Abstract

This research contributes to the literature on the effects of fiscal and monetary policy by exploiting non-Gaussianity of the time series for the identification of a Bayesian structural vector autoregression model. Using quarterly US data from 1954:IV to 2006:IV and from 1985:I to 2020:III, we formally assess the plausibility of theoretically predicted signs to label fiscal policy, monetary policy, and business cycle shocks. The impulse responses of consumption to the fiscal policy shock depend to some extent on the sample period, but the implied fiscal multiplier is always less than unity. On investment, there is a lagging crowding-out effect with a high probability, but it is not strongly evident in the latter sample. As for the responses after a contractionary monetary policy shock, we find a weakening output after some lags consistent with the leading monetary policy literature. The business cycle shock turns out to matter for government spending only in the long run, while it is already important for the federal funds rate in the short run.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

One of the most important tasks in the study of macroeconomics is identifying reliable exogenous variation in macroeconomic policy, that is, fiscal and monetary policy. Such exogenous variations are usually labeled as shocks. Once the shocks are identified and labeled correctly, we are then able to assess the effects on the economy. One widely used method to extract the shocks is the structural vector autoregression (SVAR) model.

While the fiscal policy-specific or monetary policy-specific SVAR model has been exploited extensively, not much literature analyzes both policies simultaneously. The importance of jointly identifying fiscal and monetary policy shocks using the SVAR model is stressed, for instance, in Rossi and Zubairy (2011). One issue that they raise when both are not considered simultaneously is that it may lead to an incorrect diagnosis of sources of economic fluctuations.

The existing SVAR literature relies on the restriction on structural parameters or direct restriction on the impulse responses to attain identification of either a fiscal or a monetary policy shock. Nevertheless, the inherited characteristics of fiscal variables have raised difficulties in identifying a fiscal policy shock within the SVAR framework. One would argue that a fiscal policy shock has been anticipated due to the legislative process when deciding the government budget. In other words, there are some lags from the budget announcement to its implementation that possibly make economic agents adapt their behavior in between. Some literature then suggests the use of forward-looking fiscal variables, such as news of military spending (Ramey 2016) or variables from financial markets like taxable government bonds futures (Leeper et al. 2013). Nonetheless, whether anticipated or unanticipated, both shocks qualitatively yield the same effects, except for their magnitudes (Mertens and Ravn 2010). On the other hand, there is not much debate in monetary policy literature that then comes to an understanding of a monetary policy shock as a surprise in interest rates.

Complementing the growing SVAR literature that studies the effects of fiscal and monetary policy, this paper takes advantage of the statistical properties of the macroeconomic time series data. Its main contribution lies in the application of the non-Gaussian SVAR model as in Lanne and Luoto (2020). By exploiting non-Gaussianity, we statistically examine the signs of the impact predicted by given theories. Different from conventional sign restrictions in the SVAR literature, we do not impose any restrictions either on the structural parameters or on the impulse responses. We only use the signs to label the shocks identified by non-Gaussianity. To the best of our knowledge, this kind of statistical identification has not been used in the existing literature on the joint analysis of fiscal and monetary policy.Footnote 1 Our approach also facilitates the assessment of sign restrictions used in the previous literature (see, for instance, Mountford and Uhlig 2009). In addition, we are able to test short-run restrictions, such as those imposed by Rossi and Zubairy (2011).

We consider quarterly US data from 1954:IV to 2006:IV with the same definitions of variables as in Rossi and Zubairy (2011). In addition, we also report results based on data from 1985:I to 2020:III. Due to non-Gaussianity, all structural shocks are identified, and we label three of them as the fiscal policy, monetary policy, and business cycle shocks. To this end, we find the shocks that are the likeliest to satisfy the theoretically implied sign constraints. For instance, the Real Business Cycle (RBC) model of Baxter and King (1993) predicts falling consumption following a positive government spending shock. We find evidence in favor of one of the identified shocks having this property, which facilitates labeling this shock as the fiscal policy shock.

In response to a positive fiscal policy shock, we also find instant falls in real wages and lagging falls in investment, which translate into weakening output after some lags. Hence, our results are in line with the argument of the crowding-out investment effect. However, with the data set from 1985:I to 2020:III, the crowding-out investment effect no longer holds. Instead, a crowding-in effect is found. As for the responses after a monetary policy shock, we find a weakening output after some lags, consistent with the leading monetary policy literature. Another subtlety from our results is that we find the business cycle shock to contribute to the variation in government spending only in the long run, while it contributes to the federal funds rate substantially in the short run.

The rest of this paper is structured as follows. In Sect. 2, the model and the assumptions required for identification are described. In addition, the data as well as the sign constraints needed for labeling the shocks are discussed. Section 3 contains the empirical results. Finally, Sect. 4 concludes.

2 Model

2.1 Model specification

We consider the SVAR(p) model

where \(\pmb {z}_t\) (\(n \times 1\)) is a vector of time series, \(\pmb {c}\) is an intercept, \(\pmb {A}_i\) (\(n \times n\)) are autoregressive coefficient matrices, and the non-singular matrix \(\pmb {B}\) (\(n \times n\)) comprises the contemporaneous structural relations of the errors \(\pmb {\varepsilon }_t\). The error process \(\pmb {\varepsilon }_t\) is assumed to be a sequence of independently and identically distributed random vectors. As Lanne et al. (2017) have shown, the matrix \(\pmb {B}\) is identified up to signs and permutation of its columns when the components of \(\pmb {\varepsilon }_t\) are mutually independent and at most one of them has a Gaussian marginal distribution. The mutual independence and the non-Gaussianity of \(\pmb {\varepsilon }_t\) are the necessary and sufficient conditions to achieve a global identification.Footnote 2 Instead of assuming a t distribution for each independent component of the error vector \(\pmb {\varepsilon }_t\) as in much of the previous literature, we assume that \(\pmb {\varepsilon }_{it}, i=1,\ldots ,n\) follows a skewed generalized t distribution that was also entertained in Anttonen et al. (2021).

The skewed generalized t distribution is known for its flexibility. Five parameters \(\{\mu , \sigma , \lambda , \rho , q\}\) influence the moments of the distribution (Davis 2015). While \(\mu \) is the mean, \(\sigma \) and \(\lambda \) control the variance and skewness, respectively, and \(\rho \) and q together determine the kurtosis. We assume that each component of \(\pmb {\varepsilon }_t\) has zero mean and unit scale \(\sigma _i\), adopted from Davis (2015) and Anttonen et al. (2021), and hence the skewed generalized t distribution of the ith structural shock \(\pmb {\varepsilon }_{it}, i=1,\ldots ,n\) has the following probability density function:

where \(B(\cdot )\) is the beta function and

to get the zero mean errors. Furthermore, the parameter \(v_i\) is set to 1 to have \(b_i=1\). In this case, the variance needs not to exist, and its existence can be evaluated based on the tail behavior of each \(\pmb {\varepsilon }_{it}\), which is encapsulated by \(\alpha _i = \rho _i q_i\) where \(\alpha _i\) is the tail exponent of the errors. As Davis (2015) points out, the hth moment exists only if \(\rho _i q_i > h\). Hence, the probability that the variance exists is given by \(Pr[\alpha _i > 2]\). Finally, we impose the following restrictions: \(\sigma > 0\), \(-1<\lambda <1\), \(\rho >0\), and \(q>0\).

Our main motivation for entertaining the skewed generalized t distribution is the empirical findings on the statistical properties of some macroeconomic time series. Fagiolo et al. (2008), for example, find that the distributions of output growth rates in the USA and many other OECD countries feature exponential power densities with tails much fatter than those of a Gaussian distribution. Similarly, Franke (2015) also finds evidence of a fat-tailed distribution of the US output growth, particularly during the Great Moderation period (1984:I–2007:II). The exponential power distribution in those papers is just a special case of the skewed generalized t distribution when \(\lambda =0\) and \(q \rightarrow \infty \). The skewed generalized t distribution also encompasses other families of distribution, such as the t distribution when \(\lambda =0\) and \(\rho =2\) or the normal distribution when \(\lambda =0\), \(\rho =2\), and \(q \rightarrow \infty \). Hence, the skewed generalized t distribution is more general compared to the t distribution entertained in Lanne and Luoto (2020), among others in the previous literature. With its flexibility, the skewed generalized t distribution facilitates exploiting the information contained in the higher moments for identification, for instance the third moments of errors.

