Abstract

Central Banks in major industrialized economies have struggled to keep inflation within their target ranges since the global financial crisis. The periods of missing inflation and deflation experienced in the post-crisis era have led to doubts about the traditional Fisher effect as a crucial component of the policy reaction function. We explore the NeoFisherian theory, which suggests an alternative causal relationship between the policy rate and inflation. We focus on the USA, UK, and EU and apply wavelet coherence analysis to examine the time–frequency lead–lag comovements on data spanning from January 2007 to March 2023. Our findings indicate increasing NeoFisherian dynamics, notably post-2013 taper tantrum, implying that Central Banks in industrialized economies have misunderstood monetary policy dynamics.

Similar content being viewed by others

Introduction

Metaphorically, the ‘modus operandi’ of modern Central Bank in controlling inflation can be likened to a person balancing a metre stick (inflation) using their fingertips (interest rates) in an inverted pendulum fashion. To keep the ‘metre stick’ (inflation) balanced, the Reserve Bank must move their hands (interest rates) in the same direction which the metre stick tilts towards. In practice, monetary authorities are guided by the following policy rule in performing this balancing act:

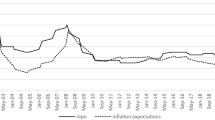

And by following such a policy rule, an independent Central Bank can steer the expectations of economic agents in a time-consistent manner [17] and adjustments in the policy rate works itself through the monetary transmission mechanism [20] together with the Phillips curve dynamics into the real economy. When inflation surpasses the target, increasing interest rates make saving more attractive than borrowing, leading to reduced spending/consumption and ultimately output. This prompts price setters to lower their prices, via the Phillips curve dynamics, due to the cooling of the economy. Conversely, when interest rates are lowered, the opposite effect occurs. It is important to note that even though interest rates have an inverse impact on inflation, the relationship appears positive due to the balancing act undertaken by Central Banks to counteract inflation. The observed positive co-movement between nominal interest rates and inflation is known as the Fisher effect and is easily observed from the scatterplot for the USA, EU and the UK in the post-global financial crisis (GFC) era in Fig. 1 below.

Scatterplot of interest rates an inflation in USA, EU and UK (2007:m01 to 2023:m03)

Following the 2007–2008 GFC, industrialized economies implemented unconventional monetary policies (UMPs) to overcome the limitations of the ‘zero-bound’ liquidity trap and stimulate their economies. However, certain inflation puzzles have emerged in these economies since then [2, 4, 22, 23]. Firstly, during the brink of a global recession in 2008–2009, Central Banks in the USA, EU and UK reduced interest rates close to zero and implemented UMPs. According to traditional theory, this should have increased inflation, but instead, inflation decreased to near-zero levels. Secondly, when the USA decided to revert to a ‘normal policy’ in 2015 and raise interest rates, inflation began to slightly increase, contrary to traditional expectations. Thirdly, following the announcement of the COVID-19 pandemic in 2020, the Central Banks in industrialized economies once again lowered interest rates close to zero and implemented UMPs, resulting in near-zero rates and recording high savings rates. Lastly, when the Ukraine–Russia war started in 2022, the Central Banks increased interest rates which was accompanied by rising inflation, thus presenting an ongoing puzzle

The NeoFisher hypothesis provides a theoretical explanation for these puzzles, suggesting that in industrialized economies, inflation started responding positively to changes in interest rates, rather than the reverse [29]. The core idea behind the NeoFisher hypothesis is that maintaining and committing to the zero-interest-rate policy (ZIRP) for a sufficiently long period of time could lead to a unique and ‘unintended’ steady state characterized by low inflation expectations and actual inflation [7]. Any increase in interest rates from the zero lower bound, even if intended to be temporary, will be viewed as permanent as it represents a permanent shift by the Central Bank towards ‘normalization’ and rational agents do not expect the central bank to return to UMPs but anticipate a continued increase in interest rates in the future [24]. Consequentially, NeoFisherian economists propose the pegging of interest rate as the most suitablė policy stance, which itself is a controversial recommendation since Friedman [12] famously contended that such policy actions can lead to a hyper-inflationary or deflationary spiral [8, 27,28,29,30].

Nonetheless, there is limited empirical research on the NeoFisher effect in industrialized economies outside the USA. Moreover, existing empirical studies examining the NeoFisherian effect in the US rely on VAR-type granger causality tests and impulse response functions and provide inconclusive evidences [5, 9, 28]. The lack of conclusive findings can be attributed to the stringent stationary requirements as well as sensitivity to structural breaks and nonlinearity in the time series methods used in these studies. To address these issues, we employ wavelet coherence analysis to investigate the NeoFisher hypothesis. This analysis examines the co-movement between two variables in a scale-by-scale manner across a time window, allowing for the analysis of causal effects, directions, and magnitudes across different time periods and frequency oscillations. The wavelet coherence method utilized in this study is noteworthy for producing results that are insensitive to the selected time window and free from possible regression errors. Consequently, there is no need to conduct analyses across distinct subsamples, as wavelet analysis inherently accounts for structural breaks and various forms of asymmetry within the data.

