Abstract

The main approach to promoting high-quality development lies in fostering self-reliance and self-improvement in science and technology, as well as enhancing the technological innovation capabilities of enterprises. In the new stage of moving from imitation to innovation, tax reduction plays an important role in promoting enterprise technological innovation. This article uses the data of A-share listed companies from 2008 to 2019 to explore the mechanism of how tax reduction exerts its core role in innovation. The findings indicate that tax cuts have a stimulating effect on firms’ research and development (R&D) innovation. These results hold true even after accounting for tax evasion and R&D manipulation behaviors. The mechanism analysis reveals that the incentive effects of tax cuts are realized through financing, specialized divisions, and the creation of added value. Notably, the “financing effect” exhibits a path dependence among high-tech enterprises. Furthermore, in terms of tax preferential policies, the “R&D expenses plus deduction” policy demonstrates the most significant incentive effect, while the “15% tax rate preference” is less effective than initially anticipated. However, the combined effect of both policy types proves to be significant in promoting R&D innovation, thereby enhancing the impact of a single-policy approach. Nevertheless, a structural phenomenon regarding the incentive effect on the input and output sides is observed. Through empirical analysis, this paper not only presents fresh ideas for improving tax reduction policies and unleashing the potential of scientific and technological innovation, but also offers essential insights for facilitating technological catch-up and achieving high-quality economic development.

Similar content being viewed by others

Introduction

Innovation assumes a pivotal role in fostering the advancement of the national economy, contributing to ~50% of the overall GDP growth (OECD, 2015). Presently, we witness a significant upswing in the latest phase of the scientific and technological revolution and industrial transformation. The amalgamation and assimilation of science, technology, economic progress, and social development gather pace, while international scientific and technological competition converges toward the forefront of knowledge. Leading nations perceive scientific and technological innovation as the primary theater for the global strategic landscape, prompting them to devise strategic plans for scientific and technological innovation spanning the forthcoming 5 to 10 years.Footnote 1In this regard, the comprehensive bolstering and strategic implementation of science and technology innovation policies have emerged as a prevailing trend and fundamental approach to foster innovation. Within the post-competitive landscape, enterprises face the formidable challenge of breaking through the technological dominance of industry leaders and resolving the issue of technological stagnation. Facilitating the innovation of pivotal core technologies with utmost efficiency and unwavering determination stands as the sole pathway for Chinese enterprises to surmount the inherent drawbacks of being latecomers and attain technological catch-up.

China is dedicated to promoting a leap-forward enhancement of production efficiency through innovation and constructing a novel model of stable growth via technological catch-up. Despite being a global manufacturing powerhouse, the ability to achieve catch-up has triggered academic discourse. Firstly, driven by cost advantages and substantial domestic market demand, Chinese enterprises primarily rely on imitation and incremental innovation of existing products or technologies (Liu et al. 2011). Secondly, a significant number of Chinese manufacturing firms find themselves confined to the lower echelons of the global value chain due to their low technological proficiency and limited value addition (Brandt and Thun, 2010; Guan and Yam, 2015). Thirdly, with the deceleration of growth, the conventional “troika” development model (consisting of consumption, investment, and exports) has become unsustainable (Liu et al. 2017). In response to the aforementioned concerns, China has expedited the realization of high-level scientific and technological self-reliance. In May 2015, the Made in China 2025 initiative was launched, harnessing the advantages of the national system and encouraging Chinese enterprises to engage in exploratory innovation by assimilating and adopting novel knowledge, thereby forging an internationally competitive manufacturing industry.

According to the National Innovation System Theory (Rikap, 2022) and the Triple Helix Theory (Etzkowitz and Leydesdorff, 2000), the government plays a crucial role in shaping innovation capabilities. As a significant policy instrument for government macro-control, tax policy can stimulate R&D investment, upgrade industrial structure, and optimize production relationships through systematic and targeted tax reduction measures. Since the introduction of “structural tax cuts” in China at the end of 2008, they have become a prominent guideline for tax reduction and even tax reform in the country. Notable milestones in the timeline of tax reduction reform include the direct increase of the income tax reduction ceiling from 500,000 yuan to 1 million yuan in 2018 and the elevation of the starting point for small-scale taxpayers in 2021, accompanied by a halving of corporate income tax for small and micro enterprises. As per the information released by the State Administration of Taxation, China has achieved cumulative tax cuts and fee reductions exceeding 12 trillion yuan from 2013 to 2021, leading to a decline in the macro tax burden from 18.7% in 2012 to 15.1% in 2021.Footnote 2The tax burden on enterprises has experienced a significant reduction, leading to substantial improvements in both the national innovation input index and innovation output index. However, empirical evidence suggests that there is still a need to enhance the ability and level of scientific and technological innovation among enterprises. The efficiency of scientific and technological investment also requires further improvement, and the tax reduction policy itself warrants further refinement. In this context, accurately evaluating the strategic impact of tax reduction and proposing an optimized tax policy scheme for the new stage becomes a pivotal topic. Drawing on the dataset of China’s listed A-share manufacturing enterprises spanning from 2008 to 2019, this paper specifically focuses on examining the influence of tax cuts on enterprises’ R&D innovation. It elucidates the role of tax reduction in promoting R&D innovation by means of enhancing financing, specialized division, and creating added value. Furthermore, this study analyzes the heterogeneous impact of this mechanism on manufacturing enterprises operating in high and low-technology sectors. Additionally, it explores the incentive effect of existing tax reduction policies on enterprises’ R&D innovation.

The paper makes several key contributions. Firstly, while the existing literature has examined the influence of tax cuts on corporate R&D innovation from various angles, the proxy variables used to measure tax cuts mostly revolve around effective tax rates for enterprises. This paper, however, takes into account corporate tax evasion and R&D manipulation, constructing a dummy variable for tax reduction. By incorporating both pre- and post-tax cut scenarios, the paper offers a more realistic indicator construction, thereby providing support for the development of a more comprehensive tax reduction policy. Secondly, departing from the extensive research focusing on the impact of tax cuts on corporate innovation solely from a cash flow perspective, this paper employs modern contract theory to delve into the mechanisms through which tax cuts influence corporate R&D investment and innovation levels. Specifically, it explores the economic dimensions of enhancing financing, specialized division, and creating added value facilitated by tax cuts, shedding light on China’s distinctive path of tax reduction incentives within the national system. Lastly, by employing existing tax rate and tax base methods, this paper empirically tests the incentive effect of individual policies as well as policy combinations on the innovation activities of various manufacturing enterprises. The findings serve as a reference for optimizing tax reduction strategies that guide the innovation trajectory of enterprises. By providing a multifaceted analysis, this paper offers a more comprehensive perspective for understanding the impact of tax cuts on innovation. Moreover, it establishes an essential foundation for enhancing tax reduction policies and achieving high-level technological self-reliance.

This paper is organized as follows. The second part is the literature review; the third part is the theoretical analysis; the fourth part describes the research design; the fifth part presents the benchmark regression and analysis; the sixth part is an expanded analysis that further explains the impact mechanism and heterogeneity of tax reduction on innovation, as well as the policy effects; and the final section presents a discussion and conclusion.

Literature review

Innovation serves as a fundamental catalyst for enhancing corporate value and driving overall economic growth (Solow, 1957; Wu et al. 2023). However, many companies exhibit hesitancy towards investing in innovative projects due to their prolonged gestation period and inherent risk of failure. As a result, governments employ a range of public policy incentives to encourage enterprise innovation. Diverging from direct R&D subsidies, tax cuts represent a more comprehensive policy instrument aimed at alleviating financial constraints (Bloom et al. 2002). Specifically, tax cuts primarily aim to reduce the cost of user capital for targeted companies, thereby stimulating R&D investment (Mukherjee et al. 2017; Bloom et al. 2019). In this context, we comprehensively review the current state of research on China, focusing on the following three aspects.

