Abstract

This paper studies the long-run mortality effects of in utero and early-life economic conditions. We examine how local economic conditions experienced during the Great Depression, proxied by county-level banking deposits during in utero and first years of life, influences old-age longevity. We find that a one-standard-deviation rise in per capita bank deposits is associated with an approximately 1.7 month increase in males’ longevity at old age. Additional analyses comparing state-level versus county-level economic measures provide insight on the importance of controlling for local-level confounders and exploiting more granular measures when exploring the relationship between early-life conditions and later-life mortality.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Increases in life expectancy have been one of the most significant improvements in households’ welfare over the last century (Cutler et al. 2006; Deaton 2003).Footnote 1 In the past 100 years, Americans have enjoyed an overall gain of approximately 25 years in life expectancy at birth. Motivated by the growing body of research showing that conditions experienced in utero and early childhood are key determinants of health and human capital outcomes later in life (Almond et al. 2018; Almond and Currie 2011; Barker 1990), we provide new evidence on the relationship between early-life economic conditions and old age mortality, by focusing on the most severe economic recession in American history, the Great Depression.

Using micro-level data on the universe of deaths from 1975 and 2005 obtained from the Social Security Administration death records and linked with the 1940 U.S. Complete Count Census, this paper analyzes how males’ longevity is affected by local economic shocks before birth and during the first years of life. We proxy local economic conditions with annual, county-level per capita bank deposits.Footnote 2 We focus on this measure because financial distress in the banking system played a major role in propagating the contraction of economic activity and employment during the Great Depression (Bernanke 1983; Fisher 1933; Friedman and Schwartz 1963). Therefore, our measure captures the severity of the economic shock experienced by households across different regions while, unlike all other measures of economic conditions used in the literature, having the advantage of being available at the county and year level prior to 1929.

Our empirical model uses a two-way fixed effects strategy that compares the longevity of cohorts born before, during, and after the Great Depression and who were differentially exposed to local economic shocks around the time of birth, controlling for county-level time-invariant characteristics, temporal shocks, and within-state county-group-by-year fixed effects. Our findings suggest that a one-standard-deviation increase in bank deposits during the in utero period, which is equivalent to roughly four times the drop in deposits between the years 1929–1933 (peak-to-trough of the Great Depression), is correlated with a roughly 1.7 months higher age at death in old age among male individuals. The effect is quite robust across a wide array of specifications. To assess whether these relationships are an artifact of overall trends in health improvements/disruptions, we implement a placebo test and show that the effects become indistinguishable from zero for deposits at pre-prenatal ages. We also argue that these effects are not driven by endogenous demographic changes in the sample due to changes in fertility, early-life survival, or migration. Additional analysis suggests that improvements in educational attainments and income in adulthood are potential mechanisms. However, using estimates from previous studies, we posit that these channels only partially reflect the pathways.

The motivation of the current study stems from the limited evidence of in utero economic conditions and later-life longevity. Van Den Berg et al. (2006) were the first to document the adverse effects of national economic conditions around birth on life expectancy using historical data for the Netherlands. The authors found that cohorts born during an economic boom lived 1.6 years longer (or 4 percent longer relative to the life expectancy of 39 years) than those born during economic recessions. No effects were found when booms were experienced during early childhood. Similarly, Lindeboom et al. (2010), also using data from the Netherlands, showed that children born during the potato famine of the mid-1900s lived 2.5–4 fewer years as adults compared to those born before the nutritional shock and with more pronounced impacts for children from lower class families.

We contribute to the literature in several ways. First, we contribute to a small literature that analyzes the link between economic conditions and mortality in the context of the Great Depression that has found mixed results. While Granados et al (2009) showed a negative correlation between the GDP per capita and the national mortality rate, Stuckler et al. (2012) found no effect between changes in bank suspensions and changes in mortality except for an increase in suicide rates. Fishback et al. (2007), in contrast, showed a small decline in death rates during the 1930s due to increases in New Deal spending. Cutler et al. (2007) found little evidence that early life exposure to the Depression affected long-term health (including mortality) using longitudinal data from the Health and Retirement Study (HRS) linked to regional-level macroeconomic data. More recently, however, Schmitz and Duque (2022) and Duque and Schmitz (2021) revisited this question in the HRS using macroeconomic data linked to the state of birth and found improvements in the magnitude and precision of the effects on old age health and mortality when economic outcomes were measured at the state level as opposed to the regional level. Importantly, these effects were localized to the in utero period specifically as opposed to the pre-conception, postnatal, childhood, or early adolescent periods. Thus, from an empirical perspective, we also contribute to the literature by using longitudinal bank deposit data measured at the county level before and during the Great Depression to explore within-state geographic variation in economic conditions, as opposed to prior studies that relied on region-level and state-level variations in the shock. In addition, our data source contains millions of observations, which adds power to our statistical tests and allows the research design to search for potential heterogeneity in the effects across different demographic groups.Footnote 3

The rest of the paper is organized as follows. Section 2 reviews the literature. Section 3 introduces data sources. Section 4 discusses the empirical framework. Section 5 reviews the results. Section 6 suggests potential mechanisms. Section 7 concludes the paper.

2 Literature review

A growing body of research evaluates the long-term effects of early life adversities (Almond et al. 2018; Almond and Currie 2011; Currie 2009; Hayward and Gorman 2004; Steptoe and Zaninotto 2020). Several studies provide suggestive evidence for the relevance of in utero and early-life conditions for short-term and later-life outcomes, including child health and mortality (Abiona and Ajefu 2023; Baird et al. 2011; Schoeps et al. 2018), cognitive development (Chang et al. 2022; Majid 2015; Yamashita and Trinh 2022), test scores (Almond et al. 2015; Shah and Steinberg 2017), education (Aizer et al. 2016a, b; Caruso and Miller 2015; Qian 2024), adulthood earnings (Black et al. 2007; Currie and Rossin-Slater 2015; Hoynes et al. 2016), and health outcomes over the life cycle (Fletcher 2018a, 2018b; Fletcher and Noghanibehambari 2024; Goodman-Bacon 2021; Miller and Wherry 2019; Noghanibehambari and Engelman 2022; Noghanibehambari and Fletcher 2023b; Persson and Rossin-Slater 2018). Early-life conditions could operate through these mediatory pathways to influence the trajectory of old-age longevity.Footnote 4 For instance, den Berg et al. (2015) employ a longitudinal panel of observations in Dutch registries covering about two centuries and showed that men who were born during an economic boom (versus a recession) are more likely to be married during adulthood and at old ages and have a lower risk of mortality. They argue that, among men, marriage has a protective effect against mortality. Grimard et al. (2010) use data from Mexico and show that socioeconomic status measures during childhood significantly affect old-age health outcomes even after accounting for education and income. Bengtsson and Broström (2009) use data from Sweden and show that early life disease loads affect old-age mortality and socioeconomic status. However, they do not find evidence that the early-life health environment effect on later-life mortality operates through wealth and socioeconomic channels. Gagnon and Bohnert (2012) employ data from Canada and show that family wealth and the socioeconomic status during early life affect mortality during old ages among males. Their results fail to provide evidence of this association among females.

Hayward and Gorman (2004) use data from the National Longitudinal Survey of Older Men and show that men’s mortality is correlated with an array of early-life and childhood conditions, including parents’ socioeconomic status, mother’s marital status, mother’s labor force status, and parents’ nativity. Montez and Hayward (2011) use the Health and Retirement Study to explore early-life family socioeconomic status on later-life mortality. They find significant positive correlations between risks of mortality during adulthood and a series of early-life adversities, including perceived poverty during childhood, having a low-educated father, and self-reported poor childhood health. On the other hand, Myrskylä (2010a, b) finds weak and modest effects of early-life conditions on adult mortality using data from several developed European countries. The results suggest a strong correlation between period effects and mortality rather than early-life effects.

