Abstract

We study how receiving credit from a social bank (Banca Prossima), created in 2008, has affected the economic performance of social enterprises in Italy in the following years. Social enterprises are key providers of welfare services in the country, but due to their legal status as not-for-profit organizations they have difficulty raising capital. Consequently, their growth is often very slow. Credit could replace capital, but not-for-profit organizations are often subject to credit constraints. Moreover, given that they cannot choose the optimal combination of credit and capital, the effect of credit on the economic performance of social enterprises is far from clear. We use a proprietary data set and a difference-in-differences approach to compare social enterprises that received credit from the social bank and those that did not receive it. The results suggest that receivers significantly increase their production, fixed assets, properties, and employment when they have access to new credit. The results are robust to several tests and an alternative identification strategy that combines matching and difference-in-differences methods.

Similar content being viewed by others

1 Introduction

In many countries, social enterprises (SEs)—organizations that pursue social as well as economic aims—are important private providers of welfare services, which also act in the related areas of urban regeneration, long-term unemployment reduction, and community development. Several of these firms—such as the Italian social cooperatives (SCs)—are not-for-profit organizations, which means that they pursue a social mission and cannot distribute surpluses to managers and employees.

Despite having grown in number, SEs struggle to fully meet the increasing demand for services. This could depend on the difficulties in raising new capital that they share with most not-for-profit organizations. As a result of these difficulties, most SEs can only rely on profits to finance their growth, which is often a slow process.

Could SEs count on credit to overcome their problems in raising capital? While this is possible in theory, in practice the credit markets are characterized by information asymmetries that banks overcome asking perspective borrowers for guarantees and collaterals. Unfortunately, due to their legal status, SEs often lack the collateral required by banks. Thus, these firms are frequently subject to credit rationing.

It should also be noted that a larger supply of credit is not necessarily beneficial for SEs. In fact, being unable to raise risk capital, SEs could rely too much on debt, increasing their total costs of capital and therefore jeopardizing their own economic stability.

Whether the positive or possible negative effects of credit prevail for SEs is an empirical question, although the literature in this field is very scarce. In this paper, we try to fill this gap in the literature analyzing the effect of a positive credit supply shock provided by the establishment in 2008 of a new Italian bank (Banca Prossima, hereafter BP)—specializing in SEs and not-for-profit firms—on the economic performance of SCs, the most common form of SE in Italy.

To estimate the impact of the new credit provided by BP, we create a longitudinal data set (spanning from 2004 through 2015) by merging confidential data provided by BP with publicly available balance sheet data of SCs in Italy. To address the possible issue of endogeneity (when credit decisions are based on the performance of SCs) and identify the effect of having access to new credit, we first employ a difference-in-differences (fixed-effect) approach by exploiting the variation in access to BP credit across time and SCs. Our main findings indicate that on average SCs with access to the new credit from this specialized bank (receivers) increase their relative production level (10 percentage points), fixed assets (FA) (20 percentage points), property, plant, and equipment (PPE) level (27 percentage points), and employment (10 percentage points) compared to non-receivers. We also show that the effects on FA and PPE come from long-term credit and persist during the post-credit period.

We perform several placebo tests to check the validity of our identification strategy. First, we investigate whether receivers and non-receivers showed different trends (as far as the main outcome variables are concerned) before credit was given. This investigation is conducted year-by-year in an event-study specification. We also control for the total debts of SCs (excluding the credit from BP) as well as other key observable time-varying indicators included in our dataset. We do not observe statistically significant differential trends prior to receiving credit from BP. This is not only true for the years prior to the foundation of BP (from 2004 to 2007) but also thereafter (from 2008 to 2012Footnote 1).

Second, to better deal with the endogeneity concern, we use an alternative identification strategy. A recent study by Degryse et al. (2019) discusses and highlights the importance of controlling for location, industry, size, and time effects to identify the effects of credit supply shocks. Therefore, we combine a difference-in-differences approach with a matching procedure. We match receivers and non-receivers adopting a propensity score matching approach within homogeneous groups defined by the SCs’ area (macro regions) and sector of activities, based on data measured right before receivers had access to credit from BP. Our econometric specification includes social cooperative and time fixed effects, and we also control for the time-varying performance indicators and the distance (over time) from the moment that SCs receive credit from BP. This setup enables us to estimate dynamic treatment effects while allowing for heterogeneity in treatment intensity (the length of treatment). Our results show that the parallel trend assumption also holds for this matched sample, and that the receivers start increasing their production, fixed assets, and PPE after obtaining credit from BP compared to the matched SCs. Taken together with the fact that very few financial tools are available to SCs in Italy (see Becchetti et al. 2011), our flexible and rich econometric models is a possible indicator of the causal effect of having access to credit from BP.

Our contribution to the literature is twofold. First, we provide—for the first time, to the best of our knowledge—evidence on the possible positive causal link between access to credit and the economic performance of not-for-profit SCs, analyzing both short- and long-term effects. Our findings complement the existing studies with rigorous empirical evidence about the potential effect of providing SCs with more credit. This result is quite relevant given that the empirical evidence on the effects of relaxing credit constraints on not-for-profit SEs is very scarce, and the theoretical reasons could lead to both positive and negative effects.

Second, our findings have important policy implications. In fact, Western public welfare systems are struggling to respond to the increasing demand for social services from the rising elderly population, the growing number of immigrants, and people affected by the recent economic and financial crisis. SEs represent one of the most effective solutions to these emerging needs, but they rarely have access to capital, credit, or financial instruments. SEs (and SCs in particular) often rely on government subsidies and grants, but the literature about the effects of government subsidies on the growth of some industries shows mixed evidence (Criscuolo et al. 2019). Therefore, our findings might hold interest to policy-makers. In fact, giving SEs better access to credit may favor their growth and could directly translate into help for individuals in need.

The remainder of this paper is organized as follows. We briefly refer to the relevant literature in Sect. 2 and depict BP in Sect. 3. In Sect. 4, we describe our data sets, the variables that we use for our analysis as well as our main econometric models. In Sect. 5, we present our results and describe the heterogeneous effects of our analyses. In Sect. 6, we test alternative identification strategies. Finally, in Sect. 7, we draw some policy conclusions.

