Abstract

We consider the class of Gaussian self-similar stochastic volatility models, and characterize the small-time (near-maturity) asymptotic behavior of the corresponding asset price density, the call and put pricing functions, and the implied volatility. Away from the money, we express the asymptotics explicitly using the volatility process’ self-similarity parameter H, and its Karhunen–Loève characteristics. Several model-free estimators for H result. At the money, a separate study is required: the asymptotics for small time depend instead on the integrated variance’s moments of orders \(\frac{1}{2}\) and \( \frac{3}{2}\), and the estimator for H sees an affine adjustment, while remaining model-free.

Similar content being viewed by others

References

Abramovitz, M., Stegun, I.A. (eds.): Handbook of Mathematical Functions. Applied Mathematics Series, vol. 55. National Bureau of Standards, Washington, DC (1972)

Alexanderian, A.: A Brief Note on the Karhunen-Loève Expansion. Technical Note. https://users.ices.utexas.edu/~alen/articles/KL.pdf (2015). Accessed 23 Apr 2018

Alòs, E., Léon, J., Vives, J.: On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Finance Stoch. 11, 571–589 (2007)

Armstrong, J., Forde, M., Lorig, M., Zhang, H.: Small-time asymptotics under local-stochastic volatility with a jump-to-default: curvature and the heat kernel expansion. arXiv:1312.2281 (2013)

Bardina, X., Es-Sebaiy, Kh: An extension of bifractional Brownian motion. Commun. Stoch. Anal. 5(2), 333–340 (2011)

Bayer, C., Friz, P., Gatheral, J.: Pricing under rough volatility. http://ssrn.com/abstract=2554754 (2015). Accessed 23 Apr 2018

Berestycki, H., Busca, J., Florent, I.: Computing the implied volatility in stochastic volatility models. Comm. Pure Appl. Math. 57, 1352–1373 (2004)

Bergomi, L.: Stochastic Volatility Modeling. Chapman & Hall/CRC Press, Boca Raton (2016)

Bojdecki, T., Gorostiza, L.G., Talarczyk, A.: Some extensions of fractional Brownian motion and sub-fractional Brownian motion related to particle systems. Electron. Commun. Probab. 12, 161–172 (2007)

Caravenna, F., Corbetta, J.: General smile asymptotics with bounded maturity. arXiv:1411.1624v1 (2014)

Chronopoulou, A., Viens, F.: Stochastic volatility models with long-memory in discrete and continuous time. Quant. Financ. 12, 635–649 (2012)

Comte, F., Renault, E.: Long memory in continuous-time stochastic volatility models. Math. Financ. 8, 291–323 (1998)

Comte, F., Coutin, L., Renault, E.: Affine fractional stochastic volatility models. Ann. Financ. 8, 337–378 (2012)

Corlay, S.: Quelques aspects de la quantification optimale, et applications en finance (in English, with French summary). PhD thesis, Université Pierre et Marie Curie (2011)

Corlay, S.: The Nyström method for functional quantization with an application to the fractional Brownian motion. hal-00515488, version 1 (2010)

Corlay, S.: Properties of the Ornstein-Uhlenbeck bridge. https://hal.archives-ouvertes.fr/hal-00875342v4 (2014). Accessed 23 Apr 2018

Corlay, S., Pagès, G.: Functional quantization-based stratified sampling methods. https://hal.archives-ouvertes.fr/hal-00464088v3 (2014). Accessed 23 Apr 2018

Daniluk, A., Muchorski, R.: The approximation of bonds and swaptions prices in a Black-Karasinski model based on the Karhunen-Loève expansion. In: 6th General AMaMeF and Banach Center Conference (2013)

Deheuvels, P., Martynov, G.: A Karhunen-Loève decomposition of a Gaussian process generated by independent pairs of exponential random variables. J. Funct. Anal. 255, 23263–2394 (2008)

Deuschel, J.-D., Friz, P.K., Jacquier, A., Violante, S.: Marginal density expansions for diffusions and stochastic volatility I: Theoretical foundations. Commun. Pure Appl. Math. 67, 40–82 (2014)

Deuschel, J.-D., Friz, P.K., Jacquier, A., Violante, S.: Marginal density expansions for diffusions and stochastic volatility I: Applications. Commun. Pure Appl. Math. 67, 321–350 (2014)

