Abstract

While the solvency analysis of immediate life annuity portfolios has been extensively studied, the case of deferred annuities has received comparatively much less attention. We assess the importance and effect of stochastic mortality models and interest rates on the solvency analysis of a portfolio of deferred annuity contracts. Our analysis considers three steps: first, the benchmark case where mortality rates and interest rates are both deterministic; then, the case in which only mortality rates are stochastic is explored; finally, the full model where both mortality rates and interest rates are stochastic. The results demonstrate the model risk stemming from the uncertainty in the mortality models and its impact on the evaluation of solvency margins for life annuities. The role of the deferment period is thoroughly discussed and compared to the case of immediate annuities.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Annuity products play a significant role in protecting policyholders from longevity risk, providing a minimum guaranteed income and reducing the risk of outliving their retirement assets. Regulators therefore have a strong incentive to achieve a deep understanding of the solvability of annuity portfolios and the impact of systematic longevity risk. While immediate life annuities have been studied extensively, deferred annuities products play an equally important role as they are commonly sold, being relatively more affordable. The solvency of deferred annuities portfolios has not been considered thoroughly in the literature, and this paper aims at filling this gap.

Yaari (1965) demonstrates that a risk averse individual should convert all of his/her assets to an immediate annuity due to the fact that people who die earlier subsidise those who live longer. However, the evidence shows that retirees are reluctant to convert retirement savings into annuities voluntarily. Many theories have been brought forward to explain this so-called “annuity puzzle”. As a result of the discounting effect and the possibility that annuitants may not survive the deferment period, a deferred annuity is much cheaper than an immediate annuity with identical benefits and therefore plays an important role in households’ portfolios. Wei-Yin and Scott (2007) apply cumulative prospect theory to the analysis of annuities and demonstrate that it can explain the low demand for immediate annuities purchased at retirement and higher preference for deferred annuities. Chen et al. (2019) extend this analysis and show that immediate annuities are not attractive for retirees at all ages due to loss aversion and preferences for deferred annuities increase with the deferred period. Moreover, Chen et al. (2020) demonstrate that a hyperbolic discount model can explain the low demand of immediate annuities at retirement and greater attractiveness of long-term deferred annuities.

In this paper we analyse the solvency capital of deferred annuities portfolios using different assumptions and scenarios for longevity and investment risk. Hypotheses about underlying mortality and interest rate dynamics play an important role in the solvency assessment of life annuity contracts. By comparing the results for deterministic and stochastic mortality models we estimate the importance and effect of random changes in the mortality for solvency analysis. The systematic risk component is analysed in Coppola et al. (2000), Coppola et al. (2002), Olivieri (2001), and Pitacco (2004). Olivieri and Pitacco (2003) use a finite range of mortality scenarios and differentiate between pooling and non-pooling risks. In contrast, De Waegenaere et al. (2010) examine pension annuities in a generalized Lee-Carter model. The stochastic Gompertz-model is used in Christiansen and Helwich (2008) both for temporary life and pure endowment insurance. Bauer and Weber (2008) and Hari et al. (2008) calculate VaR and expected shortfall for immediate life annuities using different static hedging scenarios. Jarner and Møller (2015) consider a partial internal model for longevity risk, focusing in particular on the role of the unsystematic element related to the size of the portfolio. Gylys and Šiaulys (2019) compare, for a portfolio of term assurances, the run-off and 1-year Value-at-Risk under a Lee-Carter model to the results of the Solvency II standard formula

Several stochastic mortality models have been proposed in the literature, see Cairns et al. (2009) for a review of some of the most commonly used ones. The choice of a model requires significant judgement by the analyst and a change in the model can significantly impact solvency margins and the best estimate reserves (Richards and Currie 2009). Therefore, model risk is particularly important, and its assessment requires the evaluation of many stochastic mortality framework.

We extend the solvency analysis approach of Olivieri and Pitacco (2003) to assess solvency margins for deferred annuities for a range of deferment periods. Deferred life annuities are policies providing life-long payments to the annuitants after a certain period of time, conditional on survival. Therefore, exposure to longevity risk and interest rate risk is an important factor due to the long term nature of the contract and the possibly long duration of contribution and benefit payments. Therefore, we aim at contributing to the existing literature on deferred annuities by estimating the combined effects of stochastic mortality and investment returns on the solvency of a portfolio of deferred annuities. The results are then compared to those obtained under a deterministic counterpart. Essentially, our analysis contains three risk scenarios: the benchmark case where mortality rates and interest rates are both deterministic; a second case where only mortality rates are stochastic; a third case where mortality rates and interest rates are both stochastic. To isolate the effect of these risks, we disregard expenses and inflation although these can be easily introduced in a simulation based approach.