2 Relevant Literature

Several studies show the role of SEs in producing social services (Thomas 2004; Teasdale 2011; Shaw and de Bruin 2013), increasing social cohesion (Dow 2003; Stiglitz 2009; Birchall 2010) as well as fostering economic growth, nurturing human and social capital (Bahmani et al. 2012) along with trust (Sabatini et al. 2014). In Italy, most SEs take the legal form of a social cooperative (SC) and operate in two main fields: “type-A” SCs provide education, health, and social services, while “type-B” SCs work in various sectors of the economy with the specific goal of offering at least 30% of their jobs to disadvantaged individuals (i.e., disabled people, ex-prisoners, etc.) (Thomas 2004). The number of Italian SCs constantly has increased over time, from approximately 2000 at the beginning of the 1990s to nearly 16000 in 2015 (Istat 2017). In 2011, the total value of their production was about €10.1 billion, and they employed more than 513,052 people (Istat 2014). While Italy boasts the largest number of SCs in Europe, these organizations also exist in many Western countries (European Commission 2015).

Despite their growth, SCs struggle to fully satisfy the increasing demand for their services. As suggested by Hansmann (1996) and Lumpkin et al. (2013), the gap may be a product of the difficulties that SCs experience in raising the necessary capital to expand their services. In fact, prospective investors do not have the right incentives to capitalize SCs given that these organizations cannot distribute profits and are governed by their employees, which means that investors do not have a say in many relevant decisions. Therefore, SCs rely on their profits to fund their growth, which is often a slow process.

SCs could count on credit to overcome their difficulties in raising capital. A vast body of literature—mostly related to standard business companies—shows that access to credit is beneficial to firms and crucial to their development. On the contrary, contractions in credit supply substantially harm firms, thus increasing their likelihood of failing (Franklin et al. 2020).

However, the effects of larger credit supply on the performance of SCs could be uncertain. In fact, given their difficulties in raising capital they “cannot choose the combination of debt and equity that would minimize the costs of capital” (Auteri 2003, p. 177). A higher-than-optimal level of credit would therefore lead to higher capital costs, and this could jeopardize the economic stability of SCs. In addition, in SCs the funds used to pay interests and repay principals are often government subsidies or contracts and private donations rather than market sales. These sources can set limits on how funds can be used, thus reducing the chances of repaying debts and increasing the likelihood of default. Whether the positive or possible negative effects of credit prevail for SCs is an empirical question, although literature in this field is scarce.

Moreover, when they apply for credit, SCs are touched by the information asymmetries that characterize credit markets. In fact, to overcome their information disadvantage, banks regularly ask their borrowers for collaterals. Due to their modest capitalization—a characteristic that they share with many small and medium-sized enterprises (SMEs)—SCs often do not have the collateral required by banks as a guarantee. Given that most loans to firms are collateralized (Berger and Udell 1990; Black et al. 1996; Coco 2000), SCs could therefore be subject to different kinds of credit rationing (Jaffee and Russell 1976; Stiglitz and Weiss 1981) and credit constraints.

Credit constraints have been largely acknowledged by economists and policy-makers (Banerjee and Duflo 2014). Limits to credit access are particularly relevant—but not limited—to SMEs in developing countries (de Sousa and Ottaviano 2018), as well as firms operating in disadvantaged regions of developed economies (Criscuolo et al. 2019). Credit constraints slow down the growth of these firms. However, credit constraints also affect not-for-profit firms and SEs, organizations that pursue social as well as economic aims (Thomas 2004; Teasdale 2011; Shaw and de Bruin 2013).

Considering business firms, the creation of private and public credit guarantees for SMEs has been a common solution to tackle the problem of inadequate collaterals. Research has shown that public credit guarantees could overcome the lack of collaterals, therefore giving better access to credit. Subsequently, access to credit facilitated by public guarantees improves the overall economic performance of SMEs (Hancock and Wilcox 1998; Kang and Heshmati 2008; Zecchini and Ventura 2009; Garcia-Tabuenca and Crespo-Espert 2010; Arráiz et al. 2014). On the contrary, Dvouletý et al. (2018) do not find any effect of government-supported credit guarantees on SMEs.

However, public credit guarantees are quite uncommon in the field of SEs, at least in Italy, and this exposes these firms to the discretionary decisions of the banks, particular during funding crisis. In fact, as shown by De Jonghe et al. (2020), when facing a negative funding shock, banks reallocate credit within their loan portfolio to sectors in which they have a high market share, in which they are more specialized, and to low-risk firms. None of these features fit the Italian SCs.

3 The Role of Ethical Banks and Banca Prossima

SCs face challenges in obtaining credit under traditional bank rules. However, this does not mean that they are bad debtors; rather, it may mean that the banking system has not yet developed adequate screening models or acquired adequate knowledge of the SCs’ default probability through relationship lending (Berger and Udell 2006; Peltoniemi 2007; Luppi et al. 2008; Moro et al. 2014; Banerjee et al. 2017) to fit the unique circumstances of these firms. Therefore, the development of new models that could reduce credit rationing may strongly benefit a sector that is crucial to the provision of welfare services. Social and ethical banks (institutions committed to financing ethical projects and SEs) may represent a solution to the problem of credit access for SEs (Benedikter 2011; Weber and Remer 2011). The literature (Becchetti and Garcia 2011; Cornée and Szafarz 2013) shows that when lending to SEs, these banks require lower levels of financial or real collateral than traditional banks, and instead they rely on informal collateral or relationship lending. Consequently, “ethical banks increase social welfare because the matching of ethical lenders with motivated borrowers reduces the frictions caused by the agency issue” (Barigozzi and Tedeschi 2015).

