Abstract

This paper investigates how supply noise and demand noise contribute to business cycle fluctuations in three major European economies. A structural vector autoregressive model is used to identify supply, demand, supply noise and demand shocks. The identification scheme is built on nowcast errors of output growth and the inflation rate that are derived from the Consensus Economics Survey. The results indicate that positive supply noise and positive demand noise shocks have an expansionary effect on output, but their magnitude differs across countries. The two shocks contribute equally to business fluctuations, and jointly, they account for around one quarter of the total variation in GDP in each of the three countries.

Similar content being viewed by others

1 Introduction

There is a widespread belief that changes in expectations about economic fundamentals can be an independent driver of macroeconomic fluctuations if there are no changes in the current fundamentals themselves. This belief dates back to Pigou (1929), who coined the idea that ‘wave-like swings in the mind of the business world between errors of optimism and pessimism’ are the source of economic fluctuations.

There are different interpretations of how optimism or pessimism can shape the business cycle. The literature finds three strands of thought on how economic sentiment and beliefs matter for business cycle fluctuations. First, the irrational animal spirits strand of thought sees psychological waves of optimism and pessimism driven by random shocks as the cause of macroeconomic fluctuations. The psychological waves are not backed up by fundamentals and so they eventually lead to a bust (Keynes 1936; Akerlof and Shiller 2010).

Advocates of the theory of self-fulfilling animal spirits (Farmer 1999, 2012a, b; Benhabib et al. 2016; Bacchetta and Wincoop 2013) also see that the root of macroeconomic fluctuations lies in the animal spirit style of fluctuations, but believe that actions that follow these fluctuations lead to changes in fundamentals. This makes the initial boom or bust in confidence both rational and self-fulfilling.

The news view argues that agents have access to a non-measurable source of imperfect information. As the agents are imperfectly informed, they may form misperceptions about the state of economic fundamentals. How imperfect information affects consumer expectations has received growing interest in the recent literature on macro-news. The impact of macroeconomic news on households inflation expectations has received particular attention. One source of misperceptions is noise shocks, which affect the signals that agents receive. Dräger and Lamla (2017) find evidence of imperfect information when consumers form expectations about inflation.

The driving force of any prediction is a diverse set that contains information about future policies or future demographic trends, or news about future technologies and future prices.Footnote 1 Waves of optimism occur when agents receive the information that new market opportunities will develop in the future. This causes firms to increase investment immediately so they can meet the new demand patterns when they are realised in the future. At the same time consumers increase their consumption as they feel they will be richer in the future. If the information is valid and the market opportunities do actually materialise in the future, the boom does not have to be followed by a crash. However, if the agents make an error and become overly optimistic, the boom will be followed by a crash.

Settings in which the information received by the agents may turn out to be validated by future developments, or may be proved wrong as future events do not align with the original information, are usually referred to as noise formulation. In essence, news-driven business cycles arise because of information, and errors made when noise shocks affect the information.

Beaudry and Portier (2006) reignited the idea of business cycles driven by non-fundamental factors by providing empirical evidence that news about future productivity could explain half the fluctuations in GDP. Their estimates also implied that news can create business cycle comovements, because hours and output rose with the arrival of new information.

Beaudry and Lucke (2010) reach similar conclusions using a different identification approach. At the other pole of the debate, Kurmann and Otrok (2013), Barsky and Sims (2012) and Barsky et al. (2015) find that news-driven business cycles play only a limited role. A comprehensive summary of the literature can be found in Beaudry and Portier (2014).

Some papers have highlighted problems with the Beaudry et al. identification method (Kurmann and Mertens 2014; Forni et al. 2014), in particular the problem of non-fundamentalness. One approach proposed as a solution has been to increase substantially the number of observables by using a factor augmented structural vector autoregressive (FAVAR) model when estimating the effects of news shocks (Forni and Gambetti 2014).Footnote 2 Other authors have started to use the expectations of professionals in their estimation methods to uncover noise shocks (Fujiwara et al. 2011; Milani 2011; Miyamoto and Nguyen 2014).

Another area of ongoing research is whether it is only misperceptions about supply that can affect the fluctuations of macroeconomic variables. This question is driven by the observation that presumed noise shocks often resemble demand shocks. Lorenzoni (2009) shows with a theoretical model that supply noise shocks are observationally indistinguishable from fundamental demand shocks.

In a recent paper, Benhima and Poilly (2021) propose a model for assessing the effects of a demand noise shock that also uses survey expectations of professional forecasters in their identification approach.Footnote 3Footnote 4

Using a structural vector autoregressive (SVAR) model that includes nowcast errors about output and inflation, they identify supply and demand noise shocks in the US. Their results indicate that demand-related noise shocks are recessionary and contribute considerably to output fluctuations. In their reasoning about the dynamics of the demand noise shock, Benhima and Poilly (2021) conclude that monetary policy and informational frictions play a key role in driving the recessionary effects.Footnote 5

Most of the literature focuses on the effects of non-fundamental shocks in large closed economies. Almost all the empirical studies that employ the survey expectations methodology use data from the US, and only a few studies take a comparative approach and survey the effects of such shocks in other economies. Kamber et al. (2017) develop a small open economy model to identify the effects of news shocks in four small, open, advanced economies: Australia, Canada, New Zealand and the UK. Their results indicate that news about TFP causes a considerable positive comovement between GDP, hours worked, consumption and investment in all the economies in their study. Brzoza-Brzezina and Kotłowski (2020) show how the effect of confidence shocks can be transmitted internationally. They argue that news-type shocks can travel across borders as much as sentiment-type shocks can, through direct linkages like the media, and indirect ones such as trade or financial integration. Estimating a VAR/VECM type of model, they show that confidence shocks from the euro area play an important role in explaining variations in Polish GDP.

In this paper, I focus on the effects of supply and demand shocks, both fundamental and noise shocks, in three major European economies. I use data from the Consensus Economics Survey to construct time series for the nowcast errors of output growth and inflation for France, Germany and Italy. The nowcast errors are the differences between the real time forecast of the survey participants for output growth and inflation and the actual data in the first release from the national statistical offices. This means the nowcast errors measure misperceptions about output and prices in real time.

Benhima and Poilly (2021) have provided a general framework for identifying both supply noise shocks and demand noise shocks. I follow their theoretical framework and use three European economies as applications. The identification scheme builds on the idea that the errors made by rational nowcasters need to be internationally consistent. A demand shock that drives a positive correlation between GDP growth and the inflation rate should also cause a positive correlation between the nowcaster’s error in output and the nowcast error for inflation. The baseline VAR model includes GDP growth, the inflation rate, the nowcast error for GDP growth and the nowcast error for the inflation rate.

The main results indicate that positive supply and positive demand noise shocks both have expansionary effects on output, but the magnitude of the effect differs slightly across countries. Output reacts more strongly to noise shocks in Germany and Italy, while GDP and inflation show a slightly weaker response in France. The expansionary response of GDP to supply noise shocks is observationally similar in shape to the effects of a fundamental demand shock, especially in Germany. This is in line with the theoretical arguments of Lorenzoni (2009). Benhima and Poilly (2021) extend this line of argument by showing that the effects of positive demand noise shocks may potentially resemble the effects of negative supply noise shocks. I cannot confirm those results from my analysis. A positive demand noise shock has an expansionary effect on GDP in France, Germany and Italy, though the effect seems insignificant for Italy.

