Abstract

The shipping industry has unique financial characteristics: it is capital intensive, faces highly volatile freight rates and ship prices, and exhibits strong cyclicality and seasonality. It is a sector which has a unique corporate structure, as it is normally highly geared and relies extensively on debt financing. Shipping is also a conservative sector favouring traditional finance and tapping the global capital market much later than other industries. In this sense, the shipping industry deserves its own enquiry into its financial characteristics. This paper considers listed shipping companies worldwide in terms of their overall financial performance. While default against individual financial instruments can represent early phases of corporate failure, predicting overall failure at the firm level is worth investigating. This paper studies corporate failure and financial performance in globally listed shipping firms, examining the different characteristics of financial risks, and investigating how these characteristics vary over time. A new technique, the receiver-operating characteristic curve, is introduced to compare the overall accuracies of various models for predicting binary outcomes. The findings in respect of shipping finance for listed shipping companies can benefit both shipowners and investors.

Similar content being viewed by others

Notes

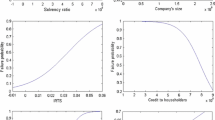

Indeed, when these factors are included in the same regression, with different possible combinations of measurement, it is found that none of the financial ratios—except for TD/TA—is significant.

The ‘6-month before’ version includes ‘ship’ as an intercept dummy.

This is mainly because the total correction rate does not discriminate between type I and type II errors, so the relationship between the total correction rate and the trade-off between type I and type II errors is quite independent over different cases.

See Zweig and Campbell (1993) for a thorough illustration of the method.

Recall that this optimal version predicted 76.5% of the true failed cases and 76.5% of the true survived cases according to its confusion matrix—see Table 4.

The draws are conducted with the bootstrap technique.

Thus, the Pareto ‘80-20 principle’ is followed when segmenting the sample.

References

Aharony, J., C.P. Jones, and I. Swary. 1980. An analysis of risk and return characteristics of corporate bankruptcy using capital market data. The Journal of Finance 35 (4): 1001–1016.

Albertijn, S., W. Bessler, and W. Drobetz. 2011. Financing shipping companies and shipping operations: A risk-management perspective. Journal of Applied Corporate Finance, Fall 23 (4): 70–82.

Altman, E.I. 1968. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The Journal of Finance 23 (4): 589–609.

Andreou, P.C., C. Louca, and P.M. Panayides. 2014. Corporate governance, financial management decisions and firm performance: Evidence from the maritime industry. Transportation Research Part E: Logistics and Transportation Review 63: 59–78.

Argenti, J. 1976. Corporate collapse: The causes and symptoms, 193. London: McGraw-Hill.

Barniv, R., A. Agarwal, and R. Leach. 2002. Predicting Bankruptcy Resolution. Journal of Business Finance and Accounting 29 (3–4): 497–520.

Birchenhall, C., H. Jessen, D. Osborn, and P. Simpson. 1999. Predicting U.S. business-cycle regimes. Journal of Business & Economic Statistics 17 (3): 313–323.

Bonfim, D. 2009. Credit risk drivers: Evaluating the contribution of firm level information and of macroeconomic dynamics. Journal of Banking & Finance 33: 281–299.

Brown, P., W. Beekes, and P. Verhoeven. 2011. Corporate governance, accounting and finance: A review. Accounting and Finance 51: 96–172.

Campbell, J.Y., J. Hilscher, and J. Szilagyi. 2008. In search of distress risk. The Journal of Finance 63 (6): 2899–2938.

Chan, K.C., and N.-F. Chen. 1991. Structural and return characteristics of small and large firms. The Journal of Finance 46: 1467–1484.

Charalambous, C., A. Charitou, and F. Kaourou. 2000. Comparative analysis of artificial neural network models: Application in bankruptcy prediction. Annals of Operations Research 99: 403–425.

Charitou, A., E. Neophytou, and C. Charalambous. 2004. Predicting corporate failure: Empirical evidence for the UK. European Accounting Review 13 (3): 465–497.

Christensen, R. 1997. Log-Linear Models and Logistic Regression, 2nd ed. New York: Springer.

Clarksons. 2017. Shipping intelligence network. https://sin.clarksons.net.

Dambolena, I.G., and S.J. Khoury. 1980. Ratio stability and corporate failure. The Journal of Finance 35 (4): 1017–1026.

Drobetz, W., D. Gounopoulos, A. Merikas, and H. Schröder. 2013. Capital structure decisions of globally-listed shipping companies. Transportation Research Part E: Logistics and Transportation Review 52: 49–76.

Erkens, D.H., M. Hung, and P. Matos. 2012. Corporate governance in the 2007–2008 financial crisis: Evidence from financial institutions worldwide. Journal of Corporate Finance 18 (2): 389–411.

Fama, E.F., and K.R. French. 1996. Multifactor explanations of asset pricing anomalies. The Journal of Finance 51: 55–84.

Gavalas, D., and T. Syriopoulos. 2015. An integrated credit rating and loan quality model: Application to bank shipping finance. Maritime Policy and Management 42 (6): 533–554.