In Italy, only one such institution (Banca Etica) existed when Banca Prossima started its activities in 2008. This new bank was created by Intesasanpaolo—the main Italian banking group—along with three of the largest philanthropic foundations in the country. BP is dedicated exclusively to providing loans to not-for-profit organizations, facilitating their access to the credit market.Footnote 2

To better pursue its goals, BP has developed two complementary tools. The first one is a proprietary rating model that screens organizations to determine which of them could safely be granted credit by BP, even when the organization lacks the collateral traditionally requested by banks (Faletti 2011). Specifically fit to not-for-profit organizations and considering the peculiar characteristics of these enterprises (Scarlata et al. 2016), the model offers information not only on the financial but also the socio-environmental characteristics of credit applicants, thus helping to overcome information asymmetries (Moro et al. 2014). The rating model aims to supplement traditional balance sheet information used to rate credit merit (Luppi et al. 2008) with two other sources of data: (1) quantitative information from a careful analysis of the firm’s current activities; and (2) qualitative data from questionnaires administered to the organization applying for credit, which is meant to appraise its specific features, such as its intangible assets (e.g. support from the community and relationships with local administrations) (Moro et al 2014). The quantitative and qualitative information is then reconciled into a single score determining the creditworthiness of the organization. This rating model should give a more precise representation of a not-for-profit firm capacity to repay its debts compared to the models generally used for SMEs, therefore reducing the information gap that limits access to credit.

BP’s second tool is an internal reserve and guarantee fund, the “Fund for Development and For Social Enterprise”, fed annually with 50% of the profits that BP’s owners decided to give up permanently. The aim of this fund is to protect and guarantee BP’s assets against possible losses deriving from credit given to socially deserving but risky organizations that would otherwise be denied credit by traditional banks. This fund has a role similar to the one played by public credit guarantees.

The two tools work together. BP rates the merit of each not-for-profit organization that applies for credit according to its rating model. If the score is close to the credit threshold but not sufficiently high to obtain credit, and the project is relevant and socially deserving, bank officials can apply for the internal fund’s guarantee. Should the debtor not be able to repay its loan, the fund would cover the loss. At the end of 2017, the total size of the fund was about €34 million. In 2008–2017, the fund guaranteed about 1000 credit positions, but only €120000 in guarantees were enforced during the entire period.

The two mechanisms should enable the bank to grant credit to deserving organizations lacking adequate collaterals that would otherwise suffer from credit rationing. Access to credit may then increase the social and economic performance of SEs by increasing their production levels and strengthening their capital structure, although it may also place their financial structure in jeopardy. With our analysis, we try to assess whether the positive effect of obtaining credit—supporting the firm growth—prevails over the possible negative effect of increasing financial costs, thus placing the very existence of the firm at risk.

4 Data and Model

4.1 Sample Structure

Our estimation sample is a combination of two different data sources. The first one is a confidential data set provided by BP that includes the amount of short- or long-term credit given to SCs (identified by their fiscal code) in 2008–2015. Information included in this data set (never used in previous research) is quite relevant because BP is the leader of this market segment. The second data set comes from Aida (Analisi informatizzata delle aziende di capitale italiane), which is produced by Bureau van Dijk and includes the balance sheets of many Italian SCs identified by their fiscal code for 2004–2015.

We merged the two data sets (matching the unique fiscal code of the SCs) and obtained a balanced sample for 2006–2015. Moreover, we were able to obtain and analyze further information for a smaller sample of SCs for 2004 and 2005. Overall, we have an unbalanced sample of 56355 cooperative-year observations for 2004–2015. Of the 7567 SCs in the sample, 883 received credit from BP at least once (receivers), while the remaining 6684 SCs never received credit from BP (non-receivers).Footnote 3

Our sample represents about 68% of all Italian SCs in 2008 (Istat 2014), which was when BP started. The share decreases in the following years because we kept our sample constant even though new SCs entered the market.Footnote 4 Overall, our sample fairly represents the population of SCs in Italy. We were unable to identify about 50% of SCs that received credit from BP in the Aida data set. The missing SCs are most likely new organizations that entered the market in recent years and therefore are not yet represented in the Aida data set. Although the missing data for these SCs might be considered a problem, including the data would have damaged our identification strategy because the availability of new credit from BP could have increased the incentives of these cooperatives to enter the market.Footnote 5

The Aida data set lacks certain balance sheet information for some SCs in different years. To minimize the impact of this problem, we selected variables that are both closely related to the performances of SCs and mostly observed in the data. Moreover, in the sensitivity analysis section in Online Appendix A, we provide results from a smaller sample with no missing variables.

4.2 Variables and Descriptive Statistics

We focus on four main outcomes variables that are strictly related to the performances of SCs: (1) property, plants, and equipment (PPE) (Immobilizzazioni materiali), which represents the total value of the SC’s equipment, buildings, vehicles and other tangible assets; (2) fixed assets (FA) (Immobilizzazioni materiali e immateriali), which represents the total value of PPE plus goodwill, intangibles and investments; (3) capital (Patrimonio netto), which represents the owner’s equity, reserves, and retained earnings, and (4) production (Valore della produzione), which represents the total value of an SC production. PPE and FA are good proxies for the effect of long-term investments, while production and capital are more relevant to the current activities and financial status of SCs and they are mostly influenced by short-term credit. We will not refer to any notion related to earned income or profits of SCs. In fact, SCs tend to show little profit in their income statements given that they cannot distribute profits to their members owing to their not-for-profit status.

Of course, changes in our outcome variables may depend on several factors besides receiving credit from BP. Therefore, to isolate the effect of obtaining credit from BP, we include control variables such as total assets,Footnote 6 debts (which includes credit from banks other than BP),Footnote 7 and receivablesFootnote 8 in our estimation process. In some cases, we also use production and PPE as control variables. We take the natural logarithm of all variables to work with distributions that are close to normal.Footnote 9

In Table 1, we show the average amount of short-term credit (less than 18 months, column 1), long-term credit (more than 18 months, column 2), and total credit (column 3) given by BP to the SCs included in our sample, as well as the total number of credit positions in different years. BP’s number of credit positions grows from 2008 to 2013, but it decreases thereafter. Moreover, in column 4 of the same table we show the average share of debt to BP among the total debt of the SCs that received credit from BP and are included in our sample. This share is around 47% for 2008–2015, which hints that debt to BP represents a large share of the average total debt of these cooperatives. This fact supports the claim that SCs have limited access to debt instruments in the market.

In Tables 2 and 3, we show descriptive statistics of the outcome and main control variables for receivers and non-receivers, respectively. In Table 2, we consider the whole set of receivers and statistics are calculated regardless of the receivers having obtained credit in that specific year. Comparing the tables, we note that on average receivers perform better than non-receivers for all variables. This is unsurprising as banks are more willing to give credit to firms that are more likely to repay the loan. This consideration could cloud our identification strategy (which will be presented in detail in the next sections), given that we want to explore the causal link between receiving credit from BP and the market performance of cooperatives, which in theory requires an exogenous credit assignment across cooperatives.