Second, I find that demand noise shocks have a limited effect on the variation in output growth. Demand noise shocks explain on average 11% of the volatility in output growth. Supply noise shocks explain a slightly larger fraction of the variation in output growth in the three European economies, ranging from 11 to 14%. This contrasts with the findings of Benhima and Poilly (2021), who find that demand noise shocks contribute 23% of output growth volatility, while supply noise shocks only explain around 8% of the volatility in GDP growth.

I contribute to the existing literature in two ways. First, I provide comparative evidence from three large European economies that supply and demand noise shocks have short-run implications for output growth. To the best of my knowledge, this is the first study of the effects of noise shocks for France, German and Italy. My second contribution is that I show that although some dynamics are similar for the set of European countries and for the USA, the response of output growth to a positive demand noise shock is different.

The paper is structured as follows. Section 2 documents the empirical model and the set of identifying restrictions. Section 3 discusses the data. In Sect. 4, I present the empirical results. In Sect. 5, I perform a number of robustness tests around the baseline identification scheme. The final section concludes.

2 Methodology

This section starts out by describing the cornerstones of the theoretical model. The second part describes the empirical model and the SVAR estimation strategy.

2.1 Theoretical model

The model develop by Benhima and Poilly (2021) extends the New Keynesian model of Galí (2015) by including noisy information about both supply shocks from technology and demand shocks from preferences. The dispersed information model consists of three agents that make decisions under conditions of uncertainty, and a representative nowcaster. The role of the nowcaster in the model is to survey the economy and publish nowcasts, which allows the survey expectations to be distinguished from the expectations of the agents. The island structure of the model is similar to that of Lorenzoni (2009), and it includes households, firms, a central bank and nowcasters. The islands are inhabited by a continuum of households who work and consume a final good. A continuum of oligopolistic firms produce differentiated intermediate goods that are used by a competitive firm to produce a final good. The households have preferences for consumption and labour supply. Firms are aware of the technology they use to produce the intermediate goods. Monetary policy is conducted by a central bank that shapes expectations for inflation and sets the interest rate.

Agents learn about the future either by observing the shocks directly or by learning about them from the public and private signals of other agents. Firms and households receive private information that is subject to an idiosyncratic noise shock. In addition, firms, households, the central bank and the nowcasters also receive a public signal about technology and preferences that may potentially be noise.Footnote 6 Signals of technology can be viewed as a sort of supply shock that alters the productivity of labour of the firm, while preference shocks can be thought of as demand shocks that shift the factor of time preferences of households. While technology shocks have a permanent component, preference shocks are only transitory. From the firm’s perspective, prices depend on the public signal and on the demand shock. Higher-order beliefs arise with dispersed information as strategic complements in price-setting lead the firms to set higher prices when they expect other firms will be doing the same thing. The central bank is setting the nominal interest rate following a Taylor rule in response to the public signal it receives.Footnote 7 Table 1 summarises the key proposition of the model.

We may first focus on how fundamental and noise shocks affect output, yt, and inflation, πt, in Table 1. In a model where agents receive private and public signals, a positive fundamental supply shock drives a positive response from output and a negative response from inflation. This is a standard assumption in New Keynesian models. Consumers observe a positive signal about productivity and start to increase their consumption. The permanent positive productivity shock also allows firms to cut their prices as they respond to lower marginal costs.

A supply noise shock should have a temporary positive effect on output and a positive effect on inflation. In this way, the behaviour of output and inflation resembles that seen in fundamental demand shocks. Consumers observe a productivity shock and, as in the first case, increase their consumption. However, the anticipated increase in productivity does not materialise.Footnote 8 As the increase in demand is not matched by an increase in actual productivity, firms raise their prices in anticipation of higher marginal costs. The central bank accentuates the positive response of output as it also misjudges the productivity shock. This leads it to cut interest rates in expectation of lower inflation, stimulating aggregate demand.

The third row in Table 1 indicates both the expansionary and inflationary effects of fundamental demand shocks. This assumption is also standard in New Keynesian models. Firms receive a signal about aggregate demand, such as a change in preferences. Expecting higher costs they raise their prices.

The last row describes the effects of demand noise shocks. These effects are more ambiguous than those of the other shocks. First, demand noise shocks have a temporary negative effect on output. The recessionary effect is driven by the reaction of the central bank. Observing a noisy public signal about demand, the central bank raises interest rates. The higher interest rate leads consumers to curb consumption, causing output to fall. However, this result depends on the parameterisation and certain assumptions that are imposed on the model. The positive response from inflation is conditional on the assumption that firms anticipate an overall rise in aggregate demand. When firms receive a public signal of a preference shock, they anticipate both a positive demand shock and a rise in the interest rate, which should have a negative effect on aggregate demand. That in turn depends on the interplay between the slope of the Phillips curve, the parameters of the reaction function of the central bank, and the informational advantage that firms have over the central bank.Footnote 9 Hence, the effect for inflation depends on the overall effect of aggregate demand.

For the expectation errors, the model proposes a negative effect from survey expectations on output, Ets(yt) − yt, and positive effect on the survey expectation for inflation, Ets(πt) − πt following fundamental supply shocks (see Table 1 columns three and four). As nowcasters underestimate output growth and overestimate inflation, a positive fundamental supply shock has a negative effect on the errors in survey expectations for output and a positive effect on the survey expectation error for inflation.Footnote 10

A supply noise shock has a positive effect on the expectation error for output and a negative effect on the survey expectation error for inflation. If the surveyors underestimate the response of output to a fundamental supply shock, a supply noise shock drives them to overestimate output when they are faced with a signal about productivity. As the expectation of output is smaller than the realisation of it, the surveyors overestimate the response of inflation, causing a negative effect on the survey expectation error for inflation.

The model suggests that in a similar fashion to the dynamics of a fundamental supply shock, positive fundamental demand shocks have a negative effect on the survey expectation error for output. When survey expectations underreact to fundamental demand shocks, the surveyors also form expectations for inflation that are lower than what is realised, leading to a negative response from the survey error for inflation.

Finally, the model proposes that demand noise shocks should have a positive effect on both the survey expectation error for output and the survey expectation error for inflation. The public signal in noise shocks makes the surveyors overly optimistic. The surveyors anticipate that inflation will increase when they receive a positive signal about demand. However, if the signal was driven by noise, inflation will not materialise fully. This means that the surveyors have overestimated inflation, and this in turn means that the effect of the survey expectation on inflation is positive.

2.1.1 Addressing non-fundamentalness

Firms and households make decisions under conditions of uncertainty as they cannot always distinguish between a fundamental shock and a noise shock when they receive news about the future that they then act upon. Neither can an econometrician with the same set of information that the agents have distinguish between fundamental and noise shocks. As Blanchard et al. (2013) point out, with imperfect information the VAR does not have a unique moving average (MA) representation as the econometrician might not be able to recover the coefficients or the shock from the current and past values of the stochastic process. In the context of research into the news-driven business cycle, this problem can render the results from SVAR methods meaningless.

The practical response of the literature to this problem has been to include information in the model that is available to the econometrician but not contemporaneously to the nowcaster.Footnote 11 To understand why the dispersed information structure of the model is essential when I want to disentangle fundamental shocks from noise shocks, consider a simple reduced form model with demand shocks and demand noise shocks. Households and firms receive private information on top of the public signal. To identify the fundamental shock and the noise shock, it is sufficient that households have more information about demand than the nowcaster, who only receives a public signal. When there is less information, the noise shock affects the survey expectation of output but not the actual contemporaneous realisation of output itself. The informational advantage over the nowcaster can come from including a measure of misperceptions, which can be the nowcast error for output and inflation growth, as the econometrician can observe the actual realisation of output, which is not available to the nowcaster contemporaneously.

