Abstract

This paper investigates the impact of active balance sheet adjustments in the non-financial corporate sector on economic growth in the EU. We jointly model firms’ ability to reduce their balance sheet imbalances and a growth equation in an instrumental variables (IV) panel context. This enables us to explicitly consider the contemporaneous interaction between corporate balance sheet adjustment and growth, which can otherwise bias inference. Our main findings inter alia suggest that periods of active corporate deleveraging are associated on average with lower output growth compared to periods when no adjustment takes place. Moreover, a decline in corporate debt overhang supports output growth. Model-based simulations are in line with these findings.

Similar content being viewed by others

Notes

Passive deleveraging could also be coupled with moderate positive credit flows (see Pontuch 2014).

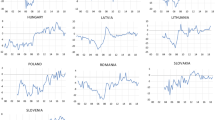

Figure 1 in the Appendix presents the evolution of the net lending/borrowing (NLB) position of firms and the net lending/borrowing to GDP ratio per country over the period 1995–2015.

Improvements in the corporate sector`s NLB position are directly associated with active deleveraging, namely with negative credit flows which tend to drive down the stock of debt-to-GDP ratio (see e.g. Pontuch 2014).

Real GDP per capita is commonly employed in the empirical literature on economic growth. It accounts for income diversity between economies (see e.g. Temple 1999) and is considered a more reliable measure of a country’s economic state. In most developed economies, where population grows at a low rate, the difference between real GDP and real GDP per capita is minor.

A more appropriate proxy of balance sheet strength would be the ratio of net worth-to-total assets, which includes both financial and non-financial assets, and liabilities. However, due to lack of data for non-financial assets of non-financial corporations, we employ financial net worth, which is the difference between financial assets and financial liabilities.

Following the literature on the transmission of monetary policy to the economy, we employ the lagged (change in the) real short-term interest rate. Empirical studies substantiate that the full pass-through of changes in monetary policy on real GDP ranges between four and six quarters in the euro area (ECB 2000, 2010).

Excluded instruments are exogenous variables that do not enter the equation to be estimated, but are included in the other equations of the system. First-stage regressions are reduced form regressions of the endogenous variables both on the (excluded) instruments and the exogenous variables included in the equation to be estimated (see also Baum et al. 2003).

It should be noted that by using IV estimation techniques, when the null hypothesis that the specified endogenous variables can be treated as exogenous is accepted, there is a loss in terms of efficiency in the estimation (i.e. the asymptotic variance of the IV estimator is large). However, using OLS when endogeneity is present should imply a greater loss, namely in terms of consistency.

Given the caveat discussed in Sect. 2.2 of the linear probability model, our discussion remains mainly qualitative.

We repeated the estimation of the balance sheet adjustment equation for this subset of countries. Indeed, the sign of financial net worth-to-assets ratio turns now negative, suggesting that higher financial net worth is associated with higher corporate investment and/or lower savings, probably reflecting financial constraints.

Developments in credit growth are underlined by both credit supply and credit demand developments. In this paper, the aim is not to distinguish the impacts of credit supply and credit demand. We control, however, for aggregate credit growth, meaning that a decline in credit growth would signal on average lower credit stemming from the bank lending channel.

Our estimates are based on heteroskedasticity- and autocorrelation-consistent (HAC) standard errors. These are obtained by using the Newey and West (1987) Bartlett kernel function with the kernel function`s bandwidth set to T1/3, where T is the number of time periods. Given our unbalanced panel, we set the bandwidth equal to 2.

The (exogenous) threshold dummy allows to partly capture nonlinear effects amid a state of higher/lower household debt (compared to average linear impacts captured by a household debt overhang covariate).

Still, the pairwise correlations of the corporate balance sheet variables are well below 0.5.

In exactly identified models, Hansen's J statistic that formally tests the exclusion restrictions on the instruments cannot be computed.

