Abstract

Although previous research endeavours have extensively explored the environmental pressure-performance relationship, their findings have been inclusive. Therefore, this paper examines the direct and indirect (through the mediating role of eco-innovation) impact of regulatory pressure and eco-friendly product demand on sustainable competitive advantage. The research model was examined using Structural Equation Modeling methodology, analyzing data gathered from 183 senior managers within Egyptian SMEs. Several findings have been yielded, which are: (1) eco-innovation is positively motivated by regulatory pressure and eco-friendly product demand; (2) the direct link between environmental pressures (regulatory pressure, eco-friendly product demand) and sustainable competitive advantages is not statistically significant; and (3) eco-innovation acts as a mediator in the relationship between these environmental pressures and sustainable competitive advantage. This research theoretically contributes to the institutional theory of the firm and competitive advantages theory. Particularly, the findings of this research theoretically emphasize that eco-innovation plays a prominent role in alleviating and translating environmental pressures exerted on manufacturing SMEs into sustainable competitive advantages. Furthermore, the research provides practical implications, policy recommendations, limitations, and further research avenues.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

A green economy is considered an essential tool for achieving sustainable development, in which businesses are increasingly pressured to reduce environmentally harmful practices, such as excessive resource consumption and pollution (Abdelkareem et al., 2024; Adebanjo et al., 2016; O’Brien et al., 2013; Zameer et al., 2021). Among these pressures, environmental regulation is viewed as the most considerable pressure pushing firms toward environmental sustainability initiatives (Chan et al., 2016). Environmental legislation and measures imposed by governments are rules of conduct for firms to adopt proactive environmental actions (Testa et al., 2011). Firms could be driven to align their activities with environmental regulations to avoid economic penalties or legal actions resulting from noncompliance with these regulations (Lee, 2020). With growing green consumerism, consumers, especially those who have environmental consciousness, have also exerted intensive pressure on firms to develop and adopt pro-environmental products, processes, and technologies (Fernando & Wah, 2017). As a result of customer pressure, firms may be forced to rethink their environmental goals (Passaro et al., 2022). Although RP and EFD can be the key drivers for improving the environmental performance of firms (Majid et al., 2019; Ramanathan et al., 2014; Zhou et al., 2022), their effects on competitiveness remain unclear.

A great deal of prior studies has focused on exploring the environmental pressure-performance relationship (Baah et al., 2021; El-Garaihy et al., 2022; Zhou et al., 2022), although their results are highly inconclusive. Some previous studies contend that environmental pressures place a great burden of compliance costs on firms and particularly manufacturing firms (Adebanjo et al., 2016; Eiadat et al., 2008). Hence, this line of research demonstrates that firm competitiveness and economic performance are detrimentally impacted by these pressures. Conversely, several studies suggest that environmental pressure has a beneficial impact on firm performance (Song & Wang, 2011; Yu et al., 2017; Zhao et al., 2015). These studies argue that environmental pressures, including RP and customer pressure, are conceived of as complementary to rather than contradictory to the firm’s overall objectives. By imposing stricter regulations and incentivizing environmentally friendly practices, RP ensures that businesses adopt sustainable measures, reducing waste generation and minimizing their environmental footprint (Xiumei et al., 2023). Similarly, customer demands for eco-friendly products and services drive businesses to invest in green capabilities, leading to improved resource efficiency and the adoption of innovative technologies that minimize environmental risks (Mady et al., 2023a). Together, these environmental pressures create a virtuous cycle where businesses actively eliminate environmental wastes and mitigate potential risks, aligning their objectives with the broader goals of sustainability and environmental stewardship. However, these inconclusive results indicate how RP and EFD can affect firm competitiveness and performance is not yet understood. Furthermore, an extensive body of studies has focused on investigating the impact of environmental pressures on business and environmental performances, overlooking sustainable competitiveness as an indicator of firms’ success (e.g., Baah et al., 2021; Song & Wang, 2011; Testa et al., 2011).

To fill the aforementioned two research gaps, this study first explores the influence of environmental pressures, namely, RP and EFD on sustainable competitive advantage (SCA) rather than economic or financial performance. As per the Dynamic Capability Theory, business performance is considered as a lagging exponent of a firm’s success, whereas SCA stands as a leading exponent for this success (Mady et al., 2022a, 2022b; Nadarajah & Kadir, 2014). As SCA also is a relational concept that is used to compare a firm’s performance to that of its competitors, it has more predictive power of a firm’s success compared to business performance (Nadarajah & Kadir, 2014). Furthermore, the current study attempts to understand the mechanism through which environmental pressures can affect SCA by including the concept of eco-innovation (EI) in this relationship. EI is a win–win solution through which firms can simultaneously relieve environmental pressures and promote economic benefits (Mady et al., 2023a, 2023b). By adopting eco-innovative practices, firms can develop and implement novel technologies, processes, and business models that reduce their environmental impact while enhancing their competitive position (Wu et al., 2024). This symbiotic approach aligns with the study’s assumption that EI acts as a mediator in the relationship between environmental pressures and SCA, providing a powerful explanation for this linkage (Janahi et al., 2021).

Overall, this study’s novel contribution lies in its examination of the specific pathways through which environmental pressures influence SCA among SMEs, with a particular focus on the role of EI. By shedding light on these mechanisms, the study offers valuable theoretical insights and practical implications for policymakers and SME managers seeking to foster EI and support SCA. As for Policymakers, the finding of this research can be utilized to design effective regulations and incentives that encourage EI and support sustainable business practices. SME managers, on the other hand, can leverage the knowledge gained from this study to develop strategies and adopt eco-innovative practices that enhance their competitiveness and contribute to a sustainable future.

2 Theoretical framework and hypotheses development

2.1 Institutional theory

Two main theories are fundamentally adopted by the literature to explore the factors that can motivate firms to implement environmentally proactive practices, which are the resource-based view and institutional theory. The former theory is used to explore the internal drivers of these practices, such as organizational resources, absorptive capacity, and internal orientation of management (Aboelmaged, 2018; Cai & Li, 2018). As per the institutional theory, businesses’ behavior toward more environmentally proactive practices is affected by the institutional environment where businesses are operating their operations (Mady et al., 2023b). The institutional theory assumes that the decision to adopt certain actions and conducts is not only made to ameliorate firm efficiency and performance, but there are also social and institutional motives (Alshumrani et al., 2022; DiMaggio & Powell, 1983; Sharfman et al., 2004). To ensure social acceptance and legitimacy as well as accessibility to limited resources, firms should fit their operations and conducts with institutional context involving rule-like social expectations and norms (Alshumrani et al., 2022; Ge et al., 2016). Hence, based on institutional theory, two main intuitional pressures are argued as the most important factors driving firms to adopt environmentally proactive practices and actions, which are RP and customer pressure (Li et al., 2019). First, regulatory pressures refer to these pressures exerted by regulatory and governmental entities or those on which firms depend on acquiring limited resources, which are reflected in environmental regulation and penalties (Gu et al., 2014; Zhou et al., 2022). Second, the pressure exerted by customers, especially those who are aware of environmental concerns, encourages firms to change their operations and products to be more environmentally (Mady et al., 2023a, 2023b; Simpson, 2012).

