Abstract

We conduct a quasi-natural experiment for Hong Kong to explore the spatial effects associated with proximity to Covid-19 infections on real estate equity performance. During the first months of the pandemic, Hong Kong reported daily roadmaps of Covid-19 cases. We use these to match with the locations of properties held by real estate companies. Using a difference-in-differences spatial discontinuity model, we find that real estate firms which own a property within 0.1 miles from an infectious site are associated with 0.23% significantly lower daily returns one day after the news. We find evidence for spillover effects for up to two miles from the Covid-19 case, and more pronounced effects on small firms. The paper provides novel findings about the spatial effects of Covid-19 news on stock markets.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The novel coronavirus Covid-19Footnote 1 was first reported in December 2019 and by March 11th 2020, the World Health Organization (WHO) declared it a global pandemic (World Health Organization, 2020). In the first three months of 2020, new Covid-19 infected cases were announced on national television and were considered headline news. To reduce the transmission of the virus and before the wide adaptation of national or regional lockdowns, a number of countries and regions, including the Hong Kong Special Administrative Region of China (Hong Kong, hereafter), which is the focus of this paper, started publicly disclosing the location of Covid-19 patients as well as the geographic footprints of Covid-19 patients immediately when this information was available through test and trace procedures.

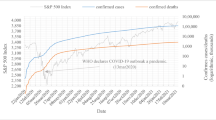

In response to the uncertainty around the emerging Covid-19 epidemic at the time, stock markets around the world plummeted in February and March 2020. In the first quarter of 2020, the Dow Jones Industrial Average and London's FTSE 100 witnessed its biggest decline since 1987, falling by 24%. The S&P fell by 20% which was the greatest loss since 2008 (BBC News, 2020). Publicly listed real estate companies were particularly strongly affected. Market capitalization of Hong Kong Real Estate Investment Trusts (REITs) dropped by approximately 20% in the first quarter of 2020. Investor and tenant sentiment in commercial real estate has also dropped globally (Royal Institution of Chartered Surveyors, 2020).

In Hong Kong, news about the buildings Covid-19 infected cases have visited, i.e. ‘Covid buildings’, were updated daily on a websiteFootnote 2 which could be accessed by everyone. This information was shared to the public to use as a roadmap and avoid infectious sites. Covid buildings therefore will be associated with a higher spatially transmitted Covid-19 risk. The risk can stem from a heightened risk of infection for the users of the affected buildings.Footnote 3 For example, Covid-19 might lead to a possible reduction in building services and an increase in sick leave for the businesses located in such buildings.

Therefore, we assume that in addition to the market effect associated with the negative market sentiment around the implications of a global pandemic, there are negative impacts stemming from the spatial properties of the virus. There can be an expectation from investors that Covid-19 risks are spatially distributed and hence only buildings close to infections are perceived to experience greater loss caused by Covid-19. The reason behind this is that Covid-19 virus is associated with high transmissibility, staying “viable and infectious in aerosols for hours and on surfaces up to days” (van Doremalen et al., 2020). The effects can be exacerbated when the building has poor ventilation, or the space is smaller (Morawska & Cao, 2020).

Using the roadmap of Covid buildings for Hong Kong, we can conduct a quasi-natural experiment to identify Covid-19 spatial effects on the performance of real estate companies. For that, we use a difference-in-differences (DID) spatial discontinuity model. We compare returns on firms which had at least one property in proximity to a Covid building to firms which did not before and after the day of a Covid-19 case disclosure, the event day. Our treatment group consists of daily equity returns of firms which own real estate within 0.1 miles from a Covid building.Footnote 4 Our control group consists of daily equity returns of real estate firms which own properties 0.1 to 5 miles away from a Covid building.Footnote 5 News about Covid cases is used as our events and happen on a daily basis. That news is associated with new patients testing positive for Covid-19 and the online publication of the locations the patients had visited in the preceding two weeks.

We construct a novel micro-level data linking Covid-19 cases and the locations of Covid buildings with the locations of properties owned by real estate companies and sort them by their proximity to the respective Covid-19 case.Footnote 6 The measure is time-varying, and we use daily frequency.

We find that companies whose underlying assets are located within 0.1 miles from a Covid building have a significant drop in daily returns. Daily returns decrease by 0.23% one day after the news. This is associated with a reduction in firm value by approximately 2.3 million US dollars on average.Footnote 7 The results demonstrate that Covid-19 risks transmit spatially.

Our results are also in line with the existing findings about the negative effect imposed by the Covid-19 pandemic on the real estate firm’s stock performance (Akinsomi, 2021; Ampountolas et al., 2023; Chong & Phillips, 2022; Ling et al., 2020, 2023; Milcheva, 2022). Our results add to the confirmatory empirical evidence of the effect of idiosyncratic risks spreading spatially and affecting properties in close proximity to a highly localized risk (Milcheva et al., 2021; Zhu & Milcheva, 2020).

The rest of the paper is organized as follows. Section 2 talks about why we look at Hong Kong and explains specifics which make it a suitable area to conduct the research for. Section 3 provides relevant literature. Section 4 presents the data. Section 5 discusses the methodology. Section 6 presents results. Section 7 provides additional robustness tests. Finally, Section 8 concludes.

Why Looking at Hong Kong?

In the early stage of the pandemic, Hong Kong did not witness an explosive growth in confirmed cases. Every time a set of newly-detected Covid-19 cases are disclosed by the Authority, a fury of media news quickly followed up with case details. In particular, the geographical footprints of Covid-19 patients received great media attention. One example of news covering detailed geographical footprints reads:

“Case number … lives in Ka Yee Building…went to Cheung Kong Center on 17 March…went to the bar Dusk till dawn in 76 Jaffe Rd, Wan Chai…”

News media also disseminated the detailed list of buildings visited or resided by Covid-19 patients (such as presenting screenshots of the lists of buildings names) as a note of caution to avoid possible viral risk. The property address also appears in the news title sometimes, such as “Covid-19 cases continuously emerged in… (building address)”. Due to the prompt media response to case disclosure, we use the post-disclosure day as the event day. On the day after the case disclosure, the surge of patient location information is likely to rapidly update investor’s cashflow expectations on properties near Covid-19. Nevertheless, it is important to note that our sample period only covers early days of the pandemic when information inflow on each newly-disclosed infection is plausibly intense, and each case will thus receive sufficient attention from investors.

Hong Kong has experienced SARS in 2003, which similar to Covid-19, is also a highly infectious respiratory viral disease. Therefore, we would expect that people remembering the effects of SARS would also respond more strongly to information about Covid-19 cases. According to a series of surveys on Covid-19 risk perception and behavior in Hong Kong conducted between January and March 2020 by Cowling et al. (2020), between 60 and 90% of the respondents “avoid going to crowded places” and 83%-88% of respondents “stay at home as much as possible”.

Unlike in the US, the Covid-19 outbreak pattern in Hong Kong features a slow growth and a relatively low geographical intensity at the early stage. As shown in Fig. 1, during the early stage of the pandemic in Hong Kong daily incremental case count is close to zero and a new case, receiving great media coverage can be seen as an exogenous shock to the markets leading to investors re-adjusting their expectations on a daily basis. Furthermore, unlike in the US, Hong Kong had past experience with SRAS in 2003, making the Hong Kong stock market more responsive to such news (see Milcheva, 2022).

(Available at: https://github.com/CSSEGISandData/COVID-19.)