Although the null hypothesis of the Sanderson-Windemeijer test that the coefficients of the instruments are jointly zero in the first-stage IV regression cannot be accepted, still the F statistic is slightly lower than the rule-of-thumb value of 10 (see Section 6 in the “Appendix”). Hence, estimates of the growth equation should be considered with caution.

Additional estimations have also been performed for the sub-sample of non-euro area countries. However, given our unbalanced panel dataset, the available degrees of freedom decrease substantially, rending all coefficient estimates statistically insignificant. Indeed, the finite-sample properties of IV estimators may be problematic and the performance of IV estimators in small samples may be poor (see e.g. Baum et al. 2003).

See also Kitsios and Patnam (2016) for a similar approach.

References

Abiad AG, Dell’Ariccia G, Li B (2011) Creditless recoveries. IMF working paper 11/58

Alesina A, Ardagna S (2010) Large changes in fiscal policy: taxes versus spending. In: Brown JR (ed) Tax policy and the economy, vol 24. National Bureau of Economic Research, Cambridge

Angrist DJ (2001) Estimation of limited dependent variable models with dummy endogenous regressors. J Bus Econ Stat 19(1):2–28

Angrist DJ, Pischke JS (2009) Mostly harmless econometrics: an empiricist`s companion. Princeton University Press, Princeton

Baum CF, Schaffer ME, Stillman S (2003) Instrumental variables and GMM: estimation and testing. Stata J 3(1):1–31

Baum CF, Schaffer ME, Stillman S (2007) Enhanced routines for instrumental variables/generalised method of moments estimation and testing. Stata J 7(4):465–506

Bijsterbosch M, Dahlhaus T (2011) Determinants of credit-less recoveries. ECB working paper No. 1358

Bornhorst F, Ruiz-Arranz M (2013) Indebtedness and deleveraging in the Euro area. Euro area policies, 2013 article IV consultation selected issues, IMF country report 13/232

Breusch T, Qian H, Schmidt P, Wyhowski D (1999) Redundancy of moment conditions. J Econom 91(1):89–111

Bricongne J-C, Mordonu AM (2015) Interlinkages between household and corporate debt in advanced economies. European Commission, European economy discussion paper no. 017

Bricongne J-C, Demertzis M, Pontuch P, Turrini A (2016) Macroeconomic relevance of insolvency frameworks in a high-debt context: an EU perspective. European Commission, discussion paper no. 032

Calvo GA, Izquierdo A, Talvi E (2006) phoenix miracles in emerging markets: recovering without credit from systemic financial crisis. NBER working paper no. 12101

Cecchetti SG, Mohanty MS, Zampolli F (2011) The real effects of debt. BIS working papers no. 352 (Basel)

Çelik S, Demirtaş G, Isaksson M (2019) Corporate bond markets in a time of unconventional monetary policy. OECD Capital Market Series, Paris

Chen, S., Kim, M., Otte, M.., Wiseman, K.. and A., Zdzienicka (2015). Private sector deleveraging and growth following busts. IMF Working Paper WP/15/35

Claessens S, Kose MA, Terrones M (2008) What happens during recessions, crunches and busts. IMF working paper no. 08/274

Diamond WD, He Z (2014) A theory of debt maturity: the long and short of debt overhang. J Finance 69(2):719–762

European Central Bank (ECB) (2000). The interest rate transmission mechanism in the euro area: methodologies and an illustration. ECB Monthly Bulletin July 2000

European Central Bank (ECB) (2010) Monetary policy transmission in the euro area, a decade after the introduction of the euro. ECB Monthly Bulletin May 2010

European Commission (2017) Analysis of European corporate bond markets. Report from the commission expert group on corporate bonds

Goretti M, Souto M (2013) Macro-financial implications of corporate (de)leveraging in the euro area periphery. IMF working paper WP/13/154

Greene W (2000) Econometric analysis, 4th edn. Prentice-Hall, Upper Saddle River

Guajardo J, Leigh D, Pescatori A (2011) Expansionary austerity: new international evidence. IMF working paper WP/11/158