2.2 Estimation and identification strategy

The theoretical model allows for testable assumptions. To analyse the effects of supply noise shocks and demand noise shocks on output and inflation, I estimate a SVAR model using a set of restrictions that come from the proposition outlined in Sect. 2.1.

The canonical VAR model that I estimate is:

where Yt = (Y1,t,... Yn,t) is a vector of observables, L is the lag operator, Φ is the matrix of estimated parameters, and νt is a vector of reduced form residuals with νt ~ iid \(\left( {0, {\Sigma }} \right). \)

For the structural VAR I follow the same estimation strategy as in Benhima and Poilly (2021). I implement the sign and zero restrictions using the algorithm of Arias et al. (2018). Instead of drawing the parameters from the posterior distribution of a Bayesian VAR, I use a Monte Carlo strategy as suggested by Hamilton (2020) to generate a set of coefficients \(\hat{\Phi }(L)\) that are drawn from the asymptotic distribution of the estimated reduced-form parameters. Draws from the asymptotic distribution of the variance-covariance matrix of the reduced-form residuals are used to construct the matrix \(\hat{\Sigma }\). This estimation technique is conceptually equivalent to using a flat prior distribution. The baseline VAR model is estimated for each country individually.

The observables in the VAR are:

∆yt is the annualised growth rate of real GDP, and πt is the annualised consumer price index (CPI) inflation rate. The third term reflects the nowcast errors of real GDP, and the fourth term reflects the errors of CPI inflation. The nowcast errors of real GDP are calculated as \(E_{t} \{ \Delta y_{t} \} - \Delta \tilde{y}_{t}\), which is the difference between the mean nowcast of Consensus Economics and the first release GDP estimate from the national statistical office. The nowcast error of CPI inflation, \(E_{t} \{ \pi_{t} \} - \tilde{\pi }_{t}\), is calculated in the same way.

I aim to disentangle fundamental supply and demand shocks from supply and demand noise shocks. The identifying restrictions needed for this are based on the set of sign restrictions from a structural New Keynesian model. Table 2 summarises the set of sign restrictions of the SVAR model needed to identify the shocks.

Let us first focus on the fundamental shocks. A positive fundamental supply shock drives a positive response from output growth and a negative response from inflation. For our baseline identification strategy, it is only necessary to restrict the response of GDP to be positive. I impose that only fundamental supply shocks have a long-run effect on GDP by taking the sum of the cumulated impulse responses of GDP growth as in Armantier and Quah (1989). Other fundamental and noise shocks are only transitory.

A positive response from GDP and a positive response from inflation to a fundamental demand shock is also a standard assumption in New Keynesian models. For the restrictions of the errors I assume, following from the theoretical model, that when nowcasters overestimate a fundamental demand shock, the nowcast errors of GDP and inflation must be underestimated. As I am particularly interested in understanding the response of GDP to fundamental demand shocks, I leave the response of output growth unrestricted.

For the restrictions of the noise shocks, I first impose a positive response from output growth to a supply noise shock. As with the fundamental supply shocks, I leave the response of inflation unrestricted. Finally, I restrict the response of the endogenous variables to demand noise shocks. The first thing to note is that I leave the response of output growth to demand noise shocks unrestricted, as I did for fundamental demand shocks. Second, I restrict the response of inflation to be positive. The response of inflation can also be restricted to be negative, as this helps in distinguishing between negative fundamental demand shocks and positive demand noise shocks. Looking only at the restrictions of the errors might not allow these two shocks to be disentangled if there are no restrictions on the response of GDP. This means I need to assume that there is a positive response from inflation so that I can distinguish between negative fundamental demand shocks and positive demand noise shocks.

Another important feature of the baseline identification scheme is that supply noise shocks affect the expectation errors with opposite signs, while fundamental demand shocks and demand noise shocks drive the expectation errors in the same direction. This allows for a clearer distinction between supply noise and the two demand shocks.Footnote 12

3 Data

The main data source for studies analysing the effects of expectations on macroeconomic fluctuations using a survey-based expectation approach has been the US Survey of Professional Forecasters (SPF).Footnote 13 The US SPF is conducted on a quarterly basis, and the survey panellists are asked to provide their estimates for output growth and inflation for the current quarter and for longer horizons.

My analysis assesses the effects of expectational errors on business cycle fluctuations in Europe.Footnote 14 As I am particularly interested in whether supply and demand side noise shocks have different effects across the biggest European economies, I require information on nowcasts for individual countries.Footnote 15

I propose to use data from the Consensus Economics survey, as that survey is closest in design to the US SPF. Consensus Economics is a private survey firm that polls more than 700 private-sector individuals and economic research institutes.Footnote 16 The Consensus Economics survey is conducted on a monthly basis and provides nowcasts and forecasts for a large set of macroeconomic variables for different countries. Like in the US SPF, survey panellists receive a questionnaire each month on the Monday of the week that contains the 15th of the month. The survey participants submit their nowcasts for the quarterly year-on-year percentage change in private consumption and the national consumer prices by the following Monday.

The survey participants are asked to provide quarter-on-quarter and year-on- year nowcasts for GDP. To be consistent in the reference point of the nowcast, I use the year-on-year errors in the baseline specification of the model. In the robustness section, I show the results when the errors are calculated from the quarter-on-quarter GDP nowcasts. To make the results more comparable to the studies from the US I annualise all the variables that enter the VAR.

Reliable nowcasts and first release estimates of GDP and inflation are available from 2003Q1 for France and Germany and from 2003Q2 for Italy. The sample ends in 2019Q4 to avoid the large distortionary effects that the Covid-19 pandemic had on key macroeconomic variables. I use all the available data in the baseline estimation, while some robustness checks are done in Section 5.

No flash estimates for output growth for the latest quarter exist from public data sources but the forecasters need to be aware of output growth in the preceding quarters to provide estimates for year-on-year GDP growth rates. This means that the only uncertainty should arise from the unknown output growth and inflation in the current quarter when they provide their estimates for the year-on-year percentage changes. The forecasters are aware of the final release data for inflation of the first month of the quarter, and at least the first release data on inflation in the second month of the quarter. As the inflation rates for the first and the second months are known, the forecasters have to provide an estimate for the last month of the quarter to construct the quarterly year-on-year inflation rate. I do not have the data to disaggregate the nowcasts and so I use the survey’s mean nowcast.Footnote 17

Our analysis is based on the nowcast errors. The nowcast errors are computed as the difference between the nowcast predictions of GDP growth and inflation from the Consensus Economics survey, and the first-release data for actual real GDP growth and actual inflation. The first-release data are obtained from the national statistical offices. Figure 11 in the Appendix shows the difference between the errors calculated from first release data and the errors calculated from the final release data in France, which arise from more exact second release estimates and data revisions. The final release data, or the most recent series, incorporate changes in the methodology of the national accounts and data revisions that cannot be foreseen by the forecaster, which might bias the results (Croushore 2010).

Figure 1 depicts the nowcast errors of GDP and the nowcast errors of inflation. Observations in the top left quadrant reflect nowcasts where survey participants underestimated GDP growth but overestimated inflation. The bottom left quadrant shows nowcasts where GDP growth was overestimated and inflation was underestimated. The figure shows that nowcast errors tend to be equally centred around zero. A standard t-test against zero cannot reject the hypothesis that the means are different from zero for either Germany or France. For the Italian GDP errors, there is weak evidence that the GDP nowcast errors are different from zero. This indicates that survey participants do not systematically overpredict or underpredict contemporaneous output growth or the inflation rate. With few exceptions, the errors for each time observation overlap or are close to each other.