Studies that examine the role of economic conditions on later-life mortality outcomes exploit measures of economic conditions at various levels of aggregation and find different results. For instance, Van Den Berg et al. (2006) use historical longitudinal data from the Netherlands to explore economic conditions in early life on old-age mortality. They exploit the cyclicality of national gross domestic product (GDP) as a proxy for economic conditions and find that being born during a boom versus a recession results in 8 percent lower mortality rates. Arthi (2018) explores the persistent effects of in utero and childhood exposure to state-level measures of the Dust Bowl, a devastating environmental shock followed by agriculture failure and reductions in income, on later-life human capital and health. The result suggests long-lasting effects on income, disability, and college completion. Similarly, Duque and Schmitz (2021) and Schmitz and Duque (2022) find a connection between state-level in utero exposure to wages, employment, and car sales during the Great Depression and late-life aging outcomes and mortality. However, an earlier paper by Cutler et al. (2007) that used exposure to economic variation at the census-region level during the Great Depression failed to find any evidence that fetal exposure to economic conditions was associated with disability and chronic disease later in life. Atherwood (2022) implements county-level Dust Bowl measures and explores the effects of young adulthood exposure on later-life longevity. He finds insignificant average effects. Noghanibehambari and Fletcher (2024) re-examine the effects of early-life exposure to the Dust Bowl on old-age longevity. They employ difference-in-difference method and account for county-level heterogeneity. They find intent-to-treat effects of about 1 month reduction in longevity among cohorts that were severely affected by their county-of-birth topsoil erosion in early life.

3 Data and sample selection

The primary data source is the Social Security Administration Death Master File (hereafter DMF) records extracted from the CenSoc Project database (Goldstein et al. 2021). The DMF data contains death records among males between 1975 and 2005 that are linked to the full-count 1940 census. Therefore, they have a wide array of early-life social and economic variables. There are three advantages of DMF data over similar data sources that contain mortality information necessary for our research design. The availability of county identifiers in the 1940 census allows for more granular and detailed environmental information as opposed to virtually all other data sources with state identifiers. Second, the DMF builds a longitudinal panel that contains millions of observations while similar longitudinal data provides several thousand (e.g., Health and Retirement Study). Third, the DMF-census-linked data offers a wide array of family-level covariates, including parental education and a socioeconomic score that can be used in our balancing tests, in analysis of heterogeneous impacts by family resources, and adds the robustness to our identification strategy.

We proxy local economic conditions using changes in bank deposits compiled by the Federal Deposit Insurance Corporation (FDIC) and taken from Manson et al. (2017). The data reports total annual deposits in all state and federal banks in each county (except Wyoming and DC) over the years 1920–1936 as of December of each year. Our choice of this proxy is based on two facts. First, later in the paper, we will illustrate the positive association between changes in bank deposits and similar proxies of state-level and county-level economic covariates. Second, similar studies show an association between banking crises and city-level economic conditions during a similar period (Stuckler et al. 2012).

To infer county of birth from the DMF census sample, we take two approaches. First, we use cross-census linking rules provided by the Census Linking Project to merge 1940 census records with 1930 census. In our sample, we are able to match 48 percent of cohorts born 1926–1930 to their 1930 census records. For these matched records, we use county of residence in 1930 as county of birth. For unmatched cohorts of 1926–1930, and for all cohorts of 1931–1936, we continue to infer the county of birth using the second approach. Specifically, we use information from three variables reported in 1940 census. First, we use information on the county of residence in 1935 as the benchmark proxy for location of birth using the fact that the 1940 census reports the migration status from five years prior. Second, we use county of residence in 1940 if the individual reported having stayed in the same house since 1935. Third, if the migration status is missing and the person’s state of birth is the same as state of residence in 1940, we again use county of residence in 1940 as the proxy for the county of birth. To further reduce the migration issue, we limit the sample to children up to 15 years old as older children usually leave their original household. Doing so will limit the sample to cohorts born after 1926.

Since our purpose is to explore in utero exposures, we calculate a weighted average of deposits for the nine months before birth, assuming an average of nine months of gestation.Footnote 5 In so doing, we assign the current year of deposits to our in utero deposit measure for births occurring in the months of October through December. For births occurring between January to September, the in utero measure is a weighted average of current and previous year’s deposits. The weights are proportionate to the fraction of pregnancy that overlap with current and previous year. For instance, consider an infant born in March 1930. This infant has been exposed to three months of current year’s (1930) deposits and six months of the previous year’s (1929) deposits during prenatal development. Hence, the weights are \(\frac{3}{9}\) and \(\frac{6}{9}\) for 1930 and 1929 deposits, respectively. We then merge DMF-census sample to bank deposit data based on inferred county of birth and the weighted average of previous nine-month deposits.

To control for other county-level sociodemographic changes, we use full-count decennial censuses from Ruggles et al. (2020) for the decennial years 1920–1940. We then linearly interpolate covariates for inter-decennial years. Moreover, for the analysis to explore the association of bank deposits with other economic variables, we use county-level retail sale per capita and state-level income per capita extracted from Fishback et al. (2007).

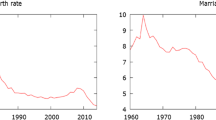

The final sample includes 1,221,113 individuals from 3042 counties in 47 states born between 1926 and 1936 who died between 1975 and 2005.Footnote 6 Summary statistics of the final sample are reported in Table 1. The average per capita bank deposit is $331. Over the sample period, roughly 10 percent of individuals are born in counties that experienced a 5 to 10 percent drop in total banking deposits relative to the county-specific previous year’s value. About 23 percent of individuals live in counties that experienced a drop of more than 10 percent in deposits. The top and middle panels of Fig. 1 depict the cross-sectional geographic distribution of per capita deposits and per capita retail sales. There is a visual correlation between our proxy for economic conditions (bank deposits) and a measure of local consumption expenditure (retail sales per capita). The bottom panel of Fig. 1 illustrates the distribution of age at death by county of birth for cohorts born in 1930. Figure 2 illustrates the time-series evolution of bank deposits per capita for different census divisions. Not surprisingly, the figure reveals a significant drop in deposits as the Great Depression hit the economy and started to recover from the years 1933-1934, as the economy starts to recover. There is also a visual correlation between these two measures and long-run longevity. In a cross-sectional and correlational manner, Fig. 3 depicts the differences in the density distribution of age at death in the subsample of above-median per capita deposit (in green) versus below median per capita deposit (in red). While these are suggestive figures, they do not convey any informative interpretation of the statistical association.

Geographic distribution of variables. The colors in the map are based on the county’s quartile rank in the nation’s distribution of the respective variable

Time-series evolution of per capita bank deposits across census regions

Density distribution of age at death by county above/below median bank deposits per capita

4 Econometric method

Our identification strategy exploits within-county and over-time variations in bank deposits. Specifically, we implement regressions of the following form:

where the outcome is age at death (\(DA\)) of individual \(i\) born in county of birth \(c\), state economic area \(s\), and birth year \(b\). State economic areas (SEA) are geographic boundaries that covers several counties within the same state that have similar economic and demographic conditions (Bogue 1951). SEA was introduced in census 1950 and then was applied to counties in 1940 census. Since the period of the Great Depression was accompanied by vast changes in economic conditions, we prefer exploiting within-SEA across-counties variations to better isolate the impacts of economic conditions. The parameter \(PCBD\) represents per capita bank deposits assigned to each individual based on county of birth and the average of nine months leading to birth (\({b}^{*}\)). To ease the interpretation, we standardize this variable with respect to the mean and standard deviation of the sample. In \(X\), we include as individual controls dummies for race. The matrix \(X\) also contains parental characteristics, including dummies for maternal education, paternal education, and socioeconomic status. The parameter \(Z\) represents a series of county-by-birth year covariates constructed based on full-count decennial censuses 1920–1940 and interpolated for inter-decennial years. These covariates include the share of homeowners, the share of married people, and the average occupational income score. The county fixed effects, represented by \(\xi\), control for time-invariant unobserved features of counties. To account for temporal cohort-level changes in longevity, we add birth cohort fixed effects, represented by \(\zeta\). To account for all SEA-by-year divergence in the outcome and other time-varying local determinants, we include SEA-by-birth-year fixed effects represented by \(\eta\). Therefore, the identifying variation comes from changes in bank deposits across counties within an SEA year. Finally, \(\varepsilon\) is a disturbance term. We cluster standard errors at the county level to account for serial correlation in the error term. The coefficient of interest is \({\alpha }_{1}\) that, conditional on covariates and fixed effects, captures the effect of one-standard-deviation (from mean) change in per capita bank deposits on later-life old-age longevity.

