Abstract

This paper studies the impact of jumps on volatility estimation and inference based on various realised variation measures such as realised variance, realised multipower variation and truncated realised multipower variation. We review the asymptotic theory of those realised variation measures and present a new estimator for the asymptotic ‘variance’ of the centered realised variance in the presence of jumps. Next, we compare the finite sample performance of the various estimators by means of detailed Monte Carlo studies. Here we study the impact of the jump activity, of the jump size of the jumps in the price and of the presence of additional independent or dependent jumps in the volatility. We find that the finite sample performance of realised variance and, in particular, of log-transformed realised variance is generally good, whereas the jump-robust statistics tend to struggle in the presence of a highly active jump process.

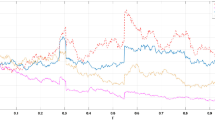

Finally, we investigate the impact of jumps on inference on volatility empirically, where we study high frequency data from the Standard & Poor’s Depository Receipt (SPY).

Similar content being viewed by others

References

Aït-Sahalia, Y., Jacod, J.: Testing for jumps in a discretely observed process. Ann. Stat. 37(1), 184–222 (2009)

Aït-Sahalia, Y., Jacod, J.: Is Brownian motion necessary to model high frequency data? Ann. Stat. 38(5), 3093–3128 (2010)

Aït-Sahalia, Y., Kimmel, R.: Maximum likelihood estimation of stochastic volatility models. J. Financ. Econ. 83(2), 413–452 (2007)

Andersen, T.G., Bollerslev, T., Diebold, F.X., Labys, P.: Great realizations. Risk 13, 105–108 (2000)

Andersen, T.G., Bollerslev, T., Diebold, F.X., Ebens, H.: The distribution of realized stock return volatility. J. Financ. Econ. 61, 43–76 (2001a)

Andersen, T.G., Bollerslev, T., Diebold, F.X., Labys, P.: The distribution of exchange rate volatility. J. Am. Stat. Assoc. 96, 42–55 (2001b). Correction published in 2003, 98, 501

Andersen, T.G., Bollerslev, T., Diebold, F.X.: Parametric and nonparametric measurement of volatility. In: Aït-Sahalia, Y., Hansen, L.P. (eds.) Handbook of Financial Econometrics, vol. 1, pp. 67–137. Elsevier, Amsterdam (2010). Chap. 2

Bandi, F.M., Renò, R.: Nonparametric stochastic volatility (2010). Available at SSRN: http://ssrn.com/abstract=1158438

Barndorff-Nielsen, O.E., Shephard, N.: Non-Gaussian Ornstein–Uhlenbeck-based models and some of their uses in financial economics (with discussion). J. R. Stat. Soc. B 63, 167–241 (2001)

Barndorff-Nielsen, O.E., Shephard, N.: Econometric analysis of realised volatility and its use in estimating stochastic volatility models. J. R. Stat. Soc. B 64, 253–280 (2002)

Barndorff-Nielsen, O.E., Shephard, N.: Econometric analysis of realised covariation: high frequency covariance, regression and correlation in financial economics. Econometrica 72, 885–925 (2004a)

Barndorff-Nielsen, O.E., Shephard, N.: Power and bipower variation with stochastic volatility and jumps (with discussion). J. Financ. Econom. 2, 1–48 (2004b)

Barndorff-Nielsen, O.E., Shephard, N.: Econometrics of testing for jumps in financial economics using bipower variation. J. Financ. Econom. 4, 1–30 (2006)

Barndorff-Nielsen, O.E., Shephard, N.: Variation, jumps, market frictions and high frequency data in financial econometrics. In: Blundell, R., Torsten, P., Newey, W.K. (eds.) Advances in Economics and Econometrics. Theory and Applications. Ninth World Congress, Econometric Society Monographs, vol. III. Cambridge University Press, Cambridge (2007)

Barndorff-Nielsen, O.E., Shephard, N., Winkel, M.: Limit theorems for multipower variation in the presence of jumps. Economics Papers 2005-W07, Economics Group, Nuffield College, University of Oxford (2005)

Barndorff-Nielsen, O.E., Hansen, P.R., Lunde, A., Shephard, N.: Designing realized kernels to measure the ex post variation of equity prices in the presence of noise. Econometrica 76(6), 1481–1536 (2008)

Barndorff-Nielsen, O.E., Hansen, P.R., Lunde, A., Shephard, N.: Multivariate realised kernels: consistent positive semidefinite estimators of the covariation of equity prices with noise and non-synchronous trading. J. Econom. 162(2), 149–169 (2011)

Black, F.: Studies of stock market volatility changes. In: Proceedings of the Business and Economic Statistics Section, pp. 177–181. American Statistical Association, Alexandria (1976)

Blumenthal, R., Getoor, R.: Sample functions of stochastic processes with independent increments. J. Math. Mech. 10, 493–516 (1961)

Christensen, K., Oomen, R., Podolskij, M.: Fact or friction: Jumps at ultra high frequency. Preprint (2011)

Cont, R., Mancini, C.: Nonparametric tests for pathwise properties of semimartingales. Bernoulli 17(2), 781–813 (2011)

