Abstract

Background

In many low-income countries, households bear most of the health care costs. Community-based health insurance (CBHI) schemes have multiplied since the 1990s in West Africa. They have significantly improved their members’ access to health care. However, a large proportion of users are reluctant to subscribe to a local CBHI. Identifying the major factors affecting membership will be useful for improving CBHI coverage. The objective of this research is to obtain a general overview of existing evidence on the determinants of CBHI membership in West Africa.

Methods

A review of studies reporting on the factors determining membership in CBHI schemes in West Africa was conducted using guidelines developed by the Joanna Briggs Institute. Several databases were searched (PubMed, ScienceDirect, Global Health database, Embase, EconLit, Cairn.info, BDPS, Cochrane database and Google Scholar) for relevant articles available by August 15, 2022, with no methodological or linguistic restrictions in electronic databases and grey literature.

Results

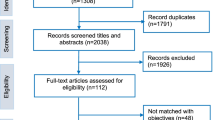

The initial literature search resulted in 1611 studies, and 10 studies were identified by other sources. After eliminating duplicates, we reviewed the titles of the remaining 1275 studies and excluded 1080 irrelevant studies based on title and 124 studies based on abstracts. Of the 71 full texts assessed for eligibility, 32 additional papers were excluded (not relevant, outside West Africa, poorly described results) and finally 39 studies were included in the synthesis. Factors that negatively affect CBHI membership include advanced age, low education, low household income, poor quality of care, lack of trust in providers and remoteness, rules considered too strict or inappropriate, low trust in administrators and inadequate information campaign.

Conclusions

This study shows many lessons to be learned from a variety of countries and initiatives that could make CBHI an effective tool for increasing access to quality health care in order to achieve universal health coverage. Coverage through CBHI schemes could be improved through communication, improved education and targeted financial support.

Similar content being viewed by others

Introduction

Over the last few decades, most low- and middle-income countries (LMICs) have been confronted with sustainability issues related to their health care systems. In these countries, out-of-pocket payments account for a large proportion of the health care expenditures. This contrasts with European countries which have moved towards mandatory social health insurance systems, thereby reducing the proportion of out-of-pocket payments [1, 2].

Each year, approximately 44 million households around the world -more than 150 million people- face very important health care expenditures and over 100 million people fall into poverty due to health care costs [3].

To overcome these difficulties, community-based health insurance (CBHI) systems have emerged in Sub-Saharan Africa. A CBHI is a non-profit organisation governed by its members, based on the principles of solidarity and mutual aid between individuals who participate freely and voluntarily. It aims to improve access to health care for the population by sharing the financial risks of illness among its members [4, 5]. Despite the efforts made to develop CBHI schemes, the low levels of membership, both initial enrolment and renewal of membership, continue to threaten their financial viability while encountering a multitude of obstacles to their development [5, 6].

Among the various challenges facing CBHI schemes, enrolment currently appears to be the predominant issue [5,6,7]. Although the mutualist movement is growing steadily in West Africa, the coverage of the target population rarely exceeds 30% [7,8,9,10]. One thing is clear everywhere: the membership rates of CBHI schemes remain relatively low, sometimes even calling into question the very viability of the organisation [5, 11].

To try to understand this low participation rate of the population, one can question the economic theory of health insurance by trying to define its essential parameters for the specific context of West African countries. However, our main objective here is at another level and is based on the following observation: over the past decade, several empirical studies have been conducted, albeit with widely varied methodologies, on factors that may explain the decision to participate or not in a CBHI in West Africa. In this context, we would like to see if, beyond this great methodological heterogeneity, it is nevertheless possible to identify some convergent results that could enlighten public and private actors in this field.

Although there are already a few reviews on the determinants of CBHI membership in LMICs [8, 9, 11, 12], this review has several advantages. Firstly, it aims to update existing data by considering a broad time period up to 2022. Second, it focuses on the West African region. This group of countries, different from other LMICs, shares particular socioeconomic and political characteristics that influence their health care financing and systems. These countries suffer from economic inefficiencies and weak public governance, and their populations are largely rural with low financial capacity. Their health sectors are often underfunded and the quality of public health services offered is limited [1,2,3,4].

Methods

Research strategy and data source

We conducted a review of studies reporting on the factors explaining the persistence of the low rate of CBHI membership in West Africa using the guidelines for conducting scoping reviews developed by the Joanna Briggs Institute [13].