To see the connections between the skewed generalized t distribution and the more commonly used Gaussian distribution as well as the t distribution, consider the five parameters \(\{\mu , \sigma , \lambda , \rho , q\}\) mentioned previously. The tail exponent \(\rho q\) in the skewed generalized t distribution is akin to the degree-of-freedom parameter of the t distribution. When a random variable, for instance, has properties of \(\lambda =0\) and \(\rho =2\), meaning that it follows a t distribution, the tail exponent is just equivalent to the degree-of-freedom parameter of the t distribution. It follows that the t distributed random variable becomes Gaussian when the degree-of-freedom parameter goes to infinity, or in this case \(q \rightarrow \infty \).

Another motivation for entertaining the skewed generalized t distribution is the inspection of the data series, where we find that most of them deviate from the normal distribution.Footnote 3 We do not assume any specific law of motion for the variances, such as with the log-variances following an AR(1) process (Clark and Ravazzolo 2015) or regime-switching error variances (Lütkepohl and Woźniak 2020; Brunnermeier et al. 2021) as this literature typically relies on the normality assumption, whereas with our approach, we intend to exploit the non-normality with weaker assumptions.Footnote 4

Finally, due to the large number of parameters in the SVAR(p) model, we use Bayesian methods. We defer the discussion on the Bayesian estimation as well as prior set-up in detail to Appendix A.

2.2 Labeling the shocks

After estimating the posterior distribution of the parameters, we next make inference regarding the structural shocks based on the posterior distribution of the parameters. If the process \({\textbf {z}}_t\) in (1) satisfies the stability condition, i.e.,

the SVAR(p) model has a moving average representation

where \(\pmb {\mu }\) is the unconditional expectation of \({\textbf {z}}_t\), while \(\pmb {\Psi }{_0}=\pmb {I}_n\) and \(\pmb {\Psi }{_j}(j=1, \ldots ,p)=\sum _{l=1}^{j}\pmb {\Psi }_{j-l} \pmb {A}_l\) which is obtained recursively. The impulse responses of the ith structural shock \(\pmb {\varepsilon }_{it}, i=1,\ldots ,n\) are embedded in the ith column of matrices \(\pmb {\Psi }{_j} {\textbf {B}} \equiv \pmb {\Theta }_j, j=0,1,\ldots \). We then assess \(\pmb {\Theta }_j\) in order to find the shocks of our interest. Because the \(\pmb {\Theta }_j\) are identified only up to permutation of their columns, to find these shocks, we have to locate the columns of \(\pmb {\Theta }_j\) that are the likeliest to satisfy the given sign constraints. To that end, we use Bayes factors, as discussed below.

We have n! permutations of the columns of \(\pmb {\Theta }_j\), on which some restrictions can be placed. Following Lanne and Luoto (2020), we first fix the permutation and then compute the posterior probability of each permutation that reflects each combination of the shocks in a particular order that satisfies the sign constraints. In practice, we draw from the posterior distribution of the parameters and count the share of the draws that satisfy the sign restrictions. We then calculate the Bayes factor of the restricted model against the unrestricted model and pick the model(s) based on the Bayes factor.

To facilitate comparison with Rossi and Zubairy (2011), we consider the same SVAR(p) model estimated on similar quarterly data from 1954:IV to 2006:IV. Hence, we have eight variables in the SVAR(p) model in (1): government spending (\(g_t\)), GDP (\(y_t\)), hours worked in non-farm business sector (\(h_t\)), non-durable and services consumption (\(c_t\)), gross private investment and durable consumption (\(i_t\)), real wages in non-farm business sector (\(w_t\)), GDP deflator inflation (\(p_t\)), and the federal funds rate (\(r_t\)). Other than \(r_t\) and \(p_t\), all variables are in log levels and real terms deflated by the GDP deflator, and \(g_t\), \(y_t\), \(h_t\), ,\(c_t\) and \(i_t\) are expressed in per-capita terms. The definitions of all variables follow Rossi and Zubairy (2011), and Appendix B describes the variables and their construction in greater detail. We concentrate on the same data period as Rossi and Zubairy (2011) to facilitate comparison with their results. Besides, US monetary policy is likely to follow a different regime after the global financial crisis of 2008 (the regime of unconventional monetary policy), and our linear SVAR model is not designed to capture multiple regimes.

Although the SVAR(p) model has eight variables, we focus on only three shocks, i.e., the fiscal policy, the monetary policy, and the business cycle shocks. To label the statistically identified shocks, we need additional information. To that end, we rely on the sign restrictions of Mountford and Uhlig (2009). Unlike them, however, we do not impose any sign restrictions on the impulse responses. The sign constraints in Table 1 are only used in labeling the shocks identified by non-Gaussianity. In other words, after estimating the unrestricted model, the shocks that are the likeliest to satisfy the sign constraints are labeled accordingly.

In addition to the signs as in Mountford and Uhlig (2009), we add one more sign constraint, according to which a positive fiscal policy shock hurts consumption (\(c_t\)), following the prediction of the RBC model (Baxter and King 1993). Note that we do not impose these sign constraints as in the traditional sign restriction literature. Instead, we only consider the unrestricted model and find the shocks that are the likeliest to satisfy the constraints, and label them accordingly. Under the RBC framework where Ricardian equivalence holds, we expect future taxes to compensate for current deficit spending. Due to expectations of higher taxes, economic agents then lower their current consumption.

Table 1 presents all the sign constraints. A plus sign (\(+\)) indicates an increase, while a minus sign (−) indicates a decrease in the variable in question in the following four quarters. For instance, a plus sign (\(+\)) of a fiscal policy shock on \(g_t\) indicates that we expect an increase in government spending for four quarters after a positive fiscal shock. Likewise, a minus sign (−) of a monetary policy shock on \(p_t\), for example, indicates that we expect a decrease in the price for four quarters after a positive monetary policy shock or a monetary policy tightening.

Following a monetary policy shock, we expect to see a rise in interest rates (\(r_t\)) and a fall in price (\(p_t\)). In addition, Mountford and Uhlig (2009) restrict a positive monetary policy shock to lower adjusted reserves, but this variable is not included in our model. The two constraints that we have here are consistent with the leading literature on monetary policy, such as Faust (1998) and Uhlig (2005), or more recently (Antolín-Díaz and Rubio-Ramírez 2018; Arias et al. 2019). We are in a position to verify whether the data support these constraints.

Another shock that we intend to label is the business cycle shock, which Mountford and Uhlig (2009) define as a shock that jointly moves the GDP (\(y_t\)), consumption (\(c_t\)), investment (\(i_t\)), and government revenue up for four quarters ahead. Since government revenue is not included in our model, we only consider the first three constraints to label a positive business cycle shock.

Finally, the fiscal policy shock is signified by a rise in government spending (\(g_t\)) for four quarters as also entertained in Mountford and Uhlig (2009). As they point out, the lengthy impact period is to rule out transitory shocks to fiscal variables. In our experience, distinguishing between a fiscal policy shock and a business cycle shock is problematic, with only one restriction on government spending (\(g_t\)) in labeling the fiscal policy shock because a business cycle shock is also likely to be followed by an increase in government spending (\(g_t\)). Hence, we propose one additional constraint to label a shock as a fiscal policy shock that has not been imposed by Mountford and Uhlig (2009). Specifically, we constrain a positive fiscal policy shock to hurt consumption (\(c_t\)). The negative response of consumption (\(c_t\)) to a positive fiscal policy shock accords with the RBC model where Ricardian equivalence holds. Under this condition, taxes in the future are inevitable to finance the current deficit spending. Due to expectations of higher taxes in the future, economic agents then lower current consumption (see, e.g., Baxter and King 1993; Ramey and Shapiro 1998). Unlike this view, the IS-LM model predicts consumption to rise after a positive fiscal policy shock as consumers behave based on their current disposable income instead of their lifetime resources as in the RBC model (see, e.g., Galí et al. 2007; Linnemann 2006; Perotti 2007). As with the monetary policy shock previously, we are in a position to verify whether the data support these constraints.