5 Results

5.1 Endogeneity concerns

One potential concern in our analysis is that economically improving areas attract more people and induce migration. Similarly, a recession may affect different areas to varying degrees and generates in/out-migration. If certain characteristics in migrant subpopulations correlate with their later-life health and longevity, the link between deposits and longevity is contaminated by endogeneity. For instance, if whites are more (less) likely to migrate after a county is hit by a recession, the coefficients of Eq. 1 can overstate (understate) the true effects since whites have higher longevity for reasons not necessarily captured by a race dummy. To explore this source of bias, we ask whether changes in bank deposits are associated with changes in observable characteristics, conditioning on county and SEA-year fixed effects. The results of such balancing tests are reported in Table 2. We do not observe any statistical association between bank deposits and probability of being white, mother’s schooling, father’s schooling, and father’s socioeconomic score. Moreover, the estimated effect sizes are economically small. For instance, based on percent change from the mean of the dependent variable reported in the fifth row, the effects suggest that a one-standard deviation change in bank deposits is correlated with 0.27 percent change in white, 0.15 percent change in maternal schooling, and 0.32 percent change in paternal socioeconomic score. Therefore, the big picture extracted from these numbers is a failure in finding robust and strong evidence of demographic and socioeconomic changes due to changes in bank deposits that could unbalance the sample by contaminating the long-run relationships.

Another concern is that linkage rates between DMF and the 1940 census may be predicted by early-life shocks, such as changes in deposits. While the linking rules are primarily based on name commonality, and we have little prior concern for this being correlated with local economic conditions, we explore merging issues empirically by evaluating the correlation between the merging of DMF-census records and deposits. In so doing, we start by imposing sample selections as discussed in Section 3. We also follow the procedure described in Section 3 to infer county of birth. The sample selections result in 22,285,131 observations before merging with the DMF death records. The successful merge dummy takes a value of one if DMF is merged with the census records and zero otherwise. We then regress this variable on deposits per capita, conditional on a full specification of Eq. 1. The results are reported in Table 3 for the full sample, sample of whites, sample of people with low educated mothers, and sample of persons with low socioeconomic score fathers, in columns 1–4, respectively. We find small and insignificant coefficients between deposits and successful merging. For instance, a one-standard-deviation change in banking deposits per capita results in an insignificant 0.8 basis point increase in the probability of merging, equivalently 0.15 percent change from the mean of the outcome.Footnote 7 To further complement this analysis, in Appendix M, we employ Heckman two-step correction model to correct for biases arising from truncation and selection (Heckman 1979). We find coefficients that are slightly larger than those of the main results (Section 5.2), suggesting that selection, at worst, induces a small downward bias into our regressions.

A final concern of endogeneity is regarding reverse causality as areas with healthier people might enjoy better economic conditions, hence higher bank deposits. In Appendix G, we empirically examine whether longevity of individuals can explain variations in bank deposits. Nonetheless, the results provide no evidence of this concern.

5.2 Main results

The main results of the paper are reported in Table 4. We start with a model that only includes county and SEA-by-birth-year fixed effects in column 1 and gradually add additional covariates to the model across consecutive columns. The marginal effect of bank deposits per capita is virtually unchanged across specifications.

A growing literature document the influence of family characteristics and local conditions as significant determinants of long-run health outcomes (Almond et al. 2018; Hayward and Gorman 2004). Therefore, a priori, we need to account for these potential confounders into our regressions (columns 2–4 of Table 4). However, the fact that coefficients do not change across these columns lends credibility to the exogeneity of bank deposits, i.e., deposits are not correlated with other well-known determinants of later-life health, at least with regard to the observable and available variables.Footnote 8 The results of the full specification of column 4 suggest that, on average, a one-standard-deviation change (from the mean) in per capita deposits in utero is associated with 1.7 months higher longevity during old ages. We put this number into perspective by comparing it with the coefficients of other variables. For instance, the marginal effect of a black dummy (not reported here) is −15.3 (se = 1.1). Therefore, a one-standard-deviation change in bank deposits is equivalent to roughly 11 percent of the black-white gap in longevity. The difference in average life expectancy between the US and other OECD countries is 49.2 months (76.6 years versus 80.7 years, respectively). Thus, the impact of a one-standard-deviation rise in bank deposits is equivalent to roughly 3.5 percent of the US-OECD-countries gap in longevity.

Another way to understand the magnitude of the finding is to compare with other determinants of longevity and the impact of other early-life exposures. For instance, Chetty et al. (2016) investigate the income-longevity relationship in the US using individual tax returns linked with death records. They document that each five income percentiles is associated with about 0.8 months higher age at death.Footnote 9 Therefore, the effect of a one-standard-deviation rise in bank deposits in county-year of birth is equivalent to the impact that moving up the income ladder by about one percentile has on longevity. Halpern-Manners et al. (2020) examine the education-mortality relationship using twin fixed effect strategy. They document that each additional year of education is associated with about 4 months higher longevity.Footnote 10 Therefore, the marginal effect of Table 4 is equivalent to the effect of 0.43 years of schooling on longevity. Aizer et al. (2016a, b) examine the impacts of the Mother’s Pension (MP) program, a state-local government joint initiative to help poor single mothers with cash transfers prior to social security era, on children’s old-age longevity. They find treatment-on-treated effects of about 1-year additional life to children whose mothers were selected for the MP benefits.Footnote 11 The MP benefits usually lasted for three years and transferred about 30-40 percent of pre-transfer maternal income. Therefore, our finding is equivalent to a one-time transfer of 13–17 percent of income to poor families.

5.3 Fertility response

While the balancing tests of Table 2 are inconsistent with strong demographic compositional changes due to the differences in the survival of subpopulations, one may be concerned that parents observe the economic condition and plan their fertility accordingly (Currie and Schwandt 2014; Schaller 2016; Schaller et al. 2020). However, the literature on economic conditions and fertility is not conclusive (Black et al. 2013; Cohen et al. 2013; Docquier 2004). Moreover, little empirical research has been done for our study period (Fishback et al. 2007). To explore the selective fertility of parents to the observed deposit changes, we use county-level births data over the years 1926–1936 extracted from Bailey et al. (2016). The data offers three main variables that are specifically useful for the analysis of this section: general birth rate, share of births to whites, and share of births to blacks. Since over time more counties appear in the sample and the effects may be driven by differential fertility of new counties, we balance the county-year sample so that each county has appeared in at least 5 years. This leaves us with roughly 896 counties. We merge this with deposit data and implement regressions that include the county, year, and SEA-year fixed effects.Footnote 12 The results are reported in Table 5. Deposits are positively associated with birth rates. A one-standard-deviation change in per capita deposits is associated with 0.22 additional births per 1000 women in the county, equivalent to roughly 0.6 percent rise in the mean of the outcome, a quite small change. In column 2 of this table, we observe an almost identical implied effect when we look at log fertility rate.

A similar concern arises due to the association between bank deposits and infant mortality rate. In columns 3 and 4, we observe that higher bank deposits are associated with lower infant mortality rates. However, the point estimates are small and noisy, which limits further interpretation.

To further examine fertility response, we use full-count census of 1940 and examine selective fertility response of parents to changes in deposits based on maternal education. These results, reported and discussed in Appendix D, do not provide a consistent and strong evidence of selective fertility behavior by maternal education.

5.4 Effects during pre-prenatal and postnatal periods

While the literature points to the relevance of conditions in utero for later-life outcomes, several studies also show associations between post-birth exposures and conditions and long-run outcomes (Chyn 2018; Currie and Rossin-Slater 2015; Ludwig and Miller 2007). This section complements the main results by investigating the effects of bank deposits experienced during postnatal ages and later-life longevity. Moreover, we also examine the association between changes in deposits during pre-prenatal period on longevity. The idea is that if the deposits are capturing general improvements in health conditions rather than in utero economic condition shocks, we would observe similar effects for the exposure measures assigned for pre-prenatal period. Therefore, this test provides a placebo check to assess the validity of the main results.

