Abstract

Greenhouse gas emission reduction in the passenger transport sector is a main challenge for China’s climate mitigation agenda. Electrification and shared mobility provide encouraging options for carbon emissions reduction in road transport. Based on an integrated scenario-based assessment framework, a provincial-level projection is made for vehicle growth and CO2 emissions in China under shared socioeconomic pathways (SSPs). This work illustrates how passenger car electrification and sharing contribute to China’s “30·60” climate goals (peaking of CO2 emissions by 2030 and carbon neutrality by 2060). The results demonstrate that China is en route to achieving the goal of a 2030 carbon peak (1.0Gt CO2) under current conditions, and could reach peak emissions around 2026 with optimistic growth in EVs and shared mobility. Compared with no policy action, the single EV policy (shifting from ICEVs to EVs) can reduce 71% of emissions by 2060, thus narrowing but not closing the mitigation gap to carbon neutrality in passenger cars (302 Mt CO2). Shared mobility can provide further emission reduction support, reducing emissions by 83% in 2060. Comprehensive climate actions (including electrification, sharing mobility to reduce car use, and improving vehicle efficiency and fuel carbon intensity) are needed to achieve deep decarbonization to net-zero by 2060 in the passenger transport sector.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

China’s climate targets—peaking of CO2 emissions by 2030 and carbon neutrality by 2060—are an important step for global-scale climate change mitigation and planetary health. The transport sector is a key and growing emissions source, accounting for 9% of total emissions in China in 2019, largely due to passenger cars (Xue et al. 2022). The rapid growth in both passenger car stock and carbon emissions necessitates effective strategies for emission reduction.

Electric vehicles (EVs) are currently the most widely discussed solution for decarbonizing urban transportation (Hill et al. 2019; Wolfram et al. 2021). To execute strategies toward carbon neutrality in the transport sector, many studies have applied a multiple-scenario approach to make flexible EV development policy on energy consumption and emissions in China (Peng et al. 2021; Zhang and Hanaoka 2021; Chen et al. 2022; Fang et al. 2023; Shen et al. 2023). Based on an integrated modeling framework, Fang et al. (2023) demonstrate that electrification of the passenger fleet, which is charged by a slightly cleaner power source, yields significant co-benefits of CO2 reduction and air quality improvement. Shen et al. (2023) evaluated the CO2 reduction and health benefits with the banning of new sales of internal combustion engine vehicles (ICEVs) in the private vehicle sector in Chinese provinces, and found that if there were no carbon neutrality and air pollution control goals in electricity generation, 53% of CO2 reduction would be offset by the increased power demand and consequent carbon emission and health damage in 2050.

However, the introduction of EVs alone is insufficient to reach ambitious climate targets (Zhang and Fujimori 2020; Milovanoff et al. 2020). Although many studies reflect the huge potential of electric vehicles to reduce emissions in the transport sector, they have not yet taken into account issues like production emissions and materials demand of EVs under the scenario where a large number of EVs replace ICEVs caused by vehicle growth. Betting solely on EVs to remain within suitable sectoral CO2 emission budgets for the US light-duty vehicle (LDV) fleet would imply more than 350 million on-road EVs in 2050, requiring an excessive amount of critical materials (Milovanoff et al. 2020). Hence, the question that must be addressed remains not only limited to the consistency of climate mitigation strategies building on electrification in the land transport sector, but also going beyond that.

Replacing ICEVs with EVs is just one of the common methods (Avoid-Shift-Improve options) in achieving emissions reduction from the passenger car sector (Bongardt et al. 2013; Creutzig et al. 2018). Another important strategy is shifting travel demand to the lowest-carbon mode, such as cycling and using shared mobility by restricting the sales of vehicles (Yi and Yan 2020; Arbeláez Vélez and Plepys 2021; Hu and Creutzig 2021). Sharing vehicles can improve both vehicle usage efficiency and occupancy, thus reducing the overall number of cars while maintaining mobility improvement (Creutzig 2021). Especially, electric shared vehicles and shared bikes have been proven to have significant emission reduction potential (Ding et al. 2019; International Transport Forum 2020; Yi and Yan 2020; Creutzig 2021). Combining the growth of shared mobility with electrification and optimizing climate strategies to reduce vehicle carbon emission may hence improve the chances of decarbonizing land transport early. Unfortunately, the emission reduction potential of this comprehensive strategy is currently unclear. Furthermore, to our best knowledge, the emission reduction potential of shared mobility in different provinces has not been explicitly explored in any previous studies.

To address the abovementioned knowledge gaps, this study develops a scenario-based assessment framework to provide extensive analysis on the policy mix of the “Shift” (i.e., to reduce car stock by providing high-quality shared mobility) and “Improve” (i.e., vehicle technology from ICEVs to EVs) strategies to achieve deep decarbonization in the passenger transport sector of China. Specifically, the research addresses three pivotal subquestions: (1) How much can EV development policies reduce emissions if their production emissions are taken into account? (2) Can shared mobility complement EVs to further enhance emission reductions in China’s passenger transportation sector? (3) What regional variations in CO2 reduction can be attributed to EV and shared mobility policies across different provinces? The model results could help achieve maximum emission reductions with a more comprehensive policy perspective.