We observe that the risk of random fluctuations in mortality decreases with increasing cohort size because fluctuations are smoothed in large homogeneous portfolios. Our results show the importance of systematic risk in comparison to the risk of random fluctuations. Moreover, the paper outlines the relevance of model risk and deferment period in the estimation of solvency margins.

The structure of this paper is as follows: Sect. 2 describes the general model for calculation of solvency margins. In Sect. 3 we review the approach of Olivieri and Pitacco (2003) and our adjustment to deferred annuities of the CMI reduction factor based approach, see CMI (2016). Section 4 discusses different stochastic mortality models and calculation of solvency margins for these models with deterministic interest rates, while Sect. 5 extends the previous analysis to the case of stochastic interest rates. Section 6 concludes the paper.

2 General model for solvency margins

We consider a portfolio of \(N_{0}\) identical deferred life annuities-due with payments starting at \(d\ge 0\) and continuing as long as the insured is alive. Without loss of generality, we can assume that payments will in any case stop after \(n=\omega -x_0\) years, where \(x_0\) is the common initial age of the insureds and \(\omega \) denotes the biological age limit. A single premium P is paid at contract inception, so that the insurer’s premium income at time 0 is \(N_0P\). Insureds are assumed to be homogeneous, so their residual lifetimes can be taken to be identically distributed.

Let \(N_{t}\) denote the random number of individuals alive at time t (that is at age \(x_0+t\)), so the random number of deaths in the time interval \([t,t + 1)\) is \(D_{t}=N_{t}-N_{t+1}\). The portfolio reserve at time \(t=0,\ldots ,n\) is denoted by \(\mathcal {V}_t\) and given by

where \(V_t\) is the time t individual reserve, calculated according to a given basis. For simplicity, in the following it will be assumed that the reserve and premium basis coincide, so that in particular \(V_0=P\).

The random portfolio fund at time \(t=0,\ldots ,n\) is denoted by \(Z_t\) and given by the following relations:

where \(I_t\) is the (possibly random) rate of return earned by the fund over the period \([t-1,t)\), C is the initial capital and \(\mathcal {R}_t\) is the portfolio’s annuity outflow at time t, defined by

where R is the annuity instalment.Footnote 1 In practice, the initial capital C can be partially financed by an additional premium loading.Footnote 2

The quantity \(Z_t-\mathcal {V}_t\) is called free portfolio fund at time t. Inspired by the different possible solvency criteria set out in Olivieri and Pitacco (2003), we focus on the minimum amount of initial capital necessary for the free portfolio fund to be positive at a given horizon, with a given confidence level. More precisely, the solvency margin or risk-based capital RBCFootnote 3 is the minimum initial capital C, required at time 0 on top of the premium income, guaranteeing the condition

where \(\varepsilon \) is the ruin probability. This correspond to a Value-at-Risk calculation at level \(1-\varepsilon \) for the free portfolio fund at the target horizon. Since the premium and reserve basis agree, the initial free fund and the solvency margin coincide:

The relative solvency margin \(\text {RBC}_{\%}=\frac{\text {RBC}}{\mathcal {V}_0}\) gives the required solvency capital as a percentage of the initial reserve/premium income.

While the Value-at-Risk has been widely employed in the financial and insurance industry, its use has been frequently challenged and some alternative measures have been proposed, see McNeil et al. (2015). In particular, the expected shortfall (ES) has found consistent use in the financial sector. The expected shortfall is a coherent risk measure, meaning that if several portfolios are combined, the total expected shortfall decreases, hence reflecting the benefit of diversification. Further, the ES is more conservative than the Value-at-Risk, when calculated with the same ruin probability. In the context of this paper, the expected shortfall is calculated, for a given ruin probability \(\varepsilon \), as

Similarly, the expected shortfall can be expressed in percentage of the initial reserve/premium income as \(\text {ES}_{\%}=\frac{\text {ES}}{\mathcal {V}_0}\).

