Abstract

We combine nonparametric price response modeling and dynamic pricing. In particular, we model sales response for fast-moving consumer goods sold by a physical retailer using a Bayesian semiparametric approach and incorporate the price of the previous period as well as further time-dependent covariates. All nonlinear effects including the one-period lagged price dynamics are modeled via P-splines, and embedding the semiparametric model into a Hierarchical Bayesian framework enables the estimation of nonlinear heterogeneous (i.e., store-specific) immediate and lagged price effects. The nonlinear heterogeneous model specification is used for price optimization and allows the derivation of optimal price paths of brands for individual stores of retailers. In an empirical study, we demonstrate that our proposed model can provide higher expected profits compared to competing benchmark models, while at the same time not seriously suffering from boundary problems for optimized prices and sales quantities. Optimal price policies for brands are determined by a discrete dynamic programming algorithm.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Estimating price response functions to support pricing decisions is a highly relevant topic in the marketing literature and in marketing research practice. A price response function or, more generally speaking, a sales response function relates the sales of a brand to own and competitive brand prices, to accompanying marketing activities (like feature or display advertising), and/or to further covariates accounting for time- or store-specific effects. In this paper, we focus on sales response modeling for fast-moving consumer goods that are sold by physical retailers and for which scanner data are nowadays widely available. Publications in this research area have particularly focused on the following dimensions:

First, the specification of the ‘correct’ functional form for the relationship between sales and prices was dominated by strictly parametric modeling until the 2000s, starting with simple linear regression (lin-lin) models and followed by nonlinear parametric models, especially multiplicative (log-log) and exponential (log-lin) models. To overcome the problem that parametric models can largely fail to approximate the true functional form inherent to real data (Härdle 1990; Van Heerde 1999; Leeflang et al. 2000), researchers started to apply more flexible nonparametric techniques, which are able to explore the functional shape directly from data instead of assuming a predefined parametric functional form (Hanssens et al. 2002). There is very clear evidence from many studies that these nonparametric methods can (greatly) improve the predictive model performance as well as expected profits over parametric modeling.Footnote 1 According to Van Heerde et al. (2002), managers should rely on models which provide the most accurate predictions. Besides, more flexible nonparametric estimation methods have also become established in choice modeling, see, e.g., Abe (1991), Abe (1995), Abe et al. (2004), or Boztuğ et al. (2014).

Second, it is well-known that the aggregation of store-level data across stores of a retail chain leads to biased estimates of the effects of marketing activities if these effects differ for individual stores (as one would expect) but even if marketing effects are homogeneous across stores (e.g., Krishnamurthi et al. 1990; Christen et al. 1997). Further, if marketing effects were different across individual stores of a retailer, pooling store-level data into a homogeneous model should also cause a bias in the effect estimates. Although empirical findings are not unequivocal, heterogeneous store-level sales response models that enable the estimation of store-specific effects often provided more or at least not less accurate sales predictions compared to their homogeneous (pooled) counterparts. More importantly, only heterogeneous sales response models allow for store-specific optimal pricing, also known as micro-marketing pricing (Montgomery 1997). There is further empirical evidence that accounting for (unobserved) heterogeneity can also increase expected chain profits (e.g., Montgomery 1997; Lang et al. 2015).

Third, it is reasonable to assume that past prices of brands or expected prices in future periods might affect a brand’s sales or price response in the current period. Therefore, the accommodation of price dynamics in sales response models has also been of a long tradition, be it via considering lagged or lead price covariates (e.g., Van Heerde et al. 2000, 2004), allowing for time-varying parameters (e.g., Foekens et al. 1999; Kopalle et al. 1999), or incorporating market-level reference price variables (e.g., Greenleaf 1995; Fibich et al. 2003; Aschersleben and Steiner 2022). Almost all of these dynamic approaches have been directed at either explaining structural effects of sales promotions (for example the lack of postpromotion dips in store data), or showing that dynamic pricing can increase profits over static models. Importantly, dynamic pricing allows the computation of optimal price paths, i.e., optimal prices that vary over time due to the consideration of time-dependent effects on price or sales response.

From the previous explanations, it is clear that accommodating functional flexibility in price response, store heterogeneity in marketing effects, and price dynamics can improve both sales predictions and expected chain profits, which is why it seems promising to consider these features jointly in a store-level sales response model. However, not a single approach has yet accounted for all three dimensions simultaneously. Therefore, our first research question is whether a sales response model that combines the three components can provide higher expected chain profits compared to existing simpler (nested) models. In particular, our proposed approach will allow for the derivation of optimal price paths by modeling heterogeneous nonlinear price effects via nonparametric price functions (including the one-period lagged price effect), and we will assess whether this higher model complexity pays off compared to simpler models.

As indicated above, some researchers went beyond the descriptive modeling stage and used an estimated sales or price response model as basis to subsequently derive optimal prices or price paths. Most of these optimization models assume linear price effects, i.e., price effects estimated by strictly parametric response modeling, and almost all of these parametric approaches also included price dynamics. The optimization results for many of these parametric approaches provide evidence or at least suggest the existence of corner solutions, i.e., that optimized prices hit the upper boundary of observed prices, which would make the price optimization exercise seem less useful. At this point, it is important to note that none of the dynamic optimization approaches has modeled price response more flexibly, like we propose in our model. Our second research question therefore relates to this boundary pricing problem, making our proposed approach recommendable only if optimal prices do not, or not always or not very frequently hit the boundaries of observed prices (and as well do not induce boundary solutions for related sales quantities). More explicitly, we want to analyze how prone our proposed model is to boundary price hits. If the boundary pricing problem is not an issue, we are probably the first to enable the calculation of optimal price paths for each of the stores of a retail chain via nonparametric heterogeneous price effects modeling.

The rest of the paper is organized as follows: In Sect. 2, we provide a review of the relevant literature for our approach. In Sect. 3, we introduce our new dynamic semiparametric Hierarchical Bayesian sales response model together with nested model versions. We will use the latter for model comparison. We further propose a discrete dynamic programming approach for calculating optimal price paths. Section 4 starts with a short description of the store-level scanner data used in our empirical study and provides details about model estimation and validation procedures. Moreover, optimal prices, optimized profits, and expected losses when not using the proposed model are analyzed. In Sect. 5, we conclude with a summary of findings and discuss limitations of our research.

2 Literature review

Table 1 provides a summary of relevant articles related to sales response modeling in the field of fast-moving consumer goods that have combined at least two of the dimensions discussed in the introduction (i.e., functional flexibility in price response, store heterogeneity in marketing effects, price dynamics, price optimization) in their empirical applications.

As mentioned before, nonlinear parametric models were state-of-the-art for a long time to capture price or more generally sales effects for fast-moving consumer goods (e.g., Hruschka 1997; Montgomery 1997; Foekens et al. 1999; Kopalle et al. 1999; Van Heerde et al. 2000, 2002; Hruschka 2006b; Andrews et al. 2008), and they still serve as benchmarks for the more sophisticated nonparametric approaches observed nowadays in many publications. Possible nonparametric operationalizations have ranged from kernel regression (e.g., Van Heerde et al. 2001) and neural nets (e.g., Hruschka 2006a, 2007) to splines such as stochastic cubic splines (Kalyanam and Shively 1998), B-splines (Hruschka 2000; Haupt and Kagerer 2012; Haupt et al. 2014) or Bayesian P-Splines (Steiner et al. 2007; Brezger and Steiner 2008; Weber and Steiner 2012; Lang et al. 2015; Weber et al. 2017). It is clear from the existing studies in this research area that more flexible estimation techniques are more powerful to uncover complex nonlinearities in sales response and, if these are at work, may lead to much better sales predictions and higher expected profits.