We aim to find the three shocks that are the likeliest to satisfy the inequality constraints in Table 1. As we have eight variables, we have eight statistically identified shocks, \(\varepsilon _1, \varepsilon _2,\ldots , \varepsilon _8\), and we intend to label three of them as the fiscal policy shock (\(\varepsilon _{fp}\)), the monetary policy shock (\(\varepsilon _{mp}\)), and the business cycle shock (\(\varepsilon _{bc}\)). We follow the procedure in Lanne and Luoto (2020)Footnote 5 of labeling multiple structural shocks, where after estimating the SVAR model with statistically identified shocks, we compute the Bayes factor based on the probabilities of the shocks satisfying the inequality constraints. Specifically, we impose the sign constraints in Table 1 on three shocks at a time and compute the posterior probability of the constrained SVAR model.

Then, we compute the Bayes factors of the constrained models, i.e., models whose shocks satisfy the inequality constraints, against the unconstrained model (the model without any inequality constraints). Following Kass and Raftery (1995), we deem the evidence in favor of one model against the other to be substantial if the Bayes factor is between 3.2 and 10, and strong if it is between 10 and 100. It may be that the Bayes factor lends substantial or even strong support to more than one model. In that case, we proceed by picking the likeliest model of interest, i.e., the one with the highest posterior probability of satisfying the inequality constraints, and compute the Bayes factors of that model against the other models supported by the data. If there is at least substantial evidence in favor of the likeliest model against the others, we can label the three shocks accordingly.

However, the likeliest model may not always dominate all other models. In this case, we proceed by analyzing the impulse responses and the forecast error variance decomposition as suggested by Lanne and Luoto (2020). First, after a fiscal policy shock, we expect positive median impulse responses in government spending (\(g_t\)) for at least the first four quarters and negative median impulse responses in consumption (\(c_t\)) within the same horizons. Second, after a monetary policy shock, we expect positive median impulse responses in the federal funds rate (\(r_t\)) for at least the first four quarters, and negative median impulse responses in the price (\(p_t\)) within the same horizons. Third, we expect positive median impulse responses in real GDP (\(y_t\)), consumption (\(c_t\)), and investment (\(i_t\)) for at least the first four quarters after a business cycle shock.

In analyzing the forecast error variance decomposition, the highest contributions to the forecast error variance of government spending and the federal funds rate should come from the fiscal and monetary policy shocks, respectively. Finally, we expect that the business cycle shock has the highest contribution to the forecast error variance of real GDP, consumption, and investment. We have no prior beliefs regarding whether the business cycle shock should have the highest contribution to real GDP, consumption, or investment. In this regard, we will compare our outcomes to those of Forni and Gambetti (2021) and King et al. (1991). Having studied the US economy with sample period 1959:I to 2007:IV, Forni and Gambetti (2021) define a shock that increases real GDP, consumption, and investment as a supply shock, and find that this shock explains about 46% of the forecast error variance of GDP growth while being more prominent for consumption than for investment. Similarly, such a shock explains around 35–44% of the forecast error variance of output in King et al. (1991).

3 Results and discussion

We sample two chains (\(N = 2\)) from the posterior distribution of the parameters, where each chain is composed of 500 000 draws. Every draw contains ten inner iterations (\(K = 10\)), and we discard 450 000 draws out of the 500 000. Convergence of the chains is evaluated based on the \(\hat{R}\) convergence statistic of Gelman et al. (2013) where the threshold for \(\hat{R}\) is set at 1.1. It then shows that the chains have converged for every parameter.

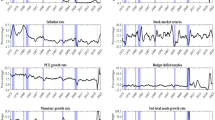

To guarantee identification, we need sufficient non-Gaussianity in the structural errors, i.e., at least \(n-1\) of them must be non-Gaussian. To evaluate this, we plot the marginal posterior distributions of the tail exponent \(\alpha _i = \rho _i q_i\) for all the statistically identified structural shocks. The tail exponent \(\rho _i q_i\) in the skewed generalized t distribution is akin to the degree-of-freedom parameter of the t distribution. Lower values imply fatter tails, while higher values imply thinner tails. For a Gaussian shock, for example, \(\rho _i=2\), \(q_i \rightarrow \infty \), hence \(\alpha _i \rightarrow \infty \). Figure 8 shows that there is sufficient non-Gaussianity as the mass tends to concentrate on relatively small values (see Appendix C.3). In addition, it also shows that the variance of each shock exists with high probability.

3.1 Assessment of the sign constraints

In the first stage, we compute the Bayes factors of the constrained models, i.e., models in which the shocks satisfy the signs constraints in Table 1, against the unconstrained model, that is, the model without any sign constraints. The results show that the data support the sign constraints specified in Table 1. However, there are many models that satisfy the sign constraints with substantial evidence (Bayes factors greater than > 3.2). In other words, multiple combinations of shocks are likely to satisfy the given sign constraints.

We next proceed by picking the likeliest model of interest, or the one with the highest posterior probability of satisfying the sign constraints. We then compute the Bayes factors of the likeliest model against the other models. Here, we find substantial evidence (Bayes factor > 3.2) in favor of the likeliest model against all others, except the three models listed in Table 2 in addition to the likeliest model. The table contains the posterior probabilities of the three shocks given in the leftmost column satisfying the sign constraints of the fiscal, monetary policy, and business cycle shocks, respectively. The likeliest combination is given in the first row, and the Bayes factors of the other combinations against it are given in the rightmost column.

Based on the results in Table 2, there are multiple candidates for the fiscal policy, the monetary policy, and the business cycle shocks. The model with the highest posterior probability of 0.39, for instance, suggests \(\varepsilon _{6}\) as the fiscal shock, \(\varepsilon _{8}\) as the monetary policy shock, and \(\varepsilon _{5}\) as the business cycle shock. On the other hand, \(\varepsilon _{3}\) and \(\varepsilon _{4}\) are also likely candidates for the fiscal policy shock. Meanwhile, \(\varepsilon _{5}\) is also a likely candidate for the monetary policy shock, and also \(\varepsilon _{8}\) is the business cycle shock with high probability. Due to the lack of substantial evidence in favor of any of the three models in Table 2 against the likeliest model, we proceed by analyzing the impulse responses together with forecast error variance decomposition.

In analyzing the impulse responses, we concentrate on \(\varepsilon _{3}, \varepsilon _{4}, \varepsilon _{5}, \varepsilon _{6}\), and \(\varepsilon _{8}\) since these are the candidates based on the results in Table 2. We have three candidates for the fiscal policy shock, i.e., \(\varepsilon _{3}\), \(\varepsilon _{4}\), and \(\varepsilon _{6}\). As we have already mentioned in the previous section, we expect positive median impulse responses of \(g_t\) for at least the first four quarters and negative median impulse responses of \(c_t\) within the same horizons. The median impulse responses to these shocks are depicted in Fig. 1. Our strong candidate is \(\varepsilon _{6}\) due to its negative median impulse responses of \(c_t\) across all horizons.

Median impulse responses to selected shocks (in order from top row: \(\varepsilon _{3}, \varepsilon _{4}, \varepsilon _{5}, \varepsilon _{6}, \varepsilon _{8}\)). The shaded area is the 68% region of the highest posterior density

Both \(\varepsilon _{5}\) and \(\varepsilon _{8}\) are candidates for the monetary policy and the business cycle shocks as the median impulse responses of \(p_t\) to these shocks are negative for at least the first four quarters, and the median impulse responses of \(r_t\) are positive. Referring to Fig. 1, the difference between the two shocks is the median impulse responses of the real GDP (\(y_t\)) that are positive to \(\varepsilon _{5}\), which become negative after four quarters following \(\varepsilon _{8}\). Hence, \(\varepsilon _{5}\) and \(\varepsilon _{8}\) are strong candidates for the business cycle and the monetary policy shocks, respectively. On the other hand, \(\varepsilon _{3}\), \(\varepsilon _{4}\), and \(\varepsilon _{6}\) are not good candidates for the business cycle and monetary policy shocks, as the median impulse responses of some variables are not as expected. The median impulse responses of \(r_t\) in the first quarter are zero in response to \(\varepsilon _{3}\) and \(\varepsilon _{4}\), whereas we expect positive responses after a monetary policy shock. Likewise, the median impulse responses of \(c_t\) are negative in response to \(\varepsilon _{6}\), whereas we expect positive responses after a business cycle shock.

