Abstract

A retiree’s appetite for risk is a common input into the lifetime utility models that are traditionally used to find optimal strategies for the decumulation of retirement savings. In this work, we consider a retiree with potentially differing appetites for the key financial risks of decumulation: liquidity risk and investment risk. We set out to determine whether these differing risk appetites have a significant impact on the retiree’s optimal choice of decumulation strategy. To do so, we design and implement a framework which selects the optimal decumulation strategy from a general set of admissible strategies in line with a retiree’s goals, and under differing appetites for the key risks of decumulation. Overall, we find significant evidence to suggest that a retiree’s differing appetites for different decumulation risks will impact their optimal choice of strategy at retirement. Through an illustrative example calibrated to the Australian context, we find results which are consistent with actual behaviours in this jurisdiction (in particular, a shallow market for annuities), which lends support to our framework and may provide some new insight into the so-called annuity puzzle.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

1.1 Background

Almost all retirees face the decumulation problem of deciding how to best spread their hard-earned savings over the rest of their lives. In general, the retiree seeks to convert their savings into a desired standard of living (SOL) over retirement by choosing a strategy under a complex web of preferences, risks and constraints. Nobel laureate William Sharpe famously coined decumulation to be the “nastiest, hardest problem in finance” (Ritholz 2017), attributing the difficulty to the sheer dimensionality of the problem. Furthermore, this complex problem is not limited to the realm of finance alone, placing intergenerational strain on structures of social security and familial support.

An approach to solving the decumulation problem may be characterised by the following three attributes:

-

1.

Exogenous parameters. Any solution will be impacted by the retiree’s personal circumstances such as age x, health status and initial wealth \(W_0\) at time of retirement \(t=0\). There is also ever-changing public policy such as compulsory minimum rates of drawdown and age pension eligibility criteria.

-

2.

Optimisation framework. An architecture designed to evaluate a strategy against a stylised interpretation of the retiree’s goals and appetite for risk. Although the overarching goal of retirement is late-life fulfillment, goals are typically assumed to be strictly financial. The optimisation framework of choice is traditionally the lifetime utility framework pioneered by Yaari (1965) and Merton (1969).

-

3.

Admissible strategies. There is a rich literature which explores different decumulation strategies (and products), with Pitacco (2016), Pitacco and Tabakova (2022) and Piggott et al. (2005) exploring innovative guarantee structures and participation mechanisms. Many of these strategies may help to protect retirement savings as improvement in healthcare continues to extend life expectancy.

Hawley and Er (2022) point out the opportunity admissible strategies to better allow the retiree to purchase longevity protection as they age, as their priorities shift away from flexibility and efficiency of investment payoff. We remark that this changing demand may indicate the presence of differing appetites for the different risks of decumulation. At any given time, the retiree is unlikely to perceive the risk of experiencing poor investment returns in the same way as the financial risk of living longer than expected.

Accordingly, Milevsky and Huang (2011) distinguish between a retiree’s aversion to ‘financial’ and ‘longevity’ risks, arriving at the natural conclusion that the retiree will consume more conservatively when they are more averse to the risk of living longer than expected. However, the authors form their conclusions from the traditional lifetime utility framework under the simplifying assumption that the retiree holds a risk-free portfolio, allowing them to account for longevity risk aversion through the parameter \(\gamma \) of constant relative risk aversion.

The retirement literature is rich with work which seeks to extend the set of admissible strategies, or determine how the optimal strategy varies across retirees of different personal circumstances. Instead, Milevsky and Huang (2011) effectively varies the optimisation framework to determine how the optimal strategy will change for given exogenous parameters over a narrow set of admissible strategies. We are similarly interested in observing the sensitivity of the optimal strategy to changes in the retiree’s risk appetite, but now allowing for a more expansive set of admissible strategies and differing appetites for different risks. This interest also motivates us to develop an optimisation framework which accommodates for the additional complexity.

If these differing risk appetites have a significant impact on the retiree’s optimal choice of decumulation strategy, there emerges the opportunity to develop attractive products which both accommodate for these preferences, and promote the sustainability of our tax and transfer system for generations to come.

1.2 Contributions

To the best of our knowledge, there has been no prior literature which has explicitly considered the impact of varying the retiree’s differing appetites for different risks on the optimal strategy. We therefore lay the foundations for future work through:

-

1.

designing a framework which selects the optimal decumulation strategy from a general set of admissible strategies in line with a retiree’s goals and differing appetites for some key risks of decumulation;

-

2.

finding an admissible set of annuity-like strategies which can be integrated with drawdown to allow us to vary the distribution of outcomes according to the retiree’s preferences;

-

3.

developing a computationally efficient approach to implement the optimisation framework which conveys how the optimal strategy may vary from retiree to retiree.

Overall, we find significant evidence to suggest that a retiree’s differing appetites for different decumulation risks will impact their choice of strategy at retirement. We calibrate our model to the Australian context, and find results which are consistent with the shallow market for annuities observed in this jurisdiction. We discuss how this lends support to our framework, and can provide new insight into the annuity puzzle.

1.3 Outline of paper

In Sect. 2, we discuss two key risks to the retiree: investment risk and liquidity risk, building upon the work of Pitacco (2016) and Pitacco (2007). The latter refers to the prominent risk associated with the retiree’s need for liquidity. In Sect. 3, we construct an optimisation framework to select the strategy which best tailors the distribution of outcomes to the retiree’s differing risk appetites. We draw on the stochastic present value (SPV) methodology of Milevsky (1997) to determine the distribution of outcomes to the retiree. We follow a similar approach to Olivieri (2001) to decompose the distribution of outcomes based on investment risk and liquidity risk, and find the optimal strategy based on the retiree’s differing appetites for these risks. In Sect. 4, we find a set of admissible strategies in a generalised family of annuities which we construct with inspiration from Piggott et al. (2005). In Sect. 5, we develop an approach to implement our optimisation framework in a general context, balancing computational efficiency and numerical precision. We then apply our implementation approach in Sect. 6 through the illustrative example of the Australian context.

2 Outline of the key decumulation risks

We define a decumulation risk as a source of uncertainty with bidirectional (both upside and downside) impact on the retiree’s goals. We focus on financial goals which surround consumption and bequest, as discussed in Sect. 3.1.

2.1 Liquidity risk

We attribute liquidity risk to the uncertain timing of all liquidity events for which there is demand for significant withdrawal of retirement savings, permanently changing the retiree’s financial circumstances. We emphasise that liquidity risk cannot be well-diversified since the retiree only lives out their retirement once.

Liquidity risk can stem from death risk due to the distribution of the random remaining time \(T_x\) until the event of death; and long-term care (LTC) risk due to the random time \(T_x^{\textrm{LTC}}\) until the event of entering permanent care. Furthermore, liquidity risk can arise from a number of events such as theft, natural disaster or the need to help children for a house deposit prior to death. In general, we define \(T_x^{\textrm{ELN}}\) as the time of first early liquidity need prior to death (if any), such that \(T_x^{\textrm{ELN}}\le T_x^{\textrm{LTC}}\).

We define the first transition time by \(T_x^* = \textrm{min}(T_x, T_x^{\textrm{ELN}})\), reflecting the time at which the fund balance must be significantly withdrawn upon and circumstances permanently change. We consider these random transition times on support \({\mathcal {S}}\) where \({\bar{T}} = \sup {\mathcal {S}}\) is the final possible time of transition.

2.1.1 Death risk

Referring to De Waegenaere et al. (2010), we attribute death risk to the uncertainty surrounding the length of the retiree’s own remaining lifetime \(T_x\). We distinguish between late death risk from \(T_x\) realising a relatively large value and early death risk from \(T_x\) realising a relatively small value. A retiree is at risk of outliving their wealth in event of late death, or leaving an incidentally large bequest in event of early death.

Whether a death time is considered early or late will depend on the objective function under consideration, with life expectancy \(\mathbb {E}[T_x]\) not always serving the most appropriate benchmark. For instance, the expected value of a non-linear function in \(T_x\) (e.g. life annuity) is unlikely to be a simple function of \(\mathbb {E}[T_x]\). When a retiree participates in a pool of n lives with remaining lifetimes \(\{T_{x; i}:i = 1,\dotsc , n\}\), the earliness of the retiree’s death time can be assessed relative to the mortality experience of these pooled lives. Following Zhou (2020), we can quantify the mortality experience of the pool through observed survival probability of the pool \(_tP_x^{(n)}\):

The retiree is therefore exposed to the aggregate death risk which arises from uncertainty in \(_tP_x^{(n)}\) relative to projected survival probabilities \(_tp_x = \mathbb {E}[\mathbb {1}_{\{ T_x > t\}}]\). We refer to the terminology of Pitacco (2007) to decompose aggregate death risk into idiosyncratic and systematic components.

Pitacco (2007) defines mortality risk as the risk of deviation in the survival of the pool \(_tP_x^{(n)}\) from projected survival probabilities \(_tp_x\) due to idiosyncratic variation amongst \(\{T_{x; i}\}\). As per Börger et al. (2023), idiosyncratic mortality fluctuations in portfolios of limited size can be diversified in large populations. By the Law of Large Numbers, it follows that \(_tP_x^{(n)}\rightarrow \,_tp_x\) for \(\{T_{x; i}\}\) independent and identically distributed. However, \(\{T_{x; i}\}\) are not independent and n is far from infinite across nations with shallow annuity markets.

