Abstract

The main purpose of the study is to explore the dynamic relationship among the TAIEX spot, futures, and options markets by proposing an innovative multivariable GARCH-M MSKST (Multivariate Skewed-Student distribution) model. In addition to the considerable feedback effects of these three markets in terms of return transmissions, a significant bidirectional relationship is also found in volatility transmissions between futures and spot markets, and unidirectional spillover occurs from futures to options markets. Specifically, futures are found to exert the most influence on spot and options, and play an important role in disclosing information and pricing discovery to the other two markets. Comparing the magnitude of the effect the positive and negative basis has on spot prices, it is evident that positive basis has a greater impact on the spot market than negative basis does. Of interest, our study shows that positive basis has even more effect than negative basis does on the conditional variance of return on spot and futures.

Similar content being viewed by others

Notes

The underlying asset is the Taiwan Stock Exchange Capitalization Weighted Stock Index (TAIEX).

In each interval, the last transaction price is identified.

The sequence derived from the overnight return tends to induce a severe heterscedasticity problem. The deletion of overnight returns ensures synchronous prices and reduce the effects of stale prices in the index. It also removes any adjustment when switching to the next contract occurs at the expiry date.

We use the tri-variate GARACH model for our research, thus the setting k = 3.

References

Abhyankar AH (1995) Return and volatility dynamics in the FTSE100 stock index and stock index futures markets. J Futures Mark 15(4):457–488

Anthony JH (1988) The interrelation of stock and options market trading-volume data. J Finance 43:949–964

Bae K, Karolyi GA (1994) Good news, bad news and international spillovers of stock return volatility between Japan and US. Pacific-Basin Finance J 2(4):405–438

Bae SC, Kwon TH, Park JW (2004) Futures trading, spot market volatility, and market efficiency: the case of the Korean index futures markets. J Futures Mark 24(12):1195–1228

Baillie RT, Bollerslev T (1990) A multivariate generalized ARCH approach to modeling risk premia in foreign exchange market. J Int Money Finance 9:309–324

Bakshi G, Cao C, Chen Z (1997) Empirical performance of alternative option pricing models. J Finance 52:2003–2049

Bauwens L, Laurent S (2005) A new class of multivariate skew densities, with application to GARCH models. J Bus Econ Stat 23(3):346–354

Beaulieu MC (1998) Time to maturity in the basis of stock market indices: evidence from the S&P 500 and the MMI. J Empir Finance 5:177–195

Beckers S (1981) Standard Deviations Implied in Options Prices. J Bank Finance 5:363–81

Berndt EK, Hall BH, Hall RE, Hausman JA (1974) Estimation inference in nonlinear structural models. Annu Econ Soc Meas 4:653–665

Black F (1976) Studies of stock price volatility changes. Proceedings of the 1976 meetings of the American statistical association, business and economics statistics section, American Statistical Association, pp 177–181

Bollerslev T (1990) Modelling the coherence in short-run nominal exchange rates: a multivariate generalized ARCH model. Rev Econ Stat 72:498–505

Bollerslev T, Chou RY, Kroner KF (1992) ARCH modeling in finance: a review of the theory and empirical evidence. J Econom 52:5–59

Booth GG, Martikainen T, Tse Y (1997) Price and volatilities spillovers in Scandinavian stock markets. J Int Money Finance 21:811–823

Booth GG, So RW, Tse Y (1999) Price discovery in the German equity index derivatives markets. J Futures Mark 19(6):619–643

Brennan MJ, Schwartz ES (1990) Arbitrage in stock index futures. J Bus 63:7–31

Chakravarty S, Gulen H, Mayhew S (2004) Informed trading in stock and option markets. J Finance 59:1235–1257

Chan KS (1992) A further analysis of the lead-lag relationship between the cash market and stock index futures market. Rev Financ Stud 5(1):123–152

Chan K, Chung YP, Fong WM (2002) The informational role of stock and option volume. Rev Finan Stud 15(4):1049–1075

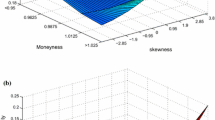

Cheng L, Chan KC, Lung PP (2003) Moneyness and the response of the implied volatilities to price changes: the empirical evidence from HIS options. Pac Basin Finance J 11:527–553

