Abstract

This paper examines the stages of the digital transformational path that lies in front of incumbent banks in their conversion into digitally driven institutions and contributes by providing clarity in the parameters that define each stage and the key metrics to be tracked. It is a general review paper, with main tools employed the relevant scholar and grey literature & field observations. The paper identifies three phases for banking institutions’ digital transformation and proceeds with defining the characteristics of the phases and the distinct actions required for an institution to progress through them, employing a set of proposed key tracking indicators. The outcome adds to the, rather limited, academic literature on the subject and can be applied to all relevant banking institutions. Research needs further insides to articulate better the findings and expand them on a cross-examination of relevant theories and approaches. This paper aims at contributing to a growing, contemporary discussion, hopefully assisting in greater collaboration between practitioners and academics.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Digital transformation is an ever-increasing popular trend that cannot be ignored by any individual, organization or country. Technological advances like Internet of Things (IoT), artificial intelligence (AI), automation, remote monitoring, predictive maintenance, additive manufacturing, big data, cloud computing, analytics are seen as new, disruptive market opportunities for firms (Parida et al 2019; Warner and Wäger, 2019, Ferreira et al 2019). Most literature actually agrees on describing digital technologies as inherently disruptive (Jahangir & Zhiping 2015). Traditional banking institutions that are based on physical interaction with customers that access services exclusively or mainly at a branch, cannot stay untouched by this disruptive technology, as so elegantly described by Clayton Christensen’s work, The Innovator’s Dilemma (1997). The banking business is being deregulated, both from within the industry but also by the regulator (e.g. PSD2, Open Banking etc.). The traditional banking paradigm of the Relationship bank of the thirteenth century’ Banco di San Giorgio, the Industrial bank of the eighteenth century Barclays Bank in the UK or the Information Technology Bank of America of the 1950s (Panzarino, 2021; 7, Hildreth 2001) is threatened by digital disruption (Arnold and Jeffery 2016, Kroszner 2015), that, in turn, is dictated by the huge leap of new technology and evolving customer needs, behaviours and high-quality expectations (Pousttchi and Dehnert 2018; Hossain et al. 2021). New entries, fintechs moving into banking such as N26, Revolut, Klarna, Zopa, hybrid bigtech approaches such as Goldman Sachs launching Apple Card and JPMorgan current account for Amazon, or new banks (neo banks) such as Chime, Current, Monzo, Starling, digital banks launched by incumbents such as HelloBank! By BNP Paribas, MoneyYou by ABN Amro, Greenhouse by Wells Fargo, all change the game. As per the majority of practitioners (Broeders and Khanna 2015; Westerman et al. & Cap Gemini 2011) and scholars (Mergel et al 2019; Margiono 2021), without a fully digitized agenda, any incumbent will soon find their offering commoditized and their business model disrupted.

Almost inevitably (Hai et al., 2021; Venkatraman 2017), incumbents have to embark into a digital transformation journey (DTJ) that should see them into a new era. On that journey, bank management will need an understanding for navigating through the different approaches and options, extending beyond the consultancy reports to more systematic empirical evidence (Mergel, 2019) on the stages and the content and context of the DTJ. This paper addresses this issue by identifying three distinct phases that comprise a DTJ and by providing a set of actionable characteristics that each phase have. Bank management and stakeholders can use it for course-plotting.

Background literature

Defining digital transformation, digitization, digitalization

Digital transformation has not enjoyed a universal definition among scholars. Vial (2019) in his literature review registers 23 unique definitions. In fact, terms like digitization, digitalization, or digital transformation are used quite often interchangeably in the literature (Mergel, 2019; 10, Reis et al 2018; 412). For the purposes of the paper, we have adapted the definition of Mazzone (2014) the “deliberate and ongoing digital evolution of a company, business model, idea process, or methodology, both strategically and tactically” as the best suited to describe the journey ahead for the incumbent institutions. We will define digitization, as the material process of converting analogue streams of information into digital bits (Brennen and Kreiss 2016), that allows digitized information to be easily stored, transferred, manipulated, and displayed. We will also adapt the definition of digitalization commonly used from Gartner glossary, “Digitalization is the use of digital technologies to change a business model and provide new revenue and value-producing opportunities; it is the process of moving to a digital business”, gartner.com/it-glossary, in Gebauer et al (2020) and Gray and Rumbe (2015).

Research on digital transformation

The paper does not aim at conducting a systematic literature review on digital transformation and the phases of it. Instead, it draws from the work done by a number of academics. For a more informative literature analysis, we recommend commencing from the work done by Christensen (1997, 2016), Christensen et al. (2015) on digital disruption and some criticism of it (e.g. Danneels 2004), and follow the literature review and analysis papers published by Mergel (2019), Vial (2019), Rosenstand et al. (2018) and then Parida (2019) and Verhoef (2021). An interesting addition is a very recent publication on digital transformation literature review by Reis and Melao (2023), who having employed a meta-review methodology reviewing an extended range of articles, notice that the field started maturing after 2018. Same team, Reis et al. in a previous paper (2018), are mentioning the small representation of digital transformation in academia. These papers help amass the data that have been produced over the past decade on digital transformation, definitions and coherence with business models innovation. Earlier scholars (Markides 2006; Morakanyane et al. 2017) have also contributed.

As far as the banking DTJ is concerned, the concept of which is debated substantially in the fourth chapter of the book of Panzarino and Hatami (2021), we tend to agree with Bouwman et al (2018) who, in their work, conclude that research on DTJ is rather scattered and sometimes lacks depth, as it tends to focus on specific elements rather than the whole entity. We found rather limited academic research on banking digital transformation (Kalsing, Verhoef), while a lot has been posted by grey literature from, virtually, all major professional houses( Selma et al 2021). They also notice that academic research on the subject is still on early stages with no dominating authors and the focus is disseminated on many different areas.

Research objectives and methodology

Background information

Digital transformation, as abrupt as it may seem to some industries, it does not come overnight. It has a start, a path and a destination. It constitutes a journey. In describing this journey, practitioners and academics alike (Panzarino et al., 2021; Markides, 2017; Kalsing 2021) provide a number of different roadmap concepts for digital transformation varying on numbers of levels, from three phases of Panzarino and Hatami, (2021, pp. 54–74) and Verhoef, (2021), four paths of digital change (Hertzog, 2019) to the five stages of digital transformation by Saldanha (2019). Venkatraman (2017), employs a 3-stage concept splitting it on digitization, digitalization, and digital transformation, while Costa et al (2015, BBVA Digital Economy Watch), break the process of transformation towards digital banking in three stages of Response, Adaptation and Strategic Positioning. O’Connor et al., (2008) approach it via the radical innovation project life cycle concept, breaking it into discovery (exploration), incubation (experimentation) and acceleration (development). Earlier work acknowledges also a process-phased concept referring to earlier Business Model structures (4I-frarmework, Fraknerberger et all, 2013). What they have in common is that they all agree on a distinct, as well as defined and conscious, metamorphosis path, with its stages and specific milestones as well as measurable metrics.