In so doing, we generate four new variables for assigning deposits at two years before birth and two years after birth. We include these variables as separate regressors in the full specifications of Eq. 1. The results are reported in Table 6. We observe small and insignificant association for two-years prior to birth. However, the coefficient of one year prior to birth suggests a significant effect of 1 month increase in longevity. This is expected as this variable partly captures the in utero period, especially for cohorts born in the beginning months of the current year. Interestingly, we observe quite small and insignificant associations for post-birth periods. The overall results imply two pieces of information. First, the results do not pick up on the overall pre-existing improvements in health. Second, the in utero period is the more correlated with economic conditions in contrast with other post-natal ages.

5.5 Exploring the relevance of county-level variations

As we discussed in Section 1, an advantage of our study compared to the previous literature is in part that we use a more granular measure of local economic conditions (i.e., county-level) versus national, census region, or state-level measures of other studies (Arthi 2018; Atherwood 2022; Cutler et al. 2007; Van den Berg et al. 2015; Duque and Schmitz 2021; Granados et al. 2009; Myrskylä, 2010b; Schmitz and Duque 2022; Scholte et al. 2015; Van Den Berg et al. 2006; Van den Berg et al. 2009). To show that this granularity is essential in this context, we explore the correlations of economic conditions at the state level with longevity in our sample. Specifically, we use state-level income per capita and deposits per capita aggregated at the state level. Since the state-level income per capita is available only from 1929, we restrict the sample to cohorts of 1929–1936. In all regressions of this section, we include individual and family covariates.

As reported in column 1 of Table 7, the unconditional correlation between state-level income per capita and death age is 9.4 months. However, a large portion of the observed correlation can be explained by unobserved state and cohort characteristics. Controlling for state and cohort time-invariant confounders reduces the coefficient by about 86 percent (column 2). Next, we aggregate the deposits from the county level to the state level and show the correlations with age at death in columns 3–4.Footnote 13 The correlation is 32.5 months (column 3). The marginal effect becomes smaller (about the same 80 percent reduction as in columns 1 and 2) and noisy once we include state and cohort fixed effects (column 4).

In the next step, we use county-level deposits per capita and replicate the results across different specifications. In column 5, we show that the correlation (excluding fixed effects) is about 0.4 months and statistically insignificant. Adding state-fixed effects provides a negative and small coefficient. These results suggest the existence of state and county level variables correlated with bank deposits that have offsetting effects. For instance, the observed coefficient of column 5 is the result of comparing longevity of differential exposure to bank deposits. Higher deposits (and income) might be the result of healthier cohorts in specific regions which then is reflected in higher (children’s) longevity. Therefore, these results imply the need to control for county level effects and focus on within-county changes in economic conditions (as measured by bank deposits).

In column 7, we include county fixed effects. The correlation between county level economic circumstances at the time of birth and later life longevity becomes positive and relatively large in magnitude. In column 8, we control for other local-level confounders by including SEA-year fixed effects. The results suggest an increase of 2.9 months due to a one-standard-deviation change in bank deposits.

5.6 Validity of bank deposits as a proxy for economic conditions

To gauge the magnitude of the paper’s main results and to explore the validity of bank deposits as a proxy for local economic conditions, we explore the relationship between per capita deposits and other local and state-level economic variables. The main limitation of this exercise is the scarcity of local-level data for the time period of this study. We know of no dataset that contains measures of county-level income or county-level unemployment rates during this time period (and that starts prior to the Great Depression). However, income data is available at the state level for the years 1929–1940. Also, retail sale data is available at the county level which is, arguably, a reasonable measure of consumption. These data are available for post-1929 years and are taken from Fishback et al. (2007). Thus, the analysis sample for both retail sales and income cover the years 1929–1936 since our sample ends in the year 1936.

We merge per capita retail sales at the county and year level with our bank deposit sample and implement regressions similar to Eq. 1. The results are reported in columns 1–3 of Table 8. We start by showing the unconditional correlation in column 1, adding county and year fixed effects in column 2, and then implementing a full specification in column 3. The unconditional correlation suggests a very strong co-movements between bank deposits and retail sales. However, fixed effects explain a large portion of this correlation. The correlation of the full model of column 3 that includes SEA-by-year fixed effects is still statistically and economically significant. A one-standard-deviation rise in per capita deposits is associated with 0.15 standard-deviations increase in per capita retail sale.Footnote 14

For the state-level income analysis, we aggregate our final sample at the state-level and merge it with income data at the state-year level and implement regressions that include state, year, and region-by-year fixed effects. These results are reported in columns 4–6 of Table 8. The full specification of column 6 implies that for a one-standard-deviation change in deposits per capita the income per capita changes by 0.4 standard deviations. Between the years 1929 and 1933 (peak to trough of the Great Depression), income per capita decreased from $611 to $326, a decrease of about 1.5 times its standard deviation over the sample period. Using figures from Table 8 and this drop in income, one can deduce a roughly 6.1 months drop in later-life longevity.Footnote 15 This is an economically large effect.

5.7 Robustness checks

In Table 9, we explore the robustness of the main results to alternative specifications. In column 1, we replicate the results of the full specification of Table 4 as the benchmark comparison. In column 2, we allow for the time-invariant effects of counties to vary by individual covariates. In column 3, we add county-by-parental-characteristics fixed effects so that the unobserved time-invariant features of a county can be absorbed differently by families with different sociodemographic backgrounds. The resulting marginal effects are almost identical to the main results. In column 4, we control for all unobserved county characteristics that evolve linearly over cohorts by including county-by-birth-year linear trend. The effect rises and remain statistically significant.

There is evidence that season of birth and season of death may influence health and longevity of individuals (Simmerman et al. 2009; Vaiserman 2021). In column 5, we control for seasonality in birth and death outcomes by adding birth-month and death-month fixed effects.Footnote 16 The resulting coefficient is comparable to that of column 1.

In column 6, we check for robustness of the functional form by replacing the outcome with the log of age at death. The effect suggests 0.2 percent change in the outcome as a result of one-standard-deviation change in deposits, an effect that is almost identical to the percent change effect shown in column 4 of Table 4. In columns 7–8, we replace the outcome with a dummy to indicate longevity beyond age 70 and 65, respectively. A one-standard-deviation increase in in utero bank deposits per capita is associated with 62 and 53 basis-points higher likelihood of living beyond age 70 and 65. These effects are equivalent to roughly 2.6 and 1.1 percent change from the mean of their respective outcomes.

In column 9, we check for sensitivity to county-level clustering. We find that the errors are larger when we implement a two-way clustering by county and state-year. However, the resulting coefficient is still statistically significant at the 5 percent level.

We implement two sets of additional robustness checks to complement this section. First, there are concerns of the confounding influence of contemporaneous conditions on longevity. Since DMF data does not report place of death, we employ Numident death records as an alternative data source which provides state of death. In Appendix H, we show that the results are fairly robust to including time-invariant state-of-death features and time-variant state-level characteristics. Second, another robustness check could also include measures of healthcare access as potential confounding influence on infants’ health and their later-life longevity. We have information on County Health Departments and measures of medical staff at the county level for a subsample of mostly rural southern counties. We report and discuss the results in Appendix I. We find almost identical coefficients for specifications with/without these additional county covariates.

5.8 Alternative measures

In Table 10, we replicate the main results using alternative measures of banking conditions. In column 1, we ignore the differences in county population as a deflating channel for the effects of deposits and use total deposits as the main independent variable. The resulting marginal effect suggests 2.2 months higher longevity as a result of a one-standard-deviation change in deposits. In column 2, we replace the independent variable with two dummies indicating that banking deposits in a specific county and year have dropped between 5–10 and more-than-10 percent relative to the county’s previous year’s deposits, candidate measures of the banking crisis. The result suggests a reduction of 0.6 months in longevity for both measures of banking crisis. We should note that 33 percent of cohorts have experienced a banking crisis during their prenatal period, per our definition of crisis (see Table 1). Overall, these results add to the general picture that the economic conditions of early life have significant effects on later-life longevity.

5.9 Heterogeneity by subsamples

In Appendix A, we replicate the main results across two subpopulations: whites and blacks. We find that the longevity of black people is more strongly connected with economic conditions. The marginal effect of black sample is roughly 2.5 times that of the white sample, although the effects in both samples are significant.