In general, we assume that there are two sources of mortality uncertainty, one due to process risk, stemming from the individual times of death and eliminable through pooling, and another one due to the systematic risk linked to the uncertainty in future death rates. Therefore, we model the evolution of the number of survivors through

where \(q_{y,t}\) is the one-year death probability for an insured aged y prevailing at time t. These probabilities are drawn from a (possibly stochastic) best estimate mortality model used for the calculation of solvency margins. Implicit in the above assumption is that insured lifetimes are independent and identically distributed conditional on knowledge of the future death probabilities.

We analyse portfolios of identical immediate annuities, with annual instalment of \(R=100\), paid to policyholders with initial age \(x_0=65\). Different deferment periods \(d=0,\,5,\,10,\,20,\,30\), the case \(d=0\) being that of immediate annuities as in Olivieri and Pitacco (2003), and of solvency horizons \(T=5,\,10,\,n\), where \(n=\omega -x_0\), are considered. When \(T=n\) is used, a run-off perspective is adopted where solvency is analysed after the cohort of annuitants has become extinct and the free portfolio fund is given by the fund, as the reserve is then 0. Unless otherwise specified, the probability of ruin is set at \(\varepsilon =0.025\) and the initial portfolio sizes \(N_0=10^h,\,2\le h\le 5\) are used. The constant annual interest rate used for the calculation of the premium and the reserves is \(i=0.03\), while the corresponding life table, together with the best estimate mortality model for the solvency margin calculation, will be specified in the next Section.

We calculate absolute and relative solvency margins (the latter reported simply as ‘solvency margin’ in the y-axis label in Figures 1, 2, 3, 4, 5) for immediate and deferred annuities portfolios under different sets of assumptions. Section 3 considers the case of best estimate mortality rates drawn from a finite set of scenarios, as in Olivieri and Pitacco (2003). Section 4 extends the analysis to a range of full stochastic mortality models. In these Sections the return earned by the fund is deterministic and supposed to coincide with the technical rate used for premium and reserves, \(I_t=0.03\) for all t. This assumption is then dropped in Sect. 5.

3 Solvency margins under scenario based mortality projections

In this section we introduce a simplified scenario-based model used to project future mortality rates and the implications for solvency margins. As in Olivieri and Pitacco (2003), a finite set of scenarios—that is life tables—is considered, together with a subjective “degree of belief” assigned to each one of them. We choose three sets of projected mortality rates, denoted by \(q^{[\text {low}]}\), \(q^{[\text {avg}]}\) and \(q^{[\text {high}]}\) corresponding to a small, medium and high mortality scenario, respectively. When a full degree of belief is attached to \(q^{[\text {avg}]}\), the special case of a deterministic approach, where only process risk is considered, is retrieved. We choose \(q^{[\text {low}]}\), \(q^{[\text {avg}]}\) and \(q^{[\text {high}]}\) using the mortality projection model developed by the IFoA’s CMI (CMI 2016), as follows. We consider England and Wales males data obtained from the Human Mortality Database (HMD 2020), containing age-specific numbers of deaths and exposures for the period \(1965-2011\) and ages \(0-100\), calculate the corresponding death rates and use quadratic interpolation to close each life table and obtain death rates for the ages \(101-120\) as well. We then calculate annual mortality improvement rates by single year of ageFootnote 4 for the period 1965–2011 and observe that the maximum, average and minimum levels of such improvement rates, across all ages, have been \(4.16\%\), \(2.34\%\) and \(0.16\%\) respectively.Footnote 5 Noting that current mortality trends (since 2011) imply that mortality improvement rates in the future are likely to be lower, see Murphy and Grundy (2022), we apply a \(20\%\) decrease to the maximum mortality improvement rate. This figure is subjective and acknowledges that, in this scenario, future improvement rates will be higher than experienced in the last decade but still not as high as pre 2010. Finally, the maximum, average and minimum level of improvement rates are used as input for the CMI model to obtain the projected \(q^{[\text {low}]}\), \(q^{[\text {avg}]}\) and \(q^{[\text {high}]}\), respectively. We assign weights \(\rho ^{[\text {low}]}=0.2\), \(\rho ^{[\text {avg}]}=0.6\) and \(\rho ^{[\text {high}]}=0.2\) to the three scenarios. The single premium and the reserves are calculated according to the (deterministic) scenario \(q^{[\text {avg}]}\). The choice of the weights is completely subjective and reflects the possible belief of an end user who attach most confidence to the average scenario, but feels that deviations from it resulting into higher or lower death trajectories are likely. Clearly, the numerical examples of this section are strongly dependent on the choice of the weight for each scenario.

