Abstract

From an asset pricing point of view the excess return of housing over the risk free rate is negatively related to the covariance between the gross housing return rate and the stochastic discount factor. Under log-normality regularity conditions, current return premiums would require an extremely volatile stochastic discount factor, as a consequence of the observed variability of real gross housing returns. We analyse the volatility bound noticing, that the logarithmic transformation of the rent/price ratio is, respectively, negatively and positively related to subsequent real rent growth and housing return rates. In predictive regressions the logarithmic transformation of the rent/price ratio is positively and significantly correlated to subsequent excess return rates and to gross housing return volatility, at horizons of 4–16 quarters. These results are robust to the specification of the regressions conditioning variables. Further analysis with a sign identified structural vector autoregression model shows that shocks to the rent/price ratio take several quarters to be completely realized and have persistent effects on real rent growth and interest rates, which last for more than 15 years. Moreover, the logarithmic rent/price ratio forecasts in each time period both forthcoming rent growth and gross housing return rates.

Similar content being viewed by others

Availability of data and materials

The datasets of this study (data, programs and documentation files) are available in the Mendeley repository, https://doi.org/10.17632/d7bbr5t5ys.1.

Notes

We use throughout small case letters in order to represent the natural logarithm of a variable. The conditional variance and covariance are defined in terms of the conditional expectation operator as \(VAR_{t}\left[ x\right] =E_{t}\left[ x -E_{t}\left( x\right) \right] ^{2}\) and \(COV_{t}\left[ x ,y\right] =E_{t}\left[ x -E_{t}\left( x\right) \right] \left[ y -E_{t}\left( y\right) \right] \), for any two stochastic variables x and y. We assume conditional variances and covariances are constant and hence equal to unconditional ones.

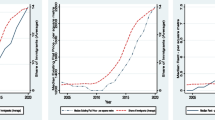

With \(P_{t}\) and \(N_{t}\) denoting real housing price and rent indices, the gross housing return between periods t and \(t +1\) can be defined as \(1 +R_{t +1} =\left( P_{t +1} +\psi N_{t +1}\right) /P_{t}\) and the rent/price ratio in period t as \(\psi N_{t}/P_{t}\), where \(\psi =N_{0}/P_{0}\) is the rent/price ratio in the base period.

The ADF tests accept the null hypothesis of a unit root for the real price variable in levels and first differences, as well as for the real gross housing return, the excess real gross returns on Treasury bill and bond rates, the term spread and the logarithmic rent/price ratio. We base our analysis on the PP tests, since the outcomes of the ADF tests might be due to the presence of seasonal patterns in the data.

In the calculations of the gross housing excess rate of return we account for the effect of Jensen’s inequality. Moreover, we assume Treasury bill and bond rates are equal to the sum of the risk-free rate and a term premium of the same order of magnitude as the depreciation rate.

We use a variable subscript to define the first and second derivatives of the single period utility function with respect to each consumption component.

Following the evidence for the equity premium presented in Mehra and Prescott (1985) alternative representations have been based on the assumption of recursive preferences or habit formation. In the present framework an essential assumption is the weak separability between non-housing and housing consumption, since with strictly separable preferences in normal conditions the observed volatility of consumption would entail extremely high relative risk aversion coefficients.

The same order is indicated by the Akaike, Schwarz and Hannan–Quinn criteria and the final prediction error.

The spectral decomposition of the covariance matrix \(\Omega =X\Lambda X^{ \prime }\), where \(\Lambda =diag\left( \lambda _{1} ,\ldots ,\lambda _{n}\right) \) is the matrix with the eigenvalues of \(\Omega \) in the principal diagonal and X is the corresponding matrix of eigenvectors, could be used as an alternative to define a model with orthogonal structural disturbances. Since \(\Omega \) is a symmetric positive definite matrix, the eigenvalues are real and positive and the matrix of eigenvectors is orthogonal. The structural representation corresponding to this case would set \(B_{0} =X^{ \prime }\) and \(\Sigma =\Lambda \). We are less interested in the spectral decomposition, as it is generally used in principal components analysis.

A square matrix Q of order n is orthogonal when \(QQ^{ \prime } =Q^{ \prime }Q =I\). Assuming \(\Sigma =I\), for any structural matrix \(B_{0}\) for which \(\Omega =B_{0}^{ -1}\left( B_{0}^{ -1}\right) ^{ \prime }\), it follows that \(\Omega =B_{0}^{ -1}Q^{ \prime }Q\left( B_{0}^{ -1}\right) ^{ \prime }\). The structural matrix \(B_{1}\) can be identified from the reduced form matrix A, \(B_{0}\) and Q: \(A =B_{0}^{ -1}Q^{ \prime }B_{1}\).

The search over the space of orthogonal matrices \({\mathcal {Q}}\) can be performed using several methods. For instance, one could sample randomly over the space of square matrices of order n and then use a QR decomposition, in order to calculate the orthogonal matrix corresponding to each draw. When the elements of the sampling square matrix are independent and identically distributed as standard normal variables, the orthogonal matrix resulting from the QR decomposition has a uniform distribution over the space of orthogonal matrices \({\mathcal {Q}}\). Rubio-Ramírez et al. (2010) argue that this procedure might turn out to be more efficient than grid search, as the number of endogenous variables in the VAR increases. We provide a description of the method of Jacobi rotations in Appendix A.

The ratio is approximately equal to one around the 80th percentile of the rank ordering by the sum of cumulative responses.