Finally, we analyze the forecast error variance decomposition, where we rely on the contributions of the shocks for the first four quarters. As with analyzing the impulse responses, we concentrate on the relative contributions of \(\varepsilon _{3}, \varepsilon _{4}, \varepsilon _{5}, \varepsilon _{6}\), and \(\varepsilon _{8}\). Referring to Table 3, the highest contribution to the forecast error variance of government spending (\(g_t\)) comes from \(\varepsilon _{6}\) and is markedly larger than the contributions from \(\varepsilon _{3}\) or \(\varepsilon _{4}\). Therefore, together with the impulse responses, the results allow us to label \(\varepsilon _{6}\), instead of \(\varepsilon _{3}\) or \(\varepsilon _{4}\), as the fiscal policy shock (\(\varepsilon _{fp}\)).

Next, from the forecast error variance decomposition of federal funds rate (\(r_t\)), \(\varepsilon _{8}\) provides the largest contribution, while it contributes very little to real GDP (\(y_t\)), consumption (\(c_t\)), and investment (\(i_t\)). In contrast to \(\varepsilon _{8}\), \(\varepsilon _{5}\) has a substantially larger contribution to real GDP, consumption, and investment. More specifically, \(\varepsilon _{5}\) explains around 36–38% of the forecast error variance in real GDP (\(y_t\)) which is comparable to King et al. (1991) and Forni and Gambetti (2021). Thus, based on the findings, together with the impulse responses, we label \(\varepsilon _{8}\) as the monetary policy shock (\(\varepsilon _{mp}\)) and \(\varepsilon _{5}\) as the business cycle shock (\(\varepsilon _{bc}\)).Footnote 6

In the following subsections, we analyze the impacts of the three labeled shocks on the economy. The medians of the impulse responses are depicted together with the 68% regions of highest posterior density. Figure 2 plots the impulse responses to the fiscal policy shock, and the impulse responses to the monetary policy and the business cycle shocks are displayed in Figs. 3 and 5, respectively.

3.2 Impact of a fiscal policy shock

The impulse responses to the fiscal policy shock and the 68% region of highest posterior density are depicted in Fig. 2. The median value of our fiscal policy shock refers to an expansion in government spending by about 0.8%. Output rises instantaneously just below 0.2% following the fiscal expansion or the positive fiscal policy shock. After four quarters, the effects are zero (with high probability) as the 68% quantiles of the pointwise posterior densities cover both positive and negative areas, in line with Mountford and Uhlig (2009). A positive shock to government spending stimulates output, but the effect lasts for longer than four quarters, as Rossi and Zubairy (2011) found. Although the median impulse responses of consumption lie below zero at all horizons considered, we find that the overall effect of a fiscal expansion on consumption is zero (with high probability) as reflected by the 68% regions of the highest posterior density. This result is similar to Mountford and Uhlig (2009), but different from Rossi and Zubairy (2011), who find that consumption increases significantly after a positive government spending shock. Our wide responses of consumption, responses that cover both positive and negative areas, to a positive fiscal policy shock are also in line with Burnside et al. (2004), who find that a positive government spending shock does not affect private consumption significantly. We check these results further with another data set, i.e., using a sample from 1985:I to 2020:III where we exclude the periods before and during the Volcker episode and include the global financial crisis (GFC) episode of 2008 as well as the subsequent episode of zero interest rates.Footnote 7 The results of falling consumption after a fiscal spending expansion seem more persistent (see Fig. 9 in Appendix D).

Impulse responses to fiscal policy shock (\(\varepsilon _{fp}\)). The black lines depict the median responses and the shaded areas are the 68% regions of the highest posterior density

As for investment, either a rise or a fall is possible depending on the persistence of the increase in government spending (Ramey 2016). It also depends on whether the catalyst effect or the higher interest rate effect dominates. If the catalyst effect dominates, investment rises, and if the latter dominates, investment falls. On the other hand, Galí et al. (2007) find that the effects are either negative or insignificant. The negative effects surface due to a higher interest rate, but if the central bank holds the interest rate steady instead, then the impact on investment is neutral.

In our results, we find that a fiscal expansion crowds out investment through higher interest rates, but the responses are negative only between 4 and 24 quarters. Hence, to some degree, our results are in line with Galí et al. (2007). However, in Blanchard and Perotti (2002) for instance, the negative responses of investment occur immediately and persistently with the peak effect between 8 and 12 quarters. In the long term, the fiscal expansion effect on investment poses a great degree of uncertainty, as shown by the widening 68% region of the highest posterior density. Unlike Mountford and Uhlig (2009), who find puzzling declining prices after a fiscal spending shock, we find intuitive results as the median impulse responses of inflation are zero in the short run, but positive in the medium-long run. Nevertheless, this result is uncertain, as the 68% region of the highest posterior density is wide. Based on these results, we also conjecture that the effect of a fiscal policy shock on national accounts and prices is temporary. With the sample from 1985:I to 2020:III, we find similar results where the median impulse responses of investment fall after some lags. However, we consider that the probability of the crowding-out effect has diminished, as the 68% regions of the highest posterior density cover both positive and negative areas.

As for the labor market, the RBC model predicts that the subsequently generated wealth effect from fiscal expansion induces labor supply, and the economy shifts the labor demand curve to a point where hours worked are higher and real wages are lower (Baxter and King 1993; Ramey and Shapiro 1998; Perotti 2007). Our results accord with their findings, where a positive fiscal shock raises hours worked and lowers real wages. Mountford and Uhlig (2009) also find negative responses in real wages after a positive fiscal spending shock, but only in the medium term. On the other hand, Rossi and Zubairy (2011) find insignificant responses of real wages and positive responses of hours worked. From Fig. 2, the effects are persistent from the short term until the medium term, while in the long run the uncertainties regarding the effects become higher. With the sample from 1985:I to 2020:III, the declining real wages still hold, but not as strongly as with the sample from 1954:IV–2006:IV (see Fig. 9 in Appendix D).

3.2.1 Anticipated vs unanticipated fiscal policy shock

One issue regarding a fiscal policy shock is whether the shock is anticipated or unanticipated. The previous analysis implicitly assumes that the fiscal policy shock is unanticipated. What if it is anticipated? Let us assume a delay of a year in the effect as imposed in Mountford and Uhlig (2009), where government spending is restricted to rise only after a year and Mountford and Uhlig (2009) label it as the anticipated government spending shock. Then, we can assess the sign constraints in Table 1 by imposing the constraints on quarters 5 to 8 only for the fiscal shock, while still on the first four quarters for the monetary policy and business cycle shocks.

It turns out that many models satisfy the sign constraints with substantial evidence, i.e., with Bayes factors > 3.2 against the unrestricted model. As in Sect. 3.1, we single out the model that has the highest posterior probability of having satisfied the sign constraints, then compute the Bayes factors of the likeliest model against the other models. This time, we find substantial evidence (Bayes factor of > 3.2) supporting the likeliest model in favor of all except two other models, as presented in Table 4. It turns out that the results in Table 4 point to the same models as in Table 2, which then leads to the same analysis as above. Hence, the labeled fiscal policy shock in our paper here is robust to whether the shock is unanticipated or anticipated. However, the higher posterior probabilities in Table 4 than in Table 2 are evidence that a fiscal policy shock may indeed be anticipated, as much previous literature suggests.

3.2.2 Fiscal multipliers

Based on the impulse responses to the fiscal policy shock as displayed in Fig. 2, we compute the present value of cumulative fiscal spending multipliers using the formula in Mountford and Uhlig (2009) with the average effective federal funds rate over the sample used as the discount rate. We report the median fiscal spending multipliers in Table 5 and compare them with the results in Lewis (2021), as he uses a similar data set to ours (1950:I–2006:IV). We also compare our data with various data samples of 1985:I–2020:III to exclude the periods before and during the Volcker episode and include the global financial crisis (GFC) episode of 2008 as well as the subsequent episode of zero interest rates.Footnote 8

On impact, our results yield a fiscal spending multiplier of 0.91 with the peak at 0.94 after one quarter. It becomes slightly lower with another data sample, as seen in Table 5. Our results here are more akin to the deficit spending multiplier of Mountford and Uhlig (2009), where the multiplier peaks after one quarter and shows a reversal in the sign in the long run, than the other previous results reported in Table 5. In the data sample of 1985:I–2020:III, however, the sign reversal of the median multipliers is not visible. The responses in real GDP in Fig. 2 are zero (with high probability), as the 68% regions of the highest posterior density cover both positive and negative areas after four quarters. Hence, the multipliers in the 8–20 quarters are zero with a high probability. Our estimates of the fiscal spending multiplier are higher than those of Lewis (2021), Mertens and Ravn (2014), and Blanchard and Perotti (2002) in the short run but lower in the longer run. Nonetheless, considering the peak multiplier of 0.89-0.94, our results are consistent with Ramey (2011), who finds a government spending multiplier between 0.8 and 1.5.