Giroud, X., and H. Mueller. 2011. Corporate governance, product market competition, and equity prices. The Journal of Finance 66: 563–600.

Gompers, P.A., J.L. Ishii, and A. Metrick. 2003. Corporate governance and equity prices. Quarterly Journal of Economics 118: 107–155.

Grammenos, C.T., A.H. Alizadeh, and N.C. Papapostolou. 2007. Factors affecting the dynamics of yield premia on shipping seasoned high yield bonds. Transportation Research Part E: Logistics and Transportation Review 43 (5): 549–564.

Grammenos, C.T., and N.S. Marcoulis. 1996. Shipping initial public offerings: A cross-country analysis. In Empirical issues in raising equity capital, ed. M. Levis, 379–400. Amsterdam: Elsevier.

Grammenos, C.T., N.K. Nomikos, and N.C. Papapostolou. 2008. Estimating the probability of default for shipping high yield bond issues. Transportation Research Part E: Logistics and Transportation Review 44 (6): 1123–1138.

Grammenos, C.T., and N.C. Papapostolou. 2012a. US shipping initial public offerings: Do prospectus and market information matter? Transportation Research Part E: Logistics and Transportation Review 48 (1): 276–295.

Grammenos, C.T., and N.C. Papapostolou. 2012b. Ship finance: US public equity markets, Chap. 20. In The Blackwell companion to maritime economics, ed. W. Talley, 735. London: Blackwell.

Jensen, M.C., and W.H. Meckling. 1976. Theory of the firm: managerial behaviour, agency costs and ownership structure. Journal of Financial Economics 3 (4): 305–360.

Kavussanos, M.G., and D.A. Tsouknidis. 2016. Default risk drivers in shipping bank loans. Transportation Research Part E: Logistics and Transportation Review 94: 71–94.

Lev, B. 1974. Financial statement analysis: A new approach. Upper Saddle River: Prentice-Hall.

McCullagh, P., and J.A. Nelder. 1989. Generalized Linear Models, 2nd ed, 532 pp. Florida: Chapman and Hall/CRC.

Mitroussi, K., J. Xu, S. Pettit, and N. Tigka. 2012. Performance drivers of shipping loans: An empirical investigation. In Conference Proceedings, International Association of Maritime Economists Annual Conference, Taipei, 5–8 September 2012.

Mitroussi, K., J. Xu, S. Pettit, W. Abouarghoub, and N. Tigka. 2016. Performance drivers of shipping loans: An empirical investigation. International Journal of Production Economics 171 (3): 438–452.

Morris, R.C. 1997. Early warning indicators of corporate failure: A critical review of previous research and further empirical evidence. Aldershot: Ashgate Publishing in association with the Institute of Chartered Accountants in England and Wales.

Ng, E. 2012. Forecasting US recessions with various risk factors and dynamic probit models. Journal of Macroeconomics 34 (1): 112–125.

Nyberg, H. 2010. Dynamic probit models and financial variables in recession forecasting. Journal of Forecasting 29 (1–2): 215–230.

Rees, B. 1990. Financial analysis, 1st ed. Hertfordshire: Prentice Hall.

Seitz, N. 1984. Financial analysis—A programmed approach, 3rd ed. Virginia: Reston Publishing.

Stopford, M. 2009. Maritime economics, 3rd ed. New York: Taylor & Francis.

Syriopoulos, T., and I. Theotokas. 2007. Value creation through corporate destruction? Corporate governance in shipping takeovers. Maritime Policy and Management 34 (3): 225–242.

Syriopoulos, T., and M. Tsatsaronis. 2011. The corporate governance model of the shipping firms: Financial performance implications. Maritime Policy and Management 38 (6): 585–604.

Tamari, M. 1978. Financial ratios, 182. Bath: Pitman Press.

UNCTAD. 2016. Review of maritime transport. Geneva: United Nations Conference on Trade and Development.

Warner, J.B. 1977. Bankruptcy, absolute priority, and the pricing of risky debt claims. Journal of Financial Economics 4 (3): 239–276.

Wayman, R. 2015. Operating cash flow: Better than net income? http://www.investopedia.com/articles/analyst/03/122203.asp.

Yurdakul, M., and Y.T. Ic. 2004. AHP approach in the credit evaluation of the manufacturing firms in Turkey. International Journal of Production Economics 88: 269–289.

Zavgren, C. 1983. The prediction of corporate failure: The state of the art. Journal of Accounting Literature 2 (1983): 1–37.

Zweig, M.H., and G. Campbell. 1993. Receiver-operating characteristic (ROC) plots: A fundamental evaluation tool in clinical medicine’. Clinical Chemistry 39 (8): 561–577.

Acknowledgements

The authors would like to extend their gratitude to the journal’s reviewers for their in-depth comments, guidance and useful advice.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Haider, J., Ou, Z. & Pettit, S. Predicting corporate failure for listed shipping companies. Marit Econ Logist 21, 415–438 (2019). https://doi.org/10.1057/s41278-018-0101-4

Published:

Issue Date:

DOI: https://doi.org/10.1057/s41278-018-0101-4