During the period of the study and specifically for post-1934 years, many counties in the Southern Plains region experienced the Dust Bowl. We examine how the effects vary by Dust Bowl exposure counties in Appendix C. We find that for counties exposed to the Dust Bowl, the correlations are about five times larger, though statistically insignificant. The effect on other counties is almost identical to that of the main results of the paper.

5.10 Sensitivity to death window and gender selection

The DMF reports death records for males in the years from 1975 to 2005. As an alternative source of data that covers both genders, we use Numident death records of the Social Security Administration extracted from the Censoc Project (Goldstein et al. 2021). Numident is also linked to the 1940 census but reports the death to both females and males for death years 1988–2005. We explore whether the results are sensitive to gender selection and death selection of DMF in Appendix B. We show that when we restrict the sample to Numident death years (i.e., 1988–2005), the effect drops by about 65 percent (column 2 of Appendix Table B-1). This is quite comparable to the Numident results (column 5 of Appendix Table B-1). Therefore, the effects are larger as we expand the death window to cover earlier deaths, suggesting that the Great Depression accelerated the age of mortality.

Looking at the male subsample of Numident reveals an effect of 0.8 months while the female subsample suggests an insignificant effect of 0.2. Therefore, the results are primarily driven by males, suggesting that early-life economic conditions are more relevant to the health of males than females. This fact is in line with studies that show the exposures in early life are more impactful for males (Clark et al. 2021; Clay et al. 2019; Rosa et al. 2019; Smith et al. 2011; Wang et al. 2017; Weinberg et al. 2008).

6 Mechanism

The results so far suggest that early-life economic conditions have moderate and robust effects on later-life longevity. To establish a candidate mediatory link, we explore the effects on later-life education-income profiles. However, in the 1940 census, the cohorts of our final sample (born in 1926–1936) had not completed their education. In addition to this issue, post-1940 censuses do not provide county identifiers. To overcome this problem, we use the 1960 census in which we have a below-state geographic identifier: Public Use Microdata Area (PUMA).

PUMA is a census-defined geographic boundary that identifies places based on their population. In urban areas with a higher population (and population density), a county contains several PUMAs. In rural areas with a lower population, several counties are grouped to form one PUMA. We convert our deposit data into PUMA level by aggregating the deposits for several-county PUMAs and assigning similar values to different PUMAs within a county that covers several PUMAs. We then merge this with observations in the 1960 census based on PUMA and birth year.Footnote 17 We also restrict the sample to male individuals born between the years 1926–1936.Footnote 18 We implement regressions that include, in addition to individual covariates, PUMA and region-birth-year fixed effects.Footnote 19 The results are reported in Table 11. We find a strong statistical association between per capita deposits in the birth year and educational outcomes and measures of the socioeconomic index. For instance, a one-standard-deviation rise in deposits is associated with 0.02 additional years of schooling (column 1), 38 basis points increase in the probability of any college education (column 2), $57 higher wage income (column 6), and 0.34 units increase in the socioeconomic score (column 8). We can scale up these effects using changes in state-level income per capita from peak to trough of the Great Depression (years 1929–1933) and its link to deposits as discussed in Section 5.6. Such changes in deposits are associated with about 1.42 percentage points fall in the probability of college education and 1.3 units drop in socioeconomic score.Footnote 20

We can use the values reported by similar studies to understand how much of the effects could operate through these channels. Fletcher and Noghanibehambari (2023) explore the effects of new college opening during adolescence on later-life longevity. They find that having a college education raises the age at death by about 1.6 years.Footnote 21 Combining this figure with the marginal effect of column 2, one can deduce that a one-standard-deviation increase in deposits raises the age at death by 0.3 months if it solely operates through increases in college education. This number can explain only 17.6 percent of the observed reduced-form effect.Footnote 22 In another study to explore the effects of education on mortality, Halpern-Manners et al. (2020) implement a twin-strategy and find that an additional year of schooling is associated with 0.34 years higher age at death.Footnote 23 Using the coefficient of column 1, we can infer that, had only the effects operated only through improvements in schooling, a one-standard-deviation rise in deposits leads to 0.08 months increase in longevity, equivalent to roughly 4.8 percent of the reduced-form marginal effect in Table 4.Footnote 24

7 Conclusion

The Great Depression was an extraordinary event in the economic history of the US. From 1929 to 1933, real output contracted by more than 25 percent and the unemployment rate increased from 3.2 to 25 percent, reaching the highest levels ever documented. Despite its magnitude, previous literature has found little evidence that the Great Depression affected adult mortality. In this paper, we provide new evidence on this link by using local banking deposits, as a proxy for economic conditions and credit market, during in utero and year of birth can influence old-age longevity. We find that a one-standard-deviation rise in per capita bank deposits is associated with about 1.7 months higher age at death during old ages. The effect is statistically significant, economically meaningful, and robust across a wide array of specification checks.

A battery of balancing tests rules out significant changes in demographic and family socioeconomic characteristics associated with changes in deposits. Moreover, we fail to find any associations between deposit changes in postnatal ages and later-life longevity suggesting that only conditions in utero and first year of life are important for later-life longevity. We also argue that endogenous fertility response of parents from different demographic groups does not affect the main results. Additional analysis suggests quite strong associations between bank deposits and retail sale and income per capita, which implies that banking deposits are indeed a reasonable proxy to capture local economic conditions. In addition, we show that improvements in education-income profile during adulthood are potential mechanisms. However, we argue that between 6 and 9 percent of the link between early-life deposits and later-life longevity can be explained by modest changes in educational outcomes. These small effects on potential mediatory outcomes suggest that the economic conditions operate through other non-labor-market channels to impact longevity such as changes in health capital that can be detected in old ages.

The Great Depression represented a unique and distinct period in the US history with severe and long-lasting downturn in economic activities. Its length and depth were unprecedented, and the economic knowledge of true policy response was limited. Therefore, it provides a different landscape compared with later recessions to examine the long-term health impacts. In the meantime, it shares some commonalities with other economic crises, such as stock market crash, resource scarcity, as well as the availability of relief programs. However, one should exercise caution in generalizing these results for other periods.

As a final note, it is important to acknowledge that while bank deposits can offer insights into local economic conditions, they may also be influenced by other factors, such as banking policies or management of commercial banks. For instance, there are shreds of evidence for the period of the Great Depression that commercial banks remained profitable and could pass the 1930s with minimal loss (Alcidi and Gros 2011). Therefore, banking deposits may understate the true exposure to economic condition, and, hence, our results provide a lower bound of true associations.

Data availability

The data and replication codes are available upon request from the corresponding author.

Notes

Several explanations have been provided in the literature for such a staggering improvement, including rising incomes and economic development (Acemoglu & Johnson 2007; Costa 2015; Fogel 1994; Preston 1975), the introduction of new drugs and scientific innovations (Bleakley 2007), and/or public health investments (Anderson et al. 2022; Cutler & Miller 2005).

The deposits reflect both the supply and the demand of credit in the local area. For instance, an economic downturn destroys local jobs and reduces earnings and subsequent savings. On the other hand, it also affects market expectations about the future of the economy and influences the decisions of firms in their demand for credit. However, we show that the equilibrium quantity co-moves strongly and significantly with alternative measures of the economy such as income and retail sales.

Our paper also contributes to an emerging literature that has looked at the role of economic resources—through specific welfare programs—on longevity. Two recent studies by Aizer et al. (2016a, b) and Aizer et al. (2020) that focused on the introduction of the U.S. Mother’s Pension program in 1937 and the largest youth training program in history implemented during the New Deal, respectively, showed significant effects of these government interventions on beneficiaries’ life expectancy.

Although these mediatory channels are post-birth outcomes, there is another channel through which economic conditions affect infants’ health: maternal stress. Financial distress resulting from worsening economic conditions may impose mental pressure among pregnant mothers, resulting in adverse birth outcomes (Carlson 2015; Lindo 2011). Besides, the impact of changes in local economic condition is different across sociodemographic groups (Hoynes et al. 2012). In Appendix J, we show that the association between early-life bank deposits and later-life mortality are significantly larger for low-educated mothers, further supporting the maternal stress mechanism.

