Abstract

Switzerland is one of the countries with the highest concentration of bank–customer relationships. The present paper seeks to find out whether this can be explained by the structure of Swiss firms or by the organization of the Swiss banking market. Using survey data from small and medium-sized enterprises in 1996 and 2002, we examine the influence of firm-, loan-, and bank-specific variables on the number of banking relationships. We find that firm and industry structure have the largest explanatory power, while banking market structure and conduct play a minor role. Relationship lending by state-owned cantonal banks and small regional banks tends to enhance the concentration of banking relationships.

Similar content being viewed by others

Notes

For a discussion of different measurements of banking relationships and their use in previous studies see Neuberger et al. (2006). In contrast to the present study, the latter focuses on the changes in lending relationships of Swiss SMEs between 1996 and 2002.

This does not necessarily imply that large banks are disadvantaged in providing credit to opaque SMEs since they may use transaction lending technologies well-suited to these enterprises, such as small business credit scoring, asset-based lending, factoring, fixed-asset lending, and leasing (Berger and Udell 2006).

Since technological change has eased the ability to lend to small firms at a distance (Petersen and Rajan 2002), out-of-market lending to small firms in local markets increased substantially in recent years (Hannan 2003).

Among others, the USA (Petersen and Rajan 1994; Berger and Udell 1995), Germany (Harhoff and Körting 1998a, b; Elsas and Krahnen 1998; Neuberger and Räthke 2008), Norway (Ongena and Smith 2001), Sweden (Berglöf and Sjögren 1998), and France (Ziane 2003); an exception is Italy (Detragiache et al. 2000; Guiso 2003; Cosci and Meliciani 2002). For overviews see Ongena and Smith (2000a, pp.243) and Neuberger and Räthke (2008).

In 1995, the ratio of outstanding credits to outstanding bonds was above 140% in Switzerland, compared to 94% in Germany, 83% in the USA, and 75% in the UK (Schmid and Varnholt 1997, p. 310; see Hertig 1998, p. 812). The volume of leasing and factoring is low in Switzerland (Pedergnana et al. 2004, p. 23). In 2002, the ratio of the volume of factoring to GDP was 0.9% compared to 11.9% in Italy (Berger and Udell 2006, p. 6).

In 1997, the big banks and cantonal banks had a combined market share of the credit volume above 80% (Schacht 2005, p. 53), with the big banks providing most of the international banking services. In 2002, 16% of the SMEs used international bank services, 70% of which were provided by the big banks (Source: own calculations with the data described below).

The cantonal banks introduced risk-adjusted pricing to a lesser extent. From 1997 to 1998, the average interest rate on SME loans was raised by 3% at the big banks, but by only 1.2% at the cantonal banks (Task Force KMU 1999, p. 7; Pedergnana et al. 2004, p.102). With the introduction of risk-adjusted pricing by the big banks in 1997, the Basel II capital adequacy rules have been largely anticipated in Switzerland (Credit Suisse 2004).

Excluding the two city cantons of Basle City and Geneva, the correlation coefficient between population density and branch density was −0.53 in 2002.

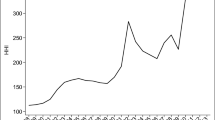

The HHI is calculated by summing the squared market shares of all banks competing in the market. We are grateful to Daniel Piazza for providing us with this data.

According to the US Merger Guidelines, markets in which the HHI exceeds 1,800 points are considered to be concentrated.

Since our dependent variable takes integer values, the Poisson model may be more suitable than OLS. The negative binomial model is a generalization of the Poisson model, which is appropriate in the case of over/underdispersion in the latter (Cameron and Trivedi 1990). Using a regression-based test, we can reject the null hypothesis of no over/underdispersion in the Poisson regression model.

