Abstract

We investigate the distribution of links in three large data sets: one of these covering interbank loans in the electronic trading platform e-MID, and the other two covering a large part of the loans of banks to non-financial companies in the Spanish and Japanese economies, respectively. In contrast to all the previous literature, we do not assume homogeneity of the link distribution over time and across different categories of agents (banks, firms) but apply our hypothesized distributions as regression models. As it turns out, many of the tested sources of heterogeneity turn out to be significant regressors. For instance, we find pervasive time heterogeneity of link formation in all three data sets, and also heterogeneity for different categories of banks/firms that can be identified in the data as well as some explanatory power of balance sheet statistics in the case of the Japanese data set. Across all networks, the Negative Binomial model almost always outperforms all alternative models confirming its good performance as a model of economic count data in many previous applications.

Similar content being viewed by others

Change history

08 October 2019

In the original publication, the article title was incorrectly published as “On the distribution of links in financial networks: structural heterogeneity and functional”.

Notes

Evidence for a Pareto shape of the distribution of firm sizes is provided by, among others, Axtell (2001) and Segarra and Teruel (2012). In contrast, Cabral and Mata (2003) provide evidence for their proximity to a Lognormal distribution. Since both candidates (as well as some others) are strongly right-skewed, statistical discrimination between them can be a delicate problem. In recent literature, Crosato and Ganugi (2007) have attempted an explicit comparison of the Pareto and lognormal distributions and find a better fit of the former.

As proposed by Vuong (1989), one then subtracts \(0.5(K_1 - K_2)\hbox {log} N\) from the differences of the likelihoods (\(K_1\) and \(K_2\) the number of parameters of both alternative models, and N the number of observations).

The overall number of cases of these two categories is too small to consider them separately.

References

Albrecht P (1984) Laplace transformation, Mellin transforms and mixed Poisson processes. Scand Acturial J 11:58–64

Anand K, Gai P, Kapadia S, Brennan S, Willison M (2013) A network model of financial system resilience. J Econ Behav Org 85:219–235

Axtell RL (2001) Zipf distribution of U.S. firm sizes. Science 293:1818–1820

Borgatti S, Everett M (1999) Models of core/periphery structures. Soc Netw 21:375–395

Cabral LMB, Mata J (2003) On the evolution of the firm size distribution: facts and theory. Am Econ Rev 93(4):1075–1090

Clauset A, Shalizi CR, Newman ME (2009) Power-law distributions in empirical data. SIAM Rev 51(4):661–703

Crosato L, Ganugi P (2007) Statistical regularity of firm size distribution: the Pareto IV and truncated Yule for Italian SCI manufacturing. Stat Methods Appl 16(1):85–115

de Masi F, Gallegati M (2012) Bank-firms topology in Italy. Empir Econ 43:851–866

de Masi G, Iori G, Caldarelli G (2006) Fitness model for the Italian interbank money market. Phys Rev E 74:066112

de Masi G, Fujiwara Y, Gallegati M, Greenwald B, Stiglitz J (2011) An analysis of the Japanese credit network. Evolut Inst Econ Rev 7:209–232

Ehrenberg A (1959) The pattern of consumer purchases. Appl Stat 8:26–41

Finger K, Lux T (2017) Network formation in the interbank money market: an application of the actor-oriented model. Soc Netw 48:237–249

Finger K, Fricke D, Lux T (2013) Network analysis of the e-MID overnight money market: the informational value of different aggregation levels for intrinsic dynamic processes. Comput Manag Sci 10:187–211

Fricke D, Lux T (2015) On the distribution of links in the interbank network: evidence from the e-MID overnight money market. Empir Econ 49:1463–1495

Gabaix X, Ibragimov R (2011) Rank-1/2: a simple way to improve the OLS estimation of tail exponents. J Bus Econ Stat 29(1):24–39

Greene W (2008) Functional forms for the negative binomial model for count data. Econ Lett 99:585–590

