of cotton. New York: J. Sutton & Company.

Entz, J. F. (1840). Exchange and cotton trade between England and the United States. E. B. Clayton, Stationer.

Goyal, A. (2010). Information, direct access to farmers, and rural market performance in Central India. American Economic Journal: Applied Economics, 2(3), 22–45.

Head, K., & Mayer, T. (2013). What separates us? Sources of resistance to globalization. Canadian Journal of Economics, 46(4), 1196–1231.

Jensen, R. (2007). The digital provide: Information (technology), market performance, and welfare in the south Indian fisheries sector. The Quarterly Journal of Economics, 122(3), 879–924.

Killick, J. R. (1977). The cotton operations of Alexander Brown and Sons in the Deep South, 1820–1860. Journal of Southern History, 43(2), 169.

McCusker, J. J. (1978). Money and exchange in Europe and America, 1600–1775. The University of North Carolina Press Chapel Hill.

Rogoff, K., Froot, K., & Kim, M. (2001). The law of one price over 700 years. NBER Work. Pap. No. 5132.

Shiue, C. H. (2002). Transport costs and the geography of arbitrage in Eighteenth-Century China. The American Economic Review, 92(5), 1406–1419.

Shiue, C. H., & Keller, W. (2007). Markets in China and Europe on the eve of the industrial revolution. American Economic Review, 97(4), 1189–1216.

Steinwender, C. (2018). Real effects of information frictions: When the States and the Kingdom became united. The American Economic Review, 108(3), 657–696.

Williams, J. C., & Wright, B. D. (1991). Storage and commodity markets. Cambridge University Press.

Williamson, J. G., & O’Rourke, K. H. (1999). Globalization and history. MIT Press.

Woodman, H. D. (1968). King cotton and his retainers: Financing and marketing the cotton crop of the South, 1800–1925. University of Kentucky Press.

Xu, C. (2022). Reshaping global trade: The immediate and long-run effects of bank failures. The Quarterly Journal of Economics, 137(4), 2107–2161.

Acknowledgements

I thank Mario Crucini, Peter Rousseau, Joel Rodrigue, Bill Whalen, Jeremy Atack, Ryan Brady, and Bill Collins for valuable comments and suggestions.

Funding

None.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The author declares he has no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

1.1 Data

Most data were collected from historical newspapers, which occasionally had missing, illegible, or qualitative data that proved unusable. As a result, I collect data from multiple newspapers in each location to reduce the number of missing observations. For New Orleans, the Daily Picayune served as the main source of data for prices, exports to New York, and news lags. The New Orleans Commercial Bulletin served as the main source of data for quantities and freight costs and as a secondary source for prices and news lags. The New-Orleans Price-Current was the main source for the rates on bills of exchange to recover interest rates while the Daily Picayune was the secondary source. For New York, The New York Herald served as the only source of data for prices and the primary source for shipping times. The New-York Daily Tribune served as a secondary source for shipping times. Weekly figures for New York storage, receipts, re-exports, and rates on bills of exchange come from the Shipping and Commercial List.

The primary source of transportation speeds comes from The New York Herald, while the secondary source is The New York Daily Tribune. These newspapers list ships that came into port on a given day, where the ships departed from, and the duration of the voyage. Since cargo descriptions were only occasionally available, I recorded the voyage duration of all ships excluding those that did not sail directly to New York and those that were waylaid by maintenance issues.

I obtained non-freight transportation costs such as wharfage, cartage, and insurance from contemporary ledgers that were printed in Boyle (1934) and Entz (1840). To obtain daily interest rates that were incurred when taking out loans for shipping costs, I use the New-Orleans Price-Current to calculate the interest spread between New York bills of exchange with 60-days and zero-day maturities. Over the sample, they average 1.77 percent which is very similar to the 1.5 percent observed in Boyle (1934), but they range from 0.875 to 3.375 percent. The breakdown of costs is provided in Table

9.

1.2 Model

Consider two different information regimes. First, a delayed information (DI) regime in which agents in NO have news from NY up to period \(t-1\) and must forecast NY prices in period \(t+1\) when their exports can be sold in NY. Let this be represented by information set \({I}_{t-1}^{M}.\) Second, an instantaneous information (II) regime where all agents have news from NY up to period \(t\) and must forecast prices for period \(t+1\). Let this be represented by information set \({I}_{t}^{M}\). Lastly, let \({\overline{a} }_{D}\) be the average level of demand such that the AR(1) demand process can be rewritten as \({a}_{D,t }-{\overline{a} }_{D}=\rho \left({a}_{D,t-1}-{\overline{a} }_{D}\right)+{e}_{t}\) where \({\overline{a} }_{D}=\frac{\alpha }{1-\rho }\). Then, the following lemmas and proofs are reproduced from Steinwender (2018) for convenience.