References

Agarwal S, Hauswald R (2006) Distance and information asymmetries in lending decisions. Paper presented at the Conference ‘Financial System Modernisation and Economic Growth in Europe’, Berlin, September

Akhavein J, Goldberg LG, White LJ (2004) Small banks, small business, and relationships: an empirical study of lending to small farms. J Financ Serv Res 26:245–261

Angelini P, Di Salvo R, Ferri G (1998) Availability and cost of credit for small businesses: customer relationships and credit cooperatives. J Bank Financ 22:925–954

Audretsch DB, Elston JA (2002) Does firm size matter? Evidence on the impact of liquidity constraints on firm investment behavior in Germany. International Journal of Industrial Organization 20:1–17

BADAC (2005) T11.11a, Ständige Wohnbevölkerung 1995–2004. 2002 IDHEAP, update 21.11. http://www.badac.ch

Bannier CE (2005) Heterogeneous multiple bank financing, optimal business risk and information disclosure. Working Paper Series Finance and Accounting no. 148, Goethe University Frankfurt, March

Berger AN, Udell GF (1995) Relationship lending and lines of credit in small firm finance. J Bus 68:351–381

Berger AN, Udell GF (2002) Small business credit availability and relationship lending: the importance of bank organisational structure. Econ J 112:F32–F53

Berger AN, Udell GF (2003) The future of relationship lending. In: Berger AN, Udell GF (eds) The Future of Banking. Westport

Berger AN, Udell GF (2006) A more complete conceptual framework for SME finance. J Bank Financ 30:2945–2966, (November)

Berger AN, Klapper LF, Udell GF (2001) The ability of banks to lend to informationally opaque small businesses. Journal of Banking and Finance 25:2127–2167

Berger AN, Klapper LF, Soledad Martinez Peria M, Zaidi R (2005) The effects of bank ownership type on banking relationships and multiple banking in developing economies detailed evidence from India. Board of Governors of the Federal Reserve System, Washington, DC

Berglöf E, Sjögren H (1998) Combining arm’s length and control oriented finance—evidence from main bank relationships in sweden. In: Hopt KJ, Kanda H, Roe MJ (eds) Comparative corporate governance: the state of the art and emerging research. Clarendon, Oxford, pp 787–808

Bichsel R (2006) State-owned banks as competition enhancers, or the grand illusion. J Financ Serv Res 30:117–150

Bolton P, Scharfstein DS (1996) Optimal debt structure and the number of creditors. J Polit Econ 104:1–25

Bonaccorsi Di Patti E, Dell’Ariccia G (2004) Bank competition and firm creation. J Money Credit Bank 36:225–251

Boot AWA (2000) Relationship banking: what do we know? J Financ Intermed 9:7–25

Boot AWA, Thakor AV (1994) Moral hazard und secured lending in an infinitely repeated credit market game. Int Econ Rev 35:899–920

Boot AWA, Thakor AV (2000) Can relationship banking survive competition? J Finance 55:679–713

Cameron A, Trivedi P (1990) Regression based tests for overdispersion in the Poisson model. J Econ 31:255–274

Carletti E (2004) The structure of bank relationships, endogenous monitoring, and loan rates. J Financ Intermed 13:58–86

Carletti E, Cerasi V, Daltung S (2007) Multiple-bank lending: diversification and free-riding in monitoring. J Financ Intermed 16:425–451

Carter DA, McNulty JE, Verbrugge JA (2004) Do small banks have an advantage in lending? An examination of risk-adjusted yields on business loans at large and small banks. J Financ Serv Res 25:233–252

Cole RA (1998) The importance of relationships to the availability of credit. J Bank Financ 22:959–977

Cosci S, Meliciani V (2002) Multiple banking relationships: evidence from the Italian experience. Manchester School Supplement 37–54

Credit Suisse (2003) Filialabbau: Raiffeisenbanken im Sog der Marktkräfte Spotlight, Economic and Policy Consulting, Credit Suisse, October 15

Credit Suisse (2004) Basel II—Meilenstein der Bankenregulierung. Economic Briefing (36), Zurich

D’Auria C, Foglia A, Reetz PM (1999) Bank interest rates and credit relationships in Italy. J Bank Financ 23:1067–1093

Degryse H, Ongena S (2001) Bank relationships and firm performance. Financ Manage 30:9–34

Degryse H, Ongena S (2007) The impact of competition on bank orientation. J Financ Intermed 399–424

Detragiache E, Garella P, Guiso L (2000) Multiple versus single banking relationships: theory and evidence. J Financ 55:1133–1161

Dewatripont M, Maskin E (1995) Credit and efficiency in centralized and decentralized economics. Rev Econ Stud 62:541–555