To the best of our knowledge, our study represents the first empirical validation of the NeoFisher effect in the USA, UE, and UK. Our research uncovers that the behaviour of monetary policy in these industrialized economies displays variations over time and in terms of frequency. Particularly noteworthy is the emergence of significant NeoFisher effects during the ‘taper tantrum’ in 2014–2015, which have remained consistently observable in subsequent periods. These findings align with the theoretical insights proposed by Schmitt-Grohe and Uribe [24], suggesting a shift in the dynamics of monetary policy following the convergence of Central Banks to the zero lower bound in the aftermath of the Global Financial Crisis. Furthermore, our study extends the arguments advanced by Williamson [29] and Uribe [28] by illustrating that NeoFisherian effects exhibit both transitory and permanent characteristics, particularly in the wake of the implementation of Unconventional Monetary Policies (UMP) as a response to the COVID-19 pandemic.

In summary, our findings imply that the understanding of monetary policy dynamics in industrialized economies has been inaccurate. This has significant implications for the credibility of policy decisions in these economies and can also lead to spillover effects on other Central Banks worldwide that look to the decisions of these influential reserve banks as models.

The rest of the study is structured as follows. Sect. "Overview of the NeoFisher effect" outlines the theoretical framework. Sect. "Methodology and data" describes the methodology. Sect. "Data and empirical strategy" presents the data and empirical strategy. Sect. "Results and discussions" presents the results and discussions whilst Sect. "Conclusions, policy implications and recommendations" concludes the study.

Overview of the NeoFisher effect

Conceptual framework

NeoFisherism has arisen as a ‘nonconventional’ conceptual framework for monetary policy which extends on the traditional Fisher identity i.e.

where \({r}_{t}\) is the real interest rate, \({R}_{t}\) is the nominal interest rate, and \({\pi }_{t}^{e}\) are inflation expectations, and assume the adjustment process of the form:

such that \({r}_{t}\) converges to its natural equilibrium \({r}^{*}\) and \({\Delta R}_{t}\) cause \(\Delta {\uppi }_{t}^{e}\). In other words, if \({R}_{t}\)(↑), then \({r}_{t}\)(↑) eventually returns to \({r}^{*}\), causing \(\Delta {\pi }_{t}^{e}\) (↑), and also vice-versa (see Fig. 2). In this sense, NeoFisher differs from the traditional Fisher effects in that nominal interest rates lead to inflation and not vice versa. Metaphorically speaking, NeoFisherism envisions the Central Banker as person holding the metrestick upside down as a pendulum and not upright as an inverted pendulum.

Response to a permanent increase in the nominal interest rate at time t

Theoretical arguments

Theoretically, the NeoFisher effect has been verified in the standard 3-equation New Keynesin (NK) model consisting of an IS schedule, the Phillips curve and the Taylor rule. Schmitt-Grohe and Uribe [24] were amongst the first to demonstrate how an economy constrained by a liquidity trap operates in an abnormal equilibrium characterized by a spiral deflation process with low output, where both UMP and the Taylor rule lose their effectiveness. They suggest a pegged interest rate-based strategy as an alternative means of escaping these liquidity traps. Furthermore, Cochrane [8] critiques the assumption of an unstable steady-state Fisher relationship underlying the policy reaction function, which requires continuous adjustment of interest rates to maintain inflation within its target. He argues that the stability of inflation at the zero bound implies that a steady Fisher relationship can hold even if interest rates are pegged. Under conditions of fiscal–monetary coordination, the economy converges to the interest rate peg minus the real rate as a continuum of perfect foresight equilibria, holding even in the presence of sticky prices, backward-looking Phillips curve, active Taylor rules, and alternative equilibrium selection rules.

Nonetheless, some researchers have presented theoretical contentions to the NeoFisher dynamics. For instance, Garin et al. [14] contend that the NeoFisher effect is limited to a New Keynesian framework, where persistent inflation targets, flexible prices, and forward-looking consumption decisions are present. However, when the model incorporates backward-looking "rule of thumb" price-setters, expectations formations become less forward-looking, reducing the likelihood of a NeoFisher effect. Similarly, Garcia-Schmidt and Woodford [13] argue that the NeoFisher effect does not hold in a New Keynesian framework when agents form expectations through explicit cognitive processes. This leads to a belief reversion process that allows for the perfect foresight equilibrium to emerge as a limiting case of a reflective equilibrium. Under fixed or pegged interest rates, the NeoFisherian equilibria become a special case where economic agents do not need to engage in further reflection on future consumption and interest rate decision.