2 Methodology and data

2.1 Model overview

This work aims to develop a scenario-based assessment framework of the passenger car fleet, taking shared socioeconomic pathways (SSPs) as a starting point. Figure 1 illustrates the general modeling process and main exogenous inputs. The evaluation framework consists of 3 main modules: fleet estimation, CO2 emission assessment, and scenario analysis. The fleet module simulates the annual car stocks. An extended Gompertz model is used to estimate future passenger car stock of 31 provinces in China (Dargay et al. 2007). The CO2 emission model quantifies the direct and indirect emissions (i.e., vehicle manufacturing, fuel production, and fuel use) for EVs and ICEVs. Finally, three main scenarios are built to evaluate policy tool effects. On the basis of these results, the carbon emission of passenger cars in China from 2010 to 2100 is evaluated at the provincial level.

Flow chart of the model estimation process

2.2 Socioeconomic framework

The shared socioeconomic pathways (SSPs) are used to quantify socioeconomic components, such as GDP, population, and urban share. The SSPs represent five global development pathways, describing the future evolution of key aspects of society that would together imply a range of challenges for mitigating and adapting to climate change (Riahi et al. 2017; Kasera et al. 2016). SSPs have been widely used in forecasting future energy demand and GHG emissions (Xing et al. 2015; Milovanoff et al. 2020; Wolfram et al. 2021). The five global development pathways are SSP1 (Sustainability), SSP2 (Middle of the Road), SSP3 (Regional Rivalry), SSP4 (Inequality), and SSP5 (Fossil-fueled Development). A brief description of SSP1-5 is shown in the supplementary information (Table S1). The SSP database only provides national-level economic forecast data. China’s provincial GDP data is from Jiang et al. (2018), the population data is from Jiang et al. (2017), and the urbanization rates data is from Chen et al. (2020). We briefly show the changes in population and urbanization rates under SSPs in the supplementary information (Table S2 and Fig S1). As mainly referenced, we use SSP1, which is regarded as the most sustainable path among all SSPs, to then demonstrate the differential impact of passenger cars and carbon emissions in three scenarios (BAU, EV, and SEV—see Fig. 1).

2.3 Fleet module for total vehicle ownership

In the “fleet” module, we developed a demand-based extended Gompertz function to simulate car stocks retrospectively (1995–2019) and prospectively (2020– 2100) for 31 provinces in China. The historical data (such as passenger car ownership, car sales, GDP, and population) are from national statistics (National Bureau of Statistics of China 2020) and the China Automotive Technology And Research Center (CATARC 2020).

The traditional Gompertz function (Eq. (1)) is widely applied to measure the S-shaped relationship between vehicle ownership and per-capita income (Dargay and Gately 1999; Dargay et al. 2007; Zheng et al. 2015; Zeng et al. 2016; Ma et al. 2019). Compared to other more intricate models such as Dynamic Simulation (Levin et al. 2017) or Linear Programming (Jones and Leibowicz 2019; Zhang et al. 2022) which offer greater flexibility in handling diverse factors but with greater data and computational intensity requirements, the Gompertz function can simply facilitate a clearer understanding and provide vehicle ownership prediction trends based on economic conditions, proving valuable for policymakers and stakeholders who may not have an extensive technical background (Shen et al. 2023). Further, the Gompertz function allows for the adjustment of parameters to match the unique characteristics of each region.

where \({V_{it}}\) is the vehicle ownership (per 1000 people) in province i in year t, \({GDP}_{it}\) is the GDP in province i in year t, \(\gamma\) > 0 is the saturation level, and \(\alpha <0\) and \(\beta <0\) are parameters defining the shape of the curve.

Figure 2 shows passenger car ownership per thousand people based on China’s national and provincial GDP per capita from 1995 to 2019. The passenger car ownership is around 109–250 per thousand people in 2019. The passenger car ownership in areas with good economic development such as Beijing and Zhejiang is significantly higher than that of other provinces such as Gansu and Jiangxi, major destinations for migrant workers in the west. For example, while the passenger car ownership in Zhejiang is 249 vehicles per thousand people, Gansu has the lowest car ownership rate, with only 109 vehicles per thousand people. Due to the strict vehicle purchase limitation policy, there is a flattening of the curve in Beijing, Tianjin, and Shanghai. However, most provinces in China are still in the initial stage of the “S shape,” which means that the passenger car stock will continue to grow. The differences between different provinces are obvious.

Passenger car ownership per thousand people based on GDP per capita from 1995 to 2019. Note GDP per capita is in PPP (constant 2005 international $)

As acknowledged, the conventional Gompertz function is limited to capturing the long-term correlation between vehicle ownership and per-capita income, while lacking the capacity to depict the dynamics of new vehicle sales and retirements. We are actively addressing this concern in the formulation of our Gompertz model. Firstly, following Dargay et al. (2007), we built an extended Gompertz function that explicitly models the vehicle saturation level as a function of observable country characteristics: urbanization and population density. Although there are many other factors that influence the modal shift on the usage of cars such as travel patterns and driver characteristics, such factors are difficult to take into account as they would require more data that are mostly unavailable for all provinces. Then, we postulated a simple partial adjustment mechanism in the econometric model to quantify the short-term relationship between the current period’s vehicle count and that of the preceding period (Eq. (2)). In this way, we used demographic and economic data to reassess vehicle production and usage from the demand side. We verified the validity and reliability of the extended Gompertz function and related parameters by comparing predicted values and historical data in the supplementary information (Fig S2-S3).