2.2 Sustainable competitive advantage (SCA)

SCA is conceived as a leading indicator of firm success, which has gained more focus from scholars, especially in the discipline of strategic management (Battour et al., 2021; Pratono et al., 2019). The SCA is also a relational notion reflecting the firm’s persistence to create added value higher than that competitors achieve (Ma, 2000; Pratono et al., 2019). The sources through which firms could achieve SCA have recently been a central concern of the literature. Earlier studies have accentuated that many sources can be determinants of the furtherance of SCA (Arsawan et al., 2022; Mahdi et al., 2019; Quaye & Mensah, 2019). For instance, wide-ranging resources and capabilities can assist firms to sustain their competitive advantage, which may involve technical skills, knowledge, intellectual property, and brand name (Fahy, 2002; Hoopes & Madsen, 2008; Quaye & Mensah, 2019). As many prior studies highlighted, innovation is acknowledged as a unique competence that enables firms to achieve SCA (Baaij et al., 2004; Karia & Asaari, 2016; Pérez‐Luño et al., 2007). To attain SCA, SMEs should provide distinctive characteristics for their products and services that distinguish them from their rival, offering a privileged market position (Quaye & Mensah, 2019; Sharma & Foropon, 2019).

A growing body of literature has recently explored how sustainability serves as a fundamental driver of competitive advantage (Ahmadi-Gh & Bello-Pintado, 2022; Lichtenthaler, 2022). Companies strive for competitiveness and are willing to embrace proactive strategies that can meet stakeholders’ expectations and improve their competitive standing (Ahmadi-Gh & Bello-Pintado, 2022). Incorporating sustainability into their business models, companies can tap into new markets and attract environmentally conscious consumers, expanding their customer base and creating long-term value (Hojnik & Ruzzier, 2016). Sustainability practices can enable companies to not only generate new value but also to minimize harm to achieve profitable outcomes (Lichtenthaler, 2022; Morioka et al., 2017).

2.3 Institutional pressures and sustainable competitive advantage (SCA)

With increasing environmental concerns and environmental pressures imposed on the business world, gaining SCA is no longer dependent only on a firm’s capabilities and competencies, but it is also subject to the effect of institutional mechanisms (Lee, 2020; Yang & Su, 2014). Drawing on the institutional theory, SCA can be influenced by institutional pressures through two main mechanisms; imposition and inducement mechanisms (Li et al., 2019; Scott, 1987). Under the former mechanism, businesses can be forced into following certain actions to avoid potential sanctions, uncertainty, and costs associated with noncompliance (Famiyeh & Kwarteng, 2018; Wang et al., 2018). As a result of the inducement mechanism, institutional pressures can also offer firms incentives to adopt certain practices (Li et al., 2019).

The institutional pressures from regulatory entities and customers present a firm with both impositions and inducements affecting its competitiveness. As concluded by Song and Wang (2011), RP using strict environmental regulations acts as a significant determinant of a firm’s competitiveness. This view is supported by Lee (2020), who found that regulatory entities can impose effective environmental regulations and incentive-based instruments to ensure a green system with highly cost-effective and ultimately leads to enhancing a firm’s competitiveness. Consequently, strict environmental regulations, if well-designed to be performance-based standards for the adapters, can not only encourage firms to improve resource allocation but also help them to obtain positive performance on the market through realizing and exploiting green business opportunities (Testa et al., 2011).

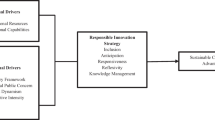

On the other side, customers who have demand for eco-friendly products exert extensive pressure on firms to adopt proactive environmental practices and thereby enhance competitiveness (Baah et al., 2021). Firms keeping up with the demand for eco-friendly products are anticipated to gain SCA. Since customers with high environmental consciousness show a willingness to pay more for environmentally friendly products, firms with environmentally conscious operations and products may be able to capitalize on this trend and fill a market niche (Cai & Li, 2018). The eco-friendly products market is also expanding quickly, which may be a segment that offers businesses a chance to gain an advantage over rivals (Hojnik & Ruzzier, 2016). As a result, businesses that are unable to satisfy the demand for eco-friendly products risk losing their clientele, which has a negative impact on their competitiveness. Hence, it is anticipated that a firm that is subjected to RP and EFD is more likely to have a SCA and we propose the following hypotheses (see Fig. 1):

Theoretical framework

H1

RP is positively associated with SCA.

H2

EFD is positively associated with SCA.

2.4 The institutional context and eco-innovation

The business world has moved into an era of environmental concerns that put extensive pressure on firms to follow proactive environmental norms and initiatives (Barforoush et al., 2021). Facing environmental pressures, environmental strategies adopted by SMEs range from reluctant, reactive, and proactive strategies (Aragón-Correa et al., 2008; Klewitz & Hansen, 2014). Of these environmental strategies, the EI strategy has emerged as the most effective strategy for dealing with environmental issues (Ben Amara & Chen, 2022). A large line of research on EI focuses particularly on investigating what and how different environmental pressures can force or motivate SMEs to adopt an EI strategy Majid et al., 2019; Qi et al., 2021). With institutional context, RP and pressure from customer demand for eco-friendly products are viewed to be the two most external institutional pressures that can foster EI practices, especially among Manufacturing SMEs (Li et al., 2019; Triguero et al., 2013; Williams & Spielmann, 2019).

Environmental regulations constitute the most powerful coercive measures imposed by the government to pressure businesses to follow proactive environmental initiatives, most notably EI (Cai & Li, 2018; Qi et al., 2020). With increasing RP, an EI strategy is adopted chiefly to help SMEs avoid financial and political burdens that can be shouldered in the case of noncompliance (Ning et al., 2022). In addition, the adoption of EI is instrumental in creating added value offsetting the costs that can result from applying regulations governing environmental issues (Hojnik & Ruzzier, 2016; Horbach, 2008; Kesidou & Demirel, 2012). However, several studies, for example, Mady et al., (2022a, 2022b) found contradictory evidence that stringent RP through imposing environmental rules and regulations is not able to motivate SMEs to be more environmentally innovative in their products, production processes, and management methods. Similarly, Eiadat et al. (2008) pressure from environmental regulators is insufficient to foster an EI strategy.

Customer demand for environmentally friendly products is another institutional pressure that can enforce or motivate manufacturing SMEs to foster EI practices (Li et al., 2019; Triguero et al., 2013). In the recent decade, concerns about environmental issues have gained importance in the eyes of customers on the global market (Yue et al., 2020). In order to cater environmental requirements of customers, businesses tend to change their existing products to be more eco-friendly (Akhtar et al., 2021). Consequently, the EI strategy is seen as an effective choice for SMEs to respond to customers’ preferences for eco-friendly products (Fernando & Wah, 2017; Li, 2014). Thus, this study puts forward the following hypotheses (see Fig. 1):

H3

RP is positively associated with EI.

H4

EFD is positively associated with EI.

2.5 Eco-innovation and sustainable competitive advantage

In the age of concern for the environment, EI constitutes a vital source enabling a firm to win the competition (Barforoush et al., 2021). EI is seen as a corporate strategic capability that can be exploited to create multiple long-lasting advantages (Zameer et al., 2020a, 2020b). Achieving a firm’s competitive edge over rivals by developing eco-friendly attributes of its products is among the relevant objectives of the EI strategy. As stated by Al-Abdallah and Al-Salim, (2021), eco-product innovation as a type of EIs can help firms stand out from other rivals by constructing their positive and eco-friendly image and satisfying the environmental requirements of customers. On the other side, eco-process innovation-oriented firms can also gain competitive benefits such as cost-saving and resource productivity (Hojnik & Ruzzier, 2016). Furthermore, Sellitto et al. (2020) conclude that cost savings and product differentiation are two benefits of eco-process innovation, whereas eco-product innovation can lead to promoting a positive image of a firm and a growing market share. Therefore, the study suggests the following hypothesis to investigate the role of EI in acquiring Egyptian manufacturing SMEs SCA (see Fig. 1).