One concern is that there is evidence that economic conditions are associated with birth outcomes, including preterm birth (Salazar et al. 2023). Therefore, the assumption of a 9-month gestation might not accurately capture the actual exposure. In Appendix K, we show that the effects are comparable and even slightly larger when we use a 7-month pre-birth weighted average.

The bank deposit data does not include data for Wyoming and DC. Also, the 1940 census does not include Alaska and Hawaii. These states are therefore omitted from the sample.

In Appendix E, we also re-do this analysis using the Numident data (death years of 1988–2005). As reported in Appendix Table E-1, we observe a small though statistically significant coefficient for successful merging between Numident death records and the 1940 census. However, the point estimates are minuscule and become insignificant for further subsample analyses.

The difference in R-squared of the full specification of column 4 and column 1 is relatively small, roughly 1.4% of baseline R-squared of column 1. However, the coefficients of race, father socioeconomic index, and maternal education are all statistically significant. Therefore, the minor change in R-squared does not refer to the lack of relevance of these variables.

This number is the average association for both men and women. We should emphasize that our sample covers males only.

The sample covered in their study covers males only, hence comparable to our study sample.

Their study also focuses on male individuals only, hence comparable to our study sample.

Since this analysis examines the contemporaneous impact of economic conditions, the “year” variable is the same as “birth year.”

We use county-level per-capita deposits and use a weighted average of this value for each state where weights are mean county population over the sample period.

In Appendix L, we use both retail sale per capita and bank deposits in the same regression. We find insignificant effects of retail sale but large and significant coefficient for bank deposits. We argue that as these two variables are highly correlated and contain similar information, most of the variations of retail sale is captured by bank deposits.

We add 11 dummies for birth-month and 11 separate dummies for death month into our regressions.

In this section, we avoid restricting the sample based on migration status. The main reason is that the population of migrants and non-migrants differ systematically. In Appendix F, we show that non-migrants in the 1960 census are significantly lower educated and have lower socioeconomic status than migrants where migration is based on state-of-birth and current state of residence. Therefore, selection based on migration is endogenous and causes sample selection concerns. However, in Appendix F, we examine the effects among migrants and non-migrants and find that the estimated effects are fairly similar among these two groups.

We use the variable indicating birth year in the 1960 censuses to identify cohorts born between 1926 and 1936. The reason behind this cohort selection is to have a sample of cohorts similar to the DMF-census-linked sample used in the main analysis of the paper.

Since in many cases PUMA contains several SEAs, most of the identifying variation comes from PUMA-year level, we avoid using SEA-year fixed effects. Instead, we include region-year fixed effects.

These figures are calculated by multiplying the associated change in bank deposits during this period, using the correlation between income and bank deposit in Table 8, and a drop of 1.5 SD in income during this period, hence an inflating factor of \(\frac{1.5}{0.4}=3.75\).

Their study uses CenSoc-Numident data and covers both men and women. Their heterogeneity analyses by race suggests slightly larger effects among male individuals.

The treatment-on-treated calculation of Fletcher and Noghanibehambari (2023) suggests 1.6 years of increased longevity as a result of college education. We combine this number with the estimated effect of column 2 of Table 11 assuming that the effects solely operate through college education channel. Hence, a one-standard deviation rise in deposits is associated with 0.0057 \(\times\) 1.6 years or 0.11 months of additional life. This number is 6.4% of the marginal effect of the reduced-form effect of deposits in longevity reported in column 4 of Table 4 (100 \(\times\) 0.11/1.7).

Their study covers a male-only sample, similar to the study sample of the current study.

References

Abiona O, Ajefu JB (2023) The impact of timing of in utero drought shocks on birth outcomes in rural households: evidence from Sierra Leone. J Popul Econ 36(3):1333–1362. https://doi.org/10.1007/S00148-022-00926-W/FIGURES/2

Acemoglu D, Johnson S (2007) Disease and development: the effect of life expectancy on economic growth. J Polit Econ 115(6):925–985. https://doi.org/10.1086/529000/SUPPL_FILE/32236DATA.ZIP

Aizer A, Eli S, Ferrie J, Muney AL (2016) The long-run impact of cash transfers to poor families. Am Econ Rev 106(4):935–971. https://doi.org/10.1257/AER.20140529

Aizer A, Eli S, Lleras-Muney A, Lee K (2020) Do youth employment programs work? Evidence from the new deal. https://doi.org/10.3386/W27103

Aizer A, Stroud L, Buka S (2016) Maternal stress and child outcomes: evidence from siblings. J Hum Resour 51(3):523–555. https://doi.org/10.3368/jhr.51.3.0914-6664R

Alcidi C, Gros D (2011) Great recession versus great depression: monetary, fiscal and banking policies. J Econ Stud 38(6):673–690. https://doi.org/10.1108/01443581111177385/FULL/XML

Almond D, Currie J (2011) Killing me softly: the fetal origins hypothesis. J Econ Perspect 25(3):153–172. https://doi.org/10.1257/JEP.25.3.153

Almond D, Currie J, Duque V (2018) Childhood circumstances and adult outcomes: act II. J Econ Lit 56(4):1360–1446

Almond D, Mazumder B, van Ewijk R (2015) In utero Ramadan exposure and children’s academic performance. Econ J 125(589):1501–1533. https://doi.org/10.1111/ecoj.12168

Anderson DM, Charles KK, Rees DI (2022) Reexamining the contribution of public health efforts to the decline in urban mortality. Am Econ J Appl Econ 14(2):126–157. https://doi.org/10.1257/APP.20190034

Arthi V (2018) “The dust was long in settling”: human capital and the lasting impact of the American Dust Bowl. J Econ Hist 78(1):196–230. https://doi.org/10.1017/S0022050718000074

Atherwood S (2022) Does a prolonged hardship reduce life span? Examining the longevity of young men who lived through the 1930s Great Plains drought. Popul Environ 2022:1–23. https://doi.org/10.1007/S11111-022-00398-W

Bailey M, Clay K, Fishback P, Haines M, Kantor S, Severnini E, Wentz A (2016) U.S. county-level natality and mortality data, 1915-2007. Inter-University Consortium for Political and Social Research. 10.3886/E100229V4

Baird S, Friedman J, Schady N (2011) Aggregate income shocks and infant mortality in the developing world. Rev Econ Stat 93(3):847–856. https://doi.org/10.1162/REST_a_00084

Barker DJP (1990) The fetal and infant origins of adult disease. BMJ: Br Med J 301(6761):1111

Bengtsson T, Broström G (2009) Do conditions in early life affect old-age mortality directly and indirectly? Evidence from 19th-century rural Sweden. Soc Sci Med 68(9):1583–1590. https://doi.org/10.1016/J.SOCSCIMED.2009.02.020

Bernanke BS (1983) Non-monetary effects of the financial crisis in the propagation of the Great Depression. NBER working paper series

Black DA, Kolesnikova N, Sanders SG, Taylor LJ (2013) Are children “normal”? Rev Econ Stat 95(1):21–33. https://doi.org/10.1162/REST_A_00257

Black SE, Devereux PJ, Salvanes KG (2007) From the cradle to the labor market? The effect of birth weight on adult outcomes. Q J Econ 122(1):409–439. https://doi.org/10.1162/qjec.122.1.409

Bleakley H (2007) Disease and development: evidence from hookworm eradication in the American South. Q J Econ 122(1):73–117. https://doi.org/10.1162/QJEC.121.1.73

Bogue DJ (1951) State economic areas: a description of the procedure used in making a functional grouping of the counties of the United States. US Government Printing Office

Carlson K (2015) Fear itself: the effects of distressing economic news on birth outcomes. J Health Econ 41:117–132. https://doi.org/10.1016/j.jhealeco.2015.02.003

Caruso G, Miller S (2015) Long run effects and intergenerational transmission of natural disasters: a case study on the 1970 Ancash Earthquake. J Dev Econ 117:134–150. https://doi.org/10.1016/j.jdeveco.2015.07.012

Chang G, Favara M, Novella R (2022) The origins of cognitive skills and non-cognitive skills: the long-term effect of in-utero rainfall shocks in India. Econ Hum Biol 44:101089. https://doi.org/10.1016/J.EHB.2021.101089