Covid-19 daily incremental case count, comparison between Hong Kong and US. Note: This figure demonstrates Covid-19 daily newly-confirmed case count in Hong Kong and United States for the period from 21 January 2020 to 15 April 2020. The solid line represents the incremental case count on a given day in the United States, and the dashed line represents the incremental case count on a given day in Hong Kong. Covid-19 case data is from the Covid-19 Global Cases database at Johns Hopkins University

Literature Review

The research on the impact of Covid-19 on the real estate sector and stock markets is evolving at a fast pace.Footnote 8 So far, most studies on the aggregate effects of Covid-19 on the stock market have conducted empirical analysis at the market level or firm level (Alfaro et al., 2020; Baker et al., 2020; Ling et al., 2020), while we aim to unpack spatial effects associated with proximity to individual Covid-19 infections. Ling et al. (2020) use weighted average of Covid-19 case growth in counties where firms own properties to construct firm-level exposure to Covid-19 in the US. The authors find that a one-standard-deviation increase in the daily Covid-19 exposure is associated with a 0.24–0.93% decrease in abnormal returns one-to-three days after the increase. Milcheva (2022) looks at the effects on the risk-return relationship in the cross-section of real estate equities in the US and in selected Asian countries as a result of Covid-19 acting as a global systemic shock. She constructs regional Covid-19 Risk Factors to assess how the risk exposure of stocks to the pandemic affects their performance reporting substantial differences between stocks in Asia and the US. Real estate sectors experience strong divergence in performance in the US while little sectoral difference is observed in Asia. While insignificant prior to the pandemic, the return-risk relationship becomes significantly negative during the Covid-19 period, with valuation effects driving the results in both regions.

In terms of research on the effect of similar infectious diseases in the Hong Kong context, Wong (2008) finds a Hong-Kong-wide house price decrease of 1.6% after the SARS outbreak which she attributes to a reduction in building service benefits and health risks. She uses an estate-specific SARS indicator to capture an additional decrease of less than 3% for properties that were known to the public or reported in the newspapers to have SARS cases or in close proximity to SARS. This indicates that participants in the property market are sensitive and attentive to information on disease risks associated with an individual property. Furthermore, anecdotal evidence shows that people flee from areas with high number of SARS cases into friends’ or relatives’ homes located in areas with fewer known SARS cases. This demonstrates the volition of Hong Kong people to voluntarily distance themselves from infectious disease cases and the impact of infectious diseases on real estate values.

In terms of the effects from Covid-19 on cashflows of properties, several papers present evidence from a range of countries. Chen et al. (2020) found a significant decrease of 32% (18.57 million RMB per city) in the consumer spending transactions of offline merchants during the 12-week-period of the Covid-19 outbreak in China. Lee and Lee (2022) used Korean Covid-19 cases, mobility and transaction data and found that an increase in Covid-19 risks in adjacent areas reduces non-resident inflow and retail spending in the respective neighborhood. This suggests that the public responds to Covid-19 case location disclosure by reducing their visits and their retail spending near areas with more cases.

Public crisis management and health communication research highlights citizen’s close attention to Covid-19 patient location information. Wu et al. (2023) applied fear appeal theory to offer behavioral explanations on disease-location information and risk perceptions. Information about diseases caused by Covid-19 triggers fear and anxiety which in turn motivates people to obtain and pay attention to relevant information. This is supported by surveys in Wu et al. (2023). Our study is also linked to existing research on the spatial transmissibility of highly localized risks within an asset pricing context (Adams et al., 2015; García & Norli, 2012; Milcheva & Zhu, 2016; Milcheva et al., 2021). Risks associated with one asset might spread spatially and affect nearby assets and respective real estate landlords. Zhu and Milcheva (2020) investigate the linkage between REITs stock prices and the geographical closeness of their underlying assets. The authors find excess movements for REITs that hold properties which located in nearby areas, in addition to the co-movement explained by common factors (market risk, regional risk etc.). The authors demonstrate a long-short trading strategy, which is to buy the stocks that experience an increase in their price if their connected stock returns have also increased and sell the stocks that experience a drop if their connected stock returns have also declined, could generate an average annual non-market return of approximately 10%. And among various kinds of spatial characteristics that affect the valuation of firms, our study is pertinent to the particular risks associated with asset locations and its impact on firm performance (Zhu & Lizieri, 2022). Rehse et al. (2019) study the impact of Hurricane Sandy on REIT stock performance via the exposure of their properties to the storm. Their results show that investors price in the potential negative consequences led by storm. The stock performance of firms with and without properties in evacuation zones diverge, especially during the period when the volume of the news on storm increased greatly.

Data

We start by describing how we quantify the proximity of a real estate company to Covid-19 infections. Many authorities around the world disclose the number and the location of the confirmed Covid-19 cases. However, Hong Kong’s practice of disclosing Covid-19 patients’ geographical footprints (i.e. buildings visited) is unique in that it enables us to identify a list of properties subject to higher Covid-19 risks. This list is updated on a daily basis.

Our study constructs a novel dataset merging two datasets using geographic coordinates. The first one consists of the “Covid buildings”, the properties that were visited or resided in by Covid-19 patients shortly before they were tested positive. The second one consists of properties owned by listed real estate firms in Hong Kong.

Covid-19 Cases

The Hong Kong Department of Health maintains an official database including detailed information on Covid-19 cases.Footnote 9 The database contained disclosure of places that Covid-19 patients visited two weeks prior to them testing positive for the virus. The data collection started on 20 January 2020, but the first disclosure file was online since 28 January 2020. Each entry in the dataset contains the patient ID, a building name and address that a patient or a group of patients visited or resided in. For simplicity, we refer to each “entry” as a Covid-19 “case” in this paper, meaning that each case is an address that involves one or several patients. For each address, the date last resided or visited by the patient has also been recorded. The data is updated daily. The case information is released shortly (usually three days) after the patient tests positively. We download and collapse the daily reports between 28 January 2020 and 31 March 2020. We collect data until 31 March 2020, because the Hong Kong government announced a short-term shutdown of certain types of places like game center, places for leisure and entertainment etc. from end of MarchFootnote 10 with people unlikely to be exposed to the coronavirus in those buildings after the close-down day. After implementing shutdown measures, Covid buildings should spill less spatially transmitted risks to nearby properties. Fears of Covid-19 should not lead rational investors to drive down the stock prices anymore, given that the transmission is impeded by shutdowns. We therefore use only observations before the shutdowns to ensure that the effect we find is purely associated with the perceived loss caused by Covid-19 virus on neighborhood properties. In addition, we argue that only in the early stage of the pandemic when the number of cases was still small and was reported on media on a daily basis and was of general interest, market participants are more likely to engage with such information.

In order to identify the accurate location of Covid-19 cases in Hong Kong, we obtain the longitude and latitude coordinates of each address by extracting coordinates from Google Maps. While both the Chinese and English versions of the Covid-19 Hong Kong data are available, we used the English version of building names. A problem is that building names could be identical across different locations, and this causes difficulties to our coordinate search. For instance, there are some common club names across the globe, and some real estate facilities were named after famous viewpoints or cities around the world. We address the naming issue by carefully checking the locations that returned multiple results. We deleted cases for which we were unable to accurately identify their locations. For example, this can be an address that could not be found on Google Maps or hotels located close to each other that happen to have the same name. Lastly, we filtered all the coordinates again to check for locations that are not within Hong Kong. By doing this, we obtain a list of coordinates of Covid-19 cases (i.e. Covid buildings) in Hong Kong.

Figure 2 depicts the Covid-19 situation during our sample period in Hong Kong. The dashed line in Panel A represents the number of daily newly Covid-19 patients and the solid line represents the cumulative number of patients on a given date. For most of the days in our sample period, until mid-March, the growth of confirmed Covid-19 patients is very low, except a few spikes. This means that daily new Covid-19 cases in the sample period are likely to receive extensive media coverage on case details, especially on the “footprint” of the patients shortly before the cases tested positive. In other words, the public receives the information of the location of Covid buildings in time and with very little effort and costs. This can explain why real estate company stock prices respond to such news. Panel B of Fig. 2 displays the number of newly-disclosed Covid buildings (solid line) and the number of newly-identified near-Covid properties (dashed line) on daily basis. For this graph, we use 0.1 miles as the proximity definition, i.e. properties located within 0.1 miles of a Covid building are defined as “near-Covid”. As expected, these two sets of buildings follow the same trend. As the number of confirmed Covid-19 patients grows, the daily incremental number of properties they have visited is generally growing. The daily incremental number of “near-Covid” buildings follows a very similar pattern with the Covid building.