Objectives of the research

This paper seeks to evaluate the digital maturity journey (DTJ) of the incumbent banking industry and to ascertain a path. Three research questions are being placed.

-

Q1. Is there an incumbent banking industry-specific, traceable and recognizable path for their digital maturity journey?

This question is motivated by the fact that the banking industry has been undergoing a rapid digital transformation in recent years, and it is important to understand whether there is a clear phased path that banks can follow to achieve digital maturity. We have discussed the fact that literature has provided different approaches to the stages of digital evolution, and we will be aiming at framing an answer for the banking institutions.

-

Q2. Can there be an identifiable set of enablers whose maturity defines the phases?

This question is based on the premise that achieving digital maturity involves developing specific capabilities and using technology in specific ways. By identifying the enablers that define the phases of the DTJ, we can gain a better understanding of the key factors that contribute to digital maturity in the banking industry.

-

Q3. Can a set of Progress Tracking Indicators (PTI) be developed for measuring progress made in the DTJ?

This question is important because it is essential to track progress made in the digital transformation of banks and to understand whether they are moving in the right direction. By developing a set of tracking indicators, we can better assess the progress and success of the DTJ and identify areas for improvement, providing, at the same time a useful checklist tool to practitioners.

Data gathering

The authors, applying their expertise on the field, employed three different sources of data for their research. The first source of information was the numerous published papers of grey literature by all established strategy and IT consultancies (namely, Accenture, MIT Center for Digital Business & Cap Gemini Consulting, BCG, McKinsey & Company, PWC). The references represent the reviewed sources, acknowledging that these being no scientific editions have an inevitable degree of repetition, generalization and popularization. Nevertheless, the sheer volume and attention put into the overall subject of the digital transformation and its enablers, demonstrates the relevance it has for the industry and provides an excellent source of practical knowledge. The second source of data came from the work previously done by scholars on the subject of banking digital transformation and its measurements. Quite a limited field yet, the papers that helped us build a better understanding of the scope are presented in the relevant literature support chapter, as well as in the rest of the article. Lastly, we draw also conclusions from a case study research (Yin 2013) conducted on the Greek systemic banking industry. The named research has been presented in full detail in the paper published by the authors titled, “Digital transformation journey for incumbent banks: The case of the Greek financial institutions” (submitted). The exercise remained qualitative and all relevant elements and descriptors (case, bounding system, context, in depth, study, selection, evidence, design) as presented in Table 1, [36] of Harrison et al. on their Case Study Research: Foundations and Methodological Orientations (2017) were observed.

Results

Phases of transformational life cycle

The paper examines the distinct phases of preparation, journey, and destination, and the key characteristics and actions taken in each phase. The DTJ is not strictly defined by timelines, but rather by conceptual distinctions, making it important to identify the key features of each phase. As stated, in this paper, we focus on three phases: Adapt, Grow, and Transform that we will examine separately. Understanding the characteristics of each phase is essential for banking institutions seeking to achieve digital transformation and enhance their digital capabilities. The phases are conceptually split rather that distinctly defined and they do not have a strict boundary on timelines, so, providing a very precise cut-off between the above groups/periods and the assignment of individual morphological elements to these periods was not a goal of this research.

Enablers

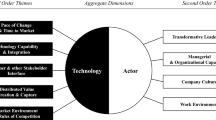

Digital transformation is multidisciplinary almost by definition, encompassing strategy, organization, information technology, supply chains and culture as well as “a host of newly defined roles for existing agents” as Verhoef names customers, partners, competitors (2021). He defines some strategic imperatives of digital transformation, i.e. identifies a set of key enablers that are necessary for any digital transformation to go ahead successfully:—Digital Resources—Organizational Structure Growth Strategy—Metrics and Goals (Verhoef et al 2021). Loonam et al (2018;) on a similar approach, stress that management needs to acknowledge the critical perspectives of strategic‐centric, customer‐ centric, organizational‐centric, and technology‐centric views in order to deliver digital transformations.

It is the paper’s view that Strategy, People, Technology but also Value Proposition formulate, in one conceptual framework (Fig. 1), the territories that include the facilitators of change that, once mobilized, can help a banking institution move across the stages. They are the contingency factors that can trigger, enable, and may even hinder the digital change, all interconnected, all contributing to every phase. We will examine their contributions per stage, later on. Figure 1 provides a schematic overview of the structure.

The key enablers to the digital transformation journey

Strategy and organization

Strategy and Organizational structure are the enablers that will configure the context within which transformation will take place. The approach for what needs to be done should start from a higher perspective on strategic positioning over the long term, it cannot be a stand-alone reaction to external factors or the technology, but it should form part of overall mission and company assessment (Kane et al. 2015; Allchin et al. 2020). Aligning operating model framework and design models with clear strategies is not a characteristic of digital transformation only, but a general management imperative (Campbell and Gutierrez 2021, and, earlier, Grundy 1995; 65–89, Porter 1980). Strategy setting in that context should follow the phases of the journey. Step 1 Diagnostics: this is the more inward-looking stage where each bank needs to do their own omphaloscopy Step 2 Direction: where do the winds blow, where do we stand, where do we want to go, how we do that. Key objective is to read the future customer preferences (Choi et al 2022), the regulatory environment, the technological advancements, the new and existing competitors’ behaviours and direction. Step 3 Transformation program: debate, decision and design of the one or multiple business models that will drive the organization into the new era (Reichert et al., BCG publications, 2022).

People and culture

Personnel theories emphasize the importance of getting everybody’s engagement and commitment. Embracing of the Digital Age will be a top down exercise and leadership should make sure (Wide, 2020) that such responsibility is not left to the IT specialists or external advisors/consultants (Selimovits, 2021). If the latter happens, any effort is no longer related to the whole organization but to the individual efforts of specialized departments. The whole team should embrace digital vision and change of culture (Henderikx and Stoffers 2022). Paying attention to the role of senior management in digital transformation is also important. The Chief Digital Officer (CDO) needs to ensure that the transformation process can be orchestrated smoothly. Singh and Hess (2017) and Margiono (2021) state that the CDO plays a different role from other C-level officers because he is responsible for the overall digital initiative and linking the IT and business functions. Training days for the top management, appointment of CDO in the top layer, sponsor of transformation at every major part of the bank, making the top executive team permanent part of the whole change, new digital roles, upskill trainings should also be part of the culture. Empowering all staff through New WoW—New Ways of Working-, remote access and fully digitized environments, will ensure cooperation and smoother transitions. As with all changes, there will be resistance to change efforts. Appropriate goal setting and critical communication can be the determinants on easing the transition (Akan et al. 2016).

