Abstract

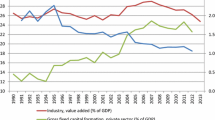

The Portuguese economy has performed remarkably well since joining the EU in 1986. Output per worker grew at an annual rate of 2.25%. The relative price of investment has declined. Real investment has increased compared to output, in part fuelled by an increase in capital inflows. At the same time, resource allocation seems to have improved as well: firm-level data shows a significant decline in the dispersion of labor productivity and size across firms. This paper argues that improvements in outside investor rights that have taken place since Portugal joined the EU is a prime candidate to explain this set of facts.

Similar content being viewed by others

Notes

See, however, Tavares (2004) for a model-free attempt at gauging the potential effect of further investor protection reforms on Portuguese economic growth.

Real variables are in millions of 2000 chained Euros.

Only the nominal investment rate has a share interpretation. Although the real investment rate does not have a share interpretation, it still provides useful information about the relative growth rates of real investment and real output. See Whelan (2002).

Data limitations prevent us from also considering the current account.

The comment in footnote 3 applies here as well.

As discussed in Appendix A.1, a further drawback of our productivity measure stems from the lack of firm or even sectoral level price deflators. Nominal sales are deflated by the GDP deflator.

Hsieh and Klenow (2007a) exploit a similar idea in their cross-country analysis. They infer distributions of firm-level distortions in China and India from observed differences in marginal products. As it is the case here, a large dispersion in factor allocation across firms, relative to some benchmark, is indicative of greater distortions.

Ideally one would like to work with a finer classification. The small number of firms in several sectors prevents us from doing that.

Portugal joined the European Exchange Rate Mechanism in 1992. Participants to this arrangement were supposed to maintain a relatively stable value of their currencies against each other. As is well-known, its success was mixed. A period of instability during 1992 and 1993 lead to a relaxation of the commitment towards exchange rate stability.

A more realistic alternative would be to assume that entrepreneurs pay a return to intermediaries. It turns out that the formulation we adopt is formally equivalent to this one, but leads to a simpler characterization of the optimization problem. See Castro et al. (2004).

Unless otherwise specified, integration is over the whole domain [0, + ∞ ).

It is not necessary to impose an analogous incentive compatibility constraint for z ′ > z. Reporting a productivity higher than the true level would require the entrepreneur to surrender more resources than he actually has, which is not feasible.

Castro et al. (2009) concentrate their attention on steady-states. Here we will be interested in the transitional dynamics as well.

This identification is valid under the assumption that ξ is the only source of cross-country heterogeneity in relative prices. This will not be the case if there are cross-country differences in sectoral productivity as well (actual, not measured productivity as in Hsieh and Klenow (2007b)). We will return to this issue in Section 5.1. Another potential difficulty would arise if the capital shares in the consumption and the investment sectors were significantly different. However, neither Chari et al. (1997) nor Hsieh and Klenow (2007b) find this to be the case.

Unfortunately the Penn World Table does not report the price levels for Singapore in 2004.

As pointed out in Section 4, identifying a change in ξ with a change in Portugal’s relative price of investment relative to Singapore’s may be problematic. If, at the same time, Portugal had become relatively more efficient at producing investment goods compared to Singapore, then the change in relative prices would also contain information about the higher relative productivity. The experiment considered in Section 5.4 illustrates this problem: changes in investment-specific productivity map into relative prices in a way qualitatively similar to investor protection. Since independent measures of either sectoral productivity or investor protection are very hard to come by, this appears to be a rather high hurdle to overcome. Considering overidentifying restrictions may provide a way around it. We are suggesting to inquire whether differences in relative productivity and in investor protection have different implications for the dispersion of other endogenous variables. This paper adopts this alternative strategy.

Although this is not apparent from Fig. 10, the improvement in investor protection has a permanent effect on the trade balance over GDP, which goes from a small positive number to a small negative number. In the new steady-state, Portugal is a net importer of capital.

Instead of replicating the chain-weighted measurement procedure used in the data, the model’s generated series are evaluated at constant prices.