More recently, Bilbiie [6] attempt to bring harmony between two seemingly discordant perspectives. Specifically, the author proposes a consolidated New Keynesian framework that advocates the appropriateness of NeoFisherian monetary policies in mitigating a liquidity trap that originates from confidence-related factors. Conversely, in circumstances where liquidity traps stem from underlying economic fundamentals, traditional Fisherian policies should be pursued. The main implication is that policymakers should be mindful of the origins of liquidity traps, as the monetary–fiscal prescriptions for these predicaments are diametrically opposed.

All in all, the contention between ‘traditional’ and Neo-Fisherian theories evolves on the direction of causality between inflation expectations and nominal interest rates in stabilizing the real interest rate. Empirically, both theories can be formally tested via the following hypotheses, i.e.

H0

Inflation expectations granger causes interest rates (traditional hypothesis).

H1

Interest rates granger causes inflation expectations (Neo-Fisherian hypothesis).

Empirical evidence

Considering that the NeoFisher hypothesis is a post-GFC phenomenon, it is not that surprising that the empirical literature on the subject is relatively small and growing. After conducting an extensive search of the literature on ‘google scholar’, we are only able to obtain 3 empirical studies and it is interesting to note that the currently available literature on industrialized economies has exclusively focused on the US economy. Bias and Hall [5] test for NeoFisher effects between January 1964 and April 2019 using vector autoregressive (VAR)-based causality tests at different sub-samples and find some NeoFisher effects for some sub-samples before 2008 but not afterwards. Similarly, Crowder [9] applies a VAR model to data spanning from January 1959 to December 2015 and also finds little NeoFisher effects between nominal interest rates and inflation. Lastly, Uribe [28] uses a structural VAR to show that permanent (temporary) shocks in the nominal interest rates lead (do not lead) to NeoFisher effects in the data.

From the currently literature, we identify three gaps in the current empirical literature which our study aims to fill. Firstly, and as mentioned before, previous studies exclusive focus on the US economy. Secondly, previous studies do not focus on periods subsequent to the emergence of the COVID-19 pandemic and consequentially do not account for the periods of missing deflation experienced since the start of the Ukraine–Russia war. Lastly, previous studies focus on VAR-based framework which is linear in functional form and do not account for structural breaks and other forms of nonlinearities contained in the data.

We contribute to the empirical literature by testing for the NeoFisher effects in the US, EU and UK in the post-GFC era using a battery of causality tests on interest rates and inflation. Firstly, we follow previous literature and employ VAR-causality tests to examine lead–lag relations in the time domain. Secondly, we use the frequency causality tests to examine lead-lag relations across different frequency components. Lastly, we use the wavelet coherence analysis to examine the lead–lag relations in time–frequency space. The conceptual details of the methods are given the following section.

Methodology and data

VAR-based causality tests

We firstly use a bivariate VAR(p) model of Sims [25] to test for causality effects, in the Granger [16] sense, between the nominal interest rates (i) and inflation (π). We specify the model as:

where α and β are the VAR regression coefficients which are estimated by OLS, i, is the optimal lag length determined by minimization of the AIC and BIC and the eti are regression residuals. To test for causality from inflation to nominal interest rates (i.e. the traditional Fisher effect), we impose the following restriction, \({\beta }_{\mathrm{1,1}}= {\beta }_{\mathrm{1,2}}=\dots ={\beta }_{1,j}=0\), on Eq. (4) which results in the following restricted regression.

whereas to test for reverse causality from interest rates to inflation (i.e. NeoFisher effect), we impose the following restriction, \({\alpha }_{\mathrm{2,1}}= {\alpha }_{\mathrm{2,2}}=\dots ={\alpha }_{2,j}=0\), on Eq. (5) which results in the following restricted regression:

Thereafter, we extract the sum squares of residuals (SSR) for the restricted regression (4) and (5) as well as the unrestricted regressions (6) and (7), and compute the following F-statistic:

where q is the number of restrictions, n is number of observations and k is the number of independent variables in the equation. The calculated F-statistics are compared against the critical values tabulated in the conventional F-tables. Significant causality effects are confirmed if the obtained F-statistic exceeds its associated 10 percent critical value at the relevant degrees of freedom.

Frequency-domain causality tests

The second type of causality tests we perform is in frequency domain of Geweke [15] which is a version of the VAR-based causality tests in frequency domain. The advantage of the frequency domain causality tests lies in the disentanglement of the causality structure across a range of frequencies whereas the traditional time domain based causality tests [11].