GDP growth and inflation nowcast errors. Nowcast errors of real GDP growth and consumer price inflation in annualised percentage points. Sample for Germany and France: 2003Q1–2019Q4. Sample for Italy: 2003Q2–2019Q4

From Table 8 in Appendix, I see positive correlations between the nowcast errors of GDP growth across countries. The correlation coefficient ranges from 0.36 in the year-on-year GDP nowcast errors between France and Italy, to 0.58 between Germany and Italy. As the quarterly GDP growth nowcast errors exhibit a strong positive correlation with the yearly GDP growth nowcast errors within a country, the cross-country correlation of the quarterly nowcast errors is also positively correlated. Even more so, the yearly nowcast errors for inflation show a strong positive correlation ranging from 0.43 to 0.63. There are a few markedly larger nowcaster errors in the top right quadrants.

From Fig. 11, we can see that those errors for France can be traced back to certain episodes during the Great Recession of 2009. The nowcasters presumably underestimated the large decline in GDP and consequently overestimated that consumer prices would be higher than they actually turned out to be. The German data also show larger nowcast errors for GDP growth and inflation during the recovery period of 2010 when the nowcasters underestimated GDP growth but also underestimated inflation (see Fig. 12 in the Appendix).

I provide summary statistics for the time series in Table 3. The nowcast errors are measured in annualised percentage points. The mean and standard deviation of the inflation nowcast errors are comparable across countries. As the survey participants have more information on past consumer price changes when they make their nowcasts, the errors associated with those forecasts are smaller than the error stemming from GDP forecasts. Comparing the GDP nowcast errors from the first release data shows that the GDP growth nowcast errors of Italy and France have a smaller variation around the mean, and that the standard error is considerably larger for Germany. The standard errors and the maximum realisations of the year-on-year and quarter-on-quarter observations of the nowcast errors appear similar. From Tables 5, 6, and 7, it is also visible that the year-on-year and quarter-on-quarter GDP nowcast errors are both strongly positively correlated. These observations support the idea that year-on-year nowcast errors can be interpreted as conditional quarter-on-quarter nowcast errors.

4 Results

Here I present the results of my estimation. I seek to extract fundamental and noise shocks from the nowcast errors to determine how they affect GDP fluctuations.

4.1 Impulse response analysis

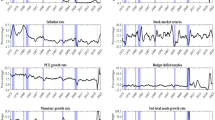

This section discusses the impulse response functions for each country. In the baseline estimation I use the nowcast errors computed for the first-release data and four lags. Figure 2 shows the IRFs for France, Fig. 3 the results for Germany and Fig. 4 the impulse response functions for Italy. The thick, solid line shows the median impulse responses of real GDP in levels, the inflation rate, the nowcast errors of GDP and the nowcast errors of inflation following fundamental and noisy shocks to both supply and demand. The dotted lines indicate the 16 and 84% confidence regions. Those intervals can be interpreted as confidence bands surrounding the median parameter estimate as they are calculated using Monte Carlo sampling.

IRF Benchmark Estimation—France. The solid lines depict the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

IRF Benchmark Estimation—Germany. The solid lines show the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

IRF Benchmark Estimation—Italy. The solid lines show the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

In the top row, I show the response of GDP, inflation and nowcast errors to fundamental supply shocks. Positive fundamental supply shocks have an expansionary effect on output. A positive fundamental supply shock has the strongest effects in Germany, followed by Italy and then France. The deflationary response of inflation is genuine and is in line with standard assumptions in Germany and France. Italian inflation also falls following a fundamental supply shock but the response is not statistically significant. Even though the response of the GDP and inflation nowcast errors are both left unrestricted, the median response of the GDP nowcast errors at impact is negative for all the countries and the responses of the inflation nowcast errors are positive. I observe almost no systematic effect after the impact period. The negative response of the GDP nowcast errors and the positive response of the inflation nowcast errors are exactly in line with the theoretical predictions of the model.

The response of GDP to a supply noise shock is expansionary and peaks after three quarters, though the magnitude differs between countries. With a supply noise shock that causes the GDP nowcast error to increase by 0.25% point on impact, GDP expands by approximately 1.2% points after two quarters in Germany, while a similarly sized shock raises output in France by only 0.6% point. The hump-shaped response of Italy’s GDP is similar to that of Germany, but it levels out slightly faster. Note that the identifying assumption for the supply noise shock only restricts the impulse response on impact but not the dynamics of the adjustment.

The response of output to the fundamental demand shocks is left unrestricted. In line with the theoretical predictions, output expands following a positive fundamental demand shock. The effect is visible for Germany and France, where the response of GDP peaks in around the third or fourth quarter and then gradually levels out. For Italy, a fundamental demand shock does not lead to the characteristic hump-shaped effect on GDP, but the results are statistically not different from zero after two quarters. The positive co-movement of output and inflation across the two shocks echoes the theoretical predictions of Lorenzoni (2009). This means that observing only the response of output and inflation would not allow the researcher to determine if the economy had been hit by a fundamental demand shock or if the agents in the economy had overestimated a permanent positive technology shock for example. Furthermore, inflation responds more slowly after a fundamental demand shock, decaying after the initially restricted response in quarters three or four.

Even though I restricted only the contemporaneous response of output to the supply noise shock and left the response to the demand noise shock unrestricted, the response of output is expansionary and quite persistent. In contrast to the baseline prediction of the theoretical model, my results for all three countries suggest that demand noise shocks are first weakly expansionary before slowly dying out. The effect of a demand noise shock seems to be strongest in Germany, and French GDP shows a slightly weaker response. The response of Italian GDP is similar in magnitude to the response of French GDP but is statistically insignificant for all periods. The weakly expansionary response of GDP to a demand noise shock stands in contrast to the results of Benhima and Poilly (2021), who find for the US that demand noise shocks are recessionary. The response of the nowcaster errors of output to all shocks die out relatively fast in each country. Comparing the responses of the nowcast errors suggests that informational frictions have a persistent effect on fluctuations in output and inflation in the short run and also in the medium run, while forecasters update their forecasts using new information quickly and do not make persistent mistakes. The responses of the French and Italian nowcast errors for inflation seem to be more volatile, and it takes them longer to die out following both the fundamental supply noise shock and the fundamental demand noise shock. In contrast, the German nowcast error of inflation responses seems to die out very quickly after the initial response on impact.

The more persistent responses of the inflation nowcast errors in France and Italy might indicate that forecasters there are biased toward a different inflation target to that of the German forecasters, making the French and Italian forecast errors more correlated. The accuracy, bias and persistence of forecast errors in Europe is discussed by Fioramanti et al. (2016). They analyse the accuracy of the European Commission’s forecasts, and they also survey the OECD, the IMF, a consensus forecast of market economists, and the ECB forecasts. They find that forecast errors were larger and to a certain degree also more persistent in the crisis and post-crisis period (2008–2014) than in the pre-crisis period (2000–2007). Interestingly, GDP in Germany and Italy seems to react slightly more strongly to noise shocks than French GDP does.

From Table 3, we can see that output volatility is highest in Germany and Italy. Not surprisingly, the variation of the GDP nowcast errors is also highest for Germany and Italy. The maximum German nowcast errors are almost twice as large as the French ones. The quantitative effect on output in response to noise shocks in the empirical model is in that respect consistent with the data.