The consideration of (unobserved) store heterogeneity in sales response modeling has become even more established, see the column ‘Store heterogeneity’ in Table 1. Some researchers have only included store intercepts in order to account for heterogeneity in baseline sales across stores. The more advanced approaches to also capture store heterogeneity in marketing effects have all been embedded into Hierarchical Bayesian (HB) estimation frameworks,Footnote 2 where some of them have accommodated both heterogeneity and functional flexibility in price effects (Hruschka 2006a, 2007; Lang et al. 2015; Weber et al. 2017) and the latter three of them price optimization in addition. Interestingly, some researchers found that accounting for store heterogeneity in a parametric sales response model did not necessarily improve the predictive model performance (Andrews et al. 2008; Weber and Steiner 2012, 2021), whereas Weber et al. (2017) did report major advantages from addressing store heterogeneity as soon as functional flexibility in price response was taken into account. Leeflang et al. (2000) already very early called for more intense research with regard to the comparison of heterogeneous versus homogeneous store-level sales response models, and we pick up their suggestion for model comparison in our empirical study later on.

Price dynamics were only seldom considered in models with nonlinear price effects, Van Heerde et al. (2004) and more recently Aschersleben and Steiner (2022) are the exceptions with their empirical studies. These two approaches, however, did not account for store-specific marketing effects. Fok et al. (2006) and Horváth and Fok (2013) proposed Hierarchical Bayesian vector autoregression models to analyze brand-/category-specific differences in dynamic price effects on sales. But the focus of these two studies was more on the investigation of brand- and category-specific characteristics as moderators for differences in own- or cross-price effects between brands and product categories rather than on within-brand store heterogeneity in price response (especially as Fok et al. 2006 used data from only one single store). The two approaches that combined price dynamics and store heterogeneity (Foekens et al. 1999; Kopalle et al. 1999) only included store intercepts to consider differences in baseline sales across stores. Similar to Leeflang et al. (2000), we here see the need for a more intense research to assess the effect of price dynamics in store-level sales response models that as well account for store-specific effects and ideally also for functional flexibility in price response. Generally, we observe quite different strategies to accommodate price dynamics in sales response models: via lagged and lead prices (Van Heerde et al. 2004; also, e.g., Van Heerde et al. 2000), via time-varying parameter models (Foekens et al. 1999; Kopalle et al. 1999; also, e.g., Ataman et al. 2010), via vector-autoregressive specifications (Fok et al. 2006; Horváth and Fok 2013; also, e.g., Nijs et al. 2001), as well as via market-level reference prices (Greenleaf 1995; Fibich et al. 2003; Aschersleben and Steiner 2022).

Only the minority of the papers collected in Table 1 provided normative implications with respect to expected profits or to expected losses from not using the sales response model with the best predictive performance. Like the milestone article on micro-marketing pricing strategies by Montgomery (1997), all more recent optimization approaches used a Hierarchical Bayesian estimation framework to allow for store-specific (or at least clusterwise) optimal pricing (Hruschka 2006a, b, 2007; Weber et al. 2017; Lang et al. 2015). None of them, however, incorporated price dynamics for price optimization. On the other hand, the three remaining approaches that considered dynamic price effects on sales response (Greenleaf 1995; Kopalle et al. 1999; Fibich et al. 2003) did not allow for price optimization by modeling nonlinear and/or heterogeneous store-level pricing effects. But, the findings from the latter three studies still indicated that accommodating price dynamics can increase profits over static price optimization.

As another important issue, several of the price optimization studies seem to provide evidence of corner solutions for optimized prices, i.e., that optimized prices would have hit the upper boundary of the observed price range if this upper boundary had been imposed as a constraint in the model.Footnote 3 Interestingly, this applies to all three papers that incorporated price dynamics for price optimization (Greenleaf 1995; Kopalle et al. 1999; Fibich et al. 2003), and these three dynamic optimization approaches have further in common that they used linear pricing effects (i.e., price effects estimated by a parametric sales response model). The corner solution problem seems as well evident in the paper of Montgomery (1997), who did not consider price dynamics but also used a parametric sales response model (an exponential one) to determine optimal prices. Three optimization approaches were based on semiparametric sales response models, where nonlinear price effects were estimated using neural nets or splines in the descriptive model stage (Hruschka 2007; Lang et al. 2015; Weber et al. 2017). Indeed, the findings reported in Hruschka (2007) and Weber et al. (2017) suggest that flexible estimation methods might be less affected by the boundary pricing problem.Footnote 4 Note that we found no evidence that optimized prices hit the lower bound of observed prices. And, neither paper further allows conclusions about boundary effects for predicted sales quantities based on optimized prices.

At this point, it is very important to mention that the findings from our explorative research on boundary price effects should be treated with caution since the corner solution problem is not explicitly addressed in any of the papers and information on boundary effects is sparse. In general, optimal prices depend on price elasticities and on variable costs (in our case the wholesale prices of a retailer). Still, the price elasticity in parametric models is much more “rigid”, as it depends on one or only few price parameter estimates which globally determine the shape of the response function over the entire observed price range. Nonparametric estimation techniques like splines, on the other hand, fit the data locally, entailing greater flexibility for uncovering complex price response patterns and allowing locally varying price elasticities. This locally fitting property can make flexible models less prone to corner solutions for optimal prices. Note that none of the dynamic optimization approaches has modeled price response more flexibly, like we propose in our dynamic model. And different from all previous studies in this field, we will put a special focus on the boundary pricing problem in our empirical study.

Based on the literature review, the central contribution of this paper is that our proposed model will allow for price optimization by modeling heterogeneous nonlinear pricing effects through nonparametric functions for own-, cross-, and lagged price response. In other words, we are probably the first to enable the computation of truly dynamic price pathsFootnote 5 for each store of a retail chain due to heterogeneous nonlinear pricing effects embedded in a semiparametric sales response model. None of the previously proposed sales response models has combined the three features functional flexibility, store heterogeneity, and price dynamics to derive optimal pricing strategies for fast-moving consumer goods.

3 Model specification and optimization approach

In the following, we introduce a semiparametric, heterogeneous, and dynamic store-level sales response model. We use Bayesian P-splines as nonparametric method to estimate immediate and lagged price effects flexibly, allowing us to uncover possibly exceptional pricing effects (like distinct threshold or saturation effects) directly from the data. An advantage of P-splines is that they can easily be constrained to provide monotonic shapes of price response (Brezger and Steiner 2008), which is reasonable from an economic point of view for fast-moving consumer goods. Following Lang et al. (2015), heterogeneity in price response across stores is captured via store-specific scaling factors, which can be as well easily embedded as additional parameters into the Gibbs sampling procedure of our Hierarchial Bayesian estimation framework. Since the shape of the price response is pooled over stores by this heterogeneity specification (i.e., functional flexibility and heterogeneity in price response are not decoupled), we further provide robustness checks by varying the number of knots and the degree of the underlying B-spline basis functions. Dynamics are accommodated via the one-period lagged own-item price since more time lags were not supported by the data for almost all brands considered. We will also check the assumptions required for a proper estimation of the models (multicollinearity, heteroskedasticity, autocorrelation). We apply a discrete dynamic programming algorithm to derive optimal price paths.