Covid-19 case count (patients and buildings). a Number of confirmed Covid-19 patients. b Number of Covid buildings and near-Covid buildings (daily incremental). Note: Graphs in this figure demonstrate Covid-19 patient number, case location count, (i.e. Covid buildings) and near-Covid property count in Hong Kong for the sample period, from 7th February 2020 to 31st March 2020 (The sample period is slightly different from the period for which we collected the Covid building locations, and this is because our sample only covers observations with no missing values in any key variables.). The dashed line in Panel A draws the trend using daily incremental number of patients, and the solid line in Panel A represents the total number of patients on a given day. The solid line in Panel B draw the trend using daily newly-disclosed Covid building count, and the dashed line in Panel B draws the trend using daily newly-identified near-Covid building count. We use 0.1 miles to define “near-Covid” for this graph. More details on Hong Kong property dataset is given in Section 3.2

Real Estate Companies

The other key dataset is the S&P Global Real Estate Properties dataset (formerly known as SNL Real Estate). We collect information on properties held by listed real estate firms as of the end of March 2020. The variables include a dummy for sector of the property such as residential, multiuse, office; the natural logarithm of property age, property size, measured as the natural logarithm of the total interior area.Footnote 11 Company-level information is for the financial year in 2019 and comes from SNL Financial. We include institutional ownership, which is winsorized at the 1% and 99% levels. It is the aggregated percentage of shares owned by all types of institutional investors in a real estate company. EBITDA/AT is the earnings before interest, taxes, depreciation, and amortization (EBITDA) divided by total assets (AT). Leverage is calculated as the total debt divided by total assets at the company level. Firm size is the natural logarithm of total assets. In addition, we obtain the property holdings of listed real estate firms, including the location of individual properties. We also obtain daily equity returns from SNL. All raw returns are winsorized at the 1% and 99% levels. As the dependent variable, we use the 1-day equity returns of a real estate firm on the transaction day following the case disclosure day. We also use the 2-day or 3-day returns which are the cumulative returns on the last two or three trading days prior and following a Covid-19 event.

In addition to raw returns, we also compute CAPM-adjusted returns to account for firm’s exposure to market risk. We estimate pre-Covid betas for each firm by regressing daily excess equity returns on the excess market index returns in the CAPM model setting as below (Sharpe, 1964):

We use Hang Seng index as the market index and 3-month HIBOR as the risk-free rate. The estimation period for the betas is the six months before the disclosure of the first Covid building on January 28, 2020. Next, we compute the CAPM-adjusted returns as the stock’s daily excess return minus the stock’s beta times the market excess return. One may be concerned that Covid-19 has changed the perception of market risk might for many firms. Hence, the betas estimated using the 2019 returns may not be a precise proxy for market risk exposure during Covid-19 (Ramelli & Wagner, 2020). Given above considerations, we therefore use both raw returns and CAPM-adjusted returns to measure stock performance in the empirical models.

Merged Dataset

We merge the Hong Kong Covid-19 dataset and S&P Global Real Estate Properties dataset using the latitude and longitude of buildings in both datasets. We create a joint dataset consisting of all pairwise combinations of Covid-19 cases and real-estate-firm-owned properties.

There are two key location variables in our merged dataset. The first is the coordinate of a Covid-19 case, the second is the coordinate of a real-estate-firm-owned property.Footnote 12 In addition, there are two time variables: the first is the date that one or several Covid-19 patients visit or reside in a building (which later is identified as a Covid building), and the second is the case disclosure date, i.e. the case information available to the general public. For Covid buildings that appear more than once in the dataset, i.e. Covid-19 patents visit the building more than once, we keep only one unique entry – the first entry. There are 919 unique addresses in total that Covid-19 patients have visited or resided in at least once in our sample period. There are 959 Hong Kong properties owned by real estate firms as reported in the S&P Global Real Estate Properties database for which coordinates are available. With the coordinates of Covid-19 cases as well as real-estate-firm-owned properties, we follow McDuff (2012) to calculate the geographic distance between a “Covid building” and a real estate firm-owned property “as the crow flies”. Therefore, our merged dataset consists of all pairwise combinations of a “Covid building” (919) and a real estate firm-owned property (959), giving a total of 881,321 (919 \(\times\) 959) pairwise distances in the primary sample. We keep only the real-estate-firm-owned properties that fall within 5 miles of a Covid-19 case. That is, any real-estate-firm-owned properties within 5 miles of a “Covid building” will contribute one observation. In the end, our sample only includes observations without missing values in key variables and that gives 193,741 pairwise distances, consisting of 895 Covid-19 case locations and 435 real-estate-firm-owned properties owned by 31 real estate firms in Hong Kong during the period of 7th February 2020 to 31st March 2020.Footnote 13 We then use the distances to construct a dummy for properties within 0.1 miles of a Covid-19 case, which we call “Covid-19 Proximity”.Footnote 14

Once the data is merged, we can create our main variable of interest, which is called ‘Covid-19 proximity’. It is a dummy variable which equals 1 if the distance between the location with a confirmed case and the real estate firm’s property is less than 0.1 miles, in the baseline specification.Footnote 15 We test for alternative definitions of distance using 0.5, 1 and 2 miles respectively. Post-case disclosure is a dummy which equals 1 if the observation is on the day after case disclosure day, and 0 if the observation is on the day before case disclosure day.

Summary Statistics

There are 435 properties owned by 31 real estate firms located across 31 Hong Kong districts.Footnote 16 Figure 3 maps the spatial distribution of properties. Solid points in Panel A in Fig. 3 represents the locations of Covid buildings and the hollow points in Panel A represents the location of properties held by Hong-Kong-listed real estate firms. In general, the properties owned by Hong-Kong-listed real estate companies have highly similar spatial distribution patterns to the spatial distribution of Covid buildings in our sample. This is partially because of the 5-mile boundary of the transmission of the virus and the small geographic area which Hong Kong inhibits. Another point to note is that denser locations of both sets of buildings are also the locations with relatively high population densityFootnote 17 (as shown in Panel B in Fig. 3) in the Hong Kong. This means that the spread of Covid-19 cases might be more severe in denser locations.

Spatial distribution of Covid buildings and Hong Kong buildings. a Spatial distribution of Covid buildings and Hong Kong buildings (in-sample). b Population density in 2019 by district. Note: Hollow points in Panel A represents properties owned by Hong-Kong-listed real estate companies and the solid points represents Covid buildings. This is mapped using observations during our sample period from 7th February 2020 to 31st March 2020. Our model only keeps Hong Kong properties that located at least 5 miles away from Covid buildings. Panel B maps the population density using 2019 data from the Census and Statistics Department of Hong Kong

Table 1 presents the summary statistics of the variables used in our analysis for the period before and after the event days. That is, the summary statistics are for one day prior to the case disclosure as well as for the day after the event. All size and ageFootnote 18 measures have been log transformed. The raw return for one day before and one day after the case disclosure is -0.45% with a standard deviation of 3.24%. The mean of the distance between a Covid-19 case and a property owned by real estate firm is 2.74 miles with a standard deviation of 1.28 miles. We will test the effect of Covid-19 proximity on equity returns using different distance bands to define proximity, namely, distance less than 0.1/0.5/1/2 miles. The mean of Distance < 2 miles is 0.3179, meaning that 31.8% of property observations in our sample located within 2 miles from a Covid building. The portion of near-Covid property observations gradually decrease to 10.3%, 4.28% and 0.3% for Distance < 1 mile, 0.5 miles and 0.1 miles respectively. Our sample of properties consists of 24% office property observations, 15% multiuse property observations, and 6% residential property observations. A single location corresponds to 1.08 Covid-19 cases, which means that a Covid-19 case or patient, Covid building, and Covid-19 location can be used interchangeably as they capture the same dynamics.