The solvency margins using the deterministic mortality model are reported in Tables 1, 2, 3 for different initial portfolio sizes, solvency horizons and ruin probabilities. The solvency capital obviously increases with the target solvency horizon, reflecting the higher uncertainty in fund results. As far as the size of the portfolio is concerned, Table 1 shows the extent of the pooling effect on the required margin. Recall that, using a deterministic mortality model, the insurance company is only exposed to diversifiable risk, which stems from an insufficiently large cohort. It can be observed that the relative solvency margins RBC\(_{\%}\) are higher for the deferred annuity portfolios than the corresponding values for the immediate annuities, whereas the absolute solvency margins RBC are lower. Clearly, in any state of the world there are less benefit payments over the target period in the case of deferred annuities. Therefore, lower reserves are required to be held. However, the relative solvency margin RBC\(_{\%}\) is higher due to the comparatively greater uncertainty associated with the postponed beginning of the benefit payments. Table 2 investigates the dependence of the solvency margin on the ruin probability, showing the extra capital necessary to satisfy a more stringent solvency criterion. While small portfolios are extremely penalized, the relative capital rapidly stabilize as the size of the portfolio grows to a reasonable size. Finally, Table 3 expands on Table 1 and demonstrates the dependence of the solvency margin on the deferment period. As hinted at before, a higher relative solvency margin is needed when the deferment period is extended. However, RBC\(_{\%}\) is unchanged when the target solvency horizon precedes the annuity payout phase, that is \(d\ge T\). This is intuitive, considering that there are no annuity cash flows before solvency is checked, therefore at contract inception the company needs to hold the same relative solvency margin in order to be solvent.

By using a deterministic life table as a model for best estimate future mortality rates, the insurance company essentially assumes that demographic risk can be diversified away completely by pooling a large number of similar individuals. To include non-pooling risk affecting each individual’s mortality in the same manner, a stochastic mortality model is needed.

Table 4 reports relative solvency margins for different combinations of portfolio sizes, solvency target horizons and deferment periods. The required capital now reflects both systematic (longevity) and diversifiable risk, and a comparison with Table 3 provides an insight on the relevance of these components as a function of the deferment period. It can be seen how the contribution of non pooling risk exacerbates as the portfolio size increases, and this effect compounds with the length of the deferment period. In relative terms, the insurer is better off with a smaller portfolio size. Also, the effect of systematic risk is sensibly lower when a run-off perspective is adopted, as solvency is assessed when the cohort of insured is extinct.

4 Solvency margins under fully stochastic mortality models

The scenario based stochastic mortality model in Sect. 3 is “static” as, one of the scenarios is drawn, the corresponding mortality table is used for all future rates. Therefore, there is no allowance for a dynamic evolution of future mortality rates, in particular for changes in mortality trend over time. Also, results depend on the choice of scenario weights, which is inevitably subjective. This section considers a set of stochastic mortality projection models which are fitted on past data and used to generate future patterns of mortality rates. These models are essentially capable of generating infinitely many mortality scenarios. Further, the degree of subjectivity is limited to the model specification and its forecasting component. Nonetheless each model has its specific features and assumptions, and will generate different solvency capital requirements. The results in this section are also useful in order to understand the model risk implicit in such an exercise, therefore providing an invaluable yardstick for the range of solvency capital required to an insurance company.

Consistently with the choice made in Sect. 2, the number of deaths at age x and calendar year t in the general population is considered to follow a Binomial distribution:

where \(q_{x,t}\) is the one year death rate for age x prevailing at time t and \(E_{x,t}^0\) is the population matching initial exposed to risk. Following Villegas et al. (2018), the death rates are modelled through

where \(\eta _{xt}\) is the predictor which is then characterized by a given combination of age and time specific terms and/or cohort terms. For the purpose of this paper we use six representative models having distinct features such as the presence of a cohort term, the number of time indices and age modulating terms and whether age is treated as a quantitative or categorical variable. The models and corresponding equations are listed below.