Technology and innovation

New technologies are disrupting the traditional ways of management (Venkatraman 2017) and are subjecting all enterprises to a number of opportunities as well as challenges both internally and externally, providing a revamped opportunity for revitalization, transforming the very core of the business model as well as the wider environment that the company operates (Barrett et al. 2015). Technology, at its newest forms, is coming, with credit risk assessed by artificial intelligence, customer service covered by robotics, ledgers service back office, contracts serviced via blockchain and all core systems cloud-based (Harris and Wonglimpiyarat 2019). An earlier empirical study, with a strong focus on end-users inside the IT within banks in the German banking industry by Schmidt et al. (2016), revealed that inside experts consider the banks not ready for the last phase. If anything, banks still have to deal with a low degree of integration of their IT systems, not enough optimization of business processes, non-realized automation potentials and a lack of end-user training (Schmidt et al 2017). The alignment of IT strategies with other strategies has remained a difficult and controversial endeavour with further evidence needed as to how this alignment can be conducted in practice—not only related to IT strategies, but also from an organizational perspective (Matt et al 2015). Innovation leads also to open economies, opportunities for platform creations and ecosystems (De Reuver et al 2018) and banks need to embrace it. In a very recent publication, Zhang et al (2023) identify “two innovation types that are conducive to the digital transformation of incumbent firms: process-reconstruction innovation and product-renewal innovation”. Financial institutions, although not included in their research, are matching that pattern.

Value offering

What will now be changing dramatically, as the journey moves to its destination, is the reinvention by incumbents of the customer experience (CX). The new customer wants the best experience, in chunk bites and they want it now. Incumbents have to respond. The process begins with bringing in data and analytics-based insights about what really matters to customers and how best to deliver it to them, (Mckinsey by Diaz et al., 2017 and Olanrewaju 2014). It is not easy for many companies, especially those who have not mastered the full concept of digitalization and are still focusing their attention only on the front face of the activity to see it as a complete journey that cuts across multiple functions and channels. Companies must explicitly tie the reinvented CX to their operations (King 2019). If they focus only on the front-end experience and do not change the back-end operations that support it, the new experience is unlikely to be sustainable as per Mckinsey by Diaz et al. (ibid). Changes will be needed in both underlying processes and the way employees work.

Progress tracking indicators (PTI)

We treat metrics as the perimeter, the connecting points that help managers measure their progress and signify their passing from one phase to the other. Firms tend to employ success metrics related to reaching specific market targets and financial performance. These are the “Key Performance Indicators”, they have been used across industries for a long period (Kaplan and Norton 1996) and the use and practicality of these traditional indicators that ultimately direct to the bottom line such as cost, revenue, ROI is not questioned. The innovation management literature has also employed the terms, aiming at measuring innovation process that is not strictly financially translated (O, Connor et al., 2008), while a similar method employed is the identification of the Key Success Factors (Shah and Siddiqui 2006). As Christensen et al. (2008) argue, the key performance indicators that are to be used to measure success and progress for innovation, cannot rely on traditional financial measuring tools, as these can mislead management into comparing own innovation with the do-nothing option, missing competitors’ effects on longer term profitability of the company. There is need also of proof points that support overall narrative and progress of the specific initiatives (Allchin et al. 2020), moving away from monetary terms. That is not to say that money translated targets should be abolished in transformational projects. The average transformation program that is announced in the wider financial world demands a spending of about 5% of their annual revenue of the organization, spending that includes investment attributed to a host of changes including IT, maintenance, regulatory and compliance, etc. (Allchin et al. 2020). Management should feel that this is money well spent, thus it should be measured.

We propose therefore an adaptation of the approach of Kristiansen and Ritala (2018) who argue that large firms’ radical innovation should be measured by distinct monitoring mechanisms and we will be introducing, at each phase of the transformational journey, a list of primary tracking indicators matching each key enabler, aiming at helping management design the projects and follow-up progress in a more rounded way. In the deployment of the three phases and their corresponding tables, we have focused on the performance trackers that match strategy, people technology and value creation, excluding traditionally established KPIs that, we feel, research and practice have already mastered. These should be used as assessment criteria for the bank to place itself in the ranking vs competitors and self-vision, Grebe et al. (BCG, 2021), Kaufman et al. (2020), Wodzicki et al. (2020). Useful inputs to the search came for professional publications (Digital Directions Team 2022; Choi 2022; Mallick 2020; Schrage et al 2022).

Phases of the journey

Phase I: Adaptation phase “Toe in the water”

The first phase, describes the adaptation to the digital world, which is identified with incumbents looking at aligning digital technology with strategic priorities, mostly translated into improving their front-line offering, without really going into the specifics of the digital concept. It is the time that it is becoming clear that digital models are being embraced across all industry sectors (Weinstein, 2020). Rappa (2010) reports nine types (categories) and more than 40 sub-categories where online models fit well with the paradigm of the relevant industries, including banking & finance. Products themselves are still channelled through their old traditional way and they are designed and manufactured to service only or mainly the existing known channels i.e. branches, while electronic banking is still seen as novelty and complementary (Daniel and Storey 1997). The cost of introducing new technology at this phase is relatively smaller because it is easy to pick up the products, processes and channels that can be digitized with lesser resources, being in the periphery of the core proposition. Even more so, sales at that stage can benefit hugely as long as the institution understands that offering an online card or opening an account is far cheaper (the average transaction cost of branches is approximately 40 times higher than that of online banking, CEB Tower Group 2013), more efficient and more convenient for everybody. At these stage IT legacies remain as such, legacies and challenges. With the introduction of a completely new set of functionalities, modules and applications that now intercut with core banking, back-office processing systems are overloaded. At the same time, customers are accessing far more often their information data due to the early adaptation of online banking, increasing the pressure, resulting in disruptions, downtimes and a lot more problematic maintenance of the old systems of the bank (Panzarino). The digital potential is being understood for simple transactional interactions and digitization of back end processes but support to structural changes is still relatively low in the bank (Selimovits, 2021), cautiously avoiding challenge of status quo. Staff reductions are becoming a reality, creating a negative morale connotation for such changes. Management starts committing the organization to the new digital age.

Introduction of innovation is usually first appointed to in-house sources, mostly by the IT departments and known external IT suppliers. It is the safest approach, it starts cheaper and faster and with the added advantage of originality, since no one else would have access to such internal developments. Information Technology banks, i.e. the prevailing banking model of incumbents, having built a culture of dominance for themselves, would find it hard at that point to open the doors for cooperation with outsiders. Unknown costs that can easily escalate, scarce in-house talent, politics, will soon erode the beliefs in that approach. Most digital initiatives are an isolated approach.

Table 1outlines the key enablers and features required for an organization to turn towards digitization of business. The first track, Strategy & Organization, focuses on automating back-end processes, redesigning the customer front end, and streamlining IT attention towards digital developments. Key PTIs include the percentage of processes/products/documents digitized versus physical, the number of steps/stages reduced per process, and the percentage of internal projects with digital scope over the total annual plan of IT projects. The second track, People & Culture, highlights the importance of management commitment, creating a distinct digital unit, and embracing the new digital age. PTIs include the percentage of response to internal digital job openings, the percentage of staff adaptation of new ways, and the percentage of time spent working in new e-work environments. The third track, Technology & Innovation, focuses on business process redesigning, in-house innovation and experimentation, and introducing lean initiatives at branches/front office. PTIs include the number of new technologies and innovations introduced, the percentage of budget allocated, and the time to market for new propositions. The final track, Value Proposition, highlights the introduction of remote access/banking online/mobile presence, an advanced CRM environment, and digital retail sales channels. PTIs include the number of monthly active users, the net promoter score, and the number of applicants via digital channels.