3.1 Semiparametric heterogeneous dynamic model

We use the following additive sales response model with smooth nonparametric and multiplicative random price effects.Footnote 6 Accordingly, the (log) unit sales of a brand in a specific store and week are assumed to depend on own- and competitive price effects (where the latter are captured at the quality tier level), as well as a dynamic, one-week lagged own-price effect. We further include promotional activities for the brand (use of a display, odd pricing) and accommodate seasonality effects via a smooth monthly trend and unobserved store-specific effects. Models are estimated for each brand separately, thus brand indices are omitted.

where \(f_0\) is an unknown smooth nonlinear time trend of the calendar month (\(m_t\)); \(f_1\) is an unknown smooth nonlinear decreasing function of the brand’s own price (\(p_{st}\)); \(f_2\) is an unknown smooth nonlinear increasing function of the brand’s one-week lagged own price (\(p_{s;t-1}\)); \(f_{c_i}\) are unknown smooth nonlinear increasing functions for cross-price effects (\(p^{c_i}_{st}\)) captured at the level of the price-quality tiers \(c_i\), where \(c_i \in \{(\text {prem}), \text {(nat)}, \text {(priv)}\}\) denotes premium, national, and private label brands (compare Table 6 in the Appendix); \((1 + \alpha _{s1}), (1 + \alpha _{s2}), (1 + \alpha _{s,c_i})\) are store-specific scaling factors capturing price heterogeneity in a multiplicative way; \(\varvec{v}'_{st}\) contains store-specific random slopes for marketing activities represented by indicator variables (e.g., use of a display, odd price endings), and the vector \(\varvec{\gamma }_s\) captures the corresponding parametric effects; \(\beta _s\) is a store-specific random intercept for store \(s\); \(\varepsilon _{st}\) is a Gaussian error term with mean zero and variance \(\sigma ^2\).

The unknown smooth nonlinear functions \(f\) are modeled via Bayesian P-splines (Lang and Brezger 2004), and the scaling factors \(\alpha _{s,j}\) of the price response functions account for unobserved heterogeneity in (smooth) price response across the stores. Aschersleben and Steiner (2022) recently provided a larger paragraph on the advantages of using nonparametric regression techniques in general and Bayesian P-splines in particular (Aschersleben and Steiner 2022, p. 632). In a nutshell, nonparametric estimators “read out” the functional shape of a predictor effect directly from the data, while parametric models require the specification of a fixed functional form a priori. This property of nonparametric methods is especially beneficial in our context for uncovering existing steps or strong kinks in price response (e.g., caused by effects of psychological or reference prices, or the existence of different reservation prices across consumers), which are generally more difficult to capture with parametric functions. Bayesian P-splines additionally offer some very convenient estimation properties: (a) Overfitting as a possible undesirable result of the higher flexibility of nonparametric estimators can easily be counteracted through a roughness penalty term (hence the name P-splines). (b) The amount of smoothness of a predictor effect can be estimated jointly with all other parameters when using a Bayesian estimation framework (Lang and Brezger 2004), i.e., no additional smoothing parameter selection procedures are required. (c) Not least, as mentioned above, the extended Gibbs sampling procedure as developed by Brezger and Steiner (2008) allows to easily accommodate monotonicity constraints for price effects. Steiner et al. (2007) further provided a graphical illustration how the P-spline approach works (Steiner et al. 2007, p. 391). For P-spline estimation, we use by default 20 equidistant knots within the range of observed levels of each of the metric covariates (prices, calendar time). This is in line with Eilers and Marx (1996), who introduced P-splines into the statistical literature and recommended the use of 20 to 40 knots in order to guarantee enough flexibility for a smooth function to be estimated. As noted above, a roughness penalty is imposed on neighboring knots in order to prevent an overfitting of the splines at the same time, and we use the common setting of a second-order random walk for this penalty. This smoothing or regularization implies that the effective number of parameters to be estimated is much less than the number of knots. Note that because the underlying B-spline basis functions (roughly corresponding to the number of knots) overlap and the data set therefore cannot be divided, a P-spline is not estimated as a sequence of separate (Bayesian) regression functions but as a whole, while at the same time preserving its local fitting property. Lastly, P-splines are further determined by the degree of the B-spline basis functions, where we use B-splines of degree 3 by default corresponding to cubic splines. Technical details on the Bayesian inference of our models, especially for the smooth functions for price effects and their scaling, are available from the authors upon request.

By using single-brand equations, we implicitly take the perspective of brand managers, who should be interested in analyzing the consequences of suboptimal pricing strategies from using a wrong sales response model for their brand(s), assuming fixed price patterns for competing brands and the possibility to adjust the price of the own brand in the retailer’s assortment. In case brand managers have only access to retail data on a more aggregate level, e.g., on the chain-level, they must cooperate with the retailer or outsource a project to obtain the desired analysis at the store-level (e.g., Hruschka 2006b, p. 94). In addition, product category managers of the retailer could use the brand perspective as well to analyze how price changes for one brand in the assortment affect category sales and profits. Independent of that, the study should provide evidence of the benefits of using a more complex model that includes heterogeneity, functional flexibility, and price dynamics for optimal pricing over simpler models that ignore some or all of these dimensions.

3.2 Benchmark models

As the focus of this article is on combining price dynamics, flexible nonlinear modeling, and store heterogeneity, the model as stated in Eq. (1) and referred to as DynFlexHet in the following, is the most complex one, i.e., it combines all three dimensions of interest. Contrary to that, the other (benchmark) models only account for some of these dimensions or none of them such that the most simple model is a static model without price dynamics and with parametric and homogeneous effects only (StatParHom). Table 2 shows how the three model features can be combined to a total of \(2^3 = 8\) different models, with the model in Eq. (1) as proposed model and the other seven as benchmark models. The benchmark models are nested in the DynFlexHet model in the sense that ignoring the lagged price effect leads to static models, and/or replacing the unknown smooth nonlinear functions for the price effects by parametric effects leads to parametric models, and/or ignoring heterogeneity in marketing effects leads to homogeneous models.

As in Eq. (1), all benchmark models use log brand sales as dependent variable. The parametric models are specified as multiplicative models for capturing price effects, relating log brand sales to log-transformed prices. The multiplicative model is the most widely used parametric (store) sales response model, also because of its higher flexibility to modeling cross-price effects (convex, concave, or linearly) compared to other parametric models (see among others, Foekens et al. 1999; Kopalle et al. 1999; Van Heerde et al. 2001; Hruschka 2006a, b; Weber and Steiner 2012; Horváth and Fok 2013; Weber et al. 2017). Note that the seasonality effect is generally modeled via a flexible function across the competing models (i.e., even in the parametric models) and that homogeneous models still include store-specific random intercepts in order to accommodate differences in baseline sales of the brands across stores.

3.3 Discrete dynamic pricing

Our aim is to find optimal brand prices \(p^*\) for the stores in our data set so that a brand’s total chain profit \({{\mathrm{\textit{V}}}}\) is maximized:

where \(c\) represents the variable cost (wholesale price) and \({{\,\mathrm{\textit{q}}\,}}\) the sales response function.

Optimal prices are determined from a brand management perspective based on the assumptions of a fixed promotion calendar (e.g., as described in Silva-Risso et al. 1999; Chintagunta et al. 2003) and given competitive prices in each store and week as observed in the data. This is also known as fictitious play (Brown 1951, as cited by Hruschka 2006b, p. 99) and implies that communicative promotional activities (like display advertising) as well as future prices of substitute brands occur with frequencies as in the past and do not become part of the optimization. We further dispense with error correlations between brands like in the SUR (seemingly unrelated regression) model approach by Weber et al. (2017) to prevent additional model complexity. Note that there are no interactions between stores (e.g., Montgomery 1997), i.e., the search for optimal prices can be conducted for each store separately, even if heterogeneity across stores is considered. Thus, the objective function \({{\,\mathrm{\textit{V}}\,}}\) can be written as an additive function of total profits \(v_{mi}\) across all brands (\(m\)) and stores (\(i\)):

where \(\delta = 1/(1 + r)\) is a discount factor with discount rate \(r\). As \({{\,\mathrm{\textit{q}}}}_t\) does not only depend on the current own price \(p_t\), but also on the lagged own price \(p_{t-1}\) (see Eq. (1)), this is a dynamic system, and we transfer Eq. (4) into a dynamic program by introducing the state and action variables \(s_t\) and \(x_t\) in the following to employ the optimization step. In our context, the brand’s one-period lagged own price represents the current state (\(s_t = p_{t-1}\)), and the action variable is defined as the brand’s own price to be set in period \(t\) (\(x_t = p_t\)). In the given setting, as indicated above, it is sufficient to optimize these brand- and store-specific profits \(v = v_{mi}\) separately, leading to the following general formulation:

