Abstract

In this paper we analyze the argument—which has been used by both the National Labor Relations Board and the National Collegiate Athletic Association—that unionization and/or player pay will hurt competitive balance in college sports. We present a theoretical analysis of universities that recruit athletes and examine the assumptions that are needed for player compensation to decrease competitive balance. We also empirically illustrate the differences in balance between professional and college sports. Given the theoretical and empirical analysis, we argue that unionization and/or player pay is unlikely to hurt competitive balance.

Similar content being viewed by others

Notes

In 2013, many of the football players at Northwestern University wanted to form a player’s union for college athletes. In 2014, their case went in front of the National Labor Relations Board (NLRB) and the Chicago district of the NLRB ruled that the players were employees of the university and therefore they could form a union. Northwestern appealed this ruling and in 2015 the NLRB ruled that the football players at Northwestern could not form a union. However, the NLRB did not assert jurisdiction, which means that the ruling could be overturned in the future. Since the ruling only affects Northwestern, some have interpreted this as saying that the NLRB might reverse its decision if a national union was formed, instead of just a small union of football players at one university.

In 2014, the NCAA’s expert witnesses in O’Bannon v. NCAA, 7 F.Supp.3d 955, argued that the NCAA was a cartel, which allowed it to restrict player pay, but that this restriction would help competitive balance.

A main source of payment for many college athletes are grants-in-aid (in essence, athletic scholarships), which can vary depending upon the cost of tuition at the university. Even though an athlete might not value the education similarly to the cost, the value of a college education can certainly differ across universities.

For more discussion regarding this talent function, see Salaga et al. (2014).

The size of the market is dependent upon the marginal revenue with respect to winning.

For example, competitive balance can depend on factors such as scheduling, drafts, and many other league rules.

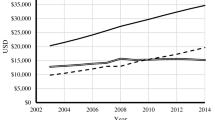

http://www.forbes.com/nfl-valuations/list/ and http://www.forbes.com/nba-valuations/list/. Accessed February 10, 2017.

Many stadiums and arenas are publicly funded with relatively low operations and rental costs that are charged to pro teams, which allows the (subsidized) owners to pocket more money than do universities that often own their own stadiums and facilities outright.

We note that in some cases, winning percentages may not add to 1 (or average 0.5) across the entirety of NCAA football or basketball. For example, some FBS teams play Football Championship Series (FCS) teams during the regular season, therefore resulting in no losses for an FBS team in the sample. However, the impact that these games have on the measure is likely to be extremely small given the number of teams, and we therefore assume that this is ignorable in our context.

References

Berri, D. J., Brook, S. L., Frick, B., Fenn, A. J., & Vicente-Mayoral, R. (2005). The short supply of tall people: Competitive imbalance and the National Basketball Association. Journal of Economic Issues, 39(4), 1029–1041.

Brown, R. (2011). Research note: Estimates of college football player rents. Journal of Sports Economics, 12(2), 200–212.

Brown, R. W. (1993). An estimate of the rent generated by a premium college football player. Economic Inquiry, 31(4), 671–684.

Brown, R. W. (1994). Measuring cartel rents in the college basketball player recruitment market. Applied Economics, 26(1), 27–34.

Brown, R. W., & Jewell, R. T. (2006). The marginal revenue product of a women’s college basketball player. Industrial Relations: A Journal of Economy and Society, 45(1), 96–101.

Depken, C. A., & Wilson, D. P. (2006). NCAA enforcement and competitive balance in college football. Southern Economic Journal, 72(4), 826–845.

Eckard, E. W. (1998). The NCAA cartel and competitive balance in college football. Review of Industrial Organization, 13(3), 347–369.

Fleisher, A. A., Shughart, W. F., & Tollison, R. D. (1988). Crime or punishment? Enforcement of the NCAA football cartel. Journal of Economic Behavior & Organization, 10(4), 433–451.

Fort, R. & Winfree, J. (2013). 15 sports myths and why they’re wrong. Stanford, CA: Stanford University Press.

Hunsberger, P. K., & Gitter, S. R. (2015). What is a blue chip recruit worth? Estimating the marginal revenue product of college football quarterbacks. Journal of Sports Economics, 16(6), 664–690.

Lane, E., Nagel, J., & Netz, J. S. (2014). Alternative approaches to measuring MRP: Are all men’s college basketball players exploited? Journal of Sports Economics, 15(3), 237–262.

Mills, B. M., & Salaga, S. (2015). Historical time series perspectives on competitive balance in NCAA Division I basketball. Journal of Sports Economics, 16(6), 614–646.

Quirk, J. (2004). College football conferences and competitive balance. Managerial and Decision Economics, 25(2), 63–75.

Rottenberg, S. (1956). The baseball players’ labor market. Journal of Political Economy, 64(3), 242–258.

Salaga, S., & Fort, R. (2017). Structural change in competitive balance in big-time college football. Review of Industrial Organization, 50(1), 27–41.

Salaga, S., Ostfield, A., & Winfree, J. A. (2014). Revenue sharing with heterogeneous investments in sports leagues: Share media, not stadiums. Review of Industrial Organization, 45(1), 1–19.

Sutter, D., & Winkler, S. (2003). NCAA scholarship limits and competitive balance in college football. Journal of Sports Economics, 4(1), 3–18.

Tullock, G. (1980). Efficient rent seeking. In J. Buchanan, R. Tollison, & G. Tullock (Eds.), Toward a theory of the rentseeking society (pp. 97–112). College Station: A&M University Press.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

If we allow for a non-zero restriction—\( \bar{\rho } \)—that does restrict both teams, then Eqs. (9) and (10) become

and

Therefore, the optimal level of indirect investment for the small-market team is given by

Since investment must be non-negative, indirect investment will stop when

As the restriction on direct investment increases, the next qualitative change in investments is either that the large-market ceases its indirect investment, or the restriction on direct investment will not be restricting for the small-market team. We will first analyze the case where large-market indirect investment stops first. In this case, \( \varphi_{S} = 0, \) and \( \rho_{S} = \bar{\rho }, \) so the impact of indirect investment by the large-market team is given by

Therefore

And this will equal zero when

If it is the case that \( a_{S} = a_{L} \), this can be simplified to

However, the small-market team might stop direct payments before the large-market team stops indirect payments. In this case, the marginal impact of direct payments to the small-market team is given by

and

and therefore

So, when \( \bar{\rho } \) surpasses that point, the restriction is no longer restrictive to the small-market team.

Finally, we find the point of a superfluous restriction where it does not restrict either team. The first-order conditions are given by,

And

which gives us

If we assume that \( \sigma = 2,\alpha_{S} = \alpha_{L} = .1 \), \( b = 2 \), and \( c = 1 \), then the small-market team will stop investing indirectly when \( \bar{\rho } = 0.06111 \); the small-market team will stop investing directly; and the large-market team will stop investing indirectly when \( \bar{\rho } = 0.2 \), and the large-market team will stop investing directly when \( \bar{\rho } = 0.39444 \).

Rights and permissions

About this article

Cite this article

Mills, B., Winfree, J. Athlete Pay and Competitive Balance in College Athletics. Rev Ind Organ 52, 211–229 (2018). https://doi.org/10.1007/s11151-017-9606-8

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11151-017-9606-8