Abstract

The problem of simultaneous estimation of eigenvalues of covariance matrix is considered for one and two sample problems under a sum of squared error loss. New classes of estimators are obtained which dominate the best multiple of the sample eigenvalues in terms of risk. These estimators shrink or expand the sample eigenvalues towards their geometric mean. Similar results are obtained for the estimation of eigenvalues of the precision matrix and the residual matrix when the original covariance matrix is partitioned into two groups. As a consequence, a new estimator of trace of the covariance matrix is obtained.

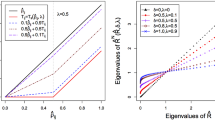

The results are extended to two sample problem where two Wishart distributions are independently observed, say, S i ∼W p (Σ i , k i ), i=1, 2, and eigenvalues of Σ1Σ2-1 are estimated simultaneously. Finally, some numerical calculations are done to obtain the amount of risk improvement.

Similar content being viewed by others

References

Dey, D. K. and Gelfand, A. E. (1986). Improved estimators in simultaneous estimation of scale parameters (unpublished manuscript).

Dey, D. K. and Srinivasan, C. (1985). Estimation of covariance matrix under Stein's loss, Ann. Statist., 13, 1581–1591.

Dey, D. K. and Srinivasan, C. (1986). Trimmed minimax estimator of a covariance matrix, Ann. Inst. Statist. Math., 38, 47–54.

Dey, D. K., Ghosh, M. and Srinivasan, C. (1986). Estimation of matrix means and the precision matrix: A unified approach (unpublished manuscript).

Haff, L. R. (1980). Empirical Bayes estimation of the multivariate normal covariance matrix, Ann. Statist., 8, 586–597.

Haff, L. R. (1983). Solutions of the Euler-Lagrange equations for certain multivariate normal estimation problems (unpublished manuscript).

James, W. and Stein, C. (1961). Estimation with quadratic loss, Proc. Fourth Berkeley Symp. Math. Statist. Prob., Vol. 1, 361–379, University of California Press, Berkeley.

Muirhead, R. J. (1982). Aspects of Multivariate Statistical Theory, Wiley, New York.

Muirhead, R. J. and Verathaworn, T. (1985). On estimating the latent roots of 147–1, (ed. P. R. Krishnaiah), Mult. Anal., VI, 431–447.

Olkin, I. and Selliah, J. B. (1977). Estimating covariance in a multivariate normal distribution, Statistical Decision Theory and Related Topics II, (eds. S. S. Gupta and D. Moore), 313–326, Academic Press, New York.

Author information

Authors and Affiliations

About this article

Cite this article

Dey, D.K. Simultaneous estimation of eigenvalues. Ann Inst Stat Math 40, 137–147 (1988). https://doi.org/10.1007/BF00053961

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1007/BF00053961