Abstract

This paper aims to study the impact of exchange rate and capital flows on output in one unifying model. To explore this issue, we apply a vector auto-regression (VAR) model with Cholesky decomposition to a group of developed economies (Canada, Switzerland, Australia, Italy, the Netherlands, and Spain) and developing economies (Mexico, Indonesia, Korea, Malaysia, Philippines, Brazil, and Chile). The sample period varies for each country with the longest for Switzerland (1970:1–2010:3) and the shortest for Chile (1996:1–2010:3). The findings suggest first that contractionary devaluation is more likely to happen in developing countries while expansionary devaluation is more prevalent in developed countries. Second, the current account tends to improve in some of the countries facing currency depreciation. However, whether output increases after a real devaluation or not has little to do with whether the current account improves or not. Third, in response to capital inflows, output in developed countries are largely unaffected, while output in developing countries generally increases.

Similar content being viewed by others

Notes

In a textbook model, adverse external shocks lead to a depreciation of the real exchange rate that by stimulating net exports, boosts aggregate demand and offsets the effects of the initial shock. Therefore, flexible exchange rates can absorb adverse external shocks.

See Edwards (1986) for the summary of the theoretical background of contractionary devaluation effect on output.

The summary of the table for exchange rate regime classification from 1997 to 2007 is available upon request.

Nominal effective exchange rate is the trade-weighted average of bilateral exchange rates against the US dollar. The weighting schemes are as follows: for Australia, (US, Japan, UK) = (0.33, 0.33, 0.33), for Spain, (Germany, France, Italy) = (0.4, 0.4, 0.2), for Italy, (Germany, France) = (0.6, 0.4), for the Netherlands, (Germany, Belgium, UK, France) = (0.4, 0.2, 0.2, 0.2), for Brazil, (US, Argentina, Germany) = (0.53, 0.3, 0.17), for Chile, (US, Japan, UK) = (0.51, 0.26, 0.23), for Indonesia, (Japan, US, Korea) = (0.51, 0.35, 0.16), for Korea, (US, Japan) = (0.5, 0.5), for the Philippines, (US, Japan, Korea) = (0.54, 0.36, 0.14), and for Malaysia, (US, Japan) = (0.6, 0.4). For Canada and Mexico, the US is considered as a foreign country, while for Switzerland, Germany takes on the role due to the preeminent role of each country for each group.

The results of the unit root test are available upon request.

The sample periods are as follows: Australia (1976:Q1-2009:Q3), Brazil (1995:Q1-2009:Q4), Canada (1971:Q2-2009:Q3), Chile (1991:Q1-2009:Q3), Indonesia (1990:Q1-2009:Q3), Italy (1971:Q2-2009:Q3), Korea (1976:Q1-2009:Q3), Malaysia (1981:Q1-2009:Q1), Mexico (1981:Q1-2009:Q3), the Netherlands (1971:Q2-2009:Q3), the Philippines (1986:Q1-2007:Q4), Switzerland (1976:Q2-2009:Q3), and Spain (1976:Q2-2009:Q3).

Kim and Ying (2001) also show that a change in the U.S. real GDP and the interest rates explains why there are more than 50 % of capital inflows into Korea and Mexico.

The AIC selects 4 or less lags for all countries except Spain, Italy, and Korea, for which 5 lags are chosen.

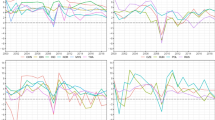

Due to the length of the paper, we only display the impulse responses of the capital account, the real output, and the current account in Australia, Switzerland, and Italy for developed countries in Figure 1 and the same variables in Brazil, Chile, and Indonesia for developing countries in Fig. 2. Full results are available upon request.

Standard errors for the impulse responses and forecast error variance decompositions are computed using Monte Carlo simulations with 1000 iterations.

Devaluation is the term that usually applies to exchange rate changes under a fixed exchange rate regime whereas part of the countries in this study maintained a floating exchange rate. We use devaluation and depreciation interchangeably.

The results are available upon request.

Due to the length of the paper, the impulse responses from panel regressions for a capital inflow shock are not presented but are available upon request.

References

Abdelal, R., & Alfaro, L. (2003). Capital and control: lessons from Malaysia. International Finance and Trade, Challenge, 46(4), 36–53.

Agenor, P. R., & Montiel, P. (1996). Development Macroeconomics. Princeton: Princeton University Press.

Aitken, B. J., & Harrison, A. E. (1999). Do domestic firms benefit from direct foreign investment? Evidence from Venezuela. American Economic Review, 89(3), 605–618.

Calvo, G. A., Leiderman, L., & Reinhart, C. M. (1996). Inflows of capital to developing countries in the 1990s. The Journal of Economic Perspectives, 10(2), 123–139.

Cooper, R. N. (1971). Currency Depreciation in Developing Countries. In: Princeton Essays in International Finance (86). Princeton University.

Cowan, K. and De Gregorio, J. (2007). International Borrowing, Capital Controls, and the Exchange Rate: Lessons from Chile. Capital Controls and Capital Flows in Emerging Economies: Policies, Practices, and Consequences, National Bureau of Economic Research.

Diaz-Alejandro, C. F. (1963). A note on the impact of devaluation and the redistributive effect. The Journal of Political Economy, 71(6), 577–580.

Edwards, S. (1986). Are devaluations contractionary? The Review of Economics and Statistics, 68(3), 501–508.

Edwards, S. (1989). Real Exchange Rates, Devaluation, and Adjustment: Exchange Rate Policy in Developing Countries. Cambridge: MIT Press.

Eichengreen, B., & Sachs, J. (1985). Exchange rates and economic recovery in the 1930s. Journal of Economic History, 44(4), 925–946.