Methodology

Identifying the effect of Covid-19 on stock prices is challenging, as it is usually difficult to track down the exact location of a Covid-19 case and put it in a relationship with returns. In this study, we use information about the exact location based on the address that Covid-19 patients have visited or resided in (i.e. Covid buildings) and link this to the location of properties owned by real estate firms. We employ a difference-in-differences (DID) estimation as in Bertrand et al. (2004) and Currie et al. (2015). A DID framework provides clean identification. Next to a treatment group, it includes a control group, which does not receive the treatment. Our treatment group consists of properties within 0.1 miles of a Covid building. Our control group are properties between 0.1 to 5 miles from a Covid building. We assume that both groups would similarly be affected by local conditions but differently by news about Covid-19 cases.

Using the DID setting below, our empirical design is more robust and alleviate the concerns that the contemporaneous trends might confound the treatment effect. The model is given as:

where \({Y}_{d,i,t}\) denotes the daily equity return of a real estate firm \(d\) that owns a property \(i\) in day \(t\). We only have two options for \(t\), the first trading day after the case disclosure where \(t\) = 1 or the last trading day before the case disclosure where \(t\)= 0. The index \(i\) in the dependent variable means that we associate each return with each building in the firm’s portfolio. This helps with the right-hand side of the equation, which uses the location of the property for identification of the Covid-19 effects. Specifically, we calculate the distance between each property \(i\) and each Covid-19 case \(j\), and construct Covid-19 proximity dummy variables later based on the distance calculated.

The post-case disclosure variable, \({Post}_{j,t}\), takes the value of one for returns observed one day after the Covid-19 disclosure date and zero otherwise.Footnote 19 The indicator \({[Covid19 Proximity]}_{i,j}\) equals one for companies holding properties that located within 0.1 miles from the Covid-19 case at any one point in time, even prior to the disclosure of that new Covid-19 case. The coefficient \({\beta }_{3}\) on the interaction term \({\left[Covid19 Proximity\right]}_{i,j}\times {Post}_{j,t}\) is the one identifying the treatment effect and is of most interest for us. It captures the differential impact of a Covid-19 case on the stock performance of real estate firms which own properties in proximity to the Covid-19 case relative to real estate firms with properties located further away after the closure, i.e.\(\left({\overline{Y} }_{Near}^{Post}-{\overline{Y} }_{Near}^{Pre}\right)-\left({\overline{Y} }_{Far}^{Post}-{\overline{Y} }_{Far}^{Pre}\right)\). That is, we compare the change in equity returns for treated properties (before vs. after treatment) to the change in equity returns in the control group over the same time period. The coefficient of interest \({\beta }_{3}\) might hence be negative. We also use alternative distances to define proximity by gradually relaxing the boundary of geographical proximity to assess whether the magnitude of \({\beta }_{3}\) changes substantially.

Since markets will only react after the Hong Kong authority discloses the information (as it is very hard to find out about the case prior to that), and there is usually a 3-day window between case confirmation and case disclosure, we use the date of the case disclosure as the event date the treatment comes into effect. This is the date that the Covid-19 case location information will be known to the public. In our baseline, we measure investor’s reactions one day after the case disclosure. The pre-treatment sample consists of the returns one day prior to the event day. The post-treatment sample consists of the returns one day after the event.

Our analysis includes control variables that have been identified in previous studies. These variables are measured as of the end of 2019. We control for property characteristics. We also include the total number of Covid-19 cases reported in a property to control for investors’ concern that a building is becoming a ‘hotspot’ for Covid-19 infections and the level of Covid-19 risk of such buildings is particularly higher. Appendix 1 provides definitions and sources of the variables.

We include firm fixed effects to control for pre-treatment differences in returns and account for time-invariant firm-specific determinants.Footnote 20 In one of our robustness tests, we include a set of firm characteristicsFootnote 21 instead of the firm fixed effects.

In the baseline specification, we include day-district fixed effects to account for localized trends and hence increase the power of our statistic tests. Additional robustness tests include time and district effect individually. The time fixed effect is to absorb shocks that are common to all stocks and the district fixed effect is to address the concerns that movements in stock prices are caused by exposure to regions with certain economic dynamics.

Results

Baseline Results

We show the impact of proximity to Covid buildings on equity returns following an exogenous idiosyncratic Covid-19 shock. The setting with geographical variations (of being close and far away from Covid buildings), and temporal variations (before and after a Covid building is revealed to public) allows us for clear identification in a DID model.

To assess the causal relationship of being close to a Covid building on the returns of the real estate company, we employ a DID estimation. This is our baseline model as specified in Eq. (2). Within this set-up, we are able to identify its spillover effects on nearby properties and their owners. The results are presented in Models (1) and (2) in Table 2. Model (1) controls for property district-time fixed effects and Model (2) also adds firm fixed effects.Footnote 22 The key regression results are the coefficients of the interaction term of Covid19 Proximity and the post-disclosure dummy. There is a statistically significant negative interaction coefficient, which signifies the marginal effect associated with significant lower daily returns of institutional landlords who happen to own a property in close proximity to a Covid building just after the footprint of a new Covid-19 case has been disclosed, as compared to the control group, which is located further away. The treatment effect takes the value of 0.23% and can be interpreted as the differential impact caused by a newly-disclosed Covid-19 infection location on landlords holding properties within 0.1 miles of the Covid building, relative to landlords holding properties located between 0.1 and 5 miles away. Both models have a high R-square of above 0.7. Given that the average firm in our sample has one billion US dollars in market capitalization as of the end of 2019, the exposure to a Covid-19 case is associated with a reduction in firm value by approximately 2.3 million US dollars on average.

The coefficient on the interaction term remains significant after adding firm fixed effects, confirming that the negative effect we observe is not driven by omitted time-invariant firm characteristics. The results also remain robust using CAPM-adjusted returns as shown in Models (3) and (4) in Table 2. Significant and consistent results are found with similar sizes of the negative effects. Overall, we conclude from Table 2 that Covid-19 proximity information shocks exert economically and statistically significant negative effects on equity returns.

As a robustness, we also explore if the effect caused by Covid-19 proximity will strengthen with multiple cases occurring nearby. We create a new variable as the count of Covid-19 cases a firm is exposed to via its property portfolio in a given day. We do not report the results for brevity but can report that the regression coefficient associated with this variable is insignificant. It seems that the presence of only a single Covid-19 case in proximity is enough to serve as a trigger for investors and significantly affects their perception of risk. Additional cases seem not to proportionally increase this perceived risk. This observation might be attributed to the complexity of assessing risk and the information overload in the early stages of the pandemic. We show it can lead to a simplified decision-making process of investors. Hong and Kim (2020) discovered that information overload is associated with the tendency towards more heuristic processes (including heuristic cues and simple judgmental rules) and less systematic processes (involving “careful attention, deep thinking, and intensive reasoning”) when processing information related to the Covid-19 pandemic. In our paper, investors may have simplified their decision-making process by perceiving information as binary (presence vs. no presence of Covid-19 cases), rather than attempting to process more complex information, such as paying attention to the number of Covid-19 cases a firm has been exposed to via all its underlying properties.

Our findings are consistent with Ling et al. (2020) who document a negative relationship between REIT-level geographically weighted Covid-19 growth and REIT’s risk-adjusted returns. A crucial difference between our paper and previous Covid-19 study is that we did not measure aggregate regional Covid-19 exposure as a continuous variable but rather want to account for unexpected highly localized idiosyncratic Covid-19 shocks. We consider each infection event as an exogenous shock on property owners who hold properties exposed to those infections via geographical proximity. This is akin to an event study where we capture the immediate reaction of investors to such unexpected and random events.