H5

EI is positively associated with SCA.

2.6 The mediating effect of eco-innovation

EI is seen in the literature as a dual-purpose strategy aimed at helping firms respond to environmental pressures while at the same time ensuring improved business performance (Hazarika & Zhang, 2019; Horbach et al., 2013). The literature used two main perspectives explaining the effect of institutional pressures on organizational behavior and performance: the conventional economic view and the Porter hypothesis (Chen et al., 2018; Ning et al., 2022). The former view posited that different environmental pressures had placed many costs associated with inhibiting the consumption of certain raw materials and using certain environmental technologies, thereby reducing business performance. However, the porter hypothesis − a revisionist viewpoint, put out by Porter and Van Der Linde (1995), suggests that environmental pressure exerted by regulatory entities can foster rather than stifle EI and ultimately produce competitive benefits for green-oriented firms (Daddi et al., 2016; Lee, 2020). By adopting eco-innovative practices, firms can find ways to reduce the costs associated with inhibiting the consumption of certain raw materials and implementing specific environmental technologies (Hojnik & Ruzzier, 2016; Horbach, 2008; Kesidou & Demirel, 2012). For instance, EI can involve the development of more efficient production techniques that minimize resource consumption and waste generation, thereby reducing associated costs. It can also entail the creation of new products or services that are environmentally friendly, meeting consumer demand for sustainable alternatives and potentially opening up new market opportunities (Barforoush et al., 2021). Therefore, the study tries to examine the mediating role of EI in the relationship between environmental pressures and SCA, as shown in the following hypotheses (see Fig. 1).

H6

EI mediates the relationship between RP and SCA.

H7

EI mediates the relationship between EFD and SCA.

3 Materials and methods

The current study assesses the direct and indirect (through EI) association of RP (H1) and EFD (H2) with the SCA of small and medium-scale manufacturing firms in Egypt followed by testing the direct association of RP (H3) and EFD (H4) with the EI. The study also puts forward hypothesis H5 to test the direct association of EI with sustainable competitive advantage. The study proposes a comprehensive hypothesized framework (H6) and EFD (H7) not only affect a manufacturing firm’s sustainable competitive advantage directly but indirectly as well through the mediation of EI. For this purpose, the study adopts the positivist methodological approach and analyses the final data from 183 Egyptian manufacturing firms (111 small-scale and 72 medium-scale). The study uses Smart-PLS 3.0 to establish the measurement model and test the research hypotheses as the data do not hold the multivariate normality as per Mardia’s (1974) recommendations. Smart-PLS works on the PLS approach and is recommended for data samples that do not hold multivariate normality (Hair et al., 2019).

3.1 Sample participants

In conformity with the objectives of the study, the target sample was small and medium-scale Egyptian manufacturing firms. For sample determination, we identified the manufacturing SMEs on the database of the Industrial Development Authority (IDA)—an Egyptian licensing authority. 650 SMEs from four Egyptian governorates—Alexandria, Cairo, Giza, and Qalyubia were identified for the data collection. We contacted the persons (owners/CEOs) in charge of the firms’ operations and decision-making for filling out the survey as they held higher positions in their respective firms and were found suitable and capable of providing appropriate responses for the study’s variables.

3.2 Development of the survey instrument

As the study model comprises five latent variables, we developed a questionnaire adopting a continuous rating scaling technique (using a five-point Likert scale). We divided the questionnaire into two sections. Section 1 was designed to capture the demographic features of the sample (viz., industry type, firm size, respondents’ position in the firm, experience, level of education, and gender of the respondent) preceded by a brief information about the study’s objectives and significance. Section 2 was meant to gather the data on all five latent variables adopting validated measurement scales from already published studies (see Table 1 for sources of measurement scale adoption). Borrowed measurement scales were first put to some language and subjectivity modifications. Following the suggested qualitative measures by Podsakoff et al. (2012), we ensured that the observed items did not contain language errors, double-barreled statements and jargon. Initially, we developed the in English language then translated into Arabic language and then again back to English language (using the parallel-translation method) (Saunders et al., 2009). For this purpose, we recruited three linguists who are experts in English-Arabic-English translation.

3.3 Final survey

The owners/CEOs of 650 SMEs were sent the questionnaires through emails containing a cover letter describing the study’s aims while seeking the participants’ consent. Out of 650 questionnaires, we retrieved only 197 (30.30%) completed questionnaires which were then processed for pre-validation data screening and cleansing treatments. As Mellahi and Harris (2016) indicated, low response rates are a common issue in business and management research. However, Rowley (2014) emphasizes that the sufficiency of the collected questionnaires is contingent on the types of analyses that must be conducted. According to Hair Jr et al. (2014), a minimum sample size for the “PLS-SEM” model should be determined at “ten times the highest number of structural paths directed to a particular construct” subject to the significance level and the minimum R2 value. In the case of the present study’s structural model, three is the highest number of structural paths directed at the outcome variable (SCA); hence at a “5% level of significance” and achieving a minimum R2 of 0.10 (10%), the sample size is read to be 124 responses (Hair Jr et al., 2014) which is way below the study’s final sample of 183 responses achieved after data cleaning and screening.

3.4 Data screening

The study put the data to cleansing and screening treatments before establishing the measurement model and testing the structural model. We first checked for missing, inappropriate, and outlier responses. Upon examination, we found six cases with inappropriate responses; thus, they were discarded. We applied Cook’s distance technique to identify outlier responses and found that eight responses were found to be showing Cook’s statistics above the threshold of 1 (Pituch & Stevens, 2015); hence these eight responses were also discarded, and the study achieved the final sample of 183 SMEs comprising 111 small-scale and 72 medium-scale enterprises. The demographic profiles of the sample are given in Table 2.

3.5 Method bias

In conformity with the recommendation by Podsakoff et al. (2003), we also statistically assessed whether the data suffered from method bias or not. We applied Harman’s one-factor technique with PCA as the extraction method and Varimax as the rotation method in SPSS while allowing all 29 observed indicators to load under one single factor. The results unfolded that the total cumulative variance extracted by all 29 indicators was 38.19%, which is sufficiently below the threshold of 50% (Podsakoff et al., 2003), hence proving that the data is not adversely affected by method bias.

4 Data analysis and results

The study uses Smart-PLS 3.0 to establish the outer (measurement) model establishment and test the inner (structural) model for testing the direct and indirect paths. We opted for PLS-based SEM over CB-SEM because the study’s sample size is relatively low than the required sample for CB-SEM with the non-normal multivariate distribution. Smart-PLS works very well with a low sample and non-normally distributed multivariate data (Hair et al., 2019).