4.2 Variance decomposition

To find how much noise shocks drive business cycle fluctuations, I compute the variance decomposition using the baseline VAR model. Table 4 shows the results. I find that noise shocks account for about one quarter of the variation in GDP growth. The contribution is fairly similar across the countries, ranging from 23% in Italy and 22% in France to 25% in Germany. The explained variation for output growth is smaller than that obtained by Benhima and Poilly (2021), who find that around 31% of the total fluctuation in output can be explained by noise shocks. In sum, the contribution of supply noise shocks and demand noise shocks to GDP fluctuations is fairly large.

However, supply noise shocks and demand shocks contribute quite differently to the variation, with demand noise shocks driving the variation in output growth in the USA. In the USA, supply noise shocks only explain 8% of GDP growth volatility, while 23% is explained by demand noise shocks. For Germany, the contributions of supply and demand noise shocks do not differ greatly. The results for the European sample in this paper are closer to the findings by Enders et al. (2021), who find that ‘optimism’ shocks, or noise shocks, account for about 20% of short-run output volatility.

The first and the third columns of Table 4 show the unconditional variance decomposition for fundamental shocks. Fundamental supply shocks account for 39% of the volatility in output growth in Germany and for 55% in France, while demand shocks account for 18% in France and for 32% in Germany. In Italy, I find the contribution of fundamental demand shocks to output fluctuations to be around 25%. The estimates for the fundamental demand shocks are also larger than in Benhima and Poilly (2021). Surprisingly, fundamental supply shocks contribute from 25% of inflation volatility in Germany to up to 38% in Italy. This contrasts with the findings of Benhima and Poilly (2021), who report that productivity shocks make only a minor contribution to inflation variance.

The Appendix presents the conditional variance decomposition for France in Fig. 14, for Germany in Fig. 15, and for Italy in Fig. 16. Fundamental supply shocks contribute, by construction, most to GDP over longer horizons. The share of explained variance from other shocks differs across countries, with demand shocks accounting for almost half of the GDP fluctuations in Germany and Italy in the first two to three quarters. The contribution of demand noise shocks starts to increase from the second quarter in France but then levels out quickly. A similar pattern can be observed in Italy. In Germany, however, demand noise shocks explain only a small variation in GDP from the sixth quarter. Clearly, fundamental shocks are the driving force of variations in GDP in the three biggest economies in Europe. This indicates that demand noise shocks play a minor but not insignificant role in explaining variations in short-run GDP; this is a factor that has been neglected in the existing noise-driven business cycle literature. Note however that noise shocks contribute considerably to the variation in inflation in all the countries. Supply noise shocks and fundamental demand shocks explain the bulk of the variation in inflation in Italy and Germany across all horizons. In France, demand noise shocks contribute between 20 and 40% of the variation in inflation starting from quarter five and running until the end of the forecast horizon.

The observed differences in how real GDP growth responds to demand noise shocks in my analysis and in that of Benhima and Poilly (2021) have multiple possible causes. One of them could be that the results are driven by genuine differences in the industry structure that determine the composition of the information set of European firms and US firms. Furthermore, differences in consumer sentiments and demand patterns in the US and in the three European countries might affect the results. Kappler and Aarle (2012) argue that agents may start to frame news in periods when economic sentiments are declining or improving strongly. In doing so, the agents emphasise news that is in line with their individual economic sentiment and downplay news that is not in line with it. As the business cycles and economic sentiment shifts in the USA and the euro area are partly desynchronised during the sample of common observations, we might assume there to be differences in the effects of demand noise shocks.

Additionally, differences in the information set of the European Central Bank (ECB) and the Federal Reserve and differences in how effective the transmission process of monetary policy is might also affect the results. Whereas the Federal Reserve conducts monetary policy for quite a homogeneous set of individual states in the US, the ECB faces a more complex challenge. It has to conduct monetary policy for all parts of the euro area, taking account of the reduced synchronisation between the stages of the business cycle, the institutional differences, the fragmented fiscal frameworks, and the incomplete nature of the financial markets. This all means that the correct stance of monetary policy is different for different parts of the euro area.

Finally, the differences between the results for the three large economies in Europe and those for the USA can also be driven by differences in the sample under observation. Benhima and Poilly (2021) use spans from 1968 to 2017 for their sample, but the data available for Europe are much shorter. The robustness section of Benhima and Poilly (2021) indicates that changing the sample size can change the relative importance of supply noise shocks. The estimation period in my study is dominated by the Great Recession and the European debt crisis, whose long-lasting effects weighed more heavily on European economies than on the USA.

4.3 Historical decomposition

In this section, I analyse the cumulative effects of the set of structural shocks on real GDP growth over the sample period.Footnote 18

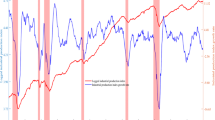

Figure 5 illustrates the use of the historical decomposition in understanding real GDP growth in France from 2004 to 2020. Figures 6 and 7 focus on the role of the structural shocks in explaining real GDP growth in Germany and Italy, respectively.

Historical Decomposition of GDP growth—France. The historical decomposition is obtained by taking the median from the set of all the accepted draws in the baseline SVAR

Historical Decomposition of GDP growth—Germany. The historical decomposition is obtained by taking the median from the set of all the accepted draws in the baseline SVAR

Historical Decomposition of GDP growth—IT. The historical decomposition is obtained by taking the median from the set of all the accepted draws in the baseline SVAR

Variations in real GDP growth in all three countries can mainly be attributed to the effects of fundamental supply shocks. GDP growth in France and Italy was first affected by fundamental supply shocks in the run up to the Great Recession of 2008-2009, while fundamental supply shocks contributed less to real output growth until the first quarter of 2009.

During periods of economic and financial stress, the supply noise shock, and to a lesser degree the demand noise shock, contributed to the negative growth in output. This is particularly visible in the Great Recession of 2008 and 2009. For Italy, supply noise and demand noise shocks also affected output growth from the middle of 2011 to the middle of 2014. This coincides with the European debt crisis which started 2009 in Greece but gained a foothold in other countries such as Ireland, Portugal and particularly Italy from 2010. It seems that Italy experienced a twin fundamental demand shock and noise demand shock that contributed to a decline in output growth. The finding that the effects of supply shocks and demand shocks are fairly persistent during times of financial crisis is in line with papers studying the effects of financial shocks, such as Fornari and Stracca (2012).

Another observation from the historical decomposition is that the effects of positive noise shocks persist for two to three periods before being eclipsed by negative noise shocks in subsequent periods. This is in line with the argument that even though noise shocks can drive economic fundamentals, their effects are short-lived as agents update their information set and learn about the true state of the economy.

5 Robustness tests

In this section, I perform a range of robustness tests. First, I test whether the results depend on the use of year-on-year or quarter-on-quarter nowcast errors. In the second robustness test, I extend the lag length of the VAR. The third robustness test analyses the effects of supply and demand shocks when the latest release nowcast errors are used in the estimation. The figures and tables are presented in the Appendix.

In the baseline specification the nowcast errors of GDP are calculated as the difference between the year-on-year GDP growth rate nowcast and the year-on- year first release estimate of the statistical office. Under the assumption that the GDP growth of the previous three quarters is known to the survey participants, the only uncertainty should stem from the nowcast in the current quarter. That all of the nowcast error stems only and entirely from the misperceptions in the most recent quarter cannot, however, be ruled out. Survey participants could, for example, make errors when summing up the GDP growth of the previous quarters. Therefore, I estimate the VAR model with the GDP nowcaster errors calculated at a quarter-on-quarter frequency rather than a year-on-year frequency. I use the nowcast of quarterly seasonally adjusted GDP growth from Consensus Economics and the first release estimate of quarter-on-quarter GDP growth, which the national statistical office provides in seasonally adjusted form, to calculate the errors. These nowcast errors are then annualised. The other variables in the VAR system, the sample length, and the lag structure remain unaltered.