By compactly defining our bivariate VAR model Zt = [it, πt] = [Yt, Xt], the transfer of the VAR model into frequency domain is conducted using the following transfer function defined as:

where is the frequency level constrained as -π ≤ ω ≤ π. Further setting the matrix P(ω) as:

allows one to compactly represent Eq. (9) in the following spectrum form:

where * is a complex conjugate transpose, Σ2 is set as \(\left(\begin{array}{cc}{\sigma }_{2}& {\upsilon }_{2}\\ {\upsilon }_{2}& {\gamma }_{2}\end{array}\right)\) with a transform matrix S=\(\left(\begin{array}{cc}1& 0\\ -\frac{{\upsilon }_{2}}{{\sigma }_{2}}& 1\end{array}\right)\) which is used to derive the transform transfer function i.e.

Thereafter, granger causality spectrum describing causality from variable Xt to variable Yt is defined as:

such that if \(\underset{X\to Y}{{\text{h}}}\left(\omega \right)\) > 0, then the past values of Xt predict the present values of Yt at frequency cycle of ω−1.

Wavelet coherence analysis

Lastly, we employ continuous wavelet analysis which can be considered a major step-up from time series-based econometric techniques such as the VAR, and present a multiresolution analysis of signal or time-series in time–frequency space. Lau and Weng [18] present an excellent analogy to explain the concept of wavelet transforms applied to time series data by comparing this transformation process to converting a two-dimensional written musical score into three-dimensional audible music tones, characterized by frequency, time position and duration, and intensity. In practice, these transforms convolute a time series with a set of complex-valued ‘daughter wavelets’ defined as:

where * is the conjugate of the complex number; τ and s are the translation and dilation parameters responsible for amplitude and phase dynamics in time–frequency space. The mother wavelet which is responsible for the shape of the daughter wavelets is defined as the following Morlet et al. [21] function:

\(\psi \left(t\right)={\pi }^{-\frac{1}{4}}{\text{exp}}\left(i\upomega t\right){\text{exp}}(-\frac{1}{2}{t}^{2})\), (15). where ω0 is set at 2π to ensure optimal joint time–frequency resolution. We can then compute the wavelet power spectrum (WPS) of the time series as:

where δt is a uniformed time step. The WPS is a representation of the enrgy distribution of the series in a time–frequency plance and is analogous to the variance.

The wavelet coherence analysis between a pair of time series across a time–frequency plane is closely related with the concept of Fourier coherency [1, 26]. Given the WPS for a pair of time series x(t) and y(t) (i.e. Wxx =|Wx|2 and Wyy =|Wy|2), their cross-wavelet transform (CWT) can be defined as (WPS)xy = Wxy =|Wxy|, from which the wavelet coherence, is computed as:

where S is a smoothing operator in both time and scale. The phase-difference dynamics are determined as:

where π < ϕx,y < -π and it provides information on i) whether the pair of series are in-phase (positive) or antiphase (negative) synchronized and ii) whether x leads y or vice-versa.

Data and empirical strategy

Empirical data

To test for NeoFisher effects, we use monthly nominal interest rate and inflation data spanning from 2007:M03 to 2023:M03 which are collected from two sources. Firstly, we source our measures of nominal interest rates from Rapheal De Rezende’s website (https://www.rafaelbderezende.com/shadow-rates) which presents time series measure of conventional interest rates such as the US Federal Fund rate (FFR), the UK bank rate (uk_br) and ECB main refinancing operations rate (EU_rate) as well as the shadow short rate (SSR) estimates for the US (US_SSR), the EU (EU_SSR) and the UK (UK_SSR). A detailed description of the construction of the SSR is provided in De Rezende and Ristiniemi [10]. For US and EU inflation, we use conventional CPI inflation sourced from Federal Reserve Economic Data (https://fred.stlouisfed.org/) online database whilst the UK CPI inflation is sourced from the UK Office for National Statistics (ONS) website (https://www.ons.gov.uk/).

The summary statistics of the variables presented in Table 1 showed some well-known stylized facts on inflation and interest rates in industrialized economies in the post-GFC. For starters, the averages of all employed time series are close to zero reflecting the fact that the industrialized economies have been in a ‘low interest rate’, ‘low inflation’ environment for a majority of the post-GFC period. Furthermore, the averages and minimum values are lower for the SSR compared to the traditional interest rate variables since the former captures a hypothetical negative interest rate corresponding to expansionary policy reflected by the UMP. Lastly, note that all series are slightly positive skewed and leptokurtic indicating that the variables are not normally distributed and most interest rate series contain unit roots whilst the inflation variables are stationary. Therefore, in conducting the VAR-based causality and frequency causality tests, we use the first differences of the interest rate variables as is required for estimation purposes. Moreover, the Johansen cointegration tests performed on different pairs of interest rate and inflation data, as reported in Table 2, further provide evidence.