4.1 Measurement (outer) model assessment

The measurement model was established by constructing a model in Smart-PLS manifesting 29 observed items with their respective reflective latent variables. First, we assessed the internal reliability of the scales considering composite reliability (CR) statistics for each latent variable. Results from Table 3 affirm that CR values for each latent variable are above the benchmark of 0.70 (Henseler et al., 2016) hence assuring the internal consistency of the measurement scales. Further, the study validates measurement model convergence considering standardized factor loadings of observed items with their respective latent variables and the average extracted variance (AVE) value of each construct. For enough convergence of observed items with a latent construct, Gefen and Straub (2005) recommended a minimum factor loading of 0.60, while the latent construct accounts for a minimum AVE value of 0.50. The study’s measurement model is found to be consistent with the recommendations of Gefen and Straub (2005), showing factor loadings as low as 0.612 while AVE values for each latent variable found beyond the suggested limit of 0.50, thus it is inferred that the study’s measurement model holds enough convergence. However, during the measurement model validation, we discarded observed items EI-ORG2, EI-ORG3, and EI-ORG5 as they failed to converge with a minimum factor loading of 0.60.

As a measurement model is supposed to hold both convergence and divergence, the study checks for the divergence validity of the model following Fornell and Larcker’s (1981) approach and HTMT ratio criteria. As per Fornell and Larcker’s (1981) approach, a latent construct is said to be divergent enough if the squared root value of a construct’s AVE is in excess of its correlations with other constructs. The study’s measurement model is consistent with the recommendations of Fornell and Larcker (1981), affirming that the squared root values of AVEs (see bold diagonal values in Table 4) for each construct are in excess of the correlation coefficients ((below off-diagonal values in Table 4), thus meeting the divergence criteria.

Moreover, we also established the divergent validity following “the HTMT criterion”, where the validity is established based on “HTMT ratios”. The measurement model tends to hold divergent validity if “HTMT ratios” among the constructs are below the threshold of 0.85 (Kline, 2015). Table 5 evidences that the “HTMT ratios” among the constructs are found below 0.85, thus referring to the establishment of divergent validity.

4.2 Structural model (hypotheses testing)

The structural (inner) model tested the multicollinearity and path coefficients among the predictors, mediator and outcome variable while accounting for adjusted R2, F2, and Q2 values for model’s predictive explanatory power. VIF values (see Table 6) were found well below the suggested limit of 5 (Hair et al., 2014), hence confirming that the study’s structural model does not suffer from multicollinearity.

The results of testing the direct relationships are portrayed in Table 7. The study tests five direct paths (hypotheses H1–H5) with 5000 bootstrap resamples at 5% significance level. The results confirm that EI is significantly influenced by RP (β = 0.264, t-value = 2.392, p-value < 0.05) and EFD (β = 0.434, t-value = 5.346, p-value < 0.01), thus hypotheses H3 and H4 were accepted while EI also significantly enhanced SCA (β = 0.687, t = 7.156, p-value < 0.01), hence extending support to hypothesis H5. However, hypotheses H1 and H2 were found unsupported as RP (β = 0.064, t-value = 0.791, p-value > 0.05) and EFD (β = 0.066, t-value = 0.710, p-value > 0.05) failed to influence SCA significantly.

As Table 8 illustrated, the structural model’s explanatory power was found to fall in the categories of moderate, i.e., R2 ≤ 0.50 and substantial, i.e., R2 ≤ 0.75 (Henseler et al., 2016). For the model with outcome variable EI, R2 value is found at 0.356 (moderately high), while for the SCA, R2 value is found to be at 0.573 (substantially high). Moreover, the study also considers Stone-Geisser’s Q2 as the indicator of model’s predictive power. Q2 is determined using the blindfolding method and gives more accurate and refined predictive power of the structural model with the following categories of model predictability: 0.02 (small), 0.15 (medium), and 0.35 (large) (Sarstedt et al., 2017). Q2 values for the study’s structural model are found in the medium category, with Q2 values of 0.198 and 0.306 for EI and SCA, respectively. We also assessed the effect sizes (F2) of the path coefficients and found the values in the small category (F2 = 0.089 for RP → EI path) and large category (F2 = 0.239 for EFD → EI path; F2 = 0.712 for EI → SCA path) (Cohen, 1988).

The results of mediation analysis (testing of hypotheses H6 and H7) unfold that the indirect paths between RP (β = 0.182, SE = 0.073, LLCI = 0.038; ULCI = 0.326), EFD (β = 0.298, SE = 0.082, LLCI = 0.137; ULCI = 0.459) and SCA are significantly mediated by EI (see Table 9). Considering that the direct paths between RP, EFD, and SCA were found insignificant (see Table 7) while the indirect path coefficients are significantly larger and making the total effects (direct effect + indirect effect) significant (see Importance-Performance Map in Fig. 2). The results infer that EI plays a full mediator role between RP, EFD, and SCA and makes their indirect relations significantly stronger compared to direct relations.

Importance-performance analysis

5 Discussion

The review of environmental sustainability emphasized that environmental pressures have two main mechanisms, namely, inducement and imposition mechanisms by which to foster proactive environmental practices, ultimately, business performance. This study investigated how RP and pressure from EFD could be powerful drivers of SCA for SMEs, furthermore, the study explored the mediating role of EI within this relationship. In this study, the hypothesized research framework is composed of four main relationships. First, the study tried to understand the extent to which these pressures can directly affect SMEs’ SCA. The second relationship was the effects of environmental pressures on EI adoption within Manufacturing SMEs. Third, this study also focuses on the role of EI in enhancing SCA. Finally, this study hypothesized the indirect effect of these environmental pressures on SCA through mediating EI.

Concerning the effects of RP and pressure from EFD on SCA, the results reveal that these pressures do not lead to enhancing SMEs’ SCA. This result is in dispute with the study conducted by Testa et al. (2011) and Lee (2020), highlighting that well-designed regulations can stimulate firms to adopt new technologies and processes that can enable them to meet environmental targets while sustaining their competitiveness. In the same vein, customer demand for eco-friendly products is viewed by many prior studies (e.g., Baah et al., 2021; Zameer et al., 2020a, 2020b) as a promising opportunity for SMEs to gain competitive benefits such as cost-savings and attracting a considerable segment of customers with highly environmentalism. These results might stem from the observation that regulatory bodies and customers are not directly imposing environmental pressures to influence the economic and productive performance of businesses. Instead, the underlying aim of such pressures is to encourage businesses to enhance their environmental practices and minimize their adverse impact on the environment. Consequently, the effect of these pressures on SCA is likely to be based on the business strategy that firms adopt as a response to such pressures.

Secondly, environmental pressures exerted by regulatory entities and customers were shown to be significant drivers of EI among manufacturing SMEs. This result aligns with a bulk of prior studies; for example, Ben Amara and Chen (2022) concluded that environmental regulation is the most influential driver of EI, followed by customer pressure that induces firms to be eco-innovator. As Jun et al. (2021) argued, the EI approach is considered a crucial choice for SMEs responding to RP and customer demand for eco-friendly demand. Thirdly, the results also reveal that adopting an EI strategy can give SMEs plenty of opportunities for gaining SCA. These results support the existing literature example (e.g., Oxborrow & Brindley, 2013; Zameer et al., 2020a, 2020b), which accentuated that while EI is a considerable challenge for SMEs, it is conceived of as a strategic organizational capability necessary for SMEs to gain eco-advantage over their rivals, especially in the era of the circular economy.