We developed a research strategy for relevant studies published between January 1, 2000 and August 15, 2022, without methodological and language restrictions, in the electronic databases PubMed, ScienceDirect, Global Health database, Embase, EconLit, Cairn.info, BDPS, Cochrane database and Google Scholar, using combinations of the following keywords: [“determinant” OR “factor” OR “driver”] AND [“community insurance” OR “community mutual” OR “mutual health”] AND [“membership” OR “enrolment” OR “subscription” OR “participation” OR “adherence” OR “retention” OR “take-up” OR “uptake” OR “demand” OR “drop-out”] AND [“West Africa”].

To make the research comprehensive and to identify additional articles, we sought additional sources and conducted searches in each of the West African countries: Benin, Burkina Faso, Cape Verde, Côte d’Ivoire, Gambia, Guinea, Guinea-Bissau, Liberia, Mali, Mauritania, Niger, Nigeria, Senegal, Sierra Leone and Togo. Ghana was excluded as this country has a national health insurance which is different from the CBHI scheme [6]. We completed the demographic, health and economic data based on the websites of the World Health Organisation (WHO), the official NHIS of the countries of interest and the World Bank. Then we applied the snowball method which allowed us to add relevant articles by reviewing the references of all the studies selected in the previous step.

Inclusion and exclusion criteria

The review included studies published between January 1, 2000 and August 15, 2022 and articles that reported on the determinants of membership in CBHI in West Africa.

Articles for which full text was not available and those that were clearly not relevant to the topic were excluded.

Selection of studies

We identified eligible articles using the PRISMA flow chart. The first and second authors independently reviewed all titles and abstracts identified by the research. Full texts of all potentially eligible articles were retrieved and reviewed for inclusion in this review according to the inclusion criteria.

Zotero reference manager software was used to organise and detect duplicate references (www.zotero.org). After removing duplicates, titles and abstracts of all articles were independently reviewed for eligibility, relevance and compliance with inclusion and exclusion criteria by two of the authors (KKC and AMC).

Data and item extraction

For the included studies, we independently extracted information on study characteristics (authors, title, year of publication, country, research method, sample size and determinants of membership and non-membership). This information was summarized in a spreadsheet, and an evidence table was generated to describe and summarize the characteristics of the included studies (Table 1).

After screening and obtaining full texts of the selected articles, we examined each publication for information on the characteristics of the determinants of membership and non-membership in CBHI, with a particular focus on recurring observations in the different countries. The observations were used to formulate recommendations for policy decisions likely to improve membership rates of CBHI schemes in West Africa. Any discrepancies in the selection and extraction process were resolved by discussion, if necessary, with two other authors (SZ and VDB).

Results

The initial literature search yielded 1611 studies and ten additional studies were identified by other sources. After eliminating duplicates, we reviewed the titles of the remaining 1275 studies and excluded 1080 irrelevant studies by title and 124 studies based on abstracts. Of the 71 full texts assessed for eligibility, 32 additional papers were excluded (not relevant, outside West Africa, poorly described results) and finally 39 studies were included in the synthesis (Fig. 1).

PRISMA flow chart of the study selection process for examining the determinants of membership in community-based health insurance (CBHI) in West Africa (2000–2022)

Key determinants of CBHI membership

Most articles were based on cross-sectional household surveys, case studies and interviews. Of the 39 studies included in the review, 17 were quantitative, 15 were qualitative, six were mixed-method studies (quantitative and qualitative approaches) and one study was exclusively a literature review. The sample sizes of the studies ranged from 23 to 29 326 households for the quantitative and mixed-method studies. The 39 studies that met our inclusion criteria were published between 2003 and 2022, mostly within the last ten years. The studies were conducted in only seven West African countries: 13 in Senegal, nine in Burkina Faso, six in Nigeria, five in Benin, two in Guinea, one in Mali, one in Mauritania and two multi-country studies (Table 1). The majority of the studies were community-based, mostly rural, except for the literature review studies. Other studies were conducted in healthcare facilities, health centres or hospitals.

The main factors of membership in CBHI schemes were identified and presented as follows: individual characteristics (age, level of education, ethnicity and religion); household socioeconomic characteristics (household financial capacity, household size, associative history, target group cohesion and therapeutic use); determinants related to healthcare services (quality of healthcare, trust in the skills of healthcare providers and geographical distance) and parameters specific to CBHI (membership procedures, services offered to members, trust in the CBHI schemes, information and understanding).