-

Lee–Carter (LC) model, see Lee and Carter (1992):

$$\begin{aligned} \eta _{xt}=\alpha _x+\beta _x^{(1)}k_t^{(1)}. \end{aligned}$$ -

Renshaw–Haberman (RH) model, see Renshaw and Haberman (2006) and Haberman and Renshaw (2011), which generalises the LC model by incorporating a cohort effect:

$$\begin{aligned} \eta _{xt}=\alpha _x+\beta _x^{(1)}k_t^{(1)}+\gamma _{t-x}. \end{aligned}$$ -

Age-period-cohort (APC) model, which is a special case of the RH model when \(\beta _x^{(1)}=1\):

$$\begin{aligned} \eta _{xt}=\alpha _x+k_t^{(1)}+\gamma _{t-x}. \end{aligned}$$ -

CBD model, see Cairns et al. (2006), with two age-period terms and pre-specified age-modulating parameters:

$$\begin{aligned} \eta _{xt}=k_t^{(1)}+(x-\bar{x})k_t^{(2)}, \end{aligned}$$where \(\bar{x}\) is the average age in the data set.

-

M7 model, see Cairns et al. (2009), which expands the CBD model by adding a quadratic term and a cohort effects:

$$\begin{aligned} \eta _{xt}=k_t^{(1)}+(x-\bar{x})k_t^{(2)}+((x-\bar{x})^2-\hat{\sigma }_x^2)k_t^{(3)}+\gamma _{t-x}, \end{aligned}$$where \(\hat{\sigma }_x^2\) is the average value of \( (x-\bar{x})^2\).

-

Plat model, see Plat (2009), in which features of the LC and CBD models are combined:

$$\begin{aligned} \eta _{xt}=\alpha _x+k_t^{(1)}+(x-\bar{x})k_t^{(2)}+(x-\bar{x})^{+}k_t^{(3)}+\gamma _{t-x}, \end{aligned}$$where \(z^+=\max \{0,z\}\).

Some of the models listed above have been presented under slightly different assumptions - for instance the number of deaths is frequently modelled using a Poisson distribution rather than Binomial. Also, several alternative models could be employed, but the structures considered here are a representative sample as they include some key features, see Table 5 for a summary and Villegas et al. (2018) for a general approach to the construction, calibration and projection of stochastic mortality models.

Once models are estimated with maximum likelihood, the time indices and cohort term are fitted and projected into the future so that simulation of future mortality rates can be obtained. Consistently with the prevailing literature, see Villegas et al. (2018), the time indexes are projected using a multivariate random walk with drift while the cohort term, when present, is modelled as an ARIMA(1,1,0), independently of the time indexes.

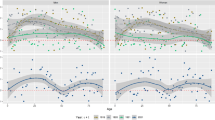

Figure 1 shows relative solvency margins, with associated 95% confidence intervals, for the 6 stochastic mortality models and different portfolio sizes. It can be seen that solvency margins decrease with the portfolio size, converging to an asymptotic value reflecting the non-pooling effect of longevity risk. Table 6 presents the relative required margins for all the models, different portfolio sizes and deferment periods when \(T=n\). For each combination of contract parameters, it can be seen how the required capital varies through the range of models, exemplifying the model risk. For a longer deferment period, the range of required capital remains wide regardless of the portfolio size. This is expanded in Fig. 2, where relative solvency margins are plotted against the deferment period, showing how model risk widens with d. It can be seen that models M7 and CBD imply higher solvency margins, whereas the LC model has consistently the lowest values.

Relative solvency margins (RBC\(_{\%}\)) for different stochastic mortality models and associated \(95\%\) confidence intervals, 5 years deferment period and \(T=n\)

Relative solvency margins (RBC\(_{\%}\)) for different stochastic mortality models, deferment periods and \(T=n\)

Tables 7, 8, 9, 10, 11 and 12 provide relative solvency margins and expected shortfalls for different target solvency horizons and deferment periods for LC, RH, APC, CBD, M7 and Plat, respectively. For each model, the solvency margin increases with the target horizon due to the greater uncertainty. For a given choice of contract parameters, there is a remarkable spread between the results obtained in Sect. 3 with the deterministic and scenario mortality model and the results in the present section. These differences also vary depending on deferment period and target horizon. The tables display both the RBC and the expected shortfall (ES\(_{\%}\)), as the latter provides information about the extent of the loss when the free fund is negative at the target horizon. When the smallest target horizon is considered, i.e. \(T=5\), the results for the RH and APC models are quite similar and higher than those for the other models, with the CBD and Plat models attaining the lowest values. Conversely, the Plat model has one of the highest required capital when a run-off perspective is adopted, that is \(T=n\). The LC model has the smallest gap between the \(T=5\) and \(T=n\) cases. The choice of model often involves significant judgement by the analyst and, as we can see, a change in model can lead to material changes in solvency margins. The M7 model produces the largest solvency margins under both the VaR and ES. As such, it is the most conservative model and therefore it is of particular interest for regulators and supervisory authorities.

