Abstract

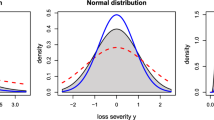

In an earlier paper, we proposed a Bayesian approach towards estimating the Value-at-Risk of an insurance loss ratio, taking into account both the parameter risk and the model risk. In this paper, we apply the approach to real data and evaluate the plausibility of the estimators.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

References

Kondo, H., Saito, S.: Bayesian approach to measuring parameter and model risk in loss ratio estimation. J. Math. Ind. 4(B), 85–89 (2012)

The General Insurance Association of Japan: Hoken Shumoku Betsu Songai Ritsu (loss ratios by line). http://www.sonpo.or.jp/archive/statistics/syumoku/pdf/index/syumoku_songairitu.pdf (2013). Accessed 22 Feb 2014

The General Insurance Association of Japan: General Insurance in Japan fact book 2012–2013. http://www.sonpo.or.jp/en/publication/pdf/fb2013e.pdf (2013). Accessed 22 Feb 2014

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2014 Springer Japan

About this paper

Cite this paper

Kondo, H., Saito, S. (2014). Applicability of Bayesian Methods for Loss Ratio Estimation. In: Wakayama, M., et al. The Impact of Applications on Mathematics. Mathematics for Industry, vol 1. Springer, Tokyo. https://doi.org/10.1007/978-4-431-54907-9_22

Download citation

DOI: https://doi.org/10.1007/978-4-431-54907-9_22

Published:

Publisher Name: Springer, Tokyo

Print ISBN: 978-4-431-54906-2

Online ISBN: 978-4-431-54907-9

eBook Packages: EngineeringEngineering (R0)