The first strand of literature examines the efficacy of tax cuts in stimulating innovation activities. Emerging economies, facing financial market distortions and challenges in intellectual property systems, encounter significant obstacles to effective management. Consequently, the function and effectiveness of tax cut schemes in these economies differ from those in developed nations (Al Fozaie, 2023; Ivus et al. 2021). The response of Chinese enterprises to tax cuts, as revealed in studies (Han and Kung, 2015; Chen, 2017; Zhang et al. 2018), demonstrates a notably positive attitude compared to their counterparts in other countries (Maffini et al. 2019; Ohrn, 2019; Rao, 2016; Yagan, 2015). Moreover, the government relies on tax incentives as a means to implement national directives, emphasizing technological upgrading and fostering the innovation sector (Wei et al. 2017).

The second strand of literature focuses on the underlying mechanisms through which tax cuts impact innovation. Firstly, tax cuts effectively address the positive externalities associated with R&D activities by lowering costs and expediting resource inflows (Cappelen et al. 2012). This, in turn, incentivizes firms to increase their R&D investments and stimulates enterprise innovation through general equilibrium effects (Lerner and Wulf, 2007) or investments in human capital (Akcigit et al. 2016; Yang et al. 2012). Secondly, tax cuts foster firm innovation by reducing the tax burden on businesses. By diminishing the minimum capital requirements for firms (Jones and Williams, 1998) and lowering the required return on investment in R&D activities for investors (Atanassov and Liu, 2020; David et al. 2000), tax cuts enable enterprises to allocate resources more effectively towards new technologies or products. Thirdly, lower taxes can reduce the resources that companies allocate to tax evasion, thereby redirecting these resources toward innovation activities.

The third line of research examines the limitations of tax cuts in fostering innovation activities. In the Chinese context, quantity-based innovation subsidies have been found to impede the growth of total factor productivity (Cao et al. 2022). When the government lacks the ability to observe the R&D productivity of enterprises, a flat tax or subsidy rate would not lead to a Pareto improvement (Akcigit et al. 2022; Yang and Zhang, 2021). Lowering corporate tax rates not only benefits firms by reducing their tax burden but also facilitates the entry of new firms and the expansion of existing ones (Giroud and Rauh, 2019). However, if the supply of R&D personnel is limited, any tax cuts may increase the demand for labor and other inputs, thereby driving up R&D costs (Suárez Serrato and Zidar, 2016). Moreover, since the reduction in corporate tax is financed by a decrease in public services, it may have a negative impact on productivity (“Timeline,” 2017). Additionally, providing corporate tax cuts necessitates additional revenue from other taxes, and the social cost of high taxes escalates as the tax burden grows, while the benefits of incentives diminish with their size (Slattery and Zidar, 2020; Corasaniti and Haag, 2019). Consequently, tax policies distort the allocation of economic resources and prove to be ineffective in promoting innovation. Innovation policies that prioritize financial returns, such as top-income tax cuts, are unlikely to yield successful outcomes (Bell et al. 2019; Cheng et al. 2019).

Even among developed countries, the impact of tax cuts on innovation has yielded diverse outcomes. These differences can be attributed to the significant heterogeneity of taxes across various R&D activities and their effects on different types of companies (Hall and Van Reenen, 2000; Cantante, 2020). While corporate tax cuts can effectively stimulate investment and employment in the overall economy, the distribution of benefits varies across sectors and groups. Manufacturing firms tend to respond to a reduction in the marginal corporate income tax rate or an increase in the investment tax credit by increasing capital expenditures and employment. Conversely, firms in the service sector often utilize the cash flow saved through tax cuts to boost dividend payments (Cloyne et al. 2023). Moreover, micro-level empirical studies vary in their approaches to addressing potential endogeneity issues arising from self-selection into R&D programs (Klette et al. 2000). Although policy incentives may increase the number of patents, they can also adversely affect patent quality as measured by claim scope (Fang et al. 2018; Dang and Motohashi, 2015). Such misallocation can perpetuate the market power of large companies and create higher barriers to entry, thus impeding overall productivity growth (Acemoglu et al. 2018).

Although it is widely acknowledged that innovation drives economic growth and requires support through policy instruments, the most effective approach in different contexts remains unclear (Brown et al. 2017). Previous research has mainly focused on examining the impact of specific policy instruments (Almus and Czarnitzki, 2003; Martin and Scott, 2000), including fiscal interventions such as R&D subsidies, tax incentives, and public procurement, as well as non-fiscal interventions such as infrastructure and regulations. However, limited attention has been given to exploring the mechanisms through which tax cuts affect heterogeneous firm innovation based on modern contract theory. Firstly, existing studies have employed narrative identification methods to assess the macroeconomic consequences of tax changes (Barro and Redlick, 2011; Cloyne, 2013; Cloyne and Surico, 2017; Nguyen et al. 2021) and have found significant impacts on macroeconomic outcomes, such as GDP, consumption, and investment (Romer and Romer, 2010). However, research from the perspective of endogenous technological change is lacking. Secondly, there is a gap in the literature when it comes to linking the macro and micro effects of tax cuts. While many studies have examined the long-term and short-term effects of tax cuts from a macro perspective (Liu and Williams, 2019; Mertens and Montiel Olea, 2018; Dabla-Norris and Lima, 2023), a substantial body of literature has estimated the impact of corporate tax reform on firm-level outcomes from a public finance standpoint. However, these studies primarily employ the difference-in-difference (DID) method to analyze cross-sectional differences resulting from policy changes (Zwick and Mahon, 2017; Ohrn, 2019; Yagan, 2015; Boissel and Matray, 2022), and the mechanisms examined mostly revolve around the impact on innovation by relaxing financial constraints, lacking a systematic analysis that links macro and micro outcomes. Thirdly, differences in methodologies and data coverage may lead to disparities in estimates. This discrepancy is often attributed to double counting, wherein subsidies targeted at firms are recorded twice—once as a separate subsidy transaction and again as part of the total national spending on incentive plans. Consequently, there is variation in the measurement of tax reduction indicators in existing research.

Theoretical analysis and research hypothesis

One of the primary hurdles in innovation lies in information asymmetry. Diverging from the current literature that primarily focuses on the impact of tax cuts in terms of cash flow preservation, this paper endeavors to examine the three economic mechanisms through which tax cuts influence technological innovation based on modern contract theory. These mechanisms encompass the relaxation of financing constraints, specialized division, and value-added creation. By formulating testable hypotheses grounded in economic theory and empirical evidence, this study aims to shed light on this subject.

Tax reduction and innovation

From an economic standpoint, both the government and firms act as rational economic agents, pursuing their respective interests throughout the process of technological innovation. Given that firms’ efficiency in technological production varies and their private information remains undisclosed to the government, we classify firms as agents and the government as principals based on their information asymmetry.

Within the framework of this principal-agent relationship, the government refrains from direct intervention in enterprises’ technological innovation activities. Consequently, it is unable to fully comprehend the technological status and R&D investments of these enterprises, placing it at an informational disadvantage. Given the divergent objectives of the government and enterprises, those enterprises possessing informational advantages will strategically engage with the government to maximize their profits. This behavior often leads to adverse selection and moral hazard. Hence, despite the incentive effects of tax cuts on firms’ technological innovation, such as cost reduction, risk dispersion, and positive signal generation (Akcigit et al. 2022), these cuts also have crowding-out effects. The crowding-out effects manifest in various ways. Firstly, the information asymmetry and conflicting objectives between enterprises and the government place the government at an informational disadvantage. Tax cuts can give rise to adverse selection and moral hazard issues for firms (Chen et al. 2021b), potentially even diminishing their enthusiasm for innovation. Secondly, the dynamic nature of the external market environment poses challenges for the government in effectively controlling the magnitude of tax cuts. As a result, R&D costs may rise, prompting firms to redirect their efforts towards more financially lucrative projects (Corasaniti and Haag, 2019), thereby potentially impeding the desired impact of tax cuts on innovation. To address the moral hazard and adverse selection issues stemming from the principal-agent relationship between the government and enterprises, the government should devise incentive mechanisms that foster the alignment of objectives between the two parties. In this regard, two key constraints come into play: the incentive compatibility constraint (IC), which binds the interests of the government and enterprises together, and the individual rationality constraint (IR), ensuring that the income derived from technological innovation for enterprises does not fall below the income generated when not engaging in such activities.