where adjustment parameters θR > 0, θF > 0, \(\alpha <0\), \(\lambda <0\), and \(\varphi <0\) are constrained to be the same for all provinces, while \({\beta _i}\) < 0 is allowed to vary across provinces. Based on the provincial historical data in China and iterative least squares regression coefficients, we obtain parameters as shown in the supplementary information (Table S3–S4). \({V_{it}}\) is the vehicle ownership (in numbers per 1000 people) in province i in year t.We assume that the maximum saturation level (\(\gamma_{max}\)) will be that estimated for Beijing because other provinces are less urbanized and less densely populated than Beijing. Under the government policy of restricting car purchases, research generally estimated that the saturation level in cities such as Beijing, Shanghai, or Tianjin will be approximately 250–400 (Zeng et al. 2016; Zheng et al. 2015; Gan et al. 2020; Huo and Wang 2012). In this study, we assumed \(\gamma_{max}\) to be 400 vehicles per 1000 people in Beijing. Furthermore, the saturation level in other provinces can be calculated according to the difference in the population density and the level of urbanization from Beijing (Eq. (3)

where \(\overline {{{D_{it}}}}\) is the population density and \(\overline {{{U_{it}}}}\) is the level of urbanization.

Income asymmetry (i.e., many provinces have experienced negative as well as positive GDP per-capita growth over the period) is taken into consideration in the extended Gompertz function in Eq. (2) as \({\theta _R}{R_{it}}+{\theta _F}{F_{it}}\) (Dargay et al. 2007) where θ = θR for income increases and θ = θF for income decreases. Rit and Fit are shown in Eq. (4):

2.4 Scenarios settings for EV and shared mobility

Three main scenarios for passenger car fleet are developed to evaluate the impact of two policy tools (i.e., shift to EVs and reduce car stock with shared mobility) on decarbonizing the passenger transport sector of China. Table 1 presents their descriptions. Specific details about the scenarios are shown in the supplementary information (section SI4).To ensure the robustness of the scenarios, we carry out a sensitivity analysis (from 2030 to 2050) because the prohibition time of fuel vehicles has a high degree of uncertainty in various provinces.

3 GHG emissions

3.1 On-road CO2 emissions

On-road CO2 emissions from EVs and ICEVs are determined by car stock, traveled distance, and carbon emission factors. The on-road CO2 emissions can be calculated by Eq. (5).

where \(C{O_2}_{usage}\) is the on-road CO2 emissions for passenger cars. i stands for province i. j stands for vehicle type j (\(j=\left\{ICEV, EV\right\}\)). VKT represents the vehicle kilometers (km) traveled. VKT is an important parameter reflecting vehicle usage. The VKT of provinces in China in 2015 are from Liu et al. (2017). Due to the unavailability of provincial-level VKT time series data, we use the national average growth rate of VKT to calculate the future VKT of passenger vehicles in each province. According to Huo et al. 2012; iCET 2018; and Zhang 2024, the annual VKT of private passenger vehicles in China has decreased from 12,489 to 11,660 km between 2015 and 2020 with an average annual decrease rate of 0.93%. We further estimate the VKT of ICEVs and EVs at the provincial level based on the provincial vehicle ownership level, as shown in the supplementary information (Fig. S4). Importantly, the effect of shared mobility on VKT is complex, which depends on many factors such as the substitution of public versus private transport modes and the occupancy rate of substituted modes. Limited researches analyze the changes in VKT for shared mobility (Narayanan et al. 2020). We have compiled some of the related studies and displayed them in the supplementary information (Table S5). Shared mobility fleets are predicted to generate an additional 10~20% of travel miles (VKT/VMT). To account for this uncertainty, we set two different growth rates (10% and 20%) in the VKT of shared mobility (Fig. S5).

EMF represents the emission factors (g CO2/km). While driving, EVs emit CO2 emissions from electricity generation and ICEVs emit CO2 emissions from fuel production and fuel consumption. The detailed information on the calculation of on-road CO2 emissions is summarized in the supplementary information (section SI5).

3.2 CO2 emissions from vehicle production

The specific greenhouse gas (GHG) emission reduction potential of electric vehicles not only depends on the carbon intensity of electricity usage, but also on the production process of vehicles. In determining vehicle emissions, it is important to consider not only direct emissions during vehicle use, but also implicit emissions resulting from vehicle production. Vehicles generate massive indirect emissions during the manufacturing stage in the industry sector (Hill et al. 2019; Milovanoff et al. 2021). The exact GHG emissions from the production phase of an EV are about 13.0 t CO2eq, 24% larger than those of an ICEV (10.5 t CO2eq) in China in 2015 (Qiao et al. 2019). This part of the emissions may limit the emission reduction potential of EVs. The CO2 emissions from production will be given by the number of new vehicles produced as shown in Eq. (6).

where \(C{O_2}_{production}\) is the CO2 emission of passenger vehicle production in province i and vehicle type j. VP represents new vehicles produced. The detailed information on the calculation of vehicle production CO2 emissions is summarized in the supplementary information (section SI 5.7).

Total CO2 emission incorporates production and usage emissions as shown in Eq. (7).