3.3 Impact of a monetary policy shock

The impulse responses to a positive monetary policy shock, signified by an increase of about 25 basis points in the interest rate, and the 68% regions of highest posterior density of the pointwise posterior densities, are depicted in Fig. 3. Overall, the impact of a monetary policy shock on all variables is temporary. In terms of output responses, we find results consistent with the conventional wisdom of weakening output after a monetary policy tightening, but only after some lags. Another result that we can highlight here is the substantial degree of uncertainty regarding the effects of the monetary policy shock in the short run. Hence, our results on the output responses are consistent with Rossi and Zubairy (2011) and Uhlig (2005). At the same time, there is an instantaneous decline in inflation, with the effect peaking after two quarters. Based on these, we conjecture that no price puzzle emerges in our results. A price puzzle in the VAR literature refers to a positive response in prices following a monetary policy tightening. Not only are the medians below zero, but also the 68% joint regions of highest posterior density up to 20 quarters.

Impulse responses to monetary policy shock (\(\varepsilon _{mp}\)) with data sample of 1954:IV–2006:IV. The black lines depict the median responses and the shaded areas are the 68% regions of the highest posterior density

Following a monetary policy tightening, a negative wealth effect becomes visible as output declines sluggishly, subsequently lowering hours worked. As hours worked fall, real wages rise. Rossi and Zubairy (2011) find significantly negative responses in consumption, investment, hours worked, and real wages just after some lags following a monetary policy tightening. In contrast, our results show mixed responses, where negative responses are only apparent on hours worked between 8 and 24 quarters. One can argue that the monetary policy shock transmits to those variables more sluggishly, and its effects are temporary.

As for consumption and investment, we find the increasing effect of a monetary policy tightening unappealing. This might be due to the monetary policy shock transmitting very sluggishly to consumption and investment, as with hours worked and real wages. In contrast, Bernanke et al. (2005) find insignificant responses in personal consumption, durable consumption, and non-durable consumption after a tightening of monetary policy. Durable consumption in their paper is included in the investment variable in our paper here. To investigate further, we perform an analysis with the data set of 1985:I–2020:III where we exclude the periods before and during the Volcker episode and include the global financial crisis (GFC) episode of 2008 and the subsequent episode of zero interest rates.Footnote 9

Impulse responses to monetary policy shock (\(\varepsilon _{mp}\)) with data sample of 1985:I–2020:III. The black lines depict the median responses and the shaded areas are the 68% regions of the highest posterior density

We find more appealing results with the latter data set in which, following a monetary policy tightening of about 25 basis points in interest rate, real GDP, investment, and hours worked fall after 4 quarters and the largest effects are between 12 and 16 quarters (see Fig. 4). Consumption and real wages decline only after 20 quarters, and the effect on inflation is weak and much less persistent than with the data sample of 1954:IV–2006:IV.

3.4 Impact of a business cycle shock

The impulse responses to a positive business cycle shock and the 68% regions of highest posterior density of the pointwise posterior densities are depicted in Fig. 5. We find similar results to Mountford and Uhlig (2009) with positive effects on all variables, except inflation. The effects on consumption, real wages, and government spending are visually persistent, while they last for about 10 quarters on real GDP and hours worked. Given the persistence of the effects on investment, the steady-state capital to labor ratio may increase and produce a higher level of steady-state income as well as consumption (Mountford and Uhlig 2009).

One noticeable difference between our results and those of Mountford and Uhlig (2009) are the responses of GDP deflator inflation following the business cycle shock. We find a short-lived decline in inflation, while Mountford and Uhlig (2009) find a lagging and persistent rise in inflation. Compared with Forni and Gambetti (2021), we find that our labeled business cycle shock is more akin to the supply shock, which raises GDP, consumption, and investment, but lowers the GDP deflator. Similar to our results, Forni and Gambetti (2021) also find permanent effects of such a shock on consumption, investment, and real wages.

Impulse responses to business cycle shock (\(\varepsilon _{bc}\)). The black lines depict the median responses, and the shaded areas are the 68% regions of the highest posterior density

Table 6 presents the relative contribution of the business cycle shock (\(\varepsilon _{5}\)) (in percent) to all eight variables in the model, based on median variance decomposition. They are the medians of the posterior distributions of the proportions of the forecast error variances. The contribution of the business cycle shock to the real sector, commonly associated with the business sector and households, is persistent from the very short term up to the long horizon. It is signified by the contribution of the business cycle shock to variables such as GDP, hours worked, and investment, starting after the first quarter and remaining considerable for up to 40 quarters. On consumption and the real wage, the contribution of the business cycle shock starts to pick up after four quarters. In addition, the business cycle shock also contributes considerably to government spending and federal funds rate. While the effect on government spending peaks at the longer horizon (between 20 and 40 quarters), it peaks at the shorter horizon on the policy rates (between 8 and 20 quarters).

3.5 Cyclicality of fiscal and monetary policies

We find that we have successfully assessed the sign restrictions used in Mountford and Uhlig (2009), pointing to a business cycle shock with the same characteristics as theirs. We further analyze the responses of government spending and federal funds rate as the fiscal and monetary policy instruments, respectively, to the business cycle shock. Referring to Fig. 5, positive responses in the interest rates can be seen as a counter-cyclical response of monetary policy, which fits the description of monetary policy by Romer and Romer (1994). Meanwhile, positive responses in government spending indicate the pro-cyclicality of fiscal policy. Based on the responses in government spending in Fig. 5, we find that US fiscal policy is acyclical in the short run, but pro-cyclical in the long run. It means that if the government receives money from a business cycle boom, it will eventually spend it. These results are consistent with Mountford and Uhlig (2009) who also find that government spending increases significantly after a positive business cycle shock only after around six quarters.

Cross-validating with other studies, our results are also in line with Kaminsky et al. (2005), who find an acyclical fiscal policy in the USA, and Lane (2003), who finds pro-cyclical fiscal policy, as we find it acyclical in the short run, but pro-cyclical in the long run. Our results are slightly different from those of Bashar et al. (2017), as they find evidence of counter-cyclical US fiscal policy. However, the counter-cyclical behavior is only apparent in the 1987–2011 period and at the 10% significance level. When using the sample period 1960–1986, which covers more than half of our sample, Bashar et al. (2017) cannot reject the null hypothesis of no counter-cyclicality. Hence, our results do not contradict their results.

In terms of persistency, the responses of the federal funds rate are instantaneous and short-lived, while the responses of the government spending are lagging and long-lived. To analyze further, we compute the relative contribution of the business cycle shock based on the 16th and 84th quantiles of the posterior distributions of the proportions of the forecast error variances. The results, displayed in Table 7, confirm that monetary policy reacts to shorter fluctuations in a business cycle, while fiscal policy reacts to longer fluctuations. In the variation of the federal funds rate, the business cycle shock contributes substantially already between 4 and 20 quarters. For government spending, on the other hand, the shock’s contribution only peaks after 20 quarters.

4 Conclusions

We successfully pinpoint three shocks by extracting the statistical properties of time series data together with theoretically-based signs. We find substantial evidence that the data support the proposed sign constraints in this paper. Despite multiple permutations satisfying the sign constraints, the fiscal policy shock, monetary policy shock, and business cycle shock can be labeled through further examination. We find that their effects on the economy are congruent with theories with a relatively high probability.

Overall, we find that the effects of a positive fiscal policy shock on consumption can be either zero (with high probability) in the sample from 1954:IV to 2006:IV, or negative in the latter data set. In line with this finding, we find a fiscal multiplier below 1. On investment, we find a lagging crowding-out effect in the data sample of 1954:IV–2006:IV, but in the 1985:I–2020:III period, the probability of the lagging crowding-out effect is smaller. As for the responses after a positive monetary policy shock, we find a weakening output after some lags, consistent with the leading monetary policy literature.