References

Alvarez F, Jermann UJ (2005) Using asset prices to measure the persistence of the marginal utility of wealth. Econometrica 73(6):1977–2016

Blanchard OJ, Quah D (1989) The dynamic effects of aggregate demand and supply disturbances. Am Econ Rev 79(4):655–673

Canova F, De Nicoló G (2002) Monetary disturbances matter for business fluctuations in the G-7. J Monet Econ 49(6):1131–1159

Case KE, Shiller RJ (1989) The efficiency of the market for single-family homes. Am Econ Rev 79(1):125–137

Case KE, Shiller RJ (2003) Is there a bubble in the housing market? Brook Pap Econ Act 2003(2):299–342

Case KE, Quigley JM, Shiller RJ (2013) Wealth effects revisited 1975–2012. Crit Finance Rev 2(1):101–128

Case KE, Shiller RJ, Thompson AK (2012) What have they been thinking? Homebuyer behavior in hot and cold markets. Brookings Papers on Economic Activity, Fall, pp 265–298

Case KE, Shiller RJ, Thompson AK (2014) What have they been thinking? Homebuyer behavior in hot and cold markets—a 2014 update. Cowles Foundation discussion paper no. 1876R, March

Deaton AS (1992) Understanding consumption. Oxford University Press, Oxford

Dickey DA, Fuller WA (1979) Distribution of the estimators for autoregressive time series with a unit root. J Am Stat Assoc 74(366):427–431

Fabozzi FJ (2008) Asset pricing models. In: Fabozzi FJ (ed) Handbook of finance, vol II. Wiley, Hoboken, pp 15–23

Fabozzi FJ, Markowitz HM, Gupta F (2008) Portfolio selection. In: Fabozzi FJ (ed) Handbook of finance, vol II. Wiley, Hoboken, pp 3–13

Hansen LP, Jagannathan R (1991) Implications of security market data for models of dynamic economies. J Polit Econ 99(2):225–262

Hansen LP, Richard SF (1987) The role of conditioning information in deducing testable restrictions implied by dynamic asset pricing models. Econometrica 55(3):587–613

King RG, Plosser CI, Stock JH, Watson MW (1991) Stochastic trends and economic fluctuations. Am Econ Rev 81(4):819–840

Mehra R, Prescott EC (1985) The equity premium: a puzzle. J Monet Econ 15(2):145–161

Muellbauer J (2012) When is a housing market overheated enough to threaten stability? In: Heath A, Packer F, Windsor C (eds) Property markets and financial stability. Reserve Bank of Australia, Sydney, pp 73–105

Muellbauer J (2016) Macroeconomics and consumption. Discussion paper series no. 811, University of Oxford, Department of Economics

Phillips PCB, Perron P (1988) Testing for a unit root in time series regression. Biometrika 75(2):335–46

Piazzesi M, Schneider M, Tuzel S (2007) Housing, consumption and asset pricing. J Financ Econ 83(3):531–569

Rubio-Ramírez JF, Waggoner DF, Zha T (2010) Structural vector autoregressions: theory of identification and algorithms for inference. Rev Econ Stud 77(2):665–696

White H (1980) A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica 48(4):817–838

Funding

The research leading to the present study did not receive any funding.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The author does not have any affiliation with or involvement in any organization or entity with any financial or non-financial interest in the subject matter of this manuscript.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The views expressed herein are those of the author and do not necessarily reflect those of the Bank of Italy.

Sign identification method

Sign identification method

We describe the method of sign identification with Jacobi rotations for the n-dimensional case.

An n-dimensional Jacobi rotation matrix takes the form:

The matrix \(Q_{ij}\left( \theta _{ij}\right) \text {}\) in Eq. (A.1) is obtained from the identity matrix replacing elements i, i and j, j with \(\cos \theta _{ij}\), element i, j with \( -\sin \theta _{ij}\) and element j, i with \(\sin \theta _{ij}\), where \(0 \le \theta _{ij} \le 2\pi \). Using the prosthaphaeresis formulas it can be shown that multiplying an n-dimensional row vector \(x =\left( x_{1} ,\ldots ,x_{n}\right) \) by a matrix \(Q_{ij}\left( \theta _{ij}\right) \) determines a clockwise rotation in the plane of its i, j-th components by an angle equal to \(\theta _{ij}\). Moreover, it is straightforward to verify that \(Q_{ij}\left( \theta _{ij}\right) \) is orthogonal: \(Q_{ij}\left( \theta _{ij}\right) Q_{ij}\left( \theta _{ij}\right) ^{ \prime } =Q_{ij}\left( \theta _{ij}\right) ^{ \prime }Q_{ij}\left( \theta _{ij}\right) =I\). This in turn implies, that the matrix:

is orthogonal.

The space \({\mathcal {Q}} \equiv \left\{ Q :QQ^{ \prime } =Q^{ \prime }Q =I\right\} \) of orthogonal matrices of order n is identified by matrices that take the form (A.2), with \(0 \le \theta _{ij} \le \pi \) for \(i ,j =1 ,\ldots ,n\), \(j >i\).

For the analysis in the present work we performed a grid search over the space of orthogonal matrices of order 3. We used for each \(\theta _{ij}\), for \(i ,j =1 ,\ldots ,3\), a zero initial value and a step equal to \(\pi /50\). The search procedure allowed us to identify 1462 models. The analysis in the main text uses the first 1000 identified models.

Rights and permissions

About this article

Cite this article

Tomat, G.M. An asset-based approach to housing prices. Empir Econ 63, 265–286 (2022). https://doi.org/10.1007/s00181-021-02140-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-021-02140-1