Abstract

We obtain the optimal contract for the government (principal) to regulate a manager (agent) who has a taste for empire-building that is his/her private information. This taste for empire-building is modeled as a utility premium that is proportional to the difference between the contracted output and a reference output. We find that output is distorted upward when the manager’s taste for running large firms is weak, downward when it is strong, and equals a reference output when it is intermediate (in this case, the participation constraint is binding). We also obtain an endogenous reference output (equal to the expected output, which depends on the reference output), and find that the response of output to cost is null in the short-run (in which the reference output is fixed), whenever the manager’s type is in the intermediate range, and negative in the long-run (after the adjustment of the reference output to equal expected output).

Similar content being viewed by others

Notes

The preference for high output is related to the preference for staff considered by Williamson (1974).

More precisely, the government offers an incentive compatible set of contracts, one for each possible type of manager.

Stulz (1990), Hart and Moore (1995) and Li and Li (1996) concluded that there is overinvestment when the free cash-flow from previous investments is higher than expected, and underinvestment when it is lower. Assuming that managers have private information about productivity, Harris and Raviv (1966) concluded that there is underinvestment when productivity is higher than expected and overinvestment when productivity it is lower.

In Sect. 5.2, we propose an endogenous determination of this reference level of output.

We also allow for intermediate cases, i.e., any \(k \in (0,1)\).

In some circumstances, managers may be willing to pay a fraction of the production costs, as in some volunteering activities or internships.

By the revelation principle (Myerson 1979), given a Bayesian Nash equilibrium of a game of incomplete information, there exists a direct mechanism that has an equivalent equilibrium where the players truthfully report their types. A direct-revelation mechanism is said to be incentive compatible if, when each individual is expecting the others to be truthful, then he/she has interest in being truthful.

In the light of Proposition , it will be clear that the government obtains a positive payoff for all types \(\delta \in \left[\underline{\delta },\overline{\delta }\right]\) if and only if the reference output, \(q_{ref}\), is below a certain threshold.

This includes, for example, the case in which the participation constraint is only binding at one of the extremes of the interval (\(\delta _0 = \delta _1 = \underline{\delta }\) or \(\delta _0 = \delta _1 = \overline{\delta }\)).

This is in the spirit of Kőszegi and Rabin (2006), where the reference point of an agent corresponds to his/her rational expectation about a certain outcome.

We thank two anonymous referees for pointing out these two issues.

If we interpret the choice behavior of the managers as resulting from the objective function \(U = t + \delta q\), with participation requiring \(U \ge \delta q_{ref}\).

This looks like the result obtained by Sweezy (1939) in the very different framework of “the kinked oligopoly demand curve”.

See Basov (2005), pp. 124–126.

The participation constraint must be binding for some \(\delta \), otherwise the government could increase expected social welfare by reducing the transfers to all types of managers without violating the participation and the incentive constraints.

References

Arya A, Baldenius T, Glover J (1999) Residual Income, Depreciation, and Empire Building. Working Paper

Baron DP, Myerson RB (1982) Regulating a monopolist with unknown costs. Econometrica 50(4):911–930

Basov S (2005) Multidimensional screening. In: Studies in economic theory, vol 22. Springer, Berlin

Baumol WJ (1959) Business behavior, value and growth. Macmillan, New York

Borges AP, Correia-da-Silva J (2011) Using cost observation to regulate a manager who has a preference for empire-building. Manch Schl 79(1):29–44

Brehm J, Gates S (1997) Working, shirking, and sabotage: bureaucratic response to a democratic public. University of Michigan Press, Ann Arbor

Brown JR, Liang N, Weisbenner S (2007) Executive financial incentives and payout policy: firm responses to the 2003 dividend tax cut. J Finance 62(4):1935–1965

Chetty R, Saez E (2005) Dividend taxes and corporate behavior: evidence from the 2003 dividend tax cut. Q J Econ 120(3):791–833

Donaldson G (1984) Managing corporate wealth. Praeger, New York

Grossman S, Hart O (1988) One share-one vote and the market for corporate control. J Financial Econ 20:175–202

