Abstract

A large literature establishes the growth-enhancing benefits of foreign direct investment (FDI) flows into emerging market economies in general. Conventional wisdom holds that FDI is a preferable form of external financing compared to other types of capital flows because of its stabilizing properties. While this might hold true largely for FDI flows of the Greenfield variety, in reality, a greater share of FDI to emerging economies in general and Asian economies appears to be in the form of mergers and acquisitions (M&A). Do all types of FDI flows produce similar macroeconomic benefits? This paper empirically explores whether the type of FDI flow, i.e. Greenfield versus M&A, matters in the way it impacts economic growth and domestic investment for a large panel of developing Asian economies over 1990–2013. We find Greenfield FDI contributes positively to economic growth while FDI in the form of M&A appears to have no significant growth influence. We also find that the effects of Greenfield FDI on domestic capital formation are stronger and larger relative to M&A flows.

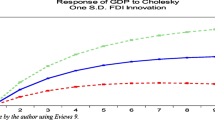

Source: Complied from UNCTAD FDI Statistics

Source: Complied from UNCTAD FDI Statistics

Source: Complied from UNCTAD FDI Statistics

Source: Complied from UNCTAD FDI Statistics

Source: Complied from UNCTAD FDI Statistics

Source: Complied from UNCTAD FDI Statistics

Similar content being viewed by others

Notes

While not explicitly captured by the data, there has been a shift in portfolio flows – from predominantly portfolio equity flows per Asian financial crisis to both portfolio bond and equity flows in the global financial crisis.

While Greenfield and M&A are in the form of new investments, a non-negligible component of FDI is in the form of retained earnings. However, data on this component are not systematically available.

While this ratio dipped a bit after the financial crisis, there appears to have been an uptick again since 2012 onwards.

In view of the complex linkages between the various capital flows, Chuhan et al. (1996) and Claessens et al (1995) argue that it may be misleading to look at capital flows individually, with the latter maintaining that it is only meaningful to examine aggregate financial accounts. Also see Sarno and Taylor (1997).

The discussion follows Gopalan and Rajan (2016).

As UNCTAD (2000) notes, FDI in the form of M&A is inferior to Greenfield FDI when the objective is to promote economic development through enhancing capital-stock.

It is useful to note that the choice governing a multinational enterprise about the form of its entry mode is a significant area of research interest in the field of international business. See Slangen and Hennart (2007) for a review of this related empirical literature.

That being said, both the papers appear to emphasize the importance of a threshold level of human capital for FDI of both types to have an impact of growth.

It is useful to note that while our data includes 42 economies, in the regressions, the final count of countries drops to 24 and those countries are highlighted in Table 3.

We also perform our empirics with two-year averages but do not report the results in the paper. They are available on request from the authors.

UNCTAD Statistics also report the value of Greenfield FDI projects, but it is not available until 2003. Also most of the UNCTAD Greenfield inflow values are much larger than FDI inflows as the reported figures are estimated value of Greenfield investments. Further, a caveat to bear in mind is that while a great deal of focus has tended to be on how to attract new equity investments, not enough attention is being paid to existing investors and how to make sure that they keep investing in the country they are already in. UNCTAD data suggests that about 40 per cent of global FDI is in the form of retained earnings. While important, there is a dearth of data on reinvested earnings, which prevents us from doing further analysis on this component.

The difference-in-Hansen tests cannot reject the null hypothesis, indicating that the instruments are exogenous.

We also tried interactions of commodity exporters with the key FDI variables but the results were insignificant. Results are available on request.

Although, for the developing economies sub-sample, they find that neither Greenfield FDI nor M&A have any significant relationship in increasing TFP.

References

Alfaro, L., Chanda, A., Kalemli-Ozcan, S., & Sayek, S. (2004). FDI and economic growth: The role of financial markets. Journal of International Economics, 64, 89–112.

Andersson, T., & Svensson, R. (1994). Entry modes for direct investment determined by the composition of firm-specific skills. Scandinavian Journal of Economics, 96, 551–560.

Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68, 29–51.

Ashraf, A., Herzer, D., & Nunnenkamp, P. (2016). The effects of Greenfield FDI and cross-border M&As on total factor productivity. World Economy 39(11), 1728–1755.

Azman-Saini, W. N. W., Law, S. H., & Ahmad, A. H. (2010). FDI and economic growth: New evidence on the role of financial markets. Economics Letters, 107, 211–213.

Bank for International Settlements (BIS). (2009) Capital flows and emerging market economies. Committee on Global Financial System Working Papers No. 33.

Barro, R. (1997). Determinants of economic growth: A cross-country empirical study. Cambridge: MIT Press.

Barro, R., & Lee, J. W. (2013). A new data set of educational attainment in the world, 1950–2010. Journal of Development Economics, 104, 184–198.

Bertrand, A. (2004). Mergers and acquisitions (M&As), Greenfield investments and extension of capacity. OECD.

Bird, G., & Rajan, R. S. (2002). Does FDI guarantee the stability of international capital flows? Evidence from Malaysia. Development Policy Review, 20, 191–202.

Blomström, M., Lipsey, R. E., & Zejan, M. (1994). What explains developing country growth? In W. J. Baumol (Ed.), Convergence of productivity: cross-national studies and historical evidence (9th ed.). New York: Oxford University Press.

Blonigen, B. (1997). Firm-specific assets and the link between exchange rates and foreign direct investment. American Economic Review, 87, 447–465.

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87, 115–143.

Borensztein, E. R., de Gregorio, J., & Lee, J. W. (1998). How does foreign direct investment affect economic growth? Journal of International Economics, 45, 115–135.

Bosworth, B., & Collins, S. (1999). Capital flows to developing economies: Implications for saving and investment. Brookings Papers on Economic Activity, 1999(1), 143–180.

Carkovic, M., & Levine, R. (2005). Does foreign direct investment accelerate economic growth? In T. Moran, E. Graham, & M. Blomstrom (Eds.), Does foreign direct investment promote development? (pp. 195–220). Washington DC: Institute for International Economics.

Choe, J. I. (2003). Do foreign direct investment and gross domestic investment promote economic growth? Review of Development Economics, 7, 44–57.

Chuhan, P., Perez-Quiros, G., & Popper, H. (1996). International capital flows: Do short-term investment and direct investment differ? World Bank Policy Research Working Paper No. 1507.

Claessens, S., Dooley, M., & Warner, A. (1995). Portfolio capital flows: Hot or cold? The World Economic Review, 9, 153–174.

Dadush, U., Dasgupta, D., & Ratha, D. (2000). The role of short-term debt in recent crises. Finance and Development, 37(December), 54–57.

Davies, R., Desbordes, R., & Ray, A. (2015). Greenfield versus merger and acquisition FDI: Same wine, different bottles? UCD Centre for Economic Research Working Paper WP15/03.

Eren, M., & Zhuang, H. (2015). Mergers and acquisitions versus greenfield investment, absorptive capacity, and economic growth: Evidence from 12 new member states of the European Union. Eastern European Economics, 53(2), 99–123.

Felices, G., Hoggarth, G., & Madouros, V. (2008). Capital Inflows into EMEs since the millennium: Risks and the potential impact of a reversa. Bank of England Quarterly Bulletin, 2008, Q1.

Fernández-Arias, E., & Hausmann, R. (2001). Is FDI a safer form of financing? Emerging Markets Review, 2, 34–49.

Gopalan, S., & Rajan, R. S. (2016). Revisiting bilateral foreign direct investment inflows to BRIC economies. Global Policy, 7(4), 510–520.

Hansen, H., & Rand, J. (2006). On the causal links between FDI and growth in developing countries. The World Economy, 29, 21–41.

Hausmann, R., & Fernandez-Arias, E. (2000). “Foreign Direct Investment: Good Cholesterol?” Seminar on The New Wave of Capital Inflows: Sea Change or Just Another Tide? IDB Annual Meetings. IDB, New Orleans, LA. Available from: http://www20.iadb.org/intal/catalogo/PE/2010/07220.pdf. Accessed 5 Nov 2017.