We are not attributing much significance to the very low value of the nominal trade balance over GDP in the first subperiod. As previously pointed out, this owes much to only a few very negative values coinciding with the recession of the early 1980s.

None of the policy experiments is consistent with the post-2000 slowdown in output per worker. Not even the increase in international capital mobility, which generates a decline in output per worker (relative to trend) that begins in 1986 and persists until 2000.

What about combining an improvement in investor protection with lower barriers to international capital mobility? It turns out that lower barriers to capital mobility act by magnifying the response of the economy to better investor protection, with all the qualitative effects of the latter policy change preserved.

In spite of these improvements, Portugal is still characterized by tighter regulation than similarly developed countries, particularly regarding the time it takes for an entrepreneur to obtain legal status. See Cabral (2007).

We note that until the mid to late 1980s, the survey was not mandatory for firms with less than 10 workers. This does not appear to introduce significant censoring, since one cannot detect a significant discreet increase in the number of firms with less than 10 workers at any year starting in 1992.

References

Albuquerque R, Wang N (2008) Agency conflicts, investment, and asset pricing. J Finance 63(1):1–40

Amador J, Cabral S, Maria JR (2007) International trade patterns over the last four decades: how does portugal compare with the other cohesion countries? Banco de Portugal, Working Paper 14 | 2007

Amaral P, Quintin E (2007) Financial intermediation and economic development: a quantitative assessment. Federal Reserve Bank of Dallas

Antunes A, Cavalcanti T, Villamil A (2008) The effect of financial repression and enforcement on entrepreneurship and economic development. J Monet Econ 55(2):278–297

Bernard AB, Eaton J, Jensen JB, Kortum S (2003) Plants and productivity in international trade. Am Econ Rev 93(4):1268–1290

Betts CM, Kehoe TJ (2001) Tradability of goods and real exchange rate fluctuations. Federal Reserve Bank of Minneapolis

Buera F, Shin Y (2008a) Financial frictions and the persistence of history: a quantitative exploration. Washington University in St. Louis

Buera F, Shin Y (2008b) Productivity growth and capital outflow: the case of a small opening economy. Washington University in St. Louis

Buera FJ, Kaboski JP, Shin Y (2009) Finance and development: a tale of two sectors. Washington University in St. Louis

Cabral LMB (2007) Small firms in portugal: a selective survey of stylized facts, economic analysis, and policy implications. Portuguese Econ J 6(1):65–88

Castro R, Clementi GL, MacDonald G (2004) Investor protection, optimal incentives, and economic growth. Q J Econ 119(3):1131–1175

Castro R, Clementi GL, MacDonald G (2009) Legal institutions, sectoral heterogeneity, and economic development. Rev Econ Stud 76(2):529–561

Chari VV, Kehoe PJ, McGrattan ER (1997) The poverty of nations: a quantitative exploration. Staff Report 204, Federal Reserve Bank of Minneapolis

Erosa A, Hidalgo-Cabrillana A (2008) On finance as a theory of tfp, cross-industry productivity differences, and economic rents. Int Econ Rev 49(2):437–473

Fonseca ML, Caldeira MJ, Esteves A (2002) New forms of migration into the european south: challenges for citizenship and governance—the Portuguese case. Int J Popul Geogr 8(2):135–152

Frankel J, Rose A (2002) An estimate of the effect of common currencies on trade and output. Q J Econ 117(2):437–466

Heston A, Summers R, Aten B (2006) Penn World Table Version 6.2. Center for International Comparisons of Production, Income and Prices at the University of Pennsylvania

Hsieh CT, Klenow PJ (2007a) Misallocation and manufacturing TFP in China and India. NBER Working Papers 13290, National Bureau of Economic Research

Hsieh CT, Klenow PJ (2007b) Relative prices and relative prosperity. Am Econ Rev 97(3):562–585

Instituto Nacional de Estatística (2007) Portugal—20 years of European integration. Instituto Nacional de Estatística, Lisbon

Kocherlakota N (1996) Inflation and growth—commentary. Fed Reserve Bank St Louis Rev 78:170–172