To tackle this problem, we use a difference-in-differences approach and investigate the outcome variables of receivers before they obtained credit from BP, showing that their relative performance was not improving. Moreover, we complement our main analysis with a matching approach (based both on “propensity score” and “exact matching” procedures) that further tackles the problem of endogeneity embedded in the credit procedures.

4.3 Baseline Difference-in-Differences Approach

Our baseline model is as follows:

where t = 2004, 2005, … 2015; Yct represents the outcome of interest for SC c in year t; ac captures unobserved-but-fixed cooperative effects; λt captures time fixed effects; Γrt is a year-specific region fixed effect that controls—non-parametrically—the trends across the Italian regions; and Dct is a dummy variable equal to 1 if SC c receives credit from BP in year t, and 0 otherwise.Footnote 10 As the new bank entered the market in 2008, Dct can equal 1 for 2008–2015. We choose to treat Dct as a dummy rather than a continuous variable to avoid working with a left censored variable.Footnote 11Pct is a dummy variable equal to 1 if SC c had access to credit in the past but not in year t. By including Pct in the right-hand side of the equation, we consider the “post-credit” period because having access to credit might have long-term effects on the performance of an SC. Pct can therefore be equal to 1 for 2009–2015. Xct is the vector of covariates used to control certain observable characteristics of SCs (which includes the total amount of credit borrowed by banks other than BP), and ϵct captures the unobservables of SC c at time t.

Our analysis focuses on parameters δcredit and γpost. We estimate a cooperative fixed effect model with standard errors clustered at the SC level, thus allowing serial correlation across time in unobservables of SCs. We replicate Eq. (1) for each outcome of interest.

Based on a cooperative fixed effect model, our identification strategy is equivalent to a difference-in-differences estimation where some SCs never received credit from BP (the control group) while other SCs received credit in certain years after 2008 (the treatment group). The main assumption of our identification strategy is that the outcome variables of the treatment and control groups would have followed common trends in the absence of credit from BP. Therefore, if SCs improve their performance to obtain credit by the bank, our estimates of δcredit will be biased due to self-selection into treatment. We address this issue in the sensitivity analysis section of the paper—available in Online Appendix A—where we extend our main econometric specification and check for any statistically significant difference in the performance of receivers compared to non-receivers before they obtain credit.

In Eq. (2), we provide insights into the differential effect of short- and long-term credit on the outcomes of interest. For this purpose, we replace the dummy variables Dct and Pct included in Eq. (1) with \({D}_{ct}^{long}\), \({D}_{ct}^{short}\) and \({P}_{ct}^{long}\), \({P}_{ct}^{short}\) respectively:

where \({D}_{ct}^{long}\) is equal to 1 if SC c receives long-term credit in year t and 0 otherwise; and \({D}_{ct}^{short}\) is equal to 1 if SC c receives short-term credit in year t and 0 otherwise. Moreover, \({P}_{ct}^{long}\) is equal to 1 for SC c during the post-long-term credit years, while \({P}_{ct}^{short}\) is equal to 1 during the post-short-term credit years. Other variables have the same meaning as in Eq. (1).

5 Results and Heterogeneous Effects

We estimate Eqs. (1) and (2) for our main outcome variables: PPE, FA, production, and capital, all of which are alternative proxies for the performances of SCs. In addition, we also measure changes in employment even though our dataset shows several missing values. We report the main results on these outcomes in Table 4.Footnote 12

5.1 Main Results

Our estimates show that credit availability increased the PPE of receivers by (a statistically significant) 27 percentage points (p.p.) compared to non-receivers (Table 4, column (1)). Moreover, this increase is persistent for each of the following years, as shown by the positive and statistically significant level of the γpost coefficient (about 20 p.p.). This result is reasonable, given that buildings, land, and machinery are long-term resources that remain on the balance sheet of the investor over time. Therefore, our outcome shows that credit available in the market (other than BP credit) does not allow non-receivers to invest in PPE as much compared to receivers. When we consider the length of credit (column (2)), we see that the overall effect is mostly driven by long-term credit. We see an increase of 40 p.p. when SCs have access to long-term credit and an increase of 15 p.p. for short-term credit.

The results for FA (Table 4, columns (3) and (4)) are in line with the previous ones. In fact, receivers increase their FA when they obtain credit and in the following years by a statistically significant 20 p.p. and 14 p.p., respectively, compared to non-receivers (column (3)). We do not see any differential effects determined by short- or long-term credit: in fact, both types of credits increase FA about 15 p.p. on average.

Credit by BP also displays its positive effect on production (Table 4, columns (5) and (6)), with a statistically significant 8 p.p. increase for receivers over non-receivers, although its effect is not persistent over time. Only short-term credit is positively linked to an increase in production (column 6), but the effect vanishes during the post-credit period, suggesting that the production levels strictly depend on the excess cash flows provided by BP.

The effect of BP credit on the amount capital of SCs is less clear: in fact, the coefficients reported in Table 4 (columns (7) and (8)) are very close to zero and not statistically significant.Footnote 13 The weak effect of credit on the amount of capital of SCs may depend on the not-for-profit nature of these firms, which do not maximize their profits and therefore do not increase their capital.

Finally, Table 4 (columns (9) and (10)) shows the effect of BP credit on the employment level of SCs. As previously mentioned, given that the employment variable is often missing in our data set, we conduct our analysis on a smaller sample.Footnote 14 The results suggest that the employment of treated SCs increases by 10 p.p. when they have access to credit and 7 p.p. in post-credit years. The reduction in size of the coefficient during the post-credit years can be explained by project-based hiring for activities that do not last over time. We also estimate the effect on the log production per employee to understand if the productivity of treated SCs also increases. We do not find any impact on this variable.Footnote 15 This is unsurprising considering the similar effects we see for production and employment.