Chetty R, Stepner M, Abraham S, Lin S, Scuderi B, Turner N, Bergeron A, Cutler D (2016) The association between income and life expectancy in the United States, 2001–2014. JAMA 315(16):1750–1766. https://doi.org/10.1001/JAMA.2016.4226

Chyn E (2018) Moved to opportunity: the long-run effects of public housing demolition on children. Am Econ Rev 108(10):3028–3056. https://doi.org/10.1257/AER.20161352

Clark AE, D’Ambrosio C, Rohde N (2021) Prenatal economic shocks and birth outcomes in UK cohort data. Econ Hum Biol 41:100964. https://doi.org/10.1016/J.EHB.2020.100964

Clay K, Portnykh M, Severnini E (2019) The legacy lead deposition in soils and its impact on cognitive function in preschool-aged children in the United States. Econ Hum Biol 33:181–192. https://doi.org/10.1016/J.EHB.2019.03.001

Cohen A, Dehejia R, Romanov D (2013) Financial incentives and fertility. Rev Econ Stat 95(1):1–20. https://doi.org/10.1162/REST_A_00342

Costa DL (2015) Health and the economy in the united states from 1750 to the present. J Econ Lit 53(3):503–570. American Economic Association. https://doi.org/10.1257/jel.53.3.503

Currie J (2009) Healthy, wealthy, and wise: socioeconomic status, poor health in childhood, and human capital development. J Econ Lit 47(1):87–122. https://doi.org/10.1257/jel.47.1.87

Currie J, Rossin-Slater M (2015) Early-life origins of life-cycle well-being: research and policy implications. Journal of Policy Analysis and Management : [The Journal of the Association for Public Policy Analysis and Management] 34(1):208–242. https://doi.org/10.1002/PAM.21805

Currie J, Schwandt H (2014) Short- and long-term effects of unemployment on fertility. Proc Natl Acad Sci USA 111(41):14734–14739. https://doi.org/10.1073/PNAS.1408975111/SUPPL_FILE/PNAS.1408975111.SAPP.PDF

Cutler D, Deaton A, Lleras-Muney A (2006) The determinants of mortality. J Econ Perspect 20(3):97–120. https://doi.org/10.1257/JEP.20.3.97

Cutler DM, Miller G, Norton DM (2007) Evidence on early-life income and late-life health from America’s Dust Bowl era. Proc Natl Acad Sci 104(33):13244–13249

Cutler D, Miller G (2005) The role of public health improvements in health advances: the twentieth-century United States. Demography 42(1):1–22. https://doi.org/10.1353/DEM.2005.0002

Deaton A (2003) The great escape. Health, wealth, and the oringins os inequality. Prinncenton University Press

Docquier F (2004) Income distribution, non-convexities and the fertility–income relationship. Economica 71(282):261–273. https://doi.org/10.1111/J.0013-0427.2004.00369.X

Duque V, Schmitz L (2021) The influence of early-life economic shocks on aging outcomes: evidence from the U.S. Great Depression. SSRN Electron J. https://doi.org/10.2139/SSRN.3985570

Fishback PV, Haines MR, Kantor S (2007) Births, deaths, and new deal relief during the Great Depression. Rev Econ Stat 89(1):1–14. https://doi.org/10.1162/REST.89.1.1

Fisher I (1933) The debt-deflation theory of Great Depressions. Econometrica 1(4):337. https://doi.org/10.2307/1907327

Fletcher JM (2018) New evidence on the impacts of early exposure to the 1918 influenza pandemic on old-age mortality. Biodemogr Soc Biol 64(2):123–126. https://doi.org/10.1080/19485565.2018.1501267

Fletcher JM (2018) The effects of in utero exposure to the 1918 influenza pandemic on family formation. Econ Hum Biol 30:59–68. https://doi.org/10.1016/J.EHB.2018.06.004

Fletcher J, Noghanibehambari H (2023) The effects of education on mortality: evidence using college expansions. Health Econ. https://doi.org/10.1002/HEC.4787

Fletcher J, Noghanibehambari H (2024) The siren song of cicadas: early-life pesticide exposure and later-life male mortality. J Environ Econ Manag 123:102903. https://doi.org/10.1016/J.JEEM.2023.102903

Fogel RW (1994) The relevance of malthus for the study of mortality today: long-run influences on health, mortality, labor force participation, and population growth. https://doi.org/10.3386/H0054

Friedman M, Schwartz AJ (1963) A monetary history of the United States, 1867-1960 (Vol. 16). Princeton University Press

Gagnon A, Bohnert N (2012) Early life socioeconomic conditions in rural areas and old-age mortality in twentieth-century Quebec. Soc Sci Med 75(8):1497–1504. https://doi.org/10.1016/J.SOCSCIMED.2012.06.007

Goldstein JR, Alexander M, Breen C, Miranda González A, Menares F, Osborne M, Snyder M, Yildirim U (2021) Censoc Project. In CenSoc Mortality File: Version 2.0. Berkeley: University of California. https://censoc.berkeley.edu/data/. Accessed 15 May 2023

Goodman-Bacon A (2021) The long-run effects of childhood insurance coverage: medicaid implementation, adult health, and labor market outcomes. Am Econ Rev 111(8):2550–2593. https://doi.org/10.1257/AER.20171671

Granados JAT, Roux AVD, Tapia Granados JA, Diez Roux AV (2009) Life and death during the Great Depression. Proc Natl Acad Sci USA 106(41):17290–17295. https://doi.org/10.1073/pnas.0904491106

Grimard F, Laszlo S, Lim W (2010) Health, aging and childhood socio-economic conditions in Mexico. J Health Econ 29(5):630–640. https://doi.org/10.1016/J.JHEALECO.2010.07.001

Halpern-Manners A, Helgertz J, Warren JR, Roberts E (2020) The effects of education on mortality: evidence from linked U.S. census and administrative mortality data. Demography 57(4):1513–1541. https://doi.org/10.1007/S13524-020-00892-6

Hayward MD, Gorman BK (2004) The long arm of childhood: the influence of early-life social conditions on men’s mortality. Demography 41(1):87–107. https://doi.org/10.1353/DEM.2004.0005

Heckman JJ (1979) Sample selection bias as a specification error. Econometrica 47(1):153–161. https://doi.org/10.2307/1912352

Hoynes H, Miller DL, Schaller J (2012) Who suffers during recessions? J Econ Perspect 26(3):27–48. https://doi.org/10.1257/jep.26.3.27

Hoynes H, Schanzenbach DW, Almond D (2016) Long-run impacts of childhood access to the safety net. Am Econ Rev 106(4):903–934. https://doi.org/10.1257/aer.20130375

Lindeboom M, Portrait F, Van Den Berg GJ (2010) Long-run effects on longevity of a nutritional shock early in life: the Dutch Potato famine of 1846–1847. J Health Econ 29(5):617–629. https://doi.org/10.1016/J.JHEALECO.2010.06.001

Lindo JM (2011) Parental job loss and infant health. J Health Econ 30(5):869–879. https://doi.org/10.1016/j.jhealeco.2011.06.008

Ludwig J, Miller DL (2007) Does head start improve children’s life chances? Evidence from a regression discontinuity design. Q J Econ 122(1):159–208. https://doi.org/10.1162/QJEC.122.1.159

Majid MF (2015) The persistent effects of in utero nutrition shocks over the life cycle: evidence from Ramadan fasting. J Dev Econ 117:48–57. https://doi.org/10.1016/j.jdeveco.2015.06.006

Manson S, Schroeder J, Riper DV, Ruggles S et al (2017). IPUMS National Historical Geographic Information System: Version 12.0 [Database]. Minneapolis: University of Minnesota, 39

Miller S, Wherry LR (2019) The long-term effects of early life Medicaid coverage. J Hum Resour 54(3):785–824. https://doi.org/10.3368/jhr.54.3.0816.8173r1

Montez J, Hayward MD (2011) Early life conditions and later life mortality. International Handbook of Adult Mortality, 187–206. https://doi.org/10.1007/978-90-481-9996-9_9