The state variable \(s_t\) is an element of the state space \(S_t = S\) that contains all possible prices and is thus discrete and constant for all periods. The same holds for the action space \(X_t(s_t) = X_t = X\) that is further independent of the current state, i.e., the action space of feasible levels for setting the price in the current period is independent from the price of the previous period (and thus constant in all periods). The next period’s state \(s_{t+1}\) equals the value of the action variable of the previous period so that the new lagged own price in period \(t+1\) is the selected own price for period \(t\) and the corresponding transition function \({{\,\mathrm{\textit{g}}\,}}\) simplifies to

Then, setting the initial value \(s_1 = p_0\), the complete dynamic program can be stated as follows:

Following Bellman’s principle of optimality, we can write this problem as a Bellman equation

and solve it iteratively via forward or backward recursion (Miranda and Fackler 2002, Ch. 7). Note that optimization in the static model variants reduces to a week- and store-wise price search without the consideration of time interdependencies and therefore does not require a dynamic program.

4 Empirical study

In this section, we describe the data used in our empirical study and provide details about model estimation including a visual inspection of model fit. We further propose measures for evaluating the predictive model performance and discuss the predictive validity results for the competing models. The section ends with a detailed analysis of normative pricing and profit implications based on the competing models (optimal price paths, optimal profits, price image issues, expected losses), as well as with an illustration and evaluation of boundary price effects.

4.1 Data

For our empirical analysis, we use scanner data for refrigerated orange juice brands sold by a large supermarket chain in the Chicago metropolitan area (Dominick’s Finer Foods). The data are freely available at the James M. Kilts Center of the University of Chicago for academic purposes. Our data refer to weekly unit sales of 64 oz. packages for \(b \in \{1, \dots , B = 8\}\) brands that can be grouped into three price-quality tiers: the two premium brands “Florida Natural” and “Tropicana Pure”, the five national brands “Citrus Hill”, “Florida Gold”, “Minute Maid”, “Tree Fresh”, and “Tropicana”, and the private label brand “Dominick’s” representing the supermarket’s own store brand. The data were collected in \(s \in \{1, \dots , S = 81\}\) stores of the supermarket chain over a time span of \(t \in \{1, \dots , T_s\}\) weeks with \(T_s \in [74; 87]\), resulting in a total of 54,260 observations. Descriptive statistics for weekly prices and price changes, market shares, and unit sales are displayed in Table 6 in the Appendix. Importantly, the share of weeks with a different store-specific price compared to the previous week ranges between 38.6% and 56.1% across brands, indicating a high price variation of the brands in this product category and making the consideration of dynamic price effects on brand sales appear promising.

We treat cross-price effects at the tier level to reduce the model complexity on the one hand but also to account for the fact that cross-price effects are commonly much weaker than own-price effects on the other hand. We therefore capture cross-price effects by using the lowest price of the competing brands within each price-quality tier per store and week, following, e.g., Brezger and Steiner (2008). This leads to three cross-price variables representing the premium brand, national brand, and private label brand tiers, denoted as \(p^\text {(prem)}\), \(p^\text {(nat)}\), \(p^\text {(priv)}\) in the following. Note that the sets of premium and national brands considered for computing the lowest competitive price within a tier differ depending on the brand for which the sales response models are estimated. And, since the retailer’s own brand is the only private label brand, sales equations for this brand only contain the two cross-price variables \(p^\text {(prem)}\) and \(p^\text {(nat)}\).

The data provide further information on the use of a display (\(D_\text {disp}\)) and whether a brand was offered at a 9-ending or a 99-ending price (\(D_\text {9}\), \(D_\text {99}\)) per week and store. We consider this information by using corresponding indicator variables (mutually exclusive for 9 and 99 price endings). Finally, we include a seasonality variable (\(m\)) as additional covariate to capture seasonal effects on a (calendar) monthly level with a smooth nonlinear function.

4.2 Model estimation and validation

All models are estimated with the public domain software package BayesX (Brezger et al. 2005), and results are analyzed using the free and open source software R (R Core Team 2022). We use Gibbs sampling to generate a total of \(52{,}000\) draws from the posterior distribution, with a burn-in period of \(2000\) iterations and a thinning value of \(50\) to minimize autocorrelation of the draws, and finally save \(D = 1000\) draws from the Markov chain. Model performance is assessed based on the individual parameter (Gibbs) draws instead of using the posterior means of estimated parameters (e.g., Montgomery 1997; Hruschka 2006b; Lang et al. 2015) to account for parameter uncertainty. This means that predictions \({\hat{\eta }}_{st}\) for log unit sales (\(\log (q_{st})\)) are calculated as the mean across \(1000\) draw-based predictions \(\hat{\eta }_{st,d}\):

Since predictions of a brand’s unit sales (and not log unit sales) are relevant for managers, conditional mean predictions for unit sales can be obtained via \({\hat{q}}_{st} = \exp ({\hat{\eta }}_{st} + {\hat{\sigma }}^2/2)\), following Greene (2008, p. 100).

We compare the prediction accuracy of the different models along different error measures. One widely used measure is the Root Mean Squared Sales Prediction Error (RMSE, see, e.g., Van Heerde et al. 2001):

In particular, we compute the Average Root Mean Squared Sales Prediction Error (\(\text {ARMSE}\)) in holdout samples based on a \(C\)-fold subsampling with \(C = 9\) folds. For this, we randomly draw \((C-1)/C = 8/9\) of the total sample of observations for a brand and use them for model estimation, calculate the \(\text {RMSE}\) for the remaining part (holdout), and finally average over the \(C = 9\) individual \(\text {RMSE}\) values:

As our second measure to assess the quality of out-of-sample predictions, we introduce the Continuous Ranked Probability Score (\(\text {CRPS}\)), which has not been used before in the store sales modeling literature.

The general idea behind this scoring rule is to compare two distributions by the integral of the squared difference of their cumulative distribution functions (cdfs) (Matheson and Winkler 1976). The \(\text {CRPS}\) is, however, most often used in a nested version to compare probabilistic and deterministic outcomes. Then, it can be used to measure the squared error between a probabilistic forecast and a point measure, the former relating to the draw-based predictions for a brand’s unit sales and the latter relating to the corresponding observed sales of a brand’s unit sales in a certain store and week in our context. In this variant, the \(\text {CRPS}\) can be seen as a continuous version of the well-known Brier score that is defined as the mean squared error between a discrete outcome \(y\) and a corresponding probabilistic forecast based on the cdf \(F\) (see, e.g., Gneiting and Raftery 2007; Jordan 2016, pp. 37–38):

In empirical applications, the underlying true distribution \(F\) is commonly unknown. Using an empirical cdf \(\hat{F}_n^{\text {ecdf}}\), based on \(n\) observations, as an approximation of \(F\), the \(\text {CRPS}\) score can be computed by the following consistent modification of Eq. (11) (Jordan 2016, Sect. 6; Krüger et al. 2021):

Figure 1 illustrates the concept behind the \(\text {CRPS}\) for a better understanding: as the score is calculated as the integral over squared differences between two distributions, with one of them being degenerated to a point measure, the \(\text {CRPS}\) represents the size of the gray-shaded area between the cumulative distribution functions. In other words, the distribution function for the predictive distribution is compared to the ideal distribution function of a point mass in a newly observed value by forming the squared distance and integrating over it. The more the two distribution functions overlap, i.e., the more they coincide, the lower is the distance between them.