Pitacco (2007) defines longevity risk as the risk of deviation in the observed survival of the pool \(_tP_x^{(n)}\) from the projected survival probabilities \(_tp_x\) due to systematic variation in population longevity from projections. We define \(_tp_x^{\textrm{ref}}\) as the survival probability associated with a given reference population selected at inception of the pooling policy. Cairns et al. (2008) claim that longevity risk is non-diversifiable since it affects all individuals, stemming from uncertainty in forecasting the distribution of population rates \(_tp_x^{\textrm{ref}}\). Where pooled lifetimes \(\{T_{x; i}\}\) are all sampled with certainty from this reference population, we can define \(_tp_x^{\textrm{ref}} = \lim _{n\rightarrow \infty } \,_tP_x^{(n)}\) since we will be pooling over the population in the limit.

Blake (2018) recognises longevity risk as a dangerous ‘trend risk’, with Liu (2013) claiming it poses a gradually developed ‘chronic’ problem to annuity providers. Where the projected death hazard rate \(\lambda _{x+t}\) happens to systematically understate or overstate the observed hazard rate \(\Lambda _{x+t}\) of \( _tp_x^{\textrm{ref}}\), the deviation of \( _tp_x^{\textrm{ref}}\) from \( _tp_x\) will structurally increase over time rather than be cyclical or self-correcting. Due to this ‘toxicity’ of longevity risk, Evans and Sherris (2010) suggest there is limited appetite in the market to reinsure this risk, forcing an annuity provider to impose higher risk margins in pricing.

2.1.2 LTC risk

We attribute LTC risk to the randomness of timing \(T_x^{\textrm{LTC}}\) in when significant unplanned costs are incurred prior to death (if at all), due to the onset of senescent disability and permanent need for support (Pitacco 2016). Rice (2014) argues that retirement savings should be invested for the different ‘phases’ of retirement as needs change, so we might consider \(T_x^{\textrm{LTC}}\) as the transition time (if any) from the active phase to the frail phase of retirement. The risk of requiring LTC prior to death has become especially prominent due to the dangerous trend of rising LTC costs in excess of general price inflation (Ramsay and Oguledo 2018).

There is a potentially perilous interaction between death risk and liquidity risk. According to Sheshinski (2008), there is an intuitive negative correlation between the liquidity risk and late death risk since disability is more likely to culminate in early death. However, Zhou-Richter and Gründl (2011) and Pitacco (2016) remark that later death times can lengthen the duration of the frail phase prior to death, incurring more LTC costs and reflecting a possible form of positive correlation between the two risks.

Following Pitacco (2016), it is natural to consider the phase \(T_x - T_x^{\textrm{LTC}}\) as more likely to be longer in duration when \(T_x\) is large, conditional on the retiree incurring LTC needs prior to death.

2.2 Investment risk

We attribute investment risk to randomness in the path of real portfolio returns, as impacted by nominal portfolio returns and price inflation. In a decumulation context, we consider the risky cost of funding a unit cash flow at future time t in today’s dollars. We denote this cost by discount factor \(I(t; {\textbf{u}})\) for \(t\in {\mathcal {S}}\) and \({\textbf{u}}\) is the trading strategy driving the retiree’s investment account \(A({\textbf{u}})\). We can further write \(I(t; {\textbf{u}})= Y(t; {\textbf{u}})\Pi (t)\) where the random portfolio discount factor \(Y(t; {\textbf{u}})\) is the source of portfolio risk and the random price level \(\Pi (t)\) is the source of inflation risk. In particular, we might regard \(\Pi (t)\) as the price level associated with the retiree’s own unique basket of goods and services.

2.2.1 Portfolio risk

We consider portfolio risk to surround the sequence and scale of market returns due to randomness in the nominal rate of return on investment. A retiree will be averse to a sequence of either volatile or unexpectedly high discount factors \(Y(t;{\textbf{u}})\), creating uncertainty around the amount of investment today required to fund their future cash flows.

In its most basic form, portfolio risk is often discussed in the context of Modern Portfolio Theory (MPT, originally introduced by Markowitz 1952) typically when considering an investment return over a single period. Unlike many traditional investments, portfolio uncertainty in decumulation must be managed over a sequence of periods. In fact, Frank and Blanchett (2010) found that uncertainty in the sequence of returns can have a greater impact on retirement outcomes than the total rate of portfolio growth over retirement. Retiring into an unexpected bear market can be more dangerous than experiencing the same poor returns closer to the end of one’s lifetime, since stable withdrawals will leave fewer assets behind to benefit from a longer future of growth. In a decumulation context, it is therefore vital not to assess the performance of a portfolio solely by the rate of return over a time horizon without regard for consumption over that same horizon (Bernhardt and Donnelly 2018).

Furthermore, Reichenstein and Dorsett (1995) discuss the phenomenon of ‘time diversification’ where portfolios become less volatile in value over longer time horizons. As such, Frank et al. (2022) find shorter periods of decumulation to be more sensitive to adverse sequences of market returns since there exists less time for the market to recover, presenting an even greater danger to older retirees who plan over shorter time horizons.

2.2.2 Inflation risk

We attribute inflation risk to the randomness in the purchasing power of each dollar of the retiree’s savings over time. This uncertainty arises largely from randomness in the price inflation of the retiree’s everyday basket of goods and services as reflected by price level \(\Pi (t)\). The potential for variability in \(\Pi (t)\) may create further uncertainty around the amount of investment today required to fund a given future cash flow. Moreover, the relationship between portfolio returns and inflation has tended to vary uncertainly over time, depending on factors such as the function of monetary policy in the economy (Zhang 2021).

Inflation risk is exacerbated in the decumulation phase, with little ability to hedge the impact of high inflation through rising wages (Fullmer 2008). This exposure extends over many decades, especially eroding the purchasing power of those individuals invested in less risky assets (Khemka et al. 2023) with little potential to receive high long-term rates of portfolio return. Though inflation-indexed bonds present themselves as an attractive hedge, the market for them is relatively illiquid in practice (Finlay and Wende 2018) and the investor will be forced to accept lower yields in order to transfer the risk. Though, we remark that the purchasing power required to sustain a given standard of living will gradually decline as the retiree ages and their everyday spending needs diminish (Hurd and Rohwedder 2008), reflecting a form of hedge against late-life inflation risk.

3 Optimisation framework

We construct a framework to find the decumulation strategy which best tailors the distribution of outcomes to the retiree’s differing risk appetites.

3.1 Aligning the retiree’s goals with a retirement plan

Although the overarching goal of retirement is late-life fulfillment, we will focus on the pursuit of a set of strictly financial goals set at retirement time \(t=0\) as below:

-

(i)

Have the ability to sustain a chosen standard of living (SOL) over time with flexibility to adjust spending as early liquidity needs are incurred over time;

-

(ii)

Have adequate savings upon death in line with some general bequest motive (if any).

Pfau (2015) calls on the value of actuarial science in modelling a consumption target in the style of a defined benefit pension. Yin (2023) similarly sets consumption to achieve a constant pre-retirement SOL in order to benchmark the adequacy of retirement savings. To evaluate decumulation strategies, we therefore define the following retirement plan:

-

1.

We initially fix the consumption target \(\left( c(t)\right) _{t\in {\mathcal {S}}}\) in real terms to best satisfy Goal (i) with the intention of changing this consumption target as early liquidity needs are incurred over time;

-

2.

The cost of funding \(\left( c(t)\right) _{t\in {\mathcal {S}}}\) is planned to deliver a bequest in line with Goal (ii), provided the initial consumption target can be maintained until death.

In pursuit of the retirement plan, the retiree will face the investment risk of having to reduce their bequest upon realisation of poor investment returns. They also face the liquidity risk of having to reduce their bequest due to unfavourable death time \(T_x\); or having to bring forward their intended bequest upon realisation of event \(T_x^{\text {ELN}} < T_x\). Indeed, Lockwood (2018) describes how intended bequests can function as an incidental form of self-insurance against large costs associated with LTC needs, which we generalise to allow for all early liquidity needs. We will observe these risks emerge in Sect. 3.2.2.

At time \(T_x^*\), consumption target \(\left( c(t)\right) _{t\in {\mathcal {S}}}\) is considered to become no longer viable as circumstances significantly change. The retiree withdraws remaining funds for immediate bequest where \(T_x^* = T_x\); or the retiree has the option to recast their retirement plan upon \(T_x^* = T_x^{\textrm{ELN}}\).

3.2 Distribution of outcomes under decumulation strategies

We define a decumulation strategy as any mechanism through which the retiree can convert their wealth into the retirement plan in Sect. 3.1. We introduce the residual liquidity function  to track the retiree’s outcome by time T against the retirement plan. We define

to track the retiree’s outcome by time T against the retirement plan. We define  as some measure of wealth available to the retiree at time T, reflecting the retiree’s remaining budget for future consumption, early liquidity needs and bequest. This budget will be random due to the risks in Sect. 2, giving rise to a distribution of possible outcomes. Where \(T = T_x^{\text {ELN}}\), we may interpret

as some measure of wealth available to the retiree at time T, reflecting the retiree’s remaining budget for future consumption, early liquidity needs and bequest. This budget will be random due to the risks in Sect. 2, giving rise to a distribution of possible outcomes. Where \(T = T_x^{\text {ELN}}\), we may interpret  as the budget for the frail phase that remains after expenditure over the active phase, allowing the retiree to recast their retirement plan and decumulation strategy as their needs change.

as the budget for the frail phase that remains after expenditure over the active phase, allowing the retiree to recast their retirement plan and decumulation strategy as their needs change.