Taken together, our results show that SCs invest in fixed assets and PPE by using long-term credit. Moreover, SCs mostly use short-term credit to increase the services they provide, thus explaining the increase in their production and employment levels. However, changes in production and employment are very similar, whereby the productivity of the SCs that receive credit does not change.

5.2 Heterogeneous Effects

We investigated the effects of BP credit on SCs acting in different geographic areas of the country and operating in different sectors (using the SC type as a proxy). To explore the effects of credit across areas, we generated five area dummy variables: dNW (Northwest), dNE (Northeast), dC (Center), dIS (Isles) and dS (South). Considering the Northwest area as a baseline, in Eq. (3) we interacted the new area dummies with the dummies included in our main specification, Dct and Pct:

where t = 2004, 2007, …2015, while Dct and Pct are the dummy variables described in Eq. (1). Estimates of \({\delta }_{credit}^{NW}\) and \({\gamma }_{post}^{NW}\) will give us, respectively, the effect of having access to credit and the effect of the post-credit period on the performance of SCs operating in the Northwest, while all of the interaction terms of Eq. (3) will show the heterogeneous effects for SCs operating in other areas of the country with respect to SCs located in the Northwest. All of the other variables have the meaning reported in Eq. (1).

The baseline estimates for receivers located in the Northwest with respect to non-receivers (Table 5) are similar to previous findings. Moreover, the results do not show major differences across areas, with a couple of notable exceptions. In columns 2 and 4, we show that receivers operating in the Isles significantly increase their production (15.9 p.p.) and capital (21.7 p.p.) over non-receivers during the credit years when compared to SCs in the Northwest. Moreover, while SCs in the Northwest significantly reduced (22.3 p.p.) their production during the post-credit period, this is not true for the SCs located in the Isles and the South. On the contrary, these SCs significantly increased their production levels by 41.4 p.p. and 32 p.p., respectively, with respect to the cooperatives in the Northwest. Given that SCs located in the southern part of the country and the Isles are generally smaller and weaker than those located elsewhere, the credit from BP appears to be particularly beneficial for the organizations that are most in need.

We also examine the effects of credit across the three types of cooperatives regulated by Law 381/1991 (type-A, type-B and mixed SCs). Note that type represents a good proxy of an SC’s activity sector. In fact, while type-A SCs mainly operate in the service sector (education, social services, and health services), type-B SCs are largely active in manufacturing or agriculture. In Eq. (4), we introduce interaction terms for the type of cooperatives identified by specific dummy variables (dA for type-A, dB for type-B and dAB for mixed SC):

where \({\delta }_{credit}^{A}\) and \({\gamma }_{post}^{A}\) show, respectively, the effect of receiving credit and having received credit for type-A SCs. On the other hand, the interaction terms show the effects on type-B and mixed SCs with respect to the effects on type-A SCs.

Table 6 shows the results. The effects on type-A SCs with respect to non-receivers—which are the baseline estimates in Eq. (4)—are like those obtain for the whole sample in Eq. (1). As for the heterogeneous effects, mixed SCs increase their production by about 22 p.p. more than the type-A SCs once they have access to credit. Moreover, type-B SCs increase their PPE 13 p.p. less than type-A cooperatives during the credit years. On the other hand, they significantly increase (13 p.p.) their capital compared to type-A cooperatives.

6 Matching and Dynamic Treatment

To further test the robustness of our results and control the selection bias that is implicit in the credit process, we introduce an alternative identification strategy that integrates a matching approach into our difference-in-differences analysis.

6.1 Matching Procedure

To match receivers to non-receivers, we use the main data set of Aida for 2006–2015. We only consider SCs with no missing values in FA, production, and PPE, credits, receivables, and total assets throughout the entire period. Moreover, we only select the SCs for which ten consecutive years of observation are available (i.e. fully balanced panel).

As a first step in the matching procedure, we find (in the group of non-receivers) matches for receivers based on two main characteristics: macro-area of establishment (Northwest, Northeast, Center, South, and Islands) and sector of activity (using the first two digits of the NACE taxonomy). If a receiver has no match, we drop it from the sample. In a second step, we calculate propensity scores for receivers and non-receivers running a logit regression on the probability of being a receiver a year before receivers obtain credit from BP for the first time. Given that the latter year can span from 2007 to 2012 in our data, we replicate the same procedure in each of those years. The logit regressions include the covariates of capital, credits, receivables, and total assets. Based on the estimated propensity scores and setting the caliper to 0.05, we select—if available—two nearest neighbors for each receiver. The final matched sample includes 314 receivers and 438 unique matched non-receivers. We allow non-receivers to match multiple receivers in different years (i.e. matching with replacement). Therefore, the sample includes a total of 569 non-unique matched non-receivers. Finally, we assign placebo “relative years” (years to, or since, obtaining credit from BP) to non-receivers based on the years when their counterparts actually received credit from BP.

Considering the data availability (2006–2015) and given that an SC could obtain BP credit for the first time during the period from 2008 to 2013, our matched sample is only fully balanced for the “relative years” from − 2 (2006–2008 = −2) to + 2 (2015–2013 = + 2). Therefore, to avoid major changes in the composition, we restrict our sample to the relative years − 4 to + 6 (while the maximum could be − 7 to + 7).

Table 7 reports the descriptive statistics of the matched sample. Columns (1)–(3) show these statistics for “relative years" − 4 to − 1, before the receivers gained their credit from BP for the first time. Columns (4)–(6) show the same statistics for “relative years” 0 to + 6, after receivers gained their credit from BP. The standardized mean differences of the variables (Std.) before receivers gained credit from BP are all within the range suggested by Imbens and Rubin (2015) for matched samples (smaller than 0.20).Footnote 16 Moreover, as we explain in the next sub-section, our identification strategy controls any differences in variables’ levels between receivers and non-receivers.