Summarizing the results, it seems that the most important model feature driving differences in solvency margins across the different dimensions is the model complexity as captured by the number of time factors with a second order effect due to the presence of the cohort term. The LC model, the simplest of all models considered, seems to consistently produce overly optimistic capital requirements for any portfolio size or deferment period. Next in rank are the RH and APC models. The former extends the LC with the inclusion of the cohort term, while the latter simplifies the RH model by constraining the age modulating parameter to a constant. The solvency margins are higher than those implied by the LC with narrow differences between the two models. It should be noted here that the cohort term need not be simulated as, for the case considered of 65 years old pensioners in 2011, it is known. Finally, models with more than one time factor produce conservative capital requirements across all portfolio sizes and deferment period. Clearly, the driving force is the greater uncertainty stemming from the presence of two stochastic ingredients, further increasing with the simulation horizon. The hybrid Plat model seems to be a partial exception, as results are comparable to those of the – apparently simpler – CBD model.

5 Stochastic interest rates

This section compounds on the previous ones and adds stochastic returns to the fund dynamics, investigating the effects on capital requirements of this additional uncertainty layer. We use the Vasicek model, see Vasicek (1977), to generate simulations of the short interest rate. It is assumed that the short rate \(r_t\), the unique source of interest rate risk in this model, follows the dynamics

where \({W_t}\) is a standard Wiener process and a, \(\gamma \) and \(\sigma \) are positive constants representing the speed of mean reversion, the long term mean and the volatility of the short rate, respectively. The random return of the portfolio fund, see (2), is given by \(I_t=e^{r_{t-1}}-1\), the latter expression implicitly assuming that the short rate remains constant over \([t-1,t)\). The parameters for the Vasicek model are given in Table 13. These parameters were chosen so that they reflect adequate stochastic fluctuations from the rate of return used in the previous sections and match the overall performance of assets, resulting from both market behaviour and the investment strategy of an insurance company. We also consider alternative values for the volatility \(\sigma \). As for the mortality model, we only consider the M7 and Plat model as these were generating the largest solvency requirements in the previous section.

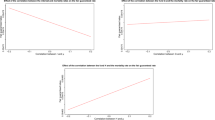

Figures 3, 4, 5 plot the relative solvency requirements with associated 95% confidence intervals, with or without stochastic interest rates for the three volatility scenarios, respectively. The greater severity of solvency margins is due to the fact that assets, cumulating at a random rate, are compared with the reserve, calculated according to a deterministic financial hypotheses which could be significantly different from the actual investment performance. The solvency margins in M7 model combined with Vasicek model are higher and the corresponding confidence intervals are wider than in Plat model.

Relative solvency margins RBC\(_{\%}\) and corresponding \(95\%\) confidence intervals for the M7 and Plat models, Vasicek interest rate model with \(\sigma =0.05\), \(d=5\) and \(T=n\)

Relative solvency margins RBC\(_{\%}\) and corresponding \(95\%\) confidence intervals for the M7 and Plat models, Vasicek interest rate model with \(\sigma =0.1\), \(d=5\) and \(T=n\)

Relative solvency margins RBC\(_{\%}\) and corresponding \(95\%\) confidence intervals for the M7 and Plat models, Vasicek interest rate model with \(\sigma =0.2\), \(d=5\) and \(T=n\)

Further, the confidence intervals for both M7 and Plat models in case of stochastic interest rates are much wider than those when interest rates are deterministic. While confidence intervals narrow down with the portfolio size, the asymptotic width reflect the overall systematic interest rate and mortality risk. The effect of stochastic interest rates on the overall width of confidence intervals in comparison with those in Sect. 4 is significant due to the non-pooling nature of interest rate risk. Moreover, it can be remarked that with greater interest rate volatility the solvency margins and their confidence intervals also increase reflecting higher levels of uncertainty.

6 Conclusions

Solvency requirements for deferred annuities have been analysed and compared to those of immediate annuities. Particular focus has been placed on the longevity risk. This has been incorporated to the analysis using different deterministic and stochastic models, particularly the family of generalized age-period-cohort stochastic mortality models. Several numerical examples illustrate solvency requirements produced by these different approaches to longevity risk. The results demonstrate the dramatic importance of the mortality models on evaluation of solvency margins for life annuities and the fact that model risk is a prevalent issue when forecasting solvency margins. Another focus of this paper is the deferment period and its effect on solvency requirements. The margins increase with longer deferment periods which is caused by the extra longevity risk and the greater uncertainty about numbers of future survivors. Section 5 explores the impact of stochastic interest rates on solvency margins and corresponding confidence intervals.