4 Results

4.1 Car stock and CO2 emission

4.1.1 Passenger car stock

We verified the validity and reliability of the extended Gompertz function and related parameters by comparing predicted values and historical data, which are shown in the supplementary information (Fig. S2 and S3). The results show that the predicted passenger car stock has good convergent validity and is reliable.

The passenger car stock in China is expected to grow before 2050 driven by increasing population and higher incomes. Figure 3a shows passenger car stock in China from 2010 to 2100 in three scenarios under SSP1. The passenger car stock will reach its peak of about 500 million vehicles around 2050 in the BAU scenario. Total car stock in the EV scenario is similar to the BAU scenario because EVs are used as alternatives for ICEVs to meet passenger travel demand. Passenger car stock dynamic in the SEV scenario is slower and muted compared to other scenarios. In the SEV scenario, the car stock will reach its peak at 410 million in 2037 and then decline to 214 million in 2060 under SSP1. The results show that shared mobility reduces vehicle use effectively. Shared mobility not only limits the maximum saturation level of passenger cars, but also slows the growth rate of new vehicles.

Passenger car stock and total CO2 emissions in China from 2010 to 2100 in three scenarios under SSP1 with decarbonization. a Passenger car stock in three scenarios under SSP1 with decarbonization. b Total CO2 emissions in three scenarios under SSP1 with decarbonization. Note: The shaded area reflects the error interval under SSPs (95% CI)

4.1.2 CO2 emission

Figure 3b shows the total CO2 emissions of passenger cars in China from 2010 to 2100 in the three scenarios considered. In all scenarios, CO2 emissions peak around 2030. In the BAU scenario, total emission peaks at 1045 Mt CO2 in 2032. In the EV scenario, total emission peaks at 980 Mt CO2—6 years earlier (2026). In the SEV scenario, total emission peaks at 963 Mt CO2 in 2026. The rapid and large-scale promotion of EVs and shared mobility accelerates the peak time and magnifies the reduction of carbon emissions in the passenger transport sector.

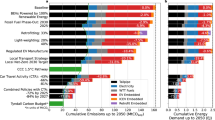

Shift to EVs and shared mobility also contribute to deep decarbonization and carbon naturality target in China. Within the three scenarios, there is varying decline in passenger transportation emissions. In the BAU scenario, the CO2 emission of passenger cars decreases to 643 Mt CO2 (a 38% reduction) by 2060 accounting for continuous decline in fuel carbon intensity. Sharp increase of EVs, mainly fueled by low-carbon electricity, speeds up the decarbonization process. The CO2 emission from passenger cars fall faster in the EV scenario than in the BAU scenario. By 2060, passenger car emission falls to 302 Mt CO2 in the EV scenario (a 71% reduction). The residual emissions are coming from the EV production emissions and usage, reflecting that the grid will still have residual carbon emissions. These results imply that EV promotion alone is insufficient to achieve carbon neutrality in the passenger transport sector. In order to reach near-zero emissions, a large number of carbon sinks or negative emissions technology are still necessary for these two scenarios. Shared mobility can significantly reduce carbon emissions by decreasing the use of passenger cars. Under the SEV scenario, the passenger transportation sector is expected to further cut GHG emissions by two-fifth (181 Mt CO2 in 2060). To achieve the same emission reduction, the total number of vehicles in the shared mobility scenario (SEV) has to be less than half of that in the EV scenario, which will greatly reduce vehicles material demand. Hence, carbon neutrality in the passenger transport sector would rely on a comprehensive climate policy (including electrification, sharing, and rapid replacement of coal and gas power plants with renewables) that maximizes the benefits of emission reduction. To strengthen the role of shared pooled mobility in the Chinese transport sector, we provide a figure that shows the contributions to emission reduction of different factors (Fig. 4). Figure 4 also intuitively shows the emission reduction contributions of different policy mix.

The contributions to emission reduction of different factors

4.1.3 Sensitivity analysis

Figure 5 further alters three key variables to test the robustness of the results. The first assumption is on the share of EV sales to total vehicle sales. Current results are under the assumption that the share of EV sales reach 100% in 2030. Despite Hainan province’s proposal to ban the sale of fuel vehicles from 2030, there is much uncertainty about when ICEVs will be delisted in other provinces of China. Figure 5a shows the influence of different electric vehicle development speed. Delaying the ban on the sale of fuel vehicles will increase the emission peak and delay the peak time of emissions in the passenger transport sector.

The sensitivity analysis of different factors on the CO2 emissions: a the year of complete banning of ICEV sales (100% EVs in 2030 ~ 2050), b the maximum saturation level (γmax = 100 ~ 300), c the share of shared mobility in 2060 (60~100%)

The second assumption is on the maximum saturation level (γmax). The maximum saturation level in shared mobility is also highly uncertain. The maximum saturation level determines the upper limit of the total vehicle stock which further limits the reduction potential of total vehicle emissions. Figure 5b shows the difference in total emission with different γmax—demonstrating the high influence of this parameter. In the SEV scenario, in 2060, emissions are 19% and 52% lower when γmax = 200 and γmax = 100, respectively, compared to the case of γmax = 250.

The last assumption is on the proportion of cars shared. The sensitivity analysis results for the share of shared mobility align with our expectations (Fig. 5c). The greater the extent to which shared mobility replaces EVs and ICEVs, the larger the potential for emissions reduction.