Individual characteristics

Nine studies show that membership appears to be related to certain individual characteristics, including the level of education that influences participation in the CBHI schemes. Literate people are more likely to participate in a CBHI scheme than illiterate people [14,15,16,17,18,19,20,21,22]. Some of our studies reported that people aged 65 and over are more economically and socially excluded from the community and therefore have more difficulty being part of CBHI [14, 22,23,24]. Seven empirical studies found greater affiliation of certain ethnic groups to CBHI schemes [18,19,20, 23, 25,26,27]. In a study in Senegal, the Peulh/Fulani ethnic group was less likely to participate in the program probably because of their nomadic lifestyle [25]. Religion, although not widely considered as a membership factor in the selected studies, could also influence household membership in a community-based health financing system. In the early 2000s, Muslims were found to be much less likely than Christians to participate because they mistakenly believed that the projects were open only to Christians [17, 18, 27].

Socioeconomic characteristics of households

Financial capacity of households

The household income level appears to be an essential parameter for membership and most studies indicate that a low capacity to contribute is a major obstacle to participate in a community health insurance system. Lack of financial resources is often the first reason given by both members and non-members to explain low participation in CBHI [14, 16,17,18, 22, 23, 25, 26, 28,29,30,31,32,33,34,35,36,37,38,39]. Several studies have shown that the socioeconomic level of members is higher than that of non-members [17, 18, 21, 25, 30, 31]. Although respondents most often consider the amount of the individual contribution to be fair or affordable (especially compared to the costs of not participating), many cannot afford to pay the contributions for all the members of the household. Households’ standard of living is summarized by three separate indicators: income, annual expenditures and perception of their financial capacity relative to others. This enables us to establish that the poorest households are much less represented in CBHI than the better-off households. Most members consider that CBHI schemes offer better financial protection [14, 16,17,18, 22, 23, 25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40].

Household size

Regarding household size, some empirical work presents results that state the greater difficulty of large households to participate in a health risk pooling system. Although these families are not considered among the poorest in the community, they are generally unable to bear the contributions for all the members of the household [14, 22, 23, 26, 28, 39, 41, 42].

Association history, target group cohesion, therapeutic use and health perceptions

The existence of informal risk-sharing associations appears to facilitate the establishment of a community health insurance scheme; the involvement of community leaders positively influences membership. One study shows that 41% of CBHI members say they signed up on the advice of an influential person and research in Burkina Faso indicates that members of a community health insurance system have a more negative perception of traditional healthcare than non-members, often judging it to be poor or ineffective [19, 20, 30, 32, 42].

Determinants of caregiving

The role played by healthcare providers in the dynamics of CBHI memberships can be considered from three angles: the quality of the healthcare, the population’s trust in the skills of healthcare providers and the geographical proximity of the healthcare centres under agreement.

Quality of healthcare

Among the included studies, many showed that factors related to healthcare quality and provider relationships were important factors in CBHI membership. On the one hand, poor quality of the care provided, including patient reception, prescription and availability of drugs, effectiveness and duration of the treatment, negatively influenced membership in a CBHI scheme. On the other hand, doubts about the organisation’s ability to improve healthcare quality also discouraged membership [14,15,16, 18, 22, 28, 33, 35, 39, 43].

The quality of the healthcare provided is an encouraging factor, even a membership condition and may also be a consequence of membership through members’ pressure to improve quality [14, 18, 26, 28, 30, 35].

Confidence in the skills of providers

In addition to user dissatisfaction with the attitude of healthcare providers towards patients, empirical research attests of distrust in the skills of healthcare workers. This scepticism about health workers’ competence reinforces the lack of trust in health workers, which negatively influences membership. Thus, trust in health workers is based above all on their professional experience and ability to listen to and inform the patient [15, 22, 23, 25, 29, 33, 35, 36].

Geographical distance

The results of surveys on the distance to health centres highlight geographic distance as a significant barrier to membership and even as a reason for disaffiliation [14, 16, 18, 19, 25, 26, 30, 34, 35, 44].

Determinants specific to CBHI schemes

Regarding membership, the community health insurance company as such could be examined according to three aspects: first, the membership modalities and the services it offers to its members, second, the trust that the communities place in it and third, the way in which it sets up and invests in the information and sensitization of the target populations.

Terms of membership and benefits offered to members

Memberships, dues and premiums, as mentioned above, are considered acceptable by the communities, despite the lack of financial resources of many of them. The frequency of payment of the membership fee seems to influence membership: it appears that the obligation to pay the membership premium and/or the annual fees at once is a major obstacle, particularly for large families [15, 29, 35, 45, 46]. The lack of coverage of certain benefits is also an obstacle to membership for some individuals. Finally, the rigidity of certain internal rules established by the CBHI scheme also hinders membership. For example, one study indicates that there is a problem of affordability for many poor and/or large families who cannot gather enough money to pay for membership of all of the household members in one go. Although it is a measure against adverse selection, this rule is perceived by communities as too rigid and inappropriate [15, 29, 35, 45,46,47].

