Abstract

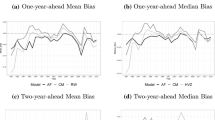

In this article, we analyze the properties of professional aggregate corporate earnings forecasts with regards to accuracy, unbiasedness, and efficiency. Using a large panel of forecasts for the years 1992–2011, we find that forecast errors are in general large, and the magnitude of forecast errors varies substantially across forecasters. Forecasts are however directionally accurate, especially during periods of slowdown. We find evidence of an underprediction bias, as forecasters failed to predict the strong growth of corporate earnings that took place over the past two decades. Forecasts biases and forecast errors are particularly large during periods of economic instability such as recession years, suggesting that biases originate in forecasters’ slow adjustment to structural shocks. Finally, we reject forecast efficiency, and find evidence of overreaction to new information, as evidenced by the negative autocorrelation of forecast revisions. Forecasters overreact equally strongly to good and bad aggregate earnings news, resulting in excessive forecast volatility.

Similar content being viewed by others

Notes

Note that \(h=24\) refers to the initial forecast, i.e. 24-month ahead; whereas \(h=1\) refers to the final forecast, 1-month ahead.

For an examination of the reasons behind the large revisions in aggregate corporate earnings estimates, see Himmeberg et al. (2004).

It should be noted that the pooled approach is different from testing efficiency on the consensus forecast. Efficiency tests on the consensus forecast are known to be biased due to the aggregation bias (Isiklar 2005). The pooled approach that we use does not have this aggregation bias.

Proof: \(r_{i,t,h}=f_{i,t,h}-f_{i,t,h+1}=\lambda _{t,h}-\lambda _{t,h+1}+\varepsilon _{i,t,h}-\varepsilon _{i,t,h+1}=u_{t,h}+\eta _{i,t,h}\)

References

Abarbanell J (1991) Do analysts’ earnings forecasts incorporate information in prior stock price changes? J Account Econ 14:147–165

Ager P, Kappler M, Osterloh S (2009) The accuracy and efficiency of the Consensus Forecasts: a further application and extension of the pooled approach. Int J Forecast 251:167–181

Altavilla C, De Grauwe P (2010) Forecasting and combining competing models of exchange rate determination. Appl Econ 42:3455–3480

Anilowski C, Feng M, Skinner J (2007) Does earnings guidance affect market returns? The nature and information content of aggregate earnings guidance. J Account Econ 44:36–63

Ball R, Sadka G, Sadka R (2009) Aggregate earnings and asset prices. J Account Res 47:1097–1133

Batchelor R (2007) Bias in macroeconomic forecasts. Int J Forecast 23:189–203

Chen Q, Jiang W (2006) Analysts’ weighting of private and public information. Rev Financ Stud 19:319–355

Cowen A, Groysberg B, Healy P (2006) Which types of analyst firms are more optimistic. J Account Econ 41:119–146

Cready W, Gurun U (2010) Aggregate market reaction to earnings announcements. J Account Res 48:289–333

Croushore D (1999) How useful are forecasts of corporate profits? Bus Rev (Federal Reserve Bank of Philadelphia), pp 3–12

Darrough M, Russell T (2002) A positive model of earnings forecasts: top down versus bottom up. J Bus 751:127–152

Davies A, Lahiri K (1995) A new framework for analysing survey forecasts using three-dimensional panel data. J Econom 68:205–227

De Bondt W, Thaler R (1990) Do security analysts overreact? Am Econ Rev 80:52–57

Deschamps B, Ioannidis C (2013) Can rational stubbornness explain forecast biases? J Econ Behav Organ 92:141–151

Easterwood J, Nutt S (1999) Inefficiency in analysts’ earnings forecasts: systematic misreaction or systematic optimism? J Finance 545:1777–1797

Ehrbeck T, Waldmann R (1996) Why are professional forecasters biased? Agency versus behavioral explanations. Q J Econ 111:21–41

Gu Z, Xue J (2007) Do analysts overreact to extreme good news in earnings. Rev Quant Finan Acc 29:415–431

Han B, Manry D, Shaw W (2001) Improving the precision of analysts’ earnings forecasts by adjusting for predictable bias. Rev Quant Finan Acc 17:81–98

Himmeberg C, Mahoney J, Bang A, Chernoff C (2004) Recent revisions to corporate profits: What we know and when we knew it. Current Issues in Econ and Finan, Federal Reserve Bank of New York 10(3):1–7