Empirical strategy

In conducting our empirical analysis, we segregate our data across two dimensions for robustness sake. Firstly, for the VAR- and frequency-based causality tests, we conduct our empirical analysis across three sub-samples segregated by two structural break points as determined by the Bai and Perron [3] tests, i.e. 2009–2016, 2016–2020 and 2020–2023 (see Table 3 for results). We use this strategy to determine whether the results from the time and frequency causality tests are susceptible to structural breaks. Secondly, we use alternative specifications of the (Neo)Fisher hypothesis, with one traditional policy rates as a conventional measure of nominal interest rates and the other using the SSR as an unconventional measure of interest rates which accounts for the stimulating effects of UMP in a hypothetical negative interest rate environment. We use this strategy to determine whether our empirical estimates are sensitive to the type of data used in measuring monetary policy stance. Also given the sheer volume of the empirical results, we only report a summary of the findings from our empirical analysis and provide the more detailed results in Tables and Figures in Appendix.

Results and discussions

VAR causality results

Table 4 summarizes results of the VAR-based granger causality tests performed on lags determined by the AIC and SC information criterion. Panel A (Panel B) of the table reports the causality effects using the traditional policy rate (SSR) as the measure of nominal interest rates at different sub-periods. The bold entries in the table highlight the results which are consistent across both measures of nominal interest rates of which we find 6 out of 12 mutual entries in each panel. The 4 italic shaded entries further show causalities describing the NeoFisher effect of which two show these effects for the USA using the full sample whilst the last is for the EU in the 2nd sub-period. The full set of results summarized in Panels A and B of Table 4 are found in Appendices I and II, respectively.

Overall, we find that with the exception of the US in the full sample, the remaining regressions appear to be sensitive to both choice of measure of nominal interest and also to selected time periods. Moreover, our findings are contrary to those of Bias and Hall [5] who use similar VAR causality tests and find little evidence NeoFisher causality effects for the US in the post-GFC era. Also considering that all economies mutually registered no causal effects between the time series in the post-COVID era is an indication that the number of observations used in this period may not suffice to induce any significant relations between the variables.

Frequency-domain causality results

Next, we present the results from the frequency domain causality tests which differs from the VAR-based causality tests which only aggregates the causal dynamics between two series across an entire time window. Conversely, the frequency-domain tests measure the extent to which past behaviour of one series influences the behaviour of another series across a frequency spectrum, ω, ranging from low frequencies to high frequencies in incremental proportions. Distinguishing between low- and high-frequency causality dynamics is important in our context since the ‘mild view’ of the NeoFisherian hypothesis, as described by Cochrane [8] and Uribe [28], allows for the possibility of traditional Fisher effects over transitory periods or high-frequency bands whist the economy converges to NeoFisher dynamics over the long run or low-frequency bands. On the other hand, the ‘pure view’ of the NeoFisher effect assumes that shocks in nominal interest rates affect inflation in both transitory and permanent horizons.

From Table 5, which summarizes the findings from the spectrum causality tests reported in Appendices III and IV, we observe that for all economies all entries except for those for high-frequency causalities in the 1st sub-sample are highlighted in ‘bold’ indicating that the results are less sensitive to the chosen measure of nominal interest rates used in the analysis. Moreover, at low frequencies we mutually find bi-directional causality across all sub-periods whereas discrepancies are solely observed at high-frequency causality. In fact, we observe NeoFisherian causalities for the USA and UK, for full sample, and the UK, the 3rd sub-sample, at higher frequencies, hence confirming the ‘pure view’ of the NeoFisher effect over transitory periods. However, one notable shortcoming with spectrum causality tests is that they inform us of lead-lag relations across different frequencies and yet do not indicate at which time these causalities occur [1, 26]. Overall, these findings do not advocate for long-run Neo-Fisher effect in industrialized economies and at best suggest that these effects are temporal.

Wavelet coherence results

Finally, we look at the results obtained from the wavelet coherence analysis, which presents the ‘best of both worlds’ in being able to localize the variables in both time and frequency space. The wavelet coherence analysis is represented in a 2-dimensional heatmap plots which describes the phase-dynamics between the variables and provides information on the strength (represented by the colour contours) sign and direction of causality (represented by arrow orientation) between the series. These are presented in Appendix V (Appendix VI) for the analysis with the traditional policy rates (SSR) as measure of nominal interest rates. It is interesting to note from these plots, that the same time–frequency dynamics are shown for USA, EU and UK regardless of the measure of nominal time series used. From the wavelet plots reported in Appendix, we observe 3 mutual phases of time–frequency co-relations for the US, UK and EU whose details we are reported in Table 6.