Trust in the CBHI scheme

Confidence in the CBHI scheme also influences the decision to participate or not. Studies highlighted two dimensions of the target population’s confidence in CBHI: on the one hand, confidence in the management of the system which depends on the skills and integrity of the CBHI managers, and on the other hand, confidence in the ability of the CBHI scheme to achieve its stated objectives. The target populations frequently adopt a cautious attitude at the launch of a CBHI scheme, preferring to observe before participating [15,16,17, 23, 28, 34, 35, 43, 45,46,47,48]. Other studies indicate that doubts about the honesty of the CBHI leaders or previous experiences with embezzlement may have a negative impact on membership [19, 35, 42, 43, 45,46,47,48].

Misunderstanding and lack of information

Inadequacy of communication is a factor influencing membership in CBHI schemes. Information to be communicated concerns the very existence of the CBHI system, knowledge of how the CBHI scheme functions and knowledge of the benefits offered by the CBHI scheme. The transmission of information is said to be deficient because the awareness campaign is not very attractive or not adapted to illiterate populations. This indicates that non-members have a limited understanding of community health principles [15, 17, 18, 23, 33, 35,36,37,38,39, 43,44,45, 49,50,51,52].

Discussion

This review aims to identify the factors influencing membership in CBHI schemes in West Africa. The synthesis of the studies made it possible to identify the factors that influence the decision to participate or not in a CBHI. These factors are mainly related to individual characteristics (age, level of education, ethnicity and religion), household size, household financial capacity, associative history, quality of health care, confidence in the skills of healthcare providers, geographical distance, membership modalities, benefits offered to members, confidence in the CBHI, information and understanding. As CBHI initial enrolment, membership renewal and drop-out determinant factors are relatively the same, we have chosen to analyse these membership factors together.

This study suggests that the people potentially interested by CBHI schemes are those who are middle-aged. A similar finding was reported by Fadlallah et al. in a systematic review [53]: in low-income countries, nine out of 51 quantitative studies suggested a positive correlation with older age (i.e., 36 years and older, on average). Regarding larger families, five out of 51 studies confirmed that larger households were less likely to participate in a CBHI. The non-membership of the elderly is likely to be part of a broader lack of social protection for this group, with, for example, less than 7% of people aged 60 and over receiving social protection in Benin [23].

Low education was found to be a barrier in ten of the included studies. These results are consistent with those reported by previously-published reviews in Sub-Saharan Africa, which showed that the higher the level of education, the greater the likelihood of participating in a CBHI, whether measured in terms of years of schooling or literacy skills [8, 9, 11].

Factors related to healthcare and relationships with healthcare providers are also important determinants of membership in a CBHI. On the one hand, poor quality of care negatively influences membership. On the other hand, people’s scepticism related to the skills of health personnel reinforces their lack of confidence in them. In addition, doubts about the organisation’s ability to improve the quality of care also contributes to non-membership. The reasons for the lack of trust in the CBHI may also be due to previous negative experiences or to suspicion of dishonesty towards the CBHI managers. These observations call for special attention to be paid to contracting modes between CBHI schemes and healthcare services. For start-up CBHI organisations, or more generally those of limited size, there is a high probability that they will not be able to influence the practices of healthcare facilities and workers. Several experiences suggest, however, that this type of situation is not inevitable. For example, when a hospital is actively involved in, or even initiates, community insurance systems, access to care, quality of care and patient confidence are significantly improved as shown in the work of Fadlallah et al. and Jütting and Tine on mutualist systems in the Thiès region of Senegal [53, 54].

Distance between the place of residence and the healthcare facility constitute a known barrier to participating in a CBHI scheme [8, 9, 11, 12]. There is an exception in Burkina Faso. De Allegri et al. showed that the distance separating mutualists from the healthcare facility was not a barrier to participate to the CBHI [35]. Membership rates were higher in the communities furthest from the health centre. This surprising result was explained by the intense promotion campaigns carried out among the most distant populations and by the fact that the CBHI scheme covers the cost of transport.

The results of our review show that the lack of information and understanding by the population can be an obstacle for CBHI membership and similar results were previously reported in different reviews [8, 9, 12, 53]. It is very often through radio and newspapers that messages are delivered. The information does not reach the relevant targets because the majority of the population, especially the most disadvantaged, do not have access to these media. This explains why some articles reported that door-to-door activities with elected members of CBHI schemes were the most effective initiative for increasing membership [55]. Communication strategies are often lacking and deserve more investment to make population aware of CBHI.

There is broad consensus among the included studies that lack of financial resources remains the main reason stated by households for not participating in a CBHI. This is similar to the mixed results on economic status found by Fadlallah et al. and Ahmad et al. in India [53, 56]. Consequently, the poorest households cannot afford paying a membership and are therefore excluded [57].