Krueger AB (2000) From Bismarck to Maastricht: the March to European union and the labor compact. Labor Econ 7(2):117–134

La Porta R, Lopez-de Silanes F, Shleifer A, Vishny R (1998) Law and finance. J Polit Econ 106:1113–1155

Lima MA (2000) Portugal in the European union: what can we tell the central and eastern European countries? World Econ 23(10):1395–1408

Lustig H, Verdelhan A (2007) The Cross-section of currency risk premia and US consumption growth risk. Am Econ Rev 97(1):89–117

Melitz MJ (2003) The impact of trade on intra-industry reallocations and aggregate industry productivity. Econometrica 71(6):1695–1725

Tavares J (2004) Institutions and economic development in Portugal: a quantitative exploration. Portuguese Econ J 3(1):49–79

Whelan K (2002) A guide to U.S. chain aggregated NIPA data. Rev Income Wealth 48(2):217–233

Author information

Authors and Affiliations

Corresponding author

Additional information

This paper was prepared for the Bank of Portugal Conference on “Desenvolvimento Económico Português no Espaço Europeu” We would like to thank the members of the Scientific Committee, the discussant José Tavares, as well as Sílvia Gonçalves, António Antunes, and Pedro Portugal for comments and suggestions. This paper builds on joint research with Glenn MacDonald. All remaining errors are our own responsibility. Most of this research was completed while Castro was visiting the Bank of Portugal and the Department of Economics at Stern School of Business, NYU. Castro thanks both institutions for their very generous hospitality.

Appendices

Appendix A: Data

All macro-level data used in this paper was obtained from the Bank of Portugal’s Boletim Económico, and spans the 1978–2006 period. The data on the relative price of investment is from Heston-Summers-Aten-06 version 6.2 of the Penn World Tables, and it only spans the 1978–2004 period.

The micro-level data set is the Quadros do Pessoal, an annual survey conducted by the Portuguese Ministry of Employment which is mandatory for all Portuguese firms. We focus on the maximum available period length of data collection, 1982–2005, except for 2001 because no data is available for this year.Footnote 23 The Quadros do Pessoal contains a wealth of information on Portuguese firms (and workers). In this paper we focus on nominal sales, number of employees, and 2 and 3-digit sector of activity.

1.1 A.1 Sales

Ideally one would like to have information on value-added per firm. Unfortunately, Quadros do Pessoal does not have data on the cost of intermediate inputs. To circumvent this problem, we’ll make some assumptions and we’ll use some economic theory. Suppose firm i in sector j at time t produces according to

where y ijt is gross output (total sales), z ijt is total factor productivity, k ijt is capital services, ℓ ijt are labor services, and x ijt are the intermediate inputs. The parameters α j ,γ j ∈ (0,1) , the shares of capital and intermediate goods in production, are potentially sector-specific. Value-added (net output) is given by

where \(p^y_{ijt}\) is the price of firm i’s output and \(p^x_t\) is the price of the intermediate input. If the market for intermediate goods is perfectly competitive, then

Replacing in the definition of value-added

In other words, value-added is proportional to nominal sales, and the constant of proportionality is sector-specific. Up to this constant, one can measure (real) value added by (real) sales. In most scenarios considered in this paper, this turns out to be very convenient—for sufficiently low levels of sectoral disaggregation, the results do not hinge upon knowing γ j . Due to the absence of comprehensive data on firm or even sectoral level price deflators, nominal sales were deflated by the GDP deflator.

One issue in Quadros do Pessoal, relevant for computing labor productivity, is that sales and the number of employees measure in a given year do not refer to the same time period. For the following discussion, it’s important to distinguish between the data collection year (the year attached to the variables in Quadros do Pessoal), and the observation year (the year the variable corresponds to). In any given data collection year, Quadros do Pessoal gathers information in the month of October. The information collected on nominal sales is always for the whole previous year. The observation year for sales is thus the year before the data collection year. Until 1993, the number of employees is for the month of March of that data collection year. However, since 1994, the number of employees is for the month of October of that data collection year—implying a 1-year observation lag between sales and the number of employees since 1994. We’ll assume that, until 1993, the information on the number of employees is coincidental with the information on sales. In this case, the observation year for both variables is the one before the data collection. After 1994, we need to lag the number of employees one year, so that sales collected in a given year coincides with the number of employees collected the year before. In this case, after 1994, sales and lagged employees refer both to the observation year prior to the data collection year. This procedure implies a missing observation for employees in the observation year 1993. we compute the number of employees in this year as the average between the number of employees in March 1993 (collected in 1993) and the number of employees in October 1994 (collected in 1994). It follows that there is no missing observation, due to this procedure, for the number of employees from observation year 1981 until 2005.