Guesnerie R, Laffont J-J (1984) A complete solution to a class of principal-agent problems with an application to the control of a self-managed firm. J Public Econ 25:329–369

Harris M, Raviv A (1996) The capital budgeting process: incentives and information. J Finance 51:1139–1174

Hart O, Moore J (1995) Debt and seniority: an analysis of the role of hard claims in constraining management. Am Econ Re 85(3):567–585

Jensen MC (1986) Agency costs of free cash flow, corporate finance and take-overs. Am Econ Rev 76(2):3323–3329

Jensen MC (1993) The modern industrial revolution, exit, and the failure of internal control systems. J Finance 48:831–880

Jullien B (2000) Participation constraints in adverse selection models. J Econ Theory 93(1):1–47

Kanniainen V (2000) Empire building by corporate managers: the corporation as a savings instrument. J Econ Dyn Control 24:127–142

Kőszegi B, Rabin M (2006) A model of reference-dependent preferences. Q J Econ 121(4):1133–1165

Laffont J-J, Martimort D (2002) The theory of incentives: the principal-agent model. Princeton University Press, Princeton

Laffont J-J, Tirole J (1986) Using cost observation to regulate firms. J Polit Econ 94(3):614–641

Laffont J-J, Tirole J (1993) A theory of incentives in procurement and regulation. MIT Press, Cambridge

Lewis TR, Sappington DEM (1989) Countervailing incentives in agency problems. J Econ Theory 49(2):294–313

Li DD, Li S (1996) A theory of corporate scope and financial structure. J Finance 51(2):691–709

Maggi G, Rodriguéz-Clare A (1995) On countervailing incentives. J Econ Theory 66(1):238–263

Marris R (1963) A model of the ‘Managerial’ enterprise. Q J Econ 77(2):185–209

Maskin E, Riley J (1984) Monopoly with incomplete information. RAND J Econ 15(2):171–196

Myerson RB (1979) Incentive compatibility and the bargaining problem. Econometrica 47(1):61–74

Niskanen WA (1971) Bureaucracy and representative government. Aldine-Atherton, Chicago

Prendergast E (2007) The motivation and bias of bureaucrats. Am Econ Rev 97(1):180–196

Stulz RM (1990) Managerial discretion and optimal financing policies. J Finan Econ 26:3–27

Sweezy PM (1939) Demand under conditions of oligopoly. J Polit Econ 47:568–573

Williamson OE (1974) The economics of discretionary behavior: managerial objectives in a theory of the firm. Academic Book Publishers, London

Wilson JQ (1989) Bureaucracy: what government agencies do and why they do it. Basic Books, New York

Zwiebel J (1996) Dynamic capital structure under management entrenchment. Am Econ Rev 86(5):1197–1215

Acknowledgments

We are grateful to Inés Macho-Stadler, David Pérez-Castrillo and two anonymous referees for very useful comments and suggestions, and we thank participants in the 2009 SAET Conference and the 3rd Economic Theory Workshop in Vigo. Ana Pinto Borges and João Correia-da-Silva thank Fundação para a Ciência e Tecnologia and FEDER for financial support (research grants PTDC/EGE-ECO/114881/2009 and PTDC/EGE-ECO/111811/2009).

Author information

Authors and Affiliations

Corresponding author

A. Appendix

A. Appendix

1.1 A.1. Incentive compatibility conditions

1.1.1 A.1.1. Differentiability of output, transfer, and utility functions

In this section, we prove that if (2) holds, then the output, transfer and value functions are almost everywhere differentiable.

For simplicity of exposition, we will denote by \(U (\tilde{\delta },\delta )\) the utility attained by a manager that announces \(\tilde{\delta }\) when his/her type is \(\delta \).

Claim 1

\(\tilde{\delta } < \delta \Rightarrow q(\tilde{\delta }) \le q(\delta )\).

Proof

If (2) holds, then:

Adding the two inequalities, we obtain:

Then, \(\delta - \tilde{\delta } > 0\) implies that \(q(\delta ) - q(\tilde{\delta }) \ge 0\). \(\square \)

Claim 2

\(U(\tilde{\delta },\delta )\), as a function of \(\tilde{\delta }\), is nondecreasing on \(\left[\underline{\delta },\delta \right]\) and nonincreasing on \(\left[\delta ,\overline{\delta }\right]\).