Phase II: Growing phase “Free style swimming”

On the second phase, the pace of transformation is picking up by entering digitalization. The new business model options are coming into the scene. Abbott (2021) provides four strategies for a banking business model (that could be stand-alone or a mix): Sell only own products—the current incumbent approach-, build a distribution-driven ecosystem, sell own capability as a service or create new propositions through non-linear business models. Incumbents could set themselves these questions: Become an infrastructure provider (a shrinking but low costs defending action that requires the bank to provide financial services via other distributors with limited customer ownership) or a lifecycle central point (an expanding option with platform build up and extra services requirements). All scenarios will require next generation capabilities set up (back office, UX, AI, networks, staff skills). Paradoxically, this is the situation where banks may actually increase their costs having to maintain their very old IT legacy and build the new approach and the new systems. The management of the organization should be having a Digital Vision that shares with all. Digital Executive Board operational progress tracking fora, C-suite level appointment, creation of new department that advocate the digital adoption such as Centre of Excellence, as well as new job profile categories should be helping change the culture throughout the organization.

A fintech strategy is supposed to solve a problem. Instead of spending years to develop internally a new scorecard (and repeat), it is easier to work with a fintech start up to develop machine-learning scorecards that keep evolving. Such specialized companies have the capability “to provide banking services in 22 out of 36 Bank domains” as illustrated in the work of Hanafizadeh and Amin (2022). As per Derek White, Barclays' chief design and digital officer, Barclays has estimated that it is five times cheaper and three times faster for the bank to work with tech companies to find solutions to its cybersecurity, CX or big-data problems than trying to find a solution for themselves (Crowe 2015). Many new entrants are now coming into the ecosystem. The choice is not clear nor unlimited. As a worldwide survey by Deloitte presented in FinForum Greece, 2021, offered services of fintech and other new players (novobanks) are not mature enough as yet, as 80% of digital champions come from traditional banks and just 20% are challengers.

At this stage, market drives reduction of branch footprint, as the management starts to realize that physical branches may no longer be needed. The positive correlation between physical and digital is a quest. So is the role of the personnel. As evidence of the research by Kaur et al (2021), branch staff he's pivotal for communicating the digital benefits to clientele. Banks will be removing some traditional staff roles, back-office data entry, branch tellers, old legacy operations staff, call centre agents and will be adding some brand-new roles like business analysts and big data interpreters, fintech specialists, relationship managers for incubator labs, tech advisors for hackathon organizations, digital product and digital sales, social media content managers (King 2019). Likewise, leaders will need to be equipped with appropriate digital skills, contributing to the optimal development of the team (Hai Thanh et al 2021). It is only natural that not all will go smoothly. The role of Chief Digital Officer is one that will concentrate all enthusiasm, tension and failures of that digital revolution (Wide, 2020). No wonder that the average manager in the role has a much smaller occupancy time expectancy compared to the other C-level peers, (Papathomas and Konteos 2022). Agile and Design Thinking methods are fuelling innovation adaptation (Ghezzi and Cavallo 2020).

The value proposition has to offer customer access to internally produced propositions but also provide access to outside offering. The relevant technology, Open Banking, APIs (Zachariadis and Ozcan 2017) is there, as well as the regulatory environment e.g. PSD2. The use of online sharing platforms in other industries has substantially changed the perception of the idea. Uber increased the efficiency of underutilized assets and lowered the consumption prices of the services for the customer, while E-commerce platforms, such as Amazon Marketplace, have greatly reduced transaction costs for many small and medium-sized enterprises (SMEs) to sell products across states and borders, Li et al. (2018). Now the bank does (or should) think of concepts of fully developed platforms and ecosystems with its offering in the middle and with key decisions that will alter its DNA. The bank should normally by now have optimized front-end channels and should have decided on a business path forward. The first-generation products and services made for Digital First environment should now be coming into the market. Yet, now the first enthusiasm is passing and problems arise. Service should be of similar experience to every option and every channel used by the end user so that customer experience CX is common and uninterrupted. Omnichannel delivery is becoming a necessary model adaptation (Zhou et al. 2020), where the sale experience and service are seamless and meld the advantages of physical stores with the information-rich experience of online accessing, irrespective of the device, Lazaris and Vrechopoulos, (2014) and Saprikis et al. (2022). The branch remains centre—although COVID-19 has done a lot to weaken that notion (see Bechlioulis and Karamanis 2022 for example)—with the belief that all customers can use it, not everybody has access, understanding or interest in specific channels for example e-mobile (customer “branch skills” vs customer “digital skills”, Panzarino, pp 59).

Table 2highlights the key enablers and features required for an organization to turn towards digitalization of business. The first track, Strategy & Organization, focuses on automating back-end processes across all channels, reducing paper usage, and turning non-customer facing units digital. progress tracking indicators include the number of processes that become digitized, the percentage of digitization within processes, the internal steps/stages reduced per process, and the real-time view of transactions. The second track, People & Culture, emphasizes the importance of ensuring a bank-wide focus on top management's digital vision, creating a digital transformation office, and promoting the need to turn digital throughout the organization. PTIs include the percentage of response to internal digital job openings, the percentage of working time spent on new e-work environments, and the number of initiatives produced. The third track, Technology & Innovation, focuses on adopting new methodologies, creating an ecosystem and integration using fintechs, and applying a mobile-first approach. PTIs include the number of new technologies introduced, the feedback received, and the budget allocated. The final track, Value Proposition, highlights the mobile-first approach, an omnichannel fully operational model, and digital sales. PTIs include the percentage of customers channelled via new channels, the net promoter score, and the percentage of sales via e-channels. By implementing these key enablers and features, an organization can successfully turn towards digitalization of business, resulting in innovation and improved customer experience.

Phase III: Transformation phase “Deep Dive”

The third phase is where revolution, not evolution, kicks in. At this stage, all market forces, customers, regulators, banks, challengers are becoming more adaptable and knowledgeable of the new paradigm and, external to the banking business, players are coming for participation. Banks, at that transformational stage, can remove 20 to 25 per cent of their cost base by leveraging this digital shift to transform how they process and service (Olanrewaju 2014). This is the (future) state where survivors are making their point while late adaptation or failed efforts are taking their tolls both on challenger players and incumbents. This is by far the hardest state on incumbents’ effort to disrupt innovatively themselves and move into a new Business Model (BM). As Markides defines it, (2006), Business-model innovation is the discovery of a fundamentally different business model in an existing business. EasyJet, and Dell compete in their respective industries in substantially different ways from their competitors, such as British Airways, and HP; Amazon sets different standards from a chain bookstore. A disruption will have to be much more than just a new strategy for expansion (Markides, ibid), it will have to aim for a whole lot bigger and better marketplace, moving from a well-established and familiar mondus operandi to a new operating model (Panzarino; 55).