In 2019, China implemented a new round of tax and fee reduction policies with the goal of inclusive, substantive, and accurate burden reduction, which has a strong expected burden reduction effect on micro tax burden subjects (Slattery and Zidar, 2020). Therefore, for the effect of China’s current tax reduction policy, the incentive effect may be greater than the crowding-out effect. Based on the above analysis, this paper proposes the following assumptions :

Hypothesis 1: The incentive effect of tax cuts on corporate technological innovation is greater than the crowding-out effect.

Impact of tax cuts on financing constraints

A crucial determinant impeding enterprise innovation and development pertains to the capital landscape. Financing constraints exert a constraining influence on the upgrading of the industrial value chain (Ge et al. 2018) as well as corporate research and development (R&D) investment (Brown et al. 2012), particularly in contexts characterized by intense market competition (Beladi et al. 2021). Enterprises with a proclivity for external financing and operating within high-tech industries showcase heightened levels of innovation within regions boasting well-established stock markets. However, the advancement of credit markets has hindered their capacity for innovation (Hsu et al. 2014).

From the perspective of cash flow, when enterprises are not beneficiaries of tax reduction policies, the marginal return on their technological innovation tends to be lower than the marginal return for society as a whole. Consequently, the optimal investment level for maximizing corporate profits falls significantly short of the investment required to maximize social benefits. Financing constraints emerge as a pivotal factor that limits both enterprise production and innovation. Effective tax reduction measures can alleviate these constraints faced by enterprises (Chen and Yang, 2019). On one hand, tax reduction can mitigate internal financing constraints for enterprises by curbing cash flow expenditures, thereby opening up possibilities for innovation (Boycko et al. 1996). On the other hand, tax reduction can also lower external financing costs (Dai and Chapman, 2022), attracting increased venture capital, mitigating external financing constraints, and stimulating enhanced innovation performance. This is achieved by conveying positive signals to the market and resolving information asymmetry between capital supply and demand (Devereux et al. 2018). Consequently, tax reduction reduces the initial-stage costs associated with enterprise innovation, resulting in a decline in the marginal cost of innovation and an increase in optimal investment in innovation compared to scenarios without tax cuts. Building upon the aforementioned analysis, this paper proposes the following hypotheses:

Hypothesis 2: Tax cuts promote corporate technological innovation by alleviating financing constraints.

Hypothesis 3: Tax cuts ease financing constraints and increase financial support for R&D activities from both internal and external financing.

Impact of tax Cuts on specialized division

Specialized division of labor enables enterprises to leverage their comparative advantage in resource allocation, accumulate production experience, drive technological progress, and enhance productivity (Constantinescu et al. 2019; Kim et al. 2022), particularly for small-scale enterprises (Becker et al. 2022). External transaction costs and internal management costs serve as primary catalysts in facilitating the specialization of enterprises (Williamson, 1987). Nevertheless, the burden of high transaction costs may prompt enterprises to opt for vertical integration, producing intermediate goods and finished goods simultaneously, thus diminishing the level of specialization within the enterprise.

Firms characterized by higher productivity demonstrate the ability to generate greater profits from equivalent R&D investments. Consequently, the allocation of a reduced profit wedge and a lower R&D wedge holds a greater appeal for high-productivity firms compared to their low-productivity counterparts. The substantial complementarity between research outcomes and firm types suggests that high-productivity firms are inclined to imitate low-productivity firms, thereby augmenting the potential for information rents and resulting in more pronounced distortions in the optimal allocation. The essence of tax reduction lies in diminishing the institutional transaction costs between enterprises and governments. Furthermore, through the reduction of information asymmetry between enterprises and markets and the alleviation of coordination and decision-making costs, tax reduction can effectively stimulate enterprise vitality and foster a specialized division of labor (Pack and Saggi, 2001). Tax reduction can also lower the costs associated with industrial division and collaboration, facilitate cross-regional cooperation among enterprises (Hoseini and Briand, 2020), guide enterprises towards focusing on products with a comparative advantage, generate technological development and economic benefits (Yu and Qi, 2022), and ultimately lead to productivity improvement. Based on the comprehensive analysis above, this paper presents the following hypotheses:

Hypothesis 4: Tax cuts promote corporate technological innovation by promoting specialized division of labor.

Impact of tax cuts on added value

Existing evidence demonstrates the influence of product market competition on innovation (Aghion et al. 2015), and corporate pricing power serves as an indicator of market forces. The markup rate reflects the disparity between product prices and the enterprise’s marginal cost, while the capacity of high markup rate firms to sustain their position is a vital measure of their dynamic competitiveness (Bellone et al. 2016). Relative to price takers, firms endowed with robust pricing capabilities can secure supernormal profits beyond the market level (De Loecker and Warzynski, 2012), thereby acquiring additional innovation resources and enhancing innovation-related income, which contributes to the advancement of enterprise innovation.

The determination of optimal profit and subsidy wedges for firms is based on the tradeoff between maximizing allocative efficiency and minimizing information rents. To incentivize firms to invest more in innovation beyond profit maximization, the government reduces the profit wedge and increases the innovation wedge. The larger the disparity between an enterprise’s private value and social value, the less likely it is to internalize the social benefits derived from investment in innovation. Therefore, it is imperative to encourage enterprises to invest in innovation. Tax reduction exerts a positive influence on the enhancement of enterprise pricing capability, albeit contingent upon the optimization of production factor allocation and improvements in production efficiency (Ottaviano and van Ypersele, 2005). Furthermore, the impact of tax reduction on markup pricing varies depending on market competition levels and reliance on external financing, with more pronounced effects observed in highly competitive industries and enterprises with low external financing dependence (Davies et al. 2018). Based on the above analysis, this paper proposes the following hypotheses:

Hypothesis 5: Tax cuts promote enterprises’ technological innovation by creating added value.

Study design

Data source and variable setting

Data source

In this paper, 2008–2019 Shanghai and Shenzhen A-share listed manufacturing enterprises are taken as samples, and the main variables are from Wind and the CSMAR database. The original data are processed as follows: first, ST, * ST, and delisting samples during the study period are excluded; second, financial industry samples are excluded; third, the observed values in the year of IPO are excluded; fourth, observed data with obvious abnormal core financial indicators are excluded; fifth, in order to improve the quality of data, the samples with continuous data for at least 5 years based on the principle of 5-year continuity are kept; sixth, the data are subject to 1% tail reduction.

Variable setting

Explained variables

Common variables that measure enterprise innovation include R&D expenditure, the proportion of R&D personnel, and the number of patent applications. Since the above variables cannot fully reflect the enterprise innovation level, this paper adopts the following two different variables to characterize the innovation level: (1) R&D expenditure intensity (Rdintensity), which is the ratio of R&D expenditure to total assets, indicating the R&D investment intensity of enterprises; and (2) the ratio of the net increment of intangible assets to total assets (ITAssetRatio), measured as (net intangible assets-net intangible assets in the previous year)/total assets. Since the intangible assets project includes innovation output, such as the patent rights and copyrights of the enterprise, the increment of net intangible assets can comprehensively evaluate the level of enterprise innovation.