Proof

Let us show monotonicity on \(\left[\underline{\delta },\delta \right]\). Assume that \(\tilde{\delta } < \delta ^{\prime } < \delta \) and, by way of contradiction, \(U(\tilde{\delta },\delta ) > U(\delta ^{\prime },\delta )\), that is:

On the other hand, we know that a firm of type \(\delta ^{\prime }\) prefers to announce \(\delta ^{\prime }\) rather than announce \(\tilde{\delta }\):

Adding the last two equations, we obtain:

Which is in contradiction with Claim 1.

Monotonicity on \(\left[\delta ,\bar{\delta }\right]\) can be proved in the same way. \(\square \)

Claims 1 and 2 imply that the functions \(q(\delta )\) and \(t(\delta )+\delta ^{\prime } \left[q(\delta ) - q_{ref}\right]\) are a.e. differentiable. Hence, \(t(\delta )\) and \(V(\delta ) = t(\delta )+\delta \left[q(\delta ) - q_{ref}\right]\) are also a.e. differentiable.

1.1.2 A.1.2. Second-order incentive compatibility condition

The local second-order condition of the maximization program is:

We want to show that (given the first-order condition) it is equivalent to \(q^{\prime }(\delta ) \ge 0\).

Differentiating (3) with respect to \(\delta \), we obtain:

Subtracting (12) from (11), the local second-order condition becomes: \(q^{\prime }(\delta ) \ge 0\).

1.1.3 A.1.3. The local second-order condition implies the global one

Claim 3

The first and second incentive compatibility conditions, () and (5), imply that truth-telling is optimal (the local second-order condition implies the global one).

Proof

For \(\tilde{\delta } > \delta \) (a similar reasoning applies to \(\tilde{\delta } < \delta \)):

To finish the proof, it is only necessary to show that \(\int _{\delta }^{\tilde{\delta }} t^{\prime }(\gamma ) + \delta q^{\prime }(\gamma ) d\gamma \le 0\).

From the second-order condition, \(q^{\prime }(\gamma ) \ge 0\), it is clear that:

The first-order condition, \(t^{\prime }(\gamma ) + \gamma q^{\prime }(\gamma ) = 0\), implies that \(\int _{\delta }^{\tilde{\delta }} t^{\prime }(\gamma ) + \gamma q^{\prime }(\gamma ) d\gamma = 0\). \(\square \)

1.2 A.2 Level of output and sign of net transfer

In the interval in which the participation constraint is binding, we must have \(q(\delta ) = q_{ref}\) and \(t(\delta ) = 0\).

For \(\delta < \delta _0\), since \(q(\delta )\) is non-decreasing and \(V(\delta )>0\), we must have \(q(\delta ) < q_{ref}\). It should be clear that if \(q(\delta ) = q_{ref}\), then \(q(\delta ^{\prime }) = q_{ref}\) for all \(\delta ^{\prime } \in \left[ \delta , \delta _0 \right]\), and, from (4), \(V(\delta )=0\) (contradicting the fact that \(\delta < \delta _0\)). Since \(q(\delta ) < q_{ref}\), participation implies that \(t(\delta ) > 0\).

Similarly, for \(\delta > \delta _1\), we must have \(q(\delta ) > q_{ref}\). To avoid type \(\delta _1\) from mimicking type \(\delta \), it is necessary that \(t(\delta ) < 0\).

1.3 A.3 Problem of the government

We start by defining a relaxed problem in which the second-order incentive compatibility condition (5) is ignored. After solving this relaxed problem, we will check that its solution is also the solution of the general problem (6).

1.3.1 A.3.1. Solution of the relaxed problem

Consider a relaxed problem in which condition (5) is omitted.

Incorporating the participation constraint in the objective function, this relaxed problem can be written as follows:Footnote 17

subject to, for all \(\delta \),

where \(\eta (\delta )\) satisfies \(\eta (\delta ) \ge 0\) and \(\eta (\delta ) \lambda V(\delta ) = 0\). Notice that \(\eta (\delta ) \lambda \) is the Lagrangian multiplier associated to the participation constraint of type \(\delta \).Footnote 18

Necessary conditions

The Hamiltonian is

where \(\mu (\delta )\) is the co-state variable associated with the incentive constraint (4).