Embrechts, P., Maejima, M.: Selfsimilar Processes. Princeton University Press, Princeton (2002)

Feng, J., Forde, M., Fouque, J.-P.: Short-maturity asymptotics for a fast mean-reverting Heston stochastic volatility model. SIAM J. Financ. Math. 1, 126–141 (2010)

Feng, J., Fouque, J.P., Kumar, R.: Small-time asymptotics for fast mean-reverting stochastic volatility models. Ann. Appl. Probab. 22, 1541–1575 (2012)

Figueroa-López, J.E., Houdré, Ch.: Small-time expansions for the transition distributions of Lévy processes. Stoch. Process. Appl. 119, 3862–3889 (2009)

Figueroa-López, J.E., Forde, M.: The small-maturity smile for exponential Lévy models. SIAM J. Financ. Math. 3, 33–65 (2012)

Forde, M., Jacquier, A.: Small-time asymptotics for implied volatility under the Heston model. IJTAF 12, 861–876 (2009)

Forde, M., Jacquier, A.: Small-time asymptotics for an uncorrelated local-stochastic volatility model. Appl. Math. Financ. 18, 517–535 (2011)

Forde, M., Jacquier, A.: Small-time asymptotics for implied volatility under a general local-stochastic volatility model. Appl. Math. Financ. 18, 517–535 (2011)

Forde, M., Jacquier, A., Mijatović, A.: Asymptotic formulae for implied volatility in the Heston model. Proc. R. Soc. Lond. A 466, 3593–3620 (2010)

Forde, M., Jacquier, A., Lee, R.: The small-time smile and term structure of implied volatility under the Heston model. SIAM J. Financ. Math. 3, 690–708 (2012)

Forde, M., Zhang, H.: Asymptotics for rough stochastic volatility and Lévy models (2015)

Fouque, J.-P., Papanicolaou, G., Sircar, K.R.: Derivatives in Financial Markets with Stochastic Volatility. Cambridge University Press, New York (2000)

Fouque, J.-P., Papanicolaou, G., Sircar, K.R., Sølna, K.: Multiscale Stochastic Volatility for Equity, Interest Rate, and Credit Derivatives. Cambridge University Press, Cambridge (2011)

Fukasawa, M.: Asymptotic analysis for stochastic volatility: martingale expansion. Financ. Stoch. 15, 635–654 (2011)

Fukasawa, M.: Short-time at-the-money skew and fractional rough volatility. arXiv:1501.06980v1 (2015)

Gao, K., Lee, R.: Asymptotics of implied volatility to arbitrary order. Financ. Stoch. 18, 349–392 (2014)

Garnier, J., Sølna, K.: Correction to Black-Scholes formula due to fractional stochastic volatility. SIAM J. Financ. Math. 8, 560–588 (2017)

Garnier, J., Sølna, K.: Option pricing under fast-varying long-memory stochastic volaitlity. arXiv:1604.00105v2 (2017)

Gatheral, J. (joint work with C. Bayer, P. Friz, T. Jaisson, A. Lesniewski, and M. Rosenbaum): Rough Volatility, Slides, National School of Development. Peking University (2014)

Gatheral, J. (joint work with C. Bayer, P. Friz, T. Jaisson, A. Lesniewski, and M. Rosenbaum): Volatility is Rough, Part 2: Pricing, Slides, Workshop on Stochastic and Quantitative Finance. Imperial College London, London (2014)

Gatheral, J., Jaisson, T., Rosenbaum, M.: Volatility is Rough. arXiv:1410.3394 (2014)

Gatheral, J., Hsu, E., Laurence, P., Ouyang, C., Wang, T.-H.: Asymptotics of implied volatility in local volatility models. Math. Financ. 22, 591–620 (2012)

Guennon, H., Jacquier, A., Roome, P.: Asymptotic behavior of the fractional Heston model. arXiv:1411.7653 (2014)

Gulisashvili, A.: Analytically Tractable Stochastic Stock Price Models. Springer, Berlin (2012)

Gulisashvili, A., Horvath, B., Jacquier, A.: Mass at zero and small-strike implied volatility expansion in the SABR model. arXiv:1502.03254v1, http://ssrn.com/abstract=2563510 (2015). Accessed 23 Apr 2018

Gulisashvili, A., Stein, E.M.: Asymptotic behavior of the stock price distribution density and implied volatility in stochastic volatility models. Appl. Math. Optim. 61, 287–315 (2010)