6.2 Event-Study Analysis

Working with a matched sample, we can introduce an additional variation into our baseline econometric specification outlined in Eq. (1): distance to treatment. We create “time-distance” dummies representing the number of years to, and since, a receiver obtained credit from BP. The same dummy variables are assigned to non-receiver SCs, based on the receiver to which they are matched. The year before BP gave credit—when the matching occurs—is considered as “time-distance” − 1 and it is used as a baseline in the event-study specification described in Eq. (5), which we estimate as follows:

where Yct is the outcome variable, t = 2006, 2007,..,2015. \({Q}_{ct}^{d}\) are dummy variables that take the value of 1 if SC c is at distance d (in years) from actually (receivers) or potentially (non-receivers) obtaining credit from BP in year t, and 0 otherwise. We interact \({Q}_{ct}^{d}\) with time dummies, λt. These interaction terms control for the time effects in each distance. \(receive{r}_{c}\) is a dummy variable that takes the value of 1 if SC c is in the treatment group, and 0 otherwise; Xct is the vector of observable variables that include total debts (net of BP credit) and receivables as continuous variables, and year-specific sector and macro-region fixed effects; and ac is SC fixed effects. The parameter of interest is φd, which estimates the relative performance of receivers before and after receiving credit from BP. It is worth noting that we only consider the first time that an SC receives credit from, which means that in the final matched sample we do not consider the years following the first allowance of credit to a SC, even if the same SC also receives credit in later years. This aims to isolate the effect of the first access to BP credit. Standard errors are clustered at the SC level.

This flexible econometric specification, similar to the one in Ichino et al. (2017), provides a clear picture for our analysis. First and foremost, matching SCs right before they receive credit from BP (based on sector, macro-area, and performance-related variables) creates a working sample in which receivers and non-receivers are very similar to each other based on characteristics that should be controlled for to identify the causal effect of credit supply shocks (see, e.g. Degryse et al. 2019). Additionally, the inclusion of SC fixed effects controls for the unobservable time-invariant characteristics of SCs, while the inclusion of time fixed effects captures any differences driven by the calendar year. This is important as different SCs received credit from BP for the first time in different years. Moreover, our sample includes SCs that never received credit as a control group (e.g. non-receivers) and we never let the SCs treated in the following years be included in the control group, not even in the years before they are treated. This addresses some of the concerns raised by the recent literature on the estimation of dynamic treatment effects with two-way fixed effects, e.g. no unit receives negative weights in our setup (for a discussion, see De Chaisemartin and D’Haultfoeuille 2020; Goodman-Bacon, 2021).

From a purely theoretical perspective, we are aware that matching and controlling for the “time-distance” to treatment and other relevant characteristics of SCs does not eliminate the endogeneity issue. Nonetheless, the placebo tests (see Online Appendix A) confirm that even after the opening of BP, the SCs that will receive credit in the future do not show differential performance compared to non-receivers. Moreover, thanks to Eq. (5) we can rigorously test this result. We expect the estimates of coefficients φ−2, φ−3, and φ−4, not to be statistically significant, so that our treatment effect would be properly identified under the common trend assumption. Note that our matching procedure does not manipulate the sample selection to generate parallel trends, given that we only matched SCs at the baseline (φ−1).

6.3 Results for the Matched Sample

In this section, we present the results obtained from the matched sample. We highlight the coefficient estimates of φd from Eq. (5) on the PPE, FA, and production variables, respectively, in Figs. 1, 2, and 3. The top panels of each figure plot the unconditional averages of the variables under investigation in the treatment and control groups over the “relative years” to and since receiving credit from BP. We observe no pre-treatment trend in any of the outcomes, given that all coefficient estimates are close to zero and not statistically significant before. Moreover, the descriptive figures in the top panels show parallel trends, reassuring that the non-significant coefficient estimates do not depend on the controls used in the econometric specifications.

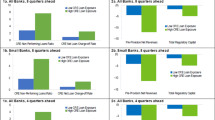

Results on property, plant, equipment (PPE). The panel at the top shows the average level of PPE for receivers (treated) and non-receivers (control) over the “relative years” before and after SCs receive credit from BP. The panel at the bottom reports the estimates of coefficient φd from Eq. (5) with 95% confidence intervals. The regression includes the following variables: SC, distance*time, time-sector, time-area fixed effects, along with total debts and receivables as continuous control variables. The vertical dashed lines represent the year when SCs received credit from BP for the first time. The continuous variables are in their natural logarithm. The sample size is 7490. R-square is 0.90

Results on fixed assets (FA). The panel at the top shows the average level of FA for receivers (treated) and non-receivers (control) over the “relative years” before and after SCs received credit from BP. The panel at the bottom reports the estimates of coefficient φd from Eq. (5) with 95% confidence intervals. The regression includes SC, distance*time, time-sector, time-area fixed effects, along with total debts and receivables as continuous control variables. The continuous variables are in their natural logarithm The vertical dashed lines represent the year when SCs received credit from BP for the first time. The sample size is 7490. R-square is 0.91

Results on production. The panel at the top shows the average level of production for receivers (treated) and non-receivers (control) over the “relative years” before and after SCs received credit from BP. The panel at the bottom reports the estimates of coefficient φd from Eq. (5) with 95% confidence intervals. The regression includes SC, distance*time, time-sector, time-area fixed effects, along with total debts and receivables as continuous control variables. The continuous variables are in their natural logarithm. The vertical dashed lines represent the year when SCs received credit from BP for the first time. The sample size is 7490. R-square is 0.94

As for the results, we observe significant increases in PPE (20 p.p), FA (26 p.p.) and production (5 p.p.) right after receiving credit from BP. Furthermore, we observe that the positive effects gradually increase over the following six consecutive years. The results from the matched sample concerning the average effects of BP credit on the economic performance of SCs are in line with those obtained from the full sample reported in Sect. 5. This reassures that our main findings are not driven by misspecifications.

7 Conclusion

In most Western countries, social enterprises (SEs)—most of them not-for-profit organizations that pursue social and economic aims—are important players in the provision of welfare services, as shown during the recent Covid pandemic. Despite their role and the growth that they have experienced over recent years, these organizations struggle to fully satisfy the increasing demand for their services. As suggested by Hansmann (1996) and Lumpkin et al. (2013), this may depend on the difficulties that SEs experience in raising new capital. Due to their not-for-profit nature, prospective investors do not have any incentives to capitalize SEs. Therefore, many SEs can only rely on profits to fund their growth, which is often a slow process.