The first-order conditions imply that:

Equation (15a) is the equation of motion of the co-state variable. Equation (15d) is the complementary slackness condition. Equation (15e) gives the transversality conditions.

Let \(\zeta (\delta )=\int _{\underline{\delta }}^{\delta }\eta (s)ds\). It is shown below that \(\eta \) is a probability distribution on \(\left[\underline{\delta },\overline{\delta }\right]\), and that, therefore, \(\zeta (\delta )\) is a c.d.f. on \(\left[\underline{\delta },\overline{\delta }\right]\).

Integrating Eq. (15a) we obtain:

and using (15e):

These last two equations imply that:

meaning that \(\eta (\cdot )\) is a probability distribution on \(\left[\underline{\delta },\overline{\delta }\right]\) and \(\zeta (\cdot )\) is the corresponding c.d.f..

Replacing Eq. (16) into (15c), we find that output is such that:

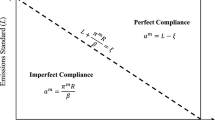

The only difference with respect to the complete information case is the last term. It should be clear that \(\zeta (\delta )=1\) implies downward distortion and \(\zeta (\delta )=0\) implies upward distortion.

Note that if the participation constraint () is not binding on some open interval, \(\left(\delta _a,\delta _b\right)\), then \(\zeta (\cdot )\) is constant on it, since \(\zeta ^{\prime }(\delta )= \eta (\delta )=0\).

Sufficient condition

The second order derivative of the Hamiltonian (14) is: \(\frac{\partial ^{2}H}{\partial q^{2}}=S^{\prime \prime }\left[ q(\delta )\right] <0\).

1.3.2 A.3.2 Solution of the general problem

We now check that the condition that was omitted in the relaxed problem (13), \(q^{\prime }(\delta )\ge 0\), is satisfied. Differentiating Eq. (17) with respect to \(\delta \), we obtain:

The assumption of monotone hazard rates is used here. Observe that:

and

For \(\delta < \delta _0\), we have \(\eta (\delta )=0\) and \( \zeta (\delta )=0\), implying that:

For \(\delta > \delta _1\), we have \(\eta (\delta )=0\) and \(\zeta (\delta )=1\), implying that:

When the participation constraint is binding, \(q(\delta ) = q_{ref}\) and, therefore, \(q^{\prime }(\delta )=0\). This implies that (5) is verified. The solution of the unconstrained problem (13) is also the solution of the general problem (6).

We also conclude that the output level is strictly increasing with \(\delta \) over the two intervals \(\left[\underline{\delta },\delta _0\right]\) and \(\left[\delta _1,\overline{\delta }\right]\), being constant and equal to \(q_{ref}\) in \(\left[\delta _0,\delta _1\right]\).

From (3), when the output level is strictly increasing, the monetary transfer, \(t(\delta )\), is strictly decreasing.

1.3.3 A.3.3 Output distortions

If \(\delta < \delta _0\), then \(\zeta (\delta ) = 0\) and the output is such that:

In the case of complete information, we had \(S^{\prime }\left[ q^*_c(\delta )\right] = (1+\lambda )(\beta -\delta ) + k\delta \), which is greater than \(S^{\prime }\left[ q(\delta )\right]\). Therefore, \(q(\delta ) > q^*_c(\delta )\).

If \(\delta > \delta _1\), then \(\zeta (\delta ) = 1\) and the output is such that:

With complete information, \(S^{\prime }\left[ q^*_c(\delta )\right] = (1+\lambda )(\beta -\delta ) + k\delta \), which is smaller than \(S^{\prime }\left[ q(\delta )\right]\). Therefore, \(q(\delta ) < q^*_c(\delta )\).

1.4 A.4 Quadratic social value and uniform distribution

Characterizing the optimal output level and the manager’s utility over the interval \(\left[ \delta _0,\delta _1\right]\) is straightforward. When \(\delta \in \left[\delta _0,\delta _1\right]\), the participation constraint is binding: \(V(\delta )=0\). From the first incentive compatibility constraint (4), we have \(q(\delta )=q_{ref}, \, \forall \, \delta \in \left[\delta _0,\delta _1\right]\).