Gulisashvili, A., Viens, F., Zhang, X.: Extreme-strike asymptotics for general Gaussian stochastic volatility models. arXiv:1502.05442v1 (2015)

Hagan, P.S., Kumar, D., Lesniewski, A., Woodward, D.E.: Managing smile risk. Wilmott Magazine (2003)

Hagan, P.S., Lesniewski, A., Woodward, D.: Probability distribution in the SABR model of stochastic volatility. In: Friz, P.K., Gatheral, J., Gulisashvili, A., Jacquier, A., Teichmann, J. (eds.) Large Deviations and Asymptotic Methods in Finance, pp. 1–36. Springer, Cham (2015)

Henry-Labordère, P.: Analysis, Geometry and Modeling in Finance: Advanced Methods in Option Pricing. Financial Mathematics Series. Chapman & Hall/CRC, Boca Raton (2008)

Houdré, C., Villa, J.: An example of infinite-dimensional quasi-helix. Contemp. Math. Am. Math. Soc. 336, 195–201 (2003)

Lee, R.: The moment formula for implied volatility at extreme strikes. Math. Financ. 14, 469–480 (2004)

Lewis, A.: Option Valuation Under Stochastic Volatility: With Mathematica Code. Finance Press, Newport Beach (2000)

Lewis, A.: Option Valuation Under Stochastic Volatility II: With Mathematica Code. Finance Press, Newport Beach (2016)

Lim, S.C.: Fractional Brownian motion and multifractional Brownian motion of Riemann-Liouville type. J. Phys. A 34, 1301 (2001)

Medvedev, A., Scaillet, O.: Approximation and calibration of short-term implied volatilities under jump-diffusion stochastic volatility. Rev. Financ. Stud. 20, 427–459 (2007)

Muhle-Karbe, J., Nutz, M.: Small-time asymptotics of option prices and first absolute moments. J. Appl. Probab. 48, 1003–1020 (2011)

Nourdin, I.: Selected Aspects of Fractional Brownian Motion. Springer, Milano (2012)

Nualart, D.: Fractional Brownian motion: stochastic calculus and applications. In: Proceedings of the International Congress of Mathematicians, Madrid, Spain, pp. 1541–1562. European Mathematical Society, Paris (2006)

Paulot, L.: Asymptotic implied volatility at the second order with application to the SABR model. In: Friz, P.K., Gatheral, J., Gulisashvili, A., Jacquier, A., Teichmann, J. (eds.) Large Deviations and Asymptotic Methods in Finance. Springer, Cham (2015)

Roper, M., Rutkowski, M.: On the relationship between the call price surface and the implied volatility surface close to expiry. Int. J. Theor. Appl. Financ. 12, 427–441 (2009)

Rostek, S.: Option Pricing in Fractional Brownian Markets. Springer, Berlin (2009)

Stein, E., Stein, J.: Stock price distributions with stochastic volatility: an analytic approach. Rev. Financ. Stud. 4, 727–752 (1991)

Tankov, P., Mijatović, A.: A new look at short-term implied volatility in asset price models with jumps. Mathematical Finance. arXiv:1207.0843 (2012)

Torres, S., Tudor, C.A., Viens, F.G.: Quadratic variations for the fractional-colored stochastic heat equation. Electron. J. Probab. 19, 1–51 (2014)

Tudor, C.A.: Analysis of Variations for Self-Similar Processes. Springer, Cham (2013)

Vilela Mendez, R., Olivejra, M.J., Rodriguez, A.M.: The fractional volatility model: no-arbitrage, leverage and completeness. arXiv:1205.2866v1 (2012)

Weisstein, E.W.: Inverse Erf. From MathWorld—A Wolfram Web Resource. http://mathworld.wolfram.com/InverseErf.html (2018). Accessed 23 Apr 2018

Yaglom, A.M.: Correlation Theory of Stationary and Related Random Functions, vol. 1. Springer, New York (1987)

Acknowledgements

The authors would like to thank the anonymous referees for their insightful comments and corrections.

Author information

Authors and Affiliations

Corresponding author

Appendix: Proofs of the Main Theorems

Appendix: Proofs of the Main Theorems

Proof of Theorem 3

Fix \(x> 0\), and denote

It is clear from (13) that the small-time asymptotic behavior of the density \(D_T(x)\) is determined by that of the integral \(J_x(T)\).