Example figure for the \(\text {CRPS}\) scoring rule: the gray-shaded area represents the integrated squared difference between the empirical cumulative distribution function \(\hat{F}_n^{\text {ecdf}}\) of a sample of F and the single-point empirical cdf (ecdf) of observation y

In our case, the draws saved from the Markov chain after convergence are samples from an (unknown) posterior distribution \(F^\text {post}\), and using this scoring rule we again account for parameter uncertainty. Note that we obtain one \(\text {CRPS}\) value as “counterpart” to every observation \(q_{st}\), and averaging the \(\text {CRPS}\) values again across all weeks and stores provides us with a mean \(\text {CRPS}\) value (\(\text {MCRPS}\)) for each holdout:

Finally, averaging the individual \(\text {MCRPS}\) values over the \(C\) folds results in the \(\text {AMCRPS}\) value as our second predictive accuracy measure corresponding to the \(\text {ARMSE}\). We use the R package scoringRules (Jordan et al. 2019) to compute the \(\text {CRPS}\) values according to Eq. (12).

4.3 Estimation results and predictive model performance

4.3.1 Estimation results

Estimation results for the most complex DynFlexHet model as described in Eq. (1) are illustrated for the brand “Minute Maid” as example in Fig. 2. Remember that this model accounts for heterogeneous effects across stores, functional flexibility in price effects, and price dynamics represented by the one-period lagged own-price effect. Depicted are the heterogeneous spline estimates together with the partial residuals as well as violin plots for the display and 9- or 99-ending price effects.

Estimation results for the DynFlexHet model using the brand "Minute Maid" as example: estimated effects and partial residuals for own, lagged, and competitive price variables (accounting for heterogeneity via scaled spline slopes) as well as estimated effects for display and odd price endings (heterogeneous effects displayed by violin plots)

First, estimates and the corresponding effect sizes suggest face validity. The strongest effect is observed for the own-price effect, and it is also the one of the price effects showing a larger amount of heterogeneity across stores as is represented by the relatively large bandwidth of the scalings of the spline functions. More specifically, 21% of (a total of 3240) pairwise 80% credible intervals for the estimated scaling factors do not overlap between stores, confirming that own-price effects significantly differ between many stores. We will further discuss below in more detail that, as a rule, own-price effects for all eight brands are much more heterogeneous across stores than both cross-price effects and lagged price effects (see Fig. 4). The overall slope of the own-price effect reveals a threshold effect near 1.75$ beyond which sales of “Minute Maid” strongly increase. The lagged price effect shows a steeper slope for small price levels than for medium and high price levels (where the lagged price effect is rather flat), and in addition a less distinct threshold effect at 2.50$. This suggests that customers respond less to high prices of “Minute Maid” in the previous period, in terms of buying more of the brand in the current period, than to a very low previous price in terms of buying less of “Minute Maid” in the current period. In other words, less purchases seem to be postponed if the previous price is very high while a certain level of stockpiling appears to occur in case of a very low one, albeit these conclusions are difficult to validate with aggregate data. Some purchase deceleration however obviously exists for prices larger than 2.50$. Compared to the own-price effects (including the lagged price effect), cross-price effects turn out rather flat with sales of “Minute Maid” being least (most) affected by the private label brand (premium brands). Interestingly, the sales effect of a 9-ending price (excluding a price ending in 99) is frequently (much) larger than the one for a 99-ending price (excluding other price endings in 9) and turns out significantly positive for \(93.8\)% of the stores (\(D_{99}\): \(59.3\)%). The display effect is not significant for all stores but one.

Figure 3 displays the lagged price effects in the four dynamic models for the brand “Minute Maid”, see the homogeneous and heterogeneous parametric models (top left and right panels) and the corresponding flexible model versions (bottom panels). The advantage of using a flexible approach instead of modeling the effect in a parametric way becomes obvious again, as was already visible in Fig. 2: nonlinearities with piecewise steeper or flatter slopes can be modeled with Bayesian P-splinesFootnote 7 but not with parametric functions. Nevertheless, a closer look at the bottom left panel reveals wide confidence bands at the lowest price levels, where only a few observations are available.Footnote 8

Estimated effect of the lagged price on the sales of the brand “Minute Maid” for the different dynamic model variants

Note that there is virtually no difference in the estimated own-price effects between the respective static and dynamic model variants, as illustrated in Fig. 9 in the Appendix. This implies that the immediate own-price effect remains highly robust even if the models are extended to capture price dynamics. Plots of the estimated lagged price effects for all eight brands obtained by the DynFlexHet models are provided in Fig. 10 in the Appendix, showing very different shapes across brands and hence confirming the benefits of nonparametric estimation as well for the dynamic price effects. The complete estimation results for all brands are available from the authors upon request.

Figure 4 shows density plots of the estimated store-specific scaling or random effects parameters for the DynParHet and DynFlexHet models in order to get a deeper understanding about how much heterogeneity is inherent to our data and how this heterogeneity is handled by these two model variantsFootnote 9. Some points from Fig. 4 are in particular noteworthy. First, as already illustrated in Fig. 1 for the brand “Minute Maid”, heterogeneity across stores is especially distinct for the own-price effect; this applies more or less to all eight brands independent whether the own-price effect is captured flexibly or parametrically. Second, heterogeneity between stores does not seem to be an issue for both the lagged price effect nor for cross-price effects if price effects are modeled parametrically (DynParHet). However, once price response is modeled flexibly both lagged price effects and cross-price effects do reveal a moderate amount of store heterogeneity for all brands. Lang et al. (2015) have previously provided a possible explanation for this phenomenon, albeit not in the context of price dynamics. And third, there is also some heterogeneity across stores in the effects of using odd prices and a display for all brands and, like for the own-price, the effects are rather stable across the two models (DynParHet, DynFlexHet).

Density plots of store-specific scaling or random effect parameter estimates (centered around their mean) for the DynParHet and DynFlexHet models

4.3.2 Predictive performance

We evaluate the predictive performance of the competing models in terms of the Average Root Mean Squared Sales Prediction Error (\(\text {ARMSE}\)) and the Average Mean Continuous Ranked Probability Score (\(\text {AMCRPS}\)), which were introduced in Sect. 4.2. We use a 9-fold subsampling, where 8/9 of the data (randomly drawn without replacement) are used each time for model estimation and the remaining 1/9 of the data serves as holdout sample. The predictive validity results for the two performance measures are reported in Table 3 for the \(\text {ARMSE}\) measure and in Table 4 for the \(\text {AMCRPS}\) measure, together with relative improvements or deteriorations of the different models in predictive accuracy compared to the proposed DynFlexHet model (for each brand and aggregated at the median) and frequencies in how many cases each model provided the best performance (row ‘# best’).

From Table 3, we at first observe that different models perform best for different brands in terms of the \(\text {ARMSE}\) measure, i.e., there seems to be no clear favorite model under this error measure at first glance. For seven out of eight brands, a flexible model version provides the best predictive accuracy, as does a dynamic model version for six of the brands, while for three brands the best model is a heterogeneous one. On the other hand, when aggregated across brands, the proposed DynFlexHet model is only slightly outperformed by the DynFlexHom model and provides the second-best predictions, see the median in relative changes in the \(\text {ARMSE}\) measure at the bottom of the table.

In Table 4, the picture is completely different and very clear. Using the \(\text {CRPS}\) measure to assess the predictive model performance, the most complex model (DynFlexHet) always provides the most accurate predictions, and concerning the three model dimensions functional flexibility, store heterogeneity, and price dynamics the more complex model variant outperforms its simpler counterpart (i.e., heterogeneous models perform better than homogeneous ones, flexible models better than parametric ones, and dynamic models better than static ones).