Consistent with the Porter hypothesis, this study finally finds evidence for the hypothesis that EI is mediating the relationship between environmental pressures, namely, RP and EFD, and SCA. Intensive environmental pressures have made EI a strategic approach not only for avoiding these pressures but also for gaining SCA. Put differently, besides alleviating environmental pressures exposing on firms; an EI strategy provides firms with competitive benefits. Based on the imposition mechanism, SMEs can follow strict environmental regulations and standards by implementing EI practices to avoid the costs and penalties due to noncompliance with such regulations (Berrone et al., 2013). In addition, as per the inducement mechanism, following environmental regulations through EI can enable SMEs to enhance cost efficiency and competitiveness (Chan et al., 2016; Jun et al., 2021). On the other hand, a lack of responsiveness to EFD could lead to the loss of a considerable segment of customers that are willing to pay higher prices for green benefits provided by eco-friendly products (Sharma & Foropon, 2019). As such, eco-friendly demand constitutes a market opportunity inducing firms to initiate and develop eco-product innovations by which their product can be differentiated and attractive to those who are more environmentally aware (Fernando & Wah, 2017; Sáez-Martínez et al., 2016).

5.1 Conclusion and implications

This research focuses on the direct and indirect (through the mediating role of EI) effects of RP and EFD on SCA in manufacturing SMEs. The findings emphasized the significant positive impact of RP on SCA and EI. Additionally, while EFD significantly enhances EI, it has an insignificant impact on SCA. Furthermore, EI enhances SCA. Regarding the indirect impact, EI mediates the relationship between RP and SCA from one side and the relationship between EFD and SCA from the other side.

5.2 Theoretical implications

While this research theoretically contributes to the literature on EI and SCA, it empirically provides several research contributions. Theoretically, this endeavor represents a successful empirical examination of the institutional theory of the firm (DiMaggio & Powell, 1983). As per the theory, companies must adhere to environmental pressures in order to establish legitimacy and secure access to scarce resources (Alshumrani et al., 2022; Ge et al., 2016). However, this research introduces regulatory pressure and customer pressure as two prominent environmental pressures that firms need to adapt to sustain their operations. Furthermore, this study contributes to the competitive advantages theory (Porter, 1985). According to the theory, firms must develop attributes that enable them to generate superior value compared to their competitors (Ma, 2000; Pratono et al., 2019). This study indicates the positive link between two types of environmental pressures (regulatory pressure and EFD) and SCA. Therefore, firms’ compliance with environmental pressures represents one attribute that allows an organization to outperform its competitors. Additionally, the adoption of EI is considered another competitive advantage for any firm. The findings indicate eco-innovation’s direct effect and mediating effect on SCA.

5.3 Managerial implications

Empirically, the practical implication of this research is threefold. First, SMEs are recommended to adopt eco-innovation as a business strategy. Our findings are consistent with the literature indicating eco-innovation as a fundamental source enabling firms to win competition (Barforoush et al., 2021). Second, environmental orientation within SMEs should be developed to acquire the ability to respond to external pressure related to environmental goals. Responsiveness to environmental pressures and setting environmental goals produce competitive benefits for SMEs (Daddi et al., 2016; Lee, 2020). Third, policymakers are advised to suggest active initiatives for encouraging eco-friendly demand and environmentalism orientation, as the green economy is essential for sustainable development.

5.4 Limitations and future research avenues

This research is not without limitations, which in turn open up avenues for further investigation. First, this research concentrated on the regulatory pressures and eco-friendly product demand as two types of external pressures and their impact on SCA. Future research could delve into the impact of internal pressures or other types of external pressures, such as quality pressure and competitor pressure. Second, SCA was examined in this research as a dependent variable; other research could examine the impact of environmental pressure on strategic decision-making speed and quality. Third, while this research focused on SMEs, it investigates the Egyptian context, which has not been done before. Furthermore, the data collected from the manufacturing sector gain a huge concern regarding environmental pressures. Future research endeavors could replicate this study in different domains or industries. Fourth, while this research was quantitatively conducted using cross-sectional data, other research could adopt the qualitative approach or conduct a longitudinal study.

Data availability

“Data sharing is not possible due to ethical and privacy restrictions”.

Abbreviations

- RP:

-

Regulatory pressure

- EFD:

-

Eco-friendly product demand

- SCA:

-

Sustainable competitive advantage

- EI:

-

Eco-innovation

- SMEs:

-

Small and medium-sized enterprises

- PLS-SEM:

-

Partial least squares structural equation modeling

- CB-SEM:

-

Covariance-based structural equation modeling

- PCA:

-

Principal component analysis

- AVE:

-

Average variance extracted

- CR:

-

Composite reliability

- HTMT:

-

Heterotrait-monotrait ratio of correlations

- VIF:

-

Variance inflation factor

References

Abdelkareem, R. S., Mady, K., Lebda, S. E., & Elmantawy, E. S. (2024). The effect of green competencies and values on carbon footprint on sustainable performance in healthcare sector. Cleaner and Responsible Consumption, 12, 100179.

Aboelmaged, M. (2018). Direct and indirect effects of eco-innovation, environmental orientation and supplier collaboration on hotel performance: An empirical study. Journal of Cleaner Production, 184, 537–549. https://doi.org/10.1016/j.jclepro.2018.02.192

Adebanjo, D., Teh, P. L., & Ahmed, P. K. (2016). The impact of external pressure and sustainable management practices on manufacturing performance and environmental outcomes. International Journal of Operations and Production Management, 36(9), 995–1013. https://doi.org/10.1108/IJOPM-11-2014-0543

Agan, Y., Acar, M. F., & Borodin, A. (2013). Drivers of environmental processes and their impact on performance: A study of Turkish SMEs. Journal of Cleaner Production, 51, 23–33. https://doi.org/10.1016/j.jclepro.2012.12.043

Ahmadi-Gh, Z., & Bello-Pintado, A. (2022). Why is manufacturing not more sustainable? The effects of different sustainability practices on sustainability outcomes and competitive advantage. Journal of Cleaner Production, 337, 130392. https://doi.org/10.1016/j.jclepro.2022.130392

Akhtar, R., Sultana, S., Masud, M. M., Jafrin, N., & Al-Mamun, A. (2021). Consumers’ environmental ethics, willingness, and green consumerism between lower and higher income groups. Resources, Conservation and Recycling, 168(September 2020), 105274. https://doi.org/10.1016/j.resconrec.2020.105274

Al-Abdallah, G. M., & Al-Salim, M. I. (2021). Green product innovation and competitive advantage: An empirical study of chemical industrial plants in Jordanian qualified industrial zones. Benchmarking, 28(8), 2542–2560. https://doi.org/10.1108/BIJ-03-2020-0095

Alshumrani, S., Baird, K., & Munir, R. (2022). Management innovation: The influence of institutional pressures and the impact on competitive advantage. International Journal of Manpower, 43(5), 1204–1220. https://doi.org/10.1108/IJM-05-2021-0291

Aragón-Correa, J. A., Hurtado-Torres, N., Sharma, S., & García-Morales, V. J. (2008). Environmental strategy and performance in small firms: A resource-based perspective. Journal of Environmental Management, 86(1), 88–103. https://doi.org/10.1016/j.jenvman.2006.11.022

Arsawan, I. W. E., Koval, V., Rajiani, I., Rustiarini, N. W., Supartha, W. G., & Suryantini, N. P. S. (2022). Leveraging knowledge sharing and innovation culture into SMEs sustainable competitive advantage. International Journal of Productivity and Performance Management, 71(2), 405–428. https://doi.org/10.1108/IJPPM-04-2020-0192