The bank has by now transferred most of its in-house branch capabilities into its external channels and it is ready to offer and possibly already does, digital only products. Barclays and the other High Street Banks in the UK have removed totally card and loan applications from branches. This is a full transformation state, a stage not without its perils or hard decision-making. Incumbents rarely create new digital business models; they are more likely to use digital technologies to extend or improve their existing activities in an evolutionary manner (Foss and Saebi 2017; Volberda et al. 2021; Warner and Wager, 2019). It is rather difficult to fundamentally alter a business model so that it reflects the changes brought about both by new digital technologies and changing customer needs and competitive dynamics (Chesbrough 2010). Research on the adoption of new technologies indicates that cognitive barriers affect the process; managers may not fully understand the structural impediments to change, and dominant logics within the firm may prevent people from adopting new ways of thinking (Chesbrough 2010; Chesbrough and Rosenbloom 2002). In fact, as the process of adopting digital technology is one of experimentation, trial-and-error learning, and discovery (see, for example, Frankenberger et al. 2013; McGrath 2010), the speed with which new digital business models are envisioned and the direction taken hinge critically on decision-makers’ cognitive make-up, which determines their awareness and understanding of the key issues and the range of possibilities for refashioning the business model (Chesbrough 2010; Sosna et al. 2010). It may be then to no surprise that the first intentions of banking industry, as described by CEOs, are an adaptation of a Phygital model (description at Anker 2021), a “safe bet” in that context.

By now, the bank has built its own in-house team of experts recognizing that the traditional accounting and econometrics degrees have, to a certain extent, to be replaced by coding programming and online marketing degrees. Executives need to address the organizational barriers that may arise during the transformation process, especially cultural inertia. Inertia in this context refers to the resistance that emerges during the transformation process, which could lead to slowing down or stopping the process. Inertia can take the form of employee resistance, which may prevent companies from achieving their digital transformation objectives, Margiono (2020). Many banks’ jobs at that stage will be very different from the nowadays-typical banking profile. Skills for digital development (data scientists, artificial learning engineers and blockchain integrators) will be in high demand but other new set of skills will also be required e.g. product managers for designing the CX and ensuring appropriate on boarding identity, behaviour psychologists to blend and fuse banking experiences with life cycle (King 2019).

On the future form of the customer interaction with banks and banking, things are clear. A survey of North American C-level executives revealed that 84% of their customers wanted individualized experiences, which can lead to an additional 18% in annual revenues. It is not really a choice for the banking sector. They have to find the model that produces no more channels or products but experiences. All coming generations of banks customers will expect to have a fully personalized experience, at the time of their liking, the device of their choice, with the service level constant and predictable. This is well demonstrated on the results of a research conducted by Majumdar and Pujari (2022) in the UAE that concluded “perceived ease and usefulness—and information—were the most influential factors on the usage and adoption of mobile banking apps”. In terms of timing, customer experience setting may be coming late for banks, as the retail CX is fully transformed, and business models are already entering the “now” economy. The FAAMG companies—Facebook, Apple, Amazon, Microsoft and Google (and a host of other names of course) are setting the barriers very high for everybody else by teaching retail customers worldwide what to expect—or demand. Millennials will not settle for two working days to clear a money transfer nor will they wait for the branch opening hours to buy stocks (Saprikis and Avlogiaris 2021). It is the Now Economy for Weinstein (2020), Right Now Economy for Tullman (2015).

Table 3outlines the key enablers and features required for an organization to implement a new business model, focusing on a customer-centred digital manufacturing approach. The first track, Strategy & Organization, highlights the importance of running one or multiple business models simultaneously, introducing intelligent process automation to replace human tasks, and centralizing, consolidating, and homogenizing scattered business lines through the use of digital. Key progress tracking indicators include the percentage spend on R&D, the cost of branch network reduction, and the net promoter score. The second track, People & Culture, emphasizes the importance of creating a digital-first culture, embedding digital skills in all job profiles, and implementing an end-to-end paperless back office. PTIs include the percentage of paper consumption, internal survey on satisfaction, and the percentage of adaptation of new ways by staff. The third track, Technology & Innovation, focuses on implementing next-generation technical capabilities, such as artificial intelligence and machine learning, robotic process automation, and blockchain management of contracts and transactions. PTIs include the metrics on applied systems, lean process redesign, and the percentage reduction cost to serve. The final track, Value Proposition, highlights the importance of providing instant time-to-yes on applications, multi-service offerings, and a holistic digital service. PTIs include the net promoter score, the percentage customer conversion from app to account, and the cross-sales ratio. By implementing these key enablers and features, an organization can successfully implement a customer-centred digital manufacturing approach, resulting in innovation and improved customer experience.

Discussion and limitations

Theoretical contribution

The objective of this study was to use academic and professional publications and empirical evidence to analyse and synthesize a framework that could provide a sounding board against which bank executives can compare and understand where their institutions stand in the DTJ and how to track it.

The research commenced with three Questions that defined the study, respectively. Each one contributes to academia in their own right. The contribution of Q1 is that it confirms the existence of a theoretical path that can deliver to banking institutions digital maturity status and highlights the characteristics of the journey from early adaption to growth and maturity. Q2 identified and analysed the four enablers of the process, Strategy, Technology, People, and—a, highly underrepresented in academia, element—Value. The study provided insights into the specific capabilities and technologies that banks need to develop and use to achieve digital maturity. Lastly, the theoretical contribution of Q3 is that it helps to track progress made by listing a set of Progress Tracking Indicators that can be used to assess the success of the DTJ and identify areas for improvement. This allows management of banking institutions and consultants to better understand where their institutions stand in the DTJ and make decisions that are more informed.

Overall, the study's theoretical contributions confirm the distinct, traceable, and recognizable metamorphosis path of digital maturity in incumbent banks and provide a practical framework for banks seeking to achieve digital maturity. The study extends the literature by incorporating all these three concepts (Phases, Enablers, PTIs) into one usable framework, in the form of three Tables, which has not previously been combined in a research context. The field is rather underrepresented in the academic literature, which leads us to believe that academia may have misinterpreted the importance of such practical and measurable indexes in a field that is anyway too new to be saturated.

Managerial contribution

This paper aims at contributing to a growing, contemporary discussion, hopefully assisting in greater collaboration between practitioners and academics. We believe that the paper adds well to the limited research that relates to digital transformation of banking institutions in three key ways: It progresses further the concepts of the phased transformational journey and the dependant key enablers by dwelling deeper on their characteristics. It also presents an inclusive, defined and articulated list of key tracking indicators that are of immediate use as a tool to bank managers and consultants alike for usage on their digital transformation tactical implementation assessment. This understanding is important in order to make necessary changes and investments in infrastructure and talent, and create a culture that supports digital transformation. The three Tables, that represent the accumulation of the article’s theoretical deployment, can be used as part of a handbook for a digital transformation project plan.