SEs could rely on credit to overcome their difficulties in raising capital. Nonetheless, due to their modest capitalization SEs often lack the collateral required by banks as a guarantee. Therefore, owing to the information asymmetries that characterize the credit market, they are subject to credit rationing and constraints. Furthermore, while credit shows a positive effect on the economic performance of business firms, the effects of larger credit supply on SEs could be uncertain because they have difficulties choosing the combination of debt and equity that minimizes the costs of capital. High credit would therefore lead to higher capital costs, and this could jeopardize the economic stability of the SEs.

Therefore, whether the positive effect of obtaining credit—supporting the firm growth—or the negative effect—increasing financial costs, thus placing the very existence of the firm at risk—prevails is a matter of measurement.

Our main findings indicate—with some caution—that obtaining credit from BP has been beneficial for Italian SCs, many of which are subject to credit rationing and generally have access to a limited set of financial instruments. In fact, these firms increased their production level (10 p.p.), fixed assets (20 p.p.), and PPE (27 p.p.) compared to SCs that had no access to the same credit. We also show that the effects on fixed assets and PPE mostly depend on long-term credit, whose effect persists during the post-credit period. As for the capital of SCs, the effect of credit is much weaker and uncertain, which can be explained by the not-for-profit nature of SCs.

Our study has important policy implications given the significant changes in Italian demographics in recent years, such as the increasing elderly population and the influx of immigrants who have increased the demand for social services. SCs operate efficiently in these fields and have high moral incentives in the production of public goods and social services at the community level. Nonetheless, given that their market share remains small, increasing the production levels of SCs can directly translate into help for individuals who need human services.

Moreover, our findings suggest that the credit market has shown some failures that the screening method and the reserve fund adopted by BP helped to mend. In fact, given that our data show that no more than one SC defaulted on its credit payments to BP, credit rationing against SCs was not fully justified. This indicates that the credit rating method created by BP is not only effectively working but is also moving the credit market towards equilibrium.

Data and Material Availability

Data will be made available upon request, except for data coming from Banca Prossima.

Notes

2012 is the last year in our dataset in which we observe SCs in our treatment group that received credit from BP for the first time in the subsequent years.

Banca Prossima was then merged into Intesasanpaolo in 2019.

Of course, non-receivers may have received credit from banks other than BP. We do not have detailed information about credit from other banks, but we control for the total amount of credit received by SCs, a variable that includes credit from banks.

The share was 65% in 2009, 62% in 2010, and 60% in 2011.

Moreover, we observe that all of the SCs that received credit from BP and were tracked in the Aida data set (and are therefore included in our sample) were still in business at the end of our observation period. Therefore, we can say that our analysis is not plagued by the so-called “survivorship bias.”.

Total assets (TA) (Totale attivo) represents the sum of current and non-current assets.

We subtract the amount of credit borrowed by BP from the debts of receivers.

Total receivables (TR) (Totale crediti) represents the sum of accounts and notes receivable.

This decision does not significantly alter our results and the results obtained from the original values of variables are available on request.

Since our sample comprises non-receivers and receivers, and our treatment is at the SC level, the inclusion of time and SC fixed effects into our specification makes Dct equivalent to the interaction term, say, POST*TREATED in a diff-in-diff specification in which treatment is at the aggregate level.

The results do not change when Dct is defined as a continuous variable.

In Table 4, all estimates come from models that include the full set of control variables as well as year-specific region fixed effects. Nevertheless, in Online Appendix B we report our results for each outcome with and without control variables.

In Table 13 (included in Online Appendix B), we show a positive (about 20 p.p.) and statistically significant increase of the amount of capital of receivers over non-receivers, mostly driven by short-term credit (column (3)). Nonetheless, the effect disappears when the control variables are considered.

We replicated the previous analyses (for PPE, fixed assets, production, and capital) with the smaller sample that we used for estimating the effects on employment. The results are in line with those presented so far.

We do not report this result in Table 4. The estimated coefficient for productivity (log(production/employee)) is 0.035 with a p-value of .163.

See also Britto et al. (2021) for a similar use of this technique.

References

Arráiz I, Meléndez M, Stucchi R (2014) Partial credit guarantees and firm performance: evidence from Colombia. Small Bus Econ 43(3):711–724

Auteri M (2003) The entrepreneurial establishment of a nonprofit organization. Public Organ Rev 3(2):171–189

Bahmani S, Galindo MA, Méndez MT (2012) Non-profit organizations, entrepreneurship, social capital and economic growth. Small Bus Econ 38(3):271–281

Banerjee AV, Duflo E (2014) Do firms want to borrow more? Testing credit constraints using a directed lending program. Rev Econ Stud 81(2):572–607

Banerjee R, Gambacorta L, Sette E (2017) The real effects of relationship lending. Bank of Italy Temi di Discussione (Working Paper) No 1133

Barigozzi F, Tedeschi P (2015) Credit markets with ethical banks and motivated borrowers. Rev Financ 19:1281–1313

Becchetti L, Garcia MM (2011) Informal collateral and default risk: do ‘Grameen-like’ banks work in high-income countries? Appl Financ Econ 21:931–947

Becchetti L, Garcia MM, Trovato G (2011) Credit rationing and credit view: empirical evidence from an ethical bank in Italy. J Money Credit Bank 43:1217–1245

Benedikter R (2011) Social banking and social finance: answers to the economic crises. Springer, New York

Berger AN, Udell GF (1990) Collateral, loan quality, and bank risk. J Monet Econ 25:24–42

Berger AN, Udell GF (2006) A more complete conceptual framework for SME finance. J Bank Financ 30(11):2945–2966

Birchall J (2010) People-centered business: co-operatives, mutuals and the idea of membership. Palgrave Macmillan, London

Black J, de Meza D, Jeffreys D (1996) House prices, the supply of collateral and the entreprise economy. Econ J 106:60–75

Borzaga C, Fazzi L (2014) Civil society, third sector, and healthcare: the case of social cooperatives in Italy. Soc Sci Med 123:234–241

Britto DCG, Pinotti P, Sampaio B (2021) The effect of job loss and unemployment insurance on crime in Brazil. Econometrica (forthcoming)

Chapelle K (2010) Non-profit and for-profit entrepreneurship: a trade-off under liquidity constraint. Int Entrepreneurial Manage J 6:55–80

Coco G (2000) On the use of collateral. J Econ Surv 14:191–214

Cornée S, Szafarz A (2013) Vive la différence: social banks and reciprocity in the credit markets. J Bus Ethics 125:361–380