Baah, C., Opoku-Agyeman, D., Acquah, I. S. K., Agyabeng-Mensah, Y., Afum, E., Faibil, D., & Abdoulaye, F. A. M. (2021). Examining the correlations between stakeholder pressures, green production practices, firm reputation, environmental and financial performance: Evidence from manufacturing SMEs. Sustainable Production and Consumption, 27, 100–114. https://doi.org/10.1016/j.spc.2020.10.015

Baaij, M., Greeven, M., & Van Dalen, J. (2004). Persistent superior economic performance, sustainable competitive advantage, and schumpeterian innovation: Leading established computer firms 1954–2000. European Management Journal, 22(5), 517–531. https://doi.org/10.1016/j.emj.2004.09.010

Barforoush, N., Etebarian, A., Naghsh, A., & Shahin, A. (2021). Green innovation a strategic resource to attain competitive advantage. International Journal of Innovation Science, 13(5), 645–663. https://doi.org/10.1108/IJIS-10-2020-0180

Battour, M., Barahma, M., & Al-Awlaqi, M. (2021). The relationship between hrm strategies and sustainable competitive advantage: Testing the mediating role of strategic agility. Sustainability (switzerland), 13(9), 5315. https://doi.org/10.3390/su13095315

Ben Amara, D., & Chen, H. (2022). Driving factors for eco-innovation orientation: Meeting sustainable growth in Tunisian agribusiness. International Entrepreneurship and Management Journal, 18(2), 713–732. https://doi.org/10.1007/s11365-021-00792-0

Berrone, P., Fosfuri, A., Gelabert, L., & Gomez-Mejia, L. R. (2013). Necessity as the mother of ‘Green’ inventions: Institutional pressures and environmental innovations. Strategic Management Journal, 34, 891–909. https://doi.org/10.1002/smj

Cai, W., & Li, G. (2018). The drivers of eco-innovation and its impact on performance: Evidence from China. Journal of Cleaner Production, 176, 110–118.

Chan, H. K., Yee, R. W. Y., Dai, J., & Lim, M. K. (2016). The moderating effect of environmental dynamism on green product innovation and performance. International Journal of Production Economics, 181, 384–391. https://doi.org/10.1016/j.ijpe.2015.12.006

Chen, X., Yi, N., Zhang, L., & Li, D. (2018). Does institutional pressure foster corporate green innovation? Evidence from China’s top 100 companies. Journal of Cleaner Production, 188, 304–311. https://doi.org/10.1016/j.jclepro.2018.03.257

Cheng, C. C. J. J., Yang, C. L., & Sheu, C. (2014). The link between eco-innovation and business performance: A Taiwanese industry context. Journal of Cleaner Production, 64, 81–90. https://doi.org/10.1016/j.jclepro.2013.09.050

Cohen, J. (1988). Statistical power analysis for the behavioural sciences. Lawrence Earlbaum Associates.

Daddi, T., Testa, F., Frey, M., & Iraldo, F. (2016). Exploring the link between institutional pressures and environmental management systems effectiveness: An empirical study. Journal of Environmental Management, 183, 647–656. https://doi.org/10.1016/j.jenvman.2016.09.025

DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited : Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.1016/j.jclepro.2015.02.067

Eiadat, Y., Kelly, A., Roche, F., & Eyadat, H. (2008). Green and competitive? An empirical test of the mediating role of environmental innovation strategy. Journal of World Business, 43(2), 131–145. https://doi.org/10.1016/j.jwb.2007.11.012

El-Garaihy, W. H., Badawi, U. A., Seddik, W. A. S., & Torky, M. S. (2022). Investigating performance outcomes under institutional pressures and environmental orientation motivated green supply chain management practices. Sustainability (switzerland), 14(3), 1523. https://doi.org/10.3390/su14031523

Fahy, J. (2002). A resource-based analysis of sustainable competitive advantage in a global environment. International Business Review, 11(1), 57–77. https://doi.org/10.1016/S0969-5931(01)00047-6

Famiyeh, S., & Kwarteng, A. (2018). Implementation of environmental management practices in the Ghanaian mining and manufacturing supply chains. International Journal of Productivity and Performance Management, 67(7), 1091–1112. https://doi.org/10.1108/IJPPM-04-2017-0095

Fernando, Y., & Wah, W. X. (2017). The impact of eco-innovation drivers on environmental performance: Empirical results from the green technology sector in Malaysia. Sustainable Production and Consumption, 12(November 2016), 27–43. https://doi.org/10.1016/j.spc.2017.05.002

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39. https://doi.org/10.2307/3151312

Ge, B., Jiang, D., Gao, Y., & Tsai, S. B. (2016). The influence of legitimacy on a proactive green orientation and green performance: A study based on transitional economy scenarios in China. Sustainability (switzerland), 8(12), 1–20. https://doi.org/10.3390/su8121344

Gefen, D., & Straub, D. (2005). A practical guide To factorial validity using PLS-graph: Tutorial and annotated example. Communications of the Association for Information Systems, 16, 91–109.

Gu, V. C., Hoffman, J. J., Cao, Q., & Schniederjans, M. J. (2014). The effects of organizational culture and environmental pressures on IT project performance: A moderation perspective. International Journal of Project Management, 32(7), 1170–1181. https://doi.org/10.1016/j.ijproman.2013.12.003

Hair, J. F., Jr., Hult, G. T. M., Ringle, C., & Sarstedt, M. (2014). A primer on partial least squares structural equation modeling (PLS-SEM). Sage Publications.

Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

Hazarika, N., & Zhang, X. (2019). Factors that drive and sustain eco-innovation in the construction industry: The case of Hong Kong. Journal of Cleaner Production, 238, 117816. https://doi.org/10.1016/j.jclepro.2019.117816

Henseler, J., Hubona, G., & Ray, P. A. (2016). Using PLS path modeling in new technology research: Updated guidelines. Industrial Management and Data Systems, 116(1), 2–20. https://doi.org/10.1108/IMDS-09-2015-0382

Hojnik, J., & Ruzzier, M. (2016). The driving forces of process eco-innovation and its impact on performance: Insights from Slovenia. Journal of Cleaner Production, 133, 812–825. https://doi.org/10.1016/j.jclepro.2016.06.002

Hoopes, D. G., & Madsen, T. L. (2008). A capability-based view of competitive heterogeneity. Industrial and Corporate Change, 17(3), 393–426. https://doi.org/10.1093/icc/dtn008

Horbach, J. (2008). Determinants of environmental innovation-New evidence from German panel data sources. Research Policy, 37(1), 163–173. https://doi.org/10.1016/j.respol.2007.08.006

Horbach, J., Oltra, V., & Belin, J. (2013). Determinants and specificities of eco-innovations compared to other innovations-an econometric analysis for the french and german industry based on the community innovation survey. Industry and Innovation, 20(6), 523–543. https://doi.org/10.1080/13662716.2013.833375

Janahi, N. A., Durugbo, C. M., & Al-Jayyousi, O. R. (2021). Eco-innovation strategy in manufacturing: A systematic review. Cleaner Engineering and Technology, 5, 100343. https://doi.org/10.1016/j.clet.2021.100343

Jun, W., Ali, W., Bhutto, M. Y., Hussain, H., & Khan, N. A. (2021). Examining the determinants of green innovation adoption in SMEs: A PLS-SEM approach. European Journal of Innovation Management, 24(1), 67–87. https://doi.org/10.1108/EJIM-05-2019-0113

Karia, N., & Asaari, M. H. A. H. (2016). Innovation capability: The impact of teleworking on sustainable competitive advantage. International Journal of Technology, Policy and Management, 16(2), 181. https://doi.org/10.1504/ijtpm.2016.076318

Kesidou, E., & Demirel, P. (2012). On the drivers of eco-innovations: Empirical evidence from the UK. Research Policy, 41(5), 862–870. https://doi.org/10.1016/j.respol.2012.01.005

Klewitz, J., & Hansen, E. G. (2014). Sustainability-oriented innovation of SMEs: A systematic review. Journal of Cleaner Production, 65, 57–75. https://doi.org/10.1016/j.jclepro.2013.07.017

Kline, R. B. (2015). Principles and practice of structural equation modeling. Guilford publications.