4.1.4 Vehicle emission and production emission

GHG emissions originate not only in vehicle use, but also in production. Figure 6 shows the usage emission and production emission of ICEVs and EVs in China from 2010 to 2100 in the EV scenario. The vehicle emission of EV falls to zero by 2060 in SSP1 with decarbonization due to significant electricity grid decarbonization for carbon neutrality. We also compared emissions under different grid decarbonization scenarios in the supplementary information (section SI5.2). The degree of grid decarbonization has a significant impact on EV road emissions. However, from the perspective of life-cycle emissions, there is less impact on total emissions (supplementary information, Fig S8).

Figure 6 shows that a large-scale promotion of EVs will increase their production-related emissions, limiting their carbon emission reduction potential. This leads to an increase in the peak emissions of passenger cars in the EV scenario. In the initial stage of the rapid development of EVs, the increased emissions from EV production outweigh the emissions reduced by the usage shift from ICEVs to EVs. Moreover, the production emissions of EVs will still be around 248 Mt CO2 in 2060, and – by then – higher than their vehicle usage emissions. The results are based on the current changes in production emissionsFootnote 1. Taking this into account, the emissions from vehicle production will be higher than the emissions from vehicles driving on the road in the future due to faster-working electricity decarbonization. If production emissions were excluded from the three scenarios, an accelerated shift from ICEVs to EVs would result in greater emissions reduction benefits. Therefore, improving vehicle efficiency and decrease carbon intensity in the EV production is crucial when upscaling EV production.

ICEV and EV carbon emission in China from 2010 to 2060 in the EV scenario under SSP1 with decarbonization

4.1.5 EVs required

The Chinese government started a new energy vehicle (NEV) subsidy plan to promote the development of NEVs in 2009. Over the last decade, electric vehicles across all transport modes were increasingly adopted. Up to now, China’s EV stock has exceeded 5.5 million, accounting for 48% of the global EV stock in 2020 (IEA 2021). Figure 7 briefly analyzes how electric vehicles penetrate the passenger car market. Under the EV scenario, 500 million EVs would need to be on the road of China in 2050 to achieve maximum emission reduction in 2060 (Fig. 7a)—up to 94% of the total passenger cars (Fig. 7b). Attaining this EV share would require up to 210 million EVs by 2030. China has set ambitious electric vehicle development goals. According to the New Energy Vehicle Industry Development Plan (2021–2035), the sales of NEVs will reach about 20% of the total new car sales in 2025 (currently 5%). Pure electric vehicles will become the majority of new vehicle sales in 2035 (State Council Information Office of the People’s Republic of China 2020). These policies will contribute to reduce the emissions in the passenger transport sector. However, although the development of EVs can help reduce emissions, the total number of vehicles is not decreasing fast enough. This means that cities will still face restrictions on space for recreation, play, and parking places. Shared cars can offer door-to-door transport, and replace up to three-quarter of car trips, which is a good complement to the sustainable development of the city.

ICEV and EV stocks in China from 2010 to 2100 under the EV scenario. a On-road fleet stock, b EV share

4.2 Province level results

There will be a significant increase in the demand for passenger vehicles in all provinces over the next few decades. The model results show two main characteristics of future changes in passenger cars in China. First, there are strong regional differences. Figure 8 shows the change of provincial passenger vehicle stock in the BAU scenario under SSP1. The numbers of passenger cars in the southeast coastal provinces are significantly higher than those of other regions, especially in Shandong and Guangdong, where the numbers of passenger cars have exceeded 20 million in 2020. Further, vehicle ownership in various provinces continued to rise in the BAU scenario. By 2060, there will be 9 provinces with more than 20 million passenger cars (i.e., Jiangsu, Zhejiang, Shandong, Henan, Hebei, Guangdong, Sichuan, Anhui, and Hunan), most of which will be located in the southeast coastal areas. The demand for passenger cars in these regions is based on larger population and higher economic turnover. Special attention should be paid to provinces such as Guangdong, Henan, and Hunan. These provinces not only have large stocks, but also display strong dynamic increase.

Provincial passenger car stocks in the BAU scenario under SSP1

However, although China is the largest EV market in the world, the EV industry in the provinces has just started. The CO2 emissions from passenger cars, EV stocks, and EV shares in 31 provinces are shown in Fig. 9. In provinces where vehicle ownership continues to grow, EV development is still very slow at this stage. Guangdong and Shandong are the top 2 highest emission releasers in passenger cars with more than 80 Mt CO2 in 2020 (Fig. 9a). Although their EV holdings are also higher than other provinces (Fig. 9b), the share of EVs is only 1−2% of their total passenger cars (Fig. 9c). The EV scenario is far away from current trends. In the EV scenario, we assume that the EV sales shares in 31 provinces in China will reach 100% in 2030, which is the most optimistic policy scenario. According to the current EV market penetration, electric vehicles need to be heavily promoted in all provinces over the next ten years. The EV share of passenger cars in Shanghai, Beijing, Tianjin, and Hainan is more than 4%, while other provinces’ numbers are below 2% (Fig. 9c). These four provinces can be used as pilot provinces for banning the sale of ICEVs.