Our findings also contribute to the strand of literature that documented negative relationship between stock performance and proximity to disease outbreak. Prior literature includes studies on Ebola. Ichev and Marinč (2018) find that the news on Ebola outbreak cause negative stock reactions. The effect is stronger for stocks of companies that are geographically closers to the birthplace of the Ebola outbreak.

To assess the underlying mechanism of the adverse stock reactions we uncovered, it is imperative to consider the unique topographical features of Hong Kong and its past experience with SARS. Hong Kong's landscape, marked by steep, mountainous terrain and constricted by government land-use policies, severely limits available construction space. This, along with demographic expansion, has necessitated the extensive development of high-rise buildings and compact urban designs, making Hong Kong one of the most densely populated regions worldwide. Such density exacerbates the risk of infectious diseases, particularly those transmitted through respiratory droplets and contact routes, including Covid-19. As a result, the discovery of Covid-19 cases in these areas may prompt a more intense response, given the heightened risk of rapid transmission and the potential for mass infection.

A single Covid-19 case, leading to quarantine and the closure of buildings or operations, may not impact the cash flow expectations or valuations of adjacent real estate properties. However, should a building become a hotspot for mass infection, the value of both the affected property and those in close proximity could be drastically reduced in the Hong Kong context. This argument is supported by the aftermath of the 2003 SARS epidemic in the Hong Kong real estate sector. The most notable example is Amoy Garden, a residential estate where over 300 of Hong Kong's 1,755 SARS cases occurred. The aftermath saw residents fleeing Amoy Garden by selling homes and relocating, earning it the moniker “SARS village”.Footnote 23 Lee et al. (2005) conducted survey with residents of Amoy Garden and revealed that the majority were impacted by a stigma associated with SARS. This stigma manifested in various forms, including “being shunned, insulted, marginalized, and rejected in the domains of work, interpersonal relationships, use of services and schooling”. The survey results indicated that 41% of the respondents relocated from Amoy Garden, while 36% considered moving, and an additional 20% planned to move out in the future due to the SARS-related stigma. Additionally, Wong (2008) found that properties with confirmed SARS cases experienced price drops, highlighting the stigma attached to infected buildings. In the early stages of the Covid-19 pandemic the traumatic memory of SARS was revived, raising similar fears that Covid-19 can lead to stigma for buildings with Covid-19 cases, potentially leading to a drop in property values. Reports have indicated concerns among Hong Kong residents about a repetition of an Amoy Garden-like event during the Covid-19 pandemic.Footnote 24 Above considerations could lead to an erosion of investor confidence for companies with exposure to Covid-19 infectious sites and buildings. We believe that the negative returns observed in listed real estate companies which own properties near Covid buildings could be attributed to reputational harm arising from the stigma associated with the virus.

While it might initially seem surprising to have a significantly negative equity market reaction to a Covid-19 case, the effect makes sense in the context of Hong Kong. Research has shown that investors in this market are particularly responsive to highly granular information and are highly sensitive to negative psychological shocks on property values. For example, Bhattacharya et al. (2021) revealed a highly granular ripple effect of 'haunted' houses on the prices of nearby properties.Footnote 25 They noted that properties labeled as 'haunted' typically saw a price reduction of 20%, with this effect decreasing to 10% for units on the same floor, 7% for units in the same block, and 1% for units in the same estate. Bhattacharya et al.’s research (2021) highlights the Hong Kong market's acute awareness to factors beyond conventional economic indicators, particularly those rooted in psychological beliefs. Hong Kong investors’ awareness of highly granular and localized information also lends support to the significant negative stock reaction we uncover in our study.

In our model, we also include group-invariant property-level variables for controlling property characteristics, regardless of whether or not they are close to Covid-19 infections or not. Property-level variables show significant effect on equity return in Models (1) and (3) of Table 2. The estimated coefficients on Distance to CBD are significantly negative, indicating that investors expect poor performance from firms that hold properties closer to the CBD. This result makes sense, given that densely populated areas are likely to face heightened risks of infections, and the pandemic has led to a revaluation of urban center property values (Rosenthal et al., 2022). The estimated coefficients on Property Age are significantly negative suggesting that investors expect firms that hold older properties to perform worse during the early stage of the pandemic, perhaps due to depreciation associated with aging. The coefficients on Property Size are significantly positive, suggesting that investors expect firms holding bigger properties to perform better during the pandemic. Owners of the big properties are usually rewarded or compensated by higher yields due to market illiquidity associated with the big properties. Despite being in a thinner market, big properties might however perform better (or suffer less) when dealing with risks that jeopardize the cashflows generated from the properties. For example, Hartzell et al. (1986) argue that big properties on average have a greater number of tenants, and the impact of losing a tenant is thus less severe for a big property than that for a small property. We also explore heterogeneity of property type on affecting equity returns. We find a positive coefficient associated with Property Residential Dummy on equity returns. In addition to the relatively inelastic demand characteristics of the residential properties, the positive effect might be a result of individuals reassessing their housing needs and preferences, showing more appreciation of shelters when their fears of crowded public space and packed public commuting raise with the number of confirmed Covid-19 infections. Offices are linked to positive returns, perhaps due to the long-term feature of leases. Multiuse properties might generate positive return because holding mixed use space with diverse purpose enable investors to diversify risks, especially during the economic downturns.

To summarize, the results demonstrate that stock markets price in Covid-19 risks in a spatial manner with the effect being stronger, the closer one is to the infection. We can see that investors are concerned about this risk in a property valuation context too and differentiate between high and low exposure to the health risk. The information on the property portfolio of listed real estate firms is publicly available, and it is not surprising that investors would price highly localized risks which transmit through to company returns via their underlying assets. During the pandemic times of infectious disease like Covid-19 when physical proximity and face-to-face interactions might induce a higher chance of infection, we show that investors are aware of the Covid-19 risk spillover among properties located near each other due to the epidemiological feature of this disease. More broadly speaking, we show that investors price in spatially distributed risks such as the risk of a viral infection, regardless of whether those risks would be associated with material effects on cash flows. The differential returns can also be explained by behavioral biases and fear response to the virus rather than a rational assessment of the risk. We do not test for these as this is beyond the scope of this paper and this remains to be investigated in the future.

Negative Stock Reaction Diminishes with Longer Distances to Covid Buildings

In this section, we examine how far will investors penalize the risk spilled from Covid buildings. We extend the distance band for defining Covid-19 proximity to see how far the negative effect will persist, and how its size may change with distances. It is likely that investors’ reaction to risk spillovers diminishes with distance of the firm’s properties to Covid buildings. We run the same regression specification as in Eq. (2) and gradually relax the proximity boundary. The results are presented in Table 3. All models control for district-day fixed effects, firm fixed effects, Covid building characteristics (i.e., number of patients) and characteristics of properties held by Hong Kong firms (property-level variables as in Table 2). Models (1), (2) and (3) gradually extend the distance bands and use 0.5 miles, 1 mile and 2 miles respectively to define Covid-19 Proximity. Model (4) to (6) run the same regressions as Model (1) to (3) but using CAPM-adjusted returns as the stock performance measure. As expected, the coefficients of the interaction terms turn less negative with greater distances to the infection, providing evidence for the spatial nature of this risk. Although the weakening reaction is less obvious using CAPM-adjusted returns, comparing the results of 0.1 miles (Table 2, Model (4)) with the results of 2 miles (in Table 3, Model (6)), shows a declining trend in coefficients as distance increases. This finding is consistent with Adams et al. (2015) who show large spillover effects for REITs which have their properties in close proximity. Risk spillovers decline quickly when the geographical distance increases.