Research limitations

The findings of the paper may lack the empirical galvanization of the findings and the proven applicability of the theoretical framework i.e. tables combining all three concepts on the ground. Digital banking and all its managerial concepts are still at the very early stages of formation. Furthermore, Key metrics tend to have a wide popularity with practitioners, an interest that is not always mirrored in research journals. Further case studies analysis and follow-ups within the academia will help readjust Phases and Indicators or reconfirm their validity. It is suggested that empirical research—a possible survey or interviews among bank managers—is conducted to verify the above. We also consider that the research objectives (Phases, Enablers, PTI) themselves are too wide and they could be researched separately, giving the opportunity for a more thorough analysis.

Future recommendations

As stated, research needs further insides to articulate better the findings and expand them on a further cross-examination of relevant theories and approaches. There is a number of questions that came along the study and, we believe that, extension of research to these fields, would help advance the relevant knowledge field:

-

Are the four reviewed Enablers the key constituents or should there be a wider perspective? Do they have the same weight within each phase?

-

How are Enablers interlinked with each other? Is there an order of hierarchy and should there be other enablers?

-

What is the pace of transition from one Phase to another? Can institutions progress in the next phase without completing all enablers satisfactorily? Can financial institutions skip phases all together?

References

Akan, B., F.E. Ülker, and A.S. Ünsar. 2016. The effect of organizational communication towards resistance to change: A case study in banking sector. Economic Review: Journal of Economics and Business 14 (1): 53–67.

Allchin, C., et al. (2020). The state of the financial services industry 2020, when vision and value collide. Oliver Wyman—A Marsh & McLennan Company. https://www.oliverwyman.com/content/dam/oliver-wyman/v2/publications/2020/January/Oliver-Wyman-State-of-the-Financial-Services-Industry-2020.pdf

Anker, C. (2021). Phygital banking: The digital transformation of physical bank branches. Our Knowledge Publishing.

Arnold, D., and P. Jeffery. 2016. Chapter 5: The digital disruption of banking and payment services. In F. X. Olleros & M. Zhegu (Eds.), Research handbook on digital transformations II (pp. 72–91). Edward. https://doi.org/10.4337/9781784717766

Barrett, M., E. Davidson, J. Prabhu, and S.L. Vargo. 2015. Service innovation in the digital age: Key contributions and future directions. MIS Quarterly 39 (1): 135–154.

Bechlioulis, A.P., and D. Karamanis. 2022. Consumers’ changing financial behavior during the COVID-19 lockdown: The case of Internet banking use in Greece. Journal of Financial Services Marketing. https://doi.org/10.1057/s41264-022-00159-8.

Bouwman, H., S. Nikou, F.J. Molina-Castillo, and M. de Reuver. 2018. The impact of digitalization on business models. Digital Policy, Regulation and Governance 20 (2): 105–124. https://doi.org/10.1108/DPRG-07-2017-0039.

Brennen, J.S., and D. Kreiss. 2016. Digitalization. The International Encyclopedia of Communication Theory and Philosophy 66: 1–11. https://doi.org/10.1002/9781118766804.wbiect111.

Broeders, H., and S. Khanna. 2015. Strategic choices for banks in the digital age. McKinsey & Company. https://www.mckinsey.com/industries/financial-services/our-insights/strategic-choices-for-banks-in-the-digital-age

Campbell, A., and M. Gutierrez. 2021. Why you need an operating model: To align your people and deliver your strategy. Management and Business Review 1 (2): 66.

CEB Tower Group. 2013. Rethinking multichannel strategy: Improve the consumer experience through channel differentiation and proactive guidance. Arlington, VA: CEB Tower Group.

Chesbrough, H. 2010. Business model innovation: Opportunities and barriers. Long Range Planning 43 (2–3): 354–363. https://doi.org/10.1016/j.lrp.2009.07.010.

Chesbrough, H., and R.S. Rosenbloom. 2002. The role of the business model in capturing value from innovation: Evidence from Xerox Corporation’s technology spin-off companies. Industrial and Corporate Change 11 (3): 529–555. https://doi.org/10.1093/icc/11.3.529.

Choi, A., M. Dynes, Y. Erande, and D. Rosioru. 2022. Taking digital banking beyond customer journeys. BCG publications, retrieved from https://www.bcg.com/publications/2022/customer-value-and-banking-in-the-digital-age

Christensen, C.M. 1997. The innovator's dilemma: When new technologies cause great firms to fail. Harvard Business Publishing.

Christensen, C.M. 2016. The innovator's dilemma: When new technologies cause great firms to fail (Management of Innovation and Change). Harvard Business Review Press.

Christensen, C.M., S.P. Kaufman, and W.C. Shih. 2008. Innovation killers: How financial tools destroy your capacity to do new things. Harvard Business Review 86 (1): 98–105.

Christensen, C.M., M.E. Raynor, and R. McDonald. 2015. What is disruptive innovation? Harvard Business Review 93 (12): 44–53.

Costa, C., M. Macarena Ruesta, D. Tuesta, and P. Urbiola. 2015. Digital economy/The digital transformation of the banking industry. BBVA/Research, Digital Economy watch, 16 July 2015. https://www.researchgate.net/profile/David-Tuesta/publication/291357544_The_digital_transformation_of_the_banking_industry/links/56a2cc6f08ae1b65112cbdb9/The-digital-transformation-of-the-banking-industry.pdf

Crowe, P. 2015. Inside the new startup accelerator 'changing the DNA' of a huge bank. Business Insider Magazine. https://www.businessinsider.com/barclays-accelerator-for-tech-startups-2015-12

Daniel, E., and C. Storey. 1997. On-line banking: Strategic and management challenges. Long Range Planning 30(6): 898. https://doi.org/10.1016/s0024-6301(97)00074-5.

Danneels, E. 2004. Disruptive technology reconsidered: A critique and research agenda. Journal of Product Innovation Management 21 (4): 246–258. https://doi.org/10.1111/j.0737-6782.2004.00076.x.

De Reuver, M., C. Sørensen, and R.C. Basole. 2018. The digital platform: A research agenda. Journal Information Technology 33: 124–135. https://doi.org/10.1057/s41265-016-0033-3.

Digital Directions Team. 2022. 45 Digital Transformation KPIs: The Ultimate List. Retrieved from https://digitaldirections.com/digital-transformation-kpis/

Ferreira, J.J.M., C. Fernandes, and F. Ferreira. 2019. To be or not to be digital, that is the question: Firm innovation and performance. Journal of Business Research 101: 583–590. https://doi.org/10.1016/j.jbusres.2018.11.013.

Fin Forum. 2021. Shaping the Future of Banking & Finance. Tsomokos. http://www.tsomokos.gr/fin-forum-2021

Foss, N.J., and T. Saebi. 2017. Business models and business model innovation: Between wicked and paradigmatic problems. Long Range Planning 50 (3): 249–258. https://doi.org/10.1016/j.lrp.2017.07.006.

Frankenberger, K., T. Weiblen, M. Csik, and O. Gassmann. 2013. The 4I-framework of business model innovation: A structured view on process phases and challenges. International Journal of Product Development 18 (3/4): 249–273. https://doi.org/10.1504/IJPD.2013.055012.