Hahn J, Hausman J (2002) Note on bias in estimators for simultaneous equation models. Econ Lett 75(2):237–241

Hahn J, Hausman J, Kuersteiner G (2004) Estimation with weak instruments: accuracy of higher-order bias and MSE approximations. Econ J 7(1):272–306

Hansen L (1982) Large sample properties of generalized method of moments estimators. Econometrica 50(3):1029–1054

Hansen L, Heaton J, Yaron A (1996) Finite sample properties of some alternative GMM estimators. J Bus Econ Stat 14(3):262–280

Kalemli-Özcan Ş, Laeven L, D Moreno (2019) Debt overhang, rollover risk and corporate investment: evidence from the European crisis. ECB working paper series no. 2241

Kitsios E, Patnam M (2016) Estimating fiscal multipliers with correlated heterogeneity. IMF working paper WP/16/13

Kleibergen F, Paap R (2006) Generalized reduced rank tests using the singular value decomposition. J Econ 127(1):97–126

Laeven L, Valencia F (2012) Systemic banking crises database: an update. IMF working paper WP/12/163

Lancaster T (2000) The incidental parameters problem since 1948. J Econ 95(2):391–413

Cuerpo X, Drumond I, Lendvai J, Pontuch P, Raciborski R (2013) Indebtedness, deleveraging dynamics and macroeconomic adjustment. European Commission, European economy economic papers no. 477

Lombardi M, Mohanty M, Shim I (2017) The real effects of household debt in the short and long run. BIS working papers no. 607

Mian RA, Sufi A, Verner E (2015) Household debt and business cycles worldwide. NBER working paper no. 21581

Myers CW (1977) Determinants of corporate borrowing. J Financ Econ 5(2):147–175

Newey WK, West KD (1987) A simple, positive-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 55(3):703–708

Occhino F (2010) Is debt overhang causing firms to underinvest?. Economic commentary no. 2010-7

Occhino F, Pescatori A (2010) Debts overhang in a business cycle model. Federal Reserve Bank of cleveland working paper 10-03R

Pontuch P (2014) Private sector deleveraging: where do we stand? Eur Comm Q Rep Euro Area 13(3):7–19

Ruscher E, Wolff G (2012) Corporate balance sheet adjustment: stylized facts, causes and consequences. European Commission, European economy economic papers no. 449

Staiger D, Stock JH (1997) Instrumental variables regression with weak instruments. Econometrica 65(3):557–586

Sugawara N, Zalduendo J (2013) Credit-less recoveries: neither a rare nor an insurmountable challenge. World Bank policy research working paper no. 6459

Temple J (1999) The new growth evidence. J Econ Lit 37(1):112–156

Wooldridge JM (2003) Introductory econometrics. A modern approach, 2nd edn. South-Western College Publishing, NewYork

Acknowledgements

We thank Lucian Briciu, Björn Döhring, Evelyne Hespel, Daniel Monteiro, Werner Roeger and Lukas Vogel as well as two anonymous referees and R.M. Kunst for valuable suggestions and discussions. The views expressed in the paper are those of the authors and should not be attributed to the Bank of Canada, the European Commission, the Bank of Greece or the Eurosystem. This work was completed during the authors’ time at the European Commission. We thank the European Commission for providing the codes to the QUEST model.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

Romanos Priftis declares that he has no conflict of interest. Anastasia Theofilakou declares that she has no conflict of interest.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix: Data and sources

Econometric estimations presented in Sect. 2 are based on an annual unbalanced dataset for 25 EU Member States (i.e. apart from Luxemburg, Malta and Sweden) over the period 1995–2015. Annual sectoral financial variables at national currency (at current prices) and on a non-consolidated basis are drawn from the OECD Database on Financial Accounts (National Accounts) and Eurostat Financial Balance Sheets (nasa_10_f_bs). For households and non-financial corporations, debt is defined as the sum of debt securities and loans. Remaining annual sectoral variables are taken from the OECD Non-financial accounts by sectors and Eurostat Non-financial transactions (nasa_10_nf_tr).

