Abstract

Using a comprehensive data set of 714 Chinese mutual funds from 2004 to 2015, the study investigates these funds’ performance persistence by using the Capital Asset Pricing model, the Fama-French three-factor model and the Carhart Four-factor model. For persistence analysis, we categorize mutual funds into eight octiles based on their one year lagged performance and then observe their performance for the subsequent 12 months. We also apply Cross-Product Ratio technique to assess the performance persistence in these Chinese funds. The study finds no significant evidence of persistence in the performance of the mutual funds. Winner (loser) funds do not continue to be winner (loser) funds in the subsequent time period. These findings suggest that future performance of funds cannot be predicted based on their past performance.

Similar content being viewed by others

Notes

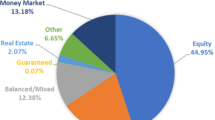

We run the regression only for principal guaranteed funds and finds beta = 0.20, which is very low to study equity funds.

Survivorship bias is a problem that cannot be ignored in Asset Pricing study. The exclusion of dead or inactive funds from the sample results in upward bias of returns. (Brown and Goetzmann 1995)

References

Abdel-Kader M, Qing KY (2007) Risk–adjusted performance, selectivity, timing ability, and performance persistence of Hong Kong mutual funds. J Asia Pac Bus 8(2):25–58

Agarwal V, Naik NY (2000) Multi-period performance persistence analysis of hedge funds. J Financ Quant Anal 35(03):327–342

Babalos V, Kostakis A, Philippas N (2007) Spurious results in testing mutual fund performance persistence: evidence from the Greek market. Appl Financ Econ Lett 3(2):103–108

Berk JB, Green RC (2004) Mutual fund flows and performance in rational markets. J Polit Econ 112(6):1269–1295

Białkowski J, Otten R (2011) Emerging market mutual fund performance: evidence for Poland. N. Am. J. Econ. Financ 22(2):118–130

Bollen NP (2007) Mutual fund attributes and investor behavior. J Financ Quant Anal 42(03):683–708

Bollen NP, Busse JA (2001) On the timing ability of mutual fund managers. J Financ 56(3):1075–1094

Brito RP, Sebastião H, Godinho P (2017) Portfolio choice with high frequency data: CRRA preferences and the liquidity effect. Port Econ J 16(2):65–86

Brown S, Goetzmann W (1995) Performance persistence. J Financ 50(2):679–698

Busse JA, Goyal A, Wahal S (2010) Performance and persistence in institutional investment management. J Financ 65(2):765–790

Carhart MM (1997) On persistence in mutual fund performance. J Financ 52(1):57–82

Casarin R, Pelizzon L, Piva A (2008) Italian equity funds: efficiency and performance persistence. University Ca'Foscari of Venice, Dept. of Economics Research Paper Series, (12_08)

Chen Z, Xiong P (2001) Discounts on illiquid stocks: evidence from China. Yale ICF working paper, 00-56. (accessed at: URL:http://faculty.som.yale.edu/zhiwuchen/EmergingMarkets/ChenXiong.pdf). Accessed 28 March 2018

Chen Z, Xiong P, Huang Z (2014) The asset management industry in China: its past performance and future prospects. J. Portf. Manag 41(5):9–30

Chi Y (2015) Private information in the chinese stock market: evidence from mutual funds and corporate insiders. Dissertations & Theses - Gradworks

Chieh-Tse Hou T (2012) Return persistence and investment timing decisions in Taiwanese domestic equity mutual funds. Manag. Financ 38(9):873–891

De Souza C, Gokcan S (2004) Hedge fund investing: A quantitative approach to hedge fund manager selection and de-selection. J Wealth Manag 6(4):52–73

Fama EF, French KR (1993) Common risk factors in the returns on stocks and bonds. J Financ Econ 33(1):3–56

Harvey CR (1997) Financial Glossary, http://biz.yahoo.com/glossary/bfglosm.html. Accessed on 16 Decemebr 2016

Heffernan S (2001) All UK investment trusts are not the same, Faculty of Finance Working Paper #WPFF-04-2001, City University Business School, London

Huang X, Mahieu RJ (2012) Performance persistence of Dutch pension funds. De Economist 160(1):17–34

Huij J, Post T (2011) On the performance of emerging market equity mutual funds. Emerg Mark Rev 12(3):238–249

Jensen MC (1968) The performance of mutual funds in the period 1945–1964. J Financ 23(2):389–416

Jiang BB, Laurenceson J, Tang KK (2008) Share reform and the performance of China's listed companies. China Econ Rev 19(3):489–501

Jun X, Li M, Shi J (2014) Volatile market condition and investor clientele effects on mutual fund flow performance relationship. Pac Basin Financ J 29(September 2014):310–334

Kang J, Lee C, Lee D (2011) Equity fund performance persistence with investment style: evidence from Korea. Emerg Mark Financ Trade 47(3):111–135

Keswani A, Stolin D (2006) Mutual fund performance persistence and competition: a cross - sector analysis. J Financ Res 29(3):349–366

Mamaysky H, Spiegel M, Zhang H (2007) Improved forecasting of mutual fund alphas and betas. Review of Finance 11(3):359–400

Qureshi F, Ismail I, Gee Chan S (2017) Mutual funds and market performance: new evidence from ASEAN markets. Invest Anal J 46(1):61–79

Ramos SB (2009) The size and structure of the world mutual fund industry.European. Financ Manag 15(1):145–180

Rao Z, Tauni MZ, Iqbal A (2015) Comparison between Islamic and general equity funds of Pakistan – difference in their performances and fund flow volatility. Emerging Economy Studies 1(2):1–16

Rao Z, Tauni MZ, Iqbal A (2016) Performance persistence in institutional investment management: the case of Chinese equity funds. Borsa Istanbul Rev 16(3):146–156

Sirri ER, Tufano P (1998) Costly search and mutual fund flows. J Financ 53(5):1589–1622

Su R, Zhao Y, Yi R, Dutta A (2012) Persistence in mutual fund returns: evidence from China. Int J Bus Soc Sci 3(13)

Tang K, Wang W, Xu R (2012) Size and performance of Chinese mutual funds: the role of economy of scale and liquidity. Pac Basin Financ J 20(2):228–246

Vicente L, Ferruz L (2005) Performance persistence in Spanish equity funds. Appl Financ Econ 15(18):1305–1313

Wahal S, Wang AY (2011) Competition among mutual funds. J Financ Econ 99(1):40–59

Acknowledgements

We are grateful to the anonymous referees for their constructive comments which helped us improving the quality of this paper. All errors and omissions are ours. Part of the study reported here was conducted when the first author was a PhD scholar at Dongbei University of Finance and Economics at China. This research is supported by the National Natural Science Foundation of China (71373236) and the Humanities and Social Sciences Foundation of the Ministry of Education, China (17YJA630015).

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

About this article

Cite this article

Rao, ZuR., Tauni, M.Z., Ahsan, T. et al. Do mutual funds have consistency in their performance?. Port Econ J 19, 139–153 (2020). https://doi.org/10.1007/s10258-019-00163-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10258-019-00163-2