The next lemma will allow us to use Theorem 2 to estimate the integral in (47). \(\square \)

Lemma 2

Fix \(\alpha \in {\mathbb {R}}\), \(b> 0\), and \(\varepsilon > 0\). Let \(x> s_0+\varepsilon \), and suppose f is an integrable function on [0, b]. Then

as \(T\rightarrow 0\).

Proof

The lemma is trivial if \(\alpha \ge 0\). For \(\alpha < 0\), we have

The following equality holds for every \(A> 0\):

It follows that for \(2A>-\alpha b^2\), the function \( u\mapsto \frac{1}{u^{\alpha }}\exp \left\{ -\frac{A}{u^2}\right\} \) is increasing on the interval (0, b]. Set \(A=\frac{\log ^2\frac{x}{s_0}}{2T^{2H+1}}\). Next, using (48), we obtain

provided that \(\log ^2\frac{x}{s_0}> b^2T^{2H+1}\). It is clear that the previous inequality holds for small enough values of T provided that \(x> s_0+\varepsilon \).

Finally, Lemma 2 follows from (49).

Using (10) with \(t=1\) and formula (8) for centered processes, we obtain

as \(y\rightarrow \infty \), where

Let \(y_0> 0\) be a constant such that the big-O estimate in (50) is valid. Our next goal is to replace the function \({\widetilde{p}}_1\) in (47) by its approximation from (50), using Lemma 2. The resulting formula is

as \(T\rightarrow 0\). Formula (52) can be obtained as follows. Applying Lemma 2 with \(\alpha =-1\), \(b=y_0\), and \(f={\widetilde{p}}_1\), to the integral with same integrand as in (47), we can include this integral in the error term in (52). Next, we can replace the function \({\widetilde{p}}_1\) in the integral over \([y_0,\infty )\) by the expression on the right-hand side of (50). Finally, we observe that

as \(T\rightarrow 0\). Indeed, formula (53) can be established by applying Lemma 2 to the expression on the left-hand side of (53) twice, first with \(\alpha =n_1(1)-2\), \(b=y_0\), and \(f(u)=\exp \{-\frac{u^2}{2\lambda _1(1)}\}\), and then with \(\alpha =n_1(1)-3\), \(b=y_0\), and \(f(u)=\exp \{-\frac{u^2}{2\lambda _1(1)}\}\). This proves formula (52). \(\square \)

To study the asymptotics of the function \(T\mapsto J_{x}(T)\) defined by (52), we consider the following two integrals:

and

Set

Note that \(\beta _{T}\) depends on x, while \(\gamma _{T}\) does not. Then we have

and

Next, making a substitution

we transform the previous integrals as follows:

and

Let us denote

Then we have \( \sqrt{\beta _{T}\gamma _{T}}=z(T)\log \frac{x}{s_{0}}. \) Therefore,

and

It follows from (54) that \(z(T)\rightarrow \infty \) as \(T\rightarrow 0 \). Our next goal is to apply Laplace’s method to study the asymptotic behavior of the functions \(T\mapsto {\widetilde{J}}_x(T)\) and \(T\mapsto \widehat{ J}_x(T)\) as \(T\rightarrow 0\). Note that the unique critical point of the function \(\psi (v)=v^{-2}+v^2\) is at \(v=1\). Moreover, we have \( \psi ^{\prime \prime }(1)=8> 0\).

We will first reduce the integrals in (55) and (56) to the integrals over the interval [0, 2] and give an error estimate. The next assertion will be helpful.

Lemma 3

Suppose \(a\in {\mathbb {R}}\) and \(0<\varepsilon < s_0\). Then

as \(t\rightarrow 0\).

Proof

Fix a small number \(r> 0\). Then for \(0< T< T_0\), we have

The proof of Lemma 3 is thus completed. \(\square \)

Now, we are ready to apply Laplace’s method to the integrals in (55) and (56). The dependence of the parameter x in (55) and (56) is very simple. This allows us to obtain uniform error estimates. By taking into account Lemma 3, we see that for every \( \varepsilon >0\) and all \(x>s_{0}+\varepsilon \),

and

as \(T\rightarrow 0\). Recall that the \(O_{\varepsilon }\) estimates in (57) and (58) are uniform with respect to \(x>s_{0}+\varepsilon \). Since

as \(T\rightarrow 0\), formulas (57) and (58) imply that

as \(T\rightarrow 0\). Since for \(T<1\),

we have

as \(T\rightarrow 0\), and therefore,

as \(T\rightarrow 0\). Moreover, for all \(T<1\) and \(x>s_{0}+\varepsilon \),

and hence

as \(T\rightarrow 0\). Finally,

as \(T\rightarrow 0\).