To validate our conjecture that the \(\text {ARMSE}\) measure is more prone to extreme observations (e.g., very high sales at very low prices) than the \(\text {AMCRPS}\) measure, we computed the Average Root Median Squared Error (\(\text {ARMedSE}\)) as further performance measure, which is known to be much more robust against extreme observations compared to the \(\text {ARMSE}\) (Franses and Ghijsels 1999). According to the \(\text {ARMedSE}\) measure, the DynFlexHom model performs best for all brands, and dynamic and flexible models almost always perform better than their static and parametric counterparts – just as when using the \(\text {AMCRPS}\). Different from the \(\text {AMCRPS}\) results, homogeneous models are preferred to heterogeneous ones in nearly all cases.Footnote 10 Based on the overall consideration of the results for all three predictive validity measures (\(\text {ARMSE}\), \(\text {AMCRPS}\), \(\text {ARMedSE}\)) we can recommend the use of either the DynFlexHet or DynFlexHom for sales predictions.

4.3.3 Further tests and robustness checks

We also conducted tests for all models (by brand) to assess the assumptions required for a proper estimation of them (multicollinearity, heteroskedasticity, autocorrelation), and briefly summarize results for the proposed DynFlexHet model in the following.Footnote 11 Multicollinearity was not a problem in any case: variance inflation factors (VIF) were never higher than 2.5 across brands and thus far from being critical, where as a rule the highest VIFs could be observed for the own-item price covariates (immediate and lagged prices). Heteroskedasticity was evaluated using the Brown-Forsythe test, which is robust against deviations from normality (Brown and Forsythe 1974). We applied the test to compare the variance of the residuals against the fitted values, and results were more mixed here. The Brown-Forsythe test was not significant for four brands, indicating that heteroskedasticity is not an issue there (e.g., with \(p=0.82\) for “Minute Maid”), while it turned out significant for the other four brands (\(p<0.01\)). We further used a modified version of the Durbin-Watson test for panel data to assess autocorrelation of the residuals, which is as well robust against deviations from the normal distribution (Bhargava et al. 1982; Ali and Sharma 1993). Given the number of covariates and sample size per brand (between 6624 and 6827 observations), the lower critical value around 1.85 is slightly undercut for two brands (\(\alpha =0.05\)), indicating positive autocorrelation only for these two brands. We found no evidence for negative autocorrelation across brands. Heteroskedasticity and autocorrelation lead to biased estimates of standard errors and can affect the validity of statistical tests, with the result of a possibly misleading statistical inference. However, as our focus lies on the predictive model performance and related profit implications, violations of these assumptions seem less severe.

We further performed robustness checks starting with modifications for the specification of the P-splines. By default, we used 20 knots and B-spline basis functions of degree 3 to estimate price effects flexibly. In order to assess the sensitivity of the predictive power (\(\text {AMCRPS}\), \(\text {ARMSE}\)) of the DynFlexHet and DynFlexHom models depending on the number of knots and/or the degree of the B-spline basis functions, we further estimated them with a lower degree of the B-splines (degree 1) and/or more knots (40 knots, corresponding to the suggested upper bound by Eilers and Marx 1996) for the immediate and lagged own-price effects. The \(\text {CRPS}\) scores turned out highly robust for all brands and, except for one brand, the \(\text {RMSE}\) measure as well, indicating that 20 knots are sufficient and B-splines of degree 1 would perform comparable. Details are provided in Tables 7 and 8 in the Appendix.

Finally, we considered only one time lag in the dynamic model versions to consider price dynamics. By definition, this implies that only short-term price-change or short-lived post-promotion effects can be analyzed, while longer persisting marketing effects cannot be accommodated. To test if the data support higher order autoregressive structures, we added two more lags for the own price to the DynFlexHet and DynFlexHom models (with the default settings of 20 knots and degree 3 for the P-splines), capturing the higher-order lag dynamics (lag 2, lag 3) parametrically to keep the model complexity manageable. Again, the \(\text {CRPS}\) scores remained extremely robust in both models except for the store brand, where adding a second price lag somewhat improved the predictive performance. In terms of \(\text {ARMSE}\), adding more lags did not pay off for all brands in the DynFlexHom model and for six brands (including the store brand) in the DynFlexHet model. Details about these dynamic model extensions are provided in Tables 9 and 10 in the Appendix.

4.4 Optimization

4.4.1 Settings and constraints

In order to find optimal (i.e., profit maximizing) store-specific prices for each brand \(m\), we use the dynamic program \((\text {P})\) introduced in Sect. 3.3. As the action space for determining a brand’s optimal price in period \(t\) is independent of the current state (i.e., the brand’s price in the previous period), the set of generally possible prices for the brand is constant over time, hence in each period the same with \(X_t(s_t) = X\). And since \(s_{t+1} = g(x_t, s_t) = x_t\), the state space equals the action space (\(S = X\)). For each brand and store, we set individual state and action spaces as to contain a grid of possible prices in 0.01$ steps between the minimum and maximum observed price levels, denoted as [\(p^\text {obs}_{m,i,\text {min}}\); \(p^\text {obs}_{m,i,\text {max}}\)], for the considered brand \(m\) in store \(i\):

The restriction of optimized prices to the range of observed price levels is chosen to preserve the retailer’s price image perceived by customers. It further helps to obtain realistic predictions, especially when using flexible functions that fit the underlying data locally such that extrapolations could be still more problematic compared to parametric functions.

To start the recursive process and solve the dynamic optimization problem, the initial state \(s_1 = p_0\) has to be fixed. As starting value, we decided to use the price in the middle of the observed price range of a considered brand and store. By conducting some sensitivity analyses, we checked that optimal price paths were fairly robust against variations of this starting value. We further set the discount rate \(r\) to 0 without loss of generality.

As a second constraint, we limit the predicted sales \(\hat{q}\) of a brand in a certain store to the largest number of sales \(q^\text {obs}_{m,i,\text {max}}\) observed for this brand in this store in our data. Using this second constraint lets us stay conservative and prevents us from an overestimation of a brand’s unit sales beyond the upper bound of observed unit sales per week and store for (very) low prices. This guarantees realistic sales scenarios as observed in the data on the one hand, but may trim the greater flexibility of the spline estimates on the other hand. In other words, if the sales forecast for a brand in a store from one of our estimated models is higher compared to the maximum observed sales, we truncate the prediction to the maximum of observed sales:

Note that predictions \(\hat{q}\) are again made at the draw level as already described in Eq. (8), i.e., we integrate the optimization criterion over the posterior distribution of the parameters by averaging the optimization criterion across draws, before optimizing it. To further speed up optimization, we use every tenth draw from the saved draws of the Markov chain after convergence.

4.4.2 Optimal price paths

We use forward recursion to solve the optimization problems and generate 5184 optimal price paths in total (81 stores times 8 brands times 8 sales response models). It seems reasonable to assume that optimal price paths might vary depending on the store-specific scaling factors \((1 + \alpha _{s1})\). For illustration, we continue with the brand “Minute Maid” as example and choose for this brand three out of the 81 stores with a low vs. medium vs. high scaling factor for the own-price effect estimated by the DynFlexHet model.

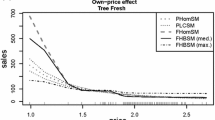

Figure 5 shows optimized price paths for the brand “Minute Maid” for the three selected stores and all heterogeneous model variants. Further depicted are variable costs (also provided in the data) and observed prices as benchmarks for optimized prices (panels in the top row). Observed prices show a very high variation during the first 25 weeks, switching back and forth mostly between only two different price levels with no more than three consecutive weeks at the high price level and no more than two consecutive weeks at the lower price level (note that the high price level is highest in the store with the high scaling parameter, 3.17$, and lowest for the store with the low scaling parameter, 2.62$.) This clear hi-lo price pattern dilutes after the first 25 weeks, but some price levels still show up more often than others (e.g., 1.99$ in all three selected stores), and price cuts of varying depths continue to occur. Also note that the general price level of “Minute Maid” decreases with decreasing variable costs (wholesale prices), as expected.