Milevsky and Robinson (2005) apply a stochastic present value (SPV) approach in their analytical approach in deriving a sustainable consumption rate \(c(t)\equiv c\), with Mindlin (2009) arguing that the SPV is a valuable tool for comprehensive actuarial risk management of funding commitments. We evaluate  by the SPV of \(W_T\) as a proportion of \(W_0\) in order to represent the portion of each dollar invested upon retirement which remains liquid at time T. We use \(W_{T}\) and \(W_T^*\) to denote the retiree’s nominal and real wealth, respectively, and give two equivalent expressions for

by the SPV of \(W_T\) as a proportion of \(W_0\) in order to represent the portion of each dollar invested upon retirement which remains liquid at time T. We use \(W_{T}\) and \(W_T^*\) to denote the retiree’s nominal and real wealth, respectively, and give two equivalent expressions for  :

:

In the following subsections, we find an expression for  under a pure drawdown strategy; and use this expression to shed light on the decumulation risks associated with this strategy.

under a pure drawdown strategy; and use this expression to shed light on the decumulation risks associated with this strategy.

3.2.1 Distribution of outcomes under a pure drawdown strategy

We first consider the standard strategy of pure drawdown from investment account \(A({\textbf{u}})\) for comparison against alternative strategies. Assuming no inflows from family, social security or corporate pensions, a pure drawdown strategy will decompose each retirement dollar as follows:

While (3.2) is stated in proportions of \(W_0\), we can informally interpret (3.2) as describing the decumulation of \(\$1\) over [0, T] to fund consumption target \((c(t))_{t\in {\mathcal {S}}}\), with  remaining at time T. The integral in (3.2) can be retrieved from Milevsky (1997) in the special case of a ‘stochastic perpetuity’ as \(T\rightarrow \infty \) under assumptions of constant nominal consumption \(c(t) = c\) and stochastic Wiener returns.

remaining at time T. The integral in (3.2) can be retrieved from Milevsky (1997) in the special case of a ‘stochastic perpetuity’ as \(T\rightarrow \infty \) under assumptions of constant nominal consumption \(c(t) = c\) and stochastic Wiener returns.

3.2.2 Understanding emergence of risk under pure drawdown

We now seek to understand the risks which shape the distribution of outcomes. To do so, we may compare the observed outcome  by time T with the planned bequest

by time T with the planned bequest  . The planned bequest will be expected upon retirement, conditional on consumption target \((c(t))_{t\in {\mathcal {S}}}\) being maintained until death.

. The planned bequest will be expected upon retirement, conditional on consumption target \((c(t))_{t\in {\mathcal {S}}}\) being maintained until death.

Since the integrand of  is non-negative and measurable, we can apply Tonelli’s Theorem to interchange the order of integration when considering planned bequest

is non-negative and measurable, we can apply Tonelli’s Theorem to interchange the order of integration when considering planned bequest  , giving deterministic integrand \(z(t) = c(t)\mathbb {E}[I(t; {\textbf{u}})\mathbb {1}_{\{T_x > t\}}]\). The retiree therefore plans their initial wealth (or $1) to be decumulated over \({\mathcal {S}}\) with \({\bar{T}} = \sup {\mathcal {S}}\) as follows:

, giving deterministic integrand \(z(t) = c(t)\mathbb {E}[I(t; {\textbf{u}})\mathbb {1}_{\{T_x > t\}}]\). The retiree therefore plans their initial wealth (or $1) to be decumulated over \({\mathcal {S}}\) with \({\bar{T}} = \sup {\mathcal {S}}\) as follows:

For T and \((I(t;{\textbf{u}}))_{t\in {\mathcal {S}}}\) independent, we rewrite (3.2) as follows:

where

We observe in (3.5) that function \(K(t; {\textbf{u}})\) measures the random variation in the retiree’s experience from the retirement plan over each interval [0, t]. By setting \(T = T_x^*\), we recognise these deviations as arising from the ensemble of risks outlined in Chapter 2. When \(I(t;{\textbf{u}})\) is generally high or T is large in (3.5), then the integral of (3.4) will end up occupying a greater share of the retiree’s initial wealth (or $1) than otherwise. That is, pure drawdown can be vulnerable to investment risk and late death risk. Conversely, the integral will shrink when T is small, as reflective of flexible access to funds in event of liquidity need.

3.2.3 Combining drawdown with alternative strategies

We now consider combining drawdown with some general alternative strategy. In Sect. 4, we will consider pooling policies (e.g. annuities) as a mechanism to mitigate the risks associated with pure drawdown.

In discussion of annuities, Yaari (1965) introduces the notion of a ‘flow of earnings’ into the retiree’s budget constraint. To reinforce that these ‘earnings’ stem from employment over the accumulation phase prior to time \(t = 0\), we instead define a random payment stream \((d(t))_{t\in {\mathcal {S}}}\) for which the retiree pays premium \(\$ P_{\theta }\). We consider each payment d(t) to flow from alternative account \(A({\tilde{\textbf{u}}})\) with trading strategy \({\tilde{\textbf{u}}}\) into the retiree’s investment account \(A({\textbf{u}})\) for the purpose of drawdown. For consistency with c(t), we state each payment d(t) and premium \(P_{\theta }\) at time 0 in real terms as proportions of \(W_0\). Given the retiree now has \(\$(1 - P_{\theta })\) to decumulate over [0, T], (3.2) generalises as follows to give an expression for the overall decumulation strategy:

As per (3.6), we can consider a retiree’s overall decumulation strategy to be composed of the investment account \(A({\textbf{u}})\) and payment stream \((d(t))_{t\in {\mathcal {S}}}\). Following the suggestions of Bernhardt and Donnelly (2018) and Hawley and Er (2022), this construction also gives the retiree the autonomy to convert payment d(t) into consumption or bequest at some future time \(s\ge t\) based on their needs.

3.3 Decomposing the distribution of outcomes by decumulation risk

We seek to decompose the distribution of outcomes in order to apply the retiree’s differing risk appetites for liquidity risk and investment risk. For motivation, we look to Olivieri (2001) who separates longevity risk from the total cost function \(C_x^{(n)}\) associated with a provider’s annuity portfolio of n lifetimes \(\{T_{x;i}\}\). They decompose the variance of \(C_x^{(n)}\) conditional on observed population survival \({\mathcal {P}} = (\,\!_tp_x^{\textrm{ref}})_{t\in {\mathcal {S}}}\) as follows:

As described by De Waegenaere et al. (2010), the first term in (3.7) reflects the risk to the annuity portfolio if there was no longevity risk, with the second term reflecting the effect due to longevity risk. We apply a similar risk decomposition to  in order to adopt the perspective of the retiree, but without necessarily assuming that variance is the best measure of each risk. We consider the impact of each decumulation risk through constructing the following two information sets:

in order to adopt the perspective of the retiree, but without necessarily assuming that variance is the best measure of each risk. We consider the impact of each decumulation risk through constructing the following two information sets:

-

1.

\({\mathcal {L}}\): information set where transition times are random, with all else occurring as planned. We define

for \(T = T_x^*\) in order to consider the impact of uncertainty in the first transition time on the liquidity available at that time. Taking conditional expectations of (3.4), we find $$\begin{aligned} 1 = X_x^{{\mathcal {L}}}+ {\int }_{\!\!\!\!0}^{{\bar{T}}} z(t)\cdot \dfrac{\mathbb {1}_{\{T_x^* > t \}}}{_tp_x}\textrm{d}{t}. \end{aligned}$$(3.8)

for \(T = T_x^*\) in order to consider the impact of uncertainty in the first transition time on the liquidity available at that time. Taking conditional expectations of (3.4), we find $$\begin{aligned} 1 = X_x^{{\mathcal {L}}}+ {\int }_{\!\!\!\!0}^{{\bar{T}}} z(t)\cdot \dfrac{\mathbb {1}_{\{T_x^* > t \}}}{_tp_x}\textrm{d}{t}. \end{aligned}$$(3.8)When \(T_x^*\) takes larger values, we observe in (3.8) that the liquidity \(X_x^{{\mathcal {L}}}\) available to the retiree at \(T_x^*\) will fall as a share of their initial wealth (or $1). We have removed the investment risk from function \(K(t;{\textbf{u}})\) in (3.5), allowing us to analyse liquidity risk independently of investment risk.

-

2.