Cherian JA, Weng WY (1999) An empirical analysis of directional and volatility trading in options markets. J Derivat 7:53–65

Chiang R, Fong WM (2001) Relative informational efficiency of cash, futures, and options markets: the case of an emerging market. J Bank Finance 25(2):355–375

Chris B, Alistar GW, Stuart T (2001) A trading strategy based on the lead-lag relationship between the spot index and futures contract for the FTSE 100. Int J Forecast 17:31–44

Chou RY (1988) Volatility persistence and stock valuation: some empirical evidence using GARCH. J Appl Econom 3:279–194

Darbar SM, Deb P (1997) Co-movements in international equity markets. J Financ Res 22(3):305–322

Deb P (1996) Finite sample properties of maximum likelihood and quasi-maximum likelihood estimators of EGARCH models. Econom Rev 15:51–68

Demus B, Fleming J, Whaley RE (1998) Implied volatility functions: empirical test. J Finance 53:2059–2106

Dickey DA, Fuller WA (1979) Distribution of the estimator for autoregressive time series with a unit root. J Am Stat Assoc 74:427–431

Diltz JD, Kim S (1996) The relationship between stock and options price changes. Financial Rev 31:499–519

Easley D, O’Hara M, Srinivas PS (1998) Option volume and stock prices: evidence on where informed traders trade. J Finance 53:431–465

Ehrmann M, Fratzscher M, Rigobon R (2005) Stocks, bonds, money markets and exchange rates: measuring international financial transmission. NBER Working Paper No 11166

Engle RF, Ng VK (1993) Measuring and testing the impact of news on volatility. J Finance 48:1749–1778

Engle R, González-Rivera G (1991) Semi-parametric ARCH models. J Bus Econ Stat 9:345–359

Ferreira MA, Lopez JA (2005) Evaluating interest rate covariance models within a value-at-risk framework. J Financ Econom 3(1):126–168

Finucane TJ (1991) Put call parity and expected returns. J Financ Quant Anal 26(4):445–457

Fleming J, Ostdiek B, Whaley RE (1996) Trading costs and the relative rate if price discovery in stock index futures markets. J Futures Mark 16:353–387

Garbade KD, Silber WL (1979) Dominant and satellite markets: a study of dually-traded securities. Rev Econ Stat 61(2):455–460

Gemmill G (1986) The forecasting performance of the London traded options market. J Bus Finance Account 13:535–546

Glosten LR, Jagannathan R, Runkle D (1993) On the relation between the expected value and the volatility of the nominal excess return on stocks. J Finance 48:1779–1801

Grunbichler A, Longstaff F, Schwartz E (1994) Electronic screen trading and the transmission of information. J Financ Intermed 3:166–187

Gwilym OA, Buckle M (2001) The lead-lag relationship between the FTSE100 stock index and its derivative contracts. Appl Financ Econ 11:385–393

Han LM, Misra L (1994) The impact of trading restrictions on the informational relationships between cash, futures, and options markets. Int Rev Econ Finance 3:429–442

Hatch BC (2003) The intraday relation between NYSE and CBOE prices. J Financ Res 26:97–113

Huang VS, Goo YJ, Tsai CC (2001) Long Memory Models Applied on the Lead-Lag Relationship between Futures and Spots: The Examples of TAIFEX and SGX-DT MSCI Taiwan Stock Index Futures. Fu-Jen Management Review 8(2):73–116

Huang YC, Shyu D (1997) An evaluation of the dynamic interaction between spot and futures markets for Taiwan stock index. Rev Secur Futures Mark 9(3):1–28

Huisman R, Koedijk K, Kool C, Palm F (1998) The fat-tailedness of FX returns. working paper, Limburg Institute of Financial Economics, Maastricht University, The Netherlands

Hsieh DA (1989) Modeling heteroskedasticity in daily foreign-exchange rates. J Bus Econ Stat 7:307–317

Kanas A (1998) Volatility spillovers across equity markets: European evidence. Appl Financ Econ 8:245–56

Karolyi GA, Stulz RM (1996) Why do markets move together? An investigation of US-Japan stock return comovements. J Finance 51(3):951–986

Koutmos G, Knif J (2002) Estimating systematic risk using time varying distributions. Eur Financ Manage 8(1):59–73