CBHI schemes that are more flexible with the collection and timing of contributions and with the membership rules would be more likely to attract new members. Jütting and Tine broke down this process into several stages during which the perception of the current and expected costs and benefits of insurance vary according to factors linked to both the situation of the individuals and the general environment [54].

In most West African countries, there are tens, sometimes hundreds different small local initiatives which positively reflect a local dynamic but at the same time may be the reason of the failure. Indeed, CBHI schemes are based on solidarity among the members (risk pooling) and logically the number of members matters. Some countries, however, managed to succeed. Examples of Ghana, Rwanda (the only country in sub-Saharan Africa to achieve a coverage above 90% [58, 59]) or India are interesting case studies. The key to Rwanda’s success in implementing the health insurance program appears to be a strong societal consensus on equal access to healthcare with financial protection, crucially supported by the government through investments in the health sector, effective legislation to provide basic care to the uninsured and an intensive national program [58, 59].

In India, most CBHI programs are run by nongovernmental organisations with considerable organisational diversity [60, 61]. Strategic procurement and effective monitoring were provided, and financial sustainability was increased by merging smaller systems. In particular, the Indian government has created a more favourable policy environment by giving legal recognition to CBHI programs and providing grants to the poor [61, 62]. These programs have been rapidly successful and reflected a trend in Asian countries to move away from informal coverage and to integrate health insurance programs into regulated government frameworks. Although the health insurance landscape in Asia differs somewhat from that in West Africa, some common patterns and lessons can be drawn.

Senegal is a strange case because it implemented the known ingredients of success but did not reach the expected coverage. The government launched in 2013 a universal health coverage initiative based on local CBHI organisations that reached 676 in 2016. The national agency standardized the benefit package and insurance premium, the government subsidized 50% of the premium for all enrolees and 100% for the poor and disabled people, and the rest of the funds from the premiums are pooled to cover health care and drugs provided or prescribed by referral hospitals [63]. According to Bousmah et al., the problem was linked to the low demand for health insurance due to limited access to information about available schemes [44].

So far, CBHI, without a strong support from governments and international aid, seems ineffective to reach universal health coverage. However, CBHI may have a role in increasing uptake of quality care and promoting accountability of healthcare providers.

The originality of our study is to review factors of CBHI membership and non- membership in West Africa and it was conducted with respect to research standards of scoping review. However, despite our best effort to review all available recent evidence available, this study has limitations. First, we found data in only seven of the 15 West African countries, while several other West African countries have previously launched similar insurance programs. Second, the quality of the included studies was not considered. Lastly, as it was not a systematic review and meta-analysis, the statistical magnitude of the different determinants of CBHI membership and non-membership were not compared.

Conclusions

This study shows many lessons that can be learned from a variety of countries and initiatives that could make CBHI an effective tool for expanding access to healthcare. Coverage through CBHI schemes could be improved through policies that include closer integration of the informal and formal sectors within the existing national health insurance systems, with increasing beneficiary participation in program design and management, improved communication and education, increased public and private financing of healthcare and targeted financial assistance. By making membership mandatory, more people could benefit from social protection. These results are likely to be instructive for government policymakers in achieving universal health coverage goals and improving health outcomes.

Availability of data and materials

Not applicable.

References

Jakovljevic M, Çalışkan Z, Fernandes PO, Mouselli S, Otim ME. Editorial: health financing and spending in low- and middle-income countries. Front Public Health. 2021;9:800333.

Dieleman JL, Templin T, Sadat N, et al. National spending on health by source for 184 countries between 2013 and 2040. Lancet. 2016;387(10037):2521–35. doi:https://doi.org/10.1016/S0140-6736(16)30167-2.

Xu K, Evans D, Carrin G, Aguilar-Rivera AM. Health financing system: how to reduce catastrophic spending. In: Technical summary for policy makers. [Internet]. WHO Department of Health Systems Financing (HSF). 2005 [cited June 22, 2021]. Available from: https://www.who.int/health_financing/pb_number_2_fr.pdf.

Abel-Smith B. Health insurance in developing countries: lessons from experience. Health Policy Plan. 1992;7(3):215–26.

Waelkens M-P, Soors W, Criel B. Community health insurance in low- and middle-income countries. Elsevier. 2017;2:82–92.

Ly MS, Bassoum O, Faye A. Universal health insurance in Africa: a narrative review of the literature on institutional models. BMJ Glob Health. 2022;7(4):e008219.