\({\mathcal {I}}\) : information set where investment returns are random, with all else occuring as planned. We define

for \(T = T_x\) in order to consider the impact of uncertainty in investment returns on bequest, provided there are no early liquidity events. Taking conditional expectations of (3.4), we find $$\begin{aligned} 1 = X_x^{{\mathcal {I}}}+ {\int }_{\!\!\!\!0}^{{\bar{T}}} z(t)\cdot \dfrac{I(t;{\textbf{u}})}{\mathbb {E}[I(t;{\textbf{u}})]}\textrm{d}{t}. \end{aligned}$$(3.9)

for \(T = T_x\) in order to consider the impact of uncertainty in investment returns on bequest, provided there are no early liquidity events. Taking conditional expectations of (3.4), we find $$\begin{aligned} 1 = X_x^{{\mathcal {I}}}+ {\int }_{\!\!\!\!0}^{{\bar{T}}} z(t)\cdot \dfrac{I(t;{\textbf{u}})}{\mathbb {E}[I(t;{\textbf{u}})]}\textrm{d}{t}. \end{aligned}$$(3.9)When \(I(t;{\textbf{u}})\) is generally higher than \(\mathbb {E}[I(t;{\textbf{u}})]\), we observe in (3.9) that the bequest available to a retiree at \(T_x\) will fall as a share of their initial wealth (or \(\$1\)). We have removed the liquidity risk from function \(K(t;{\textbf{u}})\) in (3.5), allowing us to analyse investment risk independently of liquidity risk.

for

for  for

for From (3.8) and (3.9), it follows that information sets \({\mathcal {L}}\) and \({\mathcal {I}}\) will generate two independent distributions of outcomes. In Sect. 3.4, we will seek out the optimal decumulation strategy according to the retiree’s appetites for variability across each of these two distributions, thereby optimising the overall distribution of outcomes.

3.4 Optimising the distribution of outcomes for varying risk appetites

With reference to the traditional lifetime utility approach, we will now develop risk measures which capture the unique dangers of each independent distribution, and combine them into an optimisation problem to be solved.

3.4.1 Brief review of lifetime utility optimisation

The problem of finding the optimal decumulation strategy which best satisfies Goal (i) and Goal (ii) is traditionally solved over planning horizon \({\mathcal {S}} = [0, {\bar{T}}]\) through maximising expected utility of lifetime consumption \((c(t))_{t\in {\mathcal {S}}}\) and bequest \(W_T\) at terminal time \(T\le {\bar{T}}\). Yaari (1965) pioneered the problem of best decumulating retirement savings in a setting where \(T \equiv T_x\), and the retiree faces only death risk. Merton (1969) introduces investment risk into the problem for fixed death time \(T_x\equiv t^*\), putting forward the Classical Portfolio Problem of jointly finding trading strategy \({\textbf{u}}\) and \((c(t))_{t\in {\mathcal {S}}}\) to maximise expected lifetime utility. Given time-preference parameter \(\rho \) and general bequest utility function \(u_B(\cdot )\), the objective function can be expressed as follows:

We leverage the traditional approach of maximising lifetime utility to optimise the distribution of outcomes over the \({\mathcal {I}}\) information set. We also discuss the shortfalls of using this traditional approach to reflect optimality over the \({\mathcal {L}}\) information set.

3.4.2 Constructing the investment objective function

Where consumption target \((c(t))_{t\in {\mathcal {S}}}\) is predetermined according to some chosen standard of living, the problem of maximising (3.10) reduces into the problem of maximising \(u_B(W_T, T)\). Lockwood (2012) elects to maximise the utility of the present value of bequest, remarking that the longer one lives, the ‘cheaper’ it is to leave a bequest of given present value. We therefore consider the retiree to maximise their expected utility of bequest \(Q_x^{{\mathcal {I}}} = \mathbb {E}[u(X^{{\mathcal {I}}}_x)]\) in the \({\mathcal {I}}\) information set.

In our choice of objective function, we take motivation from Landriault et al. (2018) who find a dynamic trading strategy \({\textbf{u}}\) through mean-variance optimisation of bequest given a level of risk aversion that depends on the state of the investment. In the spirit of MPT, we can consider the retiree to be a mean-variance investor with respect to \(X^{{\mathcal {I}}}_x\) to give the investment objective function:

where we define \(b \ge 0\) as the parameter of investment risk aversion (IRA). For values of \(X_x^{{\mathcal {I}}}\) where \(u(X_x^{{\mathcal {I}}})\) is concave, we assume the retiree derives higher utility from a lower funding cost of consumption; and being able to reserve a greater proportion of their initial wealth for bequest. However, Bernhardt and Donnelly (2018) deem it ‘wasteful’ to pay for surpluses of assets in excess of a target. In our setting, the bliss point \(X_x^{{\mathcal {I}}} = 1/2b\) may therefore be interpreted as the maximum share of initial wealth that the retiree may wish to bequeath.

3.4.3 Constructing the liquidity risk constraint

While the traditional approach can yield tractable solutions, it can be limited in its ability to convey the retiree’s appetite for the liquidity risk associated with random time \(T_x^*\).

In particular, Bommier and Villeneuve (2012) argue that the traditional approach is constrained by an assumed form of risk neutrality in  with respect to random death time \(T = T_x\). This risk neutrality is said to arise from the central assumption of (3.10) that consumption utility is additively separable, that is integrable over time, originally dubbed an ‘unhappy’ assumption by Yaari (1965).

with respect to random death time \(T = T_x\). This risk neutrality is said to arise from the central assumption of (3.10) that consumption utility is additively separable, that is integrable over time, originally dubbed an ‘unhappy’ assumption by Yaari (1965).

Consequentially, Davidoff et al. (2005) maximise lifetime utility to deduce that retirees derive higher utility from laying aside a fixed sum at a fixed time for bequest before annuitising their remaining wealth. This is because bequest \(W_{T_x}\) will be random in size and timing where \(T_x\) is uncertain, illustrating the failure of the traditional approach to capture a retiree’s lower tolerance to leaving a smaller bequest in the event of very early death.

Given these limitations, we take an alternative approach to incorporating liquidity risk appetite. Boido and Fasano (2023) propose a penalised utility function in the context of portfolio theory, tilting the optimal portfolio based on the manager’s desires for exposure to different risk factors. Bayraktar and Young (2008) propose a similar penalty in the context of the traditional approach, maximising the lifetime utility of consumption subject to a binding constraint on the probability of ruin.

We similarly maximise \(Q_x^{{\mathcal {I}}}\) in (3.11), subject to a maximum constraint on the probability of shortfall in the \({\mathcal {L}}\) information set. We allow the retiree to select the degree of certainty with which they want to have a given amount of liquidity in time of need, assuming investments perform as planned. We define \(\tau _{\nu }\) as the time of shortfall in \(X_x^{{\mathcal {L}}}\) relative to shortfall threshold \(\nu \). We impose a liquidity risk constraint upon the liquidity shortfall probability \(\mathbb {P}_{{\mathcal {L}}}(T_x^* \ge \tau _\nu )\) associated with falling below \(\nu \) by time \(T_x^*\):

where we define \(\psi _{\nu }\) as the parameter of liquidity risk tolerance (LRT) associated with shortfall threshold \(\nu \). Though we will assume a single value of \(\nu \) for each retiree, their liquidity risk appetite might be better parameterised by some set of tolerances \(\{\psi _{\nu }: \nu \in {\mathcal {A}}\}\) associated with threshold set \({\mathcal {A}}\), or even allowing these tolerance(s) to vary across different sources of liquidity risk. Moreover, Powers (1995) takes the Laplace Transform of the (random) ruin time as a way of conveying the higher cost of relatively early insolvency to an insurer. Since \(T_x^* \le T_{x}\), we are similarly assigning a higher penalty to the more costly possibility of early shortfall.

3.4.4 Summary of optimisation problem

In summary, we seek the optimal admissible strategy which achieves the following maximisation:

Overall, we parameterise the retiree’s risk appetites by \((b, \psi _{\nu })\) for some single choice of \(\nu \). In Sect. 4, we will construct a family of admissible strategies over which to perform this optimisation.

4 Finding a set of admissible strategies

In Sect. 3, we developed a framework to find the optimal strategy from a general set of L alternative strategies \(\{d_i(t): i = 1,\dotsc , L \}\) which may be chosen at retirement in combination with a baseline strategy of drawdown from investment account \(A({\textbf{u}})\). We discuss pooling mechanisms in Sect. 4.1, allowing us to define a family of alternative strategies in Sect. 4.2. In Sect. 4.3, we admit this family as the admissible solution set to our optimisation problem under some restrictions.

4.1 Dynamics of risk transfer via pooling

We consider pooling policies to comprise a stream of payments \((d(t))_{t\in {\mathcal {S}}}\) receivable until death time \(T_x\). The retiree can purchase a mortality credit guarantee (e.g. life annuity) from a pooling provider, or participate directly in the experience of the pool through the mutuality mechanism. The amounts released by the deceased are shared as mortality credits amongst the survivors in the participating case (Pitacco 2016), and are otherwise credited to the pooling provider.