-

The first phase, ranging from 2007 to 2013, reveals inphase or positive correlations between interest rates and inflation, with inflation causing nominal interest rates (i.e. traditional Fisher effects) in the higher-frequency bands of 16 to 40 month cycles whereas reverse causality (i.e. NeoFisher effects) is observed at lower-frequency bands of 40- to 64- month cycles.

-

From the second phase, ranging from 2013–2017, only low-frequency bands of inphase correlations between 40- and 64- month cycles are observed, with nominal interest rates causing inflation (i.e. NeoFisher effects).

-

The third phase, ranging from 2017–2023, reveals inphase or positive correlations with nominal interest rates causing inflation (i.e. NeoFisher effects) at both low-frequency (16 to 40 month cycles) and low frequency (40- to 64- month cycles) bands.

Altogether these finding imply that all industrialized economies experienced mild NeoFisher, described by Cochrane [8] and Uribe [28] effects during the first rounds of UMP in response to the GFC, whereby traditional Fisher effects are experienced in the transitory period whilst NeoFisher effects are experienced over permanent horizons. However, from the taper tantrum of 2013–2014, when Central Banks began to unwind their balances, these transitory effects disappear, leaving only low-frequency NeoFisher effects. Finally, towards the COVID-19 and stretching to the Ukraine-Russia war, transitory effects re-emerge and this time both transitory and permanent NeoFisher effects are present whereas traditional Fisher causality is not observed. One plausible explanation for these dynamics, as argued in Marques and Carvalho [19], is that during periods when the Central Banks lowered interest rates close to zero this sends a signal to price setters that the Central Bank is not concerned with inflation hence resulting in low inflation expectations. Conversely, when Central Banks revert back to ‘normalization’, this signals their concerns with inflation, hence causing economic agents to increase their expectations of future inflation.

Conclusions, policy implications, and recommendations

We examine the NeoFisher effect in USA, EU and UK using VAR causality tests, frequency-causality tests and wavelet coherence analysis applied to monthly data of nominal interest rates and inflation spanning 2007:m01 to 2023:m03. Our study highlights the advantages of wavelet coherence analysis over traditional VAR and frequency-based models in investigating the NeoFisher hypothesis in industrialized economies. We find that VAR and frequency-domain causality tests are sensitive to structural breaks in the data and/or the choice of interest rate variables. In contrast, wavelet coherence analysis is robust to such variations. Consequently, we consider the results from wavelet analysis more reliable than those relying on conventional VAR-based methods.

Our wavelet analysis indicates that monetary policy in industrialized economies has displayed NeoFisher behaviour. This suggests a fundamental misunderstanding of monetary policy dynamics since the global financial crisis. Initially, during the first few rounds of UMP in response to the GFC, traditional Fisher effects were short-lived, whilst NeoFisher effects persisted. However, after nearly a decade of being constrained by the zero lower bound, the dynamics became predominantly NeoFisherian, even during periods of ‘normalization’ following events like the Ukraine–Russia war when inflation exceeded its target.

Our findings are important since they imply that Central Banks in industrialized economies have failed to figure out their monetary policy which, in turn, could undermine their credibility and expose the Central Banks to the risk of exhibiting time-inconsistent behaviour. In further considering the significant impact that monetary policy decisions in these industrialized economies affect other Central Banks worldwide, any erroneous interest rates decisions made will inevitably spillover to other Central Banks globally.

In light of our research, policymakers should reconsider their approach to conducting monetary policy. Continuing to raise interest rates may reduce transitory inflation but could lead to persistent inflation patterns. Policymakers need to explore alternative methods of controlling inflation without necessarily abandoning the inflation targeting framework. This could include adopting a new framework for monetary–fiscal co-ordination which can simultaneously reduce inflation and the output gap in these industrialized economies.

A notable limitation of our study is that it does not shed light on the theoretical mechanisms underlying the NeoFisher effect or determine whether adherence to NeoFisherian dynamics can stabilize inflation even when it has already breached its target rate. Nonetheless, our study establishes a pivot empirical fact: a positive co-movement between interest rates and inflation exists in industrialized economies in the post-global financial crisis period, where interest rates cause inflation during both UMP and 'normalization' periods, hence implying that monetary policy is misconstrued.

Availability of data and materials

Data available upon reasonable request.