Figure 17 shows the impulse response functions for France, Fig. 18 shows them for Germany, and Fig. 19 for Italy.

Using the GDP nowcast errors based on quarter-on-quarter estimates does not change the results significantly in France or in Germany. The response of a fundamental demand shock in Italy is slightly more pronounced. A demand shock is still expansionary and all the shocks except the fundamental supply shock are still transitory. Given the observation that the results are stable with respect to the nowcasting reference point, it is possible that the VAR results would not be different for quarter-on-quarter nowcasts for inflation if they were available.

Table 9 in the Appendix shows the unconditional variance decomposition of the model where the GDP nowcast errors are calculated from quarter-on-quarter data. As expected, the results are very similar to the baseline specification. In Italy the variation explained by noise decreases marginally by 3% points but the overall picture remains the same.

Extending the lag length from four lags to eight lags comes closer to the baseline specification of Benhima and Poilly (2021). The effect of using a lag length of eight is shown in Fig. 20 for France, in Fig. 21 for Germany, and in Fig. 22 for Italy.

The responses of GDP growth following fundamental supply, supply noise and demand noise shocks are similar in shape for France. The magnitude however, seems to be larger than in the baseline specification. Surprisingly, a positive fundamental demand shock seems to have contractionary effects on real GDP growth but the results are not statistically significant.

Extending the lag length to eight for Germany leads to more volatile responses in GDP growth following any kind of shock. The shape of the responses is similar to, though more volatile than, that for the baseline specification. Both fundamental supply and supply noise shocks produce impulse responses in GDP growth that are approximately half the size of that in the baseline scenario.

The responses of GDP growth in Italy are even less pronounced than they are in the baseline specification. With a lag length of eight, the response of GDP growth tends to become insignificant following any kind of supply or demand shock.

Table 10 in the Appendix shows the unconditional variance decomposition when the baseline model is estimated with eight lags. With the eight-lag specification, more variation in GDP growth is explained by noise shocks. The variance explained by supply noise and demand noise shocks in France for example is almost twice as large as that in the specification with eight lags. The increase in explained variance is also visible from the conditional variance decomposition. Figure 23 shows the conditional variance decomposition for France. Noise shocks explain around half of the total variance in output growth fluctuations in quarter four to quarter six.

Finally, I analyse the impact of the latest release nowcast errors.Footnote 19 Final release nowcast errors are computed as the difference between the final release estimate of the national statistical office and the Consensus Economics nowcast. The final data published by the statistical offices can contain data revisions that stem from changes to the statistical methodology. Since nowcasters do not always observe the final release data, their information set is influenced by the choice of the data vignette.Footnote 20 Differences between vintage data and final release data might therefore impact econometric estimates (Croushore and Stark 2003).

The impulse response analysis does indeed show that the choice of the data vignette can matter for the statistical inference. Figure 26 illustrates that using final release data from France changes the direction of certain impulse responses. A positive fundamental demand shock leads to a minor increase in GDP growth for three quarters for example, but this is then followed by a contraction in output growth. Equally, a positive fundamental supply shock is followed by a much larger increase in GDP growth. This pattern however is not uniform across countries, and Fig. 26 shows that when final release data are used, a positive supply noise shock tends to increase output growth only slightly but leads to a contraction in output growth that reaches the bottom in quarter six after the shock. A larger response of output growth is also visible for Italy (see Fig. 26). This can partly be explained by the observation that the minimum and maximum nowcast errors tend to be larger for latest release data than for first release data. Using latest release data has no systematic effect on the unconditional variance decomposition (see Table 11). The overall explained variance of noise shocks is very similar to the baseline case. The marginally greater variation in GDP growth in Germany is explained more by fundamental supply shocks than fundamental demand shocks when the latest release data are used.

6 Conclusion

The news view of business cycles provides a framework for understanding how noise shocks can influence expectations about future economic developments and so drive the business cycle even when current fundamentals remain unaltered. There is some evidence for fluctuations in the business cycle being driven by demand noise in the USA, but little is known about how misperceptions of supply and demand affect output and inflation in Europe.

In this paper, I employ the general framework of Benhima and Poilly (2021) to analyse the effects of supply noise shocks and demand noise shocks in three major European economies. An SVAR model is estimated in order to disentangle noise shocks from fundamental shocks. One key component of the empirical identification strategy is nowcast errors, which are computed from the nowcasts of participants in the Consensus Economics survey and the first release estimates of GDP growth and consumer price inflation provided by the national statistical offices.

The main conclusions are as follows. First, I provide evidence of expansionary effects on output from both supply noise shocks and demand noise shocks in all three countries. The response is more pronounced in Germany and Italy than in France. The response of GDP growth and inflation to a supply noise shock is observationally similar to their response following a demand shock. That observation has already been pointed out by Lorenzoni (2009). Benhima and Poilly (2021) have argued that the reverse conclusion should also hold. Negative demand noise shocks should create an observationally similar response in output to that of fundamental supply shocks. The analysis of the three European samples, however, does not support this hypothesis. Positive demand noise shocks lead to an expansionary response in output in all three countries, though the response is statistically insignificant in Italy.

Second, the results of the variance decomposition show that supply noise and demand noise contribute to very similar degrees in explaining the volatility in output growth at business cycle frequencies. The joint contribution amounts to around 24% with no notable differences across countries.

The historical decomposition provides some tentative evidence that noise shocks had some fairly large and persistent effects on output growth during periods of economic and financial stress. This seems particular pronounced in the case of Italy, which was not only affected in the Great Recession but also by the European debt crisis.

The observed differences in how real GDP growth responds to demand noise shocks in my analysis and in that of Benhima and Poilly (2021) can have multiple causes. Differences in industry structure and differences between the US and Europe in the information set of monetary policy makers may be one factor driving the difference in the results. Another factor that may explain the difference in results is that the US sample covers important macroeconomic episodes such as the Great Moderation in the USA that might influence the relative importance of fundamental and noise shocks. In this spirit, the magnitude and duration of the Great Recession and the European debt crisis might also weigh on how output growth reacts to noise shocks. I leave further investigation of these issues to future research.

Notes

Empirical evidence suggests that households reacts to news to form expectations about future price changes (Wang et al. 2020). Further evidence suggests that households sometimes overreact when updating inflation news depending on the source of the news and household demographics (Easaw et al. 2013).

The results of Forni and Gambetti (2014) indicate that news shocks have a smaller role in explaining business cycle fluctuations, which contrasts with the findings of Beaudry and Portier (2006). In more recent work, Nam and Wang (2019) also use a larger VAR system but use sign restrictions to identify what they call ‘optimism’ shocks. Their results show that their optimism shocks resemble news shocks in the response they get from total factor productivity (TFP), consumption, investment and output.

While the reduced form model of Benhima and Poilly (2021) features a combined structure of incomplete and noisy information, most of the literature emphasises that incomplete news and wrong news usually stem from distinct information structures. The case when the news can be wrong is usually referred to as noise formulation (Beaudry and Portier, 2014).