The main macroeconomic variables (real GDP per capita, real effective exchange rate, CPI) are drawn from the AMECO Database and Eurostat. Share prices are taken from the OECD Monthly and Monetary Financial Statistics and are deflated by CPI. Credit growth to non-financial corporations is calculated as the annual percentage change of total loans to corporates. Data on systemic banking crises come from the systemic banking crises database of Laeven and Valencia (2012). A banking crisis is defined as systemic when there are significant signs of financial distress in the banking sector as well as policy intervention measures in response to significant losses in the banking sector. World GDP per capita growth is taken from World Bank National Accounts database. Finally, data on the short-term interest rate and the cyclically adjusted primary budget balance (as a % of potential GDP) come from the OECD Economic Outlook No.99 (Fig. 1).

Evolution of NLB and NLB-to GDP ratio per country (1995–2015)

Statistical tests on IV estimates

A battery of statistical tests is performed to ensure IV/2SLS model identification, robust inference in light of weak instruments and to test for the endogeneity of the regressors that would support the use of IV estimators. More specifically, in order to estimate Eqs. (1a, 1b) and (2), they must be identified. A necessary (though not sufficient) condition is that the order condition is met, namely the number of endogenous regressors should be less than the instruments used. The rank order condition must also be satisfied, meaning that the (excluded) instruments must be correlated with the endogenous regressors. In the opposite case, the bias in the estimated IV coefficients gets larger, and the IV estimator loses consistency (see, e.g. Baum et al. 2007; Hahn and Hausman 2002; Wooldridge 2003).

Against this background, we report the Kleibergen and Paap (2006) rk LM statistic that tests for model under-identification. Under the null hypothesis, the set of (excluded) instruments is not correlated with the endogenous regressors. Therefore, accepting the null hypothesis suggests that the model cannot be identified and estimated. Moreover, even if the model is identified, a weak correlation of the instruments with the endogenous regressors can still lead to biased IV coefficients (see also Baum et al. 2003). We account for the weak instruments problem by examining the significance of the (excluded) instruments in the first-stage IV regressions. The latter are reduced form regressions of the endogenous variables on the instrument set. Commonly, the weak instruments problem is accounted for if the F statistic of testing the joint significance of the instruments in the first-stage regression is higher than 10 (Staiger and Stock 1997). For the IV-GMM estimations, we report the Sanderson-Windemeijer test which is a weak instruments F-test in the first-stage regression. As an additional control of the weak instruments problem, the statistical significance of the individual coefficients of the instruments in the first-stage regressions is assessed.

As discussed, the use of IV estimators requires that the instruments are also uncorrelated with the error term. This can be formally tested if the number of instruments is larger than the number of endogenous regressors, namely if the equation is over-identified. For testing the over-identifying restrictions, we report the Hansen (1982) J statistic. Accepting the null hypothesis implies that the orthogonality condition is met, namely instruments are uncorrelated with the error term.

In the IV/2SLS context, output growth and balance sheet adjustments are treated as endogenous regressors in the system. This is formally tested by conducting a C test (or “GMM distance”) test of the exogeneity of these regressors. The null hypothesis is that the specified endogenous variables can be treated as exogenous. For instance, inability to accept the null when testing for the potential endogeneity of output growth in the equation of balance sheet adjustments suggests that growth should not be treated as exogenous to corporate deleveraging; there is some degree of simultaneity between the two variables.

Rights and permissions

About this article

Cite this article

Priftis, R., Theofilakou, A. Growth effects of corporate balance sheet adjustments in the EU. Empir Econ 60, 773–801 (2021). https://doi.org/10.1007/s00181-019-01769-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-019-01769-3