Lee, E. (2020). Environmental regulation and financial performance in China: An integrated view of the porter hypothesis and institutional theory. Sustainability, 12(23), 10183. https://doi.org/10.3390/su122310183

Li, Y. (2014). Environmental innovation practices and performance: Moderating effect of resource commitment. Journal of Cleaner Production, 66, 450–458. https://doi.org/10.1016/j.jclepro.2013.11.044

Li, Y., Ye, F., Dai, J., Zhao, X., & Sheu, C. (2019). The adoption of green practices by Chinese firms: Assessing the determinants and effects of top management championship. International Journal of Operations and Production Management, 39(4), 550–572. https://doi.org/10.1108/IJOPM-12-2017-0753

Lichtenthaler, U. (2022). Explicating a sustainability-based view of sustainable competitive advantage. Journal of Strategy and Management, 15(1), 76–95. https://doi.org/10.1108/JSMA-06-2021-0126

Ma, H. (2000). Competitive advantage and firm performance. Competitiveness Review: An International Business Journal, 10(2), 15–32. https://doi.org/10.1108/eb046396

Mady, K., Abdul Halim, M. A. S., & Omar, K. (2022a). Drivers of multiple eco-innovation and the impact on sustainable competitive advantage: Evidence from manufacturing SMEs in Egypt. International Journal of Innovation Science, 14(1), 40–61. https://doi.org/10.1108/IJIS-01-2021-0016

Mady, K., Abdul Halim, M. A. S., Omar, K., Abdelkareem, R. S., & Battour, M. (2022b). Institutional pressure and eco-innovation: The mediating role of green absorptive capacity and strategically environmental orientation among manufacturing SMEs in Egypt. Cogent Business and Management, 9(1), 2064259. https://doi.org/10.1080/23311975.2022.2064259

Mady, K., Abdul Halim, M. A. S., Omar, K., Battour, M., & Abdelkareem, R. S. (2023a). Environmental pressures and eco-innovation in manufacturing SMEs: The mediating effect of environmental capabilities. International Journal of Innovation Science. https://doi.org/10.1108/IJIS-08-2022-0163

Mady, K., Battour, M., Aboelmaged, M., & Abdelkareem, R. S. (2023b). Linking internal environmental capabilities to sustainable competitive advantage in manufacturing SMEs: The mediating role of eco-innovation. Journal of Cleaner Production, 417(June), 137928. https://doi.org/10.1016/j.jclepro.2023.137928

Mahdi, O. R., Nassar, I. A., & Almsafir, M. K. (2019). Knowledge management processes and sustainable competitive advantage: An empirical examination in private universities. Journal of Business Research, 94, 320–334. https://doi.org/10.1016/j.jbusres.2018.02.013

Majid, A., Yasir, M., Yasir, M., & Javed, A. (2019). Nexus of institutional pressures, environmentally friendly business strategies, and environmental performance. Corporate Social Responsibility and Environmental Management, 27(2), 706–716. https://doi.org/10.1002/csr.1837

Mardia, K. V. (1974). Applications of some measures of multivariate skewness and kurtosis in testing normality and robustness studies. Sankhyā the Indian Journal of Statistics Series B (1960–2002), 36(2), 115–128.

Mellahi, K., & Harris, L. C. (2016). Response rates in business and management research: An overview of current practice and suggestions for future direction. British Journal of Management, 27(2), 426–437.

Morioka, S. N., Bolis, I., Evans, S., & Carvalho, M. M. (2017). Transforming sustainability challenges into competitive advantage: Multiple case studies kaleidoscope converging into sustainable business models. Journal of Cleaner Production, 167, 723–738. https://doi.org/10.1016/j.jclepro.2017.08.118

Nadarajah, D., & Kadir, S. L. S. A. (2014). A review of the importance of business process management in achieving sustainable competitive advantage. TQM Journal, 26(5), 522–531. https://doi.org/10.1108/TQM-01-2013-0008

Ning, S., Jie, X., & Li, X. (2022). Institutional pressures and corporate green innovation; empirical evidence from chinese manufacturing enterprises. Polish Journal of Environmental Studies, 31(1), 231–243.

O’Brien, M., Bleischwitz, R., Steger, S., & Fischer, S. (2013). Europe in transition: Paving the way to a green economy through eco-innovation. In Eco-Innovation Observatory (Issue January). https://doi.org/10.13140/RG.2.1.4992.0409

Oxborrow, L., & Brindley, C. (2013). Adoption of “eco-advantage” by SMEs: Emerging opportunities and constraints. European Journal of Innovation Management, 16(3), 355–375.

Passaro, R., Quinto, I., Scandurra, G., & Thomas, A. (2022). The drivers of eco-innovations in small and medium-sized enterprises: A systematic literature review and research directions. Business Strategy and the Environment, 32(4), 1432–1450. https://doi.org/10.1002/bse.3197

Peng, X., & Liu, Y. (2016). Behind eco-innovation: Managerial environmental awareness and external resource acquisition. Journal of Cleaner Production, 139, 347–360. https://doi.org/10.1016/j.jclepro.2016.08.051

Pérez-Luño, A., Valle Cabrera, R., & Wiklund, J. (2007). Innovation and imitation as sources of sustainable competitive advantage. Management Research: Journal of the Iberoamerican Academy of Management, 5(2), 71–82. https://doi.org/10.2753/JMR1536-5433050201

Pituch, K. A., & Stevens, J. P. (2015). Applied multivariate statistics for the social sciences: Analyses with SAS and IBM’s SPSS. Routledge.

Podsakoff, P. M., MacKenzie, S. B., Lee, J.-Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology, 88(5), 879.

Podsakoff, P. M., MacKenzie, S. B., & Podsakoff, N. P. (2012). Sources of method bias in social science research and recommendations on how to control it. Annual Review of Psychology, 63, 539–569. https://doi.org/10.1146/annurev-psych-120710-100452

Porter, M. E. (1985). Technology and competitive advantage. Journal of Business Strategy, 5(3), 60–78.

Porter, M. E., & Van Der Linde, C. (1995). Green and competitive: Ending the stalemate. Harvard Business Review, 73(5), 120–134.