Optimal price paths for the brand “Minute Maid” for three selected stores based on the DynFlexHet model, coming up with a low, medium, or large scaling factor \((1 + \alpha _{s1})\). Variable costs (wholesale prices) and observed store-specific prices are displayed in the top row, followed by the optimized price paths for the heterogeneous static (middle row) and dynamic (bottom row) model variants

The optimized prices resulting from the StatParHet model (red lines in the middle row) “follow” the costs very closely, i.e., increased costs lead to increased prices and vice versa, and the correlation between observed costs and optimized prices (0.92) is considerably higher than the correlation between observed costs and observed prices (0.60). It is further reasonable that optimized prices end in 9 or 99 since odd pricing was shown to have positive effects on expected sales (see Sect. 4.3.1). This optimized price pattern in parts also holds for the StatFlexHet model (middle row; blue lines), but with a more clear hi-lo pricing scheme and a smaller number of different price levels. Completely different optimal price paths are obtained for the dynamic models. For the store with the low scaling parameter for the own-price effect (bottom left panel), optimized prices resulting from the DynParHet model vary in a much smaller bandwidth. Small price cuts are observed primarily in the second half of the data time window, and the high price level is constant over time. Optimized prices obtained from the DynFlexHet model hardly show any variation (bottom row; blue lines). Deep price cuts are observed in only three weeks, in all other weeks the optimal price is set consistently high at the same unique price level as suggested by the DynParHet model (bottom row; red lines). Note that the optimal high price level resulting from the DynParHet and DynFlexHet models, also interpretable as suggested “regular” price, is a few cents below the maximum observed price, which served as constraint for the upper bound of optimized prices in the optimization model (see Sect. 4.4.1). A similar optimal pricing pattern but with more frequent price cuts from a higher optimal regular price level is found for the store with a medium scaling parameter (compared to the store with the low scaling parameter). Finally, the store with the high scaling parameter for own-price effects shows a much more distinct hi-lo pricing pattern with nearly weekly price changes and very deep price cuts in the second half of the considered time window. Interestingly, the deepest price cuts below a price of 1.75$ are observed at variable costs lower than 1.50$, while the highest suggested price levels exceed 3.00$ in this store. Note that (only) six of these optimal high price levels determined by the DynFlexHet model hit the upper boundary of the observed price range for “Minute Maid” in this store (and none in the other two stores displayed).

We find similar optimal pricing patterns for most of the other brands. For some of them, optimized prices vary only between two or three different levels (especially for the flexible models). Across models and brands, we find that the number of different optimal price levels along the price paths is considerably smaller than the number of observed price levels in the data. Since the number of optimal price levels does not seem to vary that much, it seems interesting to compare optimized prices between different types of models in more detail, i.e., to see how optimized prices compare for the static, parametric, or homogeneous model variants versus the ones of the corresponding dynamic, flexible, or heterogeneous models. We contrast all competing models in a pairwise manner in Fig. 11 in the Appendix and leave a detailed analysis to the interested reader.

The corresponding results are not generalizable across brands. In a nutshell, we find high consistency in optimized prices between the different models only for one brand, i.e., where competing models share the same optimized prices very frequently. The opposite applies to “Minute Maid” (our brand for illustration), where the competing models often suggest different optimal price levels. Larger shares between 42% and 69% for identical optimized prices are observed only between homogeneous models and their corresponding heterogeneous counterparts for this brand. Note that, for many brands, homogeneous and heterogeneous counterpart models more often share the same optimal price levels in a particular store and week than can be observed for models that differ in the other dimensions (parametric vs. nonparametric price effects, static vs. dynamic models). However, even this is not generalizable for the data at hand, as counterexamples exist. Importantly, optimized and observed prices per store and week differ in at least 88% of cases for all brands and models.

To analyze whether or how the existing price image of a brand (and consequently of the retailer) is influenced when moving from the observed to the optimized prices or price paths, we compute the difference between optimized and observed price levels \((p^* - p^\text {obs}) / p^\text {obs}\) per store and week relative to the observed price and collect these ratios via box plots in Fig. 6 (homogeneous models are omitted here for the sake of clarity). The values on the x-axis in Fig. 6 correspond to these percentage changes, where relative increases versus decreases are arranged symmetrically. That is, an optimized price half as high compared to the observed price (\(-50\%\)) appears equally distant from the zero point as a price twice as high (\(+100\%\)). The figure shows that price changes of more than \(-33\%\) or \(+50\%\) occur very seldom. Furthermore, relative price changes are rather symmetrically distributed with slight tendencies to relative price increases (i.e., larger optimized than observed prices), preferably for the dynamic model versions. Overall, the price image of the brands would not be affected too much from a move to optimized prices \(p^*\) from observed prices.

Box plots of differences between optimized and observed price levels relative to the observed price \((p^* - p^\text {obs}) / p^\text {obs}\) per store and week for the heterogeneous models

4.4.3 Profit implications

Up to now, we have searched for optimal (dynamic) prices or price paths to maximize total individual brand-store profits for the retail chain. In the following, we evaluate related profit implications along three dimensions:

Equation (17) represents the actual total profit of a brand \(m\) in store \(i\) based on its observed pricing strategy as given in the data, with \(v^\text {obs}_{mit}\) denoting the corresponding observed profits in week \(t\). In Eq. (18), we compute expected total profits of a brand \(m\) in store \(i\) again based on its observed pricing but now using our estimated sales response models, where \(\hat{v}_{t}(p^\text {obs}) = (p_{t}^\text {obs} - c_{t}) \cdot \hat{q}_{t}(p_{t}^\text {obs}, p_{t-1}^\text {obs})\). The comparison between actual and model-based predicted profits provides us with an assessment of a possible prediction bias for our models, which would translate into the prediction of total expected optimal profits, too. The latter are calculated by Eq. (19) in the same manner as in Eq. (18) but using optimized prices \(p_t^*\) instead of observed prices and the resulting predicted sales \(q_t^*(p_t^*, p_{t-1}^*)\) (or \(q_t^*(p_t^*)\) for the static model variants).

Table 5 summarizes the results for observed, predicted, and optimized (expected) profits for each model and brand, along with summary statistics across brands at the bottom of the table. For each brand, the first row shows predicted mean profits \(\hat{V}^\text {obs}_{mi}\) averaged across stores by model type (cf. Eq. (18)) together with the relative increase or decrease compared to the observed mean profits across stores (\((\hat{V}^\text {obs}_{mi} - V^\text {obs}_{mi}) / V^\text {obs}_{mi}\)). In a similar way, the second row reports optimized mean profits (cf. Eq. (19)) together with the related percentage changes compared to the predicted mean profits based on observed prices. As an example, predicted mean profits for “Minute Maid” based on the DynFlexHet model amount to 1611, a value that is only \(2\)% lower compared to the actual mean profit resulting from the observed pricing strategy (1639, not reported in the table). Contrary to that, the optimized mean profit based on the DynFlexHet model (i.e., using optimized prices based on this model instead of observed prices) are much higher (2976), corresponding to an increase in expected profits of about \(86\)% over the status quo pricing strategy for “Minute Maid”.Footnote 12

The first important finding from Table 5 is that observed and predicted profits (based on observed prices) are very close across brands and models. Most of the predicted profits do not differ more than 3% in both directions as a rule, indicating that the two constraints imposed on the price optimization procedure are reasonable and prevent our models from an over- or underestimation of total profits. The only exception is “Citrus Hill”, where all parametric models consistently underestimate the observed profit by about 10% (note that this is not the case for all flexible models). Opposed to that, optimized profits are substantially higher than predicted profits (based on observed prices), with expected increases ranging between \(19\)% and \(86\)%. Optimized profits are highest under the DynFlexHet model for five brands.Footnote 13 For seven out of eight brands, the highest expected optimal profits are provided by flexible heterogeneous models (DynFlexHet, or StatFlexHet). For six brands, expected optimal profits are highest based on models including price dynamics. And the profit-maximizing model by brand is always a heterogeneous one. Aggregated across brands, the median relative improvements in optimized profits over predicted profits (based on observed prices) are highest for the DynFlexHet and DynFlexHom models (+52%), see the corresponding summary statistics at the bottom of the table. Note that the mean relative improvement (not displayed in the table) is highest for the DynFlexHet model (+55%) followed by the DynFlexHom model (+51%), reflecting the better individual performance of the DynFlexHet model at the brand level (row “# best”). Further, as a rule, expected increases in profits based on optimal prices differ less between models by brand than between brands by model.