Gebauer, H., E. Fleisch, C. Lamprecht, and F. Wortmann. 2020. Growth paths for overcoming the digitalization paradox. Business Horizons. https://doi.org/10.1016/j.bushor.2020.01.005.

Ghezzi, A., and A. Cavallo. 2020. Agile business model innovation in digital entrepreneurship: Lean startup approaches. Journal of Business Research 110: 519–537. https://doi.org/10.1016/j.jbusres.2018.06.013.

Gray, J., and B. Rumpe. 2015. Models for digitalization. Software & Systems Modeling 14 (3): 1319–1320. https://doi.org/10.1007/s10270-015-0494-9.

Grebe, M., Rüßmann, M., Leyh, M., Franke, M. R., & Anderson, W. 2021. The leaders’ path to digital value. BCG publications. https://www.bcg.com/publications/2021/digital-acceleration-index

Grundy, T. 1995. Breakthrough Strategies for Growth. Financial Times Pitman Publishing.

HaiThanh, N., N. VanQuang, and N.T. Mai. 2021. Digital transformation: Opportunities and challenges for leaders in the emerging countries in response to Covid-19 pandemic. Emerging Science Journal. https://doi.org/10.28991/esj-2021-SPER-03.

Hanafizadeh, P., and M.G.T. Amin. 2022. The transformative potential of banking service domains with the emergence of FinTechs. Journal of Financial Services Marketing. https://doi.org/10.1057/s41264-022-00161-0.

Harris, W.L., and J. Wonglimpiyarat. 2019. Blockchain platform and future bank competition. Foresight 21 (6): 625–639. https://doi.org/10.1108/FS-12-2018-0113.

Harrison, H., M. Birks, R. Franklin, and J. Mills. 2017. Case study research: Foundations and methodological orientations. Forum Qualitative Sozialforschung 18 (1): 19. https://doi.org/10.17169/fqs-18.1.2655.

Henderikx, M., and J. Stoffers. 2022. An exploratory literature study into digital transformation and leadership: Toward future-proof middle managers. Sustainability 14 (2): 687. https://doi.org/10.3390/su14020687.

Hildreth, R. 2001. The history of banks: To which is added, a demonstration of the advantages and necessity of free competition in the business of banking. Batoche Books Kitchener. https://socialsciences.mcmaster.ca/econ/ugcm/3ll3/hildreth/bank.pdf

Hossain, M.A., N. Jahan, and M. Kim. 2021. A multidimensional and hierarchical model of banking services and behavioural intentions of customers. International Journal of Emerging Markets, Ahead-of-Print. https://doi.org/10.1108/IJOEM-07-2020-0831.

Jahangir, K., and W. Zhiping. 2015. The role of dynamic capabilities in responding to digital disruption: A factor-based study of the newspaper industry. Journal of Management Information Systems 32 (1): 39–81. https://doi.org/10.1080/07421222.2015.1029380.

Kalsing, K. 2021. Three crucial phases of a digital transformation journey. Dataversity. https://www.dataversity.net/three-crucial-phases-of-a-digital-transformation-journey/#

Kane, G.C., D. Palmer, A.N. Philips, D. Kiron, and N. Buckley. 2015. Strategy, not technology, drives digital transformation. MIT Sloan Management Review and Deloitte University Press 14: 1–25.

Kaplan, R.S., and D.P. Norton. 1996. Strategic learning & the balanced scorecard. Strategy & Leadership 24 (5): 18–24. https://doi.org/10.1108/eb054566.

Kaufman, E., Lovich, D., Bailey, A., Messenböck, R., & Schuler, F. 2020. Remote work works—Where do we go from here? BCG publications. https://www.bcg.com/publications/2020/remote-work-works-so-where-do-we-go-from-here

Kaur, S.J., L. Ali, M.K. Hassan, et al. 2021. Adoption of digital banking channels in an emerging economy: Exploring the role of in-branch efforts. Journal of Financial Services Marketing 26: 107–121. https://doi.org/10.1057/s41264-020-00082-w.

King, B. 2019. Bank 4.0: Bank everywhere, never in a bank. Wiley.

Kristiansen, J.N., and P. Ritala. 2018. Measuring radical innovation project success: Typical metrics don’t work. Journal of Business Strategy 39 (4): 34–41.

Kroszner, R.S. 2015. The future of banks: Will commercial banks remain central to the financial system? In Preliminary draft: Prepared for the Federal Reserve Bank of Atlanta conference “Central Banking in the Shadows: Monetary Policy and Financial Stability Postcrisis.”

Lazaris, C., and A. Vrechopoulos. 2014. From multichannel to “Omnichannel” retailing: review of the literature and calls for research. ELTRUN—The E-Business Center Department of Management Science and Technology, Athens University of Economics and Business.

Li, W., M. Nirei, and K. Yamana. 2018. There’s no such thing as a free lunch in the digital economy. In: Sixth IMF Statistical Forum, Washington, DC.

Loonam, J., S. Eaves, V. Kumar, and G. Parry. 2018. Towards digital transformation: Lessons learned from traditional organizations. Strategic Change 27 (2): 101–109. https://doi.org/10.1002/jsc.2185.

Majumdar, S., and V. Pujari. 2022. Exploring usage of mobile banking apps in the UAE: A categorical regression analysis. Journal of Financial Services Marketing 27: 177–189. https://doi.org/10.1057/s41264-021-00112-1.

Mallick, A. 2020. Open Banking: The right KPIs for business value. Accenture publications, retrieved from https://bankingblog.accenture.com/open-banking-right-kpis-for-business-value

Margiono, A. 2021. Digital transformation: Setting the pace. Journal of Business Strategy. https://doi.org/10.1108/JBS-11-2019-0215.

Markides, C. 2006. Disruptive innovation: In need of better theory. Journal of Product Innovation Management 23 (1): 19–25. https://doi.org/10.1111/j.1540-5885.2005.00177.x.

Matt, C., T. Hess, and A. Benlian. 2015. Digital transformation strategies. Business & Information Systems Engineering 57 (5): 339–343. https://doi.org/10.1007/s12599-015-0401-5.

Mazzone, D. 2014. Digital or death: Digital transformation: The only choice for business to survive smash and conquer. Smashbox Consulting Inc.

McGrath, R. 2010. Business models: A discovery driven approach. Long Range Planning 43 (2–3): 247–261. https://doi.org/10.1016/j.lrp.2009.07.005.

Mergel, I., N. Edelmann, and N. Haug. 2019. Defining digital transformation: Results from expert interviews. Government Information Quarterly 6: 66. https://doi.org/10.1016/j.giq.2019.06.002.

Morakanyane, R., A. Grace, and Ph. O’Reilly. 2017. Conceptualizing digital transformation in business organizations: A systematic review of literature. In: 30th Bled eConference digital transformation—From connecting things to transforming our lives. https://doi.org/10.18690/978-961-286-043-1.30

Olanrewaju, T. 2014. The rise of the digital bank. McKinsey & Company. https://www.mckinsey.com/business-functions/mckinsey-digital/our-insights/the-rise-of-the-digital-bank

Panzarino, H., & Hatami, A. 2021. Reinventing banking and finance. Kogan Page limited.