As reported in Model (1) of Table 3, if a property is located within 0.5 miles of a Covid-19 case, the return is significantly negative, at -0.0006. It is smaller in magnitude compared to -0.0023, the coefficient of Covid19 Proximity \(\times\) Post of 0.1 miles in Table 2. In Model (2) of Table 3, we use 1 mile as the distance boundary. The magnitude of the coefficient further reduces, -0.0004. For robustness, we compare the effect if the proximity is 2 miles to assess if the effect is still material. The result is shown in Model (3) in Table 3. The magnitude of the coefficient reduces by half from -0.0004 to -0.0002 and is only significant at the 10% confidence bands. The weakened negative effects with longer distances suggest that the Covid-19 effect is much more strongly propagated in direct proximity to the case, which is to be expected and demonstrates the role of spatial proximity. The role of distance from a Covid-19 infection on raw returns is not linear for very small distances but linear for distances above 1 mile. So, the properties closest to the buildings with Covid-19 infections will be the ones over proportionally affected by the virus, as we have hypothesized.

The results are in line with the observation that the perceived risk of Covid-19 infections increases when people are geographically closer to a Covid-19 case, as a result, the negative market reaction turns stronger.

Overall, using alternative distance metrics supports our baseline results and demonstrate the importance spatial proximity plays for the strength of the effect of a Covid-19 shock.

Effect of Covid-19 Proximity on Firm Size

We have shown that investors expect Covid-19 infections to spill risks to neighborhood properties, and such risk spillover diminish with distances. We provide evidence that the spillover effect is up to 2 miles. However, a circular area of 2 miles radius is actually a quite large range for social interactions and disease transmission. We hence posit the mechanism behind the stock reactions as an attempt to explain the seemly irrational reaction. One possible explanation is that investors might have generated irrational estimate on expected loss led by Covid-19 infections, when the real loss is hard to estimate in absence of information. As the existing information channels for firms are heterogeneous, some firms have more established information channels to diffuse firm-specific information than others. Real estate stock with poor information dissemination might witness a stronger negative reaction and vice versa. To test this empirically, we use the 2-mile spillover model to check if investors will adjust their estimate for expected loss caused by risk spillover, when information for estimating real losses are more likely to be readily available via established channels.

We use firm size as a proxy for measuring the quality of existing information channels. Large firms are likely to have more well-established information channels compared to smaller firms (Fang & Peress, 2009). Hence, large firms’ information quality and diffusion might be better compared to smaller firms. In other words, when the risk receiver is a large firm, investors are more likely to figure out the real loss led by risk spillover from Covid buildings. As a result, investors are more likely to adjust their estimate of the expected loss and deviate less from the rational reactions. We also want to testify if the negative effect of risk spillover is more pronounced for small firms, due to lack of information to estimate real losses.

To obtain the subsamples of small and large firms, we use the median firm size to divide the sample into two subsamples. The first subsample consists of firms with below median size, i.e. small firms, and the second subsample consists of firms with above median size, i.e. large firms. We use the baseline DID model as outlined in Eq. (2) and 2 miles to define Covid-19 proximity. We use raw returns (Model 1 to 2) and CAPM-adjusted returns (Model 3 to 4) to measure stock reactions and report the results in Table 4. All models controlled for district-day fixed effects, firm fixed effects, Covid building characteristics (i.e., number of patients) and characteristics of properties held by Hong Kong firms (property-level variables as in Table 2). Model (1) and (3) present the results of the subsample consisting of small firms, and the coefficients on the interaction term Covid-19 Proximity \(\times\) Post are negative and statistically significant at 99% confidence level. The magnitude of these negative coefficients is larger than those reported in the 2-mile proximity model in Table 3. That is, the negative effect on raw returns escalates 200% from -0.0002 (Table 3, Model 3) on average firms to -0.0006 (Table 4, Model 1) on small firms. The negative effect on CAPM-adjusted returns escalates 175% from -0.0004 (Table 3, Model 6) to -0.0011 (Table 4, Model 3). In contrast, the regression outcome using large firm subsample diverge from the findings in the small firm subsample. As presented in Model (2), using large firm observations only, the coefficients on the interaction term Covid-19 Proximity \(\times\) Post is not significantly different from zero, with raw returns as the dependent variables. This means that the effect of Covid buildings on the raw returns of large property owners holding a property 2 miles away is negligible. Model (4) of Table 4 presents the results using CAPM-adjusted returns to measure stock performance. We see a negative effect but only with mild significance. The size of the effect in Model (4) is smaller compared to the coefficients in the 2-mile proximity model is Table 3. That is, the negative effect on CAPM-adjusted returns contracts 25% from -0.0004 (Table 3, Model 6) on average firms to -0.0003 (Table 4, Model 4) on large firms.

Next, to assess whether the difference in estimated coefficients of Covid-19 Proximity \(\times\) Post between large firms and small firms is statistically significant, we perform the tests for equality of coefficients. A chi-square test for equality of coefficients across the specifications in Model (1) and (2) in Table 4 yields a p-value of 0.0858. And the chi-square test for equality of coefficients across the specifications in Model (3) and (4) in Table 4 yields a p value of 0.005. The outcome of these tests confirms that the differences in estimated coefficients of Covid-19 Proximity \(\times\) Post between large and small firms are statistically significant.

Overall, our subsample analysis using small and large firms confirms the heterogeneity in investor’s reaction to risk spillover when exposed property firms have different sizes. The divergence in reaction is possibly due to the availability of information on real Covid-induced loss. For large firms which have more information channels, investors estimate the expected loss led by risk spillovers more accurately and deviate less from rational reactions. This finding is consistent with previous literature that studies the role of firm size for the magnitude of the effect. Ichev and Marinč (2018) find that news about Ebola outbreak events cause negative stock reactions, and the effect is more pronounced in small stocks than large stocks. The possible channel they posit is that the role of media is more restrained for large stocks, because large firms already have many channels for disseminating information (Fang & Peress, 2009).

Robustness Tests

We conduct robustness tests to examine how firms with different characteristics perform when their underlying properties are subject to Covid-19 risks and to account for a delay in the response of markets by using the returns in the subsequent days following the case disclosure as well. Moreover, we employ alternative recently-developed methodologies in DID estimations to enhance the robustness of our results.

In the first robustness test, we include specific firm characteristics. Given that our data is in daily frequency and covers the months of February and March 2020, we use balance-sheet variables reported at the end of 2019. The variables that capture firm characteristics are collinear with firm fixed effects because they are mostly balance-sheet figures that do not change during our sample period. CAPM betas calculated for our sample firms are in a cross-section structure i.e. a single beta for a firm during our sample period. We therefore replace the firm fixed effects with firm-level variables that have been identified as the determinants for returns (Goebel et al., 2013; Ling et al., 2020; Rehse et al., 2019). We include firm leverage, size, institutional ownership, profitability and systematic risk. The leverage is estimated as the total book value of debt divided by the book value of total assets. Size is the reported book value of total assets. Institutional ownership is the percentage of shares owned by institutional investors in a real estate firm (Goebel et al., 2013). Profitability (EBITDA/AT) is the earnings before interests, taxes, depreciation and amortization (EBITDA) divided by the book value of assets (AT). Systematic risk is measured using CAPM beta, which is estimated using the CAPM model described in Section 3.2. We use daily returns from 30 January to 3 April 2020 to calculate the betas which characterize the systematic risks during the sample period. The definitions and sources of the variables can be found in the Data section and in Appendix 1.

Model (1) of Table 5 presents the baseline model using firm characteristics to replace firm fixed effects. As shown in the model, the coefficient of firm leverage is significantly negative at 1% level. This suggests that investors expect firms with higher leverage to underperform in the early stage of the pandemic when its underlying assets are subject to the different levels of Covid-19 risks. This finding is consistent with several studies on Covid-19 and REITs (Akinsomi, 2021; Ampountolas et al., 2023; Chong & Phillips, 2022; Ling et al., 2020, 2023), and the underperformance is likely to be attributed to the financial distress of the highly-levered firms during the pandemics. The coefficient of CAPM beta is significantly positive, suggesting that investors expect riskier firms to have a higher return during the pandemic, consistent with financial theory. The coefficient of institutional ownership is significantly negative consistent with the inverse relationship between institutional investor’s ownership and REIT returns documented by Goebel et al. (2013).