Osei Afriyie D, Krasniq B, Hooley B, Tediosi F, Fink G. Equity in health insurance schemes enrollment in low and middle-income countries: a systematic review and meta-analysis. Int J Equity Health. 2022;21(1):21.

Shewamene Z, Tiruneh G, Abraha A, Reshad A, Terefe MM, Shimels T, Lemlemu E, Tilahun D, Wondimtekahu A, Argaw M, Anno A, Abebe F, Kiros M. Barriers to uptake of community-based health insurance in sub-Saharan Africa: a systematic review. Health Policy Plan. 2021;36(10):1705–14.

Adebayo EF, Uthman OA, Wiysonge CS, Stern EA, Lamont KT, Ataguba JE. A systematic review of factors that affect uptake of community-based health insurance in low-income and middle-income countries. BMC Health Serv Res. 2015;15:543.

International Labour Organization. World social protection report 2020–22: social protection at the crossroads–in pursuit of a better future [Internet]. 2021 [cited August 15, 2022].

Defourny J, Failon J. The determinants of membership in mutual health insurance in sub-Saharan Africa: an inventory of empirical work. Mondes En Dev. 2011;153(1):7–26.

Platteau JP, De Bock O, Gelade W. The demand for microinsurance: a literature review. World Dev. 2017;94:139–56.

Peters MDJ, Godfrey CM, Khalil H, McInerney P, Parker D, Soares CB. Guidance for conducting systematic scoping reviews. Int J Evid Based Healthc. 2015;13(3):141–6.

Seck I, Dia AT, Sagna O, Leye MM. Déterminants de l’adhésion et de la fidélisation aux mutuelles de santé dans la région de Ziguinchor (Sénégal) [Determinants of enrolment and retention in mutual health organization in the region of Ziguinchor (Senegal)]. Sante Publique. 2017;29(1):105–14.

Turcotte-Tremblay A-M, Haddad S, Yacoubou I, Fournier P. Mapping of initiatives to increase membership in mutual health organizations in Benin. Int J Equity Health. 2012;11:74.

Onwujekwe O, Onoka C, Uguru N, Tasie N, Uzochukwu B, Kirigia J, et al. Socio-economic and geographic differences in acceptability of community-based health insurance. Public Health. 2011;125(11):806–8.

Odeyemi IAO. Community-based health insurance programmes and the National Health Insurance Scheme of Nigeria: challenges to uptake and integration. Int J Equity Health. 2014;13:20.

Smith KV, Sulzbach S. Community-based health insurance and access to maternal health services: evidence from three West African countries. Soc Sci Med. 2008;66(12):2460–73.

De Allegri M, Kouyaté B, Becher H, Gbangou A, Pokhrel S, Sanon M, et al. Understanding enrollment in community health insurance in sub-Saharan Africa: a population-based case-control study in rural Burkina Faso. Bull World Health Organ. 2006;84(11):852–8.

Gnawali DP, Pokhrel S, Sié A, Sanon M, De Allegri M, Souares A, et al. The effect of community-based health insurance on the utilization of modern health care services: evidence from Burkina Faso. Health Policy. 2009;90(2–3):214–22.

Chankova S, Sulzbach S, Diop F. Impact of mutual health organizations: evidence from West Africa. Health Policy Plan. 2008;23(4):264–76.

Dong H, De Allegri M, Gnawali D, Souares A, Sauerborn R. Drop-out analysis of community-based health insurance membership at Nouna, Burkina Faso. Health Policy. 2009;92(2–3):174–9.

Gankpe GF, Gankpe EC, Baleba AN, Zinsou L, Mesenge C. Do mutual health insurance schemes reproduce health inequalities in Benin? Public Health 9 Sep. 2018;30(3):389–96.

Lyalomhe FO, Adekola PO, Cirella GT. Community-based health financing: empirical evaluation of the socio-demographic factors determining its uptake in Awka, Anambra state, Nigeria. Int J Equity Health. 2021;20(1):235.

Jütting JP. Do Community-based health insurance schemes improve poor people’s access to health care? Evidence from rural senegal. World Dev. 2004;32(2):273–88.

Franco LM, Diop FP, Burgert CR, Kelley AG, Makinen M, Simpara CHT. Effects of mutual health organizations on use of priority health-care services in urban and rural mali: a case-control study. Bull World Health Organ. 2008;86(11):830–8.

Jütting J. Health insurance for the poor ? Determinants of participation in community-based health insurance schemes in rural Senegal. In: OECD Development Centre. 2003. Paris: OECD Publishing. Working Papers 204.

Criel B, Waelkens MP. Declining subscriptions to the Maliando Mutual Health Organisation in Guinea-Conakry (West Africa): what is going wrong? Soc Sci Med. 2003;57(7):1205–19.