The analysis could be extended, by considering some realistic features such as level premiums, return of premium guarantees in case of premature death and guaranteed annuity during the payout phase. Each one, or combinations, of such provisions will affect the solvency margin in a way that may not be easily anticipated.

While the paper has focused most of its attention on model risk, with all models calibrated on the same fixed sample, another dimension worth exploring would involve the dependence of results on the fitting period. It is well known, see for instance Cairns et al. (2011); Basellini et al. (2023), that mortality forecasts can be highly sensitive to the length of historical data employed in the estimation process. In turn, simulations and solvency margins may also be affected. Two routes seems viable in that respect. One may engage in a careful examination of available models, seeking for the most appropriate compromise between forecasting accuracy and robustness with respect to the fitting period. Alternatively, a fully fledged model averaging approach where a range of mortality models, trained over different periods, are combined through a weighing process to produce robust results, see for instance Benchimol et al. (2016) and Shang (2012).

Notes

In practice, there will be variability of the annuity instalments across the portfolio. This heterogeneity will result in higher capital requirements than those that will be calculated in the following sections. In Clemente et al. (2022) a model to quantify demographic risk over an annual time horizon, allowing for the variability of the sum assured and consistent with Solvency II, is proposed.

In the rest of the paper we use the term solvency margin not to be confused with the solvency capital requirement (SCR), which, in the context of Solvency II, refers to a 1 year horizon capital requirement.

The improvement rate for a given age x and period \((t,t+1)\) is given by \(\frac{q_{x,t}-q_{x,t+1}}{q_{x,t}}\), where \(q_{x,t}\) is the one year death rate for age x prevailing at time t. See Richards et al. (2006), Baxter (2007) and Haberman and Renshaw (2012), also for possible alternative definitions of the improvement rates.

In this calculation, negative mortality improvement rates have been excluded.

References

Basellini, U., Camarda, C.G., Booth, H.: Thirty years on: a review of the Lee-Carter method for forecasting mortality. Int. J. Forecast. 39(3), 1033–1049 (2023). (ISSN 0169-2070)

Bauer, D., Weber, F.: Assessing investment and longevity risks within immediate annuities. Asia-Pacific J. Risk Insur. 3(1), 1 (2008)

Baxter, S.: Should projections of mortality improvements be subject to a minimum value? Br. Actuar. J. 13(3), 375–464 (2007)

Benchimol A.G., Alonso P.J., Marín Díazaraque J.M., Albarrán Lozano I. : Model uncertainty approach in mortality projection with model assembling methodologies (2016)

Cairns, A.J.G., Blake, D., Dowd, K.: A two-factor model for stochastic mortality with parameter uncertainty: theory and calibration. J. Risk Insur. 73(4), 687–718 (2006)

Cairns, A.J.G., Blake, D., Dowd, K., Coughlan, G.D., Epstein, D., Ong, A., Balevich, I.: A quantitative comparison of stochastic mortality models using data from England and Wales and the United States. North Am. Actuar. J. 13(1), 1–35 (2009)

Cairns, A.J.G., Blake, D., Dowd, K., Coughlan, G.D., Epstein, D.: Mortality density forecasts: an analysis of six stochastic mortality models. Insur. Math. Econom. 48(3), 355–367 (2011). (ISSN 0167-6687)

Chen, A., Haberman, S., Thomas, S.: Cumulative prospect theory, deferred annuities and the annuity puzzle. Rev. Behav. Finance 11(3), 277–293 (2019)

Chen, A., Haberman, S., Thomas, S.: The implication of the hyperbolic discount model for the annuitisation decisions. J. Pension Econ. Finance 19(3), 372–391 (2020)

Christiansen, M.C., Helwich, M.: Some further ideas concerning the interaction between insurance and investment risks. Bl. DGVFM 29(2), 253–266 (2008)

Clemente, G.P., Della Corte, F., Savelli, N.: A stochastic model for capital requirement assessment for mortality and longevity risk, focusing on idiosyncratic and trend components. Ann. Actuar. Sci. 16(3), 527–546 (2022)

CMI. Mortality Projections Committee (2016)

Coppola, M., Di Lorenzo, E., Sibillo, M.: Risk sources in a life annuity portfolio: decomposition and measurement tools. J. Actuar. Pract. 2000(8), 43–62 (2000)