Recall that we assumed \(r=0\). It follows from (13) and (47) that

as \(T\rightarrow 0\).

Our next goal is to remove the last \(O_{\varepsilon }\)-term from formula (60). Analyzing the expressions in (60), we see that in order to prove the statement formulated above, it suffices to show that there exists a constant \(c>0\) independent of \(T<T_{0}\) and \(x>s_{0}+\varepsilon \) and such that

The previous inequality is equivalent to the following:

Using (54), we see that the inequality in (62) follows from the inequality

To prove the inequality in (63), we observe that for every small enough number \(\tau >0\) there exists a constant \(c_{\tau ,\varepsilon }\) such that

for all \(x>s_{0}+\varepsilon \). Moreover, there exists \(T_{\tau ,\varepsilon }>0\) such that

for all \(T<T_{\tau ,\varepsilon }\). Now, it is clear that (63) follows from the estimate

for all \(T<T_{\tau }\). It is not hard to see that there exist numbers \(\tau \) and \(T_{\tau }\), for which the inequality in (64) holds. This establishes (61), and it follows that

as \(T\rightarrow 0\), where \({\widetilde{A}}\) is given by (51). Formula (65) will help us to characterize the asymptotic behavior of the function \(T\mapsto D_{T}(x)\).

Let us assume that \(x> s_0+\varepsilon \). Then we have

where \(h=\frac{\lambda _1(1)T^{2H+1}}{4}\). Therefore,

as \(T\rightarrow 0\). Moreover,

and

as \(T\rightarrow 0\). Next, combining (51), (65), (66), (67), and (68), and simplifying the resulting expressions, we obtain formula (14).

This completes the proof of Theorem 3.

Proof of Theorem 4

Let us consider the call pricing function \(T\mapsto C(T)\) with \(K> s_0 \). It is known that

Therefore, we can use the uniform estimate in formula (14) to characterize the small-time behavior of the call pricing function. Let us consider the following integrals:

and

where we use the notation in (54) for the sake of shortness.

We will next make a substitution \(u=(2z(T)-\frac{1}{2})\log \frac{x}{s_0}\) in the integral on the second line in (70). The resulting expression is as follows:

which is equal to

where the symbol \(\Gamma \) stands for the upper incomplete gamma function defined by

Making similar transformations in the other integrals in (70) and (71), we finally obtain

and

It is known that

as \(x\rightarrow \infty \). Formula (72) can be easily derived from the recurrence relation

for the upper incomplete gamma function. It follows that

as \(T\rightarrow 0\). Therefore,

as \(T\rightarrow 0\). Similarly,

as \(T\rightarrow 0\). It is not hard to see that

It follows from (73) and (74) that

as \(T\rightarrow 0\). Similarly,

as \(T\rightarrow 0\). Using (14), (69), (70) and (71), we see that

as \(T\rightarrow 0\). Next, (75) and (76), imply

as \(T\rightarrow 0\). We also have

as \(T\rightarrow 0\). Therefore,

as \(T\rightarrow 0\). Using (78), we obtain

as \(T\rightarrow 0\).

Now, it is clear that Theorem 4 follows from (77) and (79). \(\square \)

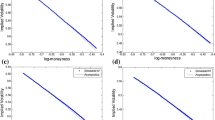

From top to bottom and left to right: IV with \(\sigma =2\), \(t\in [\)1 day, 2 weeks], \(H=0.25,\) 0.35, 0.40, 0.45, 0.49, 0.51, 0.55, 0.60, 0.75, 0.85.

Rights and permissions

About this article

Cite this article

Gulisashvili, A., Viens, F. & Zhang, X. Small-Time Asymptotics for Gaussian Self-Similar Stochastic Volatility Models. Appl Math Optim 82, 183–223 (2020). https://doi.org/10.1007/s00245-018-9497-6

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00245-018-9497-6

Keywords

- Stochastic volatility models

- Gaussian self-similar volatility

- Implied volatility

- Small-time asymptotics

- Karhunen–Loève expansions