Diamond D (1984) Financial intermediation and delegated monitoring. Rev Econ Stud 51:393–414

Elsas R (2005) Empirical determinants of relationship lending. J Financ Intermed 14:32–57

Elsas R, Krahnen JP (1998) Is relationship lending special? Evidence from credit-file data in Germany. J Bank Financ 22:1283–1316

Elsas R, Krahnen JP (2000) Collateral, default risk, and relationship lending: an empirical study on financial contracting. CFS Working Paper no. 1999/13, Center for Financial Studies, University of Frankfurt, revised version, November 25

Elyasiani E, Goldberg LG (2004) Relationship lending: a survey of the literature. J Econ Bus 56:315–330

Elsas R, Heinemann F, Tyrell M (2004) Multiple but asymmetric bank financing: the case of relationship lending.” CESifo working paper no. 1251, 2004.

Ferri G, Kang TS, Kim IJ (2001) The value of relationship banking during financial crises. Evidence from the Republic of Korea. Policy Research Working Paper 2553, The World Bank, 2001

Fok RCW, Chang YC, Lee WT (2004) Bank relationships and their effects on firm performance around the Asian financial crisis: evidence from Taiwan. Financ Manage 33:89–112

Guiso L (2003) Small business finance in Italy. European Investment Bank Papers 8:121–149

Guiso L, Minetti R (2004) Multiple creditors and information rights: theory and evidence from US Firms. CEPR Discussion Paper no. 4278

Hannan TH (2003) Changes in non-local lending to small business. J Financ Serv Res 24:31–46

Harhoff D, Körting T (1998a) Lending relationships in Germany: empirical evidence from survey data. J Bank Financ 22:1317–1353

Harhoff D, Körting T (1998b) How many creditors does it take to tango? Discussion Paper, Wissenschaftszentrum Berlin and Zentrum für Europäische Wirtschaftsforschung, Mannheim

Hauswald R, Marquez R (2006) Competition and strategic information acquisition in credit markets. Rev Financ Stud 19:967–1000

Hellwig M (1991) Banking, financial intermediation and corporate finance. In: Giovannini A, Mayer C (ed) European financial integration. Cambridge University Press, 35–63, Cambridge

Hertig G (1998) Lenders as a force in corporate governance criteria and practical examples for Switzerland. In: Hopt KJ, Kanda H, Roe MJ, Wymeresch E, Prigge S (eds) Comparative corporate governance. Clarendon, Oxford, pp 809–835

IMF (2007) Switzerland: financial sector assessment program—technical note—the Swiss banking system: structure, performance, and medium-term challenges, IMF Country Report no. 07/199. International Monetary Fund, Washington, DC

Jean-Baptiste EL (2005) Information monopoly and commitment in intermediary-firm relationships. J Financ Serv Res 27:5–26

Koziol C (2005) When does single-source versus multiple-source lending matter? Working paper, University of Mannheim, Germany

La Porta R, Lopez-de-Silanes F, Shleifer A, Vishny RW (1997) Legal determinants of external finance. J Financ 52:1131–1150

La Porta R, Lopez-de-Silanes F, Shleifer A, Vishny RW (1998) Law and finance. J Polit Econ 106:1113–1155

Lehmann E, Neuberger D (2001) Do lending relationships matter? Evidence from bank survey data in Germany. J Econ Behav Organ 45:339–359

Lehmann E, Neuberger D, Räthke S (2004) Lending to small and medium-sized firms: is there an east–west gap in Germany? Small Bus Econ 2:3:23–39

Levine R (1999) Law, finance, and economic growth. J Financ Intermed 8:8–35

Machauer A, Weber M (1998) Bank behavior based on internal credit rating of borrowers. J Bank Finance 22:1355–1383

Machauer A, Weber M (2000) Number of bank relationships: an indicator of competition, borrower quality, or just size? CFS Working Paper 2000/2006, Frankfurt/Main, Germany

Mauro P (1995) Corruption and growth. Q J Econ 110:681–712

Menkhoff L, Neuberger D, Suwanaporn C (2006) Collateral-based lending in emerging markets: evidence from Thailand. J Bank Financ 30:1–21