Pratono, A. H., Darmasetiawan, N. K., Yudiarso, A., & Jeong, B. G. (2019). Achieving sustainable competitive advantage through green entrepreneurial orientation and market orientation. The Bottom Line, 32(1), 2–15. https://doi.org/10.1108/BL-10-2018-0045

Qi, G., Jia, Y., & Zou, H. (2021). Is institutional pressure the mother of green innovation? Examining the moderating effect of absorptive capacity. Journal of Cleaner Production, 278, 123957. https://doi.org/10.1016/j.jclepro.2020.123957

Qi, G., Zou, H., & Xie, X. (2020). Governmental inspection and green innovation: Examining the role of environmental capability and institutional development. Corporate Social Responsibility and Environmental Management, 27(4), 1774–1785. https://doi.org/10.1002/csr.1924

Quaye, D., & Mensah, I. (2019). keting innovation and sustainable competitive advantage of manufacturing SMEs in Ghana. Management Decision, 57(7), 1535–1553. https://doi.org/10.1108/MD-08-2017-0784

Ramanathan, R., Poomkaew, B., & Nath, P. (2014). The impact of organizational pressures on environmental performance of firms. Business Ethics: A European Review, 23(2), 169–182. https://doi.org/10.1111/beer.12042

Rowley, J. (2014). Designing and using research questionnaires. Management Research Review, 37(3), 308–330.

Sáez-Martínez, F. J., Díaz-García, C., & Gonzalez-Moreno, A. (2016). Firm technological trajectory as a driver of eco-innovation in young small and medium-sized enterprises. Journal of Cleaner Production, 138, 28–37. https://doi.org/10.1016/j.jclepro.2016.04.108

Sarstedt, M., Ringle, C. M., & Hair, J. F. (2017). Treating unobserved heterogeneity in PLS-SEM: A multi-method approach. Partial Least Squares Path Modeling: Basic Concepts, Methodological Issues and Applications, 197–217.

Saunders, M., Lewis, P., & Thornhill, A. (2009). Research methods for business students. Prentice Hall.

Scott, W. R. (1987). The adolescence of institutional theory. Administrative Science Quarterly, 32(4), 493–511. https://doi.org/10.2307/2392880

Sellitto, M. A., Camfield, C. G., & Buzuku, S. (2020). Green innovation and competitive advantages in a furniture industrial cluster: A survey and structural model. Sustainable Production and Consumption, 23, 94–104. https://doi.org/10.1016/j.spc.2020.04.007

Sharfman, M. P., Shaft, T. M., & Tihanyi, L. (2004). A model of the global and institutional antecedents of high-level corporate environmental performance. Business & Society, 43(1), 6–36. https://doi.org/10.1177/0007650304262962

Sharma, A., & Foropon, C. (2019). Green product attributes and green purchase behavior: A theory of planned behavior perspective with implications for circular economy. Management Decision, 57(4), 1018–1042. https://doi.org/10.1108/MD-10-2018-1092

Simpson, D. (2012). Institutional pressure and waste reduction: The role of investments in waste reduction resources. International Journal of Production Economics, 139(1), 330–339. https://doi.org/10.1016/j.ijpe.2012.05.020

Song, J., & Wang, L. (2011). Research on the effect of environmental regulation on the competitiveness of coal enterprises in Henan Province. Procedia Engineering, 15, 1519–1523. https://doi.org/10.1016/j.proeng.2011.08.282

Testa, F., Iraldo, F., & Frey, M. (2011). The effect of environmental regulation on firms’ competitive performance: The case of the building & construction sector in some EU regions. Journal of Environmental Management, 92(9), 2136–2144. https://doi.org/10.1016/j.jenvman.2011.03.039

Triguero, A., Moreno-Mondéjar, L., & Davia, M. A. (2013). Drivers of different types of eco-innovation in European SMEs. Ecological Economics, 92, 25–33. https://doi.org/10.1016/j.ecolecon.2013.04.009

Tumelero, C., Sbragia, R., & Evans, S. (2018). Cooperation in R & D and eco-innovations: The role on the companies’ socioeconomic performance. Journal of Cleaner Production, 207, 1138–1149.

Wang, S., Li, J., & Zhao, D. (2018). Institutional pressures and environmental management practices: The moderating effects of environmental commitment and resource availability. Business Strategy and the Environment, 27(1), 52–69. https://doi.org/10.1002/bse.1983

Williams, C., & Spielmann, N. (2019). Institutional pressures and international market orientation in SMEs: Insights from the French wine industry. International Business Review, 28(5), 101582. https://doi.org/10.1016/j.ibusrev.2019.05.002

Wu, L., Wang, L., Philipsen, N. J., & Fang, X. (2024). The impact of eco-innovation on environmental performance in different regional settings: new evidence from Chinese cities. Environment, Development and Sustainability. https://doi.org/10.1007/s10668-023-04280-z

Xiumei, X., Ruolan, J., Shahzad, U., & Xiao, F. (2023). Sustainable innovation in small and medium-sized enterprises: Environmental regulations and digitalization as catalyst. Journal of Environment and Development, 32(4), 413–443. https://doi.org/10.1177/10704965231211585

Yang, Z., & Su, C. (2014). Institutional theory in business marketing: A conceptual framework and future directions. Industrial Marketing Management, 43(5), 721–725. https://doi.org/10.1016/j.indmarman.2014.04.001

Yu, W., Ramanathan, R., & Nath, P. (2017). Environmental pressures and performance: An analysis of the roles of environmental innovation strategy and marketing capability. Technological Forecasting and Social Change, 117, 160–169. https://doi.org/10.1016/j.techfore.2016.12.005

Yue, B., Sheng, G., She, S., & Xu, J. (2020). Impact of consumer environmental responsibility on green consumption behavior in China: The role of environmental concern and price sensitivity. Sustainability (switzerland), 12(5), 1–16. https://doi.org/10.3390/su12052074

Zameer, H., Wang, Y., & Saeed, M. R. (2021). Net-zero emission targets and the role of managerial environmental awareness, customer pressure, and regulatory control toward environmental performance. Business Strategy and the Environment, 30(8), 4223–4236. https://doi.org/10.1002/bse.2866

Zameer, H., Wang, Y., & Yasmeen, H. (2020a). Reinforcing green competitive advantage through green production, creativity and green brand image: Implications for cleaner production in China. Journal of Cleaner Production, 247, 119119. https://doi.org/10.1016/j.jclepro.2019.119119

Zameer, H., Wang, Y., Yasmeen, H., & Mubarak, S. (2020b). Green innovation as a mediator in the impact of business analytics and environmental orientation on green competitive advantage. Management Decision, 60(2), 71873064. https://doi.org/10.1108/MD-01-2020-0065

Zhao, X., Zhao, Y., Zeng, S., & Zhang, S. (2015). Corporate behavior and competitiveness: Impact of environmental regulation on Chinese firms. Journal of Cleaner Production, 86, 311–322. https://doi.org/10.1016/j.jclepro.2014.08.074

Zhou, Y., Luo, L., & Shen, H. (2022). Community pressure, regulatory pressure and corporate environmental performance. Australian Journal of Management, 47(2), 368–392. https://doi.org/10.1177/03128962211017172

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1: Mardia’s output of skewness and kurtosis calculation

https://webpower.psychstat.org/models/kurtosis/results.php?url=f754b3082ed63ecc44298cbfe253c953

Appendix 2: Measurement model assessment

Appendix 3: Structural model assessment

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Mady, K., Anwar, I. & Abdelkareem, R.S. Nexus between regulatory pressure, eco-friendly product demand and sustainable competitive advantage of manufacturing small and medium-sized enterprises: the mediating role of eco-innovation. Environ Dev Sustain (2024). https://doi.org/10.1007/s10668-024-05096-1

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s10668-024-05096-1