Relating to the classification of models given in Table 2, our results on expected profits can be summarized as follows. With the exception of one brand where optimal profits are consistently higher for static models (“Florida Natural”), dynamic model versions almost always lead to (much) higher optimal profits than their static counterparts. Also, optimized profits based on heterogeneous models usually turn out (sometimes considerably) larger compared to their homogeneous counterparts. Finally, flexible modeling (greatly) pays off for most brands compared to parametric modeling, and always provides (much) larger optimal profits once price dynamics have been accommodated. Our findings with regard to profit implications can also be confirmed on the disaggregate store level for six out of eight brands, where the pairwise comparisons between Stat/Dyn, Par/Flex, and Hom/Het models lead to better values for the more complex variants in more than 50% (and often up to over 90%) of the cases.

4.4.4 Expected losses

In the previous subsection, we analyzed profit implications for each model based on the respective optimized prices determined for this model. But which model should be ultimately used for setting prices? As mentioned in the introduction, Van Heerde et al. (2002) have recommended that managers should rely on the model with the most accurate predictions for related decision-making. Our discussion on the predictive performance of the competing models in Sect. 4.3.2 has however produced an unambiguous picture insofar that no unique best model existed across the three different predictive validity measures used. Nevertheless, more complexity always provided a better forecasting accuracy according to the \(\text {AMCRPS}\) measure, suggesting that the DynFlexHet model was the model of choice here, while the \(\text {ARMedSE}\) measure unequivocally tended to the DynFlexHom model instead. Regarding the \(\text {ARMSE}\) measure, at least one of these two models (DynFlexHet, DynFlexHom) also performed best for five brands as well as not dramatically worse for the other three brands. Therefore, without loss of generality, we choose the DynFlexHet model to compute expected losses next.

In particular, we take the optimal prices for a brand determined by the DynFlexHet model and calculate the total (store) profit for this brand (i.e., summing up over all weeks) under the DynFlexHet model. Expected losses in total (store) profit can then be computed when using optimal prices determined by a different model but inserted in the DynFlexHet model for expected profit calculations (cf., e.g., Lang et al. 2015). Note that expected store profits from the DynFlexHet model based on optimal prices of a different model can turn out higher than expected profits from the DynFlexHet model based on its true (i.e., own) optimal prices in particular weeks but not when summed up over all weeks. Therefore, expected losses in total (store) profits are negative by definition compared to the assumed “true” model.

Figure 7 shows box plots for expected losses by stores for the different heterogeneous model alternatives (homogeneous models are omitted in the figure as they provided patterns highly similar to those of their heterogeneous counterparts). One important finding here is that expected losses relative to the DynFlexHet model are generally not larger than 10% for the DynParHet model across all brands (although even a loss of “only” 10% can translate into a huge loss expressed in monetary units). The least complex heterogeneous model (StatParHet) either leads to the highest expected losses for six brands (with a maximum median expected loss of \(26\)% and largest individual store losses of up to \(-40\)% across brands) or expected losses similarly high as for its flexible counterpart (StatFlexHet). The DynFlexHom model on the other hand provides the most inconsistent results here: it shows (much) higher expected losses than the DynParHet model for five brands but performs excellently for the other three brands, where it comes up with only very small or almost negligible expected losses. Overall, the DynParHet seems to be the most robust model variant to reduce expected losses relative to the proposed DynFlexHet model. Therefore, at least for the data at hand, the use of a heterogeneous dynamic model for pricing decisions is strongly suggested. The main (preliminary) conclusion resulting from our optimization exercise is that nonlinear heterogeneous dynamic pricing provides better pricing decisions and higher expected chain profits, and can prevent losses due to suboptimal pricing. That’s why we recommend to prefer the proposed DynFlexHet model.

Box plots of expected losses by store (aggregated over weeks) for the heterogeneous model variants using the DynFlexHet model as “true” model

Finally, it is important to note that optimizing profits or evaluating expected losses based on an econometric model like we do is prone to the Lucas critique, at first glance. Transferred to our context, Lucas (1976) states that since the structure of an econometric model involves optimal decision rules of brand managers and since these rules change systematically with the structure of the time series data relevant to the retailer’s policy, any change in the retailer’s policy will alter the structure of the econometric model (Lucas 1976, p. 41). However, the focus of this paper does not lie on the evaluation of the retailer’s pricing policy but on the comparison of the statistical and normative capabilities of different variants of econometric models and in particular on assessing the benefits of including functional flexibility in price response, store heterogeneity, and/or price dynamics in a sales response model.

4.4.5 Boundary pricing effects

All optimization results discussed above would be of less value if optimized prices always or frequently hit the boundaries of the observed store-specific price ranges. In the following, we illustrate the boundary pricing issue for the following three models: the DynFlexHet, which provided the highest expected profits for most brands (and as well on average across brands) and the most accurate sales predictions based on the \(\text {CRPS}\) score; the DynFlexHom, which as well showed an excellent forecasting accuracy based on all three predictive validity statistics (\(\text {CRPS}\), \(\text {RMSE}\), \(\text {RMedSE}\)); and the DynParHet, which consistently (i.e., across brands) led to the least expected losses compared to the DynFlexHet. We included the latter model also because there seemed to be evidence from our literature search that dynamic parametric models were especially prone to upper bound corner solutions, compare Sect. 2. Figure 8 displays the distributions of store-specific shares of optimized prices hitting the upper bound of the observed price range, both by brand and across all brands. The plots indicate that boundary pricing is not a general problem by brand or model (in the sense that the boundary is always or mostly hit for certain brands or models) and that the occurrence of corner solutions is not critical for most brands. For our example brand “Minute Maid”, optimized prices almost never hit the upper bound in most stores and in the worst case in 12% of the weeks in a store. For two brands (“Citrus Hill”, “Tree Fresh”), however, the upper price bound is hit (much) more often in a larger number of stores. On the other hand, we observe highly different shares of boundary hits across the stores for these two brands (especially for the heterogeneous models), including stores with zero share (no upper boundary hits) as well. Across brands and the three dynamic models shown, 50% (75%) of the stores show upper boundary price hits in less than 10% (35%) of the weeks (not displayed in the figure). As it is further obvious, the upper price bound patterns differ more by brands than by models, which consistently applies for the other models not shown, too.

Our findings contradict the assumption that parametric models or models with linear price effects might be generally prone to boundary pricing effects. However, we consistently find more stores with higher shares of upper boundary price hits for the dynamic models compared to their static counterparts. As a rule, we also see a (much) greater bandwidth of stores with different shares of upper boundary price hits for heterogeneous models compared to their homogeneous counterparts across brands, as one might have expected. No such systematic can be derived for flexible versus parametric models.

In contrast to upper boundary price hits, lower boundary price hits as well as upper boundary sales hits were hardly observed. The share of lower bound price hits averaged across stores is not larger than 1% by both brand and type of model. The number of upper boundary sales hits never exceeds 5 times in a store across brands and models, corresponding to a maximum share of 6%. The detailed results on boundary effects by brand for all models can be obtained from the authors upon request.

Distributions of store-specific shares of optimized prices hitting the upper bound of the observed price range for the dynamic model variants DynParHet, DynFlexHom, and DynFlexHet

5 Conclusions and limitations