Abstract

We derive approximating formulas for the mean and the variance of an autocorrelation estimator which are of practical use over the entire range of the autocorrelation coefficient ρ. The least-squares estimator

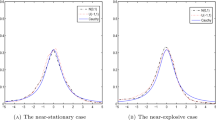

is studied for a stationary AR(1) process with known mean. We use the second order Taylor expansion of a ratio, and employ the arithmetic—geometric series instead of replacing partial Cesaro sums. In case of the mean we derive Marriott and Pope’s (1954) formula, with (n - 1)-1 instead of (n)-1, and an additional term ∝ (n - 1)-2. This new formula produces the expected decline to zero negative bias as ρ approaches unity. In case of the variance Bartlett’s (1946) formula results, with (n — 1)-1 instead of (n)-1. The theoretical expressions are corroborated with a simulation experiment. A comparison shows that our formula for the mean is more accurate than the higher-order approximation of White (1961), for ¦ρ¦> 0.88 and n ≥ 20. In principal, the presented method can be used to derive approximating formulas for other estimators and processes.

Similar content being viewed by others

References

Anderson, O.D. (1995). The precision of approximations to moments of sample moments. J. Statist. Comput. Simul. 52, 163–165.

Bartlett, M.S. (1946). On the theoretical specification and sampling properties of autocorrelated time-series. J. Roy. Statist. Soc. Supplement 8, 27–41 (Corrigenda: (1948) J. Roy. Statist. Soc. Ser. B 10, No. 1).

Box, G.E.R, Jenkins, G.M., Reinsel, G.C. (1994). Time series analysis: forecasting and control, 3rd edn. Prentice-Hall, Englewood Cliffs, NJ, 598 pp.

Kendall, M.G. (1954). Note on bias in the estimation of autocorrelation. Biometrika 41, 403–404.

Marriott, F.H.C., Pope, J.A. (1954). Bias in the estimation of autocorrelations. Biometrika 41, 390–402.

Priestley, M.B. (1981). Spectral Analysis and Time Series, Academic Press, London.

White, J.S. (1961). Asymptotic expansions for the mean and variance of the serial correlation coefficient. Biometrika 48, 85–94.

Author information

Authors and Affiliations

Rights and permissions

About this article

Cite this article

Mudelsee, M. Note on the bias in the estimation of the serial correlation coefficient of AR(1) processes. Statistical Papers 42, 517–527 (2001). https://doi.org/10.1007/s003620100077

Received:

Revised:

Issue Date:

DOI: https://doi.org/10.1007/s003620100077