Below, we obtain the values of \(\delta _0\) and \(\delta _1\) and we study the two intervals where the participation constraint is not binding: \(\delta \in \left[ 0,\delta _0 \right)\) and \(\delta \in \left(\delta _1,1\right]\).

1.4.1 A.4.1 The values of \(\delta _0\) and \(\delta _1\)

From (17), we know that:

Since \(\zeta (0)=0\) and \(\eta (\delta ) = 0\) for all \(\delta < \delta _0\), we must have \(\zeta (\delta _0)=0\). Replacing in Eq. (18) and using the fact that \(q(\delta _0)=q_{ref}\), we obtain:

When \(q_{ref} > \alpha - (1 + \lambda )\beta \equiv q^*(0)\), we obtain \(\delta _0 > 0\), whereas, when \(q_{ref} \le \alpha - (1 + \lambda )\beta \), bunching occurs at the bottom of the interval, i.e., \(\delta _0=0\).

Since \(\zeta (1)=1\) and \(\eta (\delta ) = 0\) for all \(\delta > \delta _1\), it must be the case that \(\zeta (\delta _1)=1\). Replacing in Eq. (18) and using \(q(\delta _1)=q_{ref}\), we obtain:

When \(q_{ref} < \alpha - (1 + \lambda )\beta +1 + \lambda -k \equiv q^*(1)\), we obtain \(\delta _1 < 1\); whereas, when \(q_{ref} \ge \alpha - (1 + \lambda )\beta +1 + \lambda -k\), bunching occurs at the top of interval, i.e, \(\delta _1=1\).

1.4.2 A.4.2 When \(0 < \delta < \delta _0\)

When \(\delta _0 > 0\) and \(\delta \in \left(0,\delta _0\right)\), the participation constraint is not binding. Therefore, \(\zeta (\delta )\) is null on this interval, since \(\zeta (0)=0\) and \(\eta (\delta )=0\). From (17), we obtain:

Integrating Eq. (4), we obtain the manager’s attainable utility:

where \(C\) is an integration constant. To find \(C\), we use continuity of \(V\) at \(\delta =\delta _0\). We know that \(V(\delta _0)=0\). Then:

Substituting the expression for \(\delta _0\) given by Eq. (19), we obtain \(C\!=\!\frac{\left[ \alpha - (1+\lambda ) \beta - q_{ref} \right]^{2}}{2(1+2\lambda -k)}\).

We conclude that, for \(\delta \in [0,\delta _0)\), there is upward distortion, \(q(\delta )=q_c^*(\delta ) + \lambda \delta \), and a positive monetary transfer, \(t(\delta ) > 0\):

1.4.3 A.4.3. When \(\delta _1 < \delta < 1\)

When \(\delta _1 < 1\) and \(\delta \in \left(\delta _1,1\right)\), the participation constraint is not binding. Then, \(\zeta (\delta ) = 1\) on this interval, since \(\eta (\delta ) = 0\) and \(\zeta (1) = 1\). From (17), output is given by:

Integrating Eq. (), we obtain:

To find \(C\), we use continuity of \(V\) at \(\delta =\delta _1\). Since \(V(\delta _1)=0\):

With \(\delta _1\) given by Eq. (), we obtain \(C=\frac{\left[ \alpha - \beta (1+\lambda ) - q_{ref} - \lambda \right]^2}{2(1+2\lambda -k)}\).

We conclude that, for \(\delta \in (\delta _1,1]\), there is downward distortion, \(q(\delta )=q_c^*(\delta ) - \lambda (1-\delta )\), and a negative monetary transfer, \(t(\delta ) < 0\):

1.4.4 A.4.4 The government’s participation constraint

The regulator’s welfare when the agent’s type is \(\delta \) is:

Differentiating and accounting for the incentive compatibility condition (4) we obtain:

From condition (17), we know that:

Notice that here \(f(\delta )=1\) and \(F(\delta )=\delta \). Replacing in (), we obtain:

Let us consider the three possible cases:

-

(i)

When \(\delta \in \left[\delta _0,\delta _1\right]\), it easy to check that \(W^{\prime }(\delta )=0\).