CO2 emission from a passenger cars, b EV stock, and c EV share in 31 provinces in 2020

Figure 10 displays provinces’ passenger transport sector emission in 2030 and 2060 under three scenarios. From the perspective of passenger vehicle emissions, provinces differ greatly in their emissions. The south-eastern provinces, which still have a high demand for vehicles, have significantly higher emissions than other provinces. Guangdong will be the highest passenger car emission producer in China with 86 Mt CO2 by 2030 under the BAU scenario, which is 39 times that of Tibet (2.2 Mt CO2). Figure 10 clearly shows that EVs and shared mobility can effectively reduce emissions from passenger transport in various provinces. In Guangdong province, GHG emissions will fall to 55 Mt CO2 by 2060 under the BAU scenario. Under the EV and SEV scenarios, it will further reduce emissions by 72% and 83%, respectively. Overall, south-eastern provinces will benefit more from the development of EVs and shared mobility. They have higher potential in reducing emission levels.

Provincial CO2 emission from passenger transport in 2030 and 2060 in three scenarios under SSP1 with decarbonization

5 Discussion and conclusion

5.1 Implications for China’s “30·60” goals

China is expected to achieve 2030 carbon peak from passenger cars under the BAU scenario with 1.3 Gt CO2 in SSP1 with decarbonization (sustainable path). Large-scale shift with the EV promotion can advance passenger car emissions to peak around 2026. However, EVs will not provide a solution for near-term CO2 mitigation because EVs cannot significantly reduce peak emissions.

Deep decarbonization to net-zero by 2060 in the passenger transport sector of China is easier with a comprehensive climate policy (including electrification, sharing mobility to reduce car use, and improving vehicle efficiency and fuel carbon intensity) instead of a single EV policy. The single EV policy (shift ICEVs to EVs) can reduce GHG emissions by 71% in 2060. There are still 302 Mt CO2 of emissions that need to be resolved by carbon sinks or negative emissions technology. If electric vehicles are also shared, GHG emissions will be reduced by 83% in 2060 compared to the BAU scenario. The SEV scenario explores the extreme setting of a case when all private trips change to shared trips, a fairly optimistic assumption. In contrast, the scenarios assume conservative values in decarbonization of the electricity grid. One interpretation is that combined intermediate shared mobility and electrification strategies can achieve between 71 and 83% GHG emission reductions between 2020 and 2060 on their own (around 302 Mt CO2 to 181 Mt CO2 left by 2060). More aggressive phase out of coal and scale up of renewable energy could then support the decarbonization of the residual emissions. Importantly, because of reduced demand for transport sector electrification, additional energy demand can be more easily covered by renewable energy sources (Creutzig et al. 2021; p. 1).

Additionally, analysis shows that variation of SSP has little implication for mitigation scenarios (supplementary information, Fig. S12–S13). Specifically, variation in SSPs results in GHG emissions varying little in either the BAU or mitigation scenarios (maximally 15% in 2060). Introducing technological (EV) and mobility system change (SEV) is responsible for the impactful change in GHG emission trajectories.

5.2 Shift to EVs

How fast can transport electrification and shared mobility contribute to China’s “30·60” goals depends on their share in total passenger car market. Without limiting the number of vehicles, 500 million EVs would need to be on the road in China in 2050 to achieve max emission reduction in 2060, up to 94% of the total passenger cars, a considerable challenge. In addition, the emission reduction potential in the large-scale promotion of EVs is limited due to higher production-related emissions. Improving vehicle efficiency and carbon intensity in EV production should be the basis for the large-scale promotion of EVs. Also, the increase in power consumption caused by the development of EVs has an impact on the power system. This will also put substantial pressure on the power system. Additional electric vehicle growth could result in substantial material concerns. Milovanoff et al. (2020) estimated that 8% and 29% of the identified world terrestrial resources of lithium and cobalt, respectively, would be needed for the USA alone to achieve its climate goals by electrification. China has a larger passenger car system, meaning that replacing ICEVs with EVs will require more resource consumption. Therefore, the reduction in the passenger car ownership and usage is still critical to reduce their carbon emissions. The development of shared mobility can reduce the vehicle required for emission reduction, which will greatly reduce vehicle material demand.

5.3 Province level solutions for climate change

Electric vehicles and shared mobility can effectively reduce carbon emissions from passenger transport in various provinces. In terms of regional differences, passenger car stock and carbon emission in the southeast coastal provinces is higher than those of other regions under all scenarios. At the same time, they also have higher potential in reducing emission levels. Currently, most provinces have a very low EV share (generally below 2%). The electric vehicle industry will still be in a stage of rapid development in the next decade. In addition, affected by the performance of EVs, it is difficult to use EVs in cold regions (Heilongjiang, Jilin, Liaoning) and western regions (Gansu, Qinghai, Ningxia). The provincial promotion in EVs will hence be an important research topic. The EV share of passenger cars in Shanghai, Beijing, Tianjin, and Hainan is higher. These four provinces can be used as first pilot provinces in banning the sale of ICEVs.