Abbreviations

- ADF:

-

Augmented Dickey–Fuller

- CPI:

-

Consumer price index

- CWT:

-

Cross wavelet transform

- EU:

-

European Union

- GFC:

-

Global financial crisis

- NK:

-

New Keynesian

- ONS:

-

Office for National Statistics

- SSR:

-

Shadow short rate

- UMP:

-

Unconventional monetary policy

- USA:

-

United States of America

- UK:

-

United Kingdom

- VAR:

-

Vector autoregressive

- WPS:

-

Wavelet power spectrum

- ZIRP:

-

Zero-interest rate policy

References

Aguiar-Conraria L, Soares J (2014) Continuous wavelet transforms: Moving beyond uni- and bivariate analysis. J Econ Surv 28(2):344–375

Baba C., Duval R., Lan T. and Topalova P. (2023), “The 2020–2022 inflation surge across Europe: A Phillips curve-based dissection”, IMF Working Paper No. 23/30, February.

Bai J, Perron P (2003) Computation and analysis of multiple structural change models. J Appl Economet 6(1):72–78

Ball L., Leigh D. and Mishra P. (2022), “Understanding U.S. inflation during the COVID era”, NBER Working Paper No. 30613, October.

Bias P, Hall J (2020) A test of Neo-Fisherism: 1964–2019. B.E. J Macroecon 21(1):221–251

Bilbiie F (2022) Neo-Fisherian policies and liquidity traps. Am Econ J Macroecon 14(4):378–403

Bullard J (2010) “Seven faces of ‘The Peril’”, Federal Reserve Bank of St. Louis Review 92(5):339–352

Cochrane J. (2016), “Do higher interest rates raise or lower inflation?”, Hoover Institute Working Paper, February.

Crowder W (2020) The Neo-Fisherian hypothesis: empirical implications and evidence. Empirical Econ 58(6):2867–2888

De Rezende R, Ristiniemi A (2023) A shadow rate without a lower bound constraint. J Bank Financ 146:e106686

Farne M, Montanari A (2022) A bootstrap method to test granger-causality in the frequency domain. Comput Econ 59:935–966

Friedman M (1968) The role of monetary policy. Am Econ Rev 58(1):1–17

Garcia-Schmidt M, Woodford M (2019) Are low interest rates deflationary? A paradox of perfect-foresight analysis. Am Econ Rev 109(1):86–120

Garin J, Lester R, Sims E (2018) Raise rates to raise inflation? Neo-Fisherianism in the New Keynesian model. J Money, Credit, Bank 50(1):243–259

Geweke J (1984) Measures of conditional linear dependence and feedback between time series. J Am Stat Assoc 79(388):907–915

Granger C (1969) Investigating causal relations by econometric models and cross-spectral methods. Econometrica 37(3):424–438

Kydland F, Prescott E (1977) Rules rather than discretion: The inconsistency of optimal plans. J Polit Econ 85(3):473–492

Lau K, Weng H (1995) Climate signal detection using wavelet transform: How to make a time series sing. Bull Am Meteor Soc 76(12):2391–2402

Marques A, Carvalho A (2022) Testing the Neo-Fisherian hypothesis in Brazil. Q Rev Econ Financ 86:407–419

Mishkin F (1995) Symposium on the monetary transmission mechanism. J Econ Perspect 9(4):3–10

Morlet J, Arens G, Fourgeau E, Giard D (1982) Wave propagation and sampling theory; Part I, complex signal and scattering in multi-layered media. Geophysics 47(2):203–221

Pasimeni P (2022) Supply or demand, that is the question: Decomposing Euro Area inflation. Intereconomics 57(6):384–393

Reis R. (2022), “The burst of inflation in 2021–22: How did we get here?”, CEPR Press Discussion Paper No. 17514, July.

Schmitt-Grohe S, Uribe M (2014) Liquidity traps: an interest rate based exist strategy. Manchester School 82(S1):1–14

Sims C (1980) Macroeconomics and reality. Econometrica 48(1):1–48

Torrence C, Compo G (1998) A practical guide to Wavelet analysis. Bull Am Meteor Soc 79(1):61–78

Uribe M. (2017), “The Neo-Fisher effect in the United States and Japan”, NBER Working Paper No. 23977, October.

Uribe M (2022) The Neo-Fisher effect: econometric evidence from empirical and optimizing models. Am Econ J Macroecon 14(3):133–162

Williamson S. (2016), “NeoFisherism: A radical idea, or the most obvious solution to the low-inflation problem?”, The Regional Economist, July Issue.

Williamson S (2018) Inflation control: Do Central Banks have it right? Federal Reserve Bank of St Louis 100(2):127–150

Acknowledgements

The authors have no acknowledgements to offer.

Funding

No funding was provided for the research.