Additionally, we find that the effect of a positive business cycle shock on government spending is lagged but long-lived, while it has an instantaneous and short-lived effect on the federal funds rate. The business cycle shock contributes to the variation in government spending only in the long run, whereas it contributes substantially to the federal funds rate even in the short run. One limitation of our study is that we consider only government consumption expenditures and gross investment as the measure of fiscal policy and the federal funds rate as the measure of monetary policy. We leave other measures for both policies to further research.

Notes

See Appendix C.1 for the plot of densities of the data used. We also estimated a reduced-form VAR(4) model using ordinary least squares and performed normality tests for its residuals to check the data properties further. The results, reported in Appendix C.2, as well as the data densities lend support to clear deviations from normality.

We also entertained a model where the structural error variances evolve according to a GARCH(1,1) process as in Bertsche and Braun (2022) or Clark and Ravazzolo (2015), and found qualitatively similar impulse responses (the detailed results are not reported to save space, but they are available upon request). One drawback with it was the need to have many more chains and inner iterations to achieve convergence, which made the computation less efficient. We, therefore, remain with the skewed generalized t distribution without any particular law of motion for the variances.

The detailed procedure is given in Section III of their paper.

We repeated the exercise without the constraint on consumption to label the fiscal policy shock (the first shock in Table 1), as suggested by a referee. The likeliest permutation to satisfy the modified constraints (with posterior probability of 0.8182) contained \(\varepsilon _{1}\) as the fiscal policy shock, while in the second likeliest permutation (with posterior probability of 0.8084), it was \(\varepsilon _{6}\). Despite \(\varepsilon _{1}\) being the likeliest candidate for the fiscal policy shock, its impulse responses turned out to be counter-intuitive. For instance, the negative median response of inflation to a positive shock can be interpreted as evidence against it being the fiscal policy shock. Hence, \(\varepsilon _{6}\) can be deemed the fiscal policy shock even without the constraint on consumption, and the results are unaffected by relaxing this constraint. The detailed results are not reported to save space, but they are available upon request.

We thank the referee who suggested performing an analysis with the sample starting from 1985:I.

We thank the referee who suggested performing analysis with the sample starting from 1985:I.

We thank the referee who suggested performing analysis with the sample starting from 1985:I. More detailed analysis with this subsample is reported in Appendix D.

Sign restrictions are imposed on quarters 1 to 4.

References

Antolín-Díaz J, Rubio-Ramírez JF (2018) Narrative sign restrictions for SVARs. Am Econ Rev 108(10):2802–2829

Anttonen J, Lanne M, Luoto J (2021) Statistically identified SVAR model with potentially skewed and fat-tailed errors. Available at SSRN: https://ssrn.com/abstract=3925575 or http://dx.doi.org/10.2139/ssrn.3925575

Arias JE, Caldara D, Rubio-Ramírez JF (2019) The systematic component of monetary policy in SVARs: an agnostic identification procedure. J Monet Econ 101:1–13

Bacchiocchi E, Castelnuovo E, Fanelli L (2017) Gimme a break! identification and estimation of the macroeconomic effects of monetary policy shocks in the USA. Macroecon Dyn 22:1613–1651

Bashar OH, Bhattacharya PS, Wohar ME (2017) The cyclicality of fiscal policy: new evidence from unobserved components approach. J Macroecon 53:222–234

Baxter M, King RG (1993) Fiscal policy in general equilibrium. Am Econ Rev 83(3):315–334

Bernanke BS, Boivin J, Eliasz P (2005) Measuring the effects of monetary policy: a factor-augmented vector autoregressive (FAVAR) approach. Q J Econ 120(1):387–422

Bertsche D, Braun R (2022) Identification of structural vector autoregressions by stochastic volatility. J Bus Econ Stat 40(1):328–341

Blanchard O, Perotti R (2002) An empirical characterization of the dynamic effects of changes in government spending and taxes on output. Quart J Econ 117(4):1329–1368

Brunnermeier M, Palia D, Sastry KA, Sims CA (2021) Feedbacks: financial markets and economic activity. Am Econ Rev 111(6):1845–1879

Burnside C, Eichenbaum M, Fisher JDM (2004) Fiscal shocks and their consequences. J Econ Theory 115(1):89–117

Clark TE, Ravazzolo F (2015) Macroeconomic forecasting performance under alternative specifications of time-varying volatility. J Appl Economet 30:551–575

Davis C (2015) The skewed generalized T distribution tree package vignette

Fagiolo G, Napoletano M, Roventini A (2008) Are output growth-rate distributions fat-tailed? some evidence from OECD countries. J Appl Economet 23:639–669

Faust J (1998) The robustness of identified VAR conclusions about money. Carn-Roch Conf Ser Public Policy 49:207–244

Forni M, Gambetti L (2021) Policy and business cycle shocks: a structural factor model representation of the US economy. J Risk Financ Manag 14(8):371

Franke R (2015) How fat-tailed is US output growth? Metroeconomica 66(2):213–242

Galí J, López-Salido JD, Vallés J (2007) Understanding the effects of government spending on consumption. J Eur Econ Assoc 5(1):227–270

Gelman A, Carlin JB, Stern HS, Dunson DB, Vehtari A, Rubin DB (2013) Bayesian data analysis, 3rd edn. Taylor & Francis Ltd., Oxford

Giannone D, Lenza M, Primiceri GE (2015) Prior selection for vector autoregressions. Rev Econ Stat 97(2):436–451

Kaminsky GL, Reinhart CM, Vegh CA (2005) When it rains, it pours: procyclical capital flows and macroeconomic policies. In: Gertler M, Rogoff K (eds) NBER macroeconomics annual 2004, vol 19. MIT Press, pp 11–82

Kass RE, Raftery AE (1995) Bayes Factors. J Am Stat Assoc 90(430):773–795

King RG, Plosser CI, Stock JH, Watson MW (1991) Stochastic trends and economic fluctuations. Am Econ Rev 81(4):819–840

Lane PR (2003) The cyclical behaviour of fiscal policy: evidence from the OECD. J Public Econ 87(12):2661–2675

Lanne M, Luoto J (2020) Identification of economic shocks by inequality constraints in Bayesian structural vector autoregression. Oxford Bull Econ Stat 82(2):425–452

Lanne M, Luoto J (2021) GMM estimation of non-Gaussian structural vector autoregression. J Bus Econ Stat 39(1):69–81

Lanne M, Lütkepohl H (2014) A statistical comparison of alternative identification schemes for monetary policy shocks, pp 137–152. Number 296 in Acta Wasaensia. Finland: University of Vaasa

Lanne M, Meitz M, Saikkonen P (2017) Identification and estimation of non-Gaussian structural vector autoregressions. J Econ 196(2):288–304

Leeper EM, Walker TB, Yang S-CS (2013) Fiscal foresight and information flows. Econometrica 81(3):1115–1145

Lewis DJ (2021) Identifying shocks via time-varying volatility. Rev Econ Stud 88(6):3086–3124

Linnemann L (2006) The effect of government spending on private consumption: a puzzle? J Money Credit Bank 38(7):1715–1735

Lütkepohl H, Woźniak T (2020) Bayesian inference for structural vector autoregressions identified by Markov-switching heteroskedasticity. J Econ Dyn Control 113:1–21

Mertens K, Ravn MO (2010) Measuring the impact of fiscal policy in the face of anticipation: a structural VAR approach. Econ J 120(544):393–413

Mertens K, Ravn MO (2014) A reconciliation of SVAR and narrative estimates of tax multipliers. J Monet Econ 8(S):S1–S19

Mountford A, Uhlig H (2009) What are the effects of fiscal policy shocks? J Appl Economet 24:960–992

Perotti R (2007) In search of the transmission mechanism of fiscal policy. NBER Macroecon Annu 22:237–246

Puonti P (2019) Data-driven structural BVAR analysis of unconventional monetary policy. J Macroecon 61(August 2018):103131

Ramey VA (2011) Can government purchases stimulate the economy? J Econ Lit 49(3):673–685

Ramey VA (2016) Macroeconomic shocks and their propagation, vol 1, 2nd edn. Elsevier B.V, London