Lemma 1

When switching from delayed to instantaneous information, the variance of expected demand increases, \({\text{Var}}\left[{\text{E}}\left[{{\text{a}}}_{{\text{D}},{\text{t}}+1}\mid {{\text{I}}}_{{\text{t}}-1}^{{\text{M}}}\right]\right]<\) \({\text{Var}}\left[{\text{E}}\left[{{\text{a}}}_{{\text{D}},{\text{t}}+1}\mid {{\text{I}}}_{{\text{t}}}^{{\text{M}}}\right]\right]\).

Proof

If the demand shock is \({\text{AR}}(1)\), the variances are:

Note that for a stationary \({\text{AR}}(1)\) process,

For \(0 < \rho < 1,\)

Lemma 2

Suppose \(\frac{{\overline{{\text{a}}} }_{{\text{D}}}-{\overline{{\text{a}}} }_{{\text{S}}}-\uptau }{{{\text{b}}}_{{\text{S}}}+{{\text{b}}}_{{\text{D}}}}>0\), which means that there are positive exports at the average demand shock. Then, when switching from delayed to instantaneous information:

-

(i)

Average exports increase

$$E\left[{x}_{t}^{DI}\right]<E\left[{x}_{t}^{II}\right]$$ -

(ii)

Conditional on exporting, exports increase

$$E\left[{x}_{t}^{DI}|{x}_{t}^{DI}>0\right]<E\left[{x}_{t}^{II}|{x}_{t}^{II}>0\right]$$

Proof

Consider the analytical expression for exports, and consider first uncensored exports \(\widetilde{x}_{t} : = \frac{{E\left[ {a_{D,t + 1} } \right] - \overline{a}_{S} - \tau }}{{b_{S} + b_{D} }}\). Uncensored exports in both regimes differ only in the way expectations about future demand shocks are formed. In the instantaneous-information regime the information set includes everything up to period \(t\), while the information set in the delayed-information regime includes only information up to period \(t-1\). By the Law of Iterated Expectations, average uncensored exports are the same in both regimes:

The variance of uncensored exports is a function of the variance of expected demand shocks, conditional on the respective information set:

and, using Lemma 1, Var \(\left[{\tilde{x}}_{t}^{DI}\right]<{\text{Var}}\left[{\tilde{x}}_{t}^{II}\right]\).

Uncensored exports have the same mean in both information regimes, but the variance of uncensored exports is smaller in the delayed-information regime: \(\widetilde{x}_{t}^{II} \sim N\left( {\frac{{\overline{a}_{D} - \overline{a}_{S} - \tau }}{{b_{S} + b_{D} }},\frac{{{\text{Var}}\left( {E_{t} \left[ {a_{D} } \right]} \right)}}{{\left( {b_{S} + b_{D} } \right)^{2} }}} \right)\) and \(\widetilde{x}_{t}^{DI} \sim N\left( {\frac{{\overline{a}_{D} - \overline{a}_{S} - \tau }}{{b_{S} + b_{D} }},\frac{{{\text{Var}}\left( {E_{t - 1} \left[ {a_{Dt} } \right]} \right)}}{{\left( {b_{S} + b_{D} } \right)^{2} }}} \right)\). Denoting \(\tilde{\mu }:=E\left[{\tilde{x}}_{t}\right]\) and \({\tilde{\sigma }}^{2}:={\text{Var}}\left[{\tilde{x}}_{t}\right]\), average censored exports are given by \(E\left[{x}_{t}\right]=\Phi \left(\frac{\tilde{\mu }}{\tilde{\sigma }}\right)\tilde{\mu }+\tilde{\sigma }\phi \left(\frac{\tilde{\mu }}{\tilde{\sigma }}\right)\). A change from \(DI\) to \(II\) increases the variance of censored exports\({\tilde{\sigma }}^{2}\), and this increases average censored exports \({x}_{t}\):

Truncated exports, i.e., average exports conditional on being positive, \(E\left[{x}_{t}\mid {x}_{t}>0\right]=\tilde{\mu }+\tilde{\sigma }\frac{\phi \left(\frac{\tilde{\mu }}{\tilde{\tau }}\right)}{\Phi \left(\frac{\tilde{\mu }}{\tilde{\sigma }}\right)}\) also increase when switching from DI to II:

if \(\tilde{\mu }>0\), which is assumed for exports to be positive on the average realization of the demand shock.

Note that this proof also holds if there are stochastic supply shocks. Since merchants are in NO, there will be no uncertainty about the realization of supply shocks, so information is not relevant. Supply shocks are relevant only when storage is allowed.

Lemma 3

When switching from delayed to instantaneous information, the variance of the forecast error falls,

Proof

The variance of the forecast error under the II regime (note this is the same whether conditioning on positive exports or not),

while under the DI regime,

from which follows

for \(0<\rho\). Note that this result also holds strictly for random walk shock processes.

About this article

Cite this article

Harrison, J.M. Putting the news in New York and New Orleans: the impact of information frictions on trade. Rev World Econ (2024). https://doi.org/10.1007/s10290-024-00527-7

Accepted:

Published:

DOI: https://doi.org/10.1007/s10290-024-00527-7