In either case, the actuarially fair price of the pooling policy to the retiree is  , where we refer to

, where we refer to  as the individual cost function associated with funding \((d(t))_{t\in {\mathcal {S}}}\). Further,

as the individual cost function associated with funding \((d(t))_{t\in {\mathcal {S}}}\). Further,  will contain the variability transferred to the pool and can be written:

will contain the variability transferred to the pool and can be written:

The variability of  is passed through the pooling mechanism to diversify away idiosyncratic variability associated with portfolio returns and individual lifetime \(T_x\). The pooling provider is left with a portfolio associated with total cost function \(C_x^{(n)}\), as introduced in Sect. 3.3. We write

is passed through the pooling mechanism to diversify away idiosyncratic variability associated with portfolio returns and individual lifetime \(T_x\). The pooling provider is left with a portfolio associated with total cost function \(C_x^{(n)}\), as introduced in Sect. 3.3. We write

We rewrite this exposure in terms of the average cost function \({\bar{C}}_x^{(n)}\):

By taking the arithmetic average of individual cost functions  , we assume without loss of generality that all members make the same initial investment to the pool. Otherwise, we could redefine \(_tP_x^{(n)}\) by some weighted average that accounts for differences in initial investment amount across pooled lives. By definition of d(t), it follows that \({\bar{C}}_x^{(n)}\) will be stated as a proportion of the retiree’s own initial wealth \(W_0\).

, we assume without loss of generality that all members make the same initial investment to the pool. Otherwise, we could redefine \(_tP_x^{(n)}\) by some weighted average that accounts for differences in initial investment amount across pooled lives. By definition of d(t), it follows that \({\bar{C}}_x^{(n)}\) will be stated as a proportion of the retiree’s own initial wealth \(W_0\).

A pooling provider will bear the variability of \({\bar{C}}_x^{(n)}\) in return for a higher price \(P_{\theta } = (1 + \theta )P_0\), marked up in comparison to the actuarially fair price \(P_0\). A loading factor \(\theta \) will arise from the purchase of a mortality credit guarantee, reflecting the cost of transferring risk (Pitacco 2016). Indeed, \({\bar{C}}_x^{(n)}\) reflects the provider’s exposure to asset-liability mismatch risk which we define as the risk that the value of liabilities moves differently to the value of assets held to back them. In our setting, assets are subject to investment risk due to \(I(t; {\tilde{\textbf{u}}})\); and liabilities are subject to aggregate death risk due to \(_tP_x^{(n)}\).

4.2 Annuity Family

In the following subsections, we develop a family of annuity-like products which are to be admissible in our optimisation framework. We showcase the decumulation risks associated with these products, as well as their risk mitigation capabilities.

4.2.1 Constructing the Annuity Family

We develop a family of pooling policies based on the original group self-annutisation (GSA) formulation due to Piggott et al. (2005) and discussed at depth by Zhou (2020) and Bär and Gatzert (2022). We denote \(d(t) = \phi g(t)\) where \(\phi \) is the payment rate and g(t) is the payment vehicle. We write

For illustration, we can rewrite (3.6) under (4.4) as follows:

Piggott et al. (2005) denote the factors of g(t) by the interest rate adjustment \(\textrm{IRA}_t = \mathbb {E}[I(t; {\tilde{\textbf{u}}})] / I(t; {\tilde{\textbf{u}}})\) and mortality experience adjustment \(\textrm{MEA}_t = \,_tp_x/\!\,_tP_x^{(n)}\), respectively. In our inflationary setting, we implicitly incorporate an inflationary adjustment into the \(\textrm{IRA}_t\) factor based on price level \(\Pi (t)\). We generate the Annuity Family by varying the guarantee factor \(\xi (t)\) in (4.4) to undo these adjustments and transfer the risk to a provider.

Given mortality credit guarantee where \(\xi (t)\cdot \textrm{MEA}_t \equiv 1\), we get a unit-linked annuity (ULA). Given portfolio return guarantee where \(\xi (t)\cdot \textrm{IRA}_t \equiv 1\), we retrieve the longevity-indexed annuity (LIA) due to Denuit et al. (2011). Where \(\xi (t)\cdot \textrm{MEA}_t\cdot \textrm{IRA}_t \equiv 1\), we recover an inflation-indexed annuity (IIA) with \(d(t) = \phi \). We summarise the Annuity Family in Table 1.

4.2.2 Mitigation and emergence of risks under the Annuity Family

We seek to incorporate payment streams \((d(t))_{t\in {\mathcal {S}}}\) from the Annuity Family into the retiree’s overall decumulation strategy to mitigate against the risks of (3.5) associated with pure drawdown. We denote \(z_0(t) =\phi \mathbb {E}[ I(t; {\tilde{\textbf{u}}})]\!\,_tp_x\) and find the average cost function (4.3) under (4.4) as follows:

As anticipated, we observe in (4.6) that the provider will bear the risk arising from guarantee factor \(\xi (t)\). Taking the perspective of the retiree, we denote \(z_{\theta }(t) = (1+\theta )z_0(t)\) and discover in (4.7) a trade-off between the benefits of risk mitigation and the emergence of additional decumulation risks. We have

Risk mitigation. In (4.7), we observe a form of longevity protection to the retiree in the form of a stable payment stream at older ages, with the second integral occupying a smaller share of the retiree’s initial wealth (or $1) when T is large. Indeed, Pitacco (2016) argues that the most important feature of life annuities to the retiree is protection against the risk of outliving their initial wealth \(W_0\), reflecting a form of insurance against outliving expectations. The survival probability \(\,_tP_x^{(n)}\) will fall over time as the membership ages, providing a rising stream of mortality credits to surviving participants in the pool (Thorburn 2018).

We observe the potential for portfolio variability reduction through diversification across \({\textbf{u}}\) and \({\tilde{\textbf{u}}}\); and by recognising that mortality credits and market returns are effectively uncorrelated (Blake 2018), offering diversification benefits which cannot be replicated by traditional asset classes alone (Albrecht and Maurer 2002). While longevity protection will help satisfy a given liquidity risk tolerance \(\psi _{\nu }\), this reduction in portfolio variability will be attractive to a retiree with high investment risk aversion b.

Risk emergence. In (4.7), we can set \(T = T_x^*\) to observe the impact of liquidity risk in scenarios where \(T_x^*\) takes a low value. The retiree will have effectively purchased a stream of future payments \(\{d(t):t\in [0, {\bar{T}}]\}\) at prices \(\{z_{\theta }(t): t\in [0, {\bar{T}}]\}\). However, there is a subset of payments \(\{d(t): t\in (T_x^*,{\bar{T}}]\}\) that may neither be brought forward in event of early liquidity need nor bequeathed in event of death. Where \(T_x^*\) is small, the retiree therefore pays for a larger subset of payments \(\{d(t): t\in (T_x^*,{\bar{T}}]\}\) that will never be received before first transition, that is the phase where survival status \(\mathbb {1}_{\{T_x^* > t \}}\) is non-zero.

Whether \(T_x^*\) is considered late or early may be benchmarked against the inflated survival probability \((1 + \theta )\!\,_tP_x^{(n)}\) or \(\left( 1 + \theta \right) \!\,_tp_x\), depending on the form of guarantee factor \(\xi (t)\). For instance, if the sequence of survival probabilities \(\,(_tP_x^{(n)})_{t\in {\mathcal {S}}}\) decays faster over time than expected, then the retiree must not live as long to receive their money’s worth from a GSA. That is, the second integral in (4.7) will end up occupying a comparatively smaller share of the retiree’s initial wealth \(W_0\) (or $1) if \(\,(_tP_x^{(n)})_{t\in {\mathcal {S}}}\) decays faster for fixed \(T_x^*\); or equivalently, \(T_x^*\) is large for fixed \(\,(_tP_x^{(n)})_{t\in {\mathcal {S}}}\). However, we see that the retiree effectively incurs a ‘longevity risk premium’ (Blake 2018), with a higher loading factor \(\theta \) increasing the amount of decay in \(_tP_x^{(n)}\) that is required to achieve an effect of similar order.

4.2.3 Possible extensions to the Annuity Family

We will now consider some possible extensions to the Annuity Family which might allow even finer tuning of the retiree’s distribution of outcomes in line with their differing risk appetites. Though we do not implement these extensions in full, we seek to lay the groundwork for future work.

Natural hedging. Ramsay and Oguledo (2018) argue that an attractive annuity product must satisfy the risk appetite of the retiree whilst also promoting insurer sustainability. Yaari (1965) recognises that buying a life annuity is broadly similar in concept to selling life insurance on your own lifetime \(T_x\). Thus, the retiree may like to buy a death benefit associated with their pooling policy in order to buy a natural hedge against the early death risk associated with this pooling policy. Zhou et al. (2022) find that the addition of a death benefit to an annuity to form a ‘bequest-enhanced annuity’ should theoretially lower \(\theta \) under Solvency II requirements.

We can consider the purchase of a death benefit as a natural hedge in some death benefit ratio \(\beta \) with payment rate \(\phi \), achieving some lower loading \(\theta _{\beta } \in [0, \theta ]\). In De Felice (2023), natural hedging is implemented through integration of death benefit ratio \(\beta \) into the payment vehicle, giving the bequest-enhanced (BE) payment vehicle \(g_{\beta }(t)\) as a function of \(g(t) \equiv g_0(t)\). We have then

While we do not implement natural hedging in this paper, the approach followed by De Felice (2023) is provided in Appendix A.