Coppola, M., Di Lorenzo, E., Sibillo, M.: Further remarks on risk sources measuring: the case of a life annuity portfolio. J. Actuar. Pract. 2002(10), 229–242 (2002)

De Waegenaere, A., Melenberg, B., Stevens, R.: Longevity Risk. De Economist 158(2), 151–192 (2010)

Gylys, R., Šiaulys, J.: Revisiting calibration of the Solvency II standard formula for mortality risk: does the standard stress scenario provide an adequate approximation of value-at-risk? Risks 7(2), 58 (2019)

Haberman, S., Renshaw, A.E.: A comparative study of parametric mortality projection models. Insur. Math. Econom. 48(1), 35–55 (2011)

Haberman, S., Renshaw, A.E.: Parametric mortality improvement rate modelling and projecting. Insur. Math. Econ. 50(3), 309–333 (2012)

Hari, N., De Waegenaere, A., Melenberg, B., Nijman, T.E.: Longevity risk in portfolios of pension annuities. Insur. Math. Econom. 42(2), 505–519 (2008)

HMD. University of California, Berkeley (USA), and Max Planck Institute for Demographic Research (Germany). Available at www.mortality.org and www.humanmortality.de, (2020)

Wei-Yin, H., Scott, J.S.: Behavioral obstacles in the annuity market. Financ. Anal. J. 63(6), 71–82 (2007)

Jarner, S.F., Møller, T.: A partial internal model for longevity risk. Scand. Actuar. J. 4, 352–382 (2015)

Lee, R.D., Carter, L.R.: Modeling and forecasting US mortality. J. Am. Stat. Assoc. 87(419), 659–671 (1992)

McNeil, A.J., Frey, R., Embrechts, P.: Quantitative Risk Management: Concepts, Techniques and Tools. Princeton University Press, Princeton (2015)

Murphy, M.J., Grundy, E.M.: Slowdown in mortality improvement in the past decade: a US/UK comparison. J. Gerontol. Ser. B 77(Supplement-2), S138–S147 (2022)

Olivieri, A.: Uncertainty in mortality projections: an actuarial perspective. Insur. Math. Econom. 29(2), 231–245 (2001)

Olivieri, A., Pitacco, E.: Solvency requirements for pension annuities. J. Pension Econ. Finance 2(2), 127–157 (2003)

Pitacco, E: Longevity risk in living benefits. developing an annuity market in Europe, Fornero, E. and Luciano, E. Eds, (2004)

Plat, R.: On stochastic mortality modeling. Insur. Math. Econom. 45(3), 393–404 (2009)

Renshaw, A.E., Haberman, S.: A cohort-based extension to the Lee-Carter model for mortality reduction factors. Insur. Math. Econom. 38(3), 556–570 (2006)

Richards, S.J., Currie, I.D.: Longevity risk and annuity pricing with the Lee-Carter model. Br. Actuar. J. 15(2), 317–343 (2009)

Richards, S.J., Kirkby, J.G., Currie, I.D.: The importance of year of birth in two-dimensional mortality data. Br. Actuar. J. 12(1), 5–38 (2006)

Shang, H.L.: Point and interval forecasts of age-specific life expectancies: a model averaging approach. Demogr. Res. 27(21), 593–644 (2012)

Vasicek, O.: An equilibrium characterization of the term structure. J. Financ. Econ. 5(2), 177–188 (1977)

Villegas, A., Millossovich, P, Kaishev, VK.: StMoMo: an R package for stochastic mortality modelling. J. Stat. Softw.84(3) (2018)

Yaari, Menahem E..: Uncertain Lifetime, Life Insurance, and the Theory of the Consumer. Rev. Econ. Stud. 32(2), 137 (1965). https://doi.org/10.2307/2296058

Acknowledgements

The Authors thank two referees for their insightful comments that greatly improved the paper.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

There were no potential Conflict of interest among the authors or funding sources.

Ethical approval

As the nature of this research did not involve any sensitive or potentially harmful topics, no ethical issues were encountered during the study, and therefore no ethical approvals or special permissions were required

Human or animal participants

The research did not involve Human Participants and/or Animals.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Gasimova, K., Haberman, S. & Millossovich, P. Solvency analysis of deferred annuities. Decisions Econ Finan (2024). https://doi.org/10.1007/s10203-024-00452-2

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s10203-024-00452-2