Eichengreen, B., Hausmann, R., & Panizza, U. (2002). Original Sin: The Pain, the Mystery and the Road to Redemption, paper presented at a conference on “Currency and Maturity Matchmaking: Redeeming Debt from Original Sin”. Washington D.C: Inter-American Development Bank.

Findlay, R., & Rodriguez, C. A. (1977). Intermediated imports and macroeconomic policy under flexible exchange rates. Canadian Journal of Economics, 10(2), 208–217.

Frankel, J. A. (1988). Ambiguous policy multipliers in theory and in empirical models. In R. C. Bryant, D.W. Henderson, G. Holtham, (Eds.), Empirical Macroeconomics for Interdependent Economies (pp. 17–26). Washington D.C.: The Brookings Institution.

Frankel, J. A. (2005). Mundell-fleming lecture: contractionary currency crashes in developing countries. IMF Staff Papers, 52(2), 149–182.

Giovanni, J. D., Gottselig, G., Jaumotte, F., Ricci, L. A. and Tokarick, S. (2008). Globalization: A Brief Overview, International Monetary Fund Issues Brief, Issue 02/08. https://www.imf.org/external/np/exr/ib/2008/053008.htm. Accessed 29 Dec 2014.

Goldberg, L. S. and Klein, M. (1998). Foreign Direct Investment, Trade and Real Exchange Rate Linkages in Developing Countries. In Reuven Glick (Ed.), Managing Capital Flows and Exchange Rates: Perspectives from the Pacific Basin (pp. 73–100). Cambridge University Press

Goldstein, M., & Khan, M. S. (1985). Income and price effects in foreign trade. Handbook of International Economics, 2, 1041–1105.

Gylfason, T., & Radetzki, M. (1991). Does devaluation make sense in the least developed countries? Economic Development and Cultural Change, 40(1), 1–25.

Gylfason, T., & Risager, O. (1984). Does devaluation improve the current account? European Economic Review, 25, 37–64.

Gylfason, T., & Schmid, M. (1983). Does devaluation cause stagflation? The Canadian Journal of Economics, 16(4), 641–654.

Hagen, J. and Zhang, H. (2011). International Capital Flows and Aggregate Output. CEPR Discussion Paper, DP8400. Available at SSRN: http://ssrn.com/abstract=1853129.

Hur, J., Raj, M., & Riyanto, Y. E. (2006). Finance and trade: a cross-country empirical analysis on the impact of financial development and asset tangibility on international trade. World Development, 34(10), 1728–1741.

Investopedia Staff (2014). The Effects of Currency Fluctuations on the Economy. Investopedia. http://www.investopedia.com/articles/forex/080613/effects-currency-fluctuations-economy.asp. Accessed 29 Dec 2014.

Johnson, S., Ostry, J. D., and Subramanian, A. (2006). The Prospects for Sustained Growth in Africa: Benchmarking the Constraints. NBER Working Paper, 13120.

Kamin, S. B., & Rogers, J. H. (2000). Output and the real exchange rate in developing countries: an application to Mexico. Journal of Development Economics, 61(1), 85–109.

Kim, S., & Roubini, N. (2000). Exchange rate anomalies in the industrial countries: a solution with a structural VAR approach. Journal of Monetary Economics, 45(3), 561–586.

Kim, Y., & Ying, Y. H. (2001). An empirical analysis on capital flows: the case of Korea and Mexico. Southern Economic Journal, 67(4), 954–968.

Kim, Y., & Ying, Y. H. (2007). An empirical assessment of currency devaluation in East Asian countries. Journal of International Money and Finance, 26(2), 265–283.

Kwan, C. H. (1994). Economic Interdependence in the Asia-Pacific Region: Towards a Yen Bloc. London: Routledge.

Lartey, E. K. K. (2008). Capital inflows, resource reallocation and the real exchange rate. International Finance, 11(2), 131–152.

Lee, J. Y. (1997). Sterilizing Capital Inflows. IMF Economic Issues, 7.

Mejía-Reyes, P., Osborn, D. R., & Sensier, M. (2010). Modeling real exchange rate effects on output performance in Latin America. Applied Economics, 42(19), 2491–2503.

Narayan, P. K. (2006). Examining the relationship between trade balance and exchange rate: the case of China’s trade with the USA. Applied Economics Letters, 13(8), 507–510.

Reinhart, C. M. (2000). The mirage of floating exchange rates. American Economic Review, 90(2), 65–70.

Shahbaz, M., Islam, F., & Aamir, N. (2012). Is devaluation contractionary? Empirical evidence for Pakistan. Economic Change and Restructuring, 45(4), 299–316.

Sharma, S. (2003). The Malaysian capital control regime of 1998: implementation, effectiveness, and lessons. Asian Perspective, 27(1), 77–108.

Shi, J. (2006). Are Currency Appreciations Contractionary in China? NBER Working Paper, 12551.

Sims, C. A. (1980). Macroeconomics and reality. Econometrica, 48, 1–48.

Stiglitz, J. E. (2004). Capital-market liberalization, globalization, and the IMF. Oxford Review of Economic Policy, 20(1), 57–71.

Upadhyaya, K. P., & Upadhyay, M. P. (1999). Output effects of devaluation: evidence from Asia. The Journal of Development Studies, 35(6), 89–103.

Upadhyaya, K. P., Dhakal, D. P., & Mixon, F. G. (2000). Exchange rate adjustment and output in selected Latin American countries. Economia Internazionale, 53(1), 107–117.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Kim, G., An, L. & Kim, Y. Exchange Rate, Capital Flow and Output: Developed versus Developing Economies. Atl Econ J 43, 195–207 (2015). https://doi.org/10.1007/s11293-015-9458-2

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11293-015-9458-2