Author information

Authors and Affiliations

Contributions

Andrew Phiri is the sole author.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors have no competing interests to declare.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Appendix I: VAR-based granger causality tests (traditional interest rates versus inflation)

Causal direction (NeoFisher) | F-statistics | p-value | Causal direction (Traditional) | F-statistics | p-value |

|---|---|---|---|---|---|

Panel A: full sample | |||||

iUS → πUS (12) | 3.42 | 0.00*** | πUS → iUS | 1.06 | 0.40 |

iEU → πEU (9) | 2.01 | 0.04* | πEU → iEU | 2.83 | 0.00*** |

iUK → πUK (7) | 1.73 | 0.10 | πUK → iUK | 3.05 | 0.00*** |

Panel B: 1st subsample (2007–2015) | |||||

iUS → πUS (12) | 5.07 | 0.00*** | πUS → iUS | 2.89 | 0.00*** |

iEU → πEU (9) | 1.71 | 0.11 | πEU → iEU | 3.69 | 0.00*** |

iUK → πUK (3) | 3.01 | 0.03* | πUK → iUK | 2.37 | 0.07* |

Panel C: 2nd subsample (2015–2020) | |||||

iUS → πUS (12) | 0.99 | 0.48 | πUS → iUS | 3.01 | 0.01** |

iEU → πEU (1) | 0.92 | 0.34 | πEU → iEU | 1.63 | 0.21 |

iUK → πUK (1) | 10.07 | 0.00*** | πUK → iUK | 3.45 | 0.06* |

Panel D: (2020–2023) | |||||

iUS → πUS (12) | 1.27 | 0.37 | πUS → iUS | 1.36 | 0.20 |

iEU → πEU (12) | 1.73 | 0.23 | πEU → iEU | 2.15 | 0.04* |

iUK → πUK (12) | 1.65 | 0.14 | πUK → iUK | 1.11 | 0.49 |

Appendix II: VAR-based granger causality tests (SSR versus inflation)

Causal direction | F-statistics | p-value | Causal direction | F-statistics | p-value |

|---|---|---|---|---|---|

Panel A: full sample | |||||

SSRUS → πUS (3) | 1.53 | 0.21 | πUS → SSRUS | 2.97 | 0.03* |

SSREU → πEU (8) | 1.92 | 0.06* | πEU → SSREU | 4.55 | 0.00*** |

SSRUK → πUK (12) | 3.49 | 0.00*** | πUK → SSRUK | 3.41 | 0.00*** |

Panel B: 1st subsample (2007–2015) | |||||

SSRUS → πUS (3) | 1.23 | 0.31 | πUS → SSRUS | 3.57 | 0.01** |

SSREU → πEU (7) | 1.31 | 0.26 | πEU → SSREU | 4.55 | 0.00*** |

SSRUK → πUK (3) | 2.32 | 0.08* | πUK → SSRUK | 4.41 | 0.00*** |

Panel C: 2nd subsample (2015–2020) | |||||

SSRUS → πUS (3) | 0.09 | 0.96 | πUS → SSRUS | 0.96 | 0.41 |

SSREU → πEU (2) | 2.55 | 0.08* | πEU → SSREU | 0.34 | 0.71 |

SSRUK → πUK (1) | 7.50 | 0.00*** | πUK → SSRUK | 12.38 | 0.00*** |

Panel D: (2020–2023) | |||||

SSRUS → πUS (12) | 1.12 | 0.17 | πUS → SSRUS | 1.21 | 0.17 |

SSREU → πEU (12) | 0.62 | 0.46 | πEU → SSREU | 0.32 | 0.68 |

SSRUK → πUK (12) | 1.83 | 0.41 | πUK → SSRUK | 1.33 | 0.51 |

Appendix III: Frequency-domain granger causality tests (traditional interest rates versus inflation)

Appendix IV: Frequency-domain granger causality tests (SSR versus inflation)

Appendix V

Appendix VI

The arrows inside the wavelet coherence spectrum plots indicate the phase-dynamics between the series and offer information on lead-lag dynamics (i.e., whether ‘inflation’ leads ‘interest rates’ or vice versa) and the 'sign of the relationship' (positive or negative). If the variables have positive (negative) correlations, the arrows' notations are ↑, ↗, → and ↘ (↓, ↙, ← , and ↖), indicating that the series are in-phase (anti-phase). Furthermore, the arrows orientations specifies whether ‘inflation’ leads (lags) ‘interest rates’, with the arrows ↑, ↗, and → (↘) indicating that the series are in-phase, with ‘inflation’ leading (lagging) ‘nominal interest rates’, whilst the arrows ↓, ↙, and ← (↖) indicate that the series are anti-phase, with ‘inflation x’ leading (lagging) ‘nominal interest rates’.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Phiri, A. A multiresolution analysis of NeoFisher effects in industrialized economies: Have monetary policy dynamics being misconstrued in the west?. Futur Bus J 10, 51 (2024). https://doi.org/10.1186/s43093-024-00335-3

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s43093-024-00335-3