Hattari, R., & Rajan, R. S. (2011). How different are FDI and FPI flows? Journal of Economic Integration, 26, 499–525.

Herzer, D. (2012). How does foreign direct investment really affect developing countries’ growth? Review of International Economics, 20, 396–414.

Iamsiraroj, S. (2016). The foreign direct investment-economic growth nexus. International Review of Economics and Finance, 42, 116–133.

Loungani, P., & Razin, A. (2001). How beneficial is foreign direct investment for developing countries? Finance and Development, 38. http://www.imf.org/external/pubs/ft/fandd/2001/06/loungani.htm (last accessed 15 Feb 2016).

Mankiw, N. G., Romer, D., & Weil, D. (1992). A contribution to the empirics of economic growth. Quarterly Journal of Economics, 107, 407–438.

Mencinger, J. (2003). Does foreign direct investment always enhance economic growth? Kyklos, 56, 491–508.

Mileva, E. (2008). The impact of capital flows on domestic investment in transition economies. ECB Working Paper No. 871, European Central Bank.

Mody, A., & Murshid, A. P. (2005). Growing up with capital flows. Journal of International Economics, 65, 249–266.

Muller, T. (2007). Analyzing modes of foreign entry: Greenfield investment versus acquisition. Review of International Economics, 15, 93–111.

Nagano, M. (2013). Similarities and differences among cross-border M&A and Greenfield FDI determinants: Evidence from Asia and Oceania. Emerging Markets Review, 16, 100–118.

Nickell, S. (1981). Biases in dynamic models with fixed effects. Econometrica, 49, 1417–1426.

Qiu, L. D., & Wang, S. (2011). FDI policy, Greenfield investment, and cross-border mergers. Review of International Economics, 19, 836–851.

Raff, H., Ryan, M., & Stahler, F. (2009). The choice of market entry mode: Greenfield investment, M&A and joint venture. International Review of Economics and Finance, 18, 3–10.

Rajan, R. S., Gopalan, S., & Hattari, H. (2011). Crisis, capital flows and FDI in emerging Asia. Oxford: Oxford University Press.

Razin, A. (2004). The contribution of FDI flows to domestic investment in capacity, and vice versa. In Growth and productivity in East Asia, NBER-East Asia Seminar on Economics (Vol. 13). http://www.nber.org/chapters/c10747.pdf (last accessed 15 Feb 2016).

Sahay, R., Arora, V., Arvanitis, T., Faruqee, H., N’Diaye, P., & Mancini-Griffoli, T. (2014). Emerging market volatility: Lessons from the taper tantrum, IMF Staff Discussion Note SDN/14/09, International Monetary Fund.

Sarno, L., & Taylor, M. (1997). Money, accounting labels and the permanence of capital flows to developing countries: An empirical investigation. Journal of Development Economics, 59, 337–364.

Slangen, A., & Hennart, J.-F. (2007). Greenfield or acquisition entry: A review of the empirical foreign establishment mode literature. Journal of International Management, 13, 403–429.

Stepanok, I. (2015). Cross-border mergers and Greenfield foreign direct investment. Review of International Economics, 23, 111–136.

UNCTAD. (2000). World Investment Report 2000: Cross-border mergers and acquisitions and development. New York: United Nations.

UNCTAD. (2011). World Investment Report 2011: Non-equity modes of international production and investment. New York: United Nations.

Wang, M., & Wong, M. C. S. (2009). What drives economic growth? The case of cross-border M&A and Greenfield FDI activities. Kyklos, 62(2), 316–330.

Acknowledgements

This paper was supported by China National Social Science Fund (Grant No.: 16BJY167).

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Gopalan, S., Ouyang, A. & Rajan, R.S. Impact of Greenfield FDI versus M&A on growth and domestic investment in developing Asia. Econ Polit 35, 41–70 (2018). https://doi.org/10.1007/s40888-017-0085-z

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40888-017-0085-z