Sagna O, Seck I, Dia AT, Sall FL, Diouf S, Mendy J, et al. Study of the Consumers’ preference on the universal health coverage development strategy through health mutual in Ziguinchor Region, Southwest of Senegal. Bull Soc Pathol Exot. 2016;109(3):195–206.

Onwujekwe O, Okereke E, Onoka C, Uzochukwu B, Kirigia J, Petu A. Willingness to pay for community-based health insurance in Nigeria: do economic status and place of residence matter? Health Policy. 2010;25(2):155–61.

Souares A, Savadogo G, Dong H, Parmar D, Sié A, Sauerborn R. Using community wealth ranking to identify the poor for subsidies: a case study of community-based health insurance in Nouna, Burkina Faso. Health Soc Care Commun. 2010;18(4):363–8.

Mladovsky P, Soors W, Ndiaye P, Ndiaye A, Criel B. Can social capital help explain enrollment (or lack thereof) in community-based health insurance? Results of an exploratory mixed methods study from Senegal. Soc Sci Med. 2014;101:18–27.

Ndiaye P, Kaba S, Kourouma M, Barry AN, Barry A, Criel B. MURIGA en Guinée: une expérience de mutualisation des risques liés à la grossesse et à l’accouchement. In Richard F, WitterS, De Brouwere V, editors. Réduire les barrières financières aux soins obstétricaux dans les pays à faibles ressources. Studies in Health Services Organisation & Policy; 25 Antwerp: ITGPress; 2008. pp. 129–63

Onwujekwe O, Onoka C, Uzochukwu B, Okoli C, Obikeze E, Eze S. Is community-based health insurance an equitable strategy for paying for healthcare? Experiences from southeast Nigeria. Health Policy. 2009;92(1):96–102.

De Allegri M, Sanon M, Sauerborn R. “To enrol or not to enrol? A qualitative investigation of demand for health insurance in rural West Africa. Soc Sci Med. 2006;62(6):1520–7.

Ridde V, Haddad S, Yacoubou M, Yacoubou I. Exploratory study of the impacts of mutual health organizations on social dynamics in Benin. Soc Sci Med. 2010;71(3):467–74.

Ridde V, Haddad S, Ducandas X, Yacoubou I, Yacoubou M, Gbetie M. Thanks to mutual health insurance in Benin, users have the power to say “no”. 2011;4.

Alenda-Demoutiez J, Boidin B. Community-based mutual health organisations in Senegal: a specific form of social and solidarity economy? Rev Soc Econ. 2019;77(4):417–41.

Bastin M. Mutual health insurance in northern Benin: How can the establishment of a collective membership mechanism for socio-cultural groups boost the penetration rate of mutual health insurance? " [Internet]. Catholic University of Leuven; 2018. Available from: http://hdl.handle.net/2078.1/ thesis:16928.

Bonan J, LeMay-Boucher P, Tenikue M. Households’ Willingness to pay for health microinsurance and its impact on actual take-up: results from a field experiment in Senegal. J Dev Stud. 2014;50(10):1445–62.

Koloma Y. Impact of Mutual Health Insurance on Urban Households Health Expenses and Vulnerability in Burkina Faso [Internet]. In: Kiel, Hamburg: ZBW - Leibniz Information Centre for Economics; 2021 [cited 27 Jul 2021]. Available from: https://www.econstor.eu/handle/10419/234465.

Sow PG, Bop MC, Akoetey K, Diop CT, Kâ O. Facteurs d’adhésion et utilisation des Mutuelles de Santé (MS): région Ziguinchor au Sénégal [Membership factors and use of mutual health insurance in the Ziguinchor region of Senegal]. Sante Publique. 2021;32(5):563–70.

Mladovsky P. Why do people drop out of community-based health insurance? Findings from an exploratory household survey in Senegal. Soc Sci Med. 2014;107:78–88.

Bousmah MA, Boyer S, Lalou R, Ventelou B. Reassessing the demand for community-based health insurance in rural Senegal: geographic distance and awareness. SSM Popul Health. 2021;16:100974.

Waelkens MP, Coppieters Y, Laokri S, Criel B. An in-depth investigation of the causes of persistent low membership of community-based health insurance: a case study of the mutual health organisation of Dar Naïm, Mauritania. BMC Health Serv Res. 2017;17(1):535.

De Allegri M, Sanon M, Bridges J, Sauerborn R. Understanding consumers’ preferences and decision to enrol in community-based health insurance in rural West Africa. Health Policy. 2006;76:58–71.