Demand noise shocks in the model can be influenced by misperceptions about prices. This links the model to the growing literature on the impact of macroeconomic news on the spending and investment decisions of agents.

For firms, Coibion et al. (2020) use Italian survey data to study the causal effects of inflation exceptions. They show that changes in firms inflation expectations affect investment and employment. In a another study, Coibion et al. (2022) analyse the results from a randomised control experiment on inflation news. They find that treated households who receive targeted news about inflation change their inflation expectations and change their spending and saving behaviour.

The nexus of monetary policy, supply and demand shocks and animal spirits is also discussed in, for example, Sheen and Wang (2016). They argue that a central bank needs to be concerned about possible animal spirit expectations in particular when technology shocks are prevalent. Misidentifying true animal spirits as rational expectations can have potentially high costs as it can impose a sub-optimal monetary policy rule.

Public signal refers in the context of this theoretical model to public information about technology or preferences that agents receive.

In the baseline case of the theoretical model by Benhima and Poilly (2021), the central bank follows a Taylor rule with zero weight on the output. This means that the central bank only has an inflation target.

Consumers and firms do not share the same information set. The information set of both agents is made up of potentially noisy public signal and private signals of demand and supply shocks.

Firms are better able to detect noise shocks than the central bank when the precision of the private signal they receive is high relative to that of the public signal that is shared by both the firms and the central bank.

Note that the effect on the survey expectations error is conditional on the model being specified so that agents receive a private signal. Without a private signal, fundamental supply and supply noise shocks have no effect on the survey expectation error for output, and fundamental demand and demand noise shocks have no effect on the survey expectation error for inflation.

Altering the information set of the econometrician to address the problem of potential non-invertibility is done in many studies of how expectations affect economic fluctuations. For example, studies by Chung and Leeper (2007), Romer and Romer (2010), Ramey and Vine (2011) and Leeper et al. 2013 add additional variables to the model to align the information set used by the econometrician and the agents in the context of fiscal policy analysis.

Without the restrictions on the expectational errors, a temporary supply shock such as an oil price shock could, for example, be confused with either of the demand shocks.

The SPF is also frequently used as the benchmark for assessing forecasting models (Giannone et al. 2008).

The Federal Reserve Bank of Philadelphia conducts the survey of professional forecasters for the USA. For Europe, the European Central Bank Survey of Professional Forecasters (ECB SPF) collects information on expected rates of inflation, real GDP growth and other macroeconomic variables in the euro area at several horizons (Garcia 2003). The ECBs SPF is publicly available and widely used in the forecasting domain, but the survey design differs too strongly from that of the US SPF to be useable for our purposes. First, it is only available for the euro area but not for individual countries, and more importantly it does not provide nowcasts for the current quarter but only forecasts for longer horizons.

To calculate the nowcast errors I also need the first release data for GDP growth and inflation for our set of countries. The length of my sample is restricted not only by the availability of the Consensus Economics nowcasts but also by the availability of the published first release data.

For Germany, for example, those pollsters include the German Econ Institute, Allianz insurance, Goldman Sachs and Deutsche Bank. For Italy, they include ABI, Centro Europa Ricerche, Confindustria and UniCredit. For France, they include Societe Generale, Euler Hermes, OFCE and Capital Economics.

Disaggregated data are available for the US SPF. Researchers tend to use median nowcast errors in their models as they are less prone to outliers than the mean nowcast errors (Enders et al. 2021).

The historical decompositions for the inflation rate are available upon request.

Latest release data represents the last published data for a data point. In most cases this will be the final release data from the statistical office, ex post data revisions are also part of the final release data.

In my analysis nowcasters might not observe the final release data for the real GDP growth of the previous quarter. Similarly, nowcasters have a larger information set when forming expectations about the year-on-year consumer price inflation rate, but they previous quarter year-on-year inflation rate might be subject to data revisions.

References

Akerlof GA, Shiller RJ (2010) Animal spirits: how human psychology drives the economy, and why it matters for global capitalism. Princeton University Press

Arias JE, Rubio-Ramírez JF, Waggoner DF (2018) Inference based on structural vector autoregressions identified with sign and zero restrictions: theory and applications. Econometrica 86(2):685–720

Armantier O, Quah D (1989) The dynamic effects of aggregate demand and supply disturbances. Am Econ Rev 19:655–673

Bacchetta P, Van Wincoop E (2013) Sudden spikes in global risk. J Int Econ 89(2):511–521

Barsky RB, Basu S, Lee K (2015) Whither news shocks? NBER Macroecon Ann 29(1):225–264

Barsky RB, Sims ER (2012) Information, animal spirits, and the meaning of innovations in consumer confidence. Am Econ Rev 102(4):1343–1377

Beaudry P, Lucke B (2010) Letting different views about business cycles compete. NBER Macroecon Ann 24:413–456

Beaudry P, Portier F (2006) Stock prices, news, and economic fluctuations. Am Econ Rev 96(4):1293–1307

Beaudry P, Portier F (2014) News-driven business cycles: insights and challenges. J Econ Lit 52(4):993–1074

Benhabib J, Liu X, Wang P (2016) Sentiments, financial markets, and macroeconomic fluctuations. J Financ Econ 120(2):420–443

Benhima K, Poilly C (2021) Does demand noise matter? Identification and implications. J Monet Econ 117:278–295

Blanchard O, L’Huillier J-P, Lorenzoni G (2013) News, noise, and fluctuations: an empirical exploration. Am Econ Rev 103(7):3045–3070

Brzoza-Brzezina M, Kotłowski J, Wesołowski G (2020) International information flows, sentiments, and cross‐country business cycle fluctuations. Rev Int Econ

Chung H, Leeper EM (2007) What has financed government debt? w13425. National Bureau of Economic Research, p 38

Coibion O, Gorodnichenko Y, Ropele T (2020) Inflation expectations and firm decisions: new causal evidence*. Q J Econ 135(1):165–219

Coibion O, Gorodnichenko Y, Weber M (2022) Monetary policy communications and their effects on household inflation expectations. J Polit Econ 130(6):1537–1584

Croushore D (2010) An evaluation of inflation forecasts from surveys using real-time data. BE J Macroecon 10(1)

Croushore D, Stark T (2003) A real-time data set for macroeconomists: does the data vintage matter? Rev Econ Stat 85(3):605–617

Dräger L, Lamla MJ (2017) Imperfect information and consumer inflation expectations: evidence from microdata. Oxford Bull Econ Stat 79(6):933–968

Easaw J, Golinelli R, Malgarini M (2013) What determines households inflation expectations? Theory and evidence from a household survey. Eur Econ Rev 61:1–13

Enders Z, Kleemann M, Müller GJ (2021) Growth expectations, undue optimism, and short-run fluctuations. Rev Econ Stat 103(5):905–921

Farmer REA (1999) The macroeconomics of self-fulfilling prophecies. MIT Press

Farmer REA (2012a) Confidence, crashes and animal spirits. Econ J 122(559):155–172

Farmer REA (2012b) The stock market crash of 2008 caused the great recession: theory and evidence. J Econ Dyn Control 36(5):693–707

Fioramanti M, Cabanillas LG, Roelstraete B (2016) European commission’s forecasts accuracy revisited: statistical properties and possible causes of forecast errors. Available at SSRN 2753854

Fornari F, Stracca L (2012) What does a financial shock do? First international evidence. Econ Policy 27(71):407–445

Forni M, Gambetti L (2014) Sufficient information in structural VARs. J Monet Econ 66:124–136