-

(ii)

When \(\delta \in \left[ 0,\delta _0\right)\), we know that \(\zeta (\delta )=0\), \(q(\delta )<q_{ref}\) and \(q^{\prime }(\delta )>0\). Then, \(W^{\prime }(\delta )<0\).

-

(iii)

When \(\delta \in \left[ \delta _1,1\right]\), we know that \(\zeta (\delta )=1\), \(q(\delta )>q_{ref}\) and \(q^{\prime }(\delta )>0\). Then, \(W^{\prime }(\delta )>0\).

It is enough to guarantee that social welfare is non-negative for \(\delta \in \left[\delta _0,\delta _1\right]\), i.e., that:

1.4.5 A.4.5 Short-run and long-run cost-elasticity of output

Consider an initial situation in which the reference output is given endogenously. Start by considering the short-run effect of an increase in \(\beta \).

From (7), there is a short-run increase of both \(\delta _0\) and \(\delta _1\) (unless they are at their upper bound, which is \(\overline{\delta }\)). Denote by \(\delta ^{\prime }_0\) and \(\delta ^{\prime }_1\) the new threshold values. We can divide the managers in five groups.

-

(i)

Those that have a low preference for output before and after the shock (\(\delta \le \delta _0\)) will experience a decrease of their output, as can be verified by inspection of expression (21a).

-

(ii)

Those that initially have an intermediate preference for output but move to the lower range after the shock (\(\delta _0 \le \delta \le \delta ^{\prime }_0\)) will experience a decrease of their output, as their output changes from \(q_{ref}\) to a lower value.

-

(iii)

Those that have an intermediate preference for output before and after the shock (\(\delta ^{\prime }_0 \le \delta \le \delta _1\)) will not be affected by the cost shock.

-

(iv)

Those that initially have a high preference for output but move to the intermediate range after the shock (\(\delta _1 \le \delta \le \delta ^{\prime }_1\)) will experience a decrease of their output, as their output changes from a value greater than \(q_{ref}\) to \(q_{ref}\).

-

(v)

Those that have a high preference for output before and after the shock (\(\delta \ge \delta ^{\prime }_1\)) will experience a decrease of their output, as can be verified by inspection of expression (22a).

In the long-run, the reference output decreases, according to (9). As a result, the thresholds \(\delta _0\) and \(\delta _1\) return to their initial values, given by (10).

The impact of this adjustment from the short-run to the long-run on the five mentioned types of managers will be the following.

-

(i)

Managers with \(\delta \le \delta _0\) will not be affected by the adjustment of the reference output. See expression (21a). Their cost-elasticity of output is the same in the short and in the long-run.

-

(ii)

Managers with (\(\delta _0 \le \delta \le \delta ^{\prime }_0\)) will experience a decrease of their output during the adjustment, to equal the new reference output. Their cost-elasticity of output is higher (more negative) in the long-run than in the short-run.

-

(iii)

Managers with \(\delta ^{\prime }_0 \le \delta \le \delta _1\) will see their output decrease during the adjustment, as their output changes from \(q_{ref}\) to \(q^{\prime }_{ref}\). Their cost-elasticity of output is null in the short-run but not in the long-run.

-

(iv)

Managers with (\(\delta _1 \le \delta \le \delta ^{\prime }_1\)) will experience a decrease of their output during the adjustment, from the initial reference output to a value between that and the new reference output. Their cost-elasticity of output is higher (more negative) in the long-run than in the short-run.

-

(v)

Managers with \(\delta \ge \delta ^{\prime }_1\) will not be affected by the adjustment of the reference output. See expression (22a). Their cost-elasticity of output is the same in the short and in the long-run.

Rights and permissions

About this article

Cite this article

Borges, A.P., Correia-da-Silva, J. & Laussel, D. Regulating a manager whose empire-building preferences are private information. J Econ 111, 105–130 (2014). https://doi.org/10.1007/s00712-012-0325-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00712-012-0325-1