Myrskylä M (2010) The effects of shocks in early life mortality on later life expectancy and mortality compression: a cohort analysis. Demogr Res 22:289–320. https://doi.org/10.4054/DemRes.2010.22.12

Myrskylä M (2010) The relative effects of shocks in early- and later-life conditions on mortality. Popul Dev Rev 36(4):803–829. https://doi.org/10.1111/j.1728-4457.2010.00358.x

Noghanibehambari H, Engelman M (2022) Social insurance programs and later-life mortality: evidence from new deal relief spending. J Health Econ 86. https://doi.org/10.1016/J.JHEALECO.2022.102690

Noghanibehambari H, Fletcher J (2023) Long-term health benefits of occupational licensing: evidence from midwifery laws. J Health Econ 92:102807. https://doi.org/10.1016/J.JHEALECO.2023.102807

Noghanibehambari H, Fletcher J (2024) Dust to feed, dust to gray: the effect of in utero exposure to the Dust Bowl on old-age longevity. Demography. https://doi.org/10.1215/00703370-11140760

Persson P, Rossin-Slater M (2018) Family ruptures, stress, and the mental health of the next generation. Am Econ Rev 108(4–5):1214–1252. https://doi.org/10.1257/aer.20141406

Preston SH (1975) The changing relation between mortality and level of economic development. Popul Stud 29(2):231–248. https://doi.org/10.1080/00324728.1975.10410201

Qian X (2024) Revolutionized life: long-term effects of childhood exposure to persecution on human capital and marital sorting. J Popul Econ

Rosa MJ, Nentin F, Bosquet Enlow M, Hacker MR, Pollas N, Coull B, Wright RJ (2019) Sex-specific associations between prenatal negative life events and birth outcomes. Stress 22(6):647–653. https://doi.org/10.1080/10253890.2019.1608944/SUPPL_FILE/ISTS_A_1608944_SM4672.DOCX

Ruggles S, Flood S, Goeken R, Grover J, Meyer E (2020) IPUMS USA: Version 10.0. Minneapolis, MN: IPUMS. https://doi.org/10.18128/D010.V10.0

Salazar EG, Montoya-Williams D, Passarella M, McGann C, Paul K, Murosko D, Peña MM, Ortiz R, Burris HH, Lorch SA, Handley SC (2023) County-level maternal vulnerability and preterm birth in the US. JAMA Netw Open 6(5):e2315306–e2315306. https://doi.org/10.1001/JAMANETWORKOPEN.2023.15306

Schaller J (2016) Booms, busts, and fertility: testing the becker model using gender-specific labor demand. J Hum Resour 51(1):1–29. https://doi.org/10.3368/jhr.51.1.1

Schaller J, Fishback P, Marquardt K (2020) Local economic conditions and fertility from the Great Depression through the Great Recession. AEA Papers Proc 110:236–240. https://doi.org/10.1257/PANDP.20201109

Schmitz LL, Duque V (2022) In utero exposure to the Great Depression is reflected in late-life epigenetic aging signatures. Proc Natl Acad Sci USA 119(46):e2208530119. https://doi.org/10.1073/PNAS.2208530119/SUPPL_FILE/PNAS.2208530119.SAPP01.PDF

Schoeps A, van Ewijk R, Kynast-Wolf G, Nebié E, Zabré P, Sié A, Gabrysch S (2018) Ramadan exposure in utero and child mortality in Burkina Faso: analysis of a population-based cohort including 41,025 children. Am J Epidemiol 187(10):2085–2092. https://doi.org/10.1093/AJE/KWY091

Scholte RS, Van Den Berg GJ, Lindeboom M (2015) Long-run effects of gestation during the Dutch Hunger Winter famine on labor market and hospitalization outcomes. J Health Econ 39:17–30. https://doi.org/10.1016/J.JHEALECO.2014.10.002

Shah M, Steinberg BM (2017) Drought of opportunities: contemporaneous and long-term impacts of rainfall shocks on human capital. J Polit Econ 125(2):527–561. https://doi.org/10.1086/690828/SUPPL_FILE/2013254DATA.ZIP

Simmerman JM, Chittaganpitch M, Levy J, Chantra S, Maloney S, Uyeki T, Areerat P, Thamthitiwat S, Olsen SJ, Fry A, Ungchusak K, Baggett HC, Chunsuttiwat S (2009) Incidence, seasonality and mortality associated with influenza pneumonia in Thailand: 2005–2008. PLoS ONE 4(11):e7776. https://doi.org/10.1371/JOURNAL.PONE.0007776

Smith AH, Marshall G, Yuan Y, Liaw J, Ferreccio C, Steinmaus C (2011) Evidence from Chile that arsenic in drinking water may increase mortality from pulmonary tuberculosis. Am J Epidemiol 173(4):414–420. https://doi.org/10.1093/AJE/KWQ383

Steptoe A, Zaninotto P (2020) Lower socioeconomic status and the acceleration of aging: an outcome-wide analysis. Proc Natl Acad Sci USA 117(26):14911–14917. https://doi.org/10.1073/PNAS.1915741117

Stuckler D, Meissner C, Fishback P, Basu S, McKee M (2012) Banking crises and mortality during the Great Depression: evidence from US urban populations, 1929–1937. J Epidemiol Community Health 66(5):410–419. https://doi.org/10.1136/JECH.2010.121376

Vaiserman A (2021) Season-of-birth phenomenon in health and longevity: epidemiologic evidence and mechanistic considerations. J Dev Orig Health Dis 12(6):849–858. https://doi.org/10.1017/S2040174420001221

Van Den Berg GJ, Doblhammer G, Christensen K (2009) Exogenous determinants of early-life conditions, and mortality later in life. Soc Sci Med 68(9):1591–1598. https://doi.org/10.1016/J.SOCSCIMED.2009.02.007

Van Den Berg GJ, Gupta S, van den Berg GJ, Gupta S (2015) The role of marriage in the causal pathway from economic conditions early in life to mortality. J Health Econ 40:141–158. https://doi.org/10.1016/j.jhealeco.2014.02.004

Van Den Berg GJ, Lindeboom M, Portrait F, Van Den Berg GJ, Lindeboom M, Portrait F, den Berg GJ, Lindeboom M, Portrait F (2006) Economic conditions early in life and individual mortality. Am Econ Rev 96(1):290–302. https://doi.org/10.1257/000282806776157740

Wang J, Gao ZY, Yan J, Ying XL, Tong SL, Yan CH (2017) Sex differences in the effects of prenatal lead exposure on birth outcomes. Environ Pollut 225:193–200. https://doi.org/10.1016/J.ENVPOL.2017.03.031

Weinberg J, Sliwowska JH, Lan N, Hellemans KGC (2008) Prenatal alcohol exposure: foetal programming, the hypothalamic-pituitary-adrenal axis and sex differences in outcome. J Neuroendocrinol 20(4):470–488. https://doi.org/10.1111/J.1365-2826.2008.01669.X

Yamashita N, Trinh TA (2022) Effects of prenatal exposure to abnormal rainfall on cognitive development in Vietnam. Popul Environ 43(3):346–366. https://doi.org/10.1007/S11111-021-00394-6/TABLES/6

Acknowledgements

The authors would like to thank the anonymous referees for helpful comments and suggestions. We thank editor Xi Chen, two reviewers, and members of the UW Health Economics Working Group for helpful comments.

Funding

The authors received financial support from NIA grants (R01AG060109, R01AG076830, K99AG056599, R00AG056599), the Center for Retirement Research Steven H. Sandell Grant Program pursuant to a grant from the U.S. Social Security Administration (BC20-S2), and the Center for Demography of Health and Aging (CDHA) at the University of Wisconsin-Madison under NIA core grant P30 AG17266.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Disclaimer

The content is solely the responsibility of the authors and does not necessarily represent the official views of the Social Security Administration or the NIA.

Conflict of interest

The authors declare no competing interests.

Additional information

Responsible editor: Xi Chen

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Noghanibehambari, H., Fletcher, J., Schmitz, L. et al. Early-life economic conditions and old-age male mortality: evidence from historical county-level bank deposit data. J Popul Econ 37, 32 (2024). https://doi.org/10.1007/s00148-024-01007-w

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s00148-024-01007-w