Mladovsky P, Ndiaye P, Ndiaye A, Criel B. The impact of stakeholder values and power relations on community-based health insurance coverage: qualitative evidence from three Senegalese case studies. Health Policy Plan. 2015;30(6):768–81.

Rouyard T, Mano Y, Daff BM, Diouf S, Fall Dia K, Duval L, Thuilliez J, Nakamura R. Operational and structural factors influencing enrolment in community-based health insurance schemes: an observational study using 12 waves of nationwide panel data from Senegal. Health Policy Plan. 2022;37(7):858–71.

Bocoum F, Grimm M, Hartwig R, Zongo N. Can information increase the understanding and uptake of insurance? Lessons from a randomized experiment in rural Burkina Faso. Soc Sci Med. 2019;220:102–11.

Bonan J, Dagnelie O, LeMay-Boucher P, Tenikue M. The impact of insurance literacy and marketing treatments on the demand for health microinsurance in Senegal: a randomised evaluation. J Afr Econ. 2017;26(2):169–91.

Cofie P, De Allegri M, Kouyate B, Sauerborn R. Effects of information, education, and communication campaign on a community-based health insurance scheme in Burkina Faso. Glob Health Action. 2013;6:20791.

Yusuf HO, Kanma-Okafor OJ, Ladi-Akinyemi TW, Eze UT, Egwuonwu CC, Osibogun AO. Health insurance knowledge, attitude and the uptake of community-based health insurance scheme among residents of a suburb in Lagos, Nigeria. West Afr J Med. 2019;36(2):103–11.

Fadlallah R, El-Jardali F, Hemadi N, Morsi RZ, Abou Samra CA, Ahmad A, et al. Barriers and facilitators to implementation, uptake and sustainability of community-based health insurance schemes in low- and middle-income countries: a systematic review. Int J Equity Health. 2018;17(1):13.

Jütting J, Tine J. Micro health insurance systems and health status in developing countries: an empirical analysis of the impact of mutual health insurance in rural Senegal [Internet]. 2000 [cited 30 May 2021].

WHO. Universal health coverage [Internet]. 2021 [cited June 30, 2021]. Available from: https://www.who.int/fr/news-room/fact-sheets/detail/universal-health-coverage-(uhc).

Ahmad D, Mohanty I, Irani L, Mavalankar D, Niyonsenga T. Participation in microfinance based Self Help Groups in India: Who becomes a member and for how long? PLoS ONE. 2020;15(8):e0237519.

Umeh CA, Feeley FG. Inequitable Access to health care by the poor in community-based health insurance programs: a review of studies from low- and middle-income countries. Glob Health Sci Pract. 2017;5(2):299–314.

Lu C, Chin B, Lewandowski JL, Basinga P, Hirschhorn LR, Hill K, et al. Towards universal health coverage: an evaluation of Rwanda Mutuelles in its first eight years. PLoS ONE. 2012;7(6):e39282.

Logie DE, Rowson M, Ndagije F. Innovations in Rwanda’s health system: looking to the future. Lancet. 2008;372(9634):256–61.

Soors W, Devadasan N, Durairaj V, Criel B. Community health insurance and universal coverage: multiple paths, many rivers to cross. 2010. World Health Report 2010. Background Paper 48. [cited 23 Jul 2021]; Available from: https://www.researchgate.net/publication/234072109_Community_Health_Insurance_And_Universal_Coverage_Multiple_Paths_Many_Rivers_To_Cross.

Bhageerathy R, Nair S, Bhaskaran U. A systematic review of community-based health insurance programs in South Asia. Int J Health Plann Manage. 2017 Apr;32(2):e218–31.

Devadasan N, Ranson K, Van Damme W, Acharya A, Criel B. The landscape of community health insurance in India: an overview based on 10 case studies. Health Policy. 2006;78(2–3):224–34.

Daff BM, Diouf S, Diop ESM, Mano Y, Nakamura R, Sy MM, Tobe M, Togawa S, Ngom M. Reforms for financial protection schemes towards universal health coverage, Senegal. Bull World Health Organ. 2020;98(2):100–8.

Funding

The authors received no funding for this work.

Author information

Authors and Affiliations

Contributions

KKC and AMC performed the study selection and data extraction and wrote the manuscript. SZ and VDB controlled the study selection and data extraction and revised the manuscript. MJ and MK commented on the manuscript. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not applicable.

Consent for publication

All authors approved the final manuscript.

Competing interests

The authors declare that they have no competing interests.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Conde, K.K., Camara, A.M., Jallal, M. et al. Factors determining membership in community-based health insurance in West Africa: a scoping review. glob health res policy 7, 46 (2022). https://doi.org/10.1186/s41256-022-00278-8

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s41256-022-00278-8