Criscuolo C, Martin R, Overman HG, Van Reenen J (2019) Some causal effects of an industrial policy. Am Econ Rev 109(1):48–85

De Chaisemartin C, Xavier H (2020) Two-way fixed effects estimators with heterogeneous treatment effects. Am Econ Rev 110(9):2964–2996

De Jonghe O, Dewachter H, Mulier K, Ongena S, Schepens G (2020) Some borrowers are more equal than others: bank funding shocks and credit reallocation. Rev Financ 24(1):1–43

de Sousa FL, Ottaviano GI (2018) Relaxing credit constraints in emerging economies: the impact of public loans on the productivity of Brazilian manufacturers. Int Econ 154:23–47

Degryse H, De Jonghe O, Jakovljević S, Mulier K, Schepens G (2019) Identifying credit supply shocks with bank-firm data: methods and applications. J Financ Intermed 40:100813

Dow GK (2003) Governing the firm: workers’ control in theory and practice. Cambridge University Press, Cambridge

Dvouletý O, Čadil J, Mirošník K (2018) Do firms supported by credit guarantee schemes report better financial results 2 years after the end of intervention? BE J Econ Anal Policy 19:1

European Commission (2015) Map of social enterprises and their eco-systems in Europe. Synthesis Report, Brussels

Faletti E (2011) Un modello al servizio del sociale: metodologia di sviluppo di un modello di rating dedicato alla valutazione delle imprese sociali, fondazioni ed enti di culto. Paper presented at the Fifth edition of the Colloqui sull’impresa sociale, Trento, Italy.

Franklin J, Rostom M, Thwaites G (2020) The banks that said no: the impact of credit supply on productivity and wages. J Financ Serv Res 57:149–179

Garcia-Tabuenca A, Crespo-Espert JL (2010) Credit guarantees and SME efficiency. Small Bus Econ 35(1):113–128

Goodman-Bacon A (2021) Difference-in-differences with variation in treatment timing. J Econom 225(2):254–277

Hancock D, Wilcox JA (1998) The credit crunch and the availability of credit to small business. J Bank Finance 22(6–8):983–1014

Hansmann H (1986) The role of nonprofit organisation. In: Rose-Ackerman A (ed) The economics of nonprofit institutions. Oxford University Press, New York, pp 57–93

Hansmann H (1996) Too many nonprofit organizations? Problems of entry and exit. Le Organizzazioni Senza Fini di Lucro. Milano, Giuffrè

Ichino A, Schwerdt G, Winter-Ebmer R, Zweimüller J (2017) Too old to work, too young to retire? J Econ Ageing 9:14–29

Imbens GW, Rubin DB (2015) Causal inference in statistics, social, and biomedical sciences. Cambridge University Press, Cambridge

Istat (2014) Il Profilo delle Istituzioni Nonprofit alla Luce dell’ultimo Censimento. ISTAT, Rome

Istat (2017) Censimento Permanente delle Istituzioni Nonprofit. Primi risultati. ISTAT, Rome

Jaffee DM, Russell T (1976) Imperfect information, uncertainty, and credit rationing. Q J Econ 90:651–666

Kang JW, Heshmati A (2008) Effect of credit guarantee policy on survival and performance of SMEs in Republic of Korea. Small Bus Econ 31(4):445–462

Lodigiani R, Pesenti L (2014) Public resources retrenchment and social welfare innovation in Italy: welfare cultures and the subsidiarity principle in times of crisis. J Contemp Eur Stud 22:157–170

Lumpkin G, Moss TW, Gras DM, Kato S, Amezcua AS (2013) Entrepreneurial processes in social contexts: how are they different, if at all? Small Bus Econ 40(3):761–783

Luppi B, Marzo M, Scorcu AE (2008) Credit risk and Basel II: are nonprofit firms financially different? Appl Financ Econ Lett 4:199–203

Moro A, Fink M, Kautonen T (2014) How do bank assess entrepreneurial competence? The role of voluntary information disclosure. Int Small Bus J 32(5):525–544

Peltoniemi J (2007) The benefits of relationship banking: evidence from small business financing in Finland. J Financ Serv Res 31:153–171

Sabatini F, Modena F, Tortia E (2014) Do cooperative enterprises create social trust? Small Bus Econ 42(3):621–641

Scarlata M, Zacharakis A, Walske J (2016) The effect of founder experience on the performance of philanthropic venture capital firms. Int Small Bus J 34(5):618–636

Shaw E, de Bruin A (2013) Reconsidering capitalism: the promise of social innovation and social entrepreneurship? Int Small Bus J 31(7):737–746

Stiglitz DJ (2009) Moving beyond market fundamentalism to a more balanced economy. Ann Public Cooper Econ 80(3):345–360

Stiglitz JE, Weiss A (1981) Credit rationing in markets with imperfect information. Am Econ Rev 71:393–441

Teasdale S (2011) What’s in a name? Making sense of social enterprise discourses. Public Policy Adm 27:99–119

Thomas A (2004) The rise of social cooperatives in Italy. Voluntas Int J Volunt Nonprofit Organ 15:242–263

Weber O, Remer S (2011) Social banks and the future of sustainable finance. Routledge, London

Zecchini S, Ventura M (2009) The impact of public guarantees on credit to SMEs. Small Bus Econ 32(2):191–206

Acknowledgements

We benefited from conversations with Elena Beccalli, Niels Johannesen, Fabrizio Mattesini, Diogo G.C. Britto, Tommaso Colussi, and from comments from an anonymous referee. We thank Tiziano Gerosa for help with data collection and organization of the data sets. We thank Banca Prossima for sharing information on credit recipients. The usual disclaimer applies.

Funding

Open access funding provided by Catholic University of the Sacred Heart within the CRUI-CARE Agreement. This research did not receive any specific Grant from funding agencies in the public, commercial, or non-profit sectors.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Missing Open Access funding information has been added in the Funding Note.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Aktaş, K., Barbetta, G.P. The Effect of Giving Credit to Social Enterprises: Evidence From Italy. Ital Econ J 9, 235–263 (2023). https://doi.org/10.1007/s40797-022-00188-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40797-022-00188-1