1.2 A.2 Sectoral codes

The sectoral codes are CAE codes (Portuguese Classification of Economic Activities), Revision 2 (REV2). The challenge is to obtain codes that are consistent through time. The codes were revised twice since 1982, in 1995 and again in 2003. The 2003 change (from REV2 to REV2.1) is minimal, and affects only a couple of 3-digit codes (516 and 519, which can be easily recoded back to their REV2 values). The 1995 change (from REV1 to REV2) is more comprehensive, and sometimes there is not a one-to-one mapping between REV1 and REV2 codes at the 3-digit level, and more often at the 2-digit level. Another issue is that there is a non-negligible fraction of firms that change sectoral code for reasons unrelated to the official revision. We assigned REV2 codes to REV1 codes using the following rule. From 1994 to 1995, we assumed that every code change was due to the official revision. For each REV1 code in 1994, we computed the modal REV2 code, to which the largest number of firms switched in 1995. We attributed this code to firms that exited the sample before 1994.

1.3 A.3 Sample selection

We eliminated observations with missing number of employees. We also eliminated firms with a share of public capital larger than 50% at any point in the sample. Finally, we eliminated firms in sectors that either tend to be highly-regulated, or are not primarily engaged in market activities: utilities (2-digit codes 40 and 41), public mail (3-digit sector 641), financial (2-digit codes 65, 66 and 67), public administration (2-digit code 75), education (2-digit code 80), health (2-digit code 85), public cleaning (2-digit code 90), individual’s associations (2-digit code 90), and international organizations (2-digit code 99). We also eliminated firms with sector code 000000.

Table 3 contains the subset of sector codes that are used in this study, after applying the sample selection criteria.

Appendix B: Transitional dynamics

We consider the economy with exogenous TFP growth, as described in Section 4.1. For any variable x t , let its detrended value be \(\widehat{x}_t=\gamma^{-\frac{1}{1-\alpha}t}x_t\).

The price level p and the relative size Q are constant in a balanced-growth path. Also, detrended transfers depend on the time-invariant g j (z) functions. Since these objects are time-invariant, they may be computed independently from initial conditions. Given an initial level of capital supply \(\hat{K}^S_0\), the economy’s transition path is then fully characterized by sequences \(\{\hat{K}^S_{t+1}\}_{t=0}^\infty\), \(\{\hat{K}^D_{t}\}_{t=0}^\infty\), \(\{\hat{k}_{It}\}_{t=0}^\infty\), \(\{N_t\}_{t=0}^\infty\), \(\{r_t\}_{t=0}^\infty\) which solve:

where

The above system of equations defines the economy’s transition mapping, from \(\left(N_t,\hat{K}_t^S\right)\) into \(\left(N_{t+1},\hat{K}_{t+1}^S\right)\). Given \(\hat{K}^S_0>0\), one needs to compute the unique value of N 0 that puts the economy on the saddle path. In practice, N 0 is computed as the value such that the economy converges to the steady-state starting from \(\left(N_0,\hat{K}_0^S\right)\). The full solution sequences are obtained in the process of solving for N 0, by iterating forward on the economy’s transition function.

About this article

Cite this article

Castro, R., Clementi, G.L. The economic effects of improving investor rights in Portugal. Port Econ J 8, 59–97 (2009). https://doi.org/10.1007/s10258-009-0043-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10258-009-0043-y

Keywords

- Macroeconomics

- Investment rate

- Relative prices

- Resource misallocation

- Investor protection

- Optimal contracts

- Portugal