Corsi, F., Pirino, D., Renò, R.: Threshold bipower variation and the impact of jumps on volatility forecasting. J. Econom. 159, 276–288 (2010)

Dette, H., Podolskij, M., Vetter, M.: Estimation of integrated volatility in continuous time financial models with applications to goodness-of-fit testing. Scand. J. Stat. 33, 259–278 (2006)

Foster, D.P., Nelson, D.B.: Continuous record asymptotics for rolling sample variance estimators. Econometrica 64(1), 139–174 (1996)

Hansen, P.R., Lunde, A.: Realized variance and market microstructure noise. J. Bus. Econ. Stat. 24, 127–218 (2006)

Huang, X., Tauchen, G.: The relative contribution of jumps to total price variance. J. Financ. Econom. 3(4), 456–499 (2005)

Jacod, J.: Limit of random measures associated with the increments of a Brownian semimartingale. Preprint number 120, Laboratoire de Probabilitiés, Université Pierre et Marie Curie, Paris (1994)

Jacod, J.: The Euler scheme for Lévy driven stochastic differential equations: Limit theorems. Ann. Probab. 32(3A), 1830–1872 (2004)

Jacod, J.: Asymptotic properties of realized power variations and related functionals of semimartingales: Multipower variation. Université P. et M. Curie (Paris 6), Unpublished paper (2006)

Jacod, J.: Asymptotic properties of realized power variations and related functionals of semimartingales. Stoch. Process. Appl. 118, 517–559 (2008)

Jacod, J., Protter, P.: Asymptotic error distribution for the Euler method for stochastic differential equations. Ann. Probab. 26(1), 267–307 (1998)

Jacod, J., Todorov, V.: Do price and volatility jump together? Ann. Appl. Probab. 20(4), 1425–1469 (2010)

Kristensen, D.: Nonparametric filtering of the realised spot volatility: A kernel-based approach. Econom. Theory 26, 60–93 (2010)

Lee, S.S., Mykland, P.A.: Jumps in financial markets: A new nonparametric test and jump dynamics. Rev. Financ. Stud. 21, 2535–2563 (2008)

Mancini, C.: Disentangling the jumps of the diffusion in a geometric jumping Brownian motion. G. Ist. Ital. Attuari LXIV, 19–47 (2001)

Mancini, C.: Non-parametric threshold estimation for models with stochastic diffusion coefficient and jumps. Scand. J. Stat. 36, 270–296 (2009)

Mancini, C., Gobbi, F.: Identifying the Brownian covariation from the co-jumps given discrete observations. Econom. Theory (2011, in press)

Nelson, D.B.: Conditional heteroscedasticity in asset returns: a new approach. Econometrica 59(2), 347–370 (1991)

Podolskij, M., Vetter, M.: Estimation of volatility functionals in the simultaneous presence of microstructure noise and jumps. Bernoulli 15(3), 634–658 (2009)

Protter, P.E.: Stochastic Integration and Differential Equations, 2nd edn. Springer, London (2004)

Rényi, A.: On stable sequences of events. Sankhya, Ser. A 25(3), 293–302 (1963)

Rosinski, J.: Series representations of Lévy processes from the perspective of point processes. In: Barndorff-Nielsen, O., Mikosch, T., Resnick, S. (eds.) Lévy Processes: Theory and Applications. Birkhäuser, Boston (2001)

Todorov, V., Tauchen, G.: Limit theorems for power variations of pure-jump processes with application to activity estimation. Ann. Appl. Probab. 21(2), 546–588 (2011)

Veraart, A.E.D.: Inference for the jump part of quadratic variation of Itô semimartingales. Econom. Theory 26(2), 331–368 (2010)

Veraart, A.E.D.: Web appendix: How precise is the finite sample approximation of the asymptotic distribution of realised variation measures in the presence of jumps? Available at SSRN: http://ssrn.com/abstract=1814125 (2011)

Veraart, A.E.D., Veraart, L.A.M.: Stochastic volatility and stochastic leverage. Ann. Finance (2010). doi:10.1007/s10436-010-0157-3

Vetter, M.: Limit theorems for bipower variation of semimartingales. Stoch. Process. Appl. 120, 22–38 (2010)

Woerner, J.H.C.: Power and multipower variation: inference for high frequency data. In: Shiryaev, A.N., Grossinho, M.R., Oliveira, P.E., Esquível, M.L. (eds.) Stochastic Finance, pp. 343–364. Springer, Berlin (2006)

Zhang, L.: Efficient estimation of stochastic volatility using noisy observations: A multi-scale approach. Bernoulli 12(6), 1019–1043 (2006)

Zhang, L., Mykland, P.A., Aït-Sahalia, Y.: A tale of two time scales: determining integrated volatility with noisy high-frequency data. J. Am. Stat. Assoc. 100, 1394–1411 (2005)

Zhou, H.: Itô conditional moment generator and the estimation of short-rate processes. J. Financ. Econom. 1(2), 250–271 (2003)

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Veraart, A.E.D. How precise is the finite sample approximation of the asymptotic distribution of realised variation measures in the presence of jumps?. AStA Adv Stat Anal 95, 253–291 (2011). https://doi.org/10.1007/s10182-011-0158-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10182-011-0158-1