In the second robustness test, we consider a delayed dissemination of Covid-19 information to investors. In the baseline model, we use the 1-day post-disclosure equity return to evaluate the effect of Covid-19 news. This is based on the assumption that investors react to Covid-19 information immediately.Footnote 26 However, Covid-19 case information might take longer to be disseminated among investors, and thus it might take longer for the effect to manifest itself on the stock market. To account for a delayed response, we also use 2-day and 3-day cumulative returns. As in the baseline model, we still compare the returns of firms in the treatment group who hold properties near Covid-19 cases, and firms in the comparison group who hold properties further away. Nevertheless, instead of using the returns on the transaction day before or after the event day, we now add the returns on the last two (three) transaction days before and the first two (three) transaction days after the event days, and use them as the dependent variables in the DID model. Results using 2-day and 3-day cumulative returns as the dependent variable and 0.1 miles as Covid-19 Proximity are presented in Models (2) and (3) of Table 5 respectively. Both models include firm fixed effects and district-day fixed effects. The coefficients of the interaction terms are significantly negative for both models. The coefficient using 2-day cumulative returns is -0.0071 and the coefficient using 3-day cumulative returns is -0.0113. Those are substantially larger than those for the 1-day return in the baseline models.

Overall, we see that the longer the period after the announcement, the larger the negative treatment effect is on returns. This means that markets take some time to fully process the negative news associated with Covid-19 infections.

Our results are robust when considering the delayed dissemination of information by investors, as the 2-day and 3-day cumulative equity return of the firms who own properties near Covid-19 cases are still negatively affected by nearby Covid-19 cases.

Thirdly, we consider the case of heterogeneous treatment effects. Recent literature (de Chaisemartin & D’Haultfœuille, 2020; Goodman-Bacon, 2021) discusses potential identification problems in staggered difference-in-differences regressions with time and group fixed effects. The main issue is that the treatment effects are potentially heterogeneous across groups and over time (de Chaisemartin & D’Haultfœuille, 2020). Such heterogeneity is likely to cause bias when previously-treated units are used as a control group for newly-treated units and the treatment effect lasts over time. In our case, heterogeneity in the treatment effect across groups might exists because previously-treated properties were sometimes used as control properties in a later time period.

Alternative estimators have recently been developed to address the issue of heterogeneous treatment effects. We show that our baseline findings remain consistent and significant when we employ alternative estimators introduced by Callaway and Sant’Anna (2021) and Sun and Abraham (2021). Both of these alternative estimators are designed to be consistent in the presence of heterogeneous treatment effects across time periods and across treated units.

Table 6 shows that the outcomes obtained using these alternative estimators align qualitatively with our baseline results. As both models in Table 6 show, the coefficients are not significant before the treatment day, there is hence no significant difference between the control and the treatment group before the treatment, supporting the parallel trend assumption. Figure 4, which illustrates the results from the Sun and Abraham estimator, provides a visual representation of the impact. It is evident that the 1-day CAPM-adjusted return fell below zero on the day following the event.

Coefficients estimated from the Sun-Abraham estimator

Lastly, we conduct a robustness test regarding the parallel trend assumption. Traditionally, this assumption’s plausibility is evaluated by testing for pre-treatment differences in trends. However, recent research has indicated that such pre-trend tests might suffer from low power (Roth 2022; Freyaldenhoven et al., 2019). Hence, to better assess the parallel trends assumption in our study, we implement the “honest approach” to parallel trends proposed by Rambachan and Roth (2023). Specifically, we examine parallel trend violations arising from differential secular trends (i.e., long-run trends that evolve smoothly over time) between the treated and control units. We do a sensitivity analysis on smoothness restrictions by imposing that the slope of differences in trends changes by no more than M between periods. We plot confidence sets that allow for linear violations of parallel trends and larger non-linear deviations in Fig. 5 with the robust confidence sets for the treatment effect of Covid-19 proximity on 1-day AR at t = 1. When we allow for a linear violation of parallel trends (M = 0), the confidence set is smaller than that of the original treatment effect estimate. However, as we permit larger, non-linear violations, these confidence sets widen. For values of M < 0.00047, the effect is negative and statistically significant. As the breakdown value for a significant effect is M \(\approx\) 0.00047, we can reject a null effect.

Smoothness sensitivity analysis for effect of Covid-19 proximity. Note: See Rambachan and Roth (2023) for a detailed explanation on the parameter M

Conclusion

Using a novel dataset of the roadmaps of Covid-19 cases for Hong Kong, this study is the first to examine the spatial effects related to the proximity of property holdings of real estate firms to Covid-19 cases on company's stock performance. We demonstrate a monotonic inverse relationship between distance to Covid-19 cases and returns of affected companies. When distance decreases from 2 miles to 0.1 miles, the negative effect on returns intensifies. This suggests that investors account for spatial risks induced by the potential virus contagion effects and incorporate this information into their stock valuations. We identify the effects of Covid-19 by using a DID setting. We calculate the pair-wise distance between a Covid-19 case and a property owned by a listed real estate firm to form treatment and control groups. Our model controls for a host of fixed effects, including firm, district and time.

We present novel micro-level findings which are usually masked by aggregate estimates on the effects of Covid-19 on real estate companies’ performance. Having lived through the SARS pandemic, market participants in Hong Kong responded promptly by changing their behavior and staying highly alert about Covid-19 news. In addition, as we sampled the early days of the pandemic when case growth was not explosive, each individual infection received sufficient attention. This setting allows us to identify the causal effect of news about Covid-19 infections on real estate returns. We consider each infection as an exogenous shock to nearby located properties and observe how investors in real estate companies owning those properties respond to such information.

We document the following findings. Firstly, real estate companies with a property close to (within 0.1 miles) a Covid-19 case are associated with significantly lower returns one to three days following the case disclosure. The next-day return decreases by 0.23%. Given that the average firm in our sample has one billion US dollars in market capitalization as of the end of 2019, the exposure to a Covid-19 case is associated with a reduction in firm value by approximately 2.3 million US dollars on average. The 2-day and 3-day cumulative returns reduce by 0.71% and 1.13% respectively. Secondly, returns are more strongly affected the closer a property is to a Covid-19 infection. The next-day return of a firm holding a property between 2 and 0.1 miles of a Covid-19 case is between 0.02% and 0.23% lower respectively. Though the effects reported may appear small in absolute terms, in annual terms they are relatively large, with 16% lower annual return on treated real estate firms. Lastly, we show that when information channels are limited, such as for small stocks, news about Covid-19 proximity can have a stronger negative effect on returns.

Our study adds to the research on the spatial nature of idiosyncratic risks in asset pricing. We show that investors price in spatially distributed risks, such as the risk of a viral infection, regardless of the material effects on cash flows. We posit several explanations for the observed differential returns, linked to phycological factors. Nevertheless, we do not test for these as this is beyond the scope of this paper and this remains to be investigated in the future.

Notes

The official name for the virus that causes Covid-19 disease is “severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2)”. To distinguish it from the SARS, WHO has begun to refer to this virus as “Covid-19” when communicating with the public (see: https://www.who.int/emergencies/diseases/novel-coronavirus-2019/technical-guidance/naming-the-coronavirus-disease-(covid-2019)-and-the-virus-that-causes-it). This paper refers to the novel coronavirus as “Covid-19” as well, while the reference list contains papers that named the virus “SARS-CoV-2”.

The webpage is https://www.coronavirus.gov.hk/chi/ and it was created by the Hong Kong authority. The screenshots of the interactive map disclosing the Covid buildings are presented in Fig. A1. Later on, it was communicated through mobile app notifications powered by the Hong Kong authority.