Ramey VA, Shapiro MD (1998) Costly capital reallocation and the effects of government spending. Carnegie Rochester Conf Public Policy 48:145–194

Romer CD, Romer DH (1994) What ends recessions? MIT Press, London, pp 13–80

Rossi B, Zubairy S (2011) What is the importance of monetary and fiscal shocks in explaining U.S. macroeconomic fluctuations? J Money Credit Bank 43(6):1247–1270

Shapiro SS, Wilk MB (1965) An analysis of variance test for normality (complete samples). Biometrika 52(3/4):591–611

Sims CA, Zha T (1998) Bayesian methods for dynamic multivariate models. Int Econ Rev 39(4):949–968

Ter Braak CJ (2006) A Markov chain Monte Carlo version of the genetic algorithm differential evolution: easy bayesian computing for real parameter spaces. Stat Comput 16(3):239–249

Ter Braak CJ, Vrugt JA (2008) Differential evolution Markov chain with snooker updater and fewer chains. Stat Comput 18(4):435–446

Uhlig H (2005) What are the effects of monetary policy on output? Results from an agnostic identification procedure. J Monet Econ 52(2):381–419

Wu JC, Xia FD (2016) Measuring the macroeconomic impact of monetary policy at the zero lower bound. J Money Credit Bank 48(2–3):253–291

Acknowledgements

The author thanks the Editor (Robert M. Kunst), an Associate Editor, two anonymous referees, Markku Lanne and Antti Ripatti for supervising this paper, Jani Luoto and Jetro Anttonen for the codes and discussions, and Päivi Puonti as well as the participants at the HGSE Econometrics Workshops for their helpful comments. Financial support from the Indonesia Endowment Fund for Education (LPDP) and all support from the Faculty of Social Sciences, University of Helsinki, are also gratefully acknowledged.

Funding

Open Access funding provided by University of Helsinki including Helsinki University Central Hospital.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The author certifies that there is no actual or potential conflict of interest in relation to this article.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix A: Bayesian estimation

In this appendix, we describe the Bayesian estimation in detail. Let us collect all the parameters of the model in the vector \(\pmb {\theta } = (\pi ^\prime ,\beta ^\prime ,\gamma ^\prime )^\prime \). Given the SVAR(p) model in (1) and the probability density function in (2), adopted from Lanne et al. (2017) and Anttonen et al. (2021), we have the following conditional likelihood function:

where \(\pmb {\theta } = (\pi ^\prime , \beta ^\prime , \gamma ^\prime )^\prime \), \(\pmb {\pi } = vec([c,\pmb {A}_1,\pmb {A}_2,\ldots ,\pmb {A}_p]^\prime )\), \(\pmb {\beta }=vec(\pmb {B})\), \(\pmb {\iota }_i\) is the ith unit vector, \(\pmb {\gamma } = (\lambda _1,\rho _1,q_1,\ldots ,\lambda _n,\rho _n,q_n)^\prime \) controlling the skewness and kurtosis of the shocks, and \(\pmb {u}_t(\pi ) = \pmb {z}_t - c - \pmb {A}_1 \pmb {z}_{t-1} - \ldots - \pmb {A}_p \pmb {z}_{t-p}\).

The Bayesian inference begins with prior information about the parameters. We assume that \(\lambda _i\) follows a uniform prior over the interval \([-1,1]\) and the prior of \(\rho _i\) is the truncated normal distribution with mean 2 and unit variance. It shrinks the posterior of \(\rho _i\) toward two and goes to zero relatively quickly at the tail. Meanwhile, the prior of \(q_i\) is the log-normal distribution with both log mean and log variance equal to 1, implying an uninformative prior for \(q_i\), but its posterior still shrinks toward zero quickly at the tail (see Anttonen et al. (2021) for more details and discussion).

Then, following Lanne and Luoto (2020), a Gaussian prior distribution is assumed for the inverse of the error impact matrix \(vec (\pmb {B}^{-1}) \equiv \pmb {b}, \pmb {b} \sim N(\bar{b},{\textbf {V}}_b)\) and the results are based on \(\pmb {b}=0_{n^2}\) and \(\pmb {V}_b=c_b \pmb {I}_{n^2}\) with \(c_b=10^2\). As for the deterministic terms and coefficient matrices \(\pmb {A}=[c,\pmb {A}_1^\prime ,\pmb {A}_2^\prime ,\ldots ,\pmb {A}_p^\prime ]^\prime \), a multivariate normal prior is assumed for \(vec(\pmb {A}) \equiv \pmb {a}, \pmb {a} \sim N(\bar{a},\pmb {V}_a)\). A diagonal covariance matrix \(\pmb {V}_a\) is assumed and the standard deviation of (i, j) element of lth (\(l=1,\ldots ,p\)) coefficient matrix \(\pmb {A}_l\) is set at \(\kappa _1/l^{\kappa _3}\) for \(i=j\), and at \(\sigma _i \kappa _1 \kappa _2 / \sigma _i l^{\kappa _3}\) for \(i \ne j\) where \(\sigma _i\) is the residual standard error of a \(p-\)lag autoregression for the ith variable in \(\pmb {z}\). Here, we set \(\kappa _1=0.2\), \(\kappa _2 = \kappa _3 = 1\) and \(\kappa _4 = 10 000\), while \(\pmb {a}\) is set such that the prior mean of the first lag coefficient matrix \(\pmb {A}_1=\pmb {I}_n\) and other elements of \(\pmb {A}\) are zeros. This set up involves standard Minnesota priors, which are also entertained, for instance, in Brunnermeier et al. (2021) among other Bayesian VAR literature. As far as the shrinkage prior for autoregressive parameters \(\kappa _1\) is concerned, \(\kappa _1=0.2\) returns an informative prior, which is also standard in the literature as also used in Sims and Zha (1998) and Giannone et al. (2015). We also entertained several informative priors with \(\kappa _1\) varying from 0.2 to 200 and found that the results remained intact.

After specifying the priors, our next step is to see how the data \(\pmb {z}_t\) affects us in revising the beliefs. Multiplying the conditional likelihood function in (5) by the prior density \(p(\pmb {\theta })\) we obtain the posterior distribution of \(\pmb {\theta }\):

where \(p(\pmb {z})\) is the marginal likelihood. The posterior distribution in (6) reflects the uncertainty about the parameters conditional on having observed \(\pmb {z}_t\). We estimate the posterior distribution of \(\pmb {\theta }\) by simulation using the algorithm of Anttonen et al. (2021), which implements the differential evolution Markov chain (DE-MC) method of Ter Braak (2006) and Ter Braak and Vrugt (2008) (See Anttonen et al. (2021) for details).

Appendix B: Variable definitions

All variable definitions and construction in this paper follow Rossi and Zubairy (2011). The sources of all raw data series are given in the unpublished appendix to their paper. Details of constructed variables used in the SVAR model in this paper are as in Table 8.

Appendix C: Inspection of the data, reduced-form errors, and tail exponents

1.1 Appendix C.1: The data densities

In this appendix, we inspect the data densities for both sub-samples used in this paper, i.e., sample 1954:IV–2006:IV and sample 1985:I–2020:III. We use 2-d kernel density estimates based on the highest density regions. Based on Figs. 6 and 7, most of them indicate a deviation from a normal distribution.

Data series densities sample 1954:IV–2006:IV

Data series densities sample 1985:I–2020:III

1.2 Appendix C.2: Reduced-form errors

We further examine the data properties by estimating a reduced-form VAR(4) model with a constant and a time trend using ordinary least squares. We then check the distribution of the reduced-form residuals (\(e_t\)) using Shapiro and Wilk’s (1965) normality test. The results suggest that most reduced-form errors also deviate from a normal distribution.

1.3 Appendix C.3: Tail exponents

To guarantee identification, we expect sufficient non-Gaussianity, and to evaluate this, we draw the marginal posterior distributions of the tail exponent \(\alpha _i = \rho _i q_i\), for all the statistically identified structural shocks. The tail exponent \(\rho _i q_i\) in the skewed generalized t distribution is akin to the degree-of-freedom parameter of the t distribution. Lower values imply fatter tails, while higher values imply thinner tails. For a Gaussian shock, for example, \(\rho _i=2\), \(q_i \rightarrow \infty \), hence \(\alpha _i \rightarrow \infty \).