Explanatory variables

The average effective tax rate (EATR) has significant explanatory power on the allocative efficiency of firms (Chen et al. 2021a), and its measurement is divided into forward-looking and backward-looking methods. The forward-looking average effective tax rate is the difference between the expected pre-tax return rate of marginal investment and the tax return rate, while the backward-looking average effective tax rate uses the real data of the enterprise’s tax payment and taxable income. The forward-looking average tax rate can not only describe the effect of tax reduction on technological innovation but also comprehensively reflect the influence of different financing methods. However, although the effective tax rate is the result of factors including tax reduction and corporate tax evasion, the decline in the effective tax rate is not related to tax evasion (Drake et al. 2020). Based on this fact, this paper draws on the practice of Devereux and Griffith (2003) by using the forward-looking effective average tax rate to measure the tax rate borne by enterprises and sets the sample (incentive) with an increase in profit but a decrease in effective average tax rate compared with the previous year to 1 (otherwise 0) to identify the impact of tax cuts on corporate behavior.

Control variables

To overcome the interference of omitted variables, this paper introduces control variables at the enterprise level with reference to existing studies: corporate asset-liability ratio (tLev), current debt ratio (sLev), the proportion of intangible assets (Intratio), cash holdings (cash), investment expenditure rate (Invt), Tobin ‘s Q value (tobin), return on net assets (ROE), enterprise age (lnage), growth (Growth), and liquidity ratio (Liquidity). All the control variables have passed the multicollinearity test, and the variance inflation factor was less than 10.

Asset-liability ratio (tLev, total liabilities divided by total assets at the end of the period). In general, the higher the financial leverage of a firm, the higher the debt service pressure, and the accumulation of financial risk has a certain negative impact on innovation inputs (Kaplan and Zingales, 1997).

Current Liability Ratio (sLev, current liabilities divided by total assets). The rising current debt ratio of the enterprise means that the cash flow of the enterprise will be impacted, which will increase the risk to some extent, thus affecting its innovation activities (Coricelli et al. 2012).

Proportion of intangible assets (Intratio, intangible assets divided by total assets). Intangible assets include R&D (Research and Development), organizational capital, human capital, and information capital, which are important factors that affect innovation and determine economic growth (Hansen and Serin, 1997).

Cash holdings (cash, (monetary funds + trading financial assets)/total assets). Abundant cash holdings of a firm indicate a stronger endogenous financing capacity, which can provide more financial support for innovative activities (He and Wintoki, 2016).

Tobin Q value (tobin, the ratio of the market value of a firm’s total assets to its book value). The Tobin Q value can be used to measure the investment opportunities of enterprises, which is positively related to their technological innovation activity (Ernst, 2001).

Return on net assets (ROE, net income divided by average net assets). The return on net assets is the return rate obtained by the common stock investor entrusting the company’s management personnel to apply their funds. The higher the return on net assets is, the stronger the profitability is, so the enterprise has more profits to invest in the R&D activities of the enterprise (Ederer and Manso, 2013).

Age (lnage, logarithm of years in business). Firms with longer years of operation tend to have accumulated abundant resources, laying a foundation for innovation (Coad et al. 2016). However, the longer the business life, the less innovative the firm is (Huergo, 2006).

Growth (Growth, (current year’s revenue - previous year’s revenue)/previous year’s revenue). Growth determines whether a company can occupy a key strategic position and continue to grow in an increasingly competitive marketplace (Coad and Rao, 2010). Enterprises with higher growth will generate more internal cash flow, allowing them to invest in more innovative projects.

Liquidity ratio (Liquidity, ratio of current assets to current liabilities). The liquidity ratio reflects the ability of the enterprise’s assets to meet the need for rapid liquidation of investments without affecting normal operations. A large liquidity ratio can be quickly utilized and deployed by the firm, which is suitable for the enterprise’s R&D activities (Alessandri et al. 2014).

Data descriptions

Descriptive statistics of the primary variables in this paper are presented in Table 1. The average value of Rdintensity is 3.940, and the standard deviation is 7.392, which indicates that there is a great difference in R&D investment among different enterprises, and there is polarization of R&D investment among enterprises. Furthermore, the standard deviations of Itassetratio and Incentive indicate a more balanced relationship between innovation output and tax reduction between enterprises. This means that in terms of enterprise innovation, there is a mismatch between the output side and the input side, and there is still a structural imbalance in R&D investment, achievement transformation, and innovation competitiveness.

Model setting and estimation method

To verify the influence of tax reduction on enterprise innovation level, we establish the following basic model:

where Innovation represents the innovation level of an enterprise, which is the explanatory variable in this paper, including R&D expenditure intensity (Rdintensity) and the ratio of the net increment of intangible assets to total assets (Itassetratio). incentive represents the average effective tax rate of enterprises, and α1 is the core coefficient considered in this paper, the economic meaning of which is the substitution elasticity of the average effective tax rate to the enterprise innovation level. CV is a set of control variables. ηi and ωt are individual and time-fixed effects, respectively. εi,t is the random error term of the model. A two-way fixed-effect model is used to control the fixed effects of time and industry. ε is the random error term of the model.

Benchmark regression results and analysis

Impact of tax reductions on corporate innovation

Table 2 presents the regression outcomes of the baseline model (1). Upon controlling for individual and time-fixed effects, the effects of tax reduction on the intensity of R&D expenditure and the proportion of net increment of intangible assets to total assets are reported in Columns (1) to (2). The coefficient is found to be statistically significant and positively associated at a 1% significance level, indicating that tax reduction can enhance both the level of innovation and the intensity of R&D investment.

However, it is important to acknowledge the presence of inflated R&D expenditure used by some companies to qualify as “high-tech” enterprises without genuinely allocating those funds towards actual R&D activities. The inclusion of such samples can influence the regression results. Additionally, although income shifting through patents may serve as a means for firms to avoid tax obligations (Cheng et al. 2021), existing research has not provided strong evidence of significant corporate tax avoidance or positive real economic impacts following tax reform.

To enhance the accuracy of the regression results, columns (3) to (4) exclude enterprises engaging in R&D manipulation based on the criteria set by Bhojraj et al. (2009). Remarkably, even after implementing these adjustments, the coefficient remains significantly positive. This signifies that tax reduction incentives effectively stimulate the generation of patents and copyrights, as well as the adoption and assimilation of new technologies.

The benchmark regression results indicate that tax reduction effectively reduces enterprise production and operational costs, enhances available funds for enterprises, and facilitates R&D activities. Moreover, tax reduction lowers the cost of capital associated with R&D investment, fosters greater intensity of R&D expenditure, enhances the return on investment for R&D activities, and encourages increased participation of enterprises in innovation endeavors.

Robustness test

While the previous study controls for firm-level variables of interest and examines the impact of R&D manipulation on firms’ innovation activities, the control variables fail to encompass all the factors associated with firm-level innovation. As a result, various approaches are employed to assess the robustness of the empirical findings.

Endogeneity treatment

In order to address the endogeneity issue arising from reverse causality and other factors, this study aims to construct instrumental variables. The relationship between tax reduction and tax administration has been extensively explored in the existing literature, where the limited enforcement capacity in developing countries necessitates a tax system that interacts with the financial system, resulting in suboptimal economic activity. Enhancing tax administration can help narrow the tax burden disparity among enterprises (Gordon and Li, 2009). To examine this, the present paper utilizes the intensity of tax administration as an instrumental variable, drawing inspiration from Mertens (2003), who gauges tax administration intensity through the degree of tax effort in finance.

Tit is the tax revenue of local government in year t, GDPit is the gross national product of local governments in year t, IND1it is the added value of the first industry in year t, IND2it is the added value of the secondary industry in year t, and TIEit is the total import and export amount of each local government in year t. The local government tax enforcement activities intensity (TE) is obtained by subtracting the actual value of \(\frac{{T_{it}}}{{GDP_{it}}}\) from the value of \(\frac{{\hat T_{it}}}{{\widehat {GDP}_{it}}}\) predicted by Eq. (2); the larger the value is, the greater the intensity of tax enforcement activities of local government is. And then the instrumental variables are estimated using the 2SLS regression method.