Ho LCJ, Tsay J (2004) Analysts’ forecasts of Taiwanese firms’ earnings: some empirical evidence. Rev Pac Basin Financ Markets Policies 7:571–597

Hong H, Kubik J (2003) Analyzing the analysts: career concerns and biased earnings forecasts. J Finance 58:313–351

Isiklar G (2005) On aggregation bias in fixed-event forecast efficiency tests. Econ Lett 89(3):312–16

Kanagaretnam K, Lobo G, Mathieu R (2012) CEO stock options and analysts’ forecast accuracy and bias. Rev Quant Finan Acc 38:299–322

Knill A, Minnick K, Nejadmalayeri A (2012) Experience, information asymmetry, and rational forecast bias. Rev Quant Finan Acc 39:241–272

Kothari S, Lewellen J, Warner J (2006) Stock returns, aggregate earnings surprises, and behavioral finance. J Finan Econ 79:537–568

Kwon S (2002) Financial analysts’ forecast accuracy and dispersion: high-tech versus low-tech stocks. Rev Quant Finan Acc 19:65–91

Lahiri K, Sheng X (2010) Learning and heterogeneity in GDP and inflation forecasts. Int J Forecast 26:265–292

Lim T (2001) Rationality and analysts’ forecast bias. J Finance 56:369–385

Mest D, Plummer E (2003) Analysts’ rationality and forecast bias: evidence from analysts’ sales forecasts. Rev Quant Finan Acc 21:103–122

McNichols M, O’Brien P (1997) Self-selection and analyst coverage. J Account Res 35:167–199

Mikhail M, Walher B, Willis R (1999) Does forecast accuracy matter to analysts? Acc Rev 74:185–200

Nordhaus W (1987) Forecasting efficiency: concepts and applications. Rev Econ Stat 69:667–674

Raedy J, Shane P, Yang Y (2006) Horizon-dependent underreaction in financial analysts’ earnings forecasts. Contemp Account Res 23(1):291–322

Sadka G, Sadka R (2009) Predictability and the earnings-return relation. J Finan Econ 94:87–106

Xu L, Tang A (2012) Internal control material weakness, analysts’ accuracy and bias, and brokerage reputation. Rev Quant Finan Acc 39:27–53

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

1.1 Unbiasedness test

The estimates of the forecasters’ biases, \(\phi _{i}\) can obtained by the following simple mean of forecasting errors:

For statistical inference, we use the forecasting error decomposition model of Davies and Lahiri (1995) introduced in (2). To estimate the macro shocks and the idiosyncratic components, we first compute the centered forecast error: \(\hat{v}_{i,t,h}=A_{t}-F_{i,t,h}-\hat{\phi _{i}}.\) The common macro shocks, \(\hat{\lambda }_{t,h}\), can be obtained by averaging the centered forecasting errors over each separate target year and forecast horizon:

While the estimated idiosyncratic shocks are the difference of each centered forecasting error minus the common macro shocks, \(\hat{\lambda }_{t,h}\), that is:

We test the significance of the biases using the GMM covariance matrix \(Var( \hat{\phi })=(X^{\prime }X)^{-1}X^{\prime }\Sigma X(X^{\prime }X)^{-1},\) where \(X\) is a vector of ones. To estimate \(\Sigma\) we need to compute the non-zero covariances between the composite error terms \(v\)’s, that are:

For the estimation of \(\sigma _{u}^{2}\) and \(\sigma _{i}^{2},\) see Davies and Lahiri (1995).

1.2 Efficiency test

For the individual efficiency test, we first obtain the OLS estimates of the coefficient in Eq. (4), \(\hat{\beta }_{i}\), for each forecaster. To test the hypothesis that \(\beta _{i}=0\), we use the GMM estimator of the variance of \(\hat{\beta }\) for which we need to know the covariance matrix of the error terms \(Var(\hat{\beta })=(r^{\prime },r)^{-1}r^{\prime }\Xi r(r^{\prime },r)^{-1}.\) Where \(r\) is the vector of lagged forecasting revisions, and \(\Xi\) is the error covariance matrix. To estimate \(\Xi\) we compute the non-zero covariances between the composite error terms \(\xi\)’s, that are:

Rights and permissions

About this article

Cite this article

Deschamps, B. Are aggregate corporate earnings forecasts unbiased and efficient?. Rev Quant Finan Acc 45, 803–818 (2015). https://doi.org/10.1007/s11156-014-0456-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-014-0456-2