6 Conclusion

We build a scenario-based assessment framework for China’s provincial-level projection of passenger vehicle growth and CO2 emissions under shared socioeconomic pathways (SSPs). The results indicate that the single EV policy (shift ICEVs to EVs) can only reduce emissions by 71% in 2060 but that the SEV (shared EVs) scenario achieves almost 83% mitigation. Both scenarios presuppose improved vehicle efficiency and reduced carbon intensity in the EV production and rapid upscaling of low-carbon renewable power. China’s provincial difference in passenger vehicle stocks and emission release show that the southeastern coastal provinces are huge polluters, but also suitable for advancing EV production. Together, these results demonstrate the importance of fostering rapid technological change hand-in-hand with a reorganization of motorized mobility towards shared pooled transport.

This work is not without limitations. The conclusions are dependent on a large series of assumptions on model parameters and input data, including the share of EV sales, maximum saturation level in car ownership, and carbon intensity. Although settings in this work are based on historical data and related studies, the results in the sensitivity analysis show the uncertainty of these parameters. A large-scale shift to electric vehicles and shared mobility depends on the provision of infrastructure, whose construction will include its own CO2 footprint. Due to the current diversity in types and forms of automotive batteries, coupled with rapid technological iterations, obtaining some uncertain parameters such as battery life and replacement has become extremely challenging. Although this part of the emissions is beyond the scope of this work, they will require more attention when developing future EV and shared mobility policies.

Data availability

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.

Notes

Emission factors are calculated based on the 2015–2020 annual average decline rate of 12 t CO2eq/vehicle in 2020 and extrapolated to 6.3 t CO2eq/vehicle in 2060. Taking into account the latest data currently available, we have made this assumption on the production emission factor. Note that the current assumptions are conservative.

References

Arbeláez Vélez AM, Plepys A (2021) Car sharing as a strategy to address GHG emissions in the transport system: evaluation of effects of car sharing in Amsterdam. Sustainability 13:2418. https://doi.org/10.3390/su13042418

Bongardt D, Creutzig F, Hüging H et al (2013) Low-carbon land transport: policy handbook. Routledge, Abingdon

CATARC (2020) China Automobile Low Carbon Action Plan (CALCP) 2020 Research Report. China Automotive Technology And Research Center Co., Ltd

Chen W, Sun X, Liu L et al (2022) Carbon neutrality of China’s passenger car sector requires coordinated short-term behavioral changes and long-term technological solutions. One Earth 5:875–891

Creutzig F (2021) Making smart mobility sustainable. https://www.ippi.org.il/making-smart-mobility-sustainable/. Accessed Feb 2021

Creutzig F, Roy J, Lamb WF et al (2018) Towards demand-side solutions for mitigating climate change. Nat Clim Change 8:260–263. https://doi.org/10.1038/s41558-018-0121-1

Creutzig F, Hilaire J, Nemet G et al (2021) Climate change mitigation easier than suggested by models 1. Earth Space Sci Open Arch 17. https://doi.org/10.1002/essoar.10506825.1

Dargay J, Gately D (1999) Income’s effect on car and vehicle ownership, worldwide: 1960–2015. Transp Res Part Policy Pract 33:101–138. https://doi.org/10.1016/S0965-8564(98)00026-3

Dargay J, Gately D, Sommer M (2007) Vehicle ownership and income growth. Energy J 28:143–170

Ding N, Pan J, Zhang Z, Yang J (2019) Life cycle assessment of car sharing models and the effect on GWP of urban transportation: a case study of Beijing. Sci Total Environ 688:1137–1144. https://doi.org/10.1016/j.scitotenv.2019.06.111

Fang YR, Sun X, Zhang S et al (2023) Regionally differentiated promotion of electric vehicles in China considering environmental and human health impacts. Environ Res Lett 18:074022

Gan Y, Lu Z, Cai H et al (2020) Future private car stock in China: current growth pattern and effects of car sales restriction. Mitig Adapt Strateg Glob Change 25:289–306. https://doi.org/10.1007/s11027-019-09868-3

Hill G, Heidrich O, Creutzig F, Blythe P (2019) The role of electric vehicles in near-term mitigation pathways and achieving the UK’s carbon budget. Appl Energy 251:113111. https://doi.org/10.1016/j.apenergy.2019.04.107

Hu J-W, Creutzig F (2021) A systematic review on shared mobility in China. Int J Sustain Transp 1–16. https://doi.org/10.1080/15568318.2021.1879974

Huo H, Wang M (2012) Modeling future vehicle sales and stock in China. Energy Policy 43:17–29. https://doi.org/10.1016/j.enpol.2011.09.063

Huo H, Zhang Q, He K et al (2012) Vehicle-use intensity in China: current status and future trend. Energy Policy 43:6–16. https://doi.org/10.1016/j.enpol.2011.09.019

iCET (2018) 2018 new data analysis on real-world driving and fuel consumption for passenger cars in China. The Innovation Center for Energy and Transportation (iCET)

IEA (2021) Global EV outlook 2021. IEA, Paris

International Transport Forum (2020) Assessing the environmental performance of new mobility

Kasera J, O’Neill J, Bidwell N J (2016) Sociality, tempo & flow: Learning from Namibian ridesharing. Proceedings of the First African Conference on Human Computer Interaction 36–47

Jiang T, Zhao J, Cao L, et al (2018) Projection of national and provincial economy under the shared socioeconomic pathways in China. Clim Change Res 14:50. https://doi.org/10.12006/j.issn.1673-1719.2017.161

