Abstract

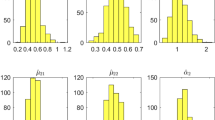

A CUSUM estimator is proposed for the change point in stochastic trend with heavy-tailed innovations. In order to avoid the outliers caused by heavy-tailed innovations, we also construct a truncating CUSUM estimator. Results in this paper show that the CUSUM estimators are consistent. Simulations demonstrate that the truncating estimator behaves better for the heavy-tailed innovations.

Similar content being viewed by others

References

Aue A, Horváth L, Hušková M, Kokoszka P (2008) Testing for changes in polynomial regression. Bernoulli 14: 637–660

Bai J (1994) Least squares estimation of a shift in linear processes. J Time Ser Anal 15: 453–472

Bai J (1995) Least absolute deviation estimation of a shift. Econom Theory 11: 403–436

Guillaume DM et al (1997) From the birds eye to the microscope: a survey of new stylized facts of the intra-daily foreign exchange markets. Finance Stoch 1: 95–129

Han S, Tian Z (2006) Truncating estimator for the mean change-point in heavy-tailed dependent observations. Comm Stat Theory Methods 35: 43–52

Horváth L, Koskoszka P (2003) A bootstrap approximation to a unit root test statistics for heavy-tailed observations. Statist Probab Lett 62: 163–173

Mittnik S, Rachev S (2000) Stable Paretian models in finance. Wiley, New York

Perron P, Zhu X (2005) Structural breaks with deterministic and stochastic trends. J Econom 129: 65–119

Phillips PCB (1990) Time series regression with a unit root and infinite-variance errors. Econom Theory 6: 44–62

Yao Y (1987) Approximating the distribution of the ML estimate of the change point in a sequence in independent random variables. Ann Statist 15: 1321–1328

Zivot E, Phillips PCB (1994) A Bayesian analysis of trend determination in economics time series. Econom Rev 13: 291–336

Author information

Authors and Affiliations

Corresponding authors

Rights and permissions

About this article

Cite this article

Qin, R., Tian, Z. & Jin, H. Truncating estimation for the change in stochastic trend with heavy-tailed innovations. Stat Papers 52, 203–217 (2011). https://doi.org/10.1007/s00362-009-0223-y

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00362-009-0223-y