Deferred annuity. Horneff et al. (2008) propose the idea that the retiree may be able to benefit from the equity premium at younger ages and from exploiting higher mortality credits later in life. As such, Milevsky and Young (2007) derive the optimal age \(x+t^*\) to which a retiree at time 0 should defer the annuitisation of their wealth. To perform this optimisation, we could write (3.6) as below:

Combinations. In practice, one can also mix payment streams to combine the risk mitigation benefits of some strategies with the flexibility of others (Thorburn 2018). A sophisticated investor may want to optimise for some combination of L payment streams \(\{d_i(t):i=1,\dotsc ,L\}\) with respective prices \(\left\{ P_i(t; \theta _i):i=1,\dotsc , L \right\} \) by writing (3.6) as (4.10):

where

Age pension. The age pension may also be included in (4.10) as the \(j^{\text {th}}\) payment stream by \(d_j(t) = m(t)\) with no premium upon retirement, that is \(P_j(t; \theta _j) = 0\). For illustration, we consider the combination of the age pension and drawdown as a type of overall decumulation strategy in (4.12):

We can observe the similarity between (4.12) and the form of  in (4.5) across the Annuity Family. For instance, an age pension that is fixed in real terms, so that \(m(t)\equiv {\bar{m}}\), will function much like a zero-premium IIA. This kind of similarity may lead to the crowding out of private annuity markets, inhibiting their successful development (Mitchell and McCarthy 2002). That is, large government social security systems provide a supply of annuities that satisfies a large portion of demand, preventing pooling providers from attaining the economies of scale which make the pooling mechanism so effective.

in (4.5) across the Annuity Family. For instance, an age pension that is fixed in real terms, so that \(m(t)\equiv {\bar{m}}\), will function much like a zero-premium IIA. This kind of similarity may lead to the crowding out of private annuity markets, inhibiting their successful development (Mitchell and McCarthy 2002). That is, large government social security systems provide a supply of annuities that satisfies a large portion of demand, preventing pooling providers from attaining the economies of scale which make the pooling mechanism so effective.

4.3 Set of admissible strategies

We find the overall decumulation strategy which maximises investment objective function in (3.11) subject to liquidity risk constraint (3.12) from a set of admissible strategies. These strategies are to comprise some choice of investment account \(A({\textbf{u}})\) and single payment stream \((d(t))_{t\in {\mathcal {S}}}\). We impose restrictions:

-

1.

We permit the retiree to choose the trading strategy \({\textbf{u}}\) of their investment account \(A({\textbf{u}})\) under the restriction that \({\textbf{u}}\) corresponds to holding some combination of the risk-free asset and the market portfolio. In particular, we define the market weight \(w \ge 0\) as the proportion of wealth remaining in investment account \(A({\textbf{u}})\) which is allocated to the market portfolio.

-

2.

We permit the retiree to choose a single payment stream \(d(t) = \phi g(t)\) from the Annuity Family under the restriction that \(\mathbb {E}[d(t)] \in [0, c(t)]\) for all \(t < T_x\). Further, we restrict our focus to \(c(t)\equiv c\) where c is given in real terms, which is consistent with the benchmarking approaches in Sect. 3.1. The drawdown strategy thus reduces into the (real) self-annuitisation case and we have the following equivalence across the Annuity Family:

$$\begin{aligned} \mathbb {E}[d(t)] \le c(t) \quad \iff \quad \phi \le c.\end{aligned}$$(4.13) -

3.

We permit the retiree to choose \((g(t))_{t\in {\mathcal {S}}}\) from Table 1. For dimensionality reduction, we assume that trading strategy \({\tilde{\textbf{u}}}\) is fully determined by the retiree’s choice of \((g(t))_{t\in {\mathcal {S}}}\). We permit a portfolio return guarantee if and only if \({\tilde{\textbf{u}}}\) is invested in the risk-free asset so that \(\mathbb {E}[I(t; {\tilde{\textbf{u}}})] \equiv I(t; {\tilde{\textbf{u}}})\). Otherwise, we set \({\tilde{\textbf{u}}} = {\textbf{u}}\) even though pooling providers are likely to hold a more efficient portfolio than any individual investor.

We thus implement the optimisation in Sect. 3.4.4 over the admissible strategies summarised in Table 2.

5 Implementing the optimisation framework

We seek to implement the optimisation framework of Sect. 3 over the admissible strategies found in Sect. 4. Our approach balances the trade-off between numerical precision of the optimum and computational speed through the following implementation approach:

-

1.

In Sect. 5.1, we prioritise numerical accuracy in the algorithm used to find the optimum;

-

2.

Across Sect. 5.2 and Sect. 5.3, we prioritise tractable assumptions to allow us to reduce run times.

5.1 Optimisation algorithm

We propose an exhaustive search algorithm which is capable of producing high precision of results at the expense of longer run times. Numerical precision is important given the high dimensionality of our decision space in Sect. 4.3. First, we consider a retiree with consumption target \((c(t))_{t\in {\mathcal {S}}}\) and risk appetites that are parameterised by b and \(\psi _{\nu }\) for some choice(s) of \(\nu \). We then analyse the sensitivity of the optimal strategy to the retiree’s risk appetite and target SOL in order to determine the effect on decision-making and validate our framework.

-

(1)

Evaluating the components of the optimisation problem. For each payment vehicle \((g(t))_{t\in {\mathcal {S}}}\) in Table 1, we compute three grids of outputs \(\mathbb {E}[X_x^{{\mathcal {I}}}]\), \(\textrm{Var}(X_x^{{\mathcal {I}}})\), \(\mathbb {P}_{{\mathcal {L}}}(T_x^* \ge \tau _{\nu })\) from a single grid of inputs \((w, \phi )\in S\).

-

(2)

Finding the optimal strategy. For each payment vehicle \((g(t))_{t\in {\mathcal {S}}}\) in Table 1, we grid search to find the admissible combination \((w, \phi )\in S\) which achieves the maximum \(Q_g^* = \max Q_x^{{\mathcal {I}}}\) subject to \(\mathbb {P}_{{\mathcal {L}}}(T_x^* \ge \tau _{\nu }) \le \psi _{\nu }\). We then determine the optimal overall strategy which achieves the global maximum \(Q^* = \max Q_g^*\) across all payment vehicles \({(g(t))_{t\in {\mathcal {S}}}}\).

-

(3)

Analysing sensitivities. We find the optimal strategy across differing risk appetites \((b, \psi _{\nu })\) and consumption targets \((c(t) )_{t\in {\mathcal {S}}}\) in order to determine how the optimal strategy may vary from retiree to retiree. By analysing these sensitivities, we can also validate the robustness of our framework.

In Algorithm 1, we execute Step (2) by searching for the optimal strategy through the grids of outputs evaluated in Step (1). We can then apply Algorithm 1 for varying \((b, \psi _{\nu })\) and \((c(t))_{t\in {\mathcal {S}}}\) as per Step (3).

Finding the optimal strategy

5.2 Theoretical assumptions

In practice, the optimisation algorithm described in Sect. 5.1 can be computationally intensive. We therefore emphasise parsimony in our choice of theoretical assumptions in order to leverage powerful theoretical results in Sect. 5.3.

5.2.1 Investment assumption

Noting that the price level \(\Pi (t)\) will drift upwards over time with some drift inflation rate \(\pi \), we choose to project inflation dynamics using Standard Brownian Motion (SBM) \(B_t^{\pi }\) on the natural filtration \({\mathcal {F}}_t\) as per, for instance, Brennan and Xia (2002). We write

As suggested by Khemka et al. (2023), the inflation-indexed bond becomes the risk-free asset when a problem is expressed in real terms. Hence, \({\textbf{u}}\) places weight w on the market portfolio and weight \(1 - w\) on inflation-indexed bonds which are assumed to deliver a risk-free rate of return r in excess of inflation. We let \(B_t^{\mu }\) be the SBM on \({\mathcal {F}}_t\) which drives the market portfolio and is assumed to be uncorrelated with \(B_t^{\pi }\). Where \(F(t; {\textbf{u}}) = 1 / Y(t; {\textbf{u}})\) is the nominal value of \(\$1\) invested today at future time t, we have

where

5.2.2 Transition assumption

As in Sheshinski (2008), we model the projected death hazard rate over \({\mathcal {S}}\) as \(\lambda _{x+t} = \lambda \) where

We will let \({\bar{T}}\rightarrow \infty \) so that the distribution of \(T_x\) approaches the exponential distribution \(\textrm{Exp}(\lambda )\) with rate parameter \(\lambda \). We similarly assume \(T_x^{\textrm{ELN}} \overset{d}{=} \textrm{Exp}(\lambda ^{\text {ELN}})\), and make the simplifying assumption that \(T_x^{\textrm{ELN}}\) and \(T_x\) are independent.

Admittedly, the assumption of a constant force of mortality is a strong one, and it fails to account for the increasing convexity of survival probability \(_tp_x\) over time. Nonetheless, this assumption will allow us to find a closed-form distribution for \(X_x^{{\mathcal {I}}}\) in Sect. 5.3 which allows greater computational efficiency in implementing the algorithm. While it is possible to relax this assumption, we would need to approximate the moments of \(X_x^{{\mathcal {I}}}\) using Monte Carlo simulation.

5.2.3 Population assumption

We assume the population survival probability \(_tp_x^{\textrm{ref}}\) is differentiable with continuous hazard rate \(\Lambda _{x+t}\). By extrapolating past mortality trends, Lee and Carter (1992) project \(\Lambda _{x+t}\) as stochastic into the future, being lognormal at each future time t. Milevsky et al. (2005) assume a diffusion process with lower bound \({\underline{\lambda }}\) reflecting some minimum mortality rate due to the hazard of accidents even after biological causes of death are removed.