Jones EC, Leibowicz BD (2019) Contributions of shared autonomous vehicles to climate change mitigation. Transp Res Part Transp Environ 72:279–298. https://doi.org/10.1016/j.trd.2019.05.005

Levin MW, Kockelman KM, Boyles SD, Li T (2017) A general framework for modeling shared autonomous vehicles with dynamic network-loading and dynamic ride-sharing application. Comput Environ Urban Syst 64:373–383. https://doi.org/10.1016/j.compenvurbsys.2017.04.006

Liu H, Man H, Cui H et al (2017) An updated emission inventory of vehicular VOCs and IVOCs in China. Atmos Chem Phys 17:12709–12724. https://doi.org/10.5194/acp-17-12709-2017

Ma L, Wu M, Tian X et al (2019) China’s provincial vehicle ownership forecast and analysis of the causes influencing the trend. Sustainability 11:3928

Milovanoff A, Posen ID, MacLean HL (2020) Electrification of light-duty vehicle fleet alone will not meet mitigation targets. Nat Clim Change 10:1102–1107. https://doi.org/10.1038/s41558-020-00921-7

Milovanoff A, Minet L, Cheah L et al (2021) Greenhouse gas emission mitigation pathways for urban passenger land transport under ambitious climate targets. Environ Sci Technol. https://doi.org/10.1021/acs.est.0c06671

Narayanan S, Chaniotakis E, Antoniou C (2020) Shared autonomous vehicle services: a comprehensive review. Transp Res Part C Emerg Technol 111:255–293. https://doi.org/10.1016/j.trc.2019.12.008

National Bureau of Statistics of China (2020) China Statistical Yearbook

Peng L, Liu F, Zhou M et al (2021) Alternative-energy-vehicles deployment delivers climate, air quality, and health co-benefits when coupled with decarbonizing power generation in China. One Earth 4:1127–1140

Riahi K, van Vuuren DP, Kriegler E et al (2017) The shared socioeconomic pathways and their energy, land use, and greenhouse gas emissions implications: An overview. Glob Environ Change 42:153–168. https://doi.org/10.1016/j.gloenvcha.2016.05.009

Qiao Q, Zhao F, Liu Z et al (2019) Life cycle greenhouse gas emissions of electric vehicles in China: combining the vehicle cycle and fuel cycle. Energy 177:222–233. https://doi.org/10.1016/j.energy.2019.04.080

Shen J, Chen X, Li H et al (2023) Incorporating health cobenefits into province-driven climate policy: a case of banning new internal combustion engine vehicle sales in China. Environ Sci Technol 57:1214–1224. https://doi.org/10.1021/acs.est.2c08450

State Council Information Office of the People’s Republic of China (2020) New Energy Vehicle Industry Development Plan (2021–2035)

Wolfram P, Weber S, Gillingham K, Edgar Hertwich (2021) Pricing of indirect emissions accelerates low-carbon transition of US light vehicle sector. Nat Portf. https://doi.org/10.21203/rs.3.rs-334331/v1

Xing R, Hanaoka T, Kanamori Y et al (2015) An impact assessment of sustainable technologies for the Chinese urban residential sector at provincial level. Environ Res Lett 10:10:065001. https://doi.org/10.1088/1748-9326/10/6/065001

Xue L, Jin Y, Yu R et al (2022) Toward net zero emissions in the road transport sector in China. WRI, Beijing

Yi W, Yan J (2020) Energy consumption and emission influences from shared mobility in China: a national level annual data analysis. Appl Energy 277:115549. https://doi.org/10.1016/j.apenergy.2020.115549

Zeng Y, Tan X, Gu B et al (2016) Greenhouse gas emissions of motor vehicles in Chinese cities and the implication for China’s mitigation targets. Appl Energy 184:1016–1025. https://doi.org/10.1016/j.apenergy.2016.06.130

Zhang W (2024) Average annual mileage of vehicles in use in China 2013–2020. China

Zhang R, Fujimori S (2020) The role of transport electrification in global climate change mitigation scenarios. Environ Res Lett 15:034019

Zhang R, Hanaoka T (2021) Deployment of electric vehicles in China to meet the carbon neutral target by 2060: provincial disparities in energy systems, CO2 emissions, and cost effectiveness. Resour Conserv Recycl 170:105622. https://doi.org/10.1016/j.resconrec.2021.105622

Zhang Y, Chen X, Zhao Y et al (2022) A methodology for measuring the environmental effect of autonomous bus considering platooning. Transp Res Part Transp Environ 107:103300. https://doi.org/10.1016/j.trd.2022.103300

Zheng B, Zhang Q, Borken-Kleefeld J et al (2015) How will greenhouse gas emissions from motor vehicles be constrained in China around 2030? Appl Energy 156:230–240. https://doi.org/10.1016/j.apenergy.2015.07.018

Acknowledgements

We gratefully acknowledge professor Tong Jiang’s team from the Nanjing University of Information Science & Technology for providing data on the economic and demographic indicators of 31 provinces in China under shared socioeconomic pathways.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare no competing interests.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Hu, J., Ayaragarnchanakul, E., Yang, Z. et al. Shared pooled mobility essential complement to decarbonize China’s transport sector until 2060. Mitig Adapt Strateg Glob Change 29, 37 (2024). https://doi.org/10.1007/s11027-024-10135-3

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s11027-024-10135-3