Table 3 reports the results of the two-stage regression of the instrumental variables. Column (1) reports the results of the first-stage regression, where TE is significantly positive at the 1% significance level, confirming the correlation between the instrumental variables and the endogenous variables. The first-stage F-value is greater than 10, which also shows that there is no weak instrumental variable problem and the exogeneity assumption cannot be rejected. The results reported in columns (2)–(3) show that the fitted incentive coefficients are significantly positive. This indicates that after the treatment with instrumental variables, tax cuts still maintain a significant contribution to the intensity of corporate R&D investment and the level of R&D innovation, and the basic findings maintain a good robustness.

Control regional fixed effects

While the benchmark model includes year-fixed effects to capture the annual macro impact experienced by all regions, it is important to acknowledge that the resource and infrastructure attributes of the region where the enterprise is situated can also influence innovation activities. Hence, our study further incorporates regional fixed effects, allowing us to control not only for the inherent characteristics of the city that remain constant over time but also the current features of the city that may change. The regression outcomes are presented in Table 4. Remarkably, despite accounting for regional-level characteristics, the regression coefficients retain their direction and significance at the 1% level. This indicates that the results remain robust even after controlling for regional characteristics, thus affirming the significant positive impact of tax reduction on enterprises’ R&D investment and innovation output.

Policy shock test

Supply-side structural reform serves as the central strategy for promoting the high-quality development of China’s economy. In the long term, this reform aims to foster new momentum and growth drivers through technological innovation, industrial transformation, and upgrading (Fuqian, 2018). Since 2016, China has implemented a series of tax and fee reduction policies as part of the supply-side structural reform, with the intention of providing enhanced support for enterprise innovation. The effects of these policies have been comprehensive. Considering the nature of fee-clearing reform, the reduced tax burden on enterprises cannot be shifted through the form of charges. Thus, the supply-side structural reform genuinely alleviates the tax burden on enterprises, enabling them to pursue innovation. To further assess the efficacy of these policies, this study conducts a policy shock test. Given that the 2016 tax and fee reduction policies constitute a nationwide reform without an explicit control or treatment group, an intensity-based DID model is constructed for estimation. The degree of policy impact serves as the basis for dividing the control and treatment groups. In this study, we employ the effective average tax rate of each industry in each year from 2008 to 2015 as an indicator to gauge the impact of the supply-side structural reform. By multiplying it with the time variable of policy implementation, we form a DID term in the multiplicative model. Subsequently, a year-and-individual fixed-effect model is constructed for estimation purposes. The specific model is set as:

where Tax is the effective average tax rate by industry in each year, and Policy is whether the firm is affected by the supply-side structural reform. Tax × Policy is the cross-factor of the supply-side structural reform, φ1 indicates the difference in the impact on firms’ R&D innovation after the supply-side structural reform for industries that are hit by the supply-side structural reform relative to those that are hit by it less. μi and ωt are the individual and year-fixed effects, which control the factors at the enterprise level and the time level.

The empirical results in Table 5 show that industries with a great decline in the average effective tax rate have a greater incentive effect on the R&D investment intensity and innovation level of enterprises, as the coefficient is always negative. This indicates that an increase in tax reduction has a significant positive effect on the R&D investment and innovation output of enterprises, and the basic conclusions maintain sound robustness.

Further analysis

Analysis of the impact mechanism

The above research shows that tax reduction can significantly promote enterprise innovation activities. However, the above analysis focuses only on the overall effect of tax reduction on corporate R&D investment and innovation output. The following text will further study the mechanism by which tax reduction promotes enterprise R&D input and innovation output. Intermediary effect analysis is an important step to test whether a variable is an intermediate variable and to what extent. Baron and Kenny (1986) provided a seminal and widely employed mediation model in the social sciences designed to determine and validate the extent to which an independent variable affects a given outcome variable through a mediator. This method hinges on a series of stepwise regression analyses, each aimed at establishing a specific condition for the mediation analysis, this paper uses stepwise test regression coefficient method to study the internal mechanism of tax reduction’s influence on enterprise innovation:

where M is the mechanism variable to measure the financing effect, specialized division effect, and added value effect of enterprises. Initially, Model (2) evaluates the “total effect” of the independent variable on the dependent variable. This first step in establishing a mediation effect seeks to demonstrate a significant relationship between the independent and dependent variables. Subsequently, Model (5) indirectly assesses the significance of the product of coefficients by sequentially testing coefficients α1 and β1, which aims to ascertain the establishment of mediation. Lastly, Model (6) is employed to discern whether the mediation by the mediator is complete or partial. When both the mediator and independent variable are included in the regression model, if the influence of the independent variable becomes non-significant or diminishes, it indicates complete mediation. If the effect of the independent variable remains significant but is reduced, it indicates partial mediation.

Financing effect test

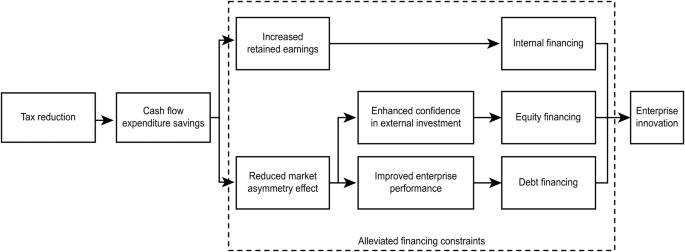

Maintaining the daily production and operational activities of an enterprise requires a sufficient cash flow, which serves as the fundamental condition. However, due to the presence of information asymmetry in the financial market, financing constraints impede the R&D activities of enterprises. When confronted with such constraints, enterprises encounter greater difficulties in accessing debt financing and equity financing, leading to increased financing costs. As a result, they tend to rely on internal financing channels. Nevertheless, given the substantial investment required for innovation, enterprises often find themselves unable to rely solely on internal cash flow to meet the demand for innovation funds, ultimately leading them to abandon innovation pursuits. In this regard, we argue that tax reduction can effectively address the aforementioned issues and promote innovation. The specific impact pathway is illustrated in Fig. 1.

It illustrates that the financing effect of tax cuts can indeed influence corporate innovation which is realized through internal financing, equity financing, and debt financing channels.

Therefore, this paper chooses financing constraints (Cfs) as an intermediate channel to test the relationship between tax reduction and innovation level. The KZ index, SA index, and WW index are commonly used to measure enterprise financing constraints in the existing literature. This paper uses the method of Hadlock and Pierce (2010) for reference and uses the SA index to calculate the financing constraints of enterprises, as shown in Eq. (6). The larger the SA index is, the greater the financial constraints of enterprises.

where Size is the natural logarithm of the total assets of the enterprise and Age is the registration period of the enterprise.

Table 6 presents the regression results of Eqs. (4) and (5), depicting the relationship between tax reduction and corporate financing constraints. The regression result of tax reduction on corporate financing constraints is presented in (1). It reveals a significantly negative impact of tax reduction on enterprise financing constraints at the 1% level, suggesting that tax reduction effectively alleviates such constraints. Additionally, Columns (2)–(3) demonstrate the impact of corporate financing constraints on R&D investment intensity and innovation levels, exhibiting a significant negative association at the 1% level. This finding underscores that financing constraints hinder enterprises from actively participating in innovation activities. Therefore, tax reduction serves as a catalyst by mitigating enterprise financing constraints, consequently promoting the intensity of R&D investments and innovation outputs.

To further analyze the influence of different financing channels on enterprises’ innovation activities, financing constraints (Cfs) are divided into internal financing (Ifs), equity financing (Efs), and debt financing (Lfs) according to the different financing channels. Referring to the treatment methods in most studies, cash flow is used to represent internal financing, i.e., (net profit of current period + depreciation of current period)/total assets of the enterprise, in which the larger the value of ifs is, the smaller the financing constraint of the enterprise is. The proportion of equity financing change in total assets (change in the value of equity/total assets) is used to measure the equity financing channel, in which the larger the value of Efs is, the smaller the financing constraint of enterprises is. Finally, the debt financing intensity is calculated by using the proportion of net expenditure of enterprise interest in total assets in the current period, and the larger the value of Lfs is, the smaller the financing constraint is.