Lee TH (1994) Spread and volatility in spot and forward exchange rates. J Int Money Finance 13:375–383

Lee S, Hansen BE (1994) Asymptotic theory for the GARCH (1,1) quasi-maximum likelihood estimator. Econ Theory 10:29–52

Lien D, Tse YK (1998) Hedging time-varying downside risk. J Futures Mark 18:705–722

Lien D, Tse YK (2000) Hedging downside risk with futures contracts. Appl Financ Econ 10:163–170

Longin F, Solnik B (1995) Is the correlation in international equity returns constant: 1960–1990? J Int Money Finance 14(1):3–26

MacBeth JD, Merville LJ (1979) An empirical examination of the Black-Scholes call option pricing model. J Finance 34:1173–1186

Miller MH (1990) International competitiveness of U. S. futures markets. J Financ Serv Res 4:387–408

Murphy KM, Topel RH (1985) Estimation and inference in two-step econometric models. J Bus Econ Stat 3(4):370–379

O’Connor ML (1999) The cross-sectional relationship between trading cost and lead/lag effects in stock and option markets. Financ Rev 34:95–117

O’Hara M (1995) Market microstructure theory. Blackwell Publishers Inc., Cambridge

Pagan AR (1984) Econometric issues in the analysis of regressions with generalized regressors. Int Econ Rev 25:221–247

Pagan AR, Sabau H (1987) On the inconsistence of the MLE in certain heteroskedasticity regression model. University of Rochester, Mimeo

Pagan A, Ullah A (1988) The economics analysis of models with risk terms. J Appl Econ 3:87–105

Park TH, Switzer LN (1995) Time-varying distributions and the optimal hedge ratios for stock index futures. Appl Financ Econ 5:131–137

Phillips PCB, Perron P (1988) Testing for a unit root in time series regression. Biometrica 75:335–346

Ross S (1989) Information and volatility: the non-arbitrage martingale approach to timing and resolution irrelevancy. J Finance 44:11–17

Shyy G, Vijayraghavan V, Scott-Quinn B (1996) A further investigation of the lead-lag relationship between the cash market and stock index futures market with the use of bid/ask quotes: the case of France. J Futures Mark 16(4):405–420

Stephan JA, Whaley RE (1990) Intraday price change and trading volume relations in the stock and stock option markets. J Finance 45(1):191–220

Stoll HR, Whaley RE (1990) The dynamics of stock index and stock index futures returns. J Financ Quant Anal 25(4):441–468

Theodossiou P, Lee U (1993) Mean and volatility spillovers across major national stock markets: further empirical evidence. J Financ Res 16(4):337–350

Tse YK (2000) A test for constant correlations in a multivariate GARCH model. J Econom 98:107–127

Tucker AL (1991) Financial futures, options, and swaps. West Publishing Company, Minneapolis

Wahab M, Lashgari M (1993) Price dynamics and error correction in stock index and stock index futures markets: a cointegration approach. J Futures Mark 13(7):711–742

Wang KL, Fawson C, Barrett CB, McDonald J (2001) A flexible parametric GARCH model with an application to exchange rates. J Appl Econom 16(4):521–536

Wang KL, Chen ML (2002) The dynamic linkage among U.S. and Taiwan future and spot markets: a more general multivariate GARCH approach. Acad Econ Papers 30(4):363–407

Wiggins J (1987) Option values under stochastic volatility: theory and empirical estimates. J Financ Econ 19(2):351–372

World Trade Report (2003) http://www.wto.org/english/res_e/booksp_e/ anrep_e/ world_trade_report_2003_e.pdf

World Trade Report (2004) http://www.wto.org/english/res_e/booksp_e/anrep_e/world_trade_report04_e.pdf

Yu SW, Wang YI (1999) Pricing, interaction and hedging performance between Nikkei 225 stock index futures and stock markets. Manage Rev 18(2):1–33

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Rights and permissions

About this article

Cite this article

Wang, KL., Chen, ML. The dynamics in the spot, futures, and call options with basis asymmetries: an intraday analysis in a generalized multivariate GARCH-M MSKST framework. Rev Quant Finan Acc 29, 371–394 (2007). https://doi.org/10.1007/s11156-007-0050-y

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-007-0050-y