Papathomas, A., and G. Konteos. 2022. Digital transformation journey for incumbent banks: The case of the Greek financial institutions. International Journal of Marketing Studies 14 (2): 13. https://doi.org/10.5539/ijms.v14n2p13.

Parida, V., D. Sjodin, and W. Reim. 2019. Reviewing literature on digitalization, business model innovation, and sustainable industry: Past achievements and future promises. Sustainability 11 (2): 391. https://doi.org/10.3390/su11020391.

Porter, M.E. 1980. Competitive strategy. Free Press.

Pousttchi, K., and M. Dehnert. 2018. Exploring the digitalization impact on consumer decision-making in retail banking. Electronic Markets 28: 265–286. https://doi.org/10.1007/s12525-017-0283-0.

Rappa, M. 2010. Business models on the web. http://digitalenterprise.org/models/models.html

Reichert, T., S. Mohr, K. Close, and A. Bailey. 2022. Digital transformation. BCG publications. https://www.bcg.com/capabilities/digital-technology-data/digital-transformation/overview

Reis, J., M. Amorim, N. Melão, and P. Matos. 2018. Digital transformation: A literature review and guidelines for future research (Chapter 41), 411–421. In: Rocha, Á., H. Adeli, L.P. Reis, and S. Costanzo eds. Trends and advances in information systems and technologies (WorldCIST'18 2018). Advances in Intelligent Systems and Computing, vol. 745. Cham: Springer. https://doi.org/10.1007/978-3-319-77703-0_41

Reis, J., and N. Melao. 2023. Digital transformation: A meta-review and guidelines for future. Heliyon 9 (1): e12834. https://doi.org/10.1016/j.heliyon.2023.e12834.

Rosenstand, C.A.F., F. Gertsen, and H. Vesti. 2018. A definition and a conceptual framework of digital disruption. In: The ISPIM innovation conference—innovation, The Name of the Game, Stockholm, Sweden on 17–20 June 2018. https://ispim.lemonstand.com/product/a_theoretical_definition_of_digital_disruption

Saldanha, T. 2019. Why digital transformations fail: The surprising disciplines of how to take off and stay ahead. Berrett-Koehler Publishers.

Saprikis, V., and G. Avlogiaris. 2021. Factors that determine the adoption intention of direct mobile purchases through social media apps. Information 12 (11): 449. https://doi.org/10.3390/info12110449.

Saprikis, V., G. Avlogiaris, and A. Katarachia. 2022. A comparative study of users versus non-users’ behavioural intention towards M-banking apps’ adoption. Information 13: 30. https://doi.org/10.3390/info13010030.

Schmidt, J., P. Drews, and I. Schirmer. 2016. End-users’ perspective on digitalization: A study on work order processing in the German banking industry. In 22nd Americas conference on information systems (AMCIS 2016).

Schmidt, J., P. Drews, and I. Schirmer. 2017. Digitalization of the banking industry: A multiple stakeholder analysis on strategic alignment. In: Presented at Americas conference on information systems (AMCIS), Boston.

Schrage, M., M. Vansh, and V. Kwan. 2022. How the wrong KPIs doom digital transformation. MIT Sloan Management Review 63 (3): 66.

Selimović, J., A. Pilav-Velić, and L. Krndžija. 2021. Digital workplace transformation in the financial service sector: Investigating the relationship between employees’ expectations and intentions. Technology in Society 66: 101640. https://doi.org/10.1016/j.techsoc.2021.101640.

Selma, V., M. Massaro, E.M. Bagarotto, and F. Dal Mas. 2021. The digital transformation of business model innovation: A structured literature review. Frontiers in Psychology 11: 539363. https://doi.org/10.3389/fpsyg.2020.539363.

Shah, M., and F. Siddiqui. 2006. Organizational critical success factors in adoption of e-banking at the Woolwich bank. International Journal of Information Management 26 (6): 442–456. https://doi.org/10.1016/j.ijinfomgt.2006.08.003.

Singh, A., and T. Hess. 2017. How chief digital officers promote the digital transformation of their companies. MIS Quarterly Executive 16 (1): 1–17.

Sosna, M., R.N. Trevinyo-Rodriguez, and S.R. Velamuri. 2010. Business model innovation through trial-and-error learning: The Naturhouse case. Long Range Planning 43: 383–407. https://doi.org/10.1016/j.lrp.2010.02.003.

Tullman, H. 2015. 4 rules of the ‘right now’ economy. Inc.com. www.inc.com/howard-tullman/four-rules-of-the-now-economy.html

Venkatraman, V. 2017. The digital matrix: New rules for business transformation through technology. Lifetree Media Book.

Verhoef, P.C., T. Broekhuizen, Y. Bart, A. Bhattacharya, J. Qi Dong, N. Fabian, and M. Haenlein. 2021. Digital transformation: A multidisciplinary reflection and research agenda. Journal of Business Research 122: 889–901. https://doi.org/10.1016/j.jbusres.2019.09.022.

Vial, G. 2019. Understanding digital transformation: A review and a research agenda. The Journal of Strategic Information Systems. https://doi.org/10.1016/j.jsis.2019.01.003.

Volberda, H., S. Khanagha, C.B. Fuller, O. Mihalache, and J. Birkinshaw. 2021. Strategizing in a digital world: Overcoming cognitive barriers, reconfiguring routines and introducing new organizational forms. Long Range Planning 54 (5): 102110. https://doi.org/10.1016/j.lrp.2021.102110.

Wodzicki, M., D. Majewski, and M. MacRae. 2020. Digital Banking Maturity 2020. Deloitte Digital. https://www2.deloitte.com/gr/en/pages/financial-services/Digital-Banking-Maturity-Report2020.html

Yin, R.K. 2013. Validity and generalization in future case study evaluations. Journal of Evaluation 19 (3): 321–332. https://doi.org/10.1177/1356389013497081.

Zachariadis, M., and P. Ozcan. 2017. The API economy and digital transformation in financial services: The case of open banking. SWIFT Institute Working Paper No. 2016-001. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2975199

Zhang, H., J. Jin, S. Li, and Y. Zhang. 2023. Digital transformation of incumbent firms from the perspective of portfolios of innovation. Technology in Society 72: 102149. https://doi.org/10.1016/j.techsoc.2022.102149.

Zhou, M., D. Dan Geng, V. Abhishek, and B. Li. 2020. When the bank comes to you: Branch network and customer omnichannel banking behaviour. Information Systems Research 31 (1): 176–197. https://doi.org/10.1287/isre.2019.0880.

Funding

Open access funding provided by HEAL-Link Greece.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

On behalf of all authors, the corresponding author states that there is no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Papathomas, A., Konteos, G. Financial institutions digital transformation: the stages of the journey and business metrics to follow. J Financ Serv Mark 29, 590–606 (2024). https://doi.org/10.1057/s41264-023-00223-x

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1057/s41264-023-00223-x