Table 7 exhibits the regression results of Eqs. (4) and (5). Columns (1) to (3) present the regression results of tax reduction and its impact on debt financing, equity financing, and internal financing, respectively. The findings indicate a significantly positive influence of tax reduction on internal financing and equity financing channels at the 1% level. This suggests that tax reduction effectively alleviates the financing constraints faced by enterprises by facilitating internal financing and equity financing. However, tax reduction does not lead to an increase in the scale of debt financing for enterprises, implying the presence of soft restraint inertia in debt financing. Columns (4) to (9) depict the impact of debt financing, equity financing, and internal financing on the intensity of R&D investment and innovation levels within enterprises. In all cases, the regression coefficients are significantly positive at the 1% or 5% levels. These results indicate that tax reduction reduces enterprise costs, enhances the level of internal free cash flow, improves the availability of equity, enhances financing capabilities, and ultimately promotes increased R&D investment and innovation output, including the introduction of new technologies.

Specialized division effect test

With increasing economic globalization, the specialized division of labor has become a form of enterprise production organization. Many enterprises have stripped noncore businesses to obtain economy-of-scale advantages, which is conducive to promoting enterprise innovation. The role of tax reduction in deepening the division of labor will be conducive to enterprise innovation. To test this mechanism, this paper introduces specialization (VAS) indicators. Referring to the practice of Devos and Li (2021), the modified value-added method is used to measure the degree of enterprise integration by the share of added value in each industry chain in sales revenue. Since integration and specialization are the two poles of enterprise production organization, the larger the VAS is, the greater the degree of enterprise integration, and the weaker the ability to specialize.

Table 8 reports the regression results of Eqs. (4) and (5). The regression result of tax reduction to a specialized division of labor is listed in column (1). The influence of tax reduction on the degree of enterprise integration is significantly negative, indicating that tax reduction can weaken the process of enterprise integration and promote the specialized division of labor. Columns (2) and (3) indicate the influence of the specialized division of labor on R&D investment intensity and innovation level. The significantly negative coefficient of VAS indicates that specialized subdivisions promote innovation. Therefore, tax reduction can play an innovative incentive role by promoting the specialized division of labor.

Added value effect test

The market pricing ability of enterprises reflects their core competitiveness. Enterprises with higher pricing power can obtain more innovative resources from the market. The strengthening effect of tax reduction on enterprise pricing ability will help improve the innovation level. To verify the existence of a markup pricing effect, this paper constructs and tests the Additionrate variable. According to the approach by De Loecker and Warzynski (2012), this paper uses the enterprise markup pricing rate to measure enterprise value-added capability. The greater the Additionrate is, the stronger the value-added capability.

Table 9 reports the regression results of Eqs. (4) and (5). The regression result of tax reduction to enterprise value-added ability is listed in column (1). The influence of tax reduction on enterprise value-added ability is significantly positive, indicating that tax reduction has an added value effect that can strengthen enterprise value-added ability. Columns (2) and (3) indicate the impact of value-added capabilities on enterprise innovation. The significantly positive coefficient of Additionrate shows that strong value-added capability can help promote innovation. Therefore, the added value effect of tax reduction helps improve enterprise innovation levels.

Financing effect formation mechanism

Financing constraints are an important obstacle to innovation in transitional economies and are also a long-term focus of government departments. Since September 2021, China has continuously emphasized the importance of small and medium-sized enterprises in solving the difficulties posed by enterprise financing difficulties and expensive financing and relieving the pressure of enterprise operations. Previous research has shown that tax reduction can promote enterprise innovation by alleviating financing constraints. At present, although the literature has recognized this mechanism, no strong driving relationship has been shown between sufficient cash flow and the necessity of innovation.

To further elucidate the formational path of the financing effect, this study conducts an empirical examination of heterogeneity among manufacturing enterprises. Utilizing the Classification of High-tech Industries (Manufacturing) (2017) issued by the National Bureau of Statistics, the listed manufacturing enterprises are divided into high-tech manufacturing enterprises and low-tech manufacturing enterprises for subsample analysis. The results are presented in Table 10. Columns (1) to (3) depict the financing effects of tax reduction on high-tech manufacturing enterprises, while columns (4) to (6) depict the financing effects on low-tech manufacturing industries. The regression outcomes demonstrate that tax reduction has a positive effect on alleviating financing constraints for both high- and low-tech manufacturing enterprises. However, the impact is more pronounced for high-tech manufacturing enterprises. Nevertheless, concerning the influence of financing constraints on the direction of enterprise investment, the alleviation of financing constraints solely promotes R&D investment and innovation levels within high-tech manufacturing enterprises. In contrast, the impact on innovation in low-tech manufacturing enterprises lacks statistical significance. These findings suggest that the establishment of a financing effect necessitates certain conditions to be met.

The above tests indicate path dependence on the financing effect of tax reduction; that is, the financing constraint mechanism only exists for high-tech enterprises. The reason is that the greater the tax reduction policy an enterprise enjoys, the higher the position of the enterprise industry or the stronger its dominant position in the market, which is beneficial to further strengthening the recognition and trust of external investors. This creates a cyclical “policy spillover” effect, thereby developing a stronger influence in the credit and equity markets and expanding financing channels. From the perspective of innovation level, tax reduction shows heterogeneity in enterprise type. This is because the innovation ability of enterprises is largely dependent on the absorption and digestibility of new technologies (Cohen and Levinthal, 1989). Although low-tech manufacturing enterprises have certain production and manufacturing foundations, innovation is mostly micro and technological in less difficult aspects such as product appearance and design. Tax reduction leads to a lower relative cost of tangible assets compared with intangible assets. Therefore, for low-tech manufacturing enterprises, it is more attractive to introduce new technology and invest fixed assets from the market to facilitate the advantage of scale economy than to invest in R&D. However, the market-oriented technology innovation services of high-tech manufacturing enterprises are based on technological innovation, so the financing effect of tax reduction plays a more significant role in promoting innovation among high-tech manufacturing enterprises.

Test of the policy effect

Against the background of the state’s strong support for enterprise technological innovation, a variety of tax incentives are used to stimulate enterprise R&D investment and promote innovation output. Different tax incentives have different effects on enterprise innovation. The same enterprise may enjoy a variety of tax incentives. Therefore, it is not only necessary to pay attention to the effect of a single policy but also to evaluate objectively the comprehensive effect of policy combinations to optimize existing policy combinations, thereby maximizing policy effectiveness and promoting enterprise innovation.

The Enterprise Income Tax Law, revised by China in 2008, defines the tax preferential mode and scope based mainly on enterprise income tax rate, plus deduction and accelerated depreciation, and integrates the original preferential tax policy to form a unified preferential tax rate. Based on the process of tax incentives, this paper divides the existing tax incentives into two categories: one is the preferential tax rate based on 15% corporate income tax rate, and the other is the preferential tax base rate based on additional deductions and accelerated depreciation. The income tax rate allows for concessions by reducing the income tax rate payable by enterprises to reduce corporate income tax costs, thereby increasing corporate profits after tax. The additional deduction policy reduces the tax payable by deducting a certain proportion of taxable income based on the actual amount. This paper selects the 15% preferential corporate income tax rate and the R&D expense super deduction tax base preferential policy as the research object. It analyzes the differences in its effect and explores whether this policy combination can produce an effect in which “1 + 1 > 2”. Further, it divides manufacturing enterprises into low- and high-tech manufacturing industries and further compares and analyzes the effects of different tax incentives on different types of enterprise innovation.