Epidemiological research also indicates the possibility of fecal transmission of Covid-19 that causes disease outbreak in communities of high-rise buildings (Kang et al., 2020) – in line with a common feature of Hong Kong’s buildings. For example, a SARS investigation in Amoy Garden indicates the possibility of long-distance transmission of virus aerosols through the exhaust or sewage pipes in toilets (Zhang et al., 2020). News and media have covered people’s worrying concerns on the reoccurrences of such geographically-clustered mass infection in local communities. See https://www.bbc.com/zhongwen/simp/chinese-news-51455176 for the news (in Chinese).

The Hong Kong authorities did not stipulate a specific distance boundary which is regarded as unsafe in the early stages of the pandemic. We also look at proximity as a continuous variable to examine how the equity returns change with growing proximity to a Covid-19 case, and the results are consistent with our baseline findings in this paper but are not reported for brevity.

We set 5 miles as the boundary for defining a local market as this is the local-community-boundary indicated by some authorities in their pandemic distancing advice. Likewise, according to similar rationale derived from epidemiological perspective, this “5-mile” boundary is inspired by the “5-mile radius rule” stipulated by the Scottish government which define “the local community” as “broadly within 5 miles”. According to this rule, travelling further than 5 miles might spread the virus from one community to another (Scottish Government, 2020).

We use the S&P Global Real Estate Properties database to match buildings in Hong Kong dataset.

This is based on the average firm in our sample having roughly one billion US dollars in market capitalization as of the end of 2019.

There have been several real estate, finance and economics studies on Covid-19. For example, Hassan et al. (2020) use a text-based measure to capture the benefits, costs, and risks of firms exposed to the pandemic (Covid-19 and other infectious diseases like SARS and H1N1). Ramelli and Wagner (2020) demonstrate how shocks and financial policies drive firm value by examining indicators like debt and cash holdings of firms across the globe. Gormsen and Koijen (2020) use aggregate stock market data to capture investor’s response to Covid-19, and they show that dividend future is a useful tool to measure future economic trends during crisis and distress times. D’Lima et al. (2022) examine the effect of shutdown and reopening orders on residential real estate markets.

Available at: https://data.gov.hk/en-data/dataset/hk-dh-chpsebcddr-novel-infectious-agent (DATA.GOV.HK).

See: https://www.info.gov.hk/gia/general/202003/27/P2020032700817.htm (Chinese version). Our sample period ends at end of March given that there could be a 3-day window between the date the Covid-19 patient visits a building and the date that this building location disclosed to the public.

The definitions and sources of all variables are provided in Appendix 1.

In an ideal scenario, we would look at the equity performance of a listed real estate firm when a property in its portfolio becomes an infectious site. However, due to the inconsistency in how building information for both Covid buildings and properties owned by Hong Kong-listed real estate firms is reported, direct matching is not possible. Therefore, we are unable to directly monitor the effect on performance, when a property a real estate company owns become an infectious site. However, due to the density of Hong Kong and the short distance metric we use, our results are a good proxy of those effects. In addition, in the ideal scenario described above, we could have explored how the results vary each time a firm's real estate holding becomes an additional Covid-19 infectious site. We construct a new variable in the model for each firm to count the company's buildings that are within the 0.1-mile radius of a Covid-19 case on a given day. Given that our models are a good proxy of the ideal scenario, this new variable is akin to the number of infectious sites a firm owns each day. We then use this new variable to test how results vary each time a firm's real estate holding becomes an additional Covid-19 infectious site. The effects are not significant and hence are not reported here for brevity. This might be due to the psychological threshold effect and the binary approach to information overload at the beginning of the unprecedent disease outbreak.

We also exclude observations on the holidays of the Hong Kong stock exchange.

We omit the hyphen in tables and formulas in case being misread as a minus sign.

The number of patients is winsorized at the 1% and 99% levels and is the number of patients reported in a Covid-19 affected building per data entry.

The names of the 31 geographical regions are in accordance with the name of the districts provided by S&P Global Real Estate Properties dataset, and therefore could be different from the names in the conventional administrative division in Hong Kong (i.e. 18 districts).

Population density data is from the Census and Statistics Department of Hong Kong. We use 2019 population density for mapping.

The age is accounted by the year of 2020, i.e. 2020-construction year.

The exact time of the day that the authority releases the Covid-19 case information is uncertain. We therefore assume that investors react to the information on the next trading day. This also gives more time for news media to follow up with extensive coverage on case details. We exclude return observations on non-trading days. The non-trading days including weekend days and Hong Kong stock exchange holiday days. We conduct robustness estimations using 2-day or 3-day cumulative returns instead and the results are presented in the Robustness section. Overall, they remain robust.

This assumption is reasonable for listed real estate firms because they are subject to regulatory regimes and can only change the factors associated with their business and firm characteristics slowly; this is also the case, as we have a relatively short sample period.

These firm characteristics include CAPM beta, leverage, EBITDA/TA (the ratio of earnings before interest, taxes, depreciation, and amortization to total assets), and the percentage of institutional ownership.

In the robustness section, we replace the firm fixed effects with a set of firm-level explanatory variables to examine how firms with different characteristics perform when their underlying assets are close to Covid-19 cases.

In a 2023 interview with residents and members of the residential committee of Amoy Garden, it was disclosed that the area has acquired the moniker "SARS village." Notably, tourists have formed groups to tour Block E of Amoy Garden, which was identified as the most severely affected. The interview can be accessed at: https://www.bbc.com/zhongwen/simp/chinese-news-65110786.

People worrying another Amoy-Garden-like mass infection occur. See the news at: https://www.bbc.com/zhongwen/simp/chinese-news-51455176.

The authors attribute above results to local beliefs that unnatural deaths generate excessive negative energy, adversely affecting property value—a concept linked to Feng Shui principles.

The exact time that the authority releases the Covid-19 case information is unknown, we therefore assume investors immediately react on the next transaction day in the baseline model. In the additional robustness tests, we consider a delayed reaction.

References

Adams, Z., Füss, R., & Schindler, F. (2015). The sources of risk spillovers among U.S. REITs: Financial characteristics and regional proximity. Real Estate Economics, 43(1), 67–100.

Akinsomi, O. (2021). How resilient are REITs to a pandemic? The COVID-19 effect. Journal of Property Investment & Finance, 39(1), 19–24.

Alfaro, L., Chari, A., Greenland, A. N., & Schott, P. K. (2020). Aggregate and firm-Level stock returns during pandemics, in real time. NBER Working Paper, No.26950.

Ampountolas, A., Legg, M., & Shaw, G. (2023). Real estate investment trusts during market shocks: Impact and resilience. Tourism Economics. https://doi.org/10.1177/13548166231219740

Baker, S. R., Bloom, N., Davis, S. J., Kost, K. J., Sammon, M. C., & Viratyosin, T. (2020). The unprecedented stock market reaction to COVID-19. Review of Asset Pricing Studies, 10(4), 742–758.

BBC News. (2020). Coronavirus: Stock markets suffer worst quarter since 1987. https://www.bbc.co.uk/news/business-52113841. Accessed 28 March 2022.

Bertrand, M., Duflo, E., & Mullainathan, S. (2004). How much should we trust differences-in-differences estimates? Quarterly Journal of Economics, 119(1), 249–275.

Bhattacharya, U., Huang, D., & Nielsen, K. M. (2021). Spillovers in prices: The curious case of haunted houses. Review of Finance, 25(3), 903–935.

Callaway, B., & Sant’Anna, P. H. C. (2021). Difference-in-Differences with multiple time periods. Journal of Econometrics, 225(2), 200–230.

Chen, H., Qian, W., & Wen, Q. (2020). The impact of the COVID-19 pandemic on consumption: Learning from high frequency transaction data. SSRN Working Paper. https://doi.org/10.2139/ssrn.3568574