Figure 8 depicts the tail exponents on the x-axis and the densities on the y-axis. It shows that there is sufficient non-Gaussianity as the mass tends to concentrate on relatively small values. We also evaluate the probability of the existence of the variance of ith shock, i.e., \(Pr[\alpha _i > 2]\), and Fig. 8 shows that they do exist.

Marginal posterior distributions of the tail exponent

Appendix D: Sub sample analysis

1.1 Sample from 1985:I to 2020:III

As suggested by one of the referees and as a robustness check, we exclude the periods before and during the Volcker episode and include the global financial crisis (GFC) episode of 2008 as well as the subsequent episode of zero interest rates, hence our sample here starts from 1985:I. As the Fed Fund Rates hit the zero lower bound during the period after GFC, we replace the Fed Fund Rates series with shadow rates of Wu and Xia (2016) since 1990. We assess the sign restrictions in Table 1 using the data sample 1985:I to 2020:III.Footnote 10 It turns out that the data support the specified sign restrictions, with even higher probabilities than with data sample 1954:IV to 2006:IV. However, again, many models satisfy the sign restrictions with substantial evidence (Bayes factors > 3.2). We then pick the likeliest model again and compute its Bayes factors against the other models.

We find substantial evidence in favor of the likeliest model against all others, except the ones listed in Table 11, where the likeliest combination is given in the first row, and the Bayes factors of the other combinations against it are given in the rightmost column. From the results in the table, we have two candidates, i.e., \(\varepsilon _{1}\) & \(\varepsilon _{6}\) for the fiscal shock, five candidates, i.e., \(\varepsilon _{6}\), \(\varepsilon _{7}\), \(\varepsilon _{5}\), \(\varepsilon _{1}\), \(\varepsilon _{8}\) for monetary policy shock, and two candidates, i.e., \(\varepsilon _{4}\) & \(\varepsilon _{8}\) for business cycle shock. We proceed by analyzing the impulse responses and FEVD in the same way as described in Sect. 3.1. The results allow us to label \(\varepsilon _{1}\), instead of \(\varepsilon _{6}\) as the fiscal policy shock (\(\varepsilon _{fp}\)) as about 48–61% of the forecast error variance of government spending (\(g_t\)) comes from \(\varepsilon _{1}\), compared to the 6.5–13% contribution of \(\varepsilon _{6}\). Then, the results also allow us to label \(\varepsilon _8\) as the monetary policy shock (\(\varepsilon _{mp}\)) as about 59–77% forecast error variance of the Fed Fund Rates comes from \(\varepsilon _8\). It also means that \(\varepsilon _4\) is the business cycle shock (\(\varepsilon _{bc}\)), as we have already labeled \(\varepsilon _8\) as the monetary policy shock (\(\varepsilon _{mp}\)). Hence, the data sample of 1985:I to 2020:IV favors the model with the posterior probability of 0.2354. Next, we compare the effects of the three labeled shocks with our analysis in Sub Sections 3.2-3.5.

Fiscal policy shock

Impulse responses to fiscal shock (\(\varepsilon _{fp}\)). The black lines depict the median responses, and the shaded areas are the 68% regions of the highest posterior density

Impulse responses to monetary policy shock (\(\varepsilon _{mp}\)). The black lines depict the median responses, and the shaded areas are the 68% regions of the highest posterior density

In the short term, negative responses in consumption seem persistent for the first four quarters. On investment, we find similar results where the median impulse responses of investment fall after some lags. However, we consider that the probability of the crowding-out effect has diminished as the 68% region of the highest posterior density covers both positive and negative areas (see Fig. 9). On the other hand, the effects on real wage and hours worked are zero (with high probability) after the shock, hence the prediction of the RBC model’s beliefs of rising hours worked and falling real wages after a fiscal expansion no longer hold.

Monetary policy shock

With a sample of 1985:I to 2020:III, the effects of a monetary policy tightening of about 25 basis point interest rate are more appealing and delayed than with a sample of 1954:IV to 2006:IV. Real GDP, investment, and hours worked fall after about 10 quarters (see Fig. 10). Real wages and consumption weaken after long delays. The effects on inflation are much softer and muted.

Business cycle shock

With a sample of 1985:I to 2020:III, all the results and analysis in Sub Sections 3.4 and 3.5 still hold, where all variables, except inflation, respond positively after a business cycle shock (see Fig. 11). Fiscal policy also still exhibits pro-cyclical behavior, while monetary policy has counter-cyclical behavior.

Impulse responses to business cycle shock (\(\varepsilon _{bc}\)). The black lines depict the median responses, and the shaded areas are the 68% regions of the highest posterior density

Impulse responses with sample 1954:IV–2006:IV. The shaded areas are the 68% region of the highest posterior density. The units on the y-axis are in percent, except the responses in interest rate (\(r_t\)), which are in basis points

Impulse responses with sample 1985:I–2020:III. The shaded areas are the 68% region of the highest posterior density. The units on the y-axis are in percent, except the responses in interest rate (\(r_t\)), which are in basis points

1.2 Comparison with the impulse responses of the unrestricted model

Here, we discuss the impulse responses of the unrestricted model with two sets of data samples, i.e., 1954:IV–2006:IV and 1985:I–2020:III (Figs. 12 and 13, respectively). As we have pointed out previously, the shocks cannot be labeled without additional information. Indeed, there are several approaches to labeling shocks ex-post as discussed in Lewis (2021), but we rely on the sign constraints in Table 1 to label the shocks, since our motivation is to see whether the data reconciles with the theoretical predictions or not.

Let us first take the case of the responses of government spending (\(g_t\)). \(g_t\) must increase after a positive fiscal policy shock. With the data sample of 1954:IV–2006:IV, on impact, \(g_t\) increases after a positive shock to \(\varepsilon _1\), \(\varepsilon _2\), \(\varepsilon _3\), and \(\varepsilon _8\) (see Fig. 12). Then, with a normalization, a positive shock to \(\varepsilon _5\), \(\varepsilon _6\), and \(\varepsilon _7\) also induces an increase in \(g_t\). Hence, we cannot distinguish which shock is the fiscal policy shock. Compared to the restricted model, the constraints limits to four models as presented in Table 2, where there are only three candidates for the fiscal policy shock, i.e., \(\varepsilon _3\), \(\varepsilon _4\), and \(\varepsilon _6\). When we further assume that a fiscal policy shock is anticipated, it then limits to only two candidates for the fiscal policy shock, i.e., \(\varepsilon _4\) and \(\varepsilon _6\) as presented in Table 4. Similarly with the data sample of 1985:I–2020:III, \(g_t\) increases after a positive shock to \(\varepsilon _1\), \(\varepsilon _2\), \(\varepsilon _4\), and \(\varepsilon _8\) (see Fig. 13). With a normalization, it is also the case after a positive shock to \(\varepsilon _3\), \(\varepsilon _5\), \(\varepsilon _6\), and \(\varepsilon _7\). Compared to the restricted model, the restricted model points to only two candidates for the fiscal policy shock, i.e., \(\varepsilon _1\) and \(\varepsilon _6\) (see Table 11).

Let us now consider the responses in interest rate (\(r_t\)). \(r_t\) must increase after a positive monetary policy shock. From Fig. 12, \(r_t\) rises after a positive shock to \(\varepsilon _3\), \(\varepsilon _4\), \(\varepsilon _5\), and \(\varepsilon _8\). This is also the case with a positive shock to \(\varepsilon _2\) and \(\varepsilon _6\) after a normalization of which the response of \(r_t\) must be positive. Compared to the restricted model, the restricted model limits the candidates for the monetary policy shocks to \(\varepsilon _5\) and \(\varepsilon _8\) only (see Table 2 or 4). Similarly with the data sample of 1985:I–2020:III, \(r_t\) also rises after a positive shock to \(\varepsilon _3\), \(\varepsilon _4\), \(\varepsilon _5\), and \(\varepsilon _8\) (see Fig. 13). If ones consider, for example, \(\varepsilon _4\) as the monetary policy shock, then an output puzzle, where output increases after a monetary policy tightening, may emerge.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Mansur, A. Simultaneous identification of fiscal and monetary policy shocks. Empir Econ 65, 697–728 (2023). https://doi.org/10.1007/s00181-022-02352-z

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-022-02352-z