We define population survival function \(_tp_x^{\textrm{ref}} = \textrm{e}^{-\Lambda t}\) where \(\Lambda - {\underline{\lambda }}\) is lognormally distributed with mean \(\lambda - {\underline{\lambda }}\), and uncertainty parameter \({\hat{\sigma }}\). Though simplified, these dynamics showcase the ‘trend’-like nature of longevity risk discussed in Sect. 2.1. This is because the projected hazard rate \(\lambda \) either overstates or understates \(\Lambda \), with \(_tp_x^{\textrm{ref}}\) trending away from projected survival probability \(_tp_x = \textrm{e}^{-\lambda t}\) over time.

When considering the participating policies GSA and LIA, we also let \(_tP_{x}^{(n)} \rightarrow \, _tp_x^{\textrm{ref}}\) by allowing the pool to become infinitely large. As suggested by Börger et al. (2023), one could also model the mortality risk associated with finite pool size n by drawing realisations for survivors over time from a suitable binomial distribution. Assuming lifetimes \(\{T_x^{(i)}\}\) are independent, conditional on \(_tp_x^{\textrm{ref}}\), we can write \(n\,_tP_x^{(n)} \overset{d}{=}\ \textrm{Bi}(n,\, _tp_x^{\textrm{ref}})\). By focusing only on longevity risk here, we potentially understate the impact of aggregate death risk on the retiree’s decision-making, potentially making the GSA and LIA seem overly attractive.

5.2.4 Loading assumption

In a simple setting without regulatory requirements, the pooling provider might target a form of Sharpe ratio S. Milevsky et al. (2006) develop a stylised framework for the pricing of aggregate death risk, accounting for the portfolio of a pooling provider with zero expenses. In (5.6), we simplify their expression for S in terms of average cost function \({\bar{C}}_x^{(n)}\), and rearrange to find loading factor \(\theta \).

5.3 Theoretical results

Since our optimisation algorithm is computationally intensive, we seek to construct tractable equations and theoretical results which reduce the need for simulation.

5.3.1 Key equations

From (5.1) and (5.2), we first derive an expression for \(I(t; {\textbf{u}}) = Y(t; {\textbf{u}})\Pi (t)\). Given \(B_t\) is a SBM on the natural filtration \({\mathcal {F}}_t\) which depends on \(B_t^{\pi }\) and \(B_t^{\mu }\), we write

where

We will consider values of w such that the expected present value (EPV) of the lifetime annuity is well-defined under our model assumptions. That is, we require \(\sigma (w)^2 < \lambda + \mu (w)\) so that we can write

While (5.9) can be surprising, it can be verified against Milevsky and Robinson (2005). There exists market weight \(w_0\) such that \(a_x(w) \ge a_x(w_0)\) for all \(w_0\). That is, the variability in the annuity present value increases in w for \(w > w_0\) without any improvement to the mean. When finding an optimal strategy, we therefore need only consider \(w \le w_0\) to avoid either purchasing or self-funding an annuity of given expected present value and excess variance.

The loading factor \(\theta \) is determined from (5.6) based on \({\bar{C}}_x^{(n)}\). Given our population assumption, we can compute \(\textrm{Var}({\bar{C}}_x^{(n)})\) in (5.6) through decomposition of variance:

From (4.6), we have \(\textrm{Var}({\bar{C}}_x^{(n)}) = 0\) for a GSA and LIA since all risk is transferred to the retiree. We can therefore take \(\theta = 0\) in (5.6) for these payment streams.

5.3.2 Expected investment utility

We begin by applying information set \({\mathcal {I}}\) to (4.5). We have

In information set \({\mathcal {I}}\), we consider population rates \(_tp_x^{\textrm{ref}}\) to be deterministic with hazard rate \(\lambda \). Hence, we have \({\hat{g}}(t)= \mathbb {E}[I(t; {\tilde{\textbf{u}}})] / I(t; {\tilde{\textbf{u}}})\). Making use of the restrictions on \({\tilde{\textbf{u}}}\) imposed in Sect. 4.3 and \(c(t) \equiv c\), we consider two cases for (5.11) across the Annuity Family. We remark that it may also be tractable to consider consumption targets of the form \(c(t) = \textrm{e}^{\varrho t}\) for \(\varrho \in \mathbb {R}\).

Case 1 (IIA, LIA). We have \({\tilde{\textbf{u}}}\) comprising only the risk-free asset. Hence, \({\hat{g}}(t) = 1\) giving

Case 2 (ULA, GSA). We have \({\tilde{\textbf{u}}} \equiv {\textbf{u}}\). Hence, \(I(t;{\textbf{u}}){\hat{g}}(t) = \mathbb {E}[I(t;{\textbf{u}})]\) giving

Through substituting (5.13) into (5.11), we can observe that the expected investment utility of a GSA is equal to that of pure drawdown for all market weights w, independent of the payment rate \(\phi \). This is reasonable since both the GSA and pure drawdown are characterised by the same trading strategy \({\textbf{u}}\) and zero loadings. Now, to compute the moments of \(X_x^{{\mathcal {I}}}\), we utilise a result attributed to Dufresne (1990) and applied by Milevsky (1997) in a drawdown context. They derive:

In (5.14), \(\Gamma (\alpha ,\eta )\) is a Gamma distribution with shape parameter \(\alpha \), rate parameter \(\eta \) and density function f as per (5.15):

It follows that the reciprocal of the common integral across (5.12) and (5.13) will follow a Gamma distribution with \(v=\lambda +\mu (w)-\frac{1}{2}\sigma (w)^2\) and \(s = \sigma (w)\). For \(\alpha > N\), the \(N^{\textrm{th}}\) moment of the integral in (5.12) and (5.13) becomes \(\eta ^N \Gamma (\alpha - N) / \Gamma (\alpha )\), as applied by Milevsky and Posner (1998) in their technique to price Asian options. It can be readily verified that the mean \(\eta /(\alpha - 1)\) is precisely equal to annuity EPV \(a_x(w)\). To use (5.14) to calculate \(\mathbb {E}[(X_x^{{\mathcal {I}}})^2]\), we require \(\alpha > 2\). Since \(\alpha (w)\) is a decreasing function of w, we take the following upper bound:

When (5.16) holds, the cost of funding the annuity will be mean-variance efficient, and we can find closed-form expressions for the moments of \(X_x^{{\mathcal {I}}}\) across the Annuity Family.

5.3.3 Liquidity shortfall probability

We look to the literature to motivate a general expression for the liquidity shortfall probability \(\mathbb {P}_{\mathcal {L}}(T_x^*\ge \tau _{\nu })\). In the case of the pure drawdown strategy, Milevsky (1997) expressed nominal wealth \(W_T\) at fixed time \(T\equiv t^*\) as per (5.17), under the assumption of nominal consumption at rate c. He writes

Milevsky (1997) remarked from the monotonicity of the integral in (5.17) that the retiree will experience the event of ruin before time T if and only if the bracketed factor falls below zero. Under the \({\mathcal {L}}\) information set, it follows that:

We consider (5.17) in our setting where \(\phi \ge 0\) and c is defined in real terms. We rewrite (5.18) in terms of real wealth \(W_T^*\) for general \(T\le T_{x}\):

The bracketed term is precisely \(X_x^{{\mathcal {L}}}\), with the ruin probability equal to the smallest non-negative root \(T = \tau _0\) of \(X_x^{{\mathcal {L}}}=0\), or equivalently \(\mathbb {E}[W_T^*\vert {\mathcal {L}}]=0\). In general, we consider the shortfall probability \(\mathbb {P}_{\mathcal {L}}(T_x^*\ge \tau _{\nu })\) where \(T = \tau _{\nu }\) is the smallest root of \(X_x^{{\mathcal {L}}} = \nu \) as per (5.20):

Since \(T_x^*\overset{d}{=}\textrm{Exp}(\Lambda + \lambda ^{\text {ELN}})\) in the \({\mathcal {L}}\) information set, we find the \(\nu \)% shortfall probability:

6 Implementation in the Australian context

To illustrate our optimisation framework and implementation approach, we calibrate and apply them to the Australian context, and obtain interesting insights. These are discussed in details in Sect. 7.

6.1 Calibrating assumptions

We begin our implementation by calibrating the assumptions of Sect. 5.2 to the Australian context.

6.1.1 Calibrating hazard rates

We will consider a retiree of exact age \(x = 67\), which is the age at which they first become eligible for the age pension in Australia. We calibrate \(\lambda = 0.051\) to a 19.42 year life expectancy, which we derive for a male aged exactly 67. We draw upon the Australian Life Table 2019-21 mortality rates \(q_{67+t}^{\text {ALT}}\) (ABS 2022), paired with the most recent Australian Government Actuary (AGA) longevity improvement factors \(f_{67+t}^{\text {AGA}}\) (Thorburn 2019), which are calibrated to the last 125 years of mortality improvement. Factors \(f_{67+t}^{\text {AGA}}\) are given as a percentage annual rate of improvement in mortality rate \(q_{67+t}^{\text {ALT}}\). In our choice of reference population, we implicitly assume there is no adverse selection of policies from the Annuity Family. Thorburn (2019) computes the one-year death probability in t years time for an individual currently aged 67:

We find that the life expectancy of a 67 year old using the more recent, albeit more unreliable, AGA 25-year improvement factors is 20.30 compared to 19.42 derived from AGA 125-year improvement factors. We therefore choose to calibrate \({\hat{\sigma }} = 0.064\) by setting \(\textrm{Var}\left( 1/\Lambda \right) = 1\), allowing for a one-year standard deviation of error in projections of life expectancy. We also set a minimum death hazard rate of \({\underline{\lambda }} = 0.010\).