Montoriol Garriga J (2006a) Relationship lending and banking competition: are they compatible? Universitat Pompeu Fabra, Barcelona

Montoriol Garriga J (2006b) The effect of relationship lending on firm performance. Universitat Pompeu Fabra, Barcelona

Neuberger D, Räthke S (2008) Microenterprises and multiple bank relationships: the case of professionals. Small Bus Econ (in press)

Neuberger D, Räthke S, Schacht C (2006) The number of bank relationships of smes: a disaggregated analysis of changes in the Swiss loan market. Econ Notes 35:1–36, (November)

Ogawa K, Sterken E, Tokutsu I (2007) Why do Japanese firms prefer multiple bank relationships? Some Evidence from firm-level data. Econ Syst 31:49–70

Ongena S, Smith DC (2000a) Bank relationships: a review. In: Harker P, Zenios SA (eds) The Performance of Financial Institutions. Cambridge University Press, Cambridge, pp 221–258

Ongena S, Smith DC (2000b) What determines the number of bank relationships? Cross-country evidence. J Financ Intermed 9:26–56

Ongena S, Smith DC (2001) The duration of bank relationships. J Financ Econ 61:449–475

Ongena S, Tümer-Alkan G, von Westernhagen N (2007) Creditor concentration: an empirical investigation. Tilburg University, Tilburg

Pedergnana M, Schacht C, Sax C (2004) Kreditbeziehungen zwischen Banken und KMU.“Luzern: Verlag IFZ–HSW

Petersen MA, Rajan RG (2002) Does distance still matter? The information revolution in small business lending. J Financ 57:2533–2570

Petersen MA, Rajan RG (1994) The benefits of lending relationships: evidence from small business data. J Financ 44:3–37

Petersen MA, Rajan RG (1995) The effect of credit market competition on lending relationships. Q J Econ 110:407–433

Qian J, Strahan PE (2005) How law and institutions shape financial contracts: the case of bank loans. NBER Working Paper 11052

Rajan RG (1992) Insiders and outsiders: the choice between informed and arm’s-length debt. J Financ 47:1367–1400

Schacht C (2005) Angebotsmechanismen und Nachfragestrukturen im Kreditmarkt Schweiz. Hamburg: Dr. Kovac

Schmid A, Varnholt B (1997) Kreditgeschäft im Wandel. In: Schmid C, Varnholt B (eds) Finanzplatz Schweiz. Probleme und Zukunftsperspektiven. Zurich, pp 309–331

Schweizerische Nationalbank (1997) Die Banken in der Schweiz 1996–2005. Zürich, 1997–2006.

Sharpe SA (1990) Asymmetric information, bank lending, and implicit contracts: a stylized model of customer relationships. J Financ 45:1069–1087

Thakor AV (1996) Capital requirements, monetary policy, and aggregate bank lending: theory and empirical evidence. J Financ 51:279–324

von Thadden EL (1992) The commitment of finance, duplicated monitoring and the investment horizon. ESF–CEPR, London

Yu H, Hsieh D (2006) Multiple versus single banking relationships in an emerging market: some Taiwanese evidence. In: Lynde VR (ed) International banking issues. Nova, USA

Ziane Y (2003) Number of banks and credit relationships: empirical results from French small business data. Eur Rev Econ Financ 2:33–60

Author information

Authors and Affiliations

Corresponding author

Additional information

This article is based on the research project no. 6476.1 FHS-ET “Lending Relationships Between Banks and SMEs”, conducted at the IFZ Institute for Financial Services Zug, University of Applied Sciences Central Switzerland. It was supported by the CTI: The Innovation Promotion Agency in Switzerland and the Association of Swiss Cantonal Banks, Bern, Switzerland. We are grateful to Christoph Schacht for valuable research assistance and contributions and to two referees for helpful suggestions. The usual disclaimers apply.

Rights and permissions

About this article

Cite this article

Neuberger, D., Pedergnana, M. & Räthke-Döppner, S. Concentration of Banking Relationships in Switzerland: The Result of Firm Structure or Banking Market Structure?. J Finan Serv Res 33, 101–126 (2008). https://doi.org/10.1007/s10693-008-0026-7

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10693-008-0026-7