Forni M, Gambetti L, Sala L (2014) No news in business cycles. Econ J 124(581):1168–1191

Fujiwara I, Hirose Y, Shintani M (2011) Can news be a major source of aggregate fluctuations? A Bayesian DSGE approach. J Money, Credit Bank 43(1):1–29

Galí J (2015) Monetary policy, inflation, and the business cycle: an introduction to the new Keynesian framework and its applications. Princeton University Press

Garcia JA (2003) An introduction to the ECB’s survey of professional forecasters. ECB Occas Pap 8:40

Giannone D, Reichlin L, Small D (2008) Nowcasting: the real-time informational content of macroeconomic data. J Monet Econ 55(4):665–676

Hamilton JD (2020) Time series analysis. Princeton University Press

Kamber G, Theodoridis K, Thoenissen C (2017) News-driven business cycles in small open economies. J Int Econ 105:77–89

Kappler M, van Aarle B (2012) Economic sentiment shocks and fluctuations in economic activity in the euro area and the USA. Intereconomics 2012(1):44–51

Keynes JM (1936) The general theory of unemployment. Interest and Money, Harcourt Brace, London

Kurmann A, Mertens E (2014) Stock prices, news, and economic fluctuations: comment. Am Econ Rev 104(4):1439–1445

Kurmann A, Otrok C (2013) News shocks and the slope of the term structure of interest rates. Am Econ Rev 103(6):2612–2632

Leeper EM, Walker TB, Susan Yang S-C (2013) Fiscal foresight and information flows. Econometrica 81(3):1115–1145

Lorenzoni G (2009) A theory of demand shocks. Am Econ Rev 99(5):2050–2084

Milani F (2011) Expectation shocks and learning as drivers of the business cycle. Econ J 121(552):379–401

Miyamoto W, Nguyen TL (2014) News shocks and business cycles: evidence from forecast data. Society for Economic Dynamics, Meeting Papers 259

Nam D, Wang J (2019) Mood swings and business cycles: evidence from sign restrictions. J Money, Credit Bank 51(6):1623–1649

Pigou AC (1929) Industrial fluctuations. Macmillan

Ramey VA, Vine DJ (2011) Oil, automobiles, and the us economy: How much have things really changed? NBER Macroecon Ann 25(1):333–368

Romer CD, Romer DH (2010) The macroeconomic effects of tax changes: estimates based on a new measure of fiscal shocks. Am Econ Rev 100(3):763–801

Sheen J, Wang BZ (2016) Animal spirits and optimal monetary policy design in the presence of labour market frictions. Econ Model 52:898–912

Wang BZ et al (2020) A note on the impact of news on US household inflation expectations. Macroecon Dyn 24(4):995–1015

Acknowledgements

The author thanks Karsten Staehr, Lenno Uusküla, Michael Funke and the participants in the PhD seminar at TalTech for helpful comments. I also thank Kenza Benhima and Céline Poilly for sharing their code for the SVAR estimation. The views expressed in this paper are those of the author and do not necessarily represent the official views of Eesti Pank or the Eurosystem. Any remaining errors are mine. This research project has received funding from the ASTRA “TTÜ arenguprogramm aastateks 2016-2022” programme under the Doctoral School in Economics and Innovation Project code: 2014-2020.4.01.16-0032

Funding

The research leading to these results received funding from the STRA “TTÜ arenguprogramm aastateks 2016–2022” Doctoral School in Economics and Innovation Project under Grant Agreement No. 2014-2020.4.01.16-0032.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The author has no conflicts of interest to declare that are relevant to the content of this article.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendices

1.1 A Data and description

See Appendix Figs.

Nowcast and official first release data—France. The solid red line shows the first release value provided by the national statistical office. The dotted turquoise line shows the mean nowcast for the current quarter provided by Consensus Economics

8,

Nowcast and official first release data—Germany. The solid red line shows the first release value provided by the national statistical office. The dotted turquoise line shows the mean nowcast for the current quarter provided by Consensus Economics

9,

Nowcast and official first release data—Italy. The solid red line shows the first release value provided by the national statistical office. The dotted turquoise line shows the mean nowcast for the current quarter provided by Consensus Economics

10,

Nowcast errors based on first and final release data—France. The first release nowcast errors are calculated as the difference between the Consensus Economics survey nowcast and the first release data of the national statistical office. The final release nowcast errors are calculated as the difference between the Consensus Economics survey nowcast and the latest available data of the national statistical office. All data are in annualised terms

11,

Nowcast errors based on first and final release data—Germany. The first release nowcast errors are calculated as the difference between the Consensus Economics survey nowcast and the first release data of the national statistical office. The final release nowcast errors are calculated as the difference between the Consensus Economics survey nowcast and the latest available data of the national statistical office. All data are in annualised terms

12 and

Nowcast errors based on first and final release data—Italy. The first release nowcast errors are calculated as the difference between the Consensus Economics survey nowcast and the first release data of the national statistical office. The final release nowcast errors are calculated as the difference between the Consensus Economics survey nowcast and the latest available data of the national statistical office. All data are in annualised terms

13 and Table

5,

6,

7 and

8.

1.2 B SVAR Analysis

See Appendix Figs.

Conditional variance decomposition of real GDP and inflation—France

14,

Conditional variance decomposition of real GDP and inflation—Germany

15 and

Conditional variance decomposition of real GDP and inflation—Italy

16.

1.3 C Robustness

1.3.1 C.1 Robustness: GDP quarter-on-quarter nowcast errors

See Appendix Figs.

IRF Robustness—France. The nowcast error of GDP is calculated from the quarter on quarter nowcast and the quarter on quarter first release estimate of the national statistical office. The solid lines depict the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

17,

IRF Robustness—Germany. The nowcast error of GDP is calculated from the quarter on quarter nowcast and the quarter on quarter first release estimate of the national statistical office. The solid lines depict the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

18 and

IRF Robustness—Italy. The nowcast error of GDP is calculated from the quarter on quarter nowcast and the quarter on quarter first release estimate of the national statistical office. The solid lines depict the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

19 and Table

9.

1.3.2 C.2 Robustness: lag length 8 quarters.

See Appendix Figs.

IRF Robustness: 8 Lags—France. The solid lines show the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

20,

IRF Robustness: 8 Lags—Germany. The solid lines show the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

21,

IRF Robustness: 8 Lags—Italy. The solid lines show the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

22,

Conditional variance decomposition of real GDP and inflation for Lag length 8—France

23,

Conditional variance decomposition of real GDP and inflation for Lag length 8—Germany

24, and

Conditional variance decomposition of real GDP and inflation for Lag length 8—Italy

25 and Table

10.

1.3.3 C.3 Robustness: final release nowcast errors.

See Appendix Figs.

IRF Robustness: Final release Nowcast Errors—France. The solid lines show the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

26,

IRF Robustness: Final release Nowcast Errors—Germany. The solid lines show the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

27,

IRF Robustness: Final release Nowcast Errors—Italy. The solid lines show the median impulse responses function. The 16th and 84th percentile confidence regions are marked by the dotted lines

28,

Conditional variance decomposition of real GDP and inflation based on final release data—France

29,

Conditional variance decomposition of real GDP and inflation based on final release data—Germany

30, and

Conditional variance decomposition of real GDP and inflation based on final release data—Italy

31 and Table

11.

Rights and permissions

About this article

Cite this article

Reigl, N. Noise shocks and business cycle fluctuations in three major European Economies. Empir Econ 64, 603–657 (2023). https://doi.org/10.1007/s00181-022-02272-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-022-02272-y