In our illustration, we set \(T_{67}^{\textrm{ELN}} \equiv T_{67}^{\textrm{LTC}}\), that is we assume LTC needs are the only form of early liquidity needs prior to death. We use the HRS data tabulated by Brown and Warshawsky (2013) to calibrate \(\lambda ^{\text {LTC}} = 0.034\). We minimise the sum of squared differences between \(\textrm{e}^{-t\lambda ^{\text {LTC}}}\) and the age-based proportions \(_tp_{67}^{\text {HRS}}\) of initially healthy individuals requiring LTC over time, attaining a \(R^2\) score of \(83\%\).

6.1.2 Calibrating investment returns

We assume a trend rate of inflation of \(\pi = 2.5\%\) to reflect the midpoint of the target range of the Reserve Bank of Australia (RBA) of between 2.0% and 3.0% p.a. on average, over time (RBA 2023). This rate is also broadly consistent with the 90-day average margin of 2.4% as at 30 June 2023 in the yields between 10-year nominal bonds issued by the Australian Government and the corresponding inflation-indexed bonds. We calibrate annual inflation volatility \(\sigma _{\pi }= 1.85\%\) based on the annualised mean square error in the quarterly growth rate of Consumer Price Index (CPI) around the \(2.5\%\) target over the 30 years to June 2023. On behalf of the RBA, Ellis (2022) states that the Australian long-term neutral cash rate is ‘at least’ 2.5%. Given the current economic uncertainty, we allow for a reasonable risk-free rate of real return of \(r=0.5\%\) through setting the yield on short-term liquid nominal bonds to \(r+\pi = 3.0\%\). In an Australian context, Bishop et al. (2018) suggests that practitioners will often use an annual market risk premium of \(6.5\%\) so we set \(\mu _M = 9.5\%\). We calibrate annual market volatility \(\sigma _M = 16\%\) according to the annualised standard deviation of daily log-returns derived for the S &P/ASX 200 over the 10 years to 30 June 2023.

6.1.3 Calibrating loadings

Realistically, insurers will hold capital for both idiosyncratic longevity risk due to finite n and systematic longevity risk (Zhou 2020). As considered by Milevsky et al. (2006), we find that setting \(S = 20\%\) in (5.6) with \(n=5000\) results in a reasonable loading factor \(\theta = 18.3\%\) for the IIA.

Dus et al. (2005) analysed the value of nominal annuities in Australia through the use of a Money’s Worth Ratio (MWR) which measures the cost effectiveness of a policy to the retiree by quantity \((1 + \theta )^{-1}\). Our simulated loading factor \(\theta \) falls within the range of obtaining the MWR of 88% derived by the authors for males aged 67, and the MWR of 66% derived more recently by Meara et al. (2015) for the IIA in an Australian context.

6.1.4 Calibrating consumption targets

We calibrate values of constant consumption target \(c(t) \equiv c\) based on the Annual Retirement Expenditure (ARE) figures given by the Association of Superannuation Funds of Australia (ASFA) for the June quarter 2023. Since ASFA grosses up weekly expenditure to arrive at ARE, and already accounts for price inflation, we can set \(c = \text {ARE}/W_0\). Furthermore, ASFA sets a higher ARE for retirees aged 67–84 than retirees aged 85+, anticipating a reduction in daily spending needs at older ages. We therefore take a weighted average measure \(\textrm{ARE}^*\) of ARE as per (6.2) in order to avoid overstating spending needs whilst maintaining a constant consumption target.

According to ASFA, the median superannuation account balance for Australians aged 60–64 was $178,808 for males and \(\$137,051\) for females (Clare 2022). However, a single homeowner seeking to retire at age 67 will require at least $595,000 wealth at retirement to afford a Comfortable SOL, even still assuming some late-life dependence on the age pension (ASFA 2023). Since 62% of Australian retirees received the age pension as at June 2022 (AIHW 2023), it is not appropriate to consider the median account balance in a setting without assuming the support of an age pension. We therefore set \(W_0 = \$595,\!000\) in Table 3.

In addition, we are interested in observing the impact of the famous ‘4% Rule’ (Bengen 1994) which sets annual consumption to 4% of initial wealth, adjusted for inflation over time. Based on an empirical study, the Bengen 4% Rule was proposed to maintain the real-value of first-year consumption over a 30 year planning horizon in 90% of scenarios (Bernhardt and Donnelly 2018). Overall, we consider consumption targets \(c\in \left\{ 4.0\%, 5.2\%, 8.2\%\right\} \).

6.2 Notes on algorithm implementation

In Sect. 5.1, we introduced an optimisation algorithm to find the optimal strategy across retirees. We now discuss some practical notes regarding implementation:

-

1.

Since \(_tP_{67}^{(5000)}\) is non-decreasing, we observe in (5.20) that \(X_{67}^{{\mathcal {L}}}\) is not necessarily monotonic in T for the GSA and LIA, sometimes having multiple non-negative roots. We therefore partition [0, 80] into a series of 10 intervals and conduct a search over each successive interval until the first root \(\tau _{\nu }\) is found.

-

2.

Given some chosen resolution of grid for \((b, \psi _{\nu })\), we seem to require some higher resolution of grid for \((w, \phi )\) to reduce noise around decisions between payment vehicles \((g(t))_{t\in {\mathcal {S}}}\) for local values of \((b, \psi _{\nu })\). We find that a \(40\times 40\) grid resolution for \((b, \psi _{\nu })\) under our calibrated assumptions will require at least a \(750\times 750\) grid resolution for \((w, \phi )\). As \(\sigma \) rises, we also notice that the required resolution falls as the trade-off between mean and variance of bequest becomes more distinct.

-

3.

The expressions for \(\textrm{Var}({\bar{C}}^{(5000)}_{67})\) in (5.10) and \(\mathbb {P}_{\mathcal {L}}(T_{67}^*\ge \tau _{\nu })\) in (5.21) arise from conditional probability, requiring iteration over the values of \(\Lambda \). Both these quantities are also functions of w, so we must perform these calculations repetitively as we generate our grids of values. We take a relatively low sample size of 200 for \(\Lambda \) to offset some computational expense.

-

4.

The expected funding cost of lifetime annuity \(a_{67}(w)\), computed from (5.9) as a present value, is a convex function of w with minimum at \(w_0 = 1.25\). As discussed in 5.3.2, \(\textrm{Var}(X_{67}^{{\mathcal {I}}})\) will be the variance of an inverse gamma distribution for all weights less than \(w_1 = 2.30\). Following from (5.16), it becomes unnecessary to consider a higher market weight than \(w_0 = 1.25\). It is also unlikely that retirees can achieve market weights exceeding 1.

Decision boundaries across Annuity Family. The optimal payment vehicle \((g(t))_{t\in {\mathcal {S}}}\) is determined for varying IRA and LRT. Whitespace indicates that there are no admissible strategies within the retiree’s appetite for liquidity risk. The highest level of risk aversion is in the top left corner of each plot.

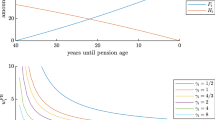

Liquidity shortfall probability for GSA. Liquidity shortfall probabilities \(\mathbb {P}_{{{\mathcal {L}}}}(T_{67}^*\ge \tau _{\nu })\) are plotted for varying target SOL, payment rate \(\phi \) and market weight w. A shortfall threshold of \(\nu = 20\%\) is taken. To illustrate dynamics, the axes are rescaled across target SOL.

7 Findings

We now present the results of implementing our optimisation framework in the Australian context and discuss the key implications for the Australian annuity market and the broader validity of our framework.

7.1 Results

Overall, we find that the retiree’s optimal choice of overall decumulation strategy will depend on the retiree’s investment risk aversion (IRA) and liquidity risk tolerance (LRT) when selecting from admissible payment vehicles \((g(t))_{t\in {\mathcal {S}}}\) and decision variables \((w, \phi )\). We compare these decisions for different choices of consumption target \(c\in \left\{ 4.0\%, 5.2\%, 8.2\%\right\} \) and shortfall threshold \(\nu \in \{0\%, 20\%\}\). Where \(\nu = 0\%\), the retiree is said only to have limited appetite for the probability of ruin in the \({\mathcal {L}}\) information set.

In Fig. 1, we find evidence of optimal strategic choice across the Annuity Family by determining the optimal choice of pooling policy (if any) associated with each retiree’s IRA and LTR. It is optimal for retirees to purchase a payment stream from the Annuity Family for the purpose of portfolio variability reduction in the case that they have little appetite for investment risk; or longevity protection in the case they have little appetite for liquidity risk. In particular, retirees with little appetite for both decumulation risks will correspond to model points in the top left-hand corner of the plot associated with their chosen consumption target c and shortfall threshold \(\nu \).