Haldane A, May R (2011) Systemic risk in banking ecosystems. Nature 469:351–355

Hilbe J (2007) Negative binomial regression. University Press, Cambridge

Illueca M, Norden L, Udell G (2014) Liberalization and risk taking: evidence from government-controlled banks. Rev Finance 18:1217–1257

Karlis D, Xekalaki E (2005) Mixed Poisson distributions. Int Stat Rev 73:35–58

Krause A, Giansante S (2013) Interbank lending and the spread of bank failures: a network model of systemic risk. J Econ Behav Org 83:583–608

Lusher D, Koskinen J, Robins G (2013) Exponential random graph models for social networks: theory, methods, and applications. Cambridge University Press, Cambridge

Lux T (2016) A model of the topology of the bank-firm credit network and its role as channel of contagion. J Econ Dyn Control 66:30–53

Marotta L, Miccich S, Fujiwara Y, Iyetomi H, Aoyama H, Gallegati M, Mantegna RN (2015) Backbone of credit relationships in the Japanese credit market. Working Paper, Universit degli Studi di Palermo

Nier E, Yang J, Yorulmazer T, Alentorn A (2008) Network models and financial stability. J Econ Dyn Control 346:2033–2060

Schmittlein D, Bemmaor A, Morrison D (1985) Why does the NBD model work? Robustness in representing product purchases, brand purchases and imperfectly recorded purchases, Marketing Science 4:225–266

Segarra A, Teruel M (2012) An appraisal of firm size distribution: does sample size matter? J Econ Behav Org 82:314–328

Vuong Q (1989) Likelihood ratio tests for model selection and non-nested hypotheses. Econometrica 57:307–333

Watts D, Strogatz S (1998) Collective dynamics of ’small-world’ networks. Nature 343:440–442

Acknowledgements

Part of this work has been conducted in the author’s capacity of Bank of Spain Professor in Computational Economics at University Jaume I in Castellon. The almost final version has been completed during a research stay at the University of Kyoto and University of Hyogo in spring 2017 which has been partially supported by a MEXT scholarship within the project ‘Exploratory Challenges on Post-K Computer.’ The Japanese data have been made available by courtesy of Nikkei Media Marketing Inc. and the consortium of EU FP7 Project No. 255987 (FOC-II). The excellent hospitality of my hosts, Hideaki Aoyama and Yoshi Fujiwara, is most gratefully acknowledged. I am also very grateful to them for many stimulating discussions on the topic of this research and the structure of the Japanese data set that forms part of its empirical basis. My thanks for stimulating discussions also extend to Abhijit Chakraborty, Lutz Honvehlmann, Hiroyasu Inoue, Eliza Lungu and Hazem Krichene. Particular thanks go to Lutz Honvehlmann for his extremely able research assistance and to an anonymous reviewer for his or her careful reading of and constructive comments on the current manuscripts.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The original version of this article was revised: The article title was updated.

Appendix: Histograms and log–log plots of degree distributions

Appendix: Histograms and log–log plots of degree distributions

See Figs. 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11 and 12.

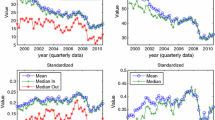

Histogram of degrees, e-MID data

Histogram of degrees, Spanish banks, in bipartite networks

Histogram of degrees, Spanish banks, one-mode projection

Histogram of degrees, Spanish firms, in bipartite network

Histogram of degrees, Japanese banks, in bipartite network

Histogram of degrees, Japanese banks, from one-mode projection

Histogram of degrees, Japanese firms, in bipartite network

Inverse cumulative distribution of degrees for e-MID interbank network in logarithmic representation

Inverse cumulative distribution of degrees for Spanish banks, from bipartite network

Inverse cumulative distribution of degrees for Spanish banks, from one-mode projection

Inverse cumulative distribution of degrees for Japanese banks, from bipartite network

Inverse cumulative distribution of degrees for Japanese banks, from one-mode projection

Rights and permissions

About this article

Cite this article

Lux, T. On the distribution of links in financial networks: structural heterogeneity and functional form. Empir Econ 58, 1019–1053 (2020). https://doi.org/10.1007/s00181-018-1569-6

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-018-1569-6