Table 11 presents the regression results of the preferential policy involving a 15% tax rate and R&D expenses plus tax reduction. Columns (1) to (6) illustrate the regression outcomes of the 15% preferential tax rate policy solely for manufacturing enterprises. M1 represents samples in Manufacturing, M2 represents samples in High-tech Manufacturing, and M3 represents samples in Low-tech Manufacturing. However, the results indicate that the impact of the 15% preferential tax rate on corporate innovation activities lacks statistical significance. Consequently, the policy has not achieved the anticipated outcomes, leaving room for further exploration. Columns (7) to (12) exhibit the regression results of the R&D expense super deduction policy exclusively for manufacturing firms. The findings reveal that the R&D expense super deduction tax base preferential approach can stimulate enterprise investment in R&D activities. Nevertheless, its impact on innovation output activities, such as technology introduction, is not statistically significant. The estimations conducted in this study reveal heterogeneous effects of existing tax incentives on corporate innovation activities. One potential explanation for this disparity is that the “one-size-fits-all” 15% preferential tax rate is exclusively applicable to individual key development industries. Once identified as “high-tech,” enterprises merely need to fulfill the pre-examination requirements to continue benefiting from the preferential tax rate, thus undermining the policy’s effectiveness. Furthermore, China’s preferential tax policies solely focus on the R&D investment stage, lacking stringent requirements for the innovation output stage. As a result, there exists a noticeable gap between the effects of this policy on enterprise innovation output and the intended expectations.

In order to investigate the combined effect of the 15% preferential tax rate and the R&D expense super deduction policy, the interaction of the 15% preferential tax rate and the R&D expense super deduction policy is introduced on the basis of a single preferential policy. If the enterprise enjoys two policies at the same time, Policy Portfolio = 1; Otherwise, it is 0. The model is further designed as follows:

The interaction coefficient χ3 reflects the impact of policy combination on the innovation activities of enterprises. If χ3 is less than 0, it indicates that the simultaneous implementation of the 15% preferential tax rate and the R&D expense super deduction policy will inhibit the effect of a single policy. On the contrary, if χ3 is greater than 0, it indicates that there is a complementary relationship between the policy combination. Table 12 shows the effect of the policy combination of the 15% preferential tax rate and the R&D expense super deduction policy. As shown in Table 12, the effect of this policy combination on the R&D investment level of manufacturing enterprises is significantly positive at the 1% level, indicating that the simultaneous application of the 15% preferential tax rate and the R&D expense super deduction policy can strengthen the single-policy innovation incentive effect. However, the impact of this policy combination on the innovation degree of manufacturing enterprises is not statistically significant. This result verifies the mismatch between the R&D input end and output end of enterprises, indicating that although tax reduction incentives can promote domestic manufacturing enterprises to invest considerably R&D activities, there are still structural imbalances in the transformation of results and innovation competitiveness.

Discussion and conclusion

Discussion

As China’s phase of catch-up economic growth approaches its conclusion, the Chinese government has been diligently working towards transforming the economy from a developing one reliant on foreign technology to an advanced economy driven by independent innovation. We have now entered the era of big science, characterized by an increased focus on organized basic research, the growing influence of institutional safeguards and policy guidance on innovation output, and the significant role of tax cuts in promoting corporate innovation.

Existing research predominantly centers on the theoretical and empirical aspects of tax reduction, specifically examining the role of alleviating financing constraints in enhancing the level of enterprise innovation from a cash flow perspective (Atanassov and Liu, 2020; Beladi et al. 2021; Cappelen et al. 2012; Jones and Williams, 1998; Yang et al. 2012; Yang and Zhang, 2021; Zhu et al., 2006). However, few studies have comprehensively investigated the impact mechanisms and pathways through which tax cuts affect corporate innovation from macro and micro perspectives. Innovation has been a subject of longstanding interest, yet a unified understanding of why implementing tax cuts promotes firm innovation remains elusive. Our main contribution lies in leveraging modern contract theory, which incorporates the notion of asymmetric information, to explore whether tax cuts implemented by the government, acting as the principal, can effectively elevate the level of innovation within society. It is important to note that R&D investment represents just one of the potential applications within this conceptual framework.

Our conceptual framework presents a novel approach to understanding the drivers of innovation. In this framework, the government acts as the principal and makes a sacrifice in terms of information rent, namely by reducing the tax burden, with the aim of incentivizing enterprises to intensify their efforts and enhance the level of innovation. To tackle the challenges of moral hazard and adverse selection inherent in the principal-agent relationship between the government and enterprises, the government must devise incentive mechanisms that foster alignment between the profit maximization objective of firms and the social welfare maximization goal of the government. Given the constraints of incentive compatibility and participation, our study focuses on three economic mechanisms: alleviating financing constraints, fostering specialized division of labor, and promoting value-added creation. These mechanisms are examined to assess the impact of tax reduction on the R&D investment and innovation levels of enterprises. The financing constraint mechanism originates from the condition of individual rationality, while the mechanisms of specialized division and value-added creation stem from the condition of incentive compatibility. Additionally, we introduce heterogeneity analysis into the model, whereby random enterprise types can capture various characteristics of the real world and yield applicable insights.

Conclusions

The influence of tax reduction on enterprise innovation has received extensive attention. Against the background of supply-side structural reform, the Chinese government has issued a series of tax and fee reduction policies to reduce enterprise tax burden, improve enterprise innovation ability, and promote enterprise transformation and upgrading to realize high-quality development. Based on the perspective of supply-side structural reform, this paper studies the effect of tax reduction on enterprise innovation activities. Through empirical analysis, the following conclusions are drawn. (1) The positive impact of tax reduction on innovation outweighs the crowding-out effect, indicating an overall stimulating effect. (2) The incentive effect of tax reduction is manifested through the mitigation of financing constraints, the specialized division effect, and the added value creation effect. However, the “financing effect” of tax cuts exhibits channel heterogeneity. Tax cuts can effectively promote corporate R&D investment and innovation output by facilitating internal financing and equity financing, while debt financing channels display a persistent soft constraint. Moreover, the establishment of the “financing effect” is path-dependent for high-tech enterprises. (3) The policy of “additional tax deduction on R&D expenses” demonstrates the most pronounced incentive effect, while the impact of the “15% preferential tax rate” is not significant. The combined implementation of these two policy types exhibits a clear incentive effect on innovation and can enhance the effectiveness of each individual policy. However, there still exists a disparity between innovation input and output, indicating a mismatch.

Based on the analysis results, the following policy recommendations are put forth. Firstly, policymakers should deepen the tax reduction and fee reduction policies based on the development requirements and innovation characteristics of enterprises. These policies should aim to reduce operational costs for enterprises and enhance the competitiveness of the manufacturing industry while safeguarding existing advantages. Additionally, it is important to expand the availability of credit loans specifically for manufacturing enterprises and encourage equity financing and debt financing to prioritize the needs of manufacturing enterprises, thereby alleviating financing constraints. Secondly, leveraging the advantages of the national system, there should be a reinforced focus on investment in basic research. Fiscal policies have varying degrees of effectiveness in incentivizing innovation behavior among innovation participants. By establishing an effective supply system that stimulates demand, fiscal policies can guide and scale innovation activities. As a key investor in basic research, the government should steadily increase financial investments and optimize the integration of tax incentives to further support this area. Thirdly, it is crucial to coordinate the dual functions of tax neutrality and regulation within the tax system. Further analysis reveals that the “financing effect” is influenced by path dependence. Tax reductions provide enterprises with increased cash flow; however, their investment flows do not primarily focus on independent R&D. Capital, being a vital production factor associated with national security and social stability, necessitates government regulation and guidance in the new phase of development. It is imperative to improve the channels for debt financing and enable the government’s leading role in unlocking the potential of scientific and technological innovation.

While this study has made practical contributions to China’s policy landscape, it is important to acknowledge certain limitations. Firstly, due to data constraints, our study predominantly focuses on China’s listed firms, potentially overlooking the impact on small and medium-sized enterprises. Future research endeavors could employ firm surveys and case studies to validate and strengthen the robustness of our findings. Secondly, despite our efforts to control for relevant variables at the firm level, it is possible that some factors influencing innovation have not been fully accounted for. Thus, future studies should consider incorporating additional control variables that may play significant roles in the innovation process. Lastly, our examination of the effect of tax reductions on firm innovation has been conducted using a fixed effects model. It would be beneficial for future research to explore alternative econometric approaches to model and assess optimal tax reduction policies at various time points, providing a more comprehensive understanding of their effects. In summary, while this study presents valuable insights into the impact of tax cuts on firm innovation, addressing these limitations through further research will enhance the comprehensiveness and applicability of the findings.

Data availability

The underlying data cannot be shared publicly owing to issues of confidentiality.

Notes

Germany adopted the High-Tech Strategy 2025 2025 (HTS 2025) in September 2018; Singapore released the Research, Innovation and Enterprise 2025 (RIE2025) in December 2020; South Korea released The Fourth Basic Plan for Supporting the Cultivation of Scientific and Technological Talents (2021–2025) in February 2021; Japan released The Sixth Basic Sci-Tech Plan (2021–2025) in March 2021; Russia introduces a new phase of the National Scientific and Technological Plan in April 2019; the National Science Board releases the Vision 2030 in May 2020; South Korea develops the Towards a Talent Power in 2030-Long-term Innovation Direction of Science and Technology Talent Policy; France started implementing the Research Planning Act 2021–2030 in January 2021; the UK released the Research and Development Roadmap in July 2020; and the EU started implementing the ninth phase of Horizon Europe (2021–2027).

In 2009, the enterprise income tax reduction for small and low-profit enterprises; in 2014, the levy rate of 6% and 4% of the degenerate value-added tax was 3%; in 2015, the zero-value-added tax rate for export services such as offshore service outsourcing and film and television services was implemented; in 2017, six tax reduction policies were implemented at one time; in 2018, the upper limit of income tax halved collection was directly increased from 500,000 yuan to 1 million yuan, and the income tax incentives for small and micro enterprises were expanded; in 2019, a series of tax reduction reforms were continuously launched for farmers’ markets, group entrepreneurship, small and micro enterprises of cultural enterprises, and software industry. In 2020, in response to the impact of the COVID-19 epidemic, many policies are bailout policies for small, medium and micro enterprises; in 2021, the “Government Work Report” proposed the implementation of new structural tax reduction measures, including raising the starting point of small-scale taxpayers, halving the corporate income tax on small and micro enterprises, etc. In 2022, we will increase the amount of tax rebates for small and micro enterprises at the end of the value-added tax period, exempt small-scale taxpayers from value-added tax, increase the proportion of additional deductions for R&D expenses of small and medium-sized technology-based small and medium-sized enterprises, implement a tax relief policy for small and micro enterprises in the manufacturing industry, increase the income tax incentives for small and micro-profit enterprises, implement the pre-tax deduction policy for equipment and equipment income tax of small and micro enterprises, further implement the six taxes and two fees reduction and exemption for small and micro enterprises and expand the scope of application.

References

Acemoglu D, Akcigit U, Alp H, Bloom N, Kerr W (2018) Innovation, reallocation, and growth. Am Econ Rev 108:3450–3491. https://doi.org/10.1257/aer.20130470

Aghion P, Cai J, Dewatripont M, Du L, Harrison A, Legros P (2015) Industrial policy and competition. Am Econ J Macroecon 7:1–32. https://doi.org/10.1257/mac.20120103

Akcigit U, Baslandze S, Stantcheva S (2016) Taxation and the international mobility of inventors. Am Econ Rev 106:2930–2981. https://doi.org/10.1257/aer.20150237

Akcigit U, Hanley D, Stantcheva S (2022) Optimal taxation and R&D policies. Econometrica 90:645–684. https://doi.org/10.3982/ECTA15445

Al Fozaie TM (2023) Behavior, religion, and socio-economic development: a synthesized theoretical framework. Hum Soc Sci Commun 10:1–15. https://doi.org/10.1057/s41599-023-01702-1

Alessandri T, Cerrato D, Depperu D (2014) Organizational slack, experience, and acquisition behavior across varying economic environments. Manag Decis 52:967–982. https://doi.org/10.1108/MD-11-2013-0608

Almus M, Czarnitzki D (2003) The effects of public R&D subsidies on firms’ innovation activities. J Bus Econ Stat 21:226. https://doi.org/10.1198/073500103288618918

Atanassov J, Liu X (2020) Can corporate income tax cuts stimulate innovation? J Financial Quant Anal 55:1415–1465. https://doi.org/10.1017/S0022109019000152

Baron RM, Kenny DA (1986) The moderator–mediator variable distinction in social psychological research: conceptual, strategic, and statistical considerations. J Pers Soc Psychol 51:1173. https://doi.org/10.1037/0022-3514.51.6.1173

Barro RJ, Redlick CJ (2011) Macroeconomic effects from government purchases and taxes. Q J Econ 126:51–102. https://doi.org/10.1093/qje/qjq002

Becker A, Hottenrott H, Mukherjee A (2022) Division of labor in R&D? Firm size and specialization in corporate research. J Econ Behav Organ 194:1–23. https://doi.org/10.1016/j.jebo.2021.12.006

Beladi H, Deng J, Hu M (2021) Cash flow uncertainty, financial constraints and R&D investment. Int Rev Financ Anal 76:101785. https://doi.org/10.1016/j.irfa.2021.101785

Bell A, Chetty R, Jaravel X, Petkova N, Van Reenen J (2019) Who becomes an inventor in America? The importance of exposure to innovation. Q J Econ 134:647–713. https://doi.org/10.1093/qje/qjy028

Bellone F, Musso P, Nesta L, Warzynski F (2016) International trade and firm-level markups when location and quality matter. J Econ Geogr 16:67–91. https://doi.org/10.1093/jeg/lbu045

Bhojraj S, Hribar P, Picconi M, McINNIS J (2009) Making sense of cents: an examination of firms that marginally miss or beat analyst forecasts. J Finance 64:2361–2388. https://doi.org/10.1111/j.1540-6261.2009.01503.x

Bloom N, Griffith R, Van Reenen J (2002) Do R&D tax credits work? Evidence from a panel of countries 1979-1997. J Public Econ 85:1–31. https://doi.org/10.1016/S0047-2727(01)00086-X

Bloom N, Van Reenen J, Williams H (2019) A toolkit of policies to promote innovation. J Econ Perspect 33:163–184. https://doi.org/10.1257/jep.33.3.163

Boissel C, Matray A (2022) Dividend taxes and the allocation of capital. Am Econ Rev 112:2884–2920. https://doi.org/10.1257/aer.20210369

Boycko M, Shleifer A, Vishny RW (1996) A theory of privatisation. Econ J 106:309–319. https://doi.org/10.2307/2235248

Brandt L, Thun E (2010) The fight for the middle: upgrading, competition, and industrial development in China. World Dev 38:1555–1574. https://doi.org/10.1016/j.worlddev.2010.05.003

Brown JR, Martinsson G, Petersen BC (2017) What promotes R&D? Comparative evidence from around the world. Res Policy 46:447–462. https://doi.org/10.1016/j.respol.2016.11.010

Brown JR, Martinsson G, Petersen BC (2012) Do financing constraints matter for R&D? Eur Econ Rev 56:1512–1529. https://doi.org/10.1016/j.euroecorev.2012.07.007

Cantante F (2020) Four profiles of inequality and tax redistribution in Europe. Hum Soc Sci Commun